fund management

TRANSCRIPT

FUND MANAGEMENT

Forms of Business Organization• Sole Proprietorship – owned by one person and

whose owner is called proprietor (for male owner) or proprietress (in case of a female owner).

• Partnership – owned by two or more persons and whose owners are called partners.

• Corporation – owned by five or more persons and whose owners are called corporators. Corporator is a generic name of the owner of the corporate form of business organization.

Types of Business Organizations• Service Concern – these are the businesses that

render services to earn income. For example shop, beauty parlor, schools, hospitals, repair shop, etc.

• Trading Concern – these are the businesses that sell to earn income. For example are drug store, hardware, sari-sari store, boutique, etc.

• Manufacturing Concern – these are businesses that convert raw materials into finished products. Like furniture shop, shoe factory, etc.

Types of Cash1) Cash on hand – this represents the cash collection waiting to

be deposited the following banking day.

2) Cash in bank – this represents the cash already deposited in the bank.

3) Cash fund – ideally, company cash has to be maintained under the imprest system of cash handling. For this matter, the company has to maintain a certain fund to comply with the other fund requirements of the company.

4) Cash equivalent – the PAS (Philippine Accounting Standards) define cash equivalents as short term and highly liquid investments are readily convertible to cash and so near their maturity that they present insignificant risk of changes in value.

Cash in bank could either be:1) Saving Account – this is an account were the

money deposited will earn interest income for the meantime while it is not yet used.

2) Demand Deposit – sometimes called checking account or current account. Normally, demand deposit account does not earn interest. This is evidenced by a checkbook.

3) Combo Account – these are some banking companies that tried to combine savings account and demand deposit into one account.

The following funds are classified as cash:

a) Petty Cash Fund – this is the fund that will cater the small expenditures of the company.

b) Change Fund – this fund is used to maintain loose change to address the concern for small bills and coins.

c) Dividend Fund – this is the fund used to pay for the dividends which the board of directors have declared and payable a time certain in the future.

Bank Products (interest are paid at maturity dates)

Overnight placementsWeekly time depositsMonthly time deposits or 30-day time deposits60 days, 90 days, 180 days, one year, 2 years,

3 years, etc.Trusts

Government Securities

1) Treasury Bills

2) Treasury Notes

3) Treasury Warrant

4) Treasury Bond

COMMERCIAL PAPERS(INTEREST ARE PAID BASED ON AGREEMENT)

