from agri to brand-led - asx · 3 twe’s journey from agri to brand-led key takeaways from today 1...

TRANSCRIPT

1

FROM AGRI TO BRAND-LEDTWE’s Inaugural Investor Day, 2017

For

per

sona

l use

onl

y

2

From Agricultural to Brand-ledMichael Clarke – Chief Executive Officer

For

per

sona

l use

onl

y

3

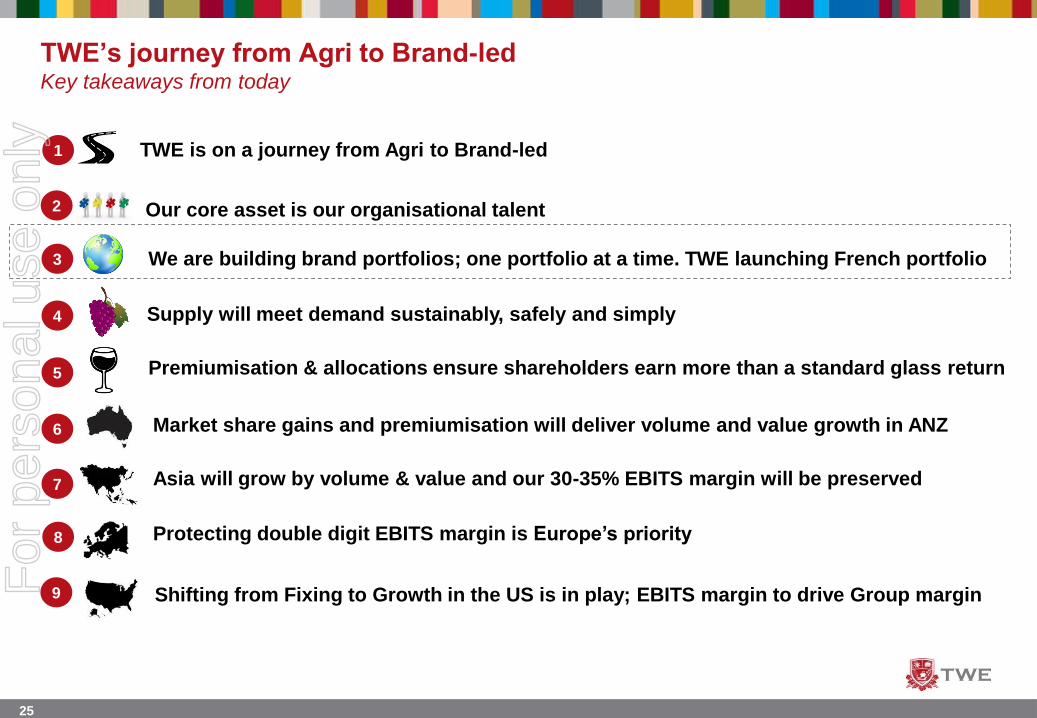

TWE’s journey from Agri to Brand-ledKey takeaways from today

1

2 Our core asset is our organisational talent

3

4

5 Premiumisation & allocations ensure shareholders earn more than a standard glass return

6 Market share gains and premiumisation will deliver volume and value growth in ANZ

7

9

8 Protecting double digit EBITS margin is Europe’s priority

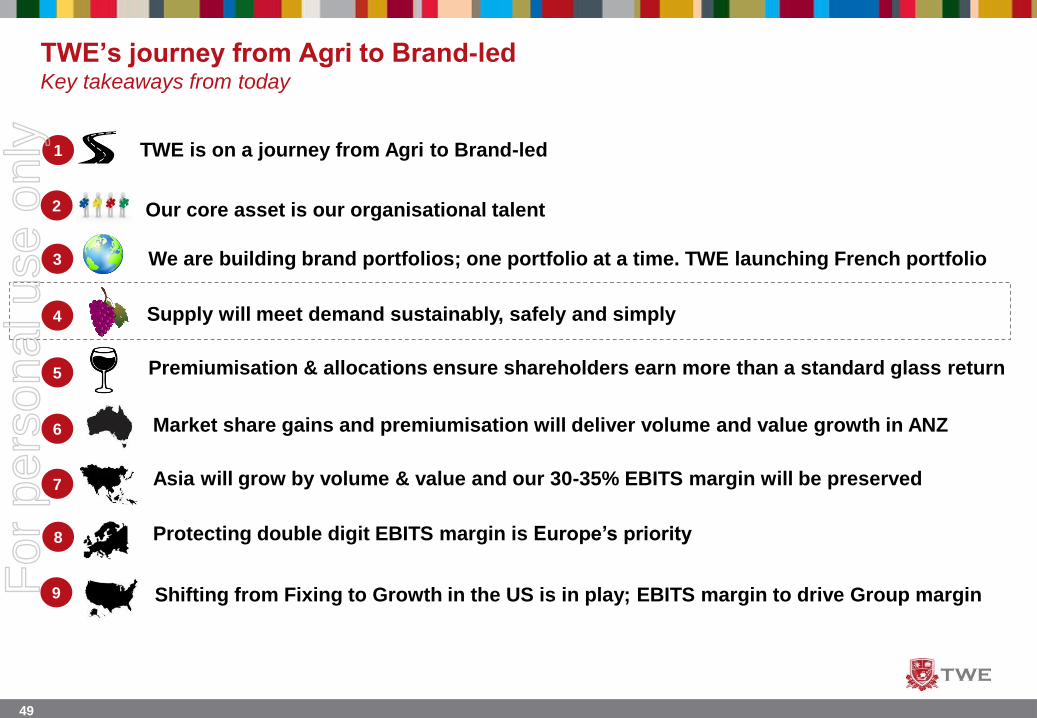

TWE is on a journey from Agri to Brand-led

We are building brand portfolios; one portfolio at a time. TWE launching French portfolio

Supply will meet demand sustainably, safely and simply

Asia will grow by volume & value and our 30-35% EBITS margin will be preserved

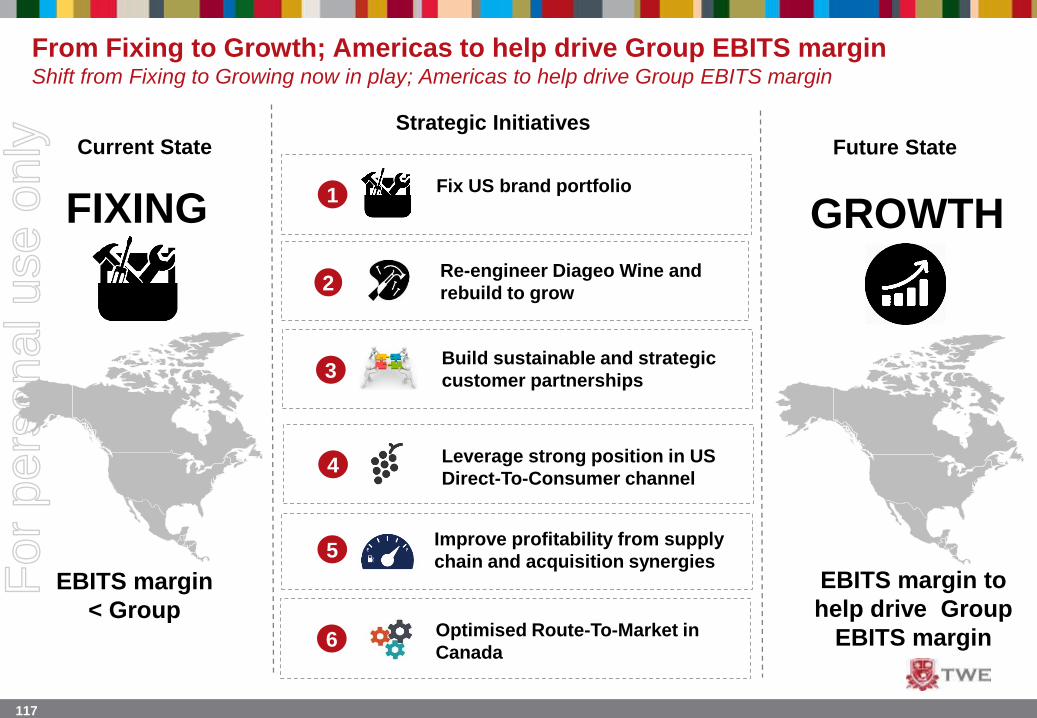

Shifting from Fixing to Growth in the US is in play; EBITS margin to drive Group marginFor

per

sona

l use

onl

y

4

TWE’s journey from Agri to Brand-ledTWE’s strategic framework

Focus on top

priorities and deliver

against them

Instil belief in our

wines, our company

and our people

Build trust by acting

with integrity and holding

ourselves to account

Collaborate with all

stakeholders to achieve

shared goals

To move from an order-taking agricultural business to a brand-led organisation

To be the world’s most celebrated wine company

Transform our

portfolio

• Grow Priority

Brands, one portfolio

at a time

• Support our

Regional Brands

• Premiumise our

portfolio

• Invest to drive

consumer pull

• Deliver bigger,

better campaigns

Win in priority

markets

• Grow share in Asia

through RTM and

portfolio expansion

• Grow in US through

premiumisation

• Strengthen no.1

position in Australia

through category

leadership

• Protect profitability in

other key markets

• Drive an inclusive,

supportive and

collaborative culture

• Grow capability now

and for the future

• Operate an efficient

and sustainable

structure

Build a high

performing

organisation

• Connect and engage

with consumers

• Partner with key

customers to grow

wine category

• Drive performance

for all stakeholders

Develop

long-term

relationships

Optimise our

capital base

• Operate sustainably,

safely and

responsibly

• Create supply chain

cost and quality

advantage

• Address high cost

structures in mature

markets

• Simplify processes

For

per

sona

l use

onl

y

5

1H14 1H17

NSR per case $53.20 $69.10

EBITS $46m $227m

EBITS margin 5.6% 17.5%

Cash conversion 25% 104%

ROCE1 5.8% 11.7%

TSR1,2 5.6% 31.2%

LOW A&P SPEND

TWE’s journey from Agri to Brand-ledOur journey and achievements to date

FROM:

Order-taking, agricultural model

TO:

Brand-led with sustainable and balanced delivery

SHORT TERM SHIPMENT FOCUS

AGRICULTURAL

I N E F F I C I E N T

UNSUSTAINABLE H I G H - C O S T

COMPLEX SUPPLY CHAIN

INNOVATION

DEPLETIONS

QUALITY

S U S T A I N A B I L I T Y

PREMIUMISATIONOPTIMISATIONM O M E N T U M

BALANCE

STRATEGIC

PARTNERSHIPSPROFITABILITY

CAPITAL EFFICIENT

MULTI-REGION SOURCING

DISCIPLINE

FIXINGHIGH PERFORMANCE CULTURE

BRAND BUILDING

1. Expressed as annualised metric

2. Total Shareholder Return (TSR) calculated using Bloomberg. Bloomberg methodology assumes dividends are reinvested into the purchase of additional

securities on each dividend date

For

per

sona

l use

onl

y

6

TWE’s three-phased journey from Agri to Brand-ledPositioning all four regions for sustainable growth

People Brands

Partners Model

ANZ

Growing sustainable share in

a mature market

Phase 1: Fixing

Phase 2:

Growing

Phase 3:

Accelerating

Asia

#1 imported wine business in

Asia by volume and value

Europe

An optimised business delivering

double digit EBITS margin

Brands

Partners Model

People Brands

Partners Model

People

Americas

From fixing to growth

People Brands

Partners Model

For

per

sona

l use

onl

y

7

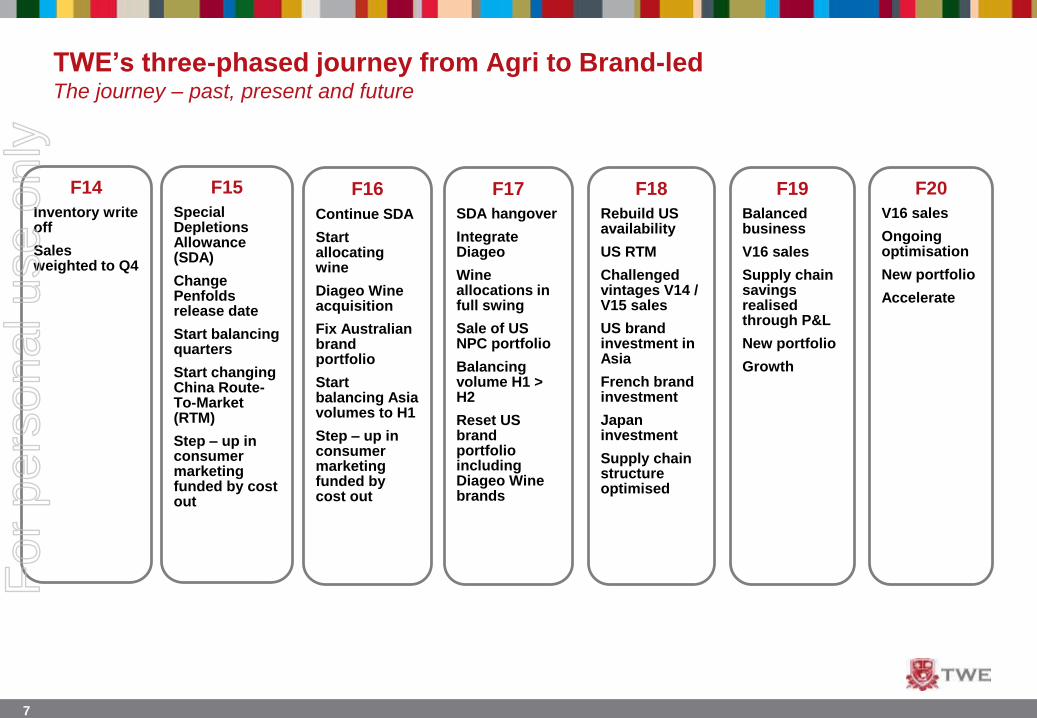

TWE’s three-phased journey from Agri to Brand-ledThe journey – past, present and future

F14

Inventory write off

Sales weighted to Q4

F15

Special Depletions Allowance (SDA)

Change Penfolds release date

Start balancing quarters

Start changing China Route-To-Market (RTM)

Step – up in consumer marketing funded by cost out

F16

Continue SDA

Start allocating wine

Diageo Wine acquisition

Fix Australian brand portfolio

Start balancing Asia volumes to H1

Step – up in consumer marketing funded by cost out

F17

SDA hangover

Integrate Diageo

Wine allocations in full swing

Sale of US NPC portfolio

Balancing volume H1 > H2

Reset US brand portfolio including Diageo Wine brands

F18

Rebuild US availability

US RTM

Challenged vintages V14 / V15 sales

US brand investment in Asia

French brand investment

Japan investment

Supply chain structure optimised

F19

Balanced business

V16 sales

Supply chain savings realised through P&L

New portfolio

Growth

F20

V16 sales

Ongoing optimisation

New portfolio

Accelerate

For

per

sona

l use

onl

y

8

TWE’s journey from Agri to Brand-ledKey takeaways from today

1

2 Our core asset is our organisational talent

3

4

5 Premiumisation & allocations ensure shareholders earn more than a standard glass return

6 Market share gains and premiumisation will deliver volume and value growth in ANZ

7

9

8 Protecting double digit EBITS margin is Europe’s priority

TWE is on a journey from Agri to Brand-led

We are building brand portfolios; one portfolio at a time. TWE launching French portfolio

Supply will meet demand sustainably, safely and simply

Asia will grow by volume & value and our 30-35% EBITS margin will be preserved

Shifting from Fixing to Growth in the US is in play; EBITS margin to drive Group marginFor

per

sona

l use

onl

y

9

From Bud to FruitMegan Collins – Chief People & Communications

Officer

For

per

sona

l use

onl

y

10

From bud to fruitSelecting the right bottle of wine

Varietal

Price

Awards & ScoresPackaging

PromotionCountry of Origin

Red Shiraz Pinot

NoirCabernet

Sauvignon R e d B l e n d

Merlot Syrah

RoseChardonnay

S

P

A

R

K

L

I

N

G

Sauvignon Blanc

Pin

ot G

ris

Riesling

PINOT

GRIGIO

Moscato

WHITE

‘World’s most

admired wine

brand’

- Drinks

International

(UK) March 16

‘Red Winemaker of

the Year’

- International Wine

Competition

‘Best New Wine 2015’

- Market Watch

New World

Old World

Buy 6

bottles @....

