fragmentation in financial markets: the rise of dark … · fragmentation in financial markets: the...

TRANSCRIPT

Fragmentation in

Financial Markets:

The Rise of Dark Liquidity

Sabrina Buti

Global Risk Institute – April 7th 2016

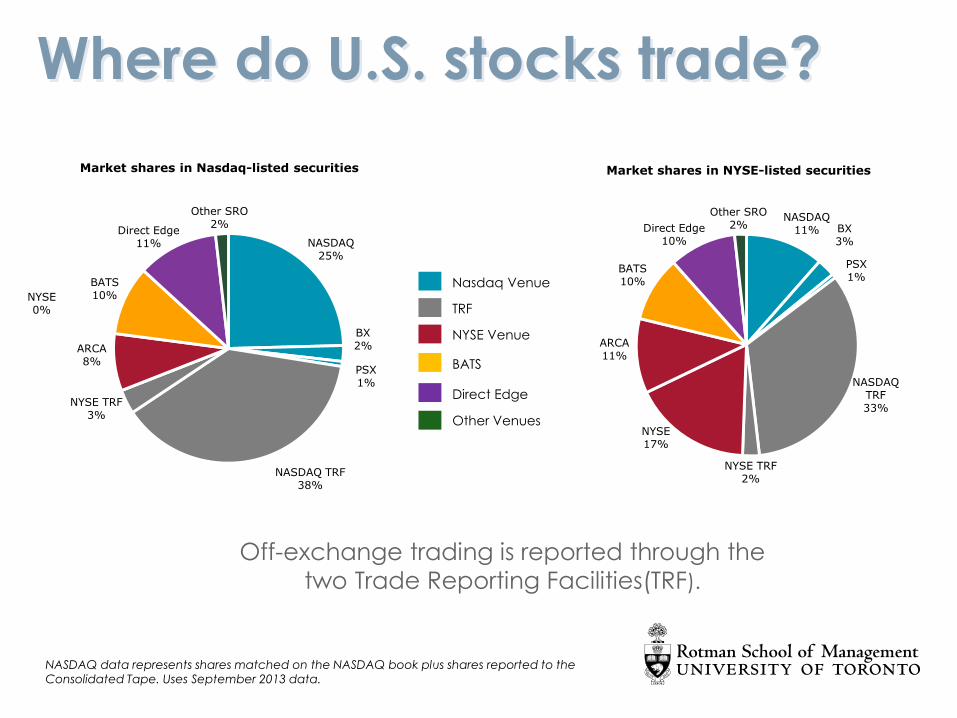

Where do U.S. stocks trade?

NASDAQ 25%

BX 2%

PSX 1%

NASDAQ TRF 38%

NYSE TRF 3%

NYSE 0%

ARCA 8%

BATS 10%

Direct Edge 11%

Other SRO 2%

Market shares in Nasdaq-listed securities

Nasdaq Venue

TRF

NYSE Venue

BATS

Direct Edge

Other Venues

NASDAQ 11% BX

3%

PSX 1%

NASDAQ TRF 33%

NYSE TRF 2%

NYSE 17%

ARCA 11%

BATS 10%

Direct Edge 10%

Other SRO 2%

Market shares in NYSE-listed securities

NASDAQ data represents shares matched on the NASDAQ book plus shares reported to the

Consolidated Tape. Uses September 2013 data.

Off-exchange trading is reported through the

two Trade Reporting Facilities(TRF).

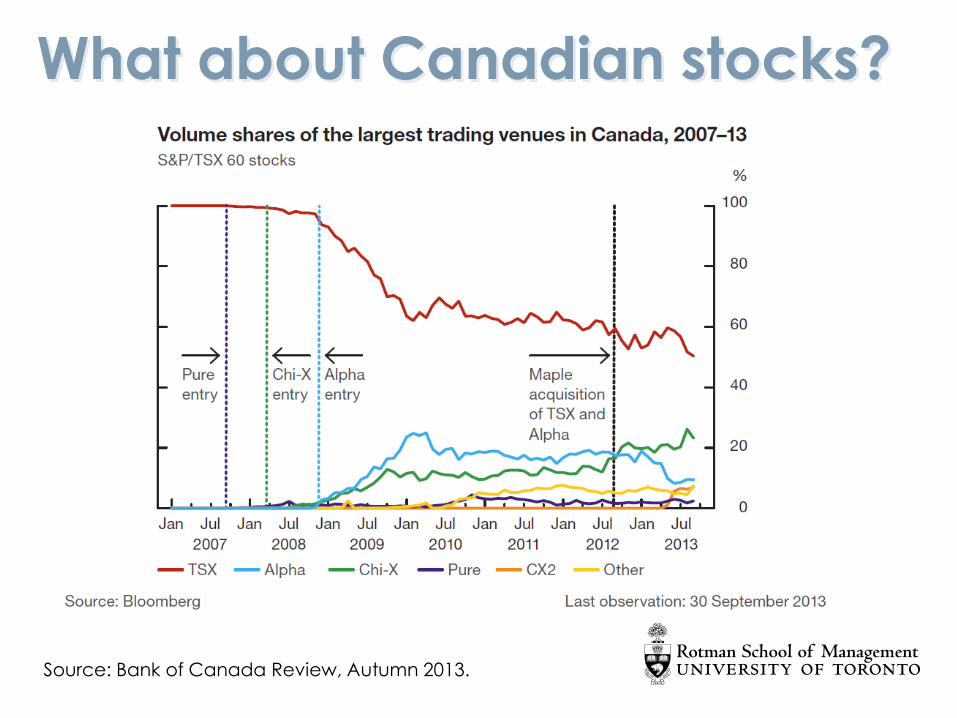

What about Canadian stocks?

