forward guidance and the exchange rate · present paper forward guidance in the open economy role...

TRANSCRIPT

Forward Guidance and the Exchange Rate

Jordi Galí

CREI, UPF, Barcelona GSE

May 2017

Jordi Galí (CREI, UPF, Barcelona GSE) Forward Guidance and the Exchange Rate May 2017 1 / 18

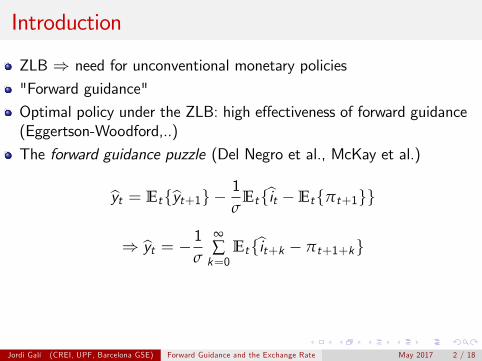

Introduction

ZLB ⇒ need for unconventional monetary policies

"Forward guidance"

Optimal policy under the ZLB: high effectiveness of forward guidance(Eggertson-Woodford,..)

The forward guidance puzzle (Del Negro et al., McKay et al.)

yt = Et{yt+1} −1σ

Et {it −Et{πt+1}}

⇒ yt = −1σ

∞∑k=0

Et {it+k − πt+1+k}

Jordi Galí (CREI, UPF, Barcelona GSE) Forward Guidance and the Exchange Rate May 2017 2 / 18

Present Paper

Forward guidance in the open economy

Role of the exchange rate in the transmission of forward guidance:

(i) theory: partial and general equilibrium(ii) empirical evidence

Jordi Galí (CREI, UPF, Barcelona GSE) Forward Guidance and the Exchange Rate May 2017 3 / 18

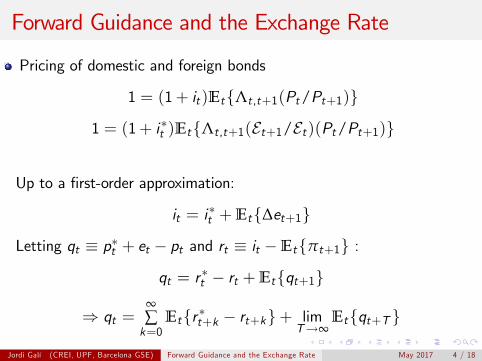

Forward Guidance and the Exchange Rate

Pricing of domestic and foreign bonds

1 = (1+ it)Et{Λt,t+1(Pt/Pt+1)}

1 = (1+ i∗t )Et{Λt,t+1(Et+1/Et)(Pt/Pt+1)}

Up to a first-order approximation:

it = i∗t +Et{∆et+1}

Letting qt ≡ p∗t + et − pt and rt ≡ it −Et{πt+1} :

qt = r∗t − rt +Et{qt+1}

⇒ qt =∞∑k=0

Et{r∗t+k − rt+k}+ limT→∞

Et{qt+T }

Jordi Galí (CREI, UPF, Barcelona GSE) Forward Guidance and the Exchange Rate May 2017 4 / 18

FG and the Exchange Rate: Partial Equilibrium

Assumption: small open economy, constant prices

Experiment: Announcement at time t

it+k = δ

for k = T ,T + 1, ...,T +D − 1

Real exchange rate response at t:

qt = −Dδ

⇒ invariance to implementation horizon (T )

Adjustment over time (fig.)

Jordi Galí (CREI, UPF, Barcelona GSE) Forward Guidance and the Exchange Rate May 2017 5 / 18

