future trends in - ispe - dach · pdf filefuture trends in biopharmaceutical ... avastin...

TRANSCRIPT

Future Trends inBiopharmaceutical Operations and Facilities

Johannes R. Roebers, PhDSenior Vice President, Biologic Strategy, Planning and Operations

Elan Pharmaceutical International Ltd, Dublin, Ireland

PresentationISPE-Workshop on “Single-Use Technologies in Biomanufacturing Processes”

26-27th May 2011, Marseilles, France

Disclaimer

The content and views in this presentation are the views of the author and not necessarily the view of Elan.

Elan and the author do not make any representation regarding the accuracy or completeness of the data presented or data used from referenced sources.

This presentation contains forward-looking statements about Elan’s financial condition, results of operations and business prospects that involve substantial risks and uncertainties.

A list and description of these risks, uncertainties and other matters can be found in Elan’s Annual Report on Form 20-F for the fiscal year ended December 31, 2010 and in its Reports of Foreign Issuer on Form 6-K filed with the SEC.

Elan assumes no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise.

Outline

• Trends in Licensed and Future Biopharmaceuticals

• Advances in Biopharmaceutical Operations

• Technology Trends in Biopharmaceutical Operations

• Elan Facility Case Study: “Traditional” vs. “Mini-Mill”

• Future Trends in Biopharmaceutical Operations

Trends in Licensed and Future Biopharmaceuticals

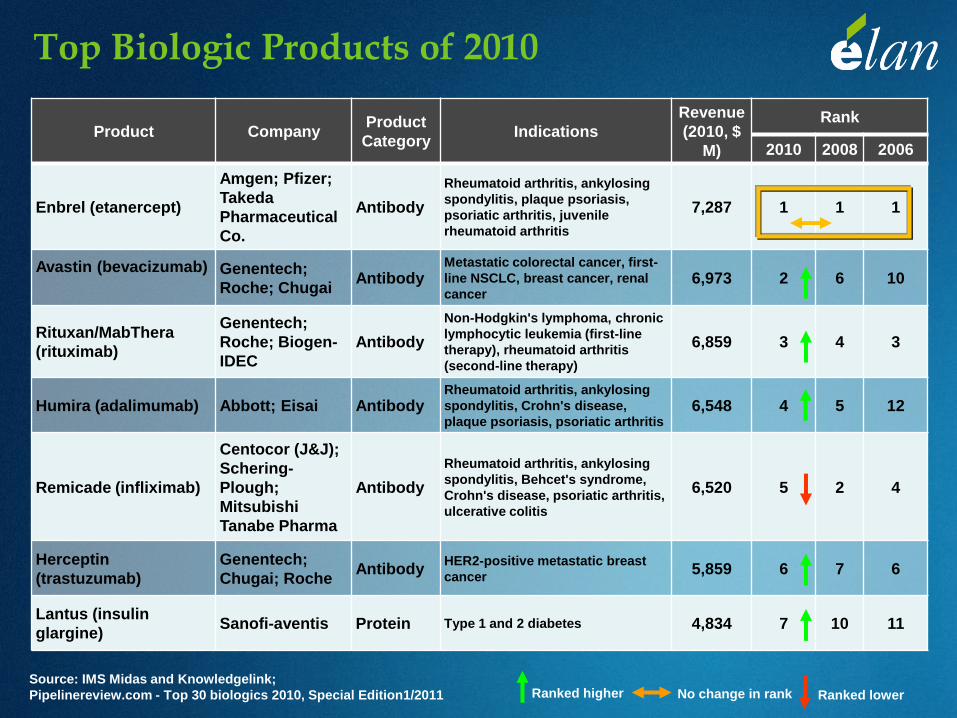

Top Biologic Products of 2010

Product CompanyProduct

CategoryIndications

Revenue

(2010, $

M)

Rank

2010 2008 2006

Enbrel (etanercept)

Amgen; Pfizer;

Takeda

Pharmaceutical

Co.