1. Private company’s bonds issuances

2. Private company’s commercial papers

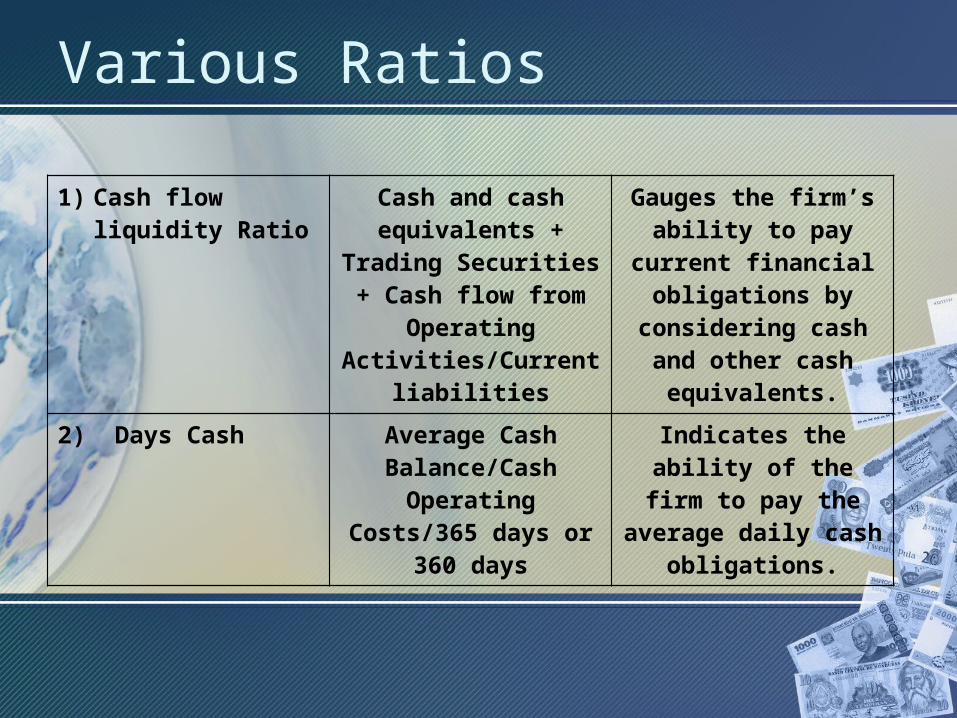

Various Ratios

1) Cash flow liquidity Ratio

Cash and cash equivalents + Trading Securities + Cash flow

from Operating Activities/Current

liabilities

Gauges the firm’s ability to pay current financial obligations by considering cash

and other cash equivalents.

2) Days Cash Average Cash Balance/Cash

Operating Costs/365 days or 360 days

Indicates the ability of the firm to pay the average daily cash

obligations.

The breakdown of the cash and cash equivalents must have been:

1. Cash on hand

2. Cash fund

3. Cash in banks

4. Investments with less than one year maturity

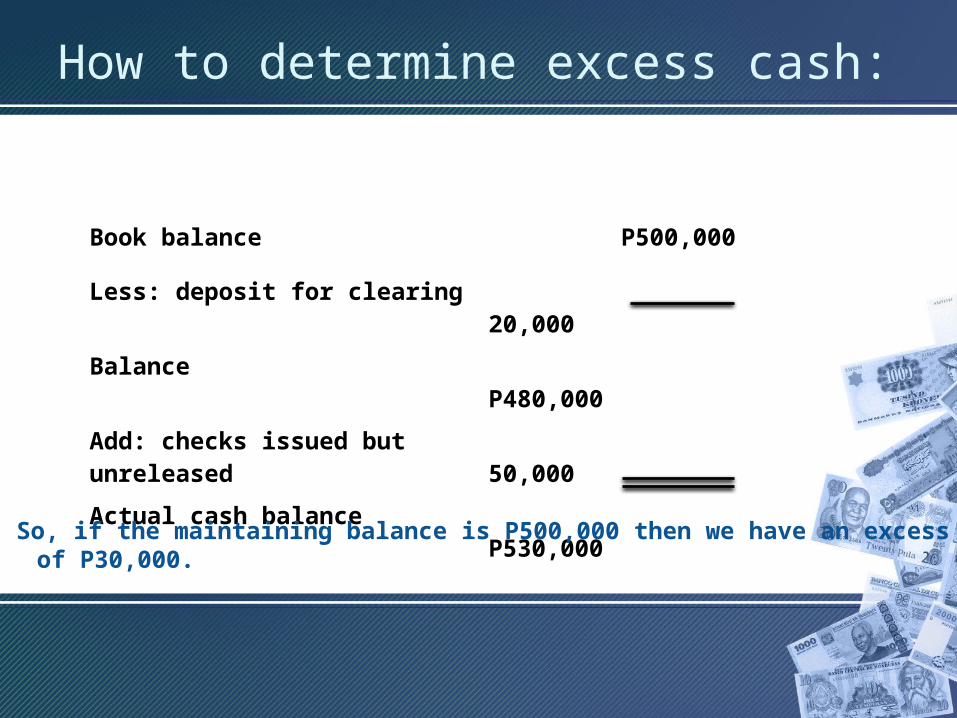

How to determine excess cash:

Book balance P500,000

Less: deposit for clearing 20,000

Balance P480,000

Add: checks issued but unreleased

50,000

Actual cash balance P530,000

So, if the maintaining balance is P500,000 then we have an excess cash of P30,000.

How do we value cash?• Cash is valued at face value. For cash denominated

in foreign currency, like the US dollar, Japanese yen, etc. this should be converted to current rate (current rate would mean the rate on the last banking day at the end of the accounting period). If the deposit is placed in a bank having financial difficulty, the face value should be written down to estimated realizable value.

