full year 2015 results presentation - ugl cms … 24 august 2015 full year 2015 results presentation...

TRANSCRIPT

Monday, 24 August 2015

Full Year 2015 Results Presentation

2

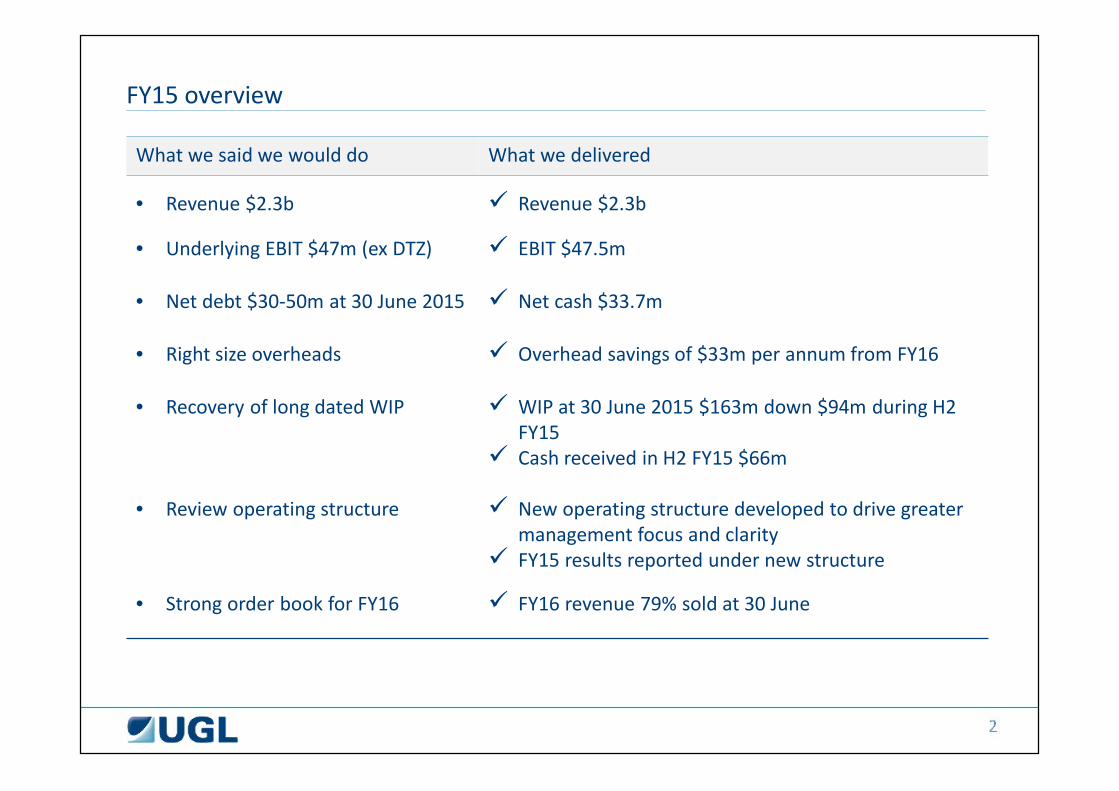

FY15 overview

What we said we would do What we delivered

• Revenue $2.3b Revenue $2.3b

• Underlying EBIT $47m (ex DTZ) EBIT $47.5m

• Net debt $30-50m at 30 June 2015 Net cash $33.7m

• Right size overheads Overhead savings of $33m per annum from FY16

• Recovery of long dated WIP WIP at 30 June 2015 $163m down $94m during H2FY15

Cash received in H2 FY15 $66m

• Review operating structure New operating structure developed to drive greatermanagement focus and clarity

FY15 results reported under new structure

• Strong order book for FY16 FY16 revenue 79% sold at 30 June

.