Antibody

Rheumatoid arthritis, ankylosing

spondylitis, plaque psoriasis,

psoriatic arthritis, juvenile

rheumatoid arthritis

7,287 1 1 1

Avastin (bevacizumab) Genentech;

Roche; ChugaiAntibody

Metastatic colorectal cancer, first-

line NSCLC, breast cancer, renal

cancer6,973 2 6 10

Rituxan/MabThera

(rituximab)

Genentech;

Roche; Biogen-

IDEC

Antibody

Non-Hodgkin's lymphoma, chronic

lymphocytic leukemia (first-line

therapy), rheumatoid arthritis

(second-line therapy)

6,859 3 4 3

Humira (adalimumab) Abbott; Eisai AntibodyRheumatoid arthritis, ankylosing

spondylitis, Crohn's disease,

plaque psoriasis, psoriatic arthritis 6,548 4 5 12

Remicade (infliximab)

Centocor (J&J);

Schering-

Plough;

Mitsubishi

Tanabe Pharma

Antibody

Rheumatoid arthritis, ankylosing

spondylitis, Behcet's syndrome,

Crohn's disease, psoriatic arthritis,

ulcerative colitis

6,520 5 2 4

Herceptin

(trastuzumab)

Genentech;

Chugai; RocheAntibody

HER2-positive metastatic breast

cancer5,859 6 7 6

Lantus (insulin

glargine)Sanofi-aventis Protein Type 1 and 2 diabetes 4,834 7 10 11

Ranked higher No change in rank Ranked lower

Source: IMS Midas and Knowledgelink;

Pipelinereview.com - Top 30 biologics 2010, Special Edition1/2011

Top Biologic Products (contd.)

Product CompanyProduct

CategoryIndications

Revenue

(2010, $

M)

Rank

2010 2008 2006

Epogen/Procrit/Eprex/

ESPO (epoetin alfa)

Amgen; Ortho

Biotech/Janssen -

Cilag (J&J);

Kyowa Hakko

Kirin

Protein Renal anemia 4,590 8 3 5, 7*

Neulasta (pegfilgrastim) Amgen Protein Neutropenia 3,558 9 9 8

Lucentis (ranibizumab)Genentech;

NovartisAntibody

Wet age-related macular

degeneration 3,106 10 13 -

Aranesp/NESP (darbepoetin

alfa)

Amgen; Kyowa

Hakko Kirin

Pharma

Protein Anemia 2,995 11 8 2

Avonex (interferon beta-1a) Biogen Idec ProteinRelapsing forms of

multiple sclerosis2,518 12 11 15

Rebif (interferon beta-1a) Merck Serono ProteinRelapsing forms of

multiple sclerosis2,297 13 15 16

Novolog, NovoRapid

(insulin aspart)Novo Nordisk

Protein Glycemic control in

children and adults with

diabetes mellitus2,198 14 22 -

Actrapid (EU)/Novolin (US)

(rhu insulin)Novo Nordisk Protein Type 1 and 2 diabetes 2,185 15 12 9

Source: IMS Midas and Knowledgelink;

Pipelinereview.com - Top 30 biologics 2010, Special Edition1/2011

*In 2006 Epogen and Procrit were ranked separatelyRanked higher No change in rank Ranked lower

Top Biologic Products (contd.)

Product CompanyProduct

CategoryIndications

Revenue

(2010, $

M)

Rank

2010 2008 2006

Advate/Recombinate

(octocog alpha)Baxter Healthcare Protein Hemophilia A 2,095 16 17 -

Humalog Mix 50:50

Premix (insulin lispro)Eli Lilly

ProteinType 1 and 2 diabetes 2,054 17 14 18

Erbitux (cetuximab)Eli Lilly; BMS;

Merck SeronoAntibody

Metastatic colorectal

carcinoma1,791 18 18

Pegasys (peginterferon

alpha -2a)Roche Protein

Chronic hepatitis C virus

infection1,775 19 20 20

Betaseron/Betaferon

(interferon beta-1b)

Berlex; Bayer

Schering PharmaProtein

All relapsing forms of

multiple sclerosis1,661 20 19 19

NovoSeven (eptacog

alpha)Novo Nordisk Protein

Hemophilia, stroke, surgery,

trauma 1,483 21 25 -

Novomix 50 (insulin

aspart)Novo Nordisk Protein Type 1 and 2 diabetes 1,445 22 - -

Botox

(onabotulinumtoxin A)

Allergan

Pharmaceuticals;

GlaxoSmithKline

Protein Medical and aesthetic

indications1,414 23 - -

Source: IMS Midas and Knowledgelink;

Pipelinereview.com - Top 30 biologics 2010, Special Edition1/2011

Ranked higher No change in rank Ranked lower

Top 7 Biologic Products of 2010

Product CompanyProduct

CategoryIndications

Revenue

(2010, $

M)

Rank

2010 2008 2006

Enbrel (etanercept)

Amgen; Pfizer;

Takeda

Pharmaceutical

Co.