Source: Bank of Canada Review, Autumn 2013.

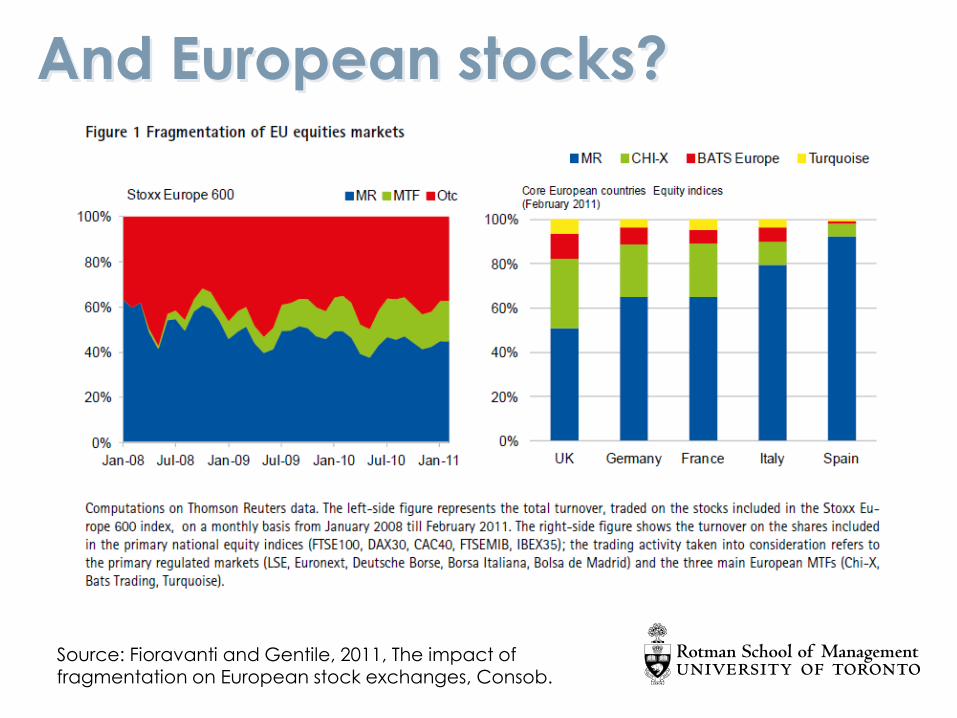

And European stocks?

Source: Fioravanti and Gentile, 2011, The impact of fragmentation on European stock exchanges, Consob.

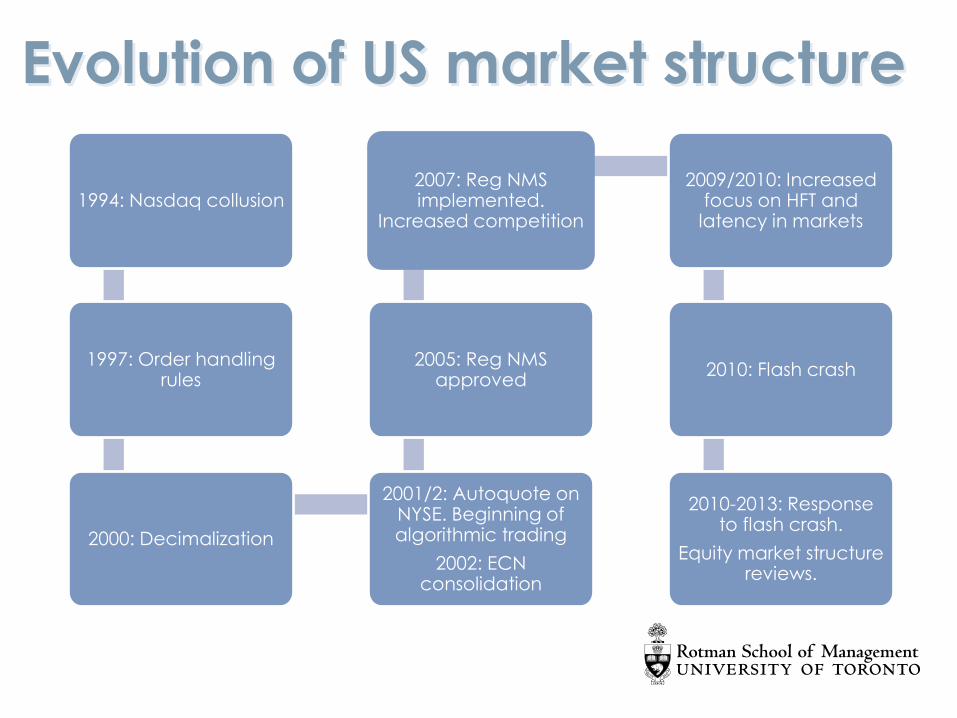

Evolution of US market structure

1994: Nasdaq collusion

1997: Order handling rules

2000: Decimalization

2001/2: Autoquote on NYSE. Beginning of algorithmic trading

2002: ECN consolidation

2005: Reg NMS approved

2007: Reg NMS implemented.

Increased competition

2009/2010: Increased focus on HFT and

latency in markets

2010: Flash crash

2010-2013: Response to flash crash.

Equity market structure reviews.

State of the market

Source: Barclays research.

