g1 bottle of soda - amazon s3s3.amazonaws.com/zanran_storage/ · bottle of soda cristina cunha ......

TRANSCRIPT

The Value Chain of a The Value Chain of a Bottle of SodaBottle of Soda

Cristina CunhaAnita Zivkovic

Focal Firms and SMEs in Global Value Chains

University of Fribourg

Agenda• Introduction into the soft drink industry• Spatial organization of production• Global value chain▫ Focal Firms▫ Bottlers▫ Suppliers▫ Distributors

• Value added• Conclusion

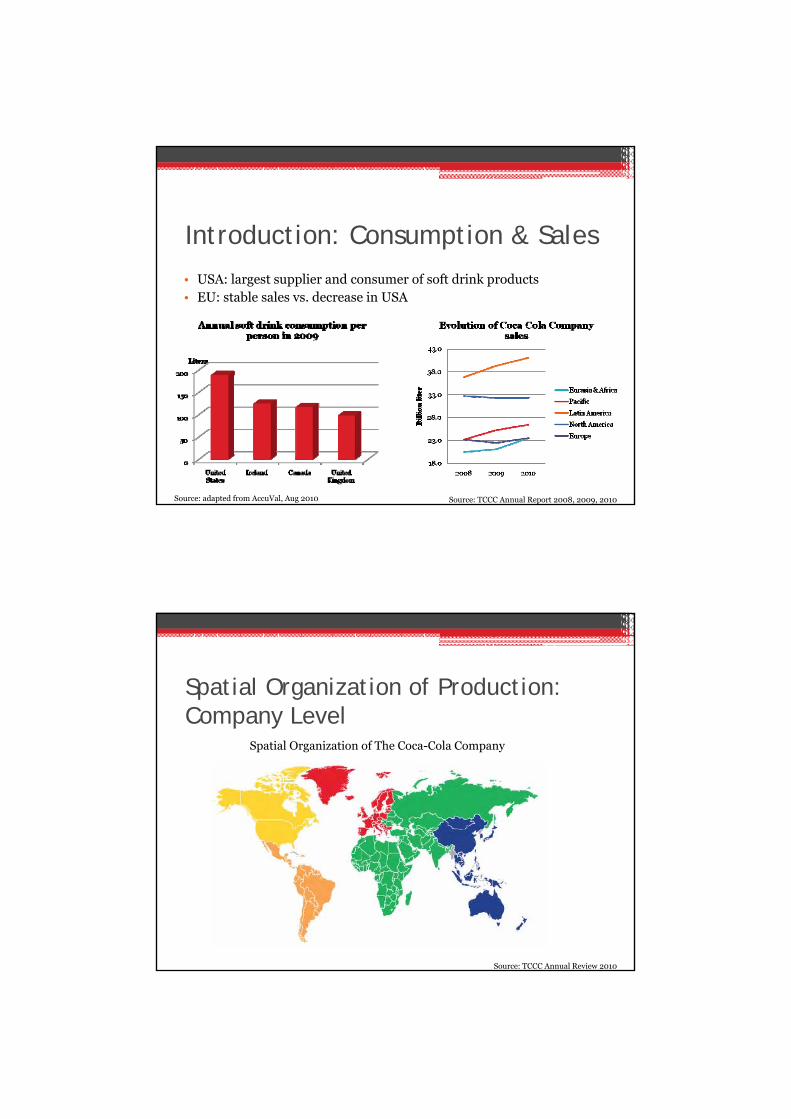

Introduction: Consumption & Sales

• USA: largest supplier and consumer of soft drink products• EU: stable sales vs. decrease in USA

Source: TCCC Annual Report 2008, 2009, 2010Source: adapted from AccuVal, Aug 2010

Spatial Organization of Production: Company Level

Spatial Organization of The Coca-Cola Company

Source: TCCC Annual Review 2010

Spatial Organization of Production: Bottlers Level

Regions covered differently by bottlers

Bottling Company Territory % of ownership% of TCCC’s

volumes

CCE North America USA, Canada 100% 18%

Coca-Cola FEMSACentral and South America

32% 10%

Coca-Cola HellenicEast Europe & Nigeria

23% 8%

Coca-Cola Amatil Pacific 30% 2%

New CCEWest and North Europe

0% 5%

Source: TCCC Annual Review 2010, TCCC Annual Report 2010

Spatial Organization of Production: European Level

Coca-Cola HellenicCoca-Cola Enterprises