Antibody

Rheumatoid arthritis, ankylosing

spondylitis, plaque psoriasis,

psoriatic arthritis, juvenile

rheumatoid arthritis

7,287 1 1 1

Avastin (bevacizumab) Genentech;

Roche; ChugaiAntibody

Metastatic colorectal cancer, first-

line NSCLC, breast cancer, renal

cancer6,973 2 6 10

Rituxan/MabThera

(rituximab)

Genentech;

Roche; Biogen-

IDEC

Antibody

Non-Hodgkin's lymphoma, chronic

lymphocytic leukemia (first-line

therapy), rheumatoid arthritis

(second-line therapy)

6,859 3 4 3

Humira (adalimumab) Abbott; Eisai AntibodyRheumatoid arthritis, ankylosing

spondylitis, Crohn's disease,

plaque psoriasis, psoriatic arthritis 6,548 4 5 12

Remicade (infliximab)

Centocor (J&J);

Schering-

Plough;

Mitsubishi

Tanabe Pharma

Antibody

Rheumatoid arthritis, ankylosing

spondylitis, Behcet's syndrome,

Crohn's disease, psoriatic arthritis,

ulcerative colitis

6,520 5 2 4

Herceptin

(trastuzumab)

Genentech;

Chugai; RocheAntibody

HER2-positive metastatic breast

cancer5,859 6 7 6

Lantus (insulin

glargine)Sanofi-aventis Protein Type 1 and 2 diabetes 4,834 7 10 11

Ranked higher No change in rank Ranked lower

Source: IMS Midas and Knowledgelink;

Pipelinereview.com - Top 30 biologics 2010, Special Edition1/2011

RANK PRODUCT MOLECULE MOLECULE CLASS EXPRESSION/MFGESTIMATED

PROTEIN MASS*

1 Enbrel Fusion Protein Antibody CHO/BATCH 900 kg

2 Remicade Chimeric Antibody Antibody MMC/PERFUSION 1000 kg

3 Rituxan Chimeric Antibody Antibody CHO/BATCH 2100 kg

4 Humira Human Antibody Antibody CHO/BATCH 260 kg

5 Avastin Humanized Antibody Antibody CHO/BATCH 1100 kg

6 Herceptin Humanized Antibody Antibody CHO/BATCH 900 kg

7 Neulasta Pegylated Filgrastin Therapeutic Protein ECOLI/BATCH < 5 kg

8 Lantus Modified Insulin Therapeutic Protein ECOLI/BATCH 1500 kg

9 Aranesp Modf. Erythropoietin Therapeutic Protein CHO/BATCH < 1 kg

10 Prevnar Vaccine Vaccine MIRCOBIAL/BATCH < 1 kg

11 Procrit/Eprex Erythropoietin Therapeutic Protein CHO/BATCH < 1kg

12 Epogen Erythropoietin Therapeutic Protein CHO/BATCH < 1 kg

* Antibodies calculated from IMS MIDAS Data. Others Extrapolated from BioPlan Associates, 4/2008 and G.

Jagschies, IBC Conference Boston, 9/2007

Top Biotech Products 2008

Why Antibodies?

AntibodiesTherapeutic

ProteinsTherapeutic

Vaccines

Growth Drivers

Unmet Need +++ + +++

Novel Targets +++ + +

Development Speed ++ ++ -

Growth Resistors

Generic Exposure ++ + +++

Market Performance

Revenue/Product +++ ++ +

Who is and will be driving Mfg?

• Most Therapeutic Proteins and all Vaccines have small Protein Mass Requirements

• Insulins are manufactured in Large-Scale Specialty Mfg Facilities

• Antibodies continue to be the leading class of Biologics in Clinical Development

Antibodies are and will continue to drive Biopharmaceutical Mfg!