Price promotion

to

Price = Quality

Price reduced from…

For

per

sona

l use

onl

y

11

From bud to fruitTerroir

Soil

Terrain

Climate

For

per

sona

l use

onl

y

12

From bud to fruitTWE’s terroir in 2013

For

per

sona

l use

onl

y

13

For

per

sona

l use

onl

y

14

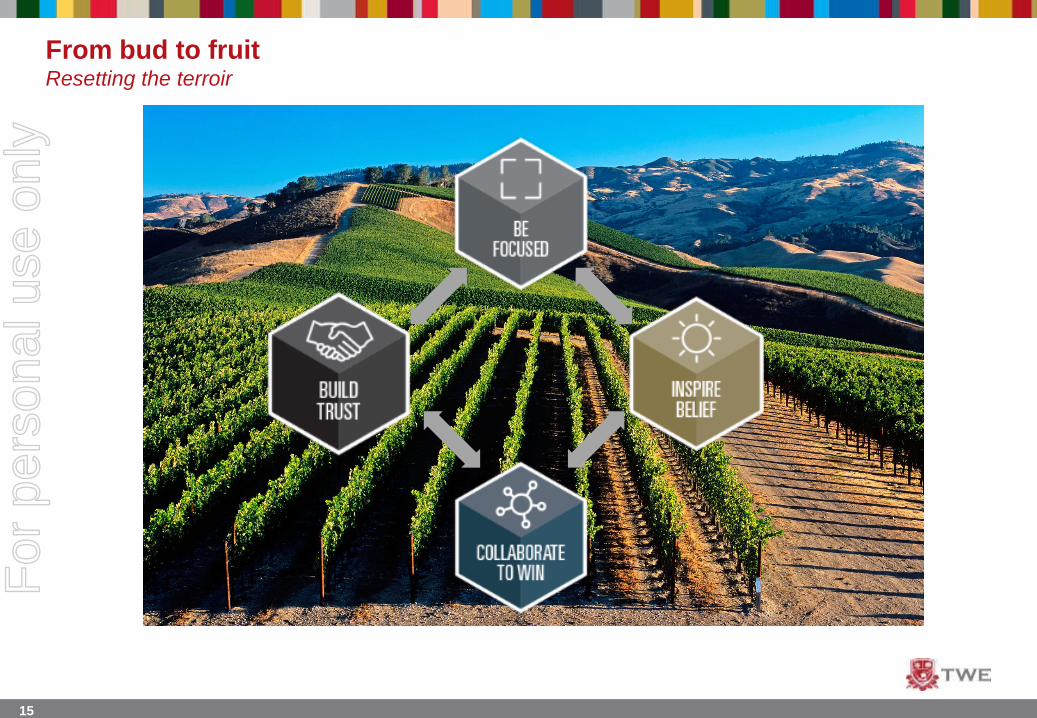

From bud to fruitResetting the terroir

For

per

sona

l use

onl

y

15

From bud to fruitResetting the terroir

For

per

sona

l use

onl

y

16

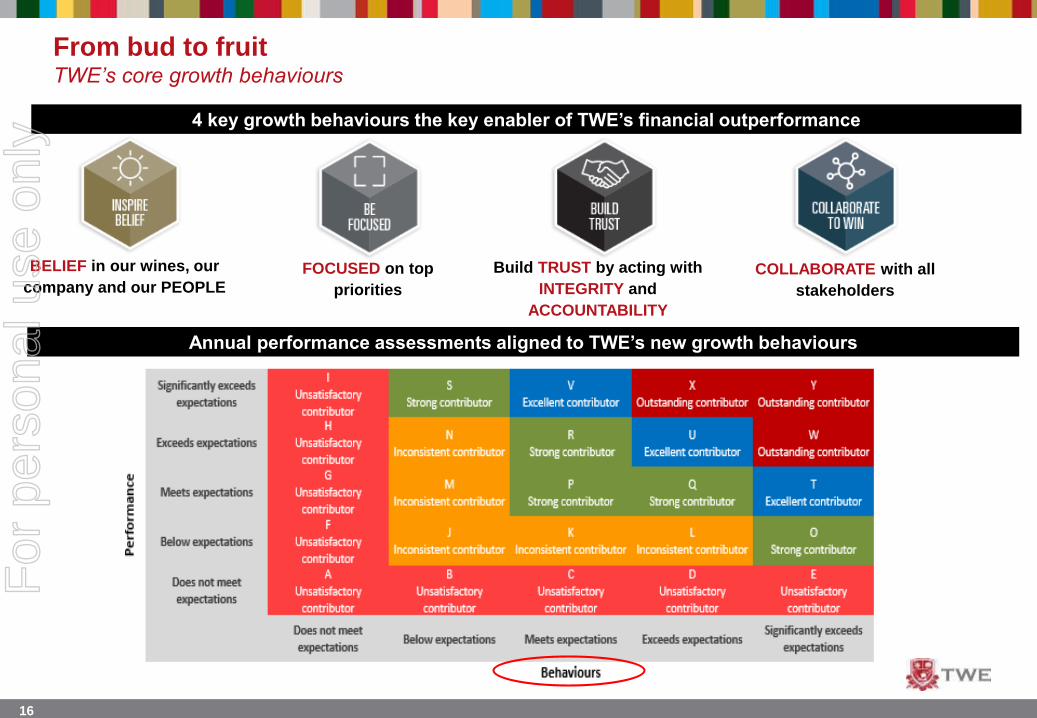

From bud to fruitTWE’s core growth behaviours

FOCUSED on top

priorities

COLLABORATE with all

stakeholders

BELIEF in our wines, our

company and our PEOPLE

Build TRUST by acting with

INTEGRITY and

ACCOUNTABILITY

4 key growth behaviours the key enabler of TWE’s financial outperformance

Annual performance assessments aligned to TWE’s new growth behaviours

For

per

sona

l use

onl

y

17

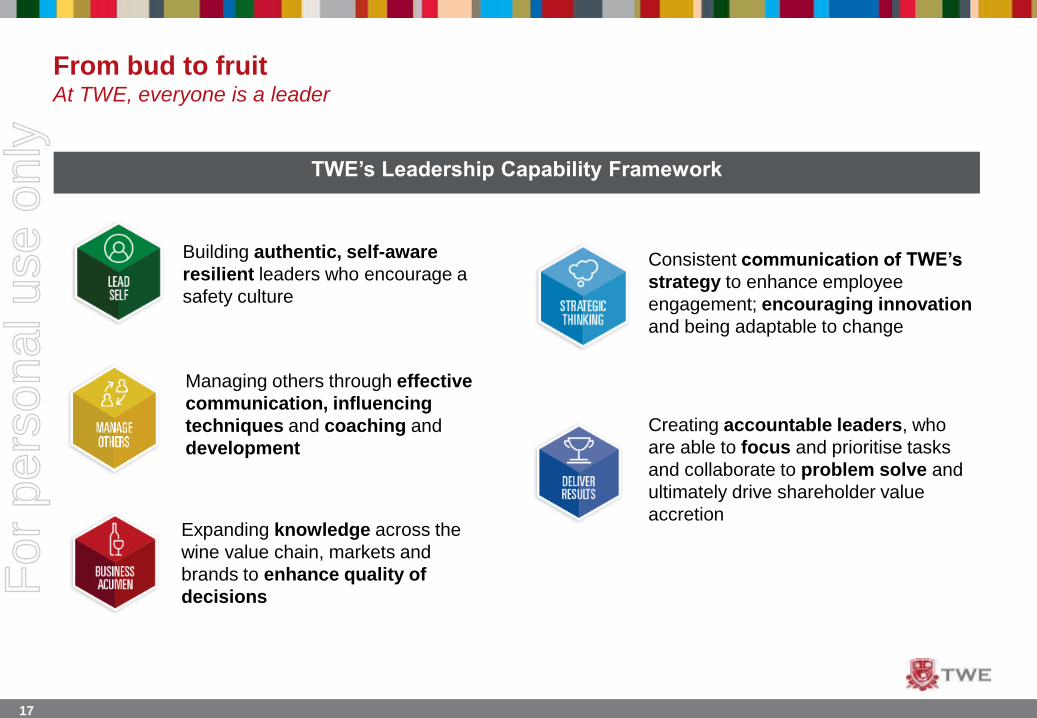

From bud to fruitAt TWE, everyone is a leader

TWE’s Leadership Capability Framework

Building authentic, self-aware

resilient leaders who encourage a

safety culture

Managing others through effective

communication, influencing

techniques and coaching and

development

Expanding knowledge across the

wine value chain, markets and

brands to enhance quality of

decisions

Consistent communication of TWE’s

strategy to enhance employee

engagement; encouraging innovation

and being adaptable to change

Creating accountable leaders, who

are able to focus and prioritise tasks

and collaborate to problem solve and

ultimately drive shareholder value

accretion

For

per

sona

l use

onl

y

18

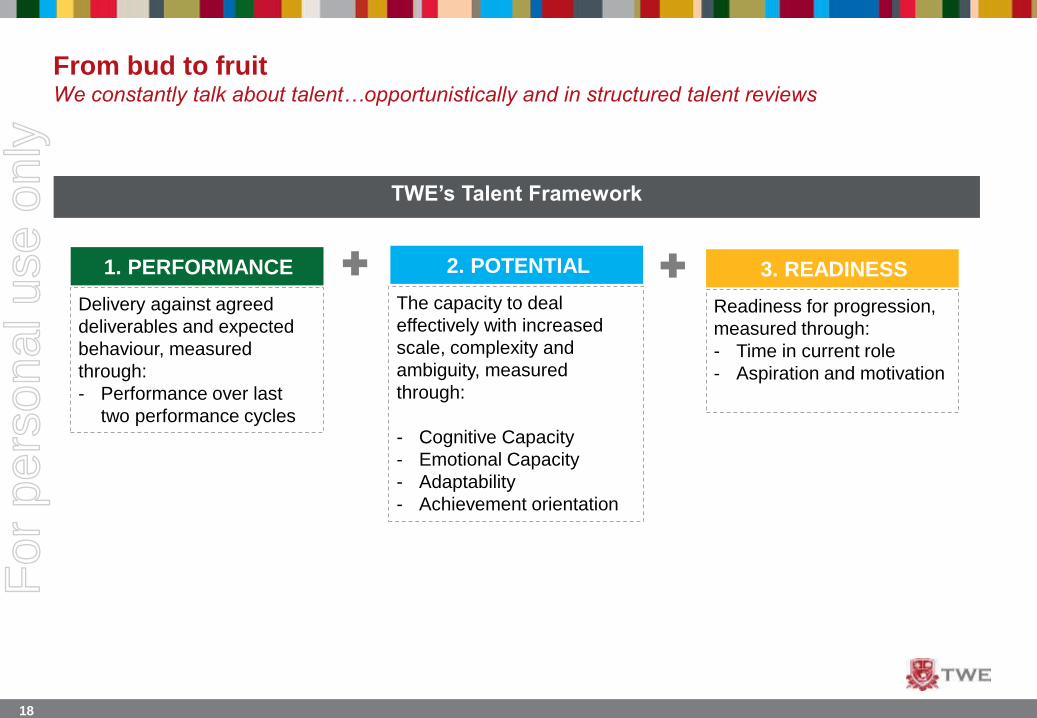

1. PERFORMANCE 2. POTENTIAL 3. READINESS

Delivery against agreed

deliverables and expected

behaviour, measured

through:

- Performance over last

two performance cycles

The capacity to deal

effectively with increased

scale, complexity and

ambiguity, measured

through:

- Cognitive Capacity

- Emotional Capacity

- Adaptability

- Achievement orientation

Readiness for progression,

measured through:

- Time in current role

- Aspiration and motivation

From bud to fruitWe constantly talk about talent…opportunistically and in structured talent reviews

TWE’s Talent Framework

For

per

sona

l use

onl

y

19

From bud to fruitBuy, develop and re-build our capability

Develop … build capability for the future

Buy … de-risk the business

Rebuild … define the new normalFor

per

sona

l use

onl

y

20

Annual business performance

aligned with employee reward…

Long term business performance

aligns employees’ financial interests

with the financial interests of

shareholders …

HIGHEST REWARDS FOR OUTPERFORMERS SHARE THE SUCCESS

Short Term Incentive Plan

(STIP)

Senior Managers

Sales Incentive Plan Salesforce

High Performance Plan (HiPP) Other high performers

Long Term Incentive Plan

(LTIP)

Executives

Restricted Equity Plan (REP) Key Talent

General Employee Share

Plan

All employees

From bud to fruitRewarding, retaining and attracting outperformers

For

per

sona

l use

onl

y

21

LEADERSHIP & PERSONAL DEVELOPMENT

Building Business

Acumen® (BBA)

FUNCTIONAL CAPABILITY

PROGRAMS

Commercial

Partnering

14

From bud to fruitActive investment in growing employee capability, now and for the future

For

per

sona

l use

onl

y

22

Focus on top

priorities and deliver

against them

Instil belief in our

wines, our company

and our people

Build trust by acting

with integrity and holding

ourselves to account

Collaborate with all

stakeholders to achieve

shared goals

To move from an order-taking agricultural business to a brand-led marketing organisation

To be the world’s most celebrated wine company

13

From bud to fruitOur focus and investment in People – an enabler of our results

• Drive an inclusive,

supportive and

collaborative culture

• Grow capability now

and for the future

• Operate an efficient

and sustainable

structure

Build a high

performing

organisation

Transform

our portfolio

• Grow Priority

Brands, one

portfolio at a time

• Support our

Regional Brands

• Premiumise our

portfolio

• Invest to drive

consumer pull

• Deliver bigger,

better campaigns

Win in priority

markets

• Grow share in Asia

through RTM and

portfolio expansion

• Grow in US through

premiumisation

• Strengthen no.1

position in Australia

through category

leadership

• Protect profitability in

other key markets

• Connect and

engage with

consumers

• Partner with key

customers to grow

wine category

• Drive performance

for all stakeholders

Develop

long-term

relationships

Optimise our

capital base

• Operate

sustainably, safely

and responsibly

• Create supply chain

cost and quality

advantage

• Address high cost

structures in mature

markets

• Simplify processes

For

per

sona

l use

onl

y

23

For

per

sona

l use

onl

y

24

QUESTIONS

For

per

sona

l use

onl

y

25

TWE’s journey from Agri to Brand-ledKey takeaways from today

1

2 Our core asset is our organisational talent

3

4

5 Premiumisation & allocations ensure shareholders earn more than a standard glass return

6 Market share gains and premiumisation will deliver volume and value growth in ANZ

7

9

8 Protecting double digit EBITS margin is Europe’s priority

TWE is on a journey from Agri to Brand-led

We are building brand portfolios; one portfolio at a time. TWE launching French portfolio

Supply will meet demand sustainably, safely and simply

Asia will grow by volume & value and our 30-35% EBITS margin will be preserved

Shifting from Fixing to Growth in the US is in play; EBITS margin to drive Group marginFor

per

sona

l use

onl

y

26

Rebuilding TWE; One Portfolio at a

TimeSimon Marton – Chief Marketing Officer

For

per

sona

l use

onl

y

27

Wine is growing share of total alcohol globally1

11.82016

26.8

2016

Litres per

capita2

Litres per

capita2 2.1

2016

Litres per

capita2

1. Trend data per Euromonitor InternationaslAlcoholic Drinks Overview by Market, September 2015, Value data per Euromonitor International, 2014

2. Euromonitor International 2016, Still Light Grape Wine, Litres per capita at legal purchasing age

For

per

sona

l use

onl

y

28

When we began our Journey 3 years ago, we were focusing on too many brands

For

per

sona

l use

onl

y

29

We have moved to a focused portfolio of 15 priority brands to maximise global growth