3

Safety – 12 month rolling

Update on Ichthys CCPP and SMP ProjectsRoss Taylor

5

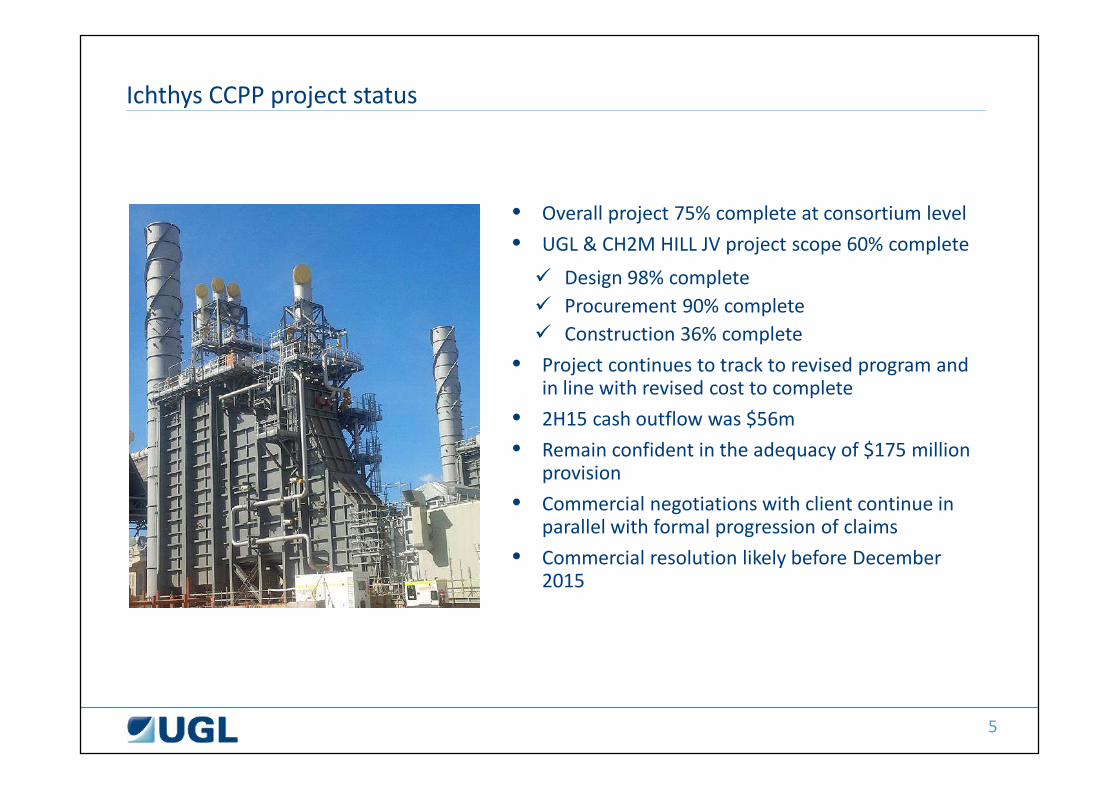

Ichthys CCPP project status

• Overall project 75% complete at consortium level• UGL & CH2M HILL JV project scope 60% complete Design 98% complete Procurement 90% complete Construction 36% complete

• Project continues to track to revised program andin line with revised cost to complete

• 2H15 cash outflow was $56m• Remain confident in the adequacy of $175 million

provision• Commercial negotiations with client continue in

parallel with formal progression of claims• Commercial resolution likely before December

2015

6

Ichthys SMP project status

• Construction 18% complete• No margin will be recognised until project is 30%

complete in accordance with JV revenuerecognition policy – expected to occur aroundDecember 2015

• Site productivity tracking in line with targets• Slippage in early milestones due to delays in site

access and client procurement• EOT claim submitted with indication by client they

will pursue a process to resolve the EOT andmitigate current schedule slippage

• Continue to submit claims and variations inaccordance with contract terms

• Commercial resolution likely before December2015

FY2015 ResultsRoss Taylor

8

Underlying ResultsResults overview

$m FY15 FY14 ChangeOperating revenue 3,048.6 4,511.5 (32%)EBIT 75.3 185.8 (59%)EBIT margin 2.5% 4.1%Interest (25.5) (37.4) 32%Tax (15.5) (30.2) 49%Minority interest (4.0) (6.4) 37%NPAT 30.3 111.7 (73%)NPAT margin 1.0% 2.5%EPS 18.2 67.1 (73%)