A new world: Trading complexity

Lit Venues

Dark Venues

10

29

50

16

13

16

2002 2009 2012

Source: Nasdaq

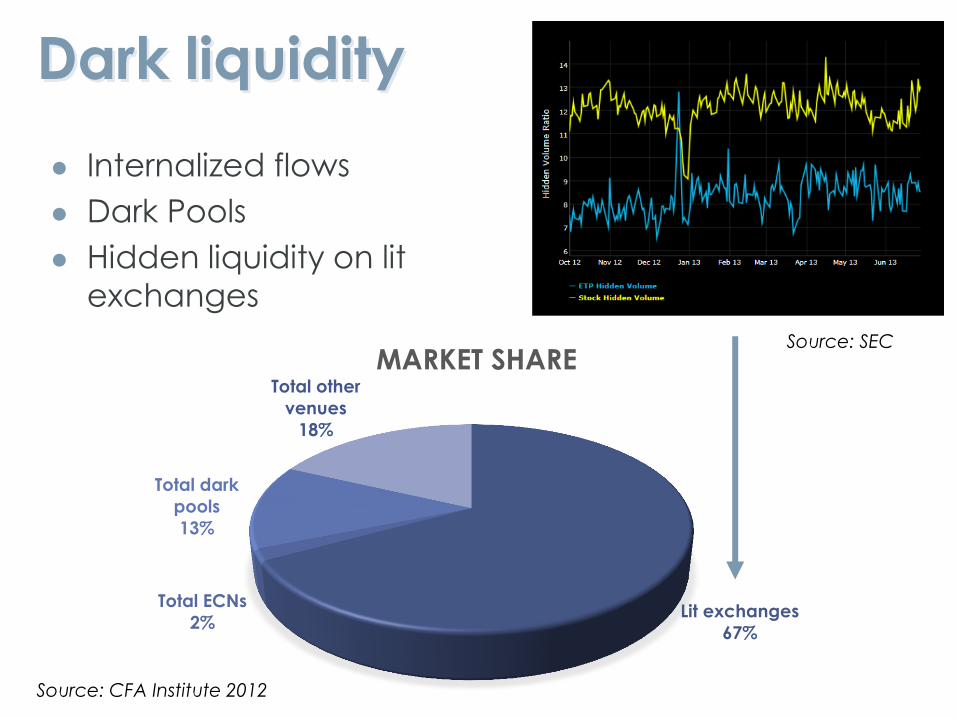

Dark liquidity

Internalized flows

Dark Pools

Hidden liquidity on lit

exchanges

Lit exchanges

67%

Total ECNs

2%

Total dark

pools

13%

Total other

venues

18%

MARKET SHARE

Source: CFA Institute 2012

Source: SEC

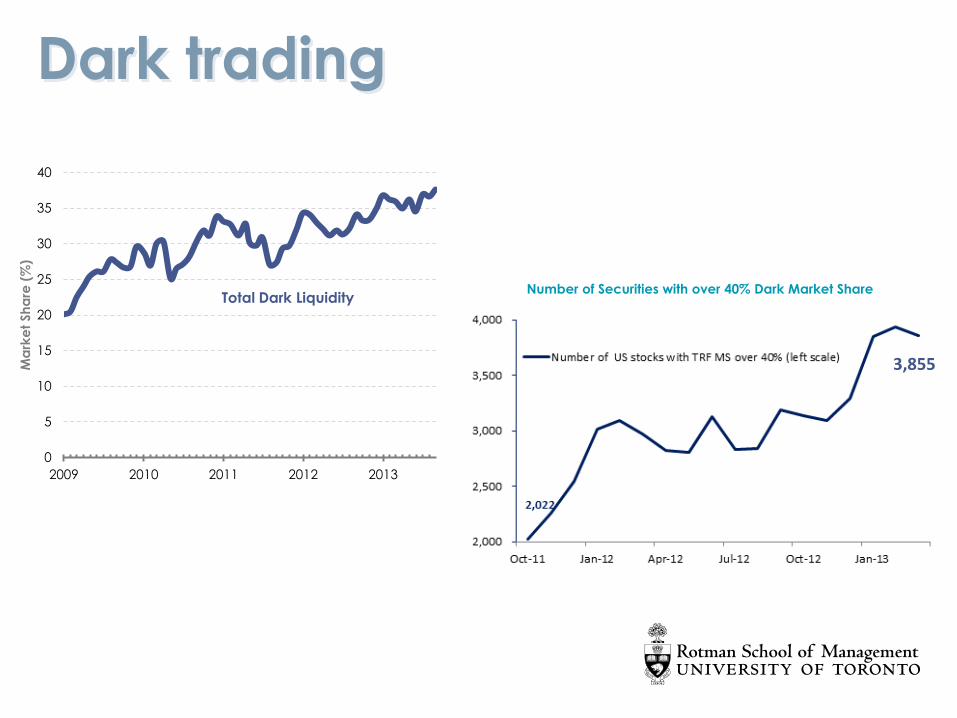

Dark trading

0

5

10

15

20

25

30

35

40

2009 2010 2011 2012 2013

Ma

rke

t Sh

are

(%

)

Total Dark Liquidity Number of Securities with over 40% Dark Market Share

3,855

What are dark pools?

Alternative Trading Systems that do

not provide their best-priced orders

for inclusion in the consolidated

quotation data

Provide anonymity and opacity pre-

trade to institutions

Derivative pricing, mid-quote, inside,

at-quotes (controversial)