Top 12 Antibodies 2008

RANK* PRODUCT COMPANY SALES ’08*EST. PROTEIN

MASS †INDICATIONS

1 Enbrel Amgen/Wyeth $6.4B 1000 kg R. Arthritis, Psoriatic Arthritis, …

2 Remicade J&J/Centocor/Scher. $6.2B 1100 kg R. Arthritis, Crohn’s Disease, …

3 Rituxan Roche/Genentech $5.5B 2100 kg NHL, R. Arthritis,…

4 Avastin Roche/Genentech $4.8B 1100 kg Colorectal, Breast, Lung Cancer, …

5 Herceptin Roche/Genentech $4.7B 900 kg Breast Cancer

6 Humira Abbott $4.5B 270 kg R. Arthritis, Psoriatic Arthritis, …

7 Erbitux Lilly/BMS/ImClone $1.8B 700 kg Colorectal, Head & Neck Cancer

8 Lucentis Roche/Genentech/Nov. $1.7B <5 kg Macular Degeneration

9 Synagis Astra Zeneca/Medim. $1.2B 100 kg Respiratory Tract Disease

10 Xolair Roche/Genentech $0.7B 200 kg Allergic Asthma

11 Tysabri Elan/Biotech IDEC $0.6B - Multiple Sclerosis, Crohn’s Disease

12 ReoPro Lilly/J&J/Centocor $0.2B - Cardiac Ischemic Complications

* Datamonitor, 09/09; †calculated from Datamonitor 09/09 and 2008 IMS MIDAS sales data.

Future Antibody Trends

• Licensed, top selling Antibodies will continue to grow and retain their leading position

• The number of licensed Antibodies will grow from 23 in 2008 to around 50 by 2014

• New “Blockbuster” Antibodies will attack new Targets:

Examples: Rankl, A-Beta

• There will be more Antibody Competition for each Target and Therapeutic Area:

Examples: CD-20, TNF Alfa, Rheumatoid Arthritis

• There will be “Biobetter” and “Biosimilar” Competition for current Antibodies

Antibody Competition

Target: CD-20

Rituxan, IDEC/Genentech/Roche

FDA License 11/1997

Arzerra, Genmab/GSK

Likely FDA Licence 2010

12+ Years with no Competition!

Antibody Competition

Target: TNF

Product Company Launch Year

Enbrel Amgen/Wyeth 1998

Remicade Centocor/J&J/S.-Pl. 1999

Humira Abbott 2003

Cimzia UCB 2009

Simponi Centocor/J&J/S.-Pl. 2009

Future Antibody Mfg Capacity

• Mfg Capacity +1000kg/yr:

Licensed, top selling Antibodies

• Mfg Capacity >500kg/yr:

New “Blockbuster” Antibodies for new Targets

• Mfg Capacity 50-500kg/yr:

New Antibodies in “competitive” Target/Therapy situations

New Antibodies for “niche” Targets/Therapies

New “Biobetter” Antibodies

“Biosimilar” Antibodies

There will be a greater need for Antibody Mfg Capacity of 50-500kg/yr!

Advances in Biopharmaceutical Operations

Biopharmaceutical Operations Parameters

• Success Rate

• Yield

• Number of Bioreactors

• Bioreactor Size

• Number of Production Bioreactor Starts/Year

• Titre

• Downstream designed to match Upstream

Improvements of Operational Parameters

PARAMETER RANGE IMPROVEMENT

Success Rate 50% or less to >95% Operational Experience

Engineering Improvements

Operational Excellence

Yield 50% or less to >70% Harvest and Purification Improvements

Bioreactor Size 10,000 to 25,000 litre Engineering Improvements

Titre <0.5 g/l to >5 g/l Cell Culture Improvements: Cell Line, Selection, Feed/Media Improvements

Industry Typical “Six Pack”6 x 15,000 litre, 25 Starts/Bioreactor/Year

Impact of Improvements

Varied Parameter

RangeFixed

ParameterProtein Mass

Success Rate 70%

95%

Titre 0.5 g/l

Yield 70%

551 kg

748 kg (+30%)

Yield 50%

70%

Titre 0.5 g/l

S. Rate 90%

506 kg

708 kg (+40%)