-4 -2 0 2 4 6 8 10 12

-1

-0.5

0

0.5

1

interest rate

exchange rate

Forward Guidance and the Exchange Rate: Partial Equilibrium

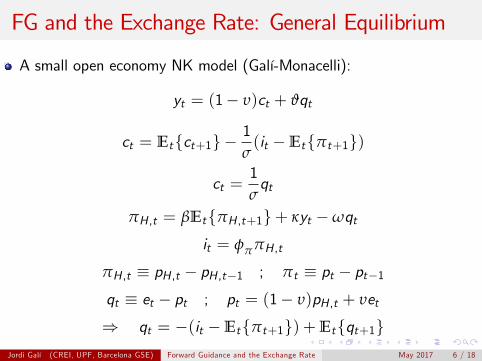

FG and the Exchange Rate: General Equilibrium

A small open economy NK model (Galí-Monacelli):

yt = (1− υ)ct + ϑqt

ct = Et{ct+1} −1σ(it −Et{πt+1})

ct =1σqt

πH ,t = βEt{πH ,t+1}+ κyt −ωqt

it = φππH ,t

πH ,t ≡ pH ,t − pH ,t−1 ; πt ≡ pt − pt−1qt ≡ et − pt ; pt = (1− υ)pH ,t + υet

⇒ qt = −(it −Et{πt+1}) +Et{qt+1}Jordi Galí (CREI, UPF, Barcelona GSE) Forward Guidance and the Exchange Rate May 2017 6 / 18

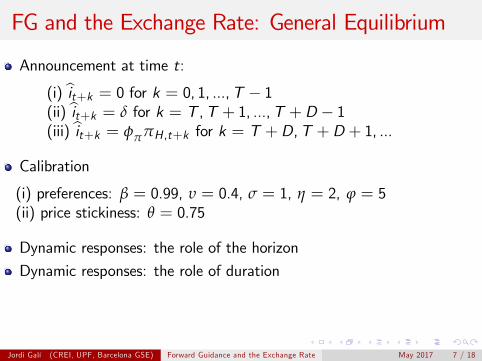

FG and the Exchange Rate: General Equilibrium

Announcement at time t:

(i) it+k = 0 for k = 0, 1, ...,T − 1(ii) it+k = δ for k = T ,T + 1, ...,T +D − 1(iii) it+k = φππH ,t+k for k = T +D,T +D + 1, ...

Calibration

(i) preferences: β = 0.99, υ = 0.4, σ = 1, η = 2, ϕ = 5(ii) price stickiness: θ = 0.75

Dynamic responses: the role of the horizon

Dynamic responses: the role of duration

Jordi Galí (CREI, UPF, Barcelona GSE) Forward Guidance and the Exchange Rate May 2017 7 / 18