9

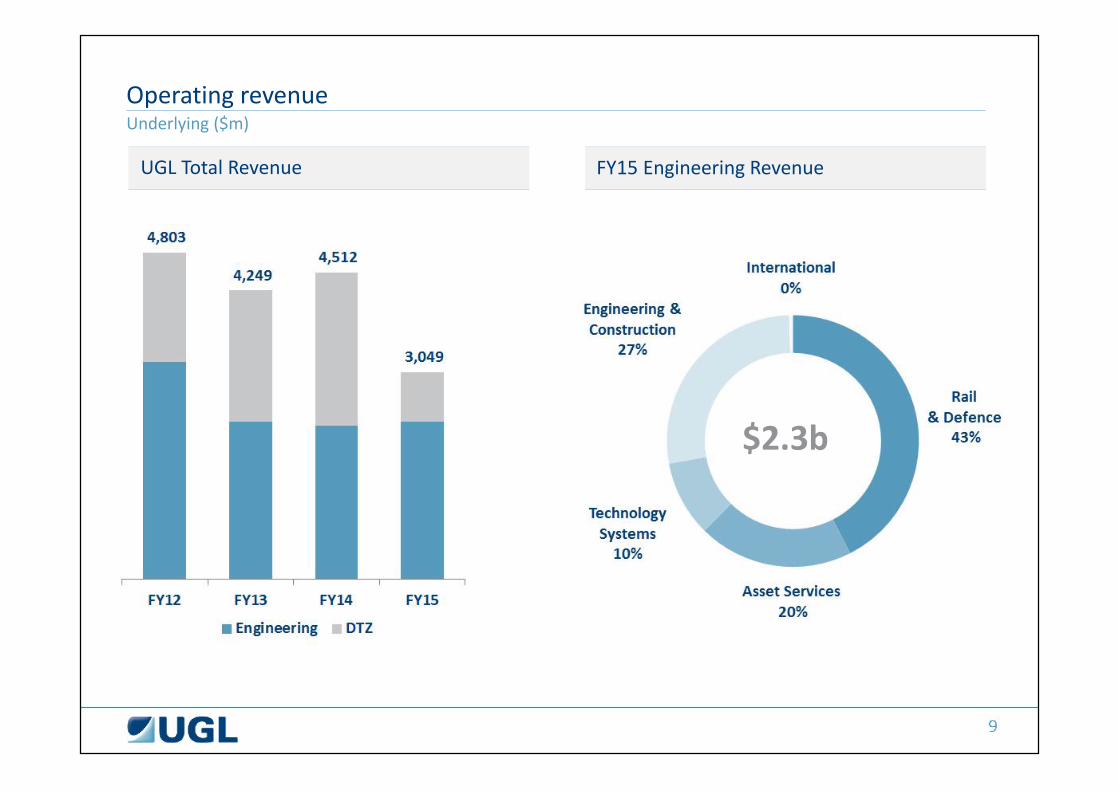

Underlying ($m)Operating revenue

UGL Total Revenue FY15 Engineering Revenue

$2.3b

10

Results excluding DTZNew UGL (Underlying)

Using the previous corporate cost overhead model

($m) FY15 FY14 ChangeRevenue 2,320.5 2,261.7 3%Engineering Operating Profit 69.5 84.1 (17%)Corporate Costs (22.0) (22.2) 0%EBIT 47.5 61.9 (23%)EBIT % 2.0% 2.7% (25%)

11

Normalising overhead historically to align with future reporting

DivisionalOverhead

GroupOverhead

DivisionalOverhead

Historical New

GroupOverhead

EngineeringGroup

Overhead

Varies bydivision

~$40m or1.7% of revenue

~$33m perannum saving

12

Results excluding DTZNew UGL (Underlying)

Engineering earnings based on new overhead model• Corporate costs 1.7% of revenue• Reflects combined group and engineering overheads with increased cost

accountability at the divisional level

($m) FY15 FY14 ChangeRevenue 2,320.5 2,261.7 3%Engineering Operating Profit 87.4 100.8 (13%)Corporate Costs (at 1.7%) (39.9) (38.9) 3%EBIT 47.5 61.9 (23%)EBIT % 2.0% 2.7% (25%)

13

Reporting under our new operating structure

Engineering& Construction

Div

isio

nsAsset Services Technology

Systems International

• Power, water andresources sector:- Engineering- Procurement- Construction- Commissioning

• Maintenanceservices

• Shutdowns andturnarounds

• Sectors:- LNG- Minerals

processing- Petroleum- Power- Water

• Passenger buildand maintenance

• Freight build andmaintenance

• GE parts sales &distribution

• Supply chainservices

• Componentmanufacture

• Naval shipmaintenance

• Road tunnelsignaling andcommunicationssystems

• Train signalingand controlsystems

• Wirelesscommunications

• Engineeringdesign,procurement,construction andcommissioning ofwater treatmentplants

• O&G pipeline EPCcapability

Mark ChilcoteShane KimptonAlan Beacham David MacKenzie Alan Beacham

Rail & DefenceO

pera

tions

EGM

14

Rail & Defence

FY15 Overview• EBIT impacted by reduced coal freight

locomotive sales and associated under-utilisation of rail facilities

• Strong performance across MTM and UGLUnipart contracts

• Solid order book with 95% recurring• Key opportunities secured : Sydney Metro Northwest Tangara technology upgrade (not in FY15

order book)

Outlook• FY16 revenue in line with FY15• Freight locomotive market remains subdued

offset by continuing strength in maintenanceand upgrade markets

• Profitability expected to improve in FY16following rationalisation of under-utilised railfacilities

Revenue $m EBIT $m

FY15 FY14 Change

Revenue - $m 986.3 971.1 2%

EBIT - $m 32.4 45.8 (29%)

EBIT margin 3.3% 4.7%

Order book - $b 2.4 2.6 (6%)

15

Asset Services

FY15 Overview• Revenue increase driven by Stanwell and

Chevron contracts secured in FY14• EBIT impacted by margin pressure in coal

maintenance and low work volumes in WAdesign business

• WA design business closed in June 2015• Strong order book predominantly recurring• Key opportunities secured: APLNG and GLNG BP fuel terminal network

Outlook• Revenue expected to grow in FY16 driven by

contracts secured in FY15 and ramp up ofChevron maintenance

• Shutdown revenue expected to increasesignificantly in FY17 as LNG plants enter firstshut down cycle