Luxury

Centre of

Gravity

Masstige

Centre of

Gravity

Commercial

Centre of

GravityFor

per

sona

l use

onl

y

30

BRAND GROUPS POWER BRANDS PRIORITY BRANDS LUXURY GEMS

BRANDS

INVESTMENT

TACTICS

Deliver 360° investment plans,

increasing consumer A&P

Invest in outstanding packaging,

merchandising and in-store/trade support

Take a portfolio approach. Focus on PR

and 90+ platform to leverage scores/

awards

With clear segmentation and associated investment tactics

For

per

sona

l use

onl

y

31

We have focused on key strategies to deliver this result

GROWTH AND MARGIN

ACCRETION

Engaging consumers

across all channels

Global Umbrella

BrandsInnovation

Creating Apparent

Scarcity

Multi Regional

Sourcing

• Capture Multiple

Consumer

Opportunities

• Build Scalable

Consumer Solutions

• Keep our Brands

relevant

• Drive Premiumisation

& Margin Accretion

• Build Global Scale

• Step Up in A&P

Investment

• Improve consumer

appeal in market

• De Risk our supply

network

• Disciplined

allocations process

and behaviours

• Global pricing

standards

For

per

sona

l use

onl

y

32

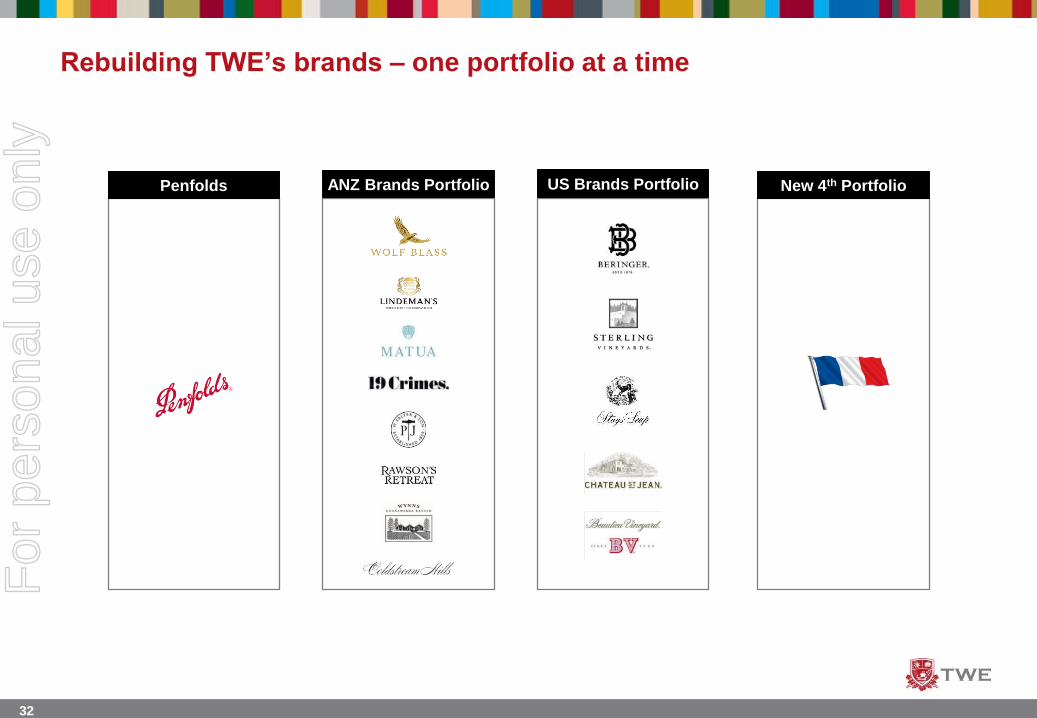

Rebuilding TWE’s brands – one portfolio at a time

Penfolds ANZ Brands Portfolio US Brands Portfolio New 4th Portfolio

For

per

sona

l use

onl

y

33

Rebuilding TWE’s brands – Penfolds

Brand potential limited

• Limited by Mar/May release

• Selling everything in Q4 every year with nothing held

back for future

• Poor pricing behaviours

• Heavy reliance on few countries

• Asia not being realised

• Under investment in recruitment of new consumers

For

per

sona

l use

onl

y

34

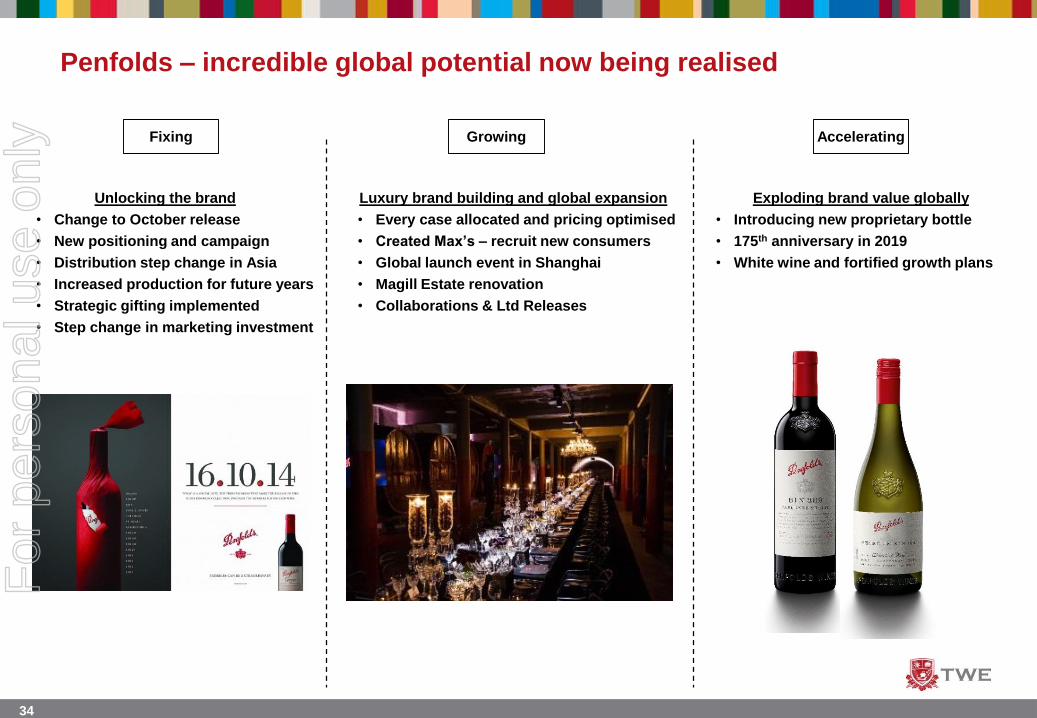

Penfolds – incredible global potential now being realised

Fixing Growing Accelerating

Unlocking the brand

• Change to October release

• New positioning and campaign

• Distribution step change in Asia

• Increased production for future years

• Strategic gifting implemented

• Step change in marketing investment

Exploding brand value globally

• Introducing new proprietary bottle

• 175th anniversary in 2019

• White wine and fortified growth plans

Luxury brand building and global expansion

• Every case allocated and pricing optimised

• Created Max’s – recruit new consumers

• Global launch event in Shanghai

• Magill Estate renovation

• Collaborations & Ltd Releases

For

per

sona

l use

onl

y

35

Rebuilding TWE’s brands – ANZ Portfolio of Brands

Brand potential limited

• Wolf Blass – stalled growth, needed revitalisation

• Lindeman's – mature brand in commercial segment

• Wynns – constrained supply, needed growth model

• Matua – innovating for growth

• 19 Crimes – category disruptor

• Regional Gems – liberating quality and heritage

For

per

sona

l use

onl

y

36

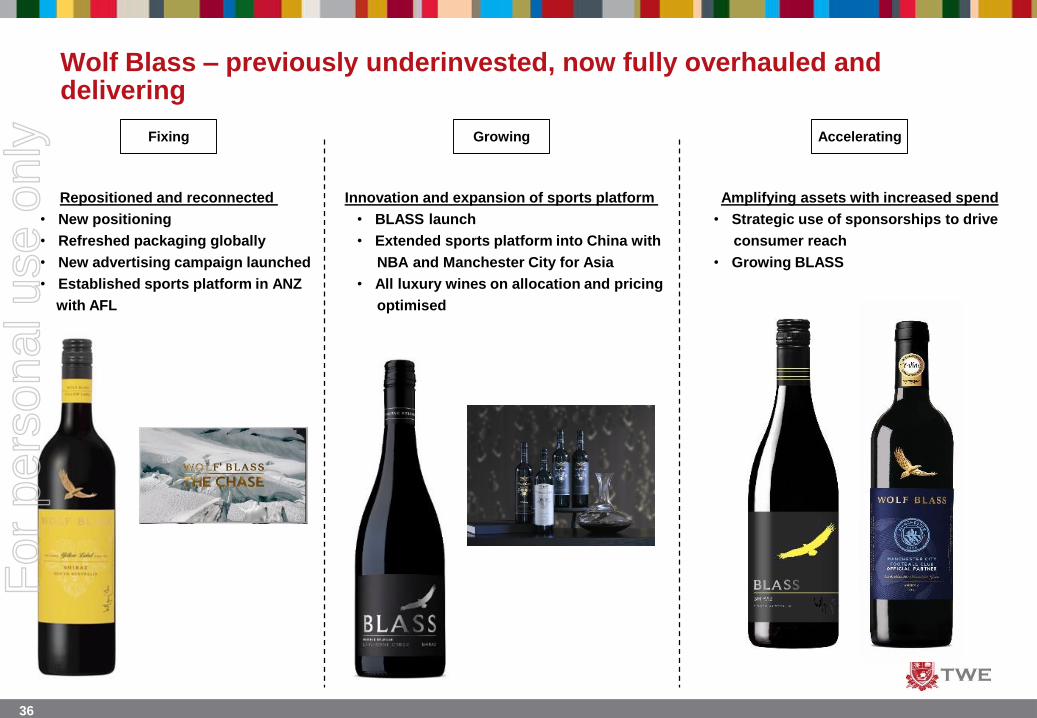

Wolf Blass – previously underinvested, now fully overhauled and delivering

Fixing Growing Accelerating

Repositioned and reconnected

• New positioning

• Refreshed packaging globally

• New advertising campaign launched

• Established sports platform in ANZ

with AFL

Amplifying assets with increased spend

• Strategic use of sponsorships to drive

consumer reach

• Growing BLASS

Innovation and expansion of sports platform

• BLASS launch

• Extended sports platform into China with

NBA and Manchester City for Asia

• All luxury wines on allocation and pricing

optimised

For

per

sona

l use

onl

y

37

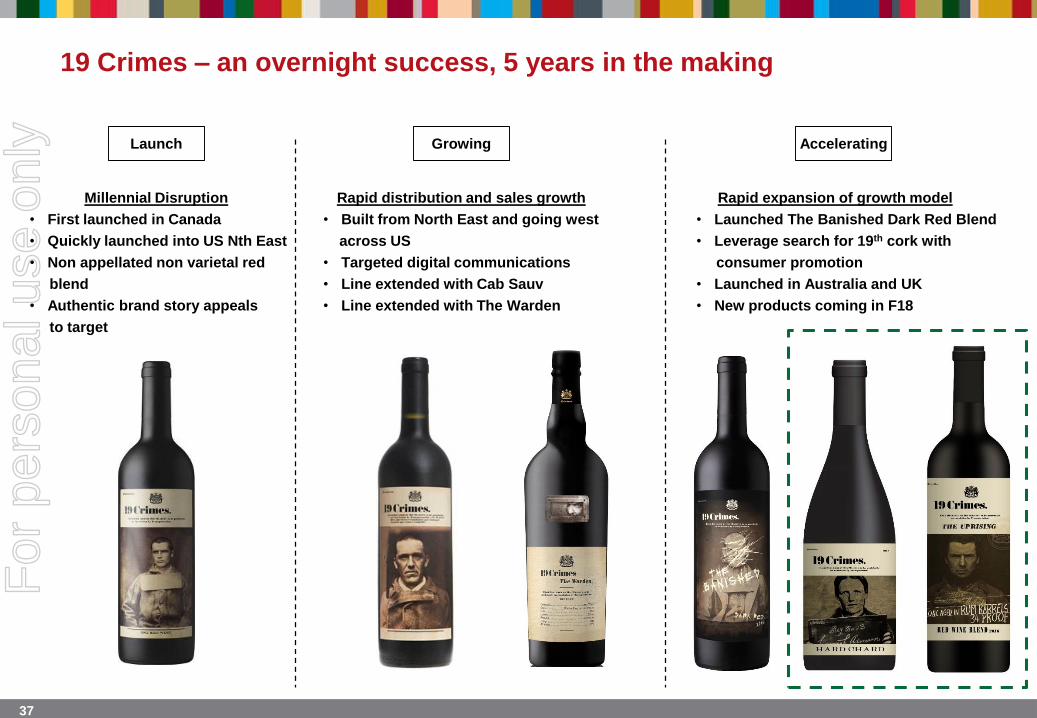

19 Crimes – an overnight success, 5 years in the making

Launch Growing Accelerating

Millennial Disruption

• First launched in Canada

• Quickly launched into US Nth East

• Non appellated non varietal red

blend

• Authentic brand story appeals

to target

Rapid expansion of growth model

• Launched The Banished Dark Red Blend

• Leverage search for 19th cork with

consumer promotion

• Launched in Australia and UK

• New products coming in F18

Rapid distribution and sales growth

• Built from North East and going west

across US

• Targeted digital communications

• Line extended with Cab Sauv

• Line extended with The Warden

For

per

sona

l use

onl

y

38

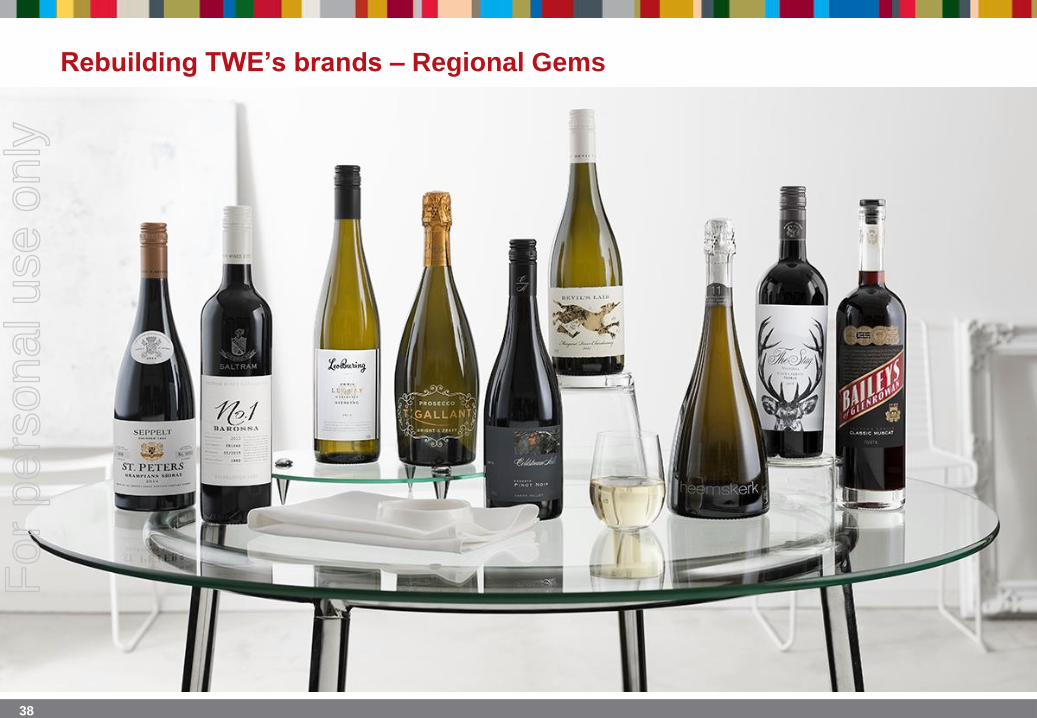

Rebuilding TWE’s brands – Regional Gems

For

per

sona

l use

onl

y

39

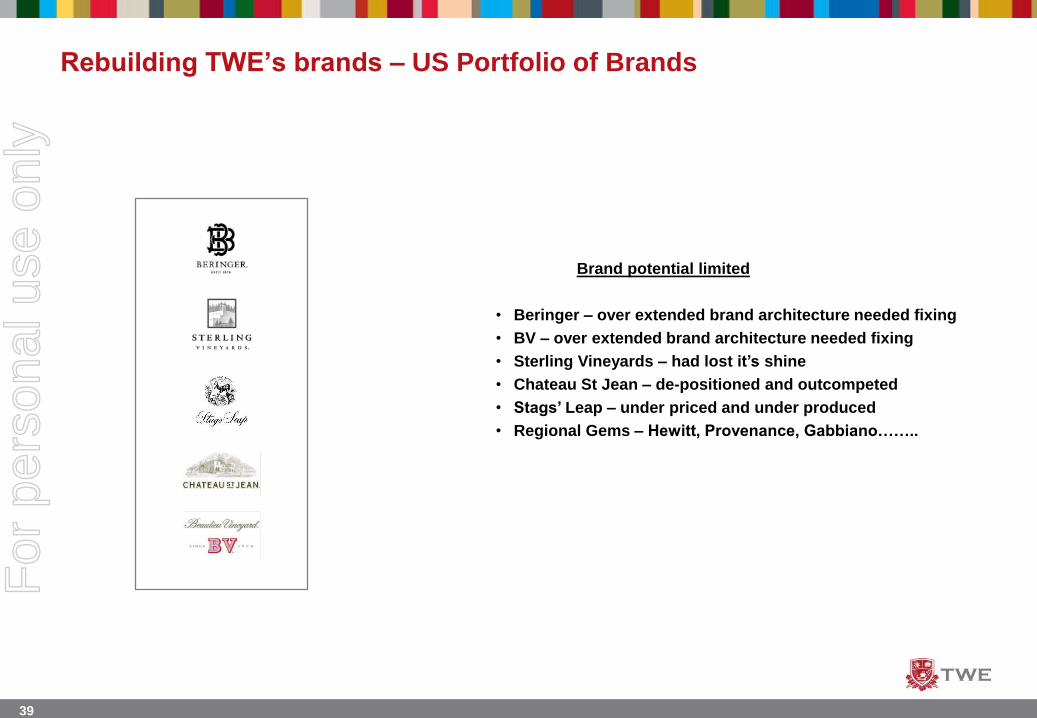

Rebuilding TWE’s brands – US Portfolio of Brands

Brand potential limited

• Beringer – over extended brand architecture needed fixing

• BV – over extended brand architecture needed fixing

• Sterling Vineyards – had lost it’s shine

• Chateau St Jean – de-positioned and outcompeted

• Stags’ Leap – under priced and under produced

• Regional Gems – Hewitt, Provenance, Gabbiano……..

For

per

sona

l use

onl

y

40

Beringer & Beaulieu Vineyards – brand separation and pack upgrades

For

per

sona

l use

onl

y

41

Sterling Vineyards – reinvented, now polished with premium potential

Fixing Growing

Complete brand overhaul

• Redefined brand positioning and new advertising campaign

• Incredible standout new packaging

• Pricing stabilised and reset

Set to shine

• All luxury wines now globally allocated and price optimised

• Launched in Asia and LATAM with winemaker and PR programs

• Digital communication spearhead

• Major innovation ready for launch in F18

For

per

sona

l use

onl

y

42

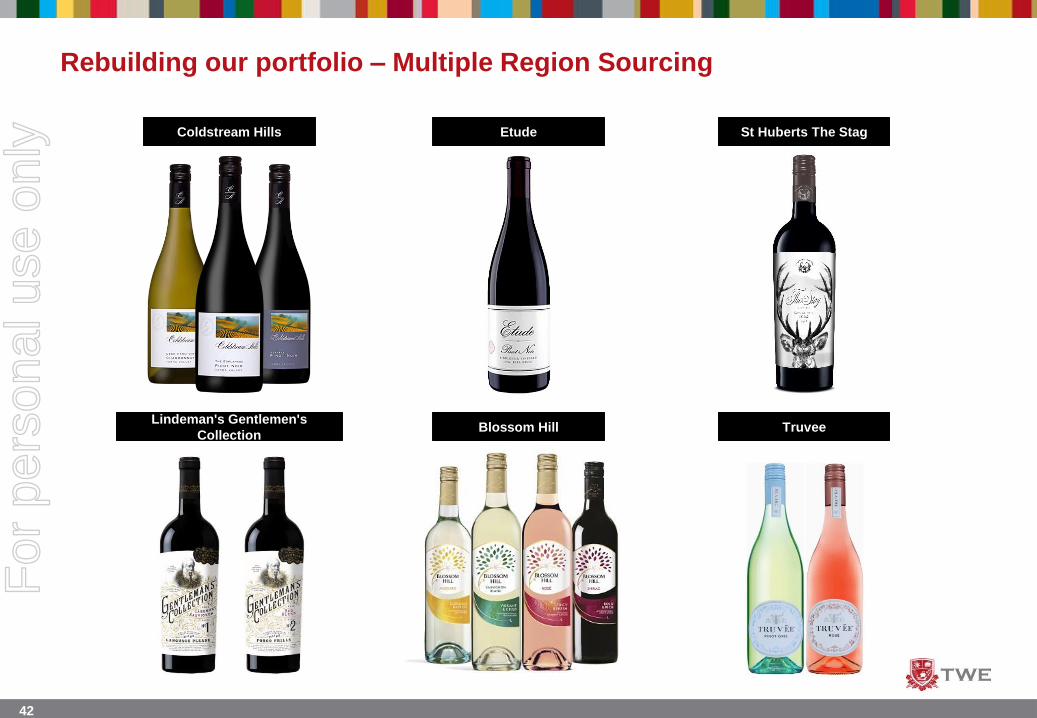

Rebuilding our portfolio – Multiple Region Sourcing

Coldstream Hills Etude St Huberts The Stag

Lindeman's Gentlemen's

CollectionBlossom Hill Truvee

For

per

sona

l use

onl

y

43

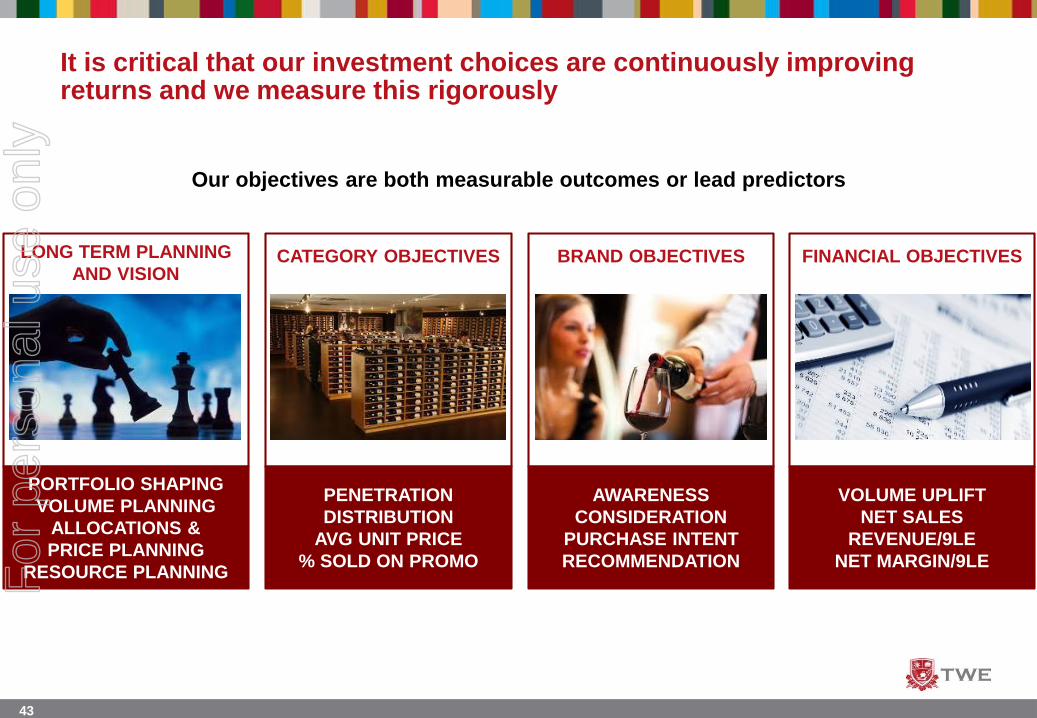

It is critical that our investment choices are continuously improving returns and we measure this rigorously

PENETRATION

DISTRIBUTION

AVG UNIT PRICE

% SOLD ON PROMO

AWARENESS

CONSIDERATION

PURCHASE INTENT

RECOMMENDATION

VOLUME UPLIFT

NET SALES

REVENUE/9LE

NET MARGIN/9LE

FINANCIAL OBJECTIVESCATEGORY OBJECTIVES BRAND OBJECTIVES

Our objectives are both measurable outcomes or lead predictors

PORTFOLIO SHAPING

VOLUME PLANNING

ALLOCATIONS &

PRICE PLANNING

RESOURCE PLANNING

LONG TERM PLANNING

AND VISION

For

per

sona

l use

onl

y

44

44

Mar Apr May June July Aug Sept Oct Nov Dec Jan Feb Mar Apr

F17

April GMBR

4th April Board presentation of

F18 Strategic Plan & F18

Budget

F18

Oct FI/GMBR

April Board presentation

of F19 Strategic Plan &

F19 Budget

S Hemi

VCN Hemi

VC

GVA 5Y Vol

Review

Development of F19-23

Strategic Plan (5Y)

F19 Regional

Brand Plan

(inc pricing)

F19 Global

Brand Plan

June

PMRSept PMR Dec PMR

N Hemi

VC

Budget

COGS F19 COGS

Placeholders

calculated

Assess budget for

material updatesDevelopment of Budget

(detailed)

Bal Sht and

Cashflow

submitted

Forecast

GVA

5YP Strat

Plan

PMR

Brand

Planning

Vintage

Commit

ELT Aug F19 Global

Brand Plan Sign Off

Jan FI/GMBR

Mar PMR

Pre-Vintage

Refresh

Detailed Regional

Activation Plan (inc pricing)

High Level Regional

Activation PlanF19 Regional

Category Plan

(inc channel)