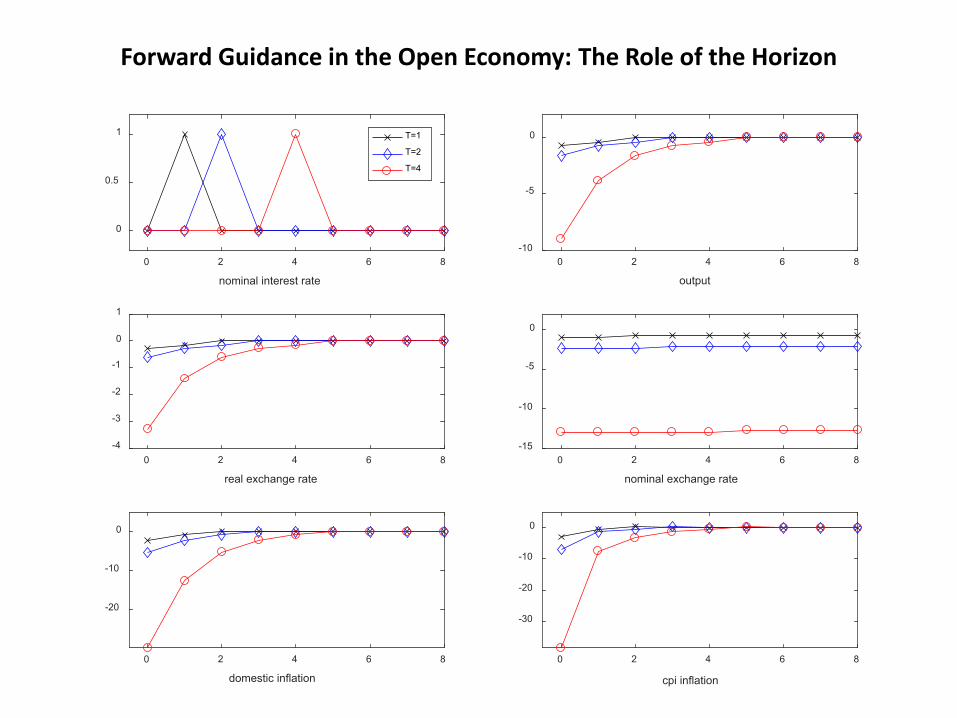

Forward Guidance in the Open Economy: The Role of the Horizon

0 2 4 6 8

real exchange rate

-4

-3

-2

-1

0

1

0 2 4 6 8

domestic inflation

-20

-10

0

0 2 4 6 8

output

-10

-5

0

0 2 4 6 8

nominal exchange rate

-15

-10

-5

0

0 2 4 6 8

cpi inflation

-30

-20

-10

0

0 2 4 6 8

nominal interest rate

0

0.5

1 T=1

T=2

T=4

Forward Guidance in the Open Economy: The Role of Duration

0 1 2 3 4 5 6 7 8

real exchange rate

-2

-1.5

-1

-0.5

0

0 1 2 3 4 5 6 7 8

domestic inflation

-15

-10

-5

0

0 1 2 3 4 5 6 7 8

output

-4

-3

-2

-1

0

0 1 2 3 4 5 6 7 8

nominal exchange rate

-8

-6

-4

-2

0

0 1 2 3 4 5 6 7 8

cpi inflation

-20

-15

-10

-5

0

0 1 2 3 4 5 6 7 8

nominal interest rate

0

0.5

1 D=1

D=2

D=3

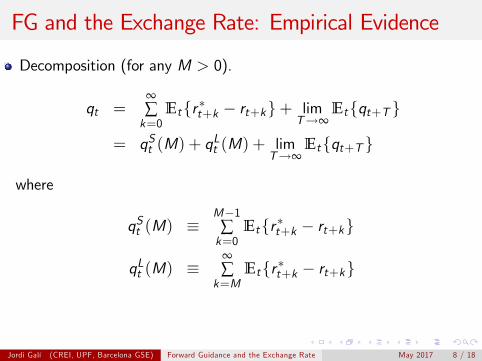