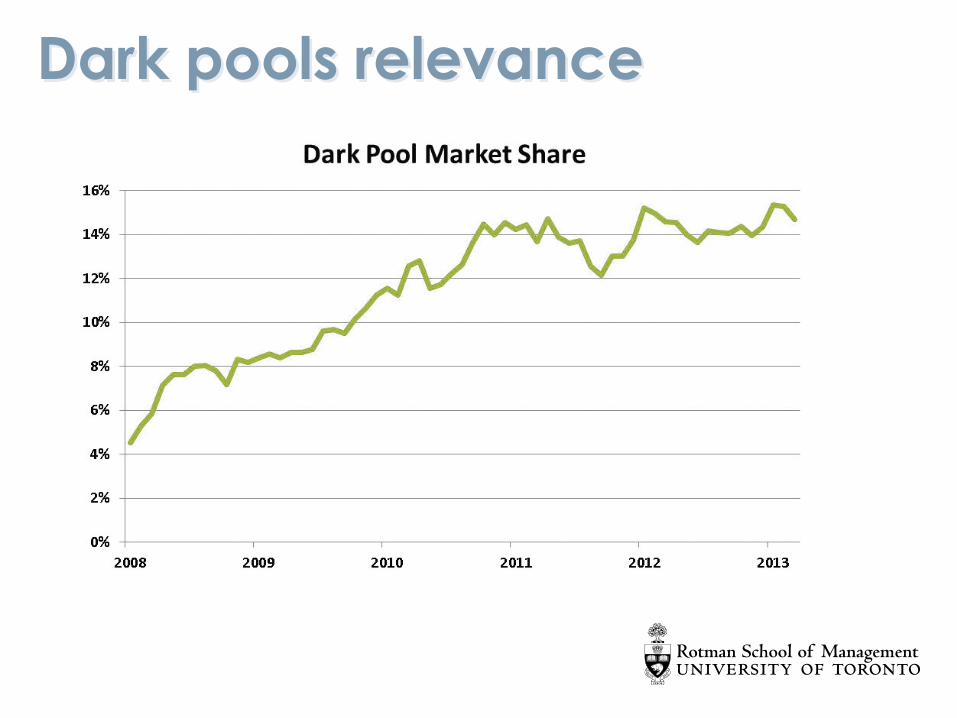

Dark pools relevance

Dark pools classification (I)

Dark Pools classification based on:

market model [periodic vs continuous crossing, blind vs

advertisement based, ...]

ownership [traditional exchange vs single or a group of broker-

dealers]

access [buy or sell side, both retail vs institutional, ...]

Dark pools classification (II)

Independent/Agency pools

Bank/Brokers pools

Market Maker pools

Consortium-Sponsored pools

Exchange-Based dark pools

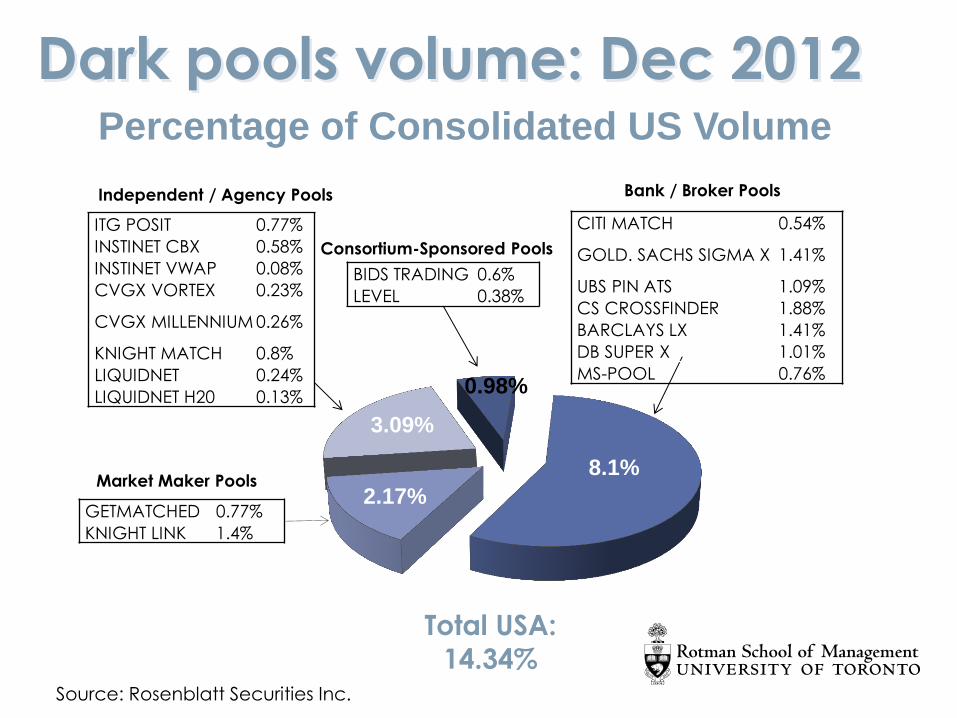

Dark pools volume: Dec 2012 Percentage of Consolidated US Volume

Source: Rosenblatt Securities Inc.

Independent / Agency Pools

0.98%

3.09%

2.17%

8.1%

ITG POSIT 0.77%

INSTINET CBX 0.58%

INSTINET VWAP 0.08%

CVGX VORTEX 0.23%

CVGX MILLENNIUM 0.26%

KNIGHT MATCH 0.8%

LIQUIDNET 0.24%

LIQUIDNET H20 0.13%

CITI MATCH 0.54%

GOLD. SACHS SIGMA X 1.41%

UBS PIN ATS 1.09%

CS CROSSFINDER 1.88%

BARCLAYS LX 1.41%

DB SUPER X 1.01%

MS-POOL 0.76%

Bank / Broker Pools

BIDS TRADING 0.6%

LEVEL 0.38%

Consortium-Sponsored Pools

Market Maker Pools

GETMATCHED 0.77%

KNIGHT LINK 1.4%

Total USA:

14.34%

A few questions about dark pools

Who wants to hide in the dark?