3Y Regional Category

Growth StrategyCategory

Planning

5Y Global

Category

Growth

Strategy

Pre-

Vintage

RefreshLux All’n

Apr FI/GMBR

F18 Budget

Development

Mar PMR

5Y Global Brand

Strategy

F18 COGS

Stds calculated

A&P All’n

Check

Ins

F16 example of our long term integrated planning as the centrepiece of

rebuilding the portfolio

For

per

sona

l use

onl

y

45

Rebuilding TWE’s brands – adding a 4th portfolio to TWE

New 4th Portfolio

For

per

sona

l use

onl

y

46

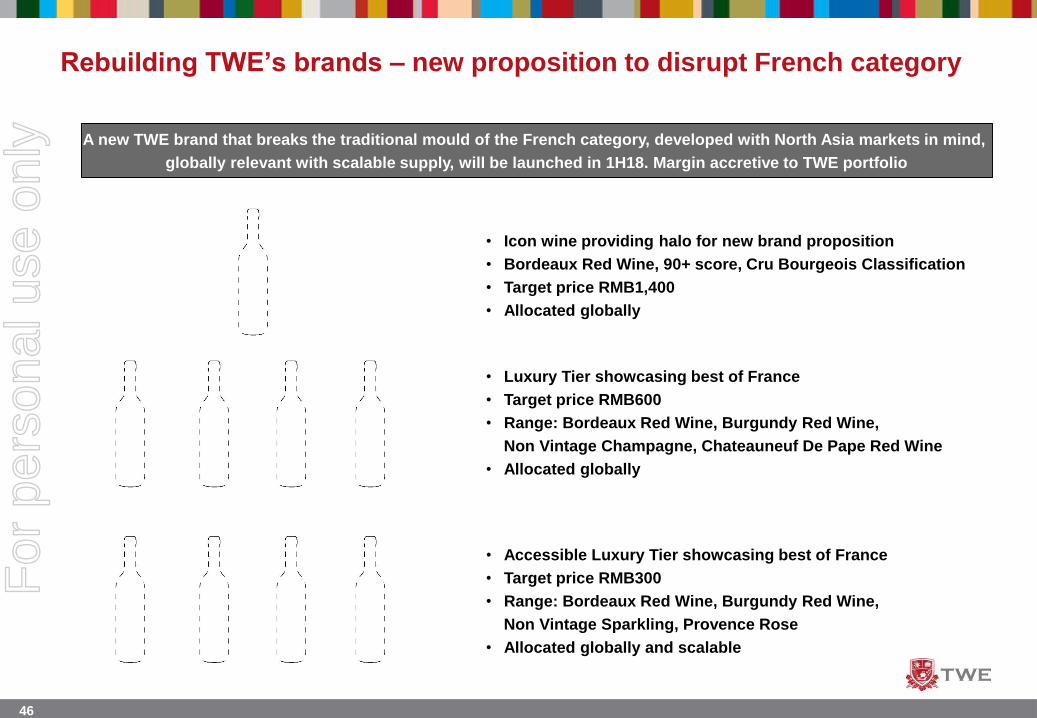

Rebuilding TWE’s brands – new proposition to disrupt French category

• Icon wine providing halo for new brand proposition

• Bordeaux Red Wine, 90+ score, Cru Bourgeois Classification

• Target price RMB1,400

• Allocated globally

• Luxury Tier showcasing best of France

• Target price RMB600

• Range: Bordeaux Red Wine, Burgundy Red Wine,

Non Vintage Champagne, Chateauneuf De Pape Red Wine

• Allocated globally

• Accessible Luxury Tier showcasing best of France

• Target price RMB300

• Range: Bordeaux Red Wine, Burgundy Red Wine,

Non Vintage Sparkling, Provence Rose

• Allocated globally and scalable

A new TWE brand that breaks the traditional mould of the French category, developed with North Asia markets in mind,

globally relevant with scalable supply, will be launched in 1H18. Margin accretive to TWE portfolio

For

per

sona

l use

onl

y

47

We have a proven and repeatable strategy that builds portfolios of brands

We have embedded discipline & rigour

We are creating long term value, by not chasing volume

We are optimising portfolio profitability globally

We have a portfolio of brands with scale backed by world class consumer & shopper insights

We are diversified and balanced on many levels;

- Brands, consumer segments, price points, sourcing and markets

We will have 4 strong brand portfolios across 4 strong regional business models

Our trust-marks are driving growth and margin accretion, for TWE and our partners, globally

So in summary, our brands are desired around the world for quality and

trust, ultimately delivering profitable growth

For

per

sona

l use

onl

y

48

QUESTIONS

For

per

sona

l use

onl

y

49

TWE’s journey from Agri to Brand-ledKey takeaways from today

1

2 Our core asset is our organisational talent

3

4

5 Premiumisation & allocations ensure shareholders earn more than a standard glass return

6 Market share gains and premiumisation will deliver volume and value growth in ANZ

7

9

8 Protecting double digit EBITS margin is Europe’s priority

TWE is on a journey from Agri to Brand-led

We are building brand portfolios; one portfolio at a time. TWE launching French portfolio

Supply will meet demand sustainably, safely and simply

Asia will grow by volume & value and our 30-35% EBITS margin will be preserved

Shifting from Fixing to Growth in the US is in play; EBITS margin to drive Group marginFor

per

sona

l use

onl

y

50

Supply Will Meet Demand;

Sustainably, Safely & SimplyTim Ford – Director of Supply Chain & Industry

Affairs

For

per

sona

l use

onl

y

51

Supply will meet demand sustainably, safely and simply TWE operates a world class supply chain model

1 Planted hectares reflect owned and leased vineyards

Sourcing profile reflects 2016 Vintage

L – Luxury, M – Masstige, C – Commercial

United States

48Vineyards

4,000 Planted

hectares1

9 Wineries

Australia New Zealand Italy

78Vineyards

8,939 Planted

hectares1

8 Wineries

8 Vineyards

339 Planted

hectares1

1 Winery

2 Vineyards

145 Planted

hectares1

1 Winery

Owned &

leased

Growers Bulk

Wine

L 67% 33% -

M 52% 47% 1%

C 5% 21% 74%

Owned &

leased

Growers Bulk

Wine

L 41% 52% 7%

M 45% 47% 8%

C 25% 59% 16%

Owned &

leased

Growers Bulk

Wine

L 86% 14% -

M 22% 77% 1%

C - - -

Owned

& leased

Growers Bulk

Wine

L 100% - -

M 54% 46% -

C - - 100%

For

per

sona

l use

onl

y

52

Supply will meet demand sustainably, safely and simply Destination Zero Harm

Every employee goes home safe, everyday

Safe plant and equipment Safe peopleSafe systems

For

per

sona

l use

onl

y

53

Supply will meet demand sustainably, safely and simply Brand Accolades

Top 100 Wines, Wine

Spectator

Awarded Impact ‘Hot Brand’ Award

2016

Won “Best New Wine” 2015 from

Market Watch

‘World’s Most Admired Wine Brand’

by Drinks International (UK), March

2016

No. 1 Australian wine brand; Norway,

Sweden and Netherlands

2015 Top 10 Global Wine Brands, Drinks

Business

Wolf Blass Black Label -

unprecedented four time winner of

‘Jimmy Watson Trophy’

TWE’s focus on quality and consistency underpins dominance in national and international wine

shows, with 57 trophies awarded in 2016

International Wine Competition (IWC)

‘Red Winemaker of the Year’ - 2016,

2013 and 2008

2008 Grange awarded 100 points

from Wine Spectator (US) and

Robert Parker’s Wine Advocate

(US)

70 90+ Scores

2016 Top 10 Global Wine Brands,

Drinks Business

100 club for Red and White wine,

Wine Spectator

For

per

sona

l use

onl

y

54

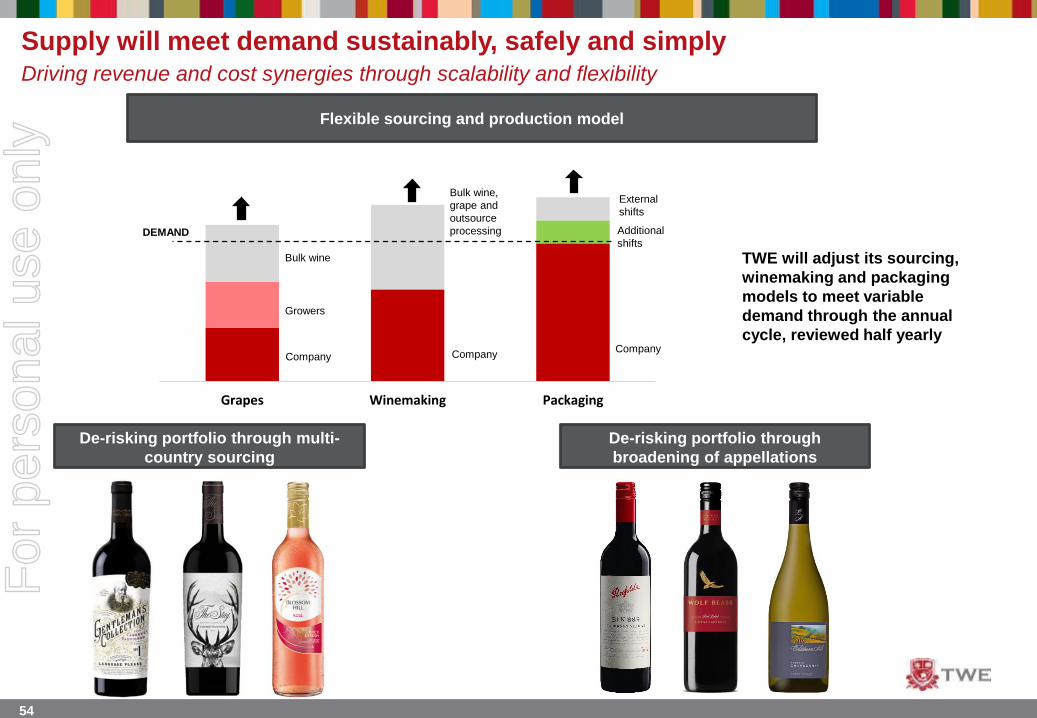

Flexible sourcing and production model

Supply will meet demand sustainably, safely and simplyDriving revenue and cost synergies through scalability and flexibility

Grapes Winemaking Packaging

TWE will adjust its sourcing,

winemaking and packaging

models to meet variable

demand through the annual

cycle, reviewed half yearly

DEMAND

Bulk wine

Growers

CompanyCompany

Bulk wine,

grape and

outsource

processing

External

shifts

Additional

shifts

Company

De-risking portfolio through multi-

country sourcing

De-risking portfolio through

broadening of appellations

For

per

sona

l use

onl

y

55

Supply will meet demand sustainably, safely and simply Supply Chain Optimisation; delivering margin accretion and optimised capital employed

Vineyards and sourcing

Production footprint Packaging, warehousing and logistics

Supply chain optimisation review

A$100mRun-rate COGS

savings by F20

Divestment

of non-core

vineyards

Reinvestment into

Luxury and

Masstige

vineyards

Shift sourcing for

Commercial fruit to

Grower and Bulk Wine

market

Consolidation

of packaging

facilities

In-market

bottling

Exit unprofitable

third party contract

packaging

Realign

warehousing

network

Optimise existing

RTM and realign

distribution network

Centres of

Excellence/Hubs

Consolidation

and closure of

excess wineries

Divestment of 12

Non-Priority

Commercial

Brands

35%Excess network

capacity removed

At least

US$35mRun-rate cash

synergies by F20 F18 Penfolds

allocation is in

line with F17;

with adverse

mix

For

per

sona

l use

onl

y

56

Supply will meet demand sustainably, safely and simply Project Uplift II

Owned vineyard yield optimisation Incremental access to Luxury and Masstige

supply

Viticultural excellence is improving TWE’s yield and access

to Luxury and Masstige supply, globally

Grade 2009 2016

Icon & A 1% 12%

B 17% 56%

C 24% 32%

D 58% Outsourced

This active investment has seen TWE’s vineyards transition

from Commercial to high-end Masstige and Luxury

Organic options include:

Expanding long term bulk wine partnerships

Building long term grower partnerships

Continued investment in shifting varietal mix

Inorganic options include:

Greenfield vineyard acquisition / leases

Established vineyard acquisition / leases

Block by block approach to vineyard management

Maximising yield vs quality trade-off across

portfolio of vineyards

Ensuring highest and best use by grade and

varietal of fruit off every block

For

per

sona

l use

onl

y

57

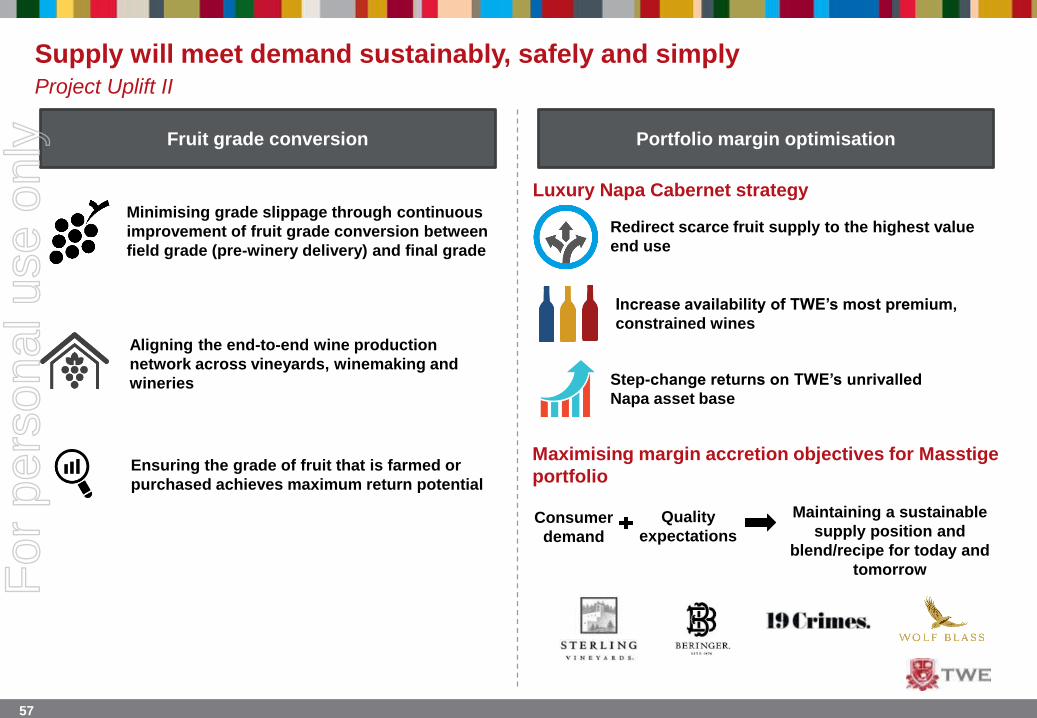

Supply will meet demand sustainably, safely and simply Project Uplift II

Fruit grade conversion Portfolio margin optimisation

Minimising grade slippage through continuous

improvement of fruit grade conversion between

field grade (pre-winery delivery) and final grade

Luxury Napa Cabernet strategy

Redirect scarce fruit supply to the highest value

end use

Increase availability of TWE’s most premium,

constrained wines

Step-change returns on TWE’s unrivalled

Napa asset base

Maximising margin accretion objectives for Masstige

portfolio

Aligning the end-to-end wine production

network across vineyards, winemaking and

wineries

Ensuring the grade of fruit that is farmed or

purchased achieves maximum return potential

Consumer

demand

Quality

expectations

Maintaining a sustainable

supply position and

blend/recipe for today and

tomorrowFor

per

sona

l use

onl

y

58

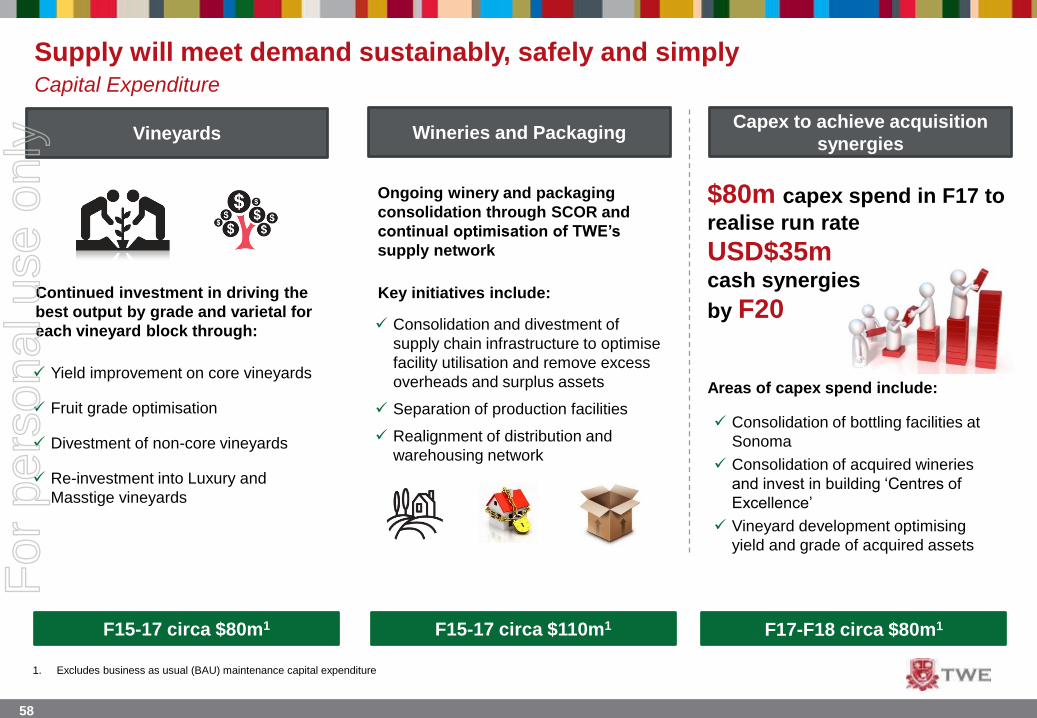

$80m capex spend in F17 to

realise run rate

USD$35mcash synergies

by F20

Vineyards Wineries and PackagingCapex to achieve acquisition

synergies

Yield improvement on core vineyards

Fruit grade optimisation

Divestment of non-core vineyards

Re-investment into Luxury and

Masstige vineyards

Continued investment in driving the

best output by grade and varietal for

each vineyard block through:

Key initiatives include:

Consolidation and divestment of

supply chain infrastructure to optimise

facility utilisation and remove excess

overheads and surplus assets

Separation of production facilities

Realignment of distribution and

warehousing network

Areas of capex spend include:

Consolidation of bottling facilities at

Sonoma

Consolidation of acquired wineries

and invest in building ‘Centres of

Excellence’

Vineyard development optimising

yield and grade of acquired assets

F17-F18 circa $80m1

Supply will meet demand sustainably, safely and simply Capital Expenditure

Ongoing winery and packaging

consolidation through SCOR and

continual optimisation of TWE’s

supply network

F15-17 circa $110m1F15-17 circa $80m1

1. Excludes business as usual (BAU) maintenance capital expenditure

For

per

sona

l use

onl

y

59

Sustainability in everything we doOur responsibility; making a positive contribution to our global community

Sustainable supply and sourcing

Independent sustainability

certification on all

owned/leased vineyards

Global roll-out of

Responsible Procurement

Code to all suppliers

Joint partnering to turn waste

into valuable products in the

Riverland region in South

Australia

Restoring river health and

floodplains of the Napa River

TWE’s Supply Chain

Optimisation Review will

realise water, energy and

emissions improvements

across wineries and packaging

Responsible consumption

>96%of employees completed

training on TWE’s

alcohol policy

Alcohol education and responsibility

initiatives

First global winemaker to

provide consumers with

access to calorie content

information

Community involvement

Corporate volunteering

Employees

80 Global Charities across

4 regions

Local Procurement

Code supporting

economic growth in

urban/regional

communities

TWE match funds for

employee fundraising

activities

1,300

For

per

sona

l use

onl

y

60

Supply will meet demand sustainably, safely and simply Summary of key takeaways

TWE produces world class wines of quality that delight consumers – and TWE will

continue to have quality at the heart of what is done in every region

Destination Zero Harm, a people-focused, behaviour-led safety culture program is in

place - at TWE we care about safety because everybody’s life is important

Aggressive implementation of initiatives will optimise and streamline the supply chain

cost base to deliver margin accretion and return on capital employed improvement

Strategic capital expenditure will support TWE’s continued investment in

premiumisation and deliver sustainable supply and benefits over the long term

Developing scalability and flexibility is now a key platform for TWE’s supply chain

strategy and execution plan to drive availability to meet future growth ambitions