FG and the Exchange Rate: Empirical Evidence

Decomposition (for any M > 0).

qt =∞∑k=0

Et{r∗t+k − rt+k}+ limT→∞

Et{qt+T }

= qSt (M) + qLt (M) + lim

T→∞Et{qt+T }

where

qSt (M) ≡M−1∑k=0

Et{r∗t+k − rt+k}

qLt (M) ≡∞∑k=M

Et{r∗t+k − rt+k}

Jordi Galí (CREI, UPF, Barcelona GSE) Forward Guidance and the Exchange Rate May 2017 8 / 18

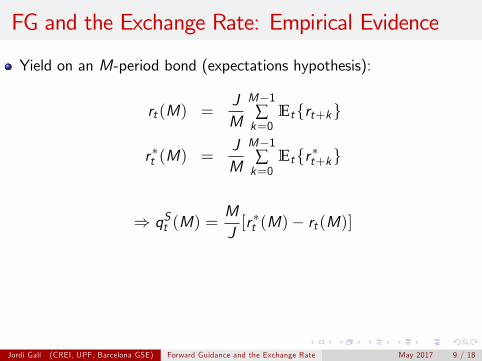

FG and the Exchange Rate: Empirical Evidence

Yield on an M-period bond (expectations hypothesis):

rt(M) =JM

M−1∑k=0

Et{rt+k}

r∗t (M) =JM

M−1∑k=0

Et{r∗t+k}

⇒ qSt (M) =MJ[r∗t (M)− rt(M)]

Jordi Galí (CREI, UPF, Barcelona GSE) Forward Guidance and the Exchange Rate May 2017 9 / 18

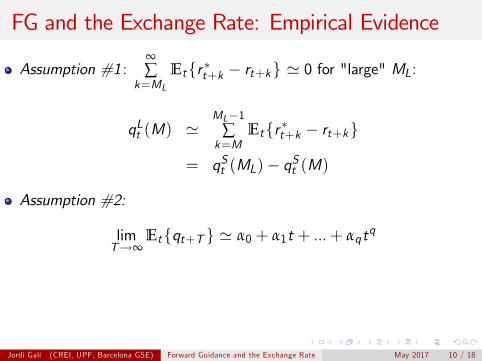

FG and the Exchange Rate: Empirical Evidence

Assumption #1 :∞∑

k=MLEt{r∗t+k − rt+k} ' 0 for "large" ML:

qLt (M) 'ML−1

∑k=M

Et{r∗t+k − rt+k}

= qSt (ML)− qSt (M)