Functions with cash handlingPosition : Collector

Directly reporting to :

Daily Duties:

1. Reviews the accounts receivable that are due for collection on that day.

2. Follow ups thru phone calls/email.

3. Issues provisional receipts to customers who paid their respective accounts.

4. Remits collections to the office cashier together with the daily remittance form fully paid out.

Responsibilities:

5. Early or on time collection of the various accounts entrusted to him for collection.

6. Report to the supervisor about the customers who are difficult to collect from.

7. Report any feedback from the customer so management can address the concern as early as possible.

Position : Accounting Supervisor

Directly reporting to :

Daily Duties:

1. Supervises accounting department personnel.

2. Approves all vouchers prior to entry in the books of accounts.

3. Analyzes the various reports coming from various departments to countercheck the reports generated by the accounting department.

Periodic Duties:

4. Checks accounting reports.

5. Reports the result of operation to the Board of Directors.

Responsibilities:

6. Financial Reporting

7. Tax Reporting

Files to maintain:

8. Accounting Reports

9. Income Tax Payments

Collectors collect the receivable of

the company

Customers, as an alternative, may pay directly to the office

The Cahier receives the money from collectors and customers

The Junior Accountant will journalize the

receipt transactionsDepository Bank

The accounting supervisor will check the entry and later on check the bank reconciliation

statement

The General Accountant will record the transaction. He will

receive the bank statement and prepare the bank reconciliation

Flow of Cash Transaction

Position : Internal Auditor

Directly reporting to :

Daily Duties:

Checks the documents coming from the cashier and from the Junior Accountant.

Periodic Duties:

1. Conducts post audit of the documents and reports.

2. Conducts compliance audit. This is an audit check on the compliance of the existing system of internal control installed by the company.

3. Evaluates of certain internal control mechanisms for enhancing its operation and asset safely.

Responsibilities:

4. See adherence of all policies and procedures by various personnel of the company.

5. Asset protection.

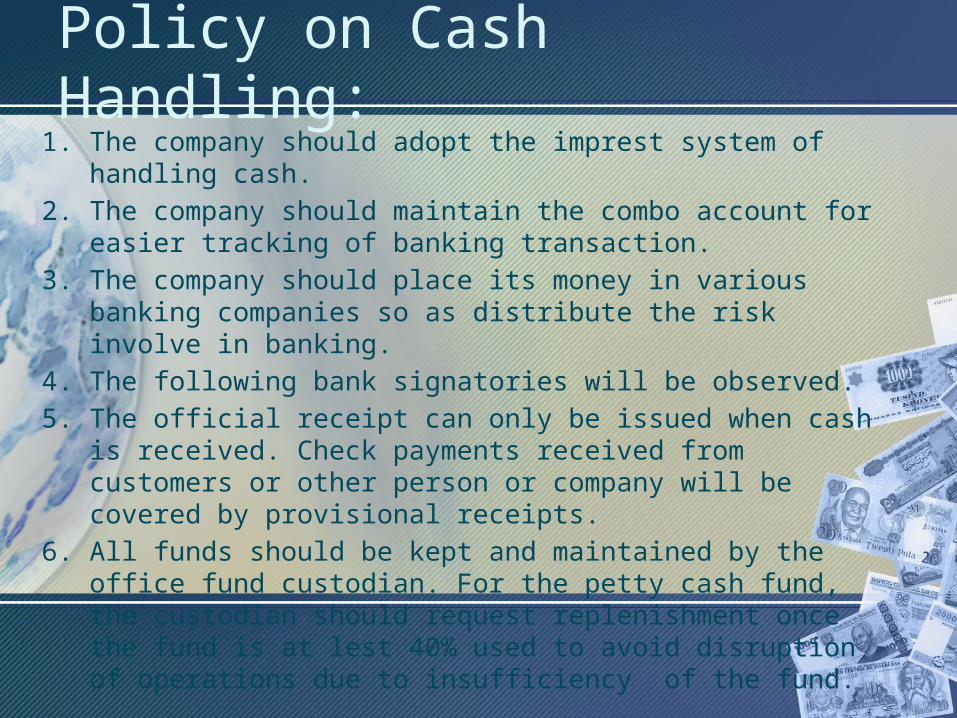

Policy on Cash Handling:1. The company should adopt the imprest system of handling cash.