For

per

sona

l use

onl

y

61

QUESTIONS

For

per

sona

l use

onl

y

62

TWE’s journey from Agri to Brand-ledKey takeaways from today

1

2 Our core asset is our organisational talent

3

4

5 Premiumisation & allocations ensure shareholders earn more than a standard glass return

6 Market share gains and premiumisation will deliver volume and value growth in ANZ

7

9

8 Protecting double digit EBITS margin is Europe’s priority

TWE is on a journey from Agri to Brand-led

We are building brand portfolios; one portfolio at a time. TWE launching French portfolio

Supply will meet demand sustainably, safely and simply

Asia will grow by volume & value and our 30-35% EBITS margin will be preserved

Shifting from Fixing to Growth in the US is in play; EBITS margin to drive Group marginFor

per

sona

l use

onl

y

63

Driving Value Creation and EBITS

Margin accretion; with a bedrock of

strong controls and disciplined capital

structureGunther Burghardt – Chief Financial Officer

For

per

sona

l use

onl

y

64

Driving value creation and EBITS margin accretionTWE’s relentless focus on continuing EBITS margin expansion

TWE is targeting long-term sustainable EBITS margin expansion

Levers to continual EBITS margin expansion include;

Revenue Management

• Re-allocation of Luxury & Masstige fruits and products across geographies, channels and customers

• Advanced pricing and promotional program analytics

• Allocation of fruit to highest margin products

1

2 Balancing our business and value streams to ensure sustainable growth

3 Optimising our capital structure to reduce cost of funds and minimize risk

4 Supply Optimisation

• Run-rate COGS savings of at least $100m from Supply Chain Optimisation initiative by F20

• Run-rate cash synergies recognised from the acquisition of Diageo Wine of US$35m by F20

• Allocation of fruit to highest margin products

5 Leveraging scale and efficiencies / savings to optimise our Cost Of Doing Business

Supported by global systems and enhanced internal controls

For

per

sona

l use

onl

y

65

Driving value creation and EBITS margin accretionTWE’s cycle of optimising value

Long Term Margin Accretion Roadmap

5 year roadmap of brand tiers pricing and margin across

key markets

Long Term Demand

5 year demand planning process allocating products

across retailers and distributors

Allocate Supply to Products

Allocation of owned/leased, grower and bulk wine across

products

Allocation of

products across markets and channels

In market pricing evolution and execution

Long Term Supply

5 year planned allocation of owned/leased, grower and bulk wine across products

5 Year Strategy

For

per

sona

l use

onl

y

66

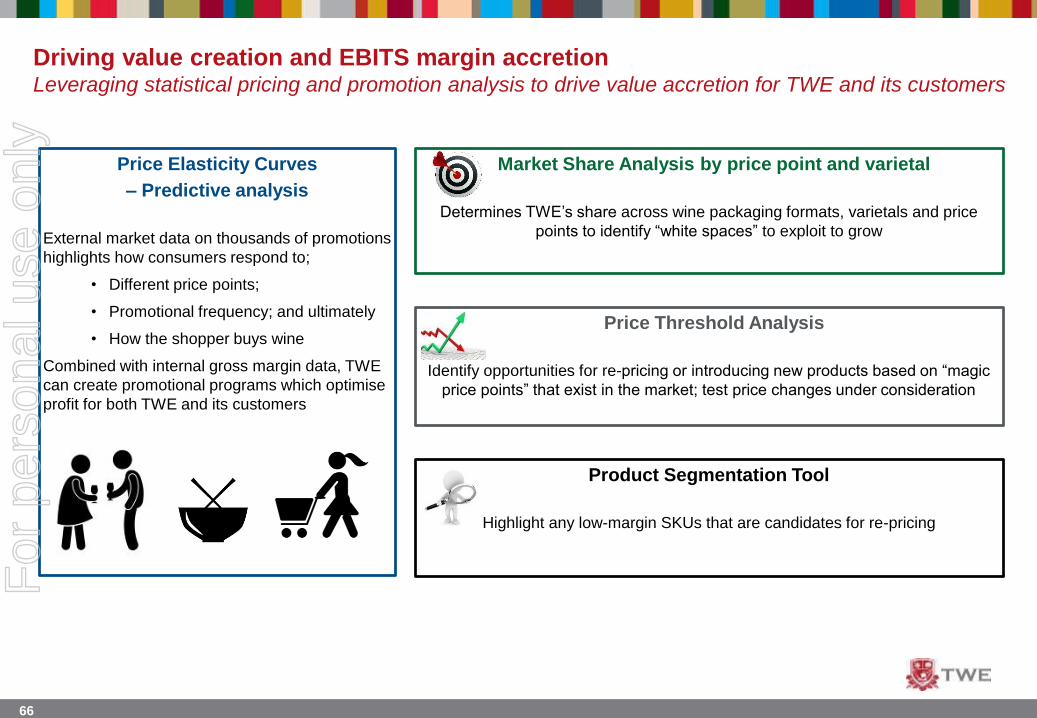

Driving value creation and EBITS margin accretionLeveraging statistical pricing and promotion analysis to drive value accretion for TWE and its customers

Price Elasticity Curves

– Predictive analysis

External market data on thousands of promotions

highlights how consumers respond to;

• Different price points;

• Promotional frequency; and ultimately

• How the shopper buys wine

Combined with internal gross margin data, TWE

can create promotional programs which optimise

profit for both TWE and its customers

Market Share Analysis by price point and varietal

Determines TWE’s share across wine packaging formats, varietals and price

points to identify “white spaces” to exploit to grow

Price Threshold Analysis

Identify opportunities for re-pricing or introducing new products based on “magic

price points” that exist in the market; test price changes under consideration

Product Segmentation Tool

Highlight any low-margin SKUs that are candidates for re-pricing

For

per

sona

l use

onl

y

67

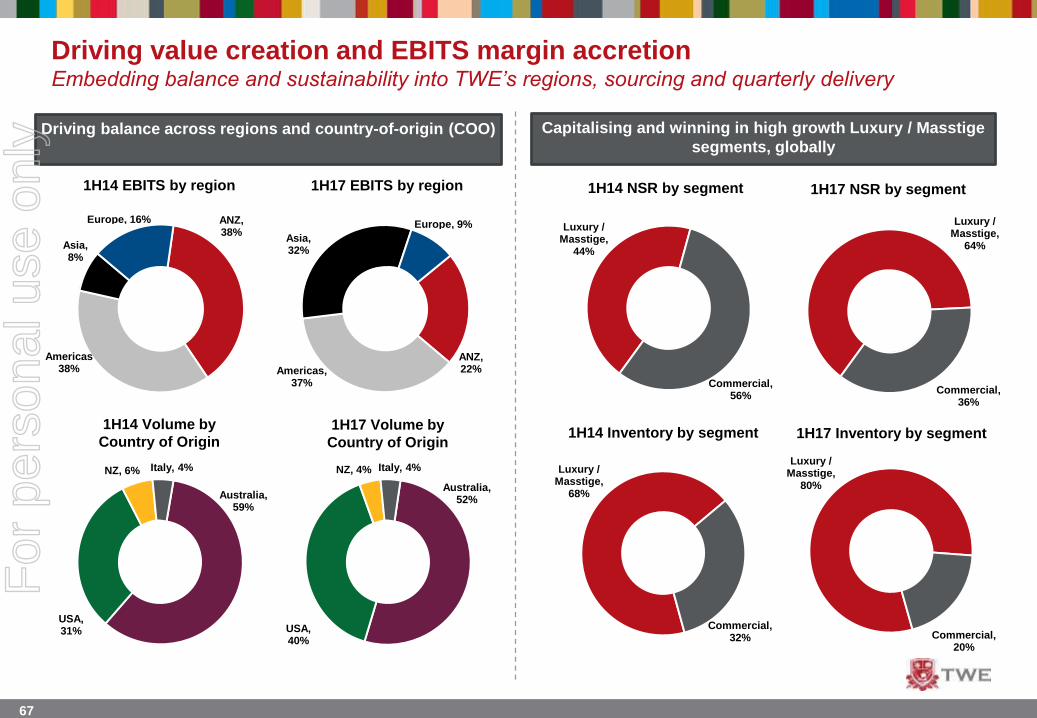

Driving value creation and EBITS margin accretion Embedding balance and sustainability into TWE’s regions, sourcing and quarterly delivery

Driving balance across regions and country-of-origin (COO) Capitalising and winning in high growth Luxury / Masstige

segments, globally

ANZ, 38%

Americas38%

Asia, 8%

Europe, 16%

1H14 EBITS by region 1H17 EBITS by region

ANZ, 22%Americas,

37%

Asia, 32%

Europe, 9%

Australia, 52%

USA, 40%

NZ, 4% Italy, 4%

Australia, 59%

USA, 31%

NZ, 6% Italy, 4%

1H14 Volume by

Country of Origin 1H17 Volume by

Country of Origin

Luxury / Masstige,

44%

Commercial, 56%

1H14 NSR by segment 1H17 NSR by segment

Luxury / Masstige,

64%

Commercial, 36%

1H14 Inventory by segment

Luxury / Masstige,

68%

Commercial, 32%

1H17 Inventory by segment

Luxury / Masstige,

80%

Commercial, 20%

For

per

sona

l use

onl

y

68

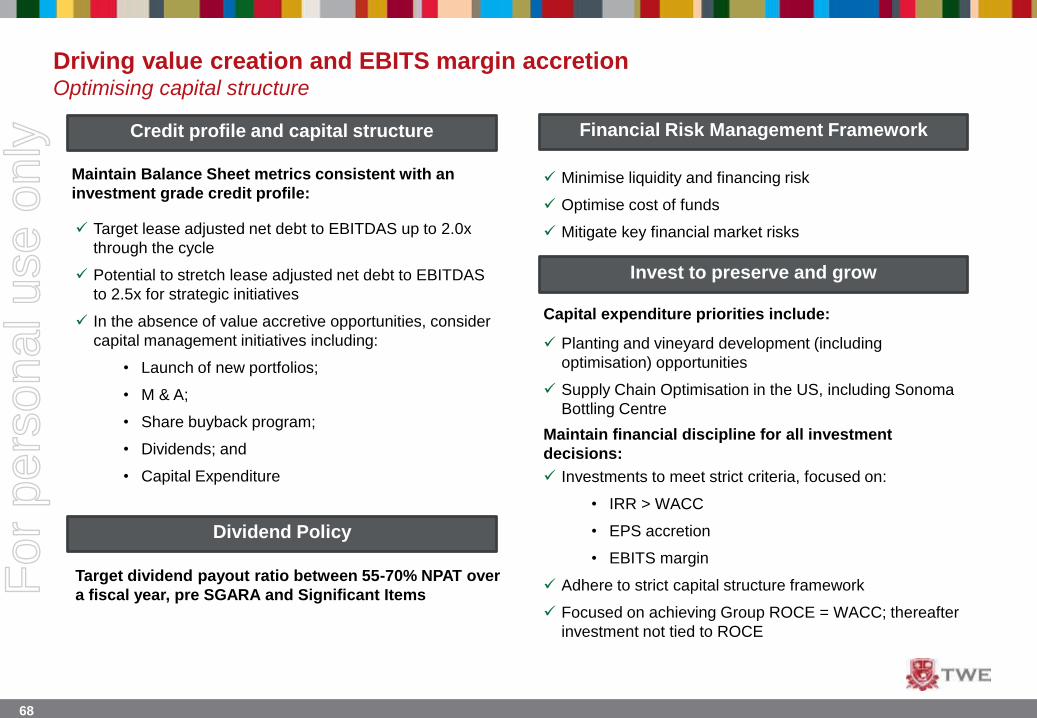

Driving value creation and EBITS margin accretionOptimising capital structure

Credit profile and capital structure Financial Risk Management Framework

Dividend Policy

Invest to preserve and grow

Maintain Balance Sheet metrics consistent with an

investment grade credit profile:

Target lease adjusted net debt to EBITDAS up to 2.0x

through the cycle

Potential to stretch lease adjusted net debt to EBITDAS

to 2.5x for strategic initiatives

In the absence of value accretive opportunities, consider

capital management initiatives including:

• Launch of new portfolios;

• M & A;

• Share buyback program;

• Dividends; and

• Capital Expenditure

Target dividend payout ratio between 55-70% NPAT over

a fiscal year, pre SGARA and Significant Items

Minimise liquidity and financing risk

Optimise cost of funds

Mitigate key financial market risks

Planting and vineyard development (including

optimisation) opportunities

Supply Chain Optimisation in the US, including Sonoma

Bottling Centre

Capital expenditure priorities include:

Maintain financial discipline for all investment

decisions:

Investments to meet strict criteria, focused on:

• IRR > WACC

• EPS accretion

• EBITS margin

Adhere to strict capital structure framework

Focused on achieving Group ROCE = WACC; thereafter

investment not tied to ROCE

For

per

sona

l use

onl

y

69

Driving value creation and EBITS margin accretionTWE’s journey to ROCE > Short term/ Long term WACC

FY 1H FY 1H FY 1H FY 1H FY 1H FY

Short Term WACC Long Term WACC ROCE

Pre Tax Long

Term WACC

Pre Tax Short

Term WACC

ROCE

Balance Sheet strategy to optimise WACC while ensuring efficient access to capital through

the cycle

For

per

sona

l use

onl

y

70

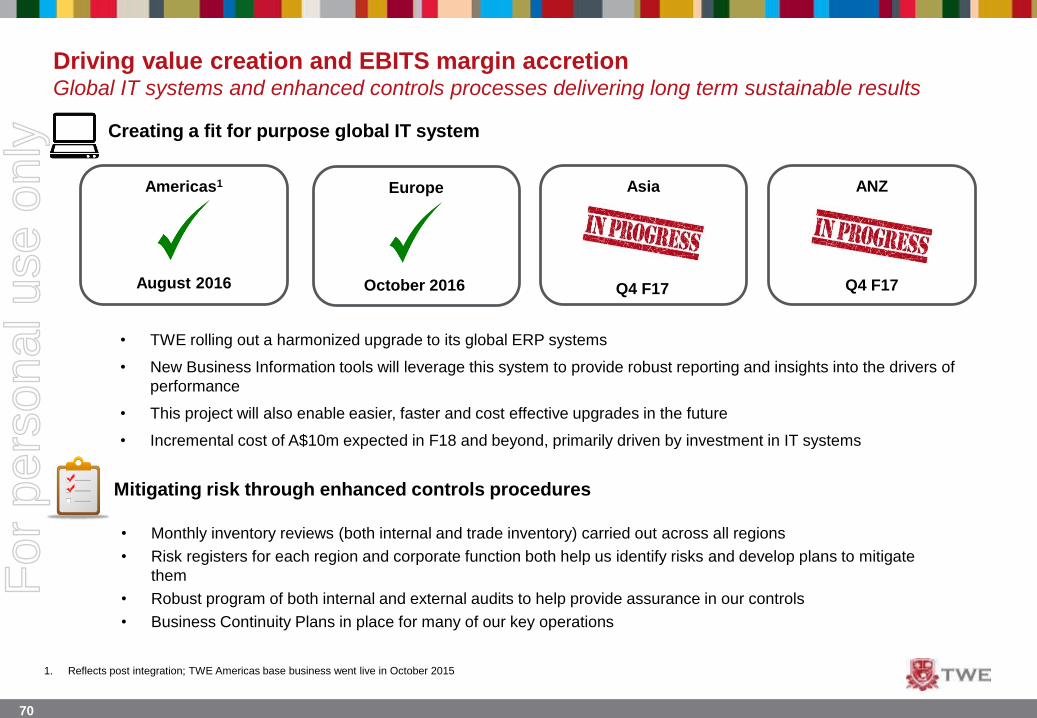

Driving value creation and EBITS margin accretionGlobal IT systems and enhanced controls processes delivering long term sustainable results

Creating a fit for purpose global IT system

Americas1 ANZAsiaEurope

August 2016 October 2016 Q4 F17

• TWE rolling out a harmonized upgrade to its global ERP systems

• New Business Information tools will leverage this system to provide robust reporting and insights into the drivers of

performance

• This project will also enable easier, faster and cost effective upgrades in the future

• Incremental cost of A$10m expected in F18 and beyond, primarily driven by investment in IT systems

Mitigating risk through enhanced controls procedures

• Monthly inventory reviews (both internal and trade inventory) carried out across all regions

• Risk registers for each region and corporate function both help us identify risks and develop plans to mitigate

them

• Robust program of both internal and external audits to help provide assurance in our controls

• Business Continuity Plans in place for many of our key operations

1. Reflects post integration; TWE Americas base business went live in October 2015

Q4 F17

For

per

sona

l use

onl

y

71

SummaryTop 5 takeaways for on how TWE will drive value while managing capital and risk effectively

TWE has a very disciplined approach to managing capital and risk, focused on maintaining

credit metrics that are consistent with an investment grade credit profile

Allocation of fruit and wines in our portfolio to “highest value use” and across geographies,

channels, customers and financial periods to drive substantial value creation for the business

When it comes to acquisitions, TWE is and will be extremely patient and we have a strong

appetite to invest for current and future value growth

We know the “levers” in our business and P&L which will drive sustainable long term EBITS

margins

Advanced pricing and promotional analytics are creating value for TWE and its customers

For

per

sona

l use

onl

y

72

QUESTIONS

For

per

sona

l use

onl

y

73

TWE’s journey from Agri to Brand-ledKey takeaways from today

1

2 Our core asset is our organisational talent

3

4

5 Premiumisation & allocations ensure shareholders earn more than a standard glass return

6 Market share gains and premiumisation will deliver volume and value growth in ANZ

7

9

8 Protecting double digit EBITS margin is Europe’s priority

TWE is on a journey from Agri to Brand-led

We are building brand portfolios; one portfolio at a time. TWE launching French portfolio