Assumption #2:

limT→∞

Et{qt+T } ' α0 + α1t + ...+ αqtq

Jordi Galí (CREI, UPF, Barcelona GSE) Forward Guidance and the Exchange Rate May 2017 10 / 18

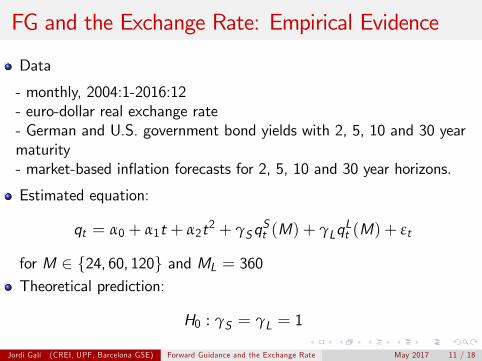

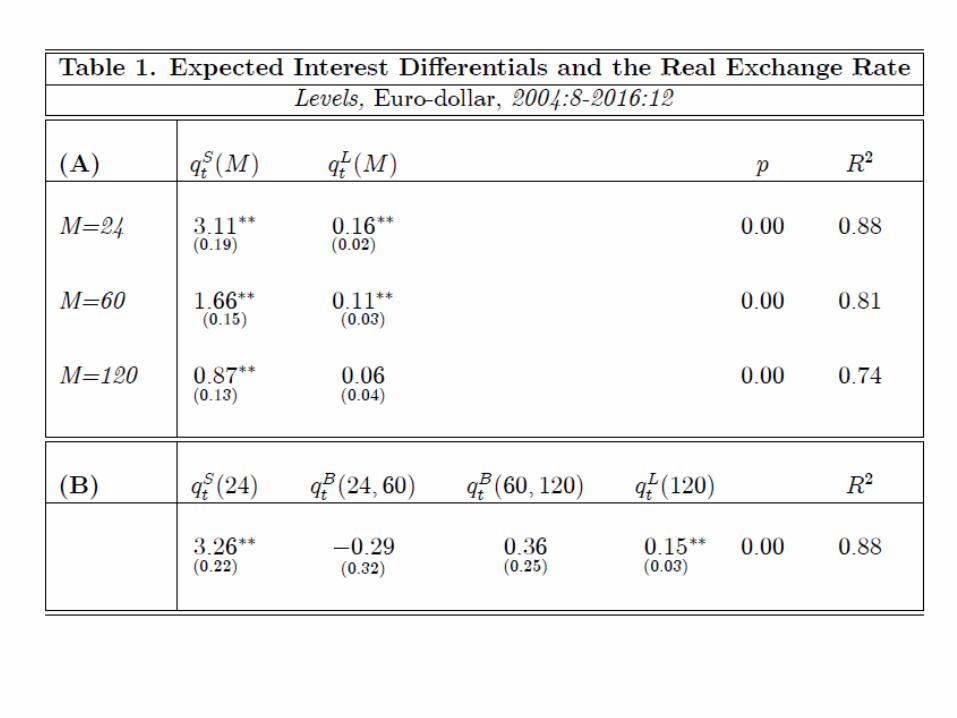

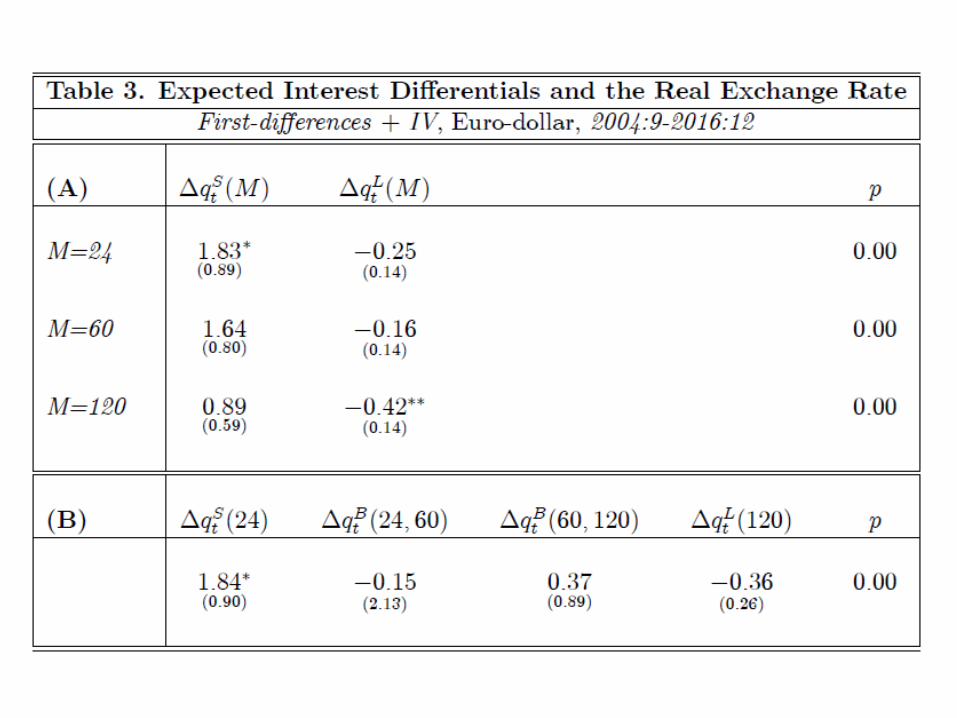

FG and the Exchange Rate: Empirical Evidence

Data

- monthly, 2004:1-2016:12- euro-dollar real exchange rate- German and U.S. government bond yields with 2, 5, 10 and 30 yearmaturity- market-based inflation forecasts for 2, 5, 10 and 30 year horizons.

Estimated equation:

qt = α0 + α1t + α2t2 + γSqSt (M) + γLq

Lt (M) + εt

for M ∈ {24, 60, 120} and ML = 360Theoretical prediction:

H0 : γS = γL = 1

Jordi Galí (CREI, UPF, Barcelona GSE) Forward Guidance and the Exchange Rate May 2017 11 / 18