• FY16 profitability expected to improve withclose of WA design business and coal sectornow reset to new base

Revenue $m EBIT $m

FY15 FY14 Change

Revenue - $m 463.2 455.8 2%

EBIT - $m 8.5 11.4 (25%)

EBIT margin 1.8% 2.5%

Order book - $b 1.0 1.0 1%

16

Technology Systems

FY15 Overview• Revenue contraction driven by completion of

Regional Rail Link and Solomon Spur duringFY15 and reduced revenue from DTRS asproject moves to later stages of the contract

• EBIT impacted by the ongoing dispute on DTRSoffset in part by a strong contribution fromRegional Rail Link

• Secured Sydney Metro Northwest

Outlook• FY16 revenue expected to be flat with Sydney

Metro Northwest replacing completed projectsin FY15

• Medium term outlook supported by largesecured contracts delivering substantialrevenue growth in FY17 as projects move fromdesign to delivery phase

• Expect to close NorthConnex in coming weeks

Revenue $m EBIT $m

FY15 FY14 Change

Revenue - $m 231.3 301.3 (23%)

EBIT - $m 10.3 21.1 (51%)

EBIT margin 4.4% 7.0%

Order book - $b 0.6 0.3 102%

17

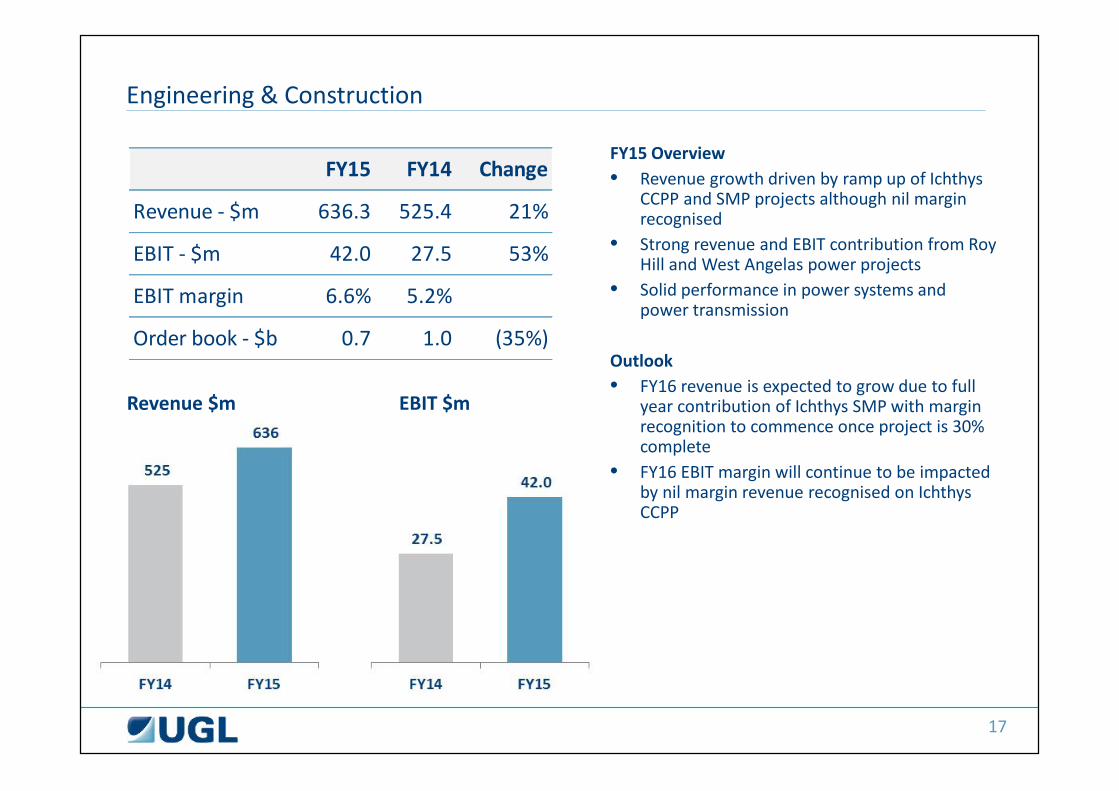

Engineering & Construction

FY15 Overview• Revenue growth driven by ramp up of Ichthys

CCPP and SMP projects although nil marginrecognised

• Strong revenue and EBIT contribution from RoyHill and West Angelas power projects

• Solid performance in power systems andpower transmission

Outlook• FY16 revenue is expected to grow due to full

year contribution of Ichthys SMP with marginrecognition to commence once project is 30%complete

• FY16 EBIT margin will continue to be impactedby nil margin revenue recognised on IchthysCCPP

Revenue $m EBIT $m

FY15 FY14 Change

Revenue - $m 636.3 525.4 21%

EBIT - $m 42.0 27.5 53%

EBIT margin 6.6% 5.2%

Order book - $b 0.7 1.0 (35%)