Supply will meet demand sustainably, safely and simply

Asia will grow by volume & value and our 30-35% EBITS margin will be preserved

Shifting from Fixing to Growth in the US is in play; EBITS margin to drive Group marginFor

per

sona

l use

onl

y

74

Growing Sustainable Share in a

Mature MarketAngus McPherson – Managing Director, ANZ

For

per

sona

l use

onl

y

75

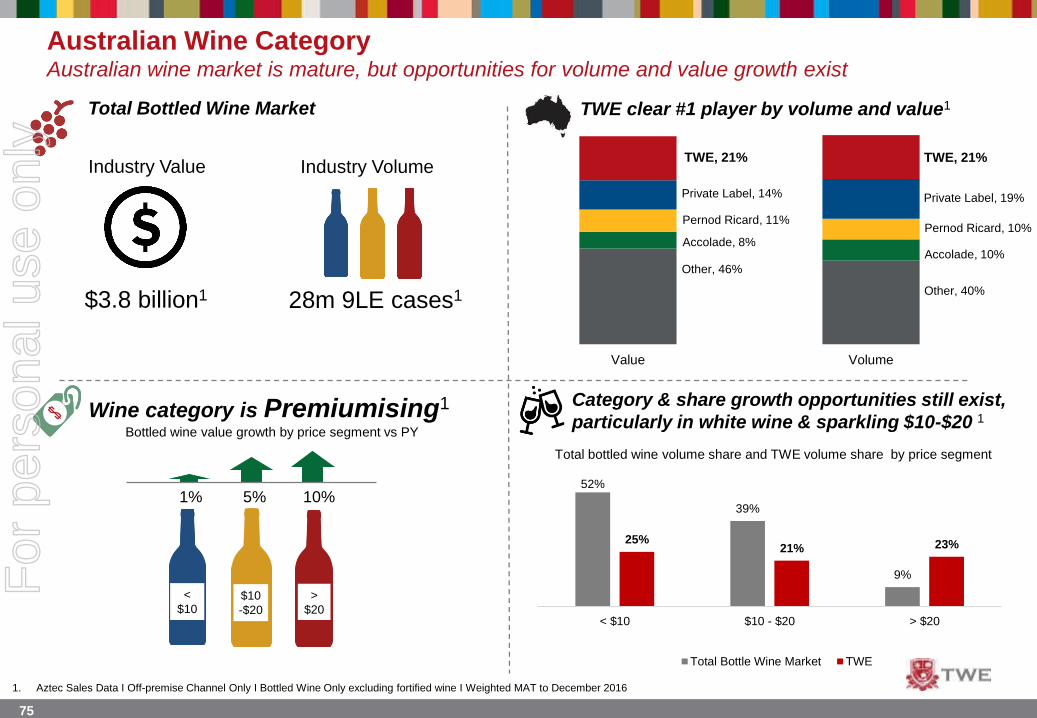

Other, 46%

Other, 40%

Accolade, 8%Accolade, 10%

Pernod Ricard, 11%Pernod Ricard, 10%

Private Label, 14% Private Label, 19%

TWE, 21% TWE, 21%

Value Volume

Australian Wine CategoryAustralian wine market is mature, but opportunities for volume and value growth exist

Total Bottled Wine Market

$3.8 billion1 28m 9LE cases1

Wine category is Premiumising1

<

$10$10

-$20

>

$20

1% 10%5%

TWE clear #1 player by volume and value1

Category & share growth opportunities still exist,

particularly in white wine & sparkling $10-$20 1

52%

39%

9%

25%21% 23%

< $10 $10 - $20 > $20

Total Bottle Wine Market TWE

Industry VolumeIndustry Value

1. Aztec Sales Data I Off-premise Channel Only I Bottled Wine Only excluding fortified wine I Weighted MAT to December 2016

Bottled wine value growth by price segment vs PY

Total bottled wine volume share and TWE volume share by price segment

For

per

sona

l use

onl

y

76

Australian Wine ConsumerAustralians tend to drink Australian wine and relatively frequently

Australia; large wine consuming

population

13.9 MillionAustralians drink wine¹

81%Of the adult population¹

26.82016

65% of wine consumers

drink wine at least

once a week1

2016

Still red and white wine have

greatest share of the category²

40% 22%38%

Australian Country of Origin

dominates the category4

New Zealand - 12%

6% 3YR CAGR

Australian – 83%

(1)% 3YR CAGR

Rest of world – 5%

Value share of bottled wine

26.5 Litres per

capita3

2011

Litres per

capita3

Per capita consumption is relatively high;

increasing population is driving growth

1.Shiraz 2. Champagne

4. Pinot Noir

3. Sauvignon Blanc

Value growth: +21%

Value share: 3%

Value growth: +4%

Value share: 17%

Value growth: +11%

Value share: 6%

Value growth: +10%

Value share: 14%

Value growth: +17%

Value share: 3%

Top 5 varietal contributors to wine

value growth2

1. Wine Intelligence Brand Tracker 2016

2. Aztec Sales Data I Off-premise Channel Only I Bottled Wine Only excluding fortified wine I Weighted MAT to December 2016

3. Euromonitor International 2016, Still Light Grape Wine, Litres per capita at legal purchasing age

4. IWSR 2016

5. Pinot Gris / Grigio

Volume share of bottled wine

For

per

sona

l use

onl

y

77

EDG, 54%

CLG, 25%

Independents, 21%

1.6%

Bricks and Mortar Retail

Channel

60%

E-Commerce

Channel

On premise

Channel

Ch

an

nel

sp

lit

Cu

sto

me

r s

ha

re o

f c

ha

nn

el

Top 10 banners = ~90% of sales

Australian Market Landscape1

Retail wine market continues to consolidate, while the E-commerce channel continues to evolve

26% 11%

Direct-To-Consumer

Channel

3%

Consolidation Highly Fragmented

Top 10 customer

= ~5% of sales

~ 44,000 On-Premise customers

Growth & New Entrants^

EDG = ~50% sales^

EDG

Gray’s

Cellar Doors

TWE = 11 of 1,6002

Cellar Doors

1. Wine Intelligence Brand Tracker 2016, Aztec MAT to January 2017, Company estimates

2. The ANZ Wine Industry Directory, 2016

^ On-line sales overlap with bricks and mortar sales

For

per

sona

l use

onl

y

78

Growing share in a mature marketTargeting 25% volume and value share

25%

Market

Share

21%

Market

Share1

Future StateStrategic Initiatives Current State

Optimising a competitive and

efficient Route-To-Market

Outstanding portfolio and brand

building activity driving category

growth

2Building strategic and sustainable

customer partnerships

1

3

1. Aztec Sales Data I Off-premise Channel Only I Bottled Wine Only excluding fortified wine I Weighted MAT to December 2016

For

per

sona

l use

onl

y

79

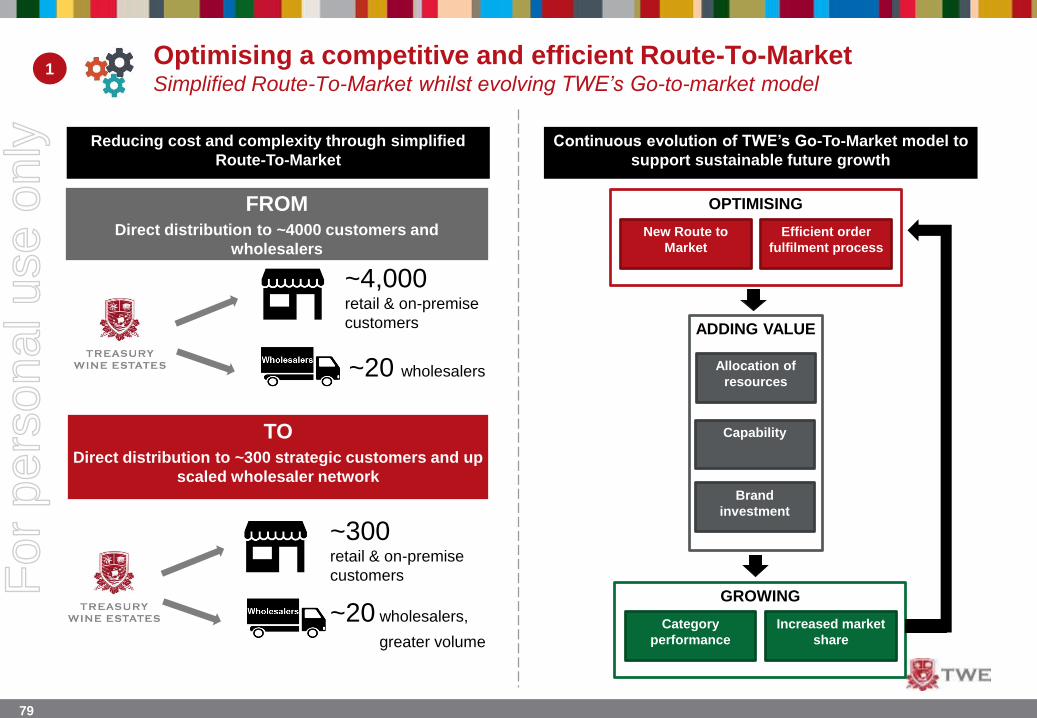

Optimising a competitive and efficient Route-To-MarketSimplified Route-To-Market whilst evolving TWE’s Go-to-market model

Reducing cost and complexity through simplified

Route-To-Market

Continuous evolution of TWE’s Go-To-Market model to

support sustainable future growth

FROMDirect distribution to ~4000 customers and

wholesalers

TODirect distribution to ~300 strategic customers and up

scaled wholesaler network

~4,000 retail & on-premise

customers

~20 wholesalers

~300 retail & on-premise

customers

~20 wholesalers,

greater volume

1

ADDING VALUE

Allocation of

resources

Capability

Brand

investment

OPTIMISING

Efficient order

fulfilment process

New Route to

Market

GROWING

Increased market

share

Category

performance

For

per

sona

l use

onl

y

80

2

Category growth strategy

Joint business planning

Brilliant execution

Joint Value

Creation

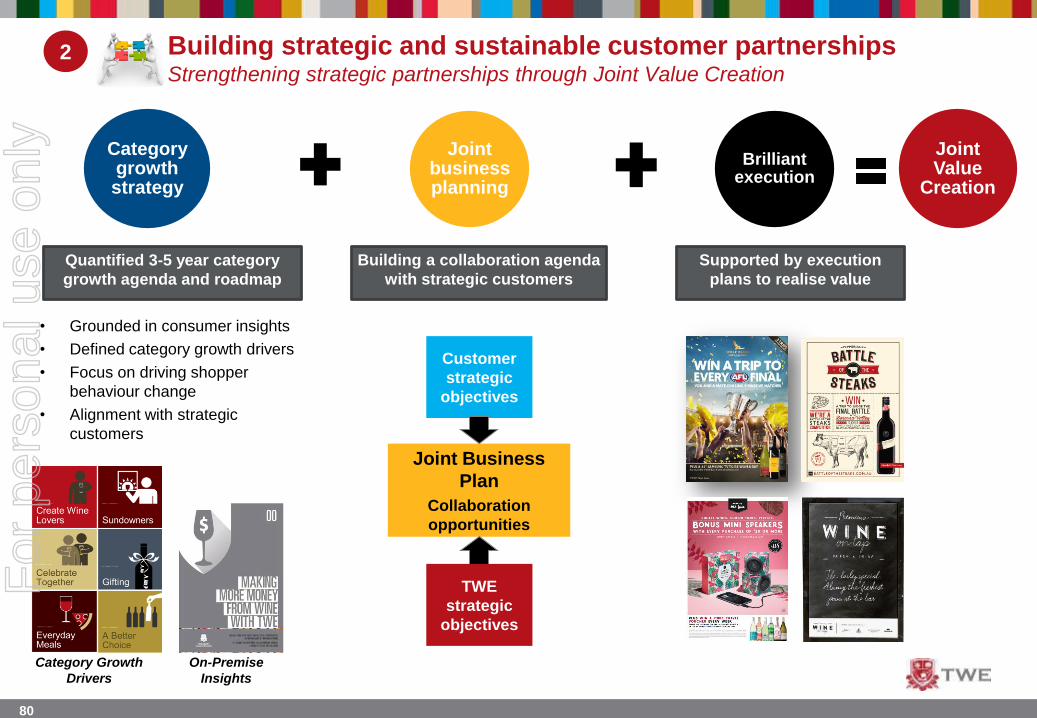

• Grounded in consumer insights

• Defined category growth drivers

• Focus on driving shopper

behaviour change

• Alignment with strategic

customers

Building a collaboration agenda

with strategic customers

Category Growth

Drivers

Building strategic and sustainable customer partnershipsStrengthening strategic partnerships through Joint Value Creation

Customer

strategic

objectives

Joint Business

Plan

Collaboration

opportunities

TWE

strategic

objectives

Supported by execution

plans to realise value

On-Premise

Insights

Quantified 3-5 year category

growth agenda and roadmap

For

per

sona

l use

onl

y

81

3

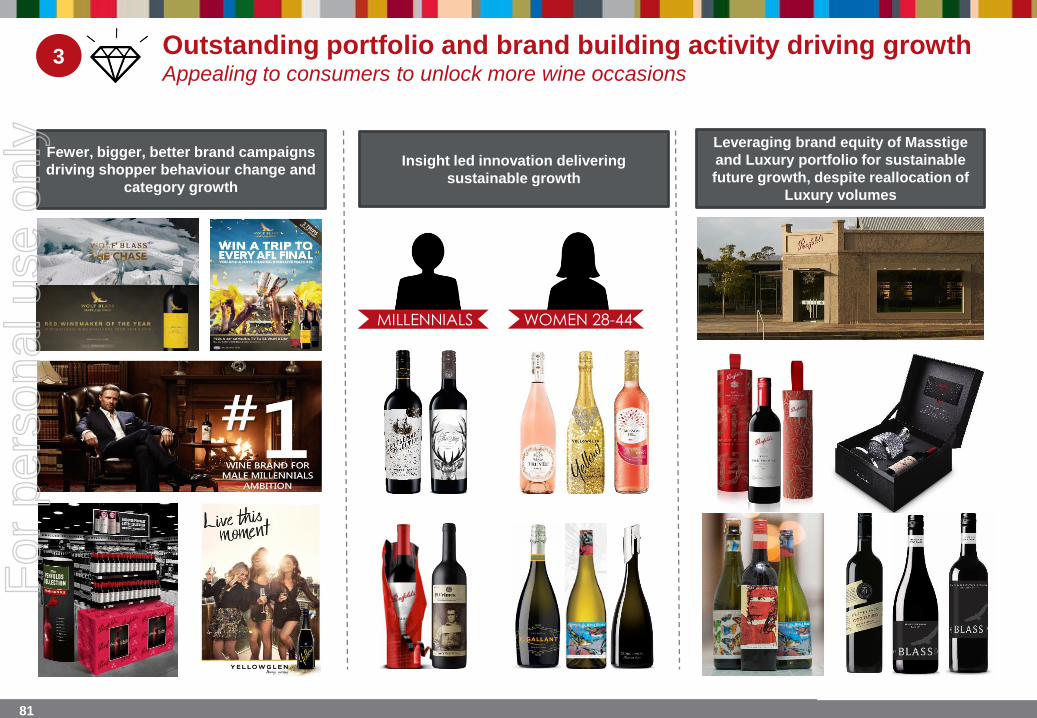

Fewer, bigger, better brand campaigns

driving shopper behaviour change and

category growth

Insight led innovation delivering

sustainable growth

MILLENNIALS WOMEN 28-44

Leveraging brand equity of Masstige

and Luxury portfolio for sustainable

future growth, despite reallocation of

Luxury volumes

Outstanding portfolio and brand building activity driving growthAppealing to consumers to unlock more wine occasions

For

per

sona

l use

onl

y

82

Capitalise on the strength of TWE’s

Regional Gems portfolio, expanding

distribution and availability

Delivering insight-led innovation

within TWE’s Australian Regional

Gems portfolio

Leverage the strength of TWE’s

winemaking and accolades received to

share the Australian Regional Gems

portfolio globally

Capturing the

varietal value

growth of cool

climate Shiraz &

Chardonnay with

the launch of The

Stag by St

Huberts

A new tier of sparkling wines

within T’Gallant aimed at females

and priced within the over-

performing Masstige segment

150 800Trophies Gold Medals

9 Premium Australian Regional

Gems Brands

Outstanding portfolio and brand building activity driving growthScale up treasured Australian Regional Gems portfolio

3F

or p

erso

nal u

se o

nly

83

Extraordinary Stories

for Experienced

Seekers looking for

Authenticity and

Exploration

3Outstanding portfolio and brand building activity driving growthIntroducing - SAMUEL WYNN & CO.

For

per

sona

l use

onl

y

84

Above The Line Support

Digital Support

In Store Retail Activations

Media Partnerships

3Outstanding portfolio and brand building activity driving growthSignificant market support, targeted towards Millennials

For

per

sona

l use

onl

y

85

3 Outstanding portfolio and brand building activity driving growthDrive growth and scale of an iconic Australian wine brand with enviable wine credentials

Icon & Luxury Premium Masstige Still Wine Masstige Sparkling Wine

• Leverage strong quality

credentials of existing Icon

and Luxury range

• Global allocation

• Varietals;

Iconic Show

Sparkling Shiraz

St Peters

Drumborg Single

Vineyard Range

• New tier leveraging

Seppelt winemaking

expertise to recruit new

consumers

• Regionally appellated

• RRP A$25

• Driving breadth and

scale

• Attract new customers

• Large and high growth

segment – accounts for

close to 1/3 of the wine

category1

• Range; Shiraz,

Chardonnay, Pinot Gris

and Rose

• Leveraging Seppelt’s

extensive Sparkling

heritage to launch an

accessible Masstige

proposition

• Focused on high

growth segments

• Range; Sparkling White,

Sparkling Shiraz and

Prosecco

1. Aztec Weighted Scan data MAT January 2017

For

per

sona

l use

onl

y

86

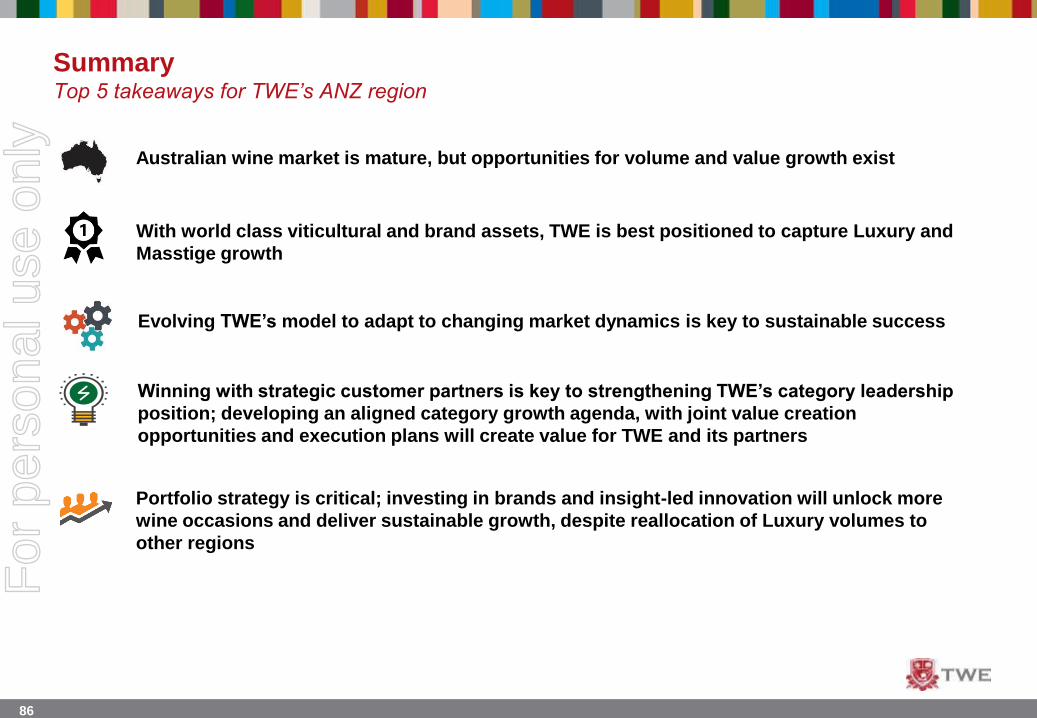

SummaryTop 5 takeaways for TWE’s ANZ region

Australian wine market is mature, but opportunities for volume and value growth exist

With world class viticultural and brand assets, TWE is best positioned to capture Luxury and