Titre 0.5 g/l

3 g/l

5 g/l

Yield 70%

S. Rate 90%

708 kg

4252 kg (+500%)

7087 kg (+900%)

Current and Future Industrial Titres

6

5

4

3

2

1

‘08 ‘09 ‘10 ‘11 ‘12 ‘13

Mfg

Tit

re (

g/l

)

2007 Industrial Avg Titre is appr. 1.7 g/l *

* BioPlan Associates, 4/2008

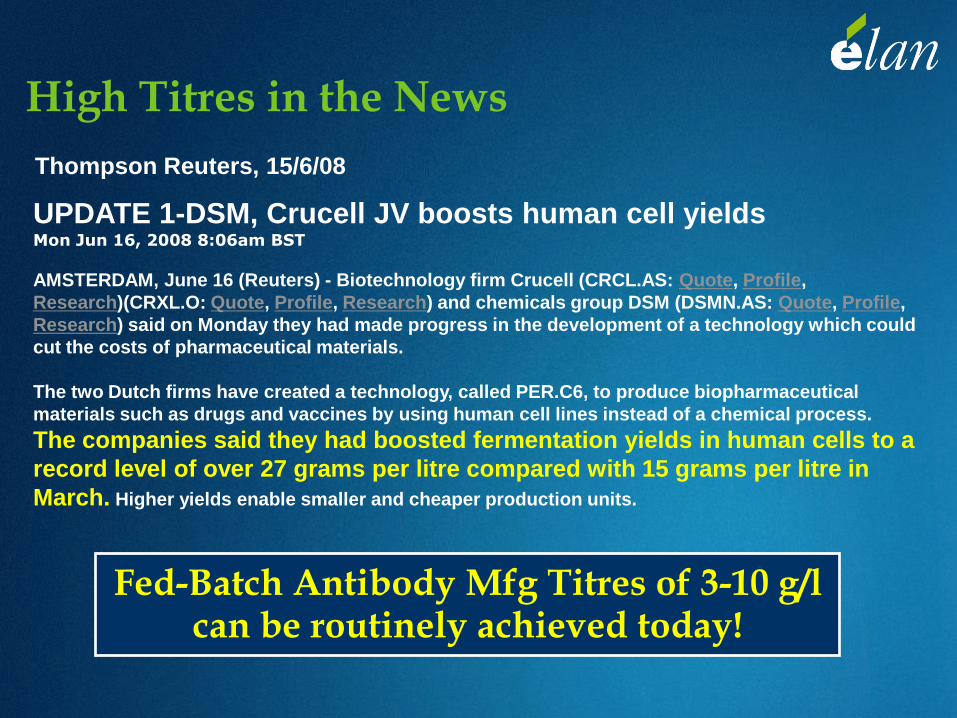

High Titres in the News

UPDATE 1-DSM, Crucell JV boosts human cell yieldsMon Jun 16, 2008 8:06am BST

AMSTERDAM, June 16 (Reuters) - Biotechnology firm Crucell (CRCL.AS: Quote, Profile,

Research)(CRXL.O: Quote, Profile, Research) and chemicals group DSM (DSMN.AS: Quote, Profile,

Research) said on Monday they had made progress in the development of a technology which could

cut the costs of pharmaceutical materials.

The two Dutch firms have created a technology, called PER.C6, to produce biopharmaceutical

materials such as drugs and vaccines by using human cell lines instead of a chemical process.

The companies said they had boosted fermentation yields in human cells to a

record level of over 27 grams per litre compared with 15 grams per litre in

March. Higher yields enable smaller and cheaper production units.

Thompson Reuters, 15/6/08

Fed-Batch Antibody Mfg Titres of 3-10 g/l can be routinely achieved today!