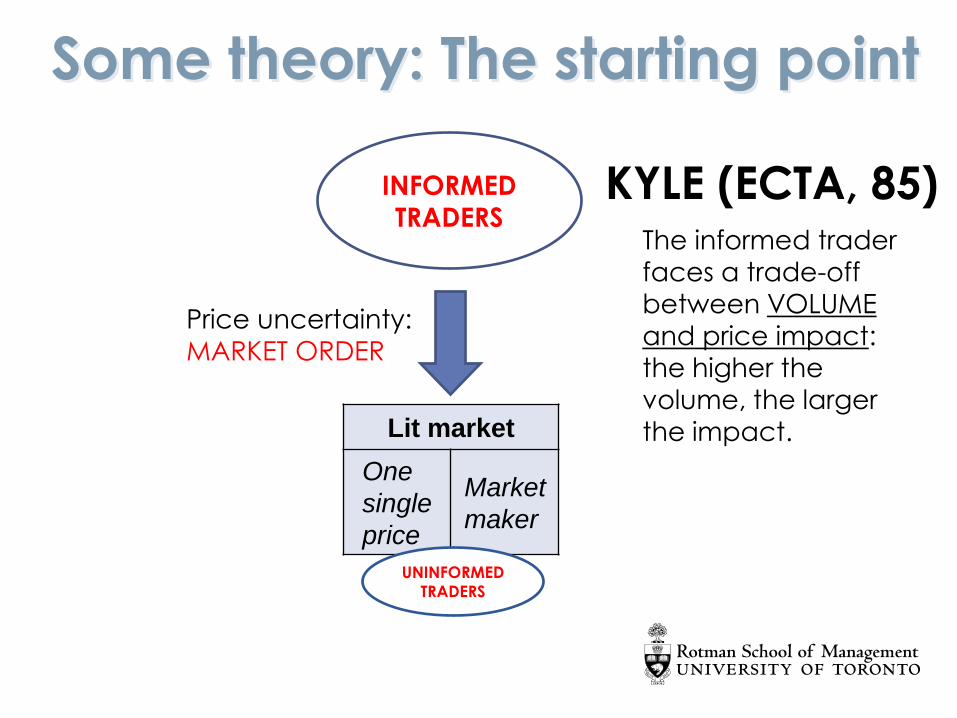

Some theory: The starting point

Price uncertainty:

MARKET ORDER

KYLE (ECTA, 85) The informed trader

faces a trade-off

between VOLUME

and price impact:

the higher the

volume, the larger

the impact.

INFORMED TRADERS

Lit market

One

single

price

Market

maker

UNINFORMED

TRADERS

INFORMED TRADERS

Derivative Price

Dark Pool (DP):

Crossing Network

UNINFORMED

TRADERS

The informed trader still

faces a trade-off

between VOLUME and price impact.

Incentives to move to

the DP, where there is

NO PRICE IMPACT.

BUT the more you

trade on the DP, the

lower is the probability of execution.

Go dark as long as it is

profitable to do so!

Execution uncertainty:

UNKNOWN IMBALANCE

Ye (WP, 2011): Informed go dark

Lit market

One

single

price

Market

maker

UNINFORMED

TRADERS

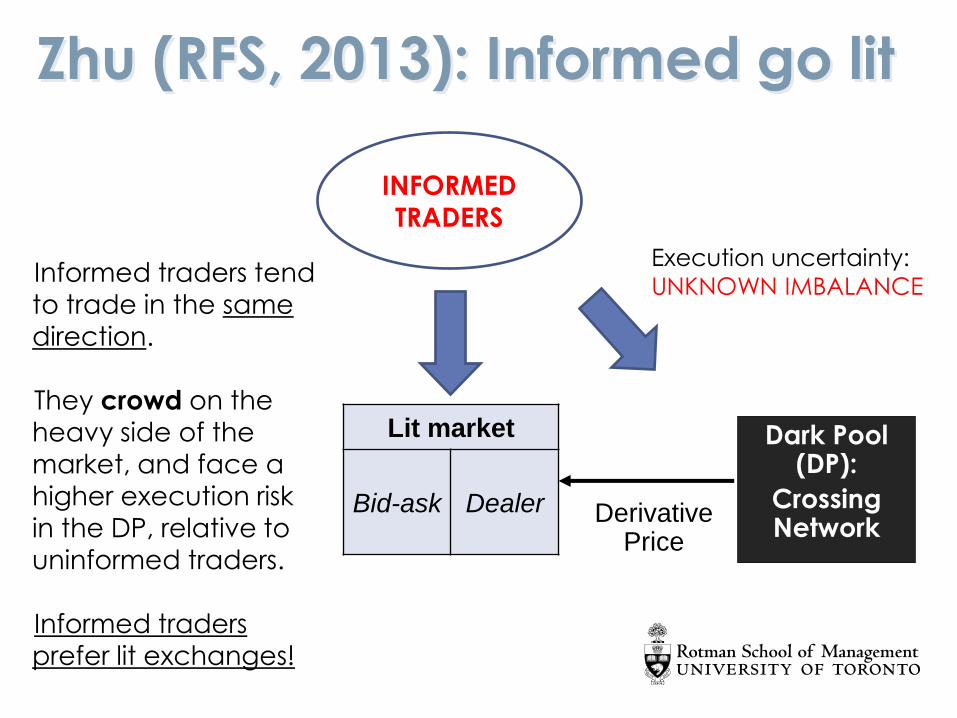

Zhu (RFS, 2013): Informed go lit

INFORMED TRADERS

Lit market

Bid-ask Dealer Derivative Price

Informed traders tend

to trade in the same

direction.

They crowd on the

heavy side of the

market, and face a

higher execution risk

in the DP, relative to

uninformed traders.

Informed traders prefer lit exchanges!

Execution uncertainty:

UNKNOWN IMBALANCE

Dark Pool (DP):

Crossing Network

To summarize…

Ye (WP, 2011):

DPs attract informed traders, harm price discovery

and decrease adverse selection on the lit market

DPs have incentives to get rid of informed traders

Zhu (RFS, 2013):

Exchanges are more attractive to informed traders,

and DPs are more attractive to uninformed traders

Adding a DP could concentrate price-relevant info

on the exchange and improve price discovery, but

reduce exchange liquidity (spread)

Now to the data!