18

International

FY15 Overview• Revenue decline driven by reduced levels of

secured infrastructure projects in South EastAsia

• Overhead costs not recovered due to lowactivity

• Cost base right-sized to support scale ofoperations in FY16

• EBIT also impacted by reduced throughputvolumes in Indian locomotive fabricationfacility

• Texmaco JV currently being exited (previouslyprovisioned)

Outlook• Strong near to medium term prospects in

tunneling, water and oil & gas pipelines inSouth East Asia

• Continued investment in the region contingenton securing identified key opportunities inFY16

Revenue $m EBIT $m

FY15 FY14 Change

Revenue - $m 11.3 22.8 (50%)

EBIT - $m (5.9) (5.1) 16%

EBIT margin (52.1)% (22.4)%

Order book - $b 0.04 0.01 161%

Financial AnalysisRay Church

20

Underlying ResultsResults overview

$m FY15 FY14 ChangeOperating revenue 3,048.6 4,511.5 (32%)EBIT (DTZ FY15 $28m FY14 $124m ) 75.3 185.8 (59%)EBIT margin 2.5% 4.1%Interest (25.5) (37.4) 32%Tax (15.5) (30.2) 49%Non controlling interest (4.0) (6.4) 37%Net profit after tax 30.3 111.7 (73%)NPAT margin 1.0% 2.5%EPS 18.2 67.1Effective tax rate 31.0% 20.4%ROFE 14.0% 11.4%Engineering CAPEX 16.8 23.2

21

DTZ overview

$m Trading Profit on sale FY15

Operating revenue 729.1 - 729.1EBIT 27.8 - 27.8

Sales Costs - (17.3) (17.3)Accounting Profit on Sale - 83.4 83.4Reported EBIT 27.8 66.1 93.9Interest (6.3) - (6.3)Tax (4.1) (17.2) (21.3)Non-Controlling Interest 0.1 - 0.1Profit from Discontinued Operations 17.5 48.9 66.4

22

Business resetOne-Off items impacting FY2015

* Excluding Ichthys CCPP

23

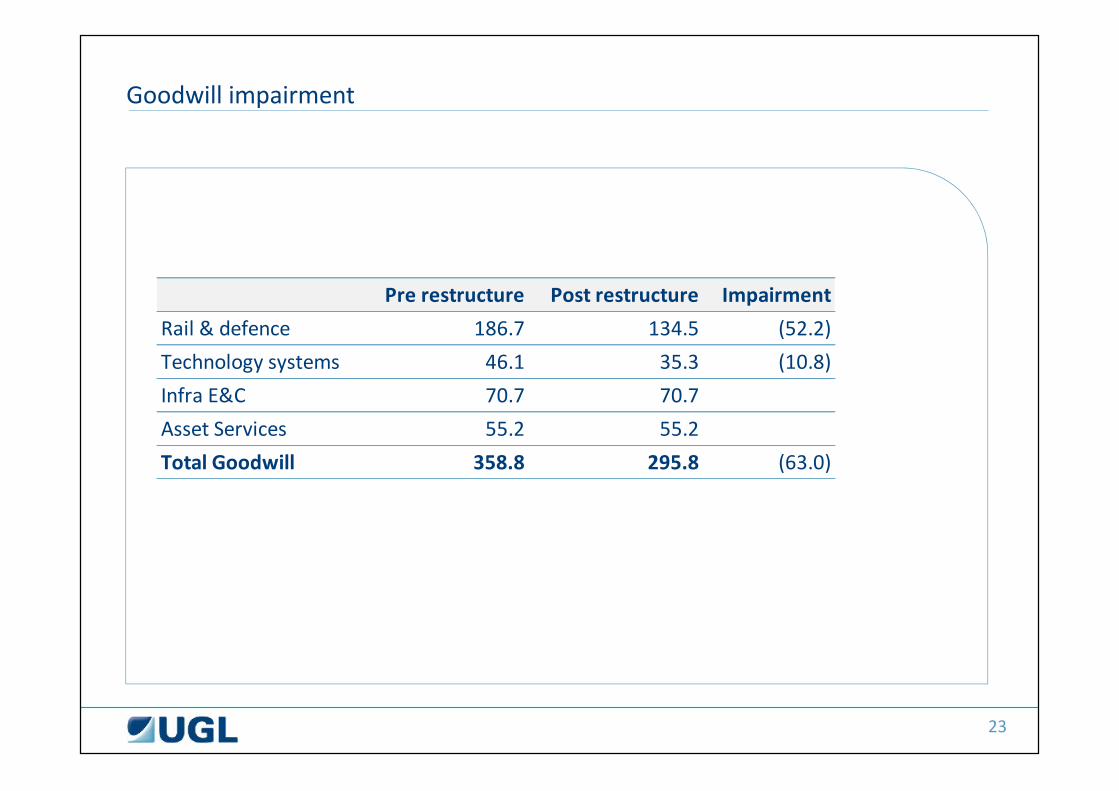

Goodwill impairment

Pre restructure Post restructure ImpairmentRail & defence 186.7 134.5 (52.2)Technology systems 46.1 35.3 (10.8)Infra E&C 70.7 70.7Asset Services 55.2 55.2Total Goodwill 358.8 295.8 (63.0)