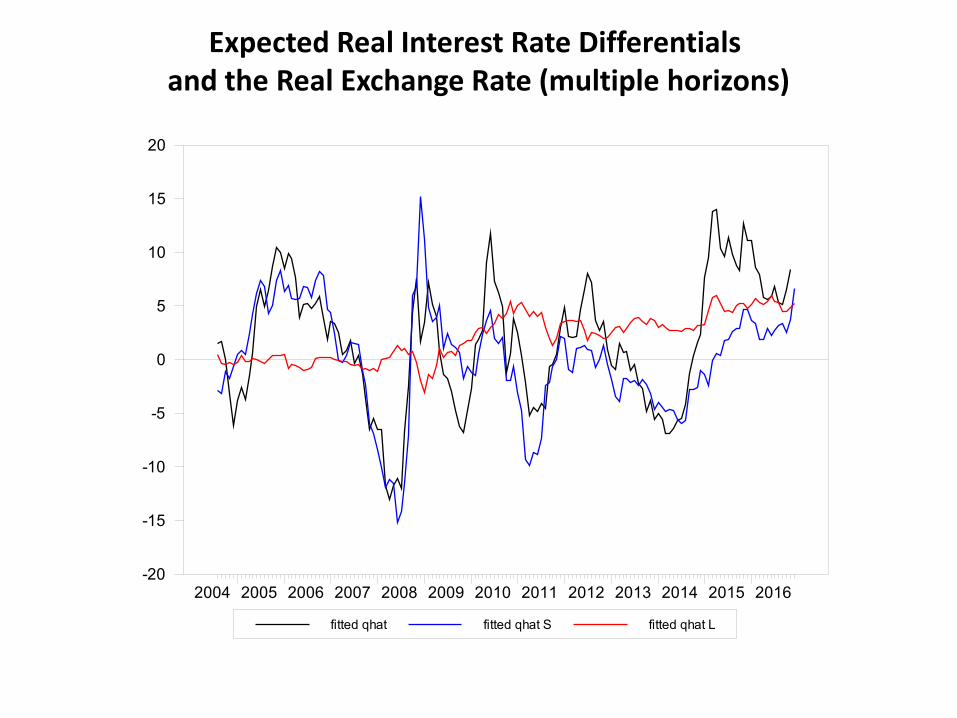

q fitted q

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016-30

-20

-10

0

10

20

30

qhat fitted qhat

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016-15

-10

-5

0

5

10

15

20

qhat fitted qhat S fitted qhat L

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016-15

-10

-5

0

5

10

15

20

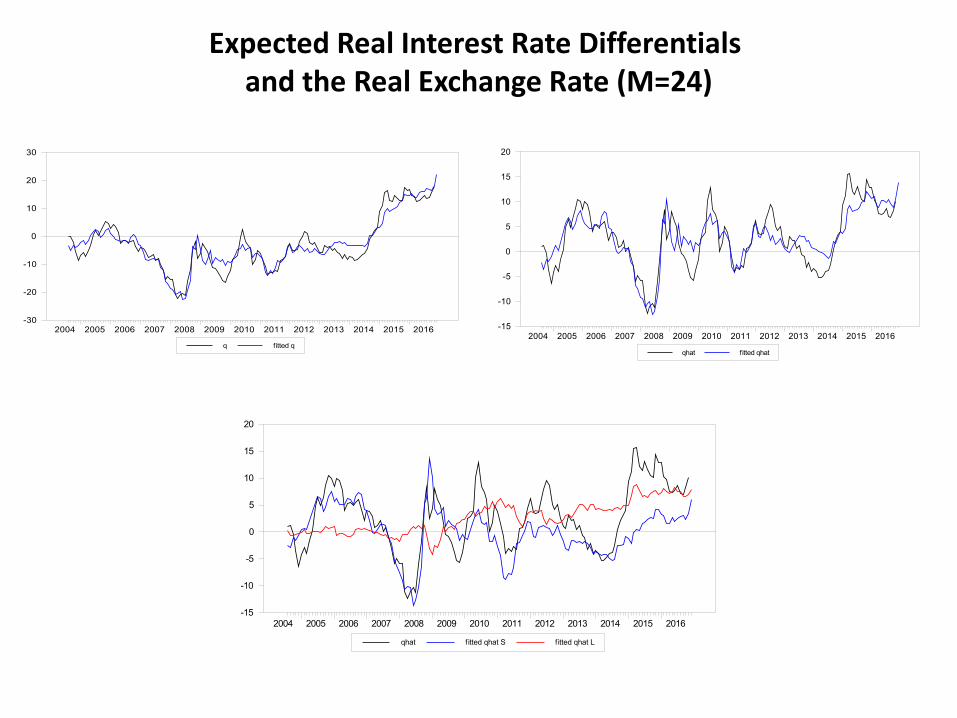

Expected Real Interest Rate Differentials and the Real Exchange Rate (M=24)

FG and the Exchange Rate: Empirical Evidence

Data- monthly, 2004:1-2016:12- euro-dollar real exchange rate- German and U.S. government bond yields with 2, 5, 10 and 30 yearmaturity- market-based inflation forecasts for 2, 5, 10 and 30 year horizons.Estimated equation:

qt = α0 + α1t + α2t2 + γSqSt (M) + γLq

Lt (M) + εt

for M ∈ {24, 60, 120} and ML = 360Theoretical prediction:

H0 : γS = γL = 1

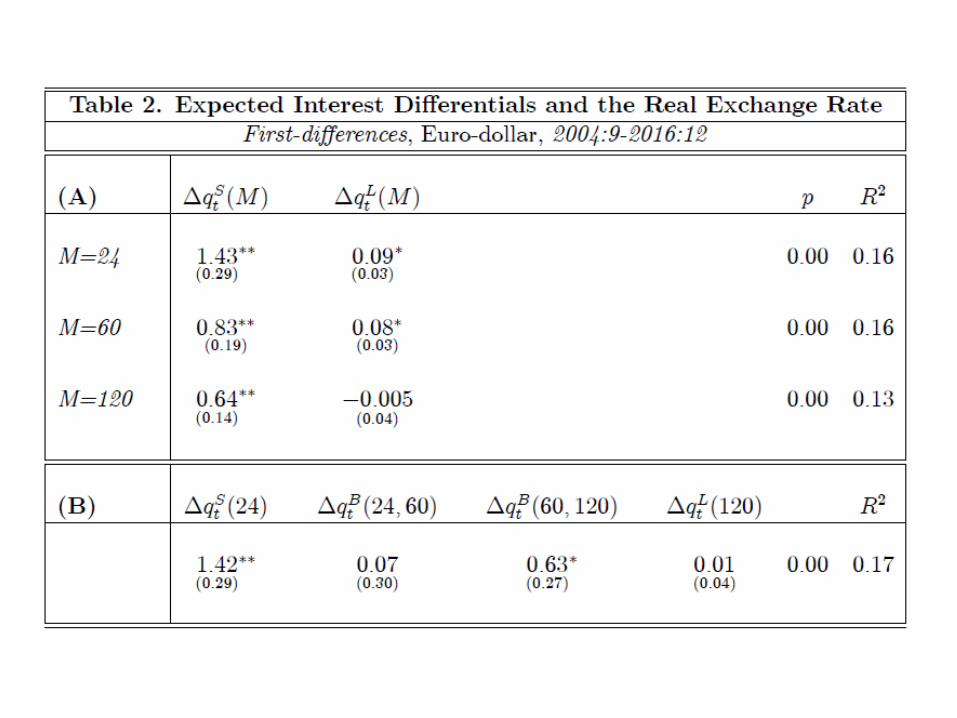

Robustness: First-difference specification

∆qt = α+ γS∆qSt (M) + γL∆qLt (M) + ξtJordi Galí (CREI, UPF, Barcelona GSE) Forward Guidance and the Exchange Rate May 2017 12 / 18

Possible Explanations?

Proposed solutions for the closed economy FG puzzle

1 Finite lives (Del Negro et al.)2 Idiosyncratic labor income risk + borrowing constraints (McKay etal.)

3 Lack of common knowledge (Angeletos-Lian)4 "Behavioral discounting" (Gabaix)

⇒ yt = αEt{yt+1} −1σ(it −Et{πt+1})

(1) and (2) do not apply to exchange rate equation

(3) and (4) cannot account for overreaction to near-termexpectations

Jordi Galí (CREI, UPF, Barcelona GSE) Forward Guidance and the Exchange Rate May 2017 13 / 18

Possible Explanations?

Time-varying foreign exchange risk premium?

zt ≡ r∗t − rt +Et{∆qt+1}

qt =∞∑k=0

Et{r∗t+k − rt+k}+ ut

= qSt (M) + qLt (M) + ut

where ut ≡ −∞∑k=0

Et{zt+k}.

Independent evidence: cov(r∗t − rt , ut) > 0 (Engel 2016) ⇒ upwardbias of OLS estimates of γ in:

qt = γqSt (ML) + ut

qt − qSt (M) = γqLt (M) + utBut γ� 1 in the data!

Jordi Galí (CREI, UPF, Barcelona GSE) Forward Guidance and the Exchange Rate May 2017 18 / 18

Concluding comments

Effectiveness of forward guidance policies in open economies;exchange rate role.

Partial equilibrium: invariance to implementation horizon

General equilibrium: stronger effects the more distant theimplementation horizon

Empirical evidence: expectations of interest rate differentials in thenear (distant) future have much larger (smaller) effects thanpredicted by the theory

⇒ a forward guidance exchange rate puzzle?

Jordi Galí (CREI, UPF, Barcelona GSE) Forward Guidance and the Exchange Rate May 2017 14 / 18

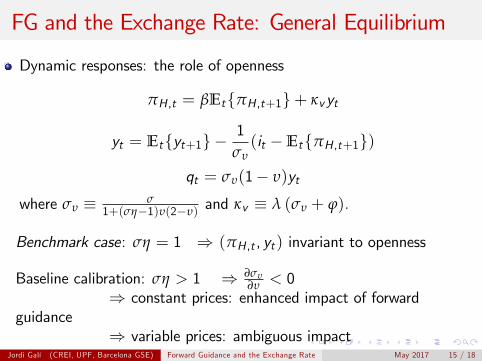

FG and the Exchange Rate: General Equilibrium

Dynamic responses: the role of openness

πH ,t = βEt{πH ,t+1}+ κvyt

yt = Et{yt+1} −1

συ(it −Et{πH ,t+1})

qt = συ(1− υ)yt

where συ ≡ σ1+(ση−1)υ(2−υ)

and κv ≡ λ (συ + ϕ).