2. The company should maintain the combo account for easier tracking of banking transaction.

3. The company should place its money in various banking companies so as distribute the risk involve in banking.

4. The following bank signatories will be observed.

5. The official receipt can only be issued when cash is received. Check payments received from customers or other person or company will be covered by provisional receipts.

6. All funds should be kept and maintained by the office fund custodian. For the petty cash fund, the custodian should request replenishment once the fund is at lest 40% used to avoid disruption of operations due to insufficiency of the fund.

Procedure in Cash Handling:1. The cashier upon receiving cash from the customer or the company

collector will issue an official receipt.

2. The cahier will also issue an official receipt for check deposits that are already cleared in banking system.

3. The cashier will deposit the cash collection up to 12noon of the current day intact within the day and money collections after 12noon will be deposited intact the following banking day.

4. The cashier will then prepare the daily cash position report.

5. The official receipt issued together with the validated deposit slip and the original copy of the daily cash position report will then be forwarded to the accounting department for file and the preparation of the appropriate accounting entries and for eventual entry in the books of accounts.

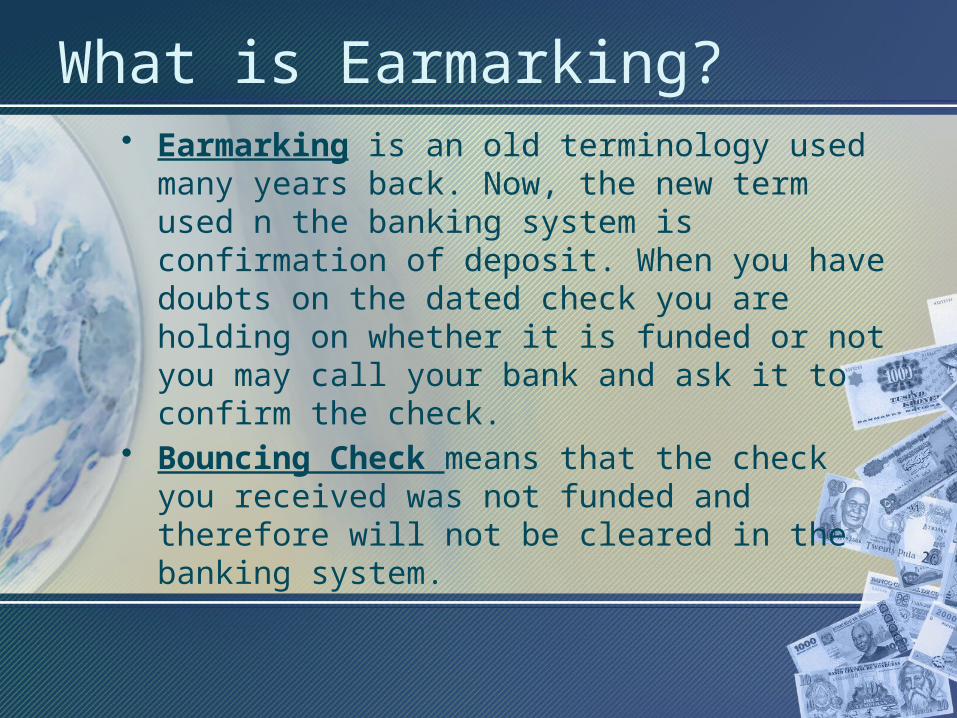

What is Earmarking?• Earmarking is an old terminology used many years

back. Now, the new term used n the banking system is confirmation of deposit. When you have doubts on the dated check you are holding on whether it is funded or not you may call your bank and ask it to confirm the check.

• Bouncing Check means that the check you received was not funded and therefore will not be cleared in the banking system.

THANKS FOR LISTENING !!!!!!