24

Reconciliation to statutory

* Includes $11m DTZ Revenue for details refer to note 3 and Note 26 of the financial statements

$m UnderlyingJV's

(Equitymethod)*

Provision forcontract loss

Claimsresolution &settlement

Resourcesslowdown

Goodwillimpairment

Tender costswritten off

Restructurecosts

Discontinuedoperations

Continuingoperations

Revenue 3,048.6 (319.9) (717.5) 2,011.1

EBIT 75.3 (6.9) (175.0) (39.8) (84.9) (63.0) (18.9) (38.1) (27.8) (379.1)

Net interest (25.5) 6.2 (19.3)

Tax (15.4) 6.9 52.5 11.9 22.6 0.0 5.7 11.4 4.1 99.6

Non-controlling interests (4.0) 0.1 (3.9)

NPAT 30.3 (122.5) (27.8) (62.4) (63.0) (13.2) (26.7) (17.4) (302.7)

Profit attributable to discontinued operations 66.3

Statutory Loss (236.4)

25

Operating Cash Flow ($m)

26

Balance Sheet - WIP reduction

Progress on WIP WIP Movement

• Good level of cash conversion in June

• Gross WIP reduced from $257m at31 December to $163m at 30 June

• WIP days at 30 June: 30 days

27

Balance Sheet - Change in accounting for unincorporated joint ventures (UJVs)

Background• UJV’s proportionally consolidated 2015• First year of material UJV impacts – previously equity accounted• Aligns with AASB 11 and industry peers

Impact on Balance Sheet• Increase of cash $91m• Decrease in net working capital balance of ($113m)

Balance Sheet 30 June 2015 ($m)Excl

UJV impactIncl UJVs

- StatutoryImpact

Cash and cash equivalents 74 165 91Trade and other receivables 214 233 19Inventories 227 245 18Investments (5) 17 22Property, plant and equipment 48 52 3Trade and other payables (265) (416) (151)Provisions (61) (63) (2)Other 202 202 -Net assets 435 435 -

28

Balance Sheet - Material items impacting net debt in H2 2015

Cash impact of material one-off items $m

Net (Debt) 31 Dec 2014 (63.0)DTZ Sale Costs (25.3)DTZ Final Proceeds 60.7DTZ Exit Costs (12.4)Claims Resolved 66.0Working Capital Movement (8.4)Ichthys CCPP (56.0)Restructure Costs (12.3)CAPEX (6.1)UJV cash 90.5Net Movement 96.7Net Cash 30 June 2015 33.7

29

Debt structure post refinancing

Maturity profile by years - $m

* Includes UJVs cash

Credit* metrics FY15 FY14

(Net cash)/Net debt ($m) (34) 567Net debt / (net debt + equity) - 32.4%Net debt / EBITDA - 2.4xInterest Cover 4.0 5.2x

Debt* and bonding facilities $m

Total facilities 381Drawn 131Cash 165(Net cash) (34)Available Facilities 250Total Liquidity 415

Bonding facilities $m

Total facilities 543Drawn 336Available facilities 207

30

Progress against FY16 priorities

Priorities Progress

Maintain lean overhead costbase

Leaner and more focused Corporate centre established withincreased functional responsibilities in Divisions

On track to realise $33m in annual overhead savings

Embed consistentstandardised commercialand project managementdisciplines

Enhanced risk and governance framework Commenced implementation of the UGL Way

• Modules rolled out over next 18 months• Priority on project management focused work streams

Execute well to maintaingross margin

Consolidated execution of higher risk projects within a singledivision under experienced leadership

Standardised project management reporting Financial delegations aligned to skills and capability Focus on strengthening project management capabilities Alignment of project team incentives to performance

Disciplined portfoliomanagement of businessesdriving capital allocationdecisions

Balance sheet distributed to Divisions Responsibility for cash flow management now with the

Divisions and down to the projects FY16 KPIs to measure return on capital as well as sales and

earnings performance

1

2

3

4

31

Order Book & PipelineRoss Taylor

32

Order Book

Order Book Over Time ($m) Order Book By Year ($m)