Buti, Rindi and Werner (WP, 2011):

DP activity in the U.S. results in improved price

efficiency based on short-term volatility measures

Comerton-Forde and Putnins (JFE, 2015):

in Australia, orders executed in the dark are less

informed that orders executed in the lit

dark trades increase adverse selection on the

main market, worsening market quality

low levels of dark trading are benign or even

beneficial for informational efficiency, but high

levels are harmful

Who wants to hide in the dark?

Price improvement in dark pools?

Should we be afraid of the dark?

A few questions about dark pools

Better prices in dark pools?

Source: Nasdaq analysis

SEC Reg NMS Rule 612

Introduced on August 29, 2005

Established minimum price variation for lit markets:

$0.01 for stocks priced higher than $1

$0.0001 for stocks priced at $1 and below

Dark markets are exempt from Rule 612 provided:

execute less than 5% of the volume

do not display their orders

So Rule 612 allows for:

broker-dealer internalization

dark trading in sub-penny

Queue jumping…

𝐴2

𝐴1

𝐵1

𝐵2

𝑣

𝑎5

𝑎2

𝑎3

𝑎4

𝑏1

𝑎1

𝑏3

𝑏2

𝑏5

𝑏4

Exchange Dark pool or

Internalization

Market order

Sub-penny trade

How does sub-penny trading work?

In theory…

Rule 612 states that no market participant can

accept, rank, or display orders priced in sub-pennies.

In practice…

On Jan. 2015 the SEC fined a dark pool operator

$14.4 million for accepting and ranking hundreds of

millions of orders priced in increments smaller than

one cent that were submitted to his dark pool.

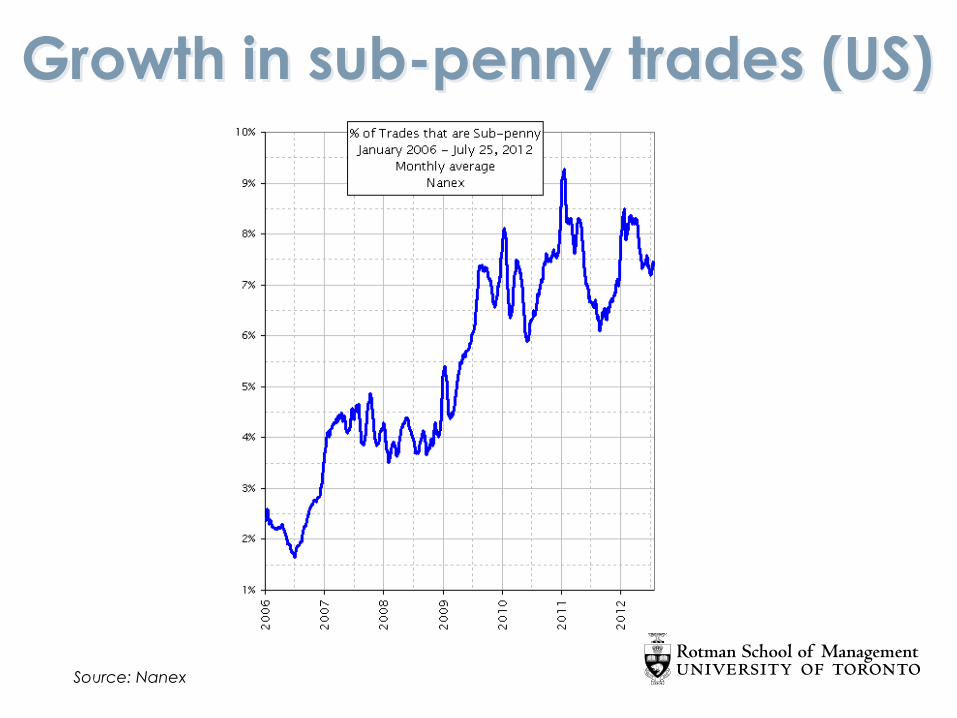

Growth in sub-penny trades (US)