Summary of Manufacturing Trends

• Success Rates and Yields have improved over time

• Mfg Titres have also greatly increased over time

• Mfg Titre has the highest potential to further increase and therefore will reduce the Biopharmaceutical Mfg Capacity

Technology Trends in Biopharmaceutical Operations

Single-Use Processing Technology

• Replacing traditional fixed, stainless steel (SS) tanks, SS piping, and SS bioreactors with sterilized, disposable plastic bags and flexible tubing

• Emerged over the last 15 years and rapidly growing

• Two important, early Innovators:

Wave Bioreactors:Bioreactors

Stedim Biosystems:Films and Bags

Single-Use Innovation: Bioreactors

1000 L Wave Bioreactor

1000 L Xcellerex Bioreactor

1000 L ThermoFisher Bioreactor

200 L Sartorius Biostat Bioreactor

1000 L ATMI Nucleo Bioreactor

200 L Kuehner/ExcellGene OrbShake Bioreactor

Potential of Single-Use Bioreactor

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

1 2 3 4 5 6 7 8 9 10

Titre g/l

Bioreactor Starts/Year 25

Bioreactor Size (l) 1,000

Overall Yield 0.70

Mass Produced (kg) 500.00

Success Rate 0.95

Nu

mb

er

of

Bio

reacto

rs

Elan Mfg Facility Case Study:

“Traditional” vs. “Mini-Mill*”

* Term created by M. Kamarck, Keynote Speaker, IBC Conference and Exhibition, Boston, MA, 9/07

Elan “Traditional” Mfg Facility Study

Site Area 30 acres

Floor Area 35,400 m2

Bioreactors 2 x 15,000 l

Stainless

Steel

Mfg Capacity

@ 3g/l Titre

1000 kg/yr

Process Dev.

Labs

No

Clinical Mfg No

Warehouse, QC

Labs, Utilities,

Offices

Yes

Elan “Mini-Mill” Mfg Facility Study

Site Area 20 acres

Floor Area 16,900 m2

Bioreactors 12 x 1,000 l

or 12 x 2,000l

Single-Use

Mfg Capacity

@ 3g/l Titre

580 kg/yr

(1000 l)

1160 kg/yr

(2000 l)

Process Dev.

Labs

Yes

Clinical Mfg Yes

Warehouse, QC

Labs, Utilities,

Offices

Yes

“Mini-Mill” Concepts

“Traditional” “Mini-Mill”

2 x 15,000 litre 12 x 1,000 litre 12 x 2,000 litre

Mfg Capacity (@3g/l titre) 1000 kg 580 kg 1160 kg

Capital Cost (w/o Start-Up Cost) €350 MM €145 MM €145 MM

Capital Cost/kg 100% 70% 35%

Gas Supply/kg 100% 23% 12%

Electrical Supply/kg 100% 74% 37%

Water Supply/kg 100% 15% 8%

Mfg Area/kg 100% 33% 17%

Production Staff/kg 100% 83% 41%

“Traditional” vs. “Mini-Mill”

Study Results

“Traditional” “Mini-Mill”

Carbon Foot Print* High Lower

Cost of Goods (full capacity) High Lower

Cost of Goods (partial capacity) Higher Lower

Speed to Market “Slow” “Fast”

Flexibility (new Products/Processes) “Painful” “Easy”

“Traditional” vs. “Mini-Mill”

Strategic Comparison

* L. Leveen, IBC Single-Use Applications Conf., San Diego, 6/08

Single-Use “Mini-Mills” are ready for Commercial Manufacturing!

Future Trends in Biopharmaceutical Operations and Facilities

Summary of Future Trends

• More Antibodies will be coming to Market

• More competition among Antibodies,

Competition from “Biobetter” and “Biosimilar” Antibodies

some Competition between Antibodies and Small Molecules

• Will lead to less “Blockbusters” Antibodies

• Titres will continue to increase

• Both trends will lower the demand for new Large Scale Mfg Capacity

Summary of Future Trends

• Increase in Acceptance and Advancement of Single-Use Technology

• Combination of High Titre and Single-Use Technology allows new Breed of Mfg Facilities: “Mini-Mills”

• Existing Large Stainless Steel Facilities for:

Leading “Blockbuster” Antibodies

Biotechs and CMOs producing multiple Antibodies

Less demand for in future

• New Opportunities for Smaller Stainless Steel and “Mini-Mills” Facilities for:

New Antibodies in competitive situations, “Biobetter”, “Biosimilar”, and “niche” Antibodies

Acknowledgements

Product Analysis

• Datamonitor Europe, England

• SmartAnalyst, England

Facility Studies

• PM Engineering, Ireland

• CRB Engineering, USA

• BioPharm Services, England

• RKD Architects, Ireland

• Elan Biologics Team, Ireland