33

Order Book – recurring/project mix

All Years FY16

34

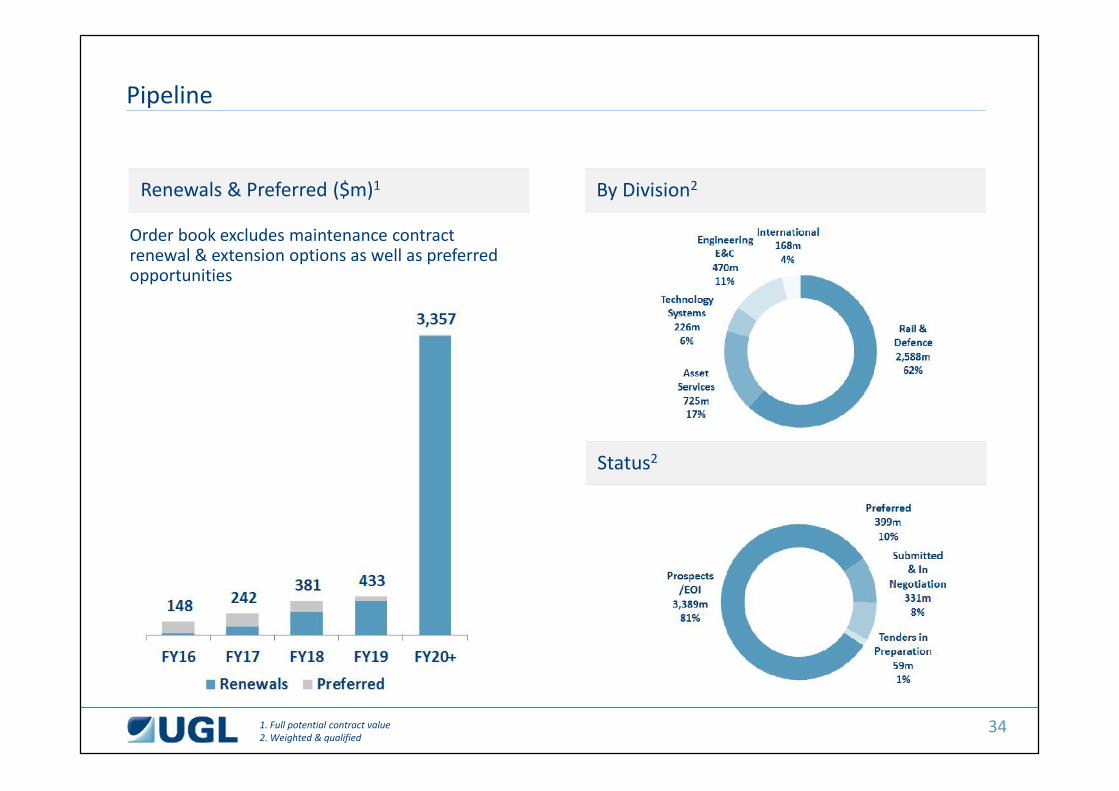

Pipeline

Renewals & Preferred ($m)1 By Division2

Order book excludes maintenance contractrenewal & extension options as well as preferredopportunities

Status2

1. Full potential contract value2. Weighted & qualified

OutlookRoss Taylor

36

Market outlook

• Diversity in revenue continues to provide balance against contraction in resources sector

• Overall markets remain competitive driven by excess capacity of service providers

• Subdued resources infrastructure and operations investment expected to continue in the medium term asresources clients retain strong focus on cost reduction and improved efficiencies

• Strong transport infrastructure opportunities supported by Government investment

Leading player in passenger rail maintenance

Proven O&M capability for privatised/franchised networks

Market leader in transport technology systems

Strong international OEM partners

• Growth in LNG maintenance as capex projects reach operational phase

Tier 1 maintenance services provider

Core base of LNG maintenance and shutdown work flow

Sufficient scale to maintain a permanent shut down crew providing competitive advantage

• Opportunities in adjacent markets such as distribution and renewables

Market leader in power systems with solid win rate

• Steady growth in waste water sector driven by conservation initiatives

Strong design capabilities and project delivery track record

37

Description• Complete project reviews and implement new initiatives

• Complete restructure of divisional and corporate overheads to right size thebusiness

• Focus on and reduce WIP balance

• Improve project gross margin delivery

• Convert identified pipeline opportunities

• Realise full run-rate of cost reduction initiatives implemented in FY15• Revenue $2.3 billion and EBIT margin increase to 3%

• Deliver average cash flow conversion of 100% of NPAT excluding Ichthys CCPP

• Revenue step change by at least $300m driven by exposure to transportinfrastructure and LNG maintenance

• Commencement of major contracts within Technology Systems and Asset Servicesdivisions

• Improvement in margin due to replacement of nil margin revenue with newprofitable contracts

• Profitable top line growth combined with lean overhead structure will see afurther EBIT margin improvement towards 4%

• Sustainable enterprise and industry leader

• Continue to seek opportunities for growth and value enhancement

Repositioned for improved performance from FY16

FY16Step 2:

Turnaround

FY17Step 3:

Step change

FY18 + beyondStep 4:Growth

FY15Step 1:Reset

Completed

On Track

Appendices

40

The new UGL Vision and strategic priorities

UGL VISION An industry disruptor that dominates the Australian market through theapplication of world leading technology and execution capabilities taking

the smartest solutions to our clients and sectors globally

UGL VISION

An industry disruptor that dominates the Australian market through the application ofworld leading technology and execution capabilities taking the smartest solutions to our

clients and sectors globally

UGL VISION

An industry disruptor that dominates theAustralian market through the applicationof world leading technology and executioncapabilities taking the smartest solutions

to our clients and sectors globally

STRATEGIC PRIORITIES

LEAD IN SAFETY AND SUSTAINABILITY

CONSISTENTLY DELIVER

BUILD A WORLD CLASSTALENT BASE

BUILD OUR PORTFOLIO STRENGTHSTHROUGH INNOVATION

DELIVER STRONG ECONOMICRETURNS FOR SHAREHOLDERS

BE THE PARTNEROF CHOICE

41

Major Contracts

Name Description DivisionOriginalValue ($m) Duration Contract type

UGL Unipart In JV with Unipart Rail, heavy maintenance andlogistics management services on 1,050 passengercars in Sydney’s passenger car fleet for Sydney Trains& Transport for NSW

Rail 1,400+$900mextensionoption

2012-2019+ 5 yearextensionoption

Schedule ofrates

Metro TrainsMelbourne

Operations and maintenance of Melbourne’spassenger train franchise

Rail 1,300excludingcapital works

2009-2017+ 7 yearextensionoption

Schedule ofrates

North WestRail Link

Design, build, finance and operate the new rapidtransit service as a member of the NRT consortium

Totalconsortiumcontract$3.7bn

• Design and deliver the tunnel systems, rolling stock,rail signalling and overall control systems in JV withMTR Corporation

TechnologySolutions

2015-2019 Lump sum

• Operations and maintenance of the service in JVwith MTR & John Holland

Rail 2019-2034 Schedule ofrates

Freightliner Maintenance of locomotives and wagons operatedby Freightliner Australia in the Hunter Valley

Rail 115 2010-2020 Schedule ofrates

Remaining contract value > $100 million

42

Major Contracts

Name Description DivisionOriginalValue ($m) Duration

Contracttype

Pacific National Upgrade and maintenance for a portion of the PacificNational Rail locomotive fleet

Rail 540 Maintenance:2013-2020Upgrade:2012-2016

Schedule ofratesLump sum

Ichthys SMP In JV with Kentz Corporation structural, mechanicaland piping construction package for the Ichthys LNGProject

E&C 370 2014-2017 Lump sum

Stanwell Facilities maintenance and management, overhaulsand project works across Stanwell’s coal, gas andhydro energy assets in Queensland

AssetServices

280 2014-2018+ potential forextension to 5years

Cost plus

Ichthys CCPPPower Station

Design, supply of the balance of plant and theconstruction of a combined cycle power plant for theIchthys LNG project

E&C 275 2012-2016 Lump sum

BP Operation and maintenance of BP’s 17 fuel terminalsacross Australia through a JV between UGL and BP

AssetServices

190 2015-2018+ 3 yearextension option

Schedule ofrates

ChevronMaintenance

Maintenance services for the operational phase ofChevron’s Western Australian assets

AssetServices

NA 2014-2019+ extensionoptions

Schedule ofrates

Remaining contract value > $100 million

43

Major Contracts

Name Description DivisionOriginalValue ($m) Duration

Contracttype

APLNG Downstream maintenance, shutdown andmodification project services for the operationalphase of the Curtis Island LNG Facility

AssetServices

NA 2015-2019 Schedule ofrates

GLNG Maintenance, shutdown, engineering and projectservices for Santos GLNG’s Curtis Island LNG facility

AssetServices

120 2015-2018+ extensionoptions up to 4years

Schedule ofrates

TangaraTechnologyUpgrade

In joint venture with Unipart Rail, technologyupgrade of fleet of 446 Tangara passenger railcars

Rail 131 2015-2018 Schedule ofrates

Remaining contract value > $100 million

44

New Contract Wins and Extensions

$2.1 billion in contract wins and renewals:

• Sydney Metro Northwest: $3.7bn operationscontract to be delivered by UGL as part of theNorthwest Rapid Transit Consortium [check nameof consortium?]

• APLNG: Multi-million dollar 4 year downstreammaintenance services contract

• GLNG: $120m 3 year downstream maintenanceservices contract

• BP: 3 year $190m operations and maintenancecontract across 17 BP fuel terminals

Post 30 June 2015 win:

• Tangara Technology Upgrade: $131m contractundertaken by UGL Unipart Rail for technologyupgrade of Tangara passenger rail fleet in Sydney

45

Order Book & Pipeline By Division

Order Book ($m) Pipeline ($m)

46

Order Book

By delivery structure ($m) By contract type ($m)