Source: Nanex

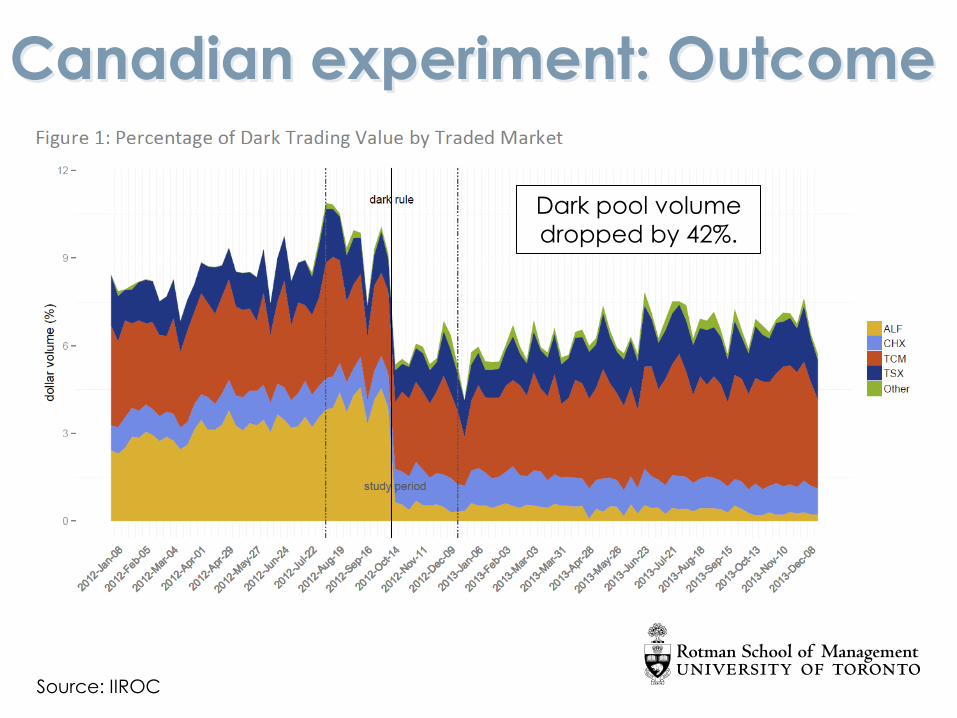

Canadian experiment

Source: IIROC

On October 15, 2012, Canadian regulators made

providing liquidity in the dark more expensive

The new rule specifies the improvement that dark

liquidity providing orders must offer relative to the

best lit bid and offer:

At least 1 cent (1/2 if the lit spread is 1 cent)

Applies to marketable orders below 5,000 shares or $100,000 in value

Does not affect midpoint orders and block trading

Dark markets moved from fractional pricing (90/10

and 80/20) to midpoint

Canadian experiment: Outcome

Source: IIROC

Dark pool volume

dropped by 42%.

What is going on?

Dark trading activity is significantly reduced:

Volume on Alpha IntraSpread, on which dark

trading interacts with a segregated flow of retail

orders, is most strongly impacted when these

market-making opportunities are reduced

Volume on TCM, in which dark participants trade

mainly to minimize information leakage and

market impact, is less impacted

Consistently, active retail traders and passive High

Frequency Traders show the greatest reduction in

dark trading

Successful experiment?

Reduction in dark volume without meaningful

price improvement

Minimal market-wide impact as most

measures of market quality showed no

deterioration

However… Talis and Putnins (JFE, forthcoming)

analyze the same experiment and find that

midpoint crossing systems do not benefit

market quality, but dark limit order markets are

beneficial to market quality

Why separate?

There are two main reasons why trades execute

on alternative trading systems at fractions of

penny:

Undercutting orders posted at the top of public limit

order books (queue-jumping& mid-crossing)

The execution system of some dark pools and broker-

dealers internalization systems follows a derivative pricing rule: trades execute at the midpoint of the

primary market inside spread (mid-crossing)

Mid-crossing therefore does not necessarily

include only undercutting and could potentially

mix different trading strategies

Back to the U.S.

October 1st – November 30th, 2010 (42

trading days)

Stratified sample of 90 Nasdaq and 90 NYSE

listed common stocks, sorted into terciles by

market capitalization and price as of the end

of 2009

Sub-penny trading is further divided into:

Mid-crossing

Queue-jumping

Example in TAQ data: IBM

ID Symbol Date Time Exchange

Price Size Rounded Price Price Improvement

Type of Sub-Penny

1 IBM 20101001 10:00:00 K 135,76 100 135,76 0 None

2 IBM 20101001 10:00:00 K 135,77 100 135,77 0 None

3 IBM 20101001 10:00:00 K 135,84 100 135,84 0 None

… IBM 20101001 10:00:00 … … … … … …

17 IBM 20101001 10:00:00 T 135,84 200 135,84 0 None

18 IBM 20101001 10:00:01 D 135,64 196 135,64 0 None

19 IBM 20101001 10:00:01 D 135,7375 200 135,74 0,0025 Queue-Jumping

20 IBM 20101001 10:00:01 N 135,67 100 135,67 0 None

… IBM 20101001 10:00:01 … … … … … …

28 IBM 20101001 10:00:03 B 135,76 100 135,76 0 None

29 IBM 20101001 10:00:03 D 135,76 100 135,76 0 None

30 IBM 20101001 10:00:03 D 135,825 300 135,83 0,005 Mid-Crossing

Queue-jumping:

price improvement ≠ 0.005

Mid-crossing:

price improvement = 0.005

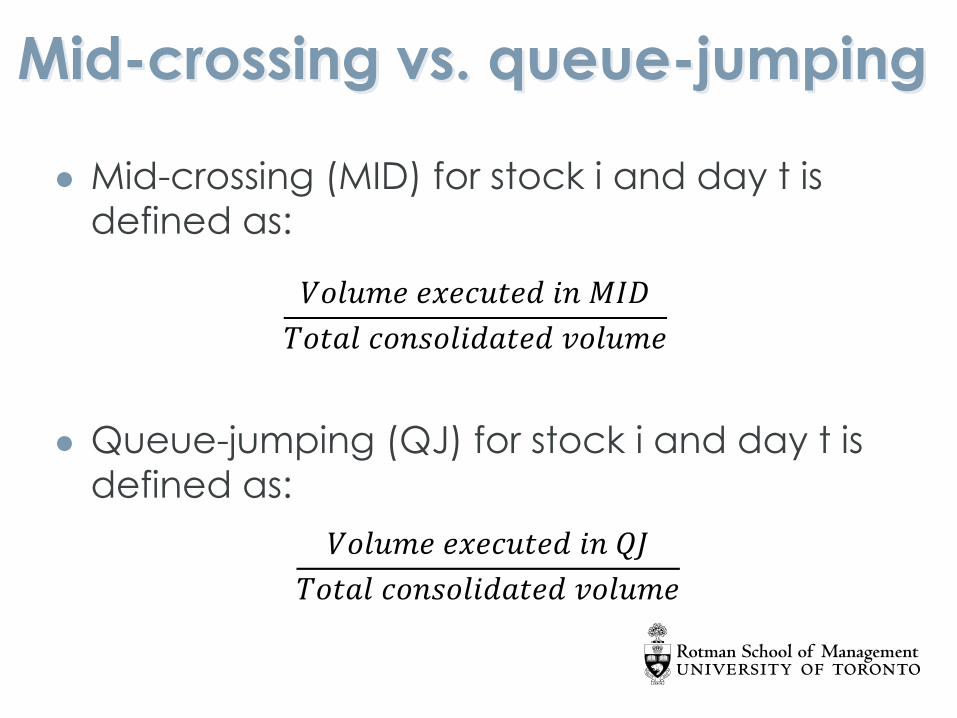

Mid-crossing vs. queue-jumping

Mid-crossing (MID) for stock i and day t is

defined as:

Queue-jumping (QJ) for stock i and day t is

defined as:

𝑉𝑜𝑙𝑢𝑚𝑒 𝑒𝑥𝑒𝑐𝑢𝑡𝑒𝑑 𝑖𝑛 𝑀𝐼𝐷

𝑇𝑜𝑡𝑎𝑙 𝑐𝑜𝑛𝑠𝑜𝑙𝑖𝑑𝑎𝑡𝑒𝑑 𝑣𝑜𝑙𝑢𝑚𝑒

𝑉𝑜𝑙𝑢𝑚𝑒 𝑒𝑥𝑒𝑐𝑢𝑡𝑒𝑑 𝑖𝑛 𝑄𝐽

𝑇𝑜𝑡𝑎𝑙 𝑐𝑜𝑛𝑠𝑜𝑙𝑖𝑑𝑎𝑡𝑒𝑑 𝑣𝑜𝑙𝑢𝑚𝑒

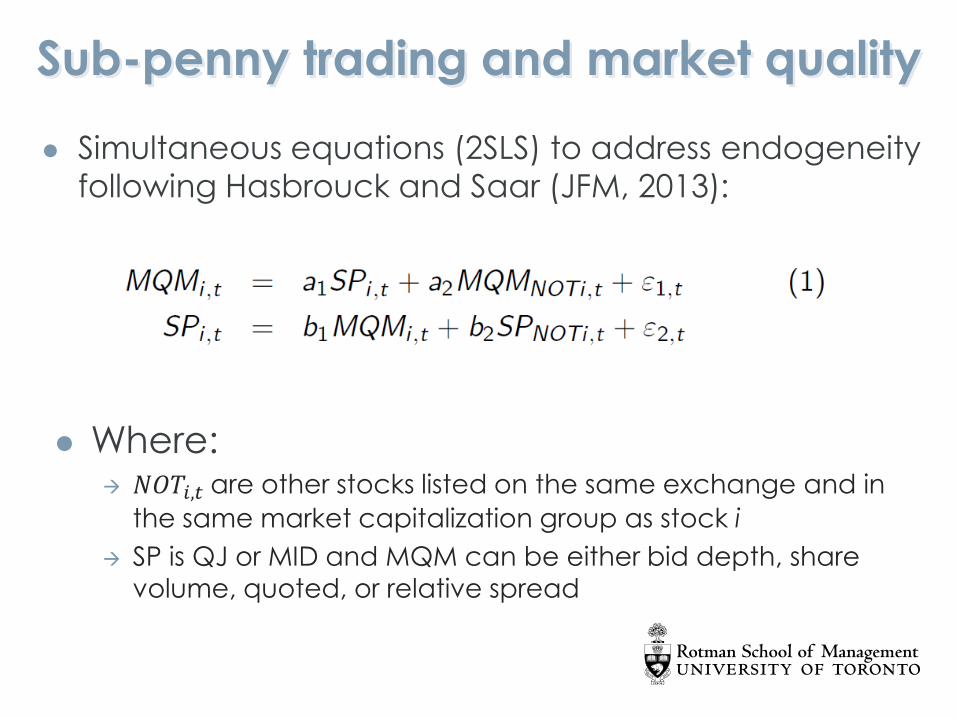

Sub-penny trading and market quality

Simultaneous equations (2SLS) to address endogeneity

following Hasbrouck and Saar (JFM, 2013):

Where: 𝑁𝑂𝑇𝑖,𝑡 are other stocks listed on the same exchange and in

the same market capitalization group as stock i

SP is QJ or MID and MQM can be either bid depth, share

volume, quoted, or relative spread

Empirical analysis

Full sample Small Large

𝑎1 0.342*** 0.044 0.281*

(3.358) (0.240) (2.338)

𝑎2 0.523*** 0.371*** 0.645***

(10.266) (4.294) (8.665)

Observations 7,560 2,520 2,520

Bid depth and QJ

Full sample Small Large

𝑎1 -0.493*** -0.551 -0.288*

(-3.749) (-1.837) (-2.339)

𝑎2 0.631*** 0.582*** 0.684***

(11.720) (5.614) (9.592)

Observations 7,560 2,520 2,520

Relative spread and QJ

Full sample Small Large

𝑎1 0.202 -0.041 0.253

(0.940) (-0.198) (0.790)

𝑎2 0.602*** 0.368*** 0.719***

(13.768) (4.279) (9.500)

Observations 7,560 2,520 2,520

Bid depth and MID

Full sample Small Large

𝑎1 -0.321 -0.076 -0.581

(-1.360) (-0.209) (-1.283)

𝑎2 0.742*** 0.719*** 0.669***

(17.162) (12.300) (5.874)

Observations 7,560 2,520 2,520

Relative spread and MID

Should we be afraid of the dark?

Dark pools seem to be used mainly by

uninformed traders and not to have a

negative effect on price efficiency

No evidence that SPT harms liquidity: QJ

seems to improve market quality at least for

liquid stocks and MID shows no significant

effect, both in US and Canada

But too early to draw final conclusions… we

still need better data!