Masstige growth

Portfolio strategy is critical; investing in brands and insight-led innovation will unlock more

wine occasions and deliver sustainable growth, despite reallocation of Luxury volumes to

other regions

Winning with strategic customer partners is key to strengthening TWE’s category leadership

position; developing an aligned category growth agenda, with joint value creation

opportunities and execution plans will create value for TWE and its partners

Evolving TWE’s model to adapt to changing market dynamics is key to sustainable success

For

per

sona

l use

onl

y

87

QUESTIONS

For

per

sona

l use

onl

y

88

TWE’s journey from Agri to Brand-ledKey takeaways from today

1

2 Our core asset is our organisational talent

3

4

5 Premiumisation & allocations ensure shareholders earn more than a standard glass return

6 Market share gains and premiumisation will deliver volume and value growth in ANZ

7

9

8 Protecting double digit EBITS margin is Europe’s priority

TWE is on a journey from Agri to Brand-led

We are building brand portfolios; one portfolio at a time. TWE launching French portfolio

Supply will meet demand sustainably, safely and simply

Asia will grow by volume & value and our 30-35% EBITS margin will be preserved

Shifting from Fixing to Growth in the US is in play; EBITS margin to drive Group marginFor

per

sona

l use

onl

y

89

#1 Imported Wine Business in Asia by

Volume & Value; Preserving 30-35%

EBITS MarginRobert Foye – President & MD, Asia & Europe

For

per

sona

l use

onl

y

90

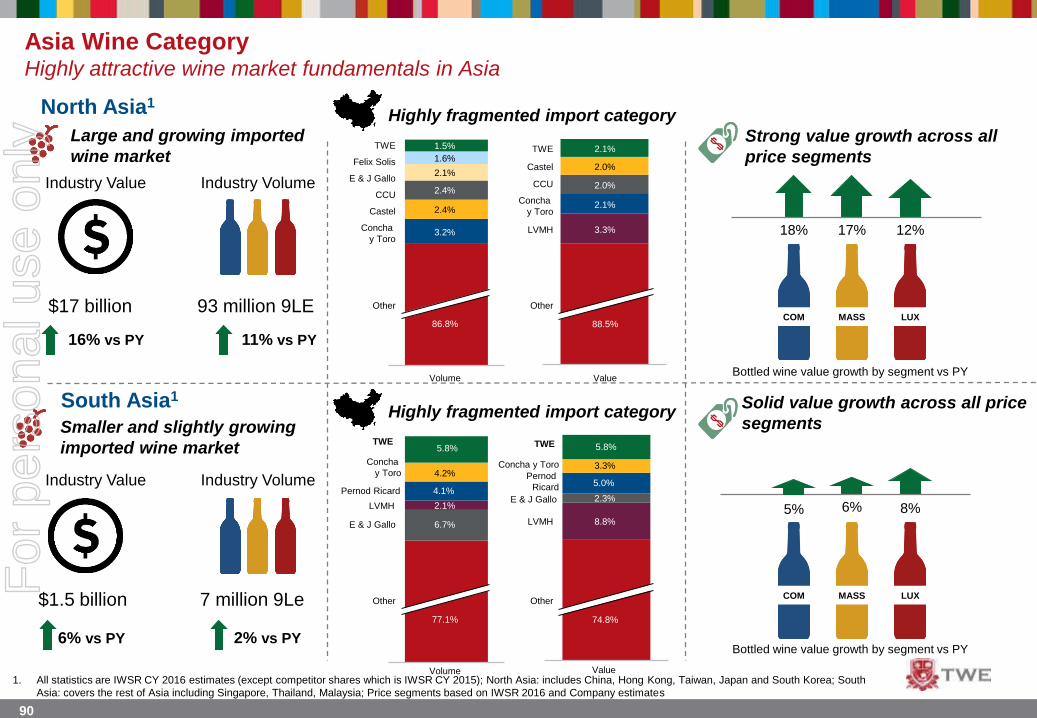

Asia Wine CategoryHighly attractive wine market fundamentals in Asia

1. All statistics are IWSR CY 2016 estimates (except competitor shares which is IWSR CY 2015); North Asia: includes China, Hong Kong, Taiwan, Japan and South Korea; South

Asia: covers the rest of Asia including Singapore, Thailand, Malaysia; Price segments based on IWSR 2016 and Company estimates

North Asia1

South Asia1

Large and growing imported

wine market

Smaller and slightly growing

imported wine market

$17 billion

16% vs PY

Industry Value

$1.5 billion

6% vs PY

Industry Volume

11% vs PY

7 million 9Le

2% vs PY

Highly fragmented import category

Strong value growth across all

price segments

COM MASS LUX

18% 12%17%

5% 8%6%

93 million 9LE

Highly fragmented import categorySolid value growth across all price

segments

3.2%Concha

y Toro

2.4%

1.5%

Volume

CCU

TWE

2.1%

Other

1.6%

86.8%

Felix Solis

E & J Gallo

Castel 2.4%

2.0%CCU

Other

2.1%

2.1%

Concha

y Toro

LVMH

Castel

88.5%

2.0%

3.3%

TWE

Value

2.1%LVMH

Concha

y Toro 4.2%

E & J Gallo

77.1%

6.7%

5.8%

Volume

Other

4.1%

TWE

Pernod Ricard

Value

Other

LVMH

2.3%E & J Gallo

Pernod

Ricard

74.8%

TWE

Concha y Toro

5.0%

5.8%

3.3%

8.8%

Bottled wine value growth by segment vs PY

Industry Value Industry Volume

COM MASS LUX

Bottled wine value growth by segment vs PY

For

per

sona

l use

onl

y

91

Asian Wine Consumer Growing per capita consumption in large alcohol consuming regions; North Asia is key

North Asia

South Asia

97Million

Wine drinkers1

Per capita consumption2

Illustrated using ChinaDemographics

2.1litres per

capita

Consumption by type1

Claimed consumer consumption

Consumption by COO3

Volume share of bottled wine

30% 13%57%

Demographics Per capita consumption2

Illustrated using Singapore

14Million

Wine drinkers1

2.4litres per

capitaSouth Asia includes a

number of non-alcohol

consuming ethnicities

30% 8%62%

French - 35%

Chilean - 17%

Spanish - 14%

Italian - 10%

Australian - 12%

Australian - 24%

Chilean - 17%

French - 18%

Italian - 10%

US - 12%

1.6litres per

capita

2.0litres per

capita

2011 2016

2011 2016

1. Wine Intelligence Brand Tracker 2016, Company Estimates

2. Euromonitor International 2015, Still light grape wine, litres per capita at legal purchasing age

3. IWSR 2016. COO: Country of Origin

Consumption by COO3

Volume share of total bottled wine market

Consumption by type1

Claimed consumer consumption

For

per

sona

l use

onl

y

92

Asian Wine Market Traditional retail format remains dominant channel; on-premise continues to be important

North Asia – Illustrated using China

South Asia – Illustrated using Singapore

Wine industry sales by channel1

Wine industry sales by channel1

~50%Bricks & Mortar Retail

~30%On-premise

~10%E - Commerce

~10%Direct to

Consumer

~65%Bricks & Mortar Retail

~30%On-premise

~5%E - Commerce

>1%Direct to

Consumer

1. IWSR 2015; Global U&A (TLE 2016); Company estimates

For

per

sona

l use

onl

y

93

Key Focus Markets

1. IWSR 2016; Company Estimates

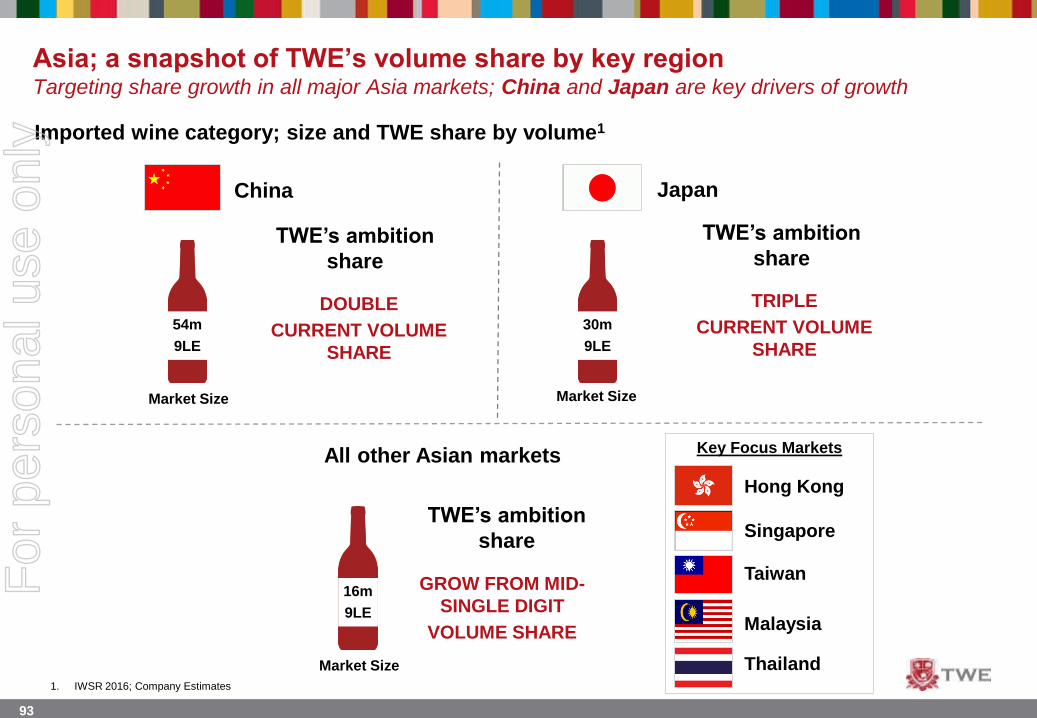

Asia; a snapshot of TWE’s volume share by key regionTargeting share growth in all major Asia markets; China and Japan are key drivers of growth

China

Market Size

54m

9LE

1.6% 3%

TWE’s ambition

share

Japan

Market Size

30m

9LE

0.4% 3%

Market Size

16m

9LE

5% 6%Taiwan

Singapore

Hong Kong

Thailand

Malaysia

All other Asian markets

Imported wine category; size and TWE share by volume1

DOUBLE

CURRENT VOLUME

SHARE

TWE’s ambition

share

TRIPLE

CURRENT VOLUME

SHARE

TWE’s ambition

share

GROW FROM MID-

SINGLE DIGIT

VOLUME SHARE

For

per

sona

l use

onl

y

94

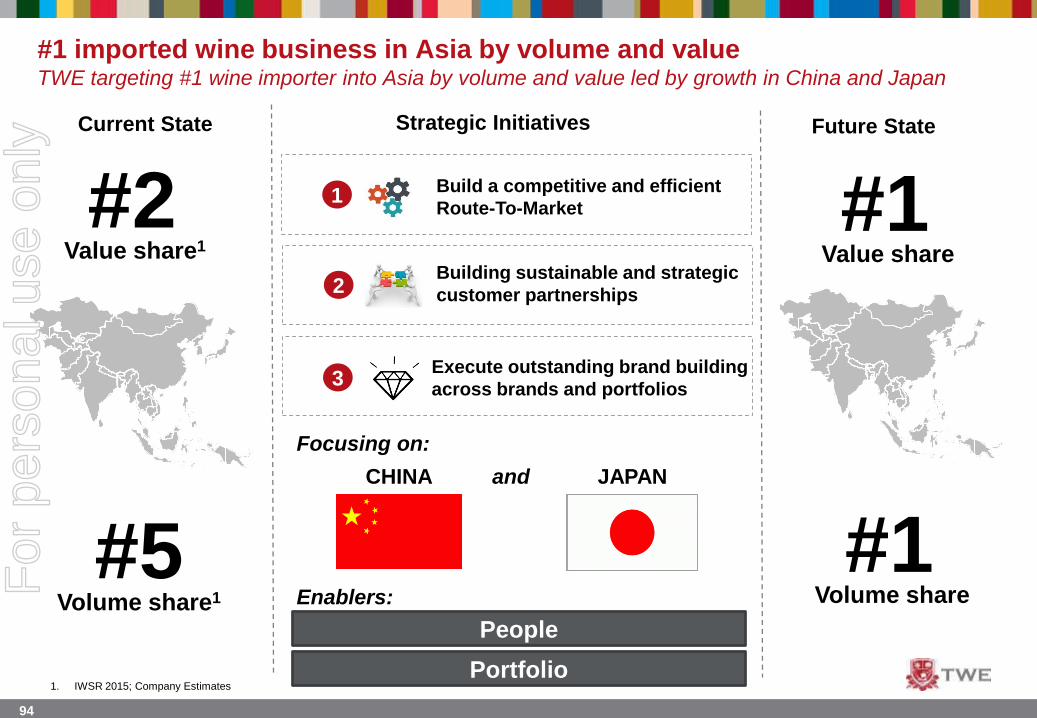

#1 imported wine business in Asia by volume and valueTWE targeting #1 wine importer into Asia by volume and value led by growth in China and Japan

Current State Future StateStrategic Initiatives

#22

Building sustainable and strategic

customer partnerships

1Build a competitive and efficient

Route-To-Market

Value share1

#5Volume share1

#1Value share

#1Volume share

3Execute outstanding brand building

across brands and portfolios

Focusing on:

Enablers:

People

Portfolio

CHINA and JAPAN

1. IWSR 2015; Company Estimates

For

per

sona

l use

onl

y

95

Leverage distribution

infrastructure to diversify brand

portfolio

Expand into strategically

important cities to drive sustainable

growth and deeper partnerships

Establish relationships with a growing customer

base

1Build a competitive and efficient Route-To-Market in ChinaTWE’s “concentric-circle” approach to expansion in China

Concentric circle model driving volume growth TWE’s current and future distribution footprint

TWE’s current geographic footprint

TWE’s targeted geographic footprint

High

Med

Low

Distribution coverage

Tier 1 and 2 Cities

100

Tier 1,2 and 3 Cities

150

The goal is to be as close to customers and consumers as possible

For

per

sona

l use

onl

y

96

1 Build a competitive and efficient Route-To-Market in ChinaGrowing TWE’s distribution footprint across Retail, E-Commerce and On-premise

Bricks and Mortar Retail

Channel

80%F16 NSR Contribution

E-Commerce

Channel

On premise

Channel

10%F16 NSR Contribution

10%F16 NSR Contribution

Ch

an

nel

sp

lit

RMB 120Average price per bottle

Cu

sto

me

rs

600

Number of Strategic & Retail

account customers

F14

50,000+F16

Servicing # indirect accounts

15F14

30F16 1

Number of E-Commerce customers

F14

7

F16

2 Exclusive On-premise distributors

Servicing:

1,600F14

1,600F16

Accounts Accounts

RMB 180Average price per bottle

Number of direct customers

RMB < 100Average price per bottle

For

per

sona

l use

onl

y

97

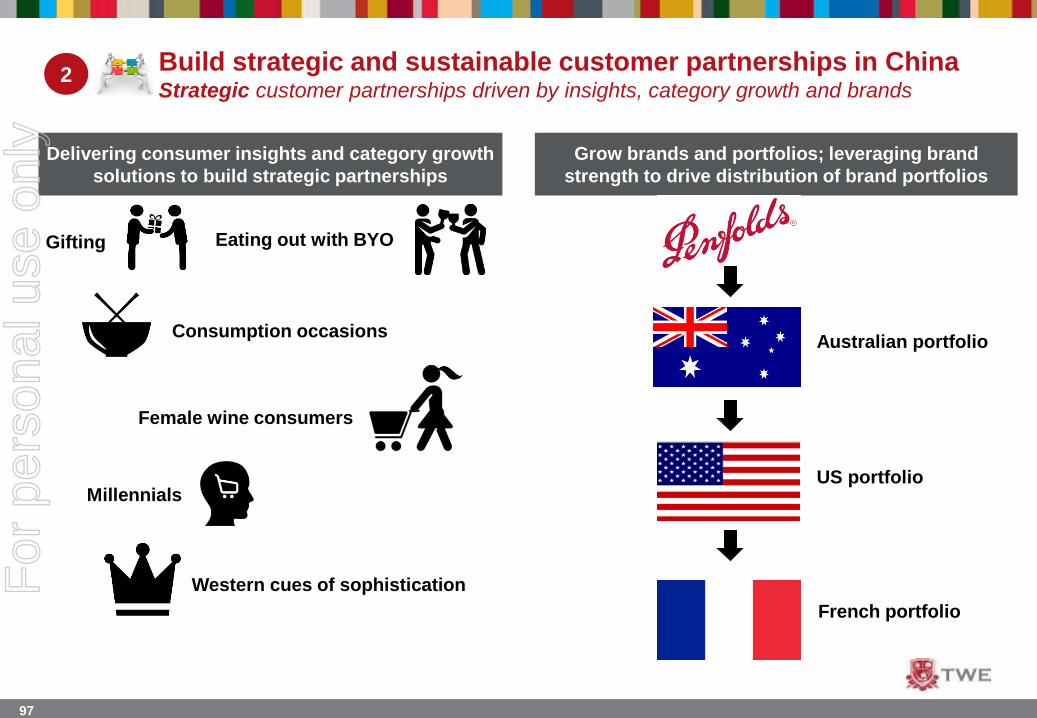

2Build strategic and sustainable customer partnerships in ChinaStrategic customer partnerships driven by insights, category growth and brands

Grow brands and portfolios; leveraging brand

strength to drive distribution of brand portfolios

Delivering consumer insights and category growth

solutions to build strategic partnerships

Gifting

Consumption occasions

Eating out with BYO

Female wine consumers

Millennials

Western cues of sophistication

Australian portfolio

US portfolio

French portfolio

For

per

sona

l use

onl

y

98

TWE

Importers

Wholesalers & retailers

Retailers, on-premisevenues & High Net Wealth

Individuals

Consumers

100%

90% - 100%

>70%

TWE field sales

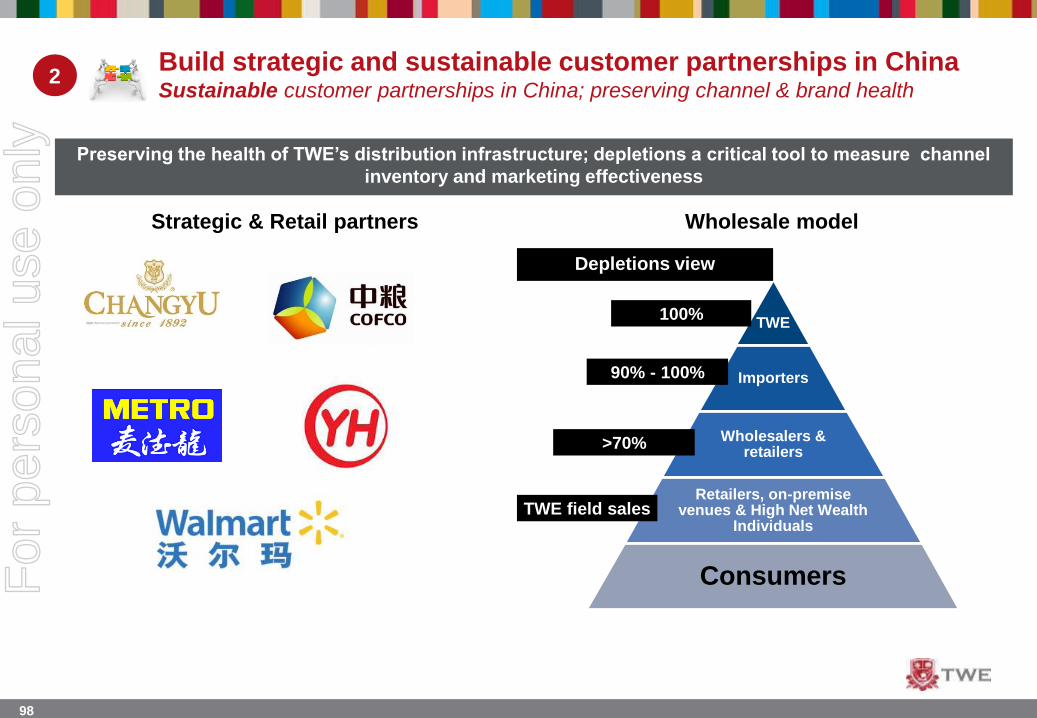

2Build strategic and sustainable customer partnerships in ChinaSustainable customer partnerships in China; preserving channel & brand health