Benchmark case: ση = 1 ⇒ (πH ,t , yt) invariant to openness

Baseline calibration: ση > 1 ⇒ ∂συ∂υ < 0

⇒ constant prices: enhanced impact of forwardguidance

⇒ variable prices: ambiguous impactJordi Galí (CREI, UPF, Barcelona GSE) Forward Guidance and the Exchange Rate May 2017 15 / 18

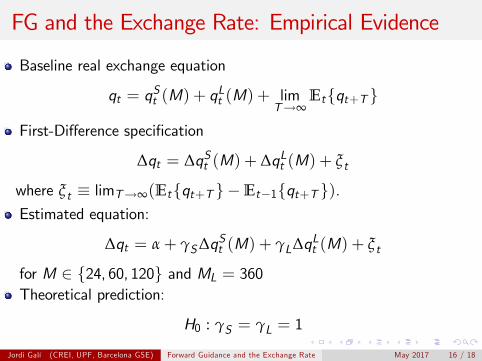

FG and the Exchange Rate: Empirical Evidence

Baseline real exchange equation

qt = qSt (M) + qLt (M) + lim

T→∞Et{qt+T }

First-Difference specification

∆qt = ∆qSt (M) + ∆qLt (M) + ξt

where ξt ≡ limT→∞(Et{qt+T } −Et−1{qt+T }).Estimated equation:

∆qt = α+ γS∆qSt (M) + γL∆qLt (M) + ξt

for M ∈ {24, 60, 120} and ML = 360Theoretical prediction:

H0 : γS = γL = 1

Jordi Galí (CREI, UPF, Barcelona GSE) Forward Guidance and the Exchange Rate May 2017 16 / 18

FG and the Exchange Rate: Empirical Evidence

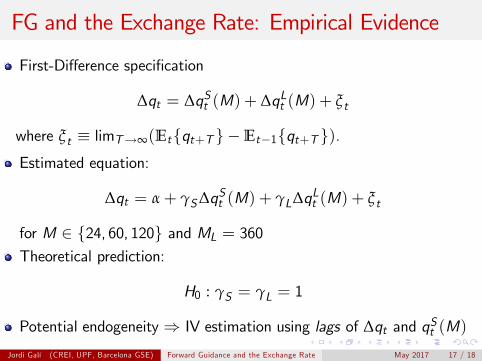

First-Difference specification

∆qt = ∆qSt (M) + ∆qLt (M) + ξt

where ξt ≡ limT→∞(Et{qt+T } −Et−1{qt+T }).Estimated equation:

∆qt = α+ γS∆qSt (M) + γL∆qLt (M) + ξt

for M ∈ {24, 60, 120} and ML = 360Theoretical prediction:

H0 : γS = γL = 1

Potential endogeneity⇒ IV estimation using lags of ∆qt and qSt (M)

Jordi Galí (CREI, UPF, Barcelona GSE) Forward Guidance and the Exchange Rate May 2017 17 / 18

0 2 4 6 8

real exchange rate

-2

-1.5

-1

-0.5

0

0.5

0 2 4 6 8

domestic inflation

-20

-15

-10

-5

0

5

0 2 4 6 8

output

-6

-4

-2

0

0 2 4 6 8

nominal exchange rate

-10

-8

-6

-4

0 2 4 6 8

cpi inflation

-30

-20

-10

0

0 2 4 6 8

nominal interest rate

0

0.5

1 =0.2

=0.4

=0.6

Forward Guidance in the Open Economy: The Role of Openness

fitted qhat fitted qhat S fitted qhat L

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016-20

-15

-10

-5

0

5

10

15

20

Expected Real Interest Rate Differentials and the Real Exchange Rate (multiple horizons)