Preserving the health of TWE’s distribution infrastructure; depletions a critical tool to measure channel

inventory and marketing effectiveness

Depletions view

Wholesale modelStrategic & Retail partners

For

per

sona

l use

onl

y

99

3Execute outstanding brand building across the portfolio in ChinaOutstanding brand building execution; winning with customers and consumers

1.6%

45m

9LE

Disruptive and engaging in-store

retail activations Education and training through

outstanding experiences

Localised key visuals which resonate

with the Chinese consumer

Simple, clear and engaging displaysCustomer education & training sessions

Exclusive consumer events with TWE

Brand Ambassadors and Winemakers

Tailored marketing & innovation to

connect with local consumers

Strategic product positioning in-store

Innovation centred around local

consumer occasions

** Penfolds allocation in F18 will be in line with F17 with adverse mix. V16 to fuel growth in F19 and beyond

For

per

sona

l use

onl

y

100

3Execute outstanding brand-building across the portfolio in ChinaOutstanding brand building execution; supporting the US brand portfolio

Educating customers and consumers on

Napa, leveraging 90+ Points platform

Interaction and engagement with TWE

Brand Ambassadors and US winemakersFirst 90+ points store in China

Disruptive and engaging in-store

retail activations Education and training through

outstanding experiences

Tailored marketing & innovation to

connect with local consumers

Celebrity key opinion leaders to

accelerate awareness and consideration

Embracing digital marketing to interact

with consumers

Simple, clear and engaging displays

** Elevated A&P investment in TWE’s US brand portfolio in 2H17 & F18 is supporting sustainable growth

For

per

sona

l use

onl

y

101

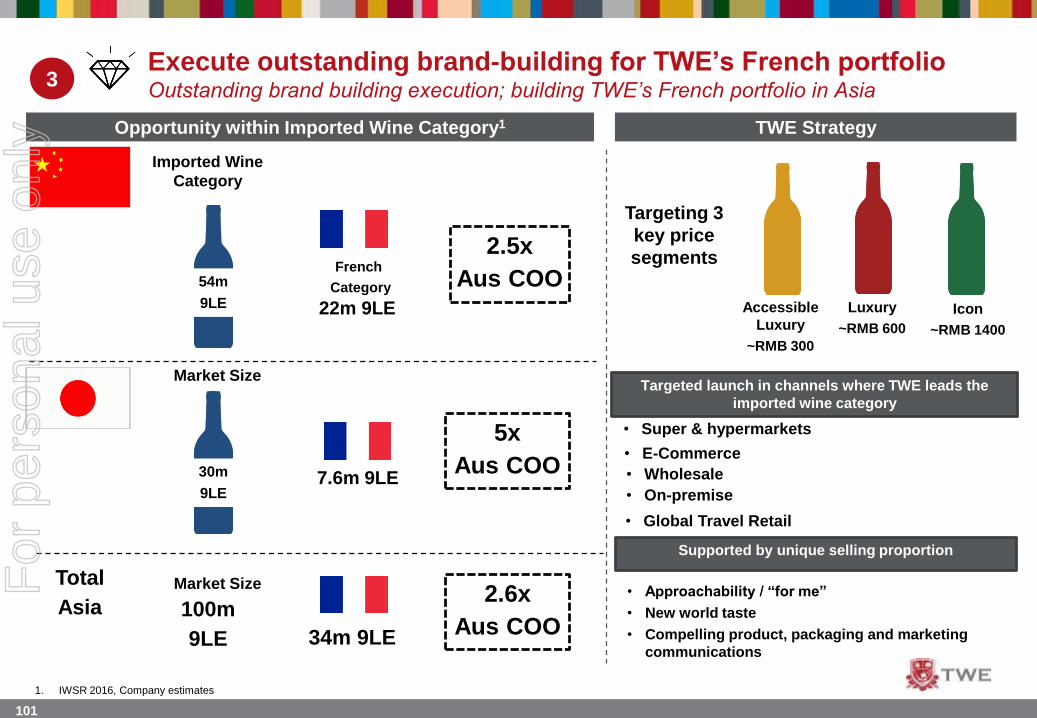

3Execute outstanding brand-building for TWE’s French portfolioOutstanding brand building execution; building TWE’s French portfolio in Asia

Opportunity within Imported Wine Category1

54m

9LE

Market Size

Imported Wine

Category

French

Category

22m 9LE

2.5x

Aus COO

30m

9LE

Market Size

7.6m 9LE

5x

Aus COO

Total

Asia 100m

9LE 34m 9LE

TWE Strategy

Targeting 3

key price

segments

Accessible

Luxury

~RMB 300

Luxury

~RMB 600

Icon

~RMB 1400

Targeted launch in channels where TWE leads the

imported wine category

Supported by unique selling proportion

• Super & hypermarkets

• E-Commerce

• On-premise

• Wholesale

• Global Travel Retail

• Approachability / “for me”

• New world taste

• Compelling product, packaging and marketing

communications

1. IWSR 2016, Company estimates

2.6x

Aus COO

For

per

sona

l use

onl

y

102

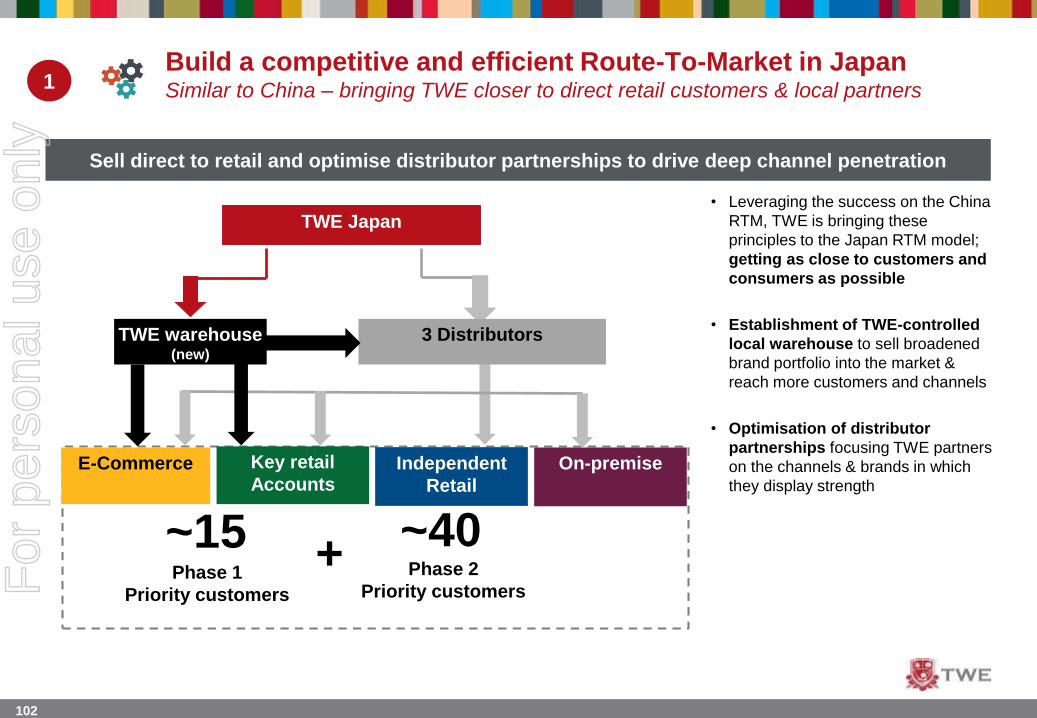

1Build a competitive and efficient Route-To-Market in JapanSimilar to China – bringing TWE closer to direct retail customers & local partners

Sell direct to retail and optimise distributor partnerships to drive deep channel penetration

Phase 1

Priority customers

~15 ~40Phase 2

Priority customers

+

• New Route-To-Market;

establishment of direct model

with key account salesforce

• Build TWE Japan

warehouse model to sell

direct to retail and wholesale

network

• Leveraging the success on the China

RTM, TWE is bringing these

principles to the Japan RTM model;

getting as close to customers and

consumers as possible

• Establishment of TWE-controlled

local warehouse to sell broadened

brand portfolio into the market &

reach more customers and channels

• Optimisation of distributor

partnerships focusing TWE partners

on the channels & brands in which

they display strength

TWE Japan

TWE warehouse(new)

3 Distributors

E-Commerce Key retail

AccountsIndependent

Retail

On-premise

For

per

sona

l use

onl

y

103

2Build strategic and sustainable customer partnerships in JapanStrategic customer partnerships supported by insights and portfolio breadth

Diversify brand portfolio in Japan to deliver growth

for TWE and its customers

MARKETING FOCUSED MORE ON BRANDS

RATHER THAN COUNTRIES OF ORIGIN

Delivering consumer insights to build strategic

partnerships – 4 common category growth insights

Relax & Unwind

Wine Lovers

GiftingMeals

For

per

sona

l use

onl

y

104

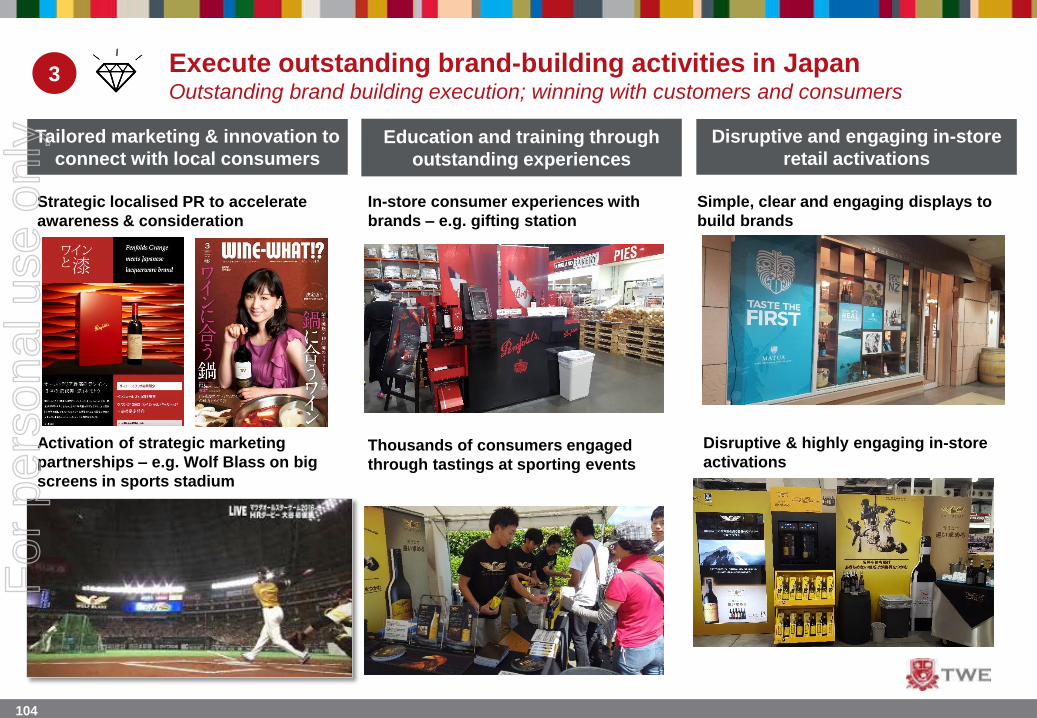

3 Execute outstanding brand-building activities in JapanOutstanding brand building execution; winning with customers and consumers

Disruptive and engaging in-store

retail activations Education and training through

outstanding experiences

Tailored marketing & innovation to

connect with local consumers

Activation of strategic marketing

partnerships – e.g. Wolf Blass on big

screens in sports stadium

Disruptive & highly engaging in-store

activations

Simple, clear and engaging displays to

build brands

In-store consumer experiences with

brands – e.g. gifting station

Thousands of consumers engaged

through tastings at sporting events

Strategic localised PR to accelerate

awareness & consideration

For

per

sona

l use

onl

y

105

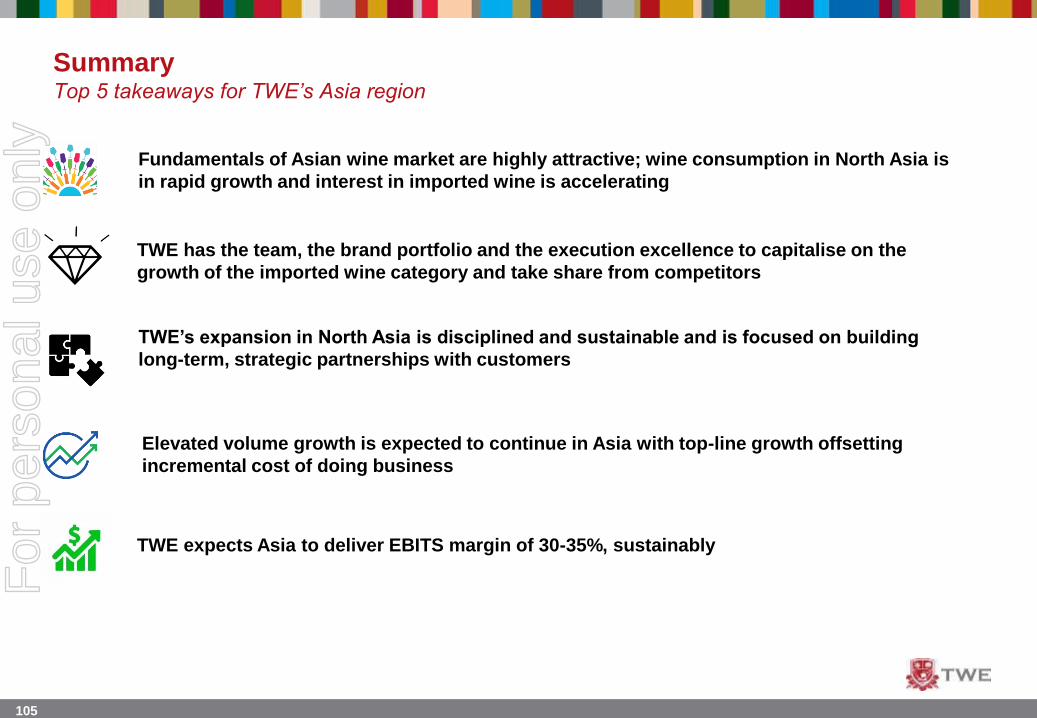

Fundamentals of Asian wine market are highly attractive; wine consumption in North Asia is

in rapid growth and interest in imported wine is accelerating

TWE has the team, the brand portfolio and the execution excellence to capitalise on the

growth of the imported wine category and take share from competitors

SummaryTop 5 takeaways for TWE’s Asia region

TWE expects Asia to deliver EBITS margin of 30-35%, sustainably

TWE’s expansion in North Asia is disciplined and sustainable and is focused on building

long-term, strategic partnerships with customers

Elevated volume growth is expected to continue in Asia with top-line growth offsetting

incremental cost of doing business

For

per

sona

l use

onl

y

106

QUESTIONS

For

per

sona

l use

onl

y

107

TWE’s journey from Agri to Brand-ledKey takeaways from today

1

2 Our core asset is our organisational talent

3

4

5 Premiumisation & allocations ensure shareholders earn more than a standard glass return

6 Market share gains and premiumisation will deliver volume and value growth in ANZ

7

9

8 Protecting double digit EBITS margin is Europe’s priority

TWE is on a journey from Agri to Brand-led

We are building brand portfolios; one portfolio at a time. TWE launching French portfolio

Supply will meet demand sustainably, safely and simply

Asia will grow by volume & value and our 30-35% EBITS margin will be preserved

Shifting from Fixing to Growth in the US is in play; EBITS margin to drive Group marginFor

per

sona

l use

onl

y

108

An Optimised Business Delivering

Double Digit EBITS MarginRobert Foye – President & MD, Asia & Europe

For

per

sona

l use

onl

y

109

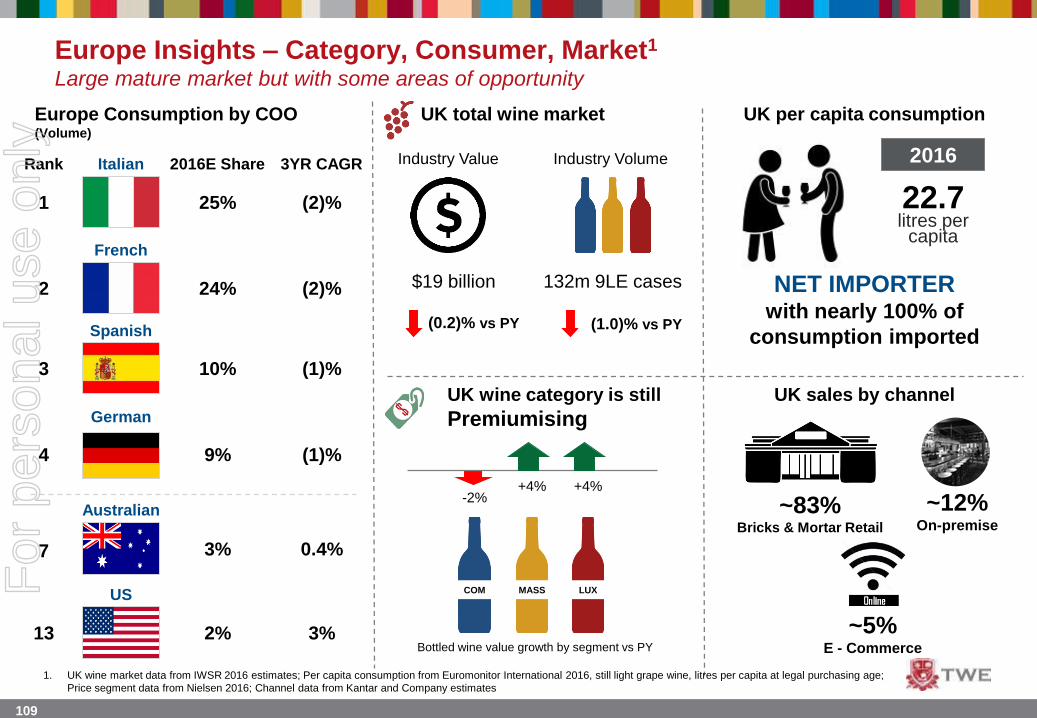

Europe Insights – Category, Consumer, Market1

Large mature market but with some areas of opportunity

UK total wine market

$19 billion

(0.2)% vs PY

Industry Value Industry Volume

132m 9LE cases

(1.0)% vs PY

UK wine category is still

Premiumising

-2%+4%+4%

UK per capita consumption

22.7litres per

capita

UK sales by channel

NET IMPORTERwith nearly 100% of

consumption imported

~83%Bricks & Mortar Retail

~12%On-premise

~5%E - Commerce

1. UK wine market data from IWSR 2016 estimates; Per capita consumption from Euromonitor International 2016, still light grape wine, litres per capita at legal purchasing age;

Price segment data from Nielsen 2016; Channel data from Kantar and Company estimates

Europe Consumption by COO (Volume)

0.4%3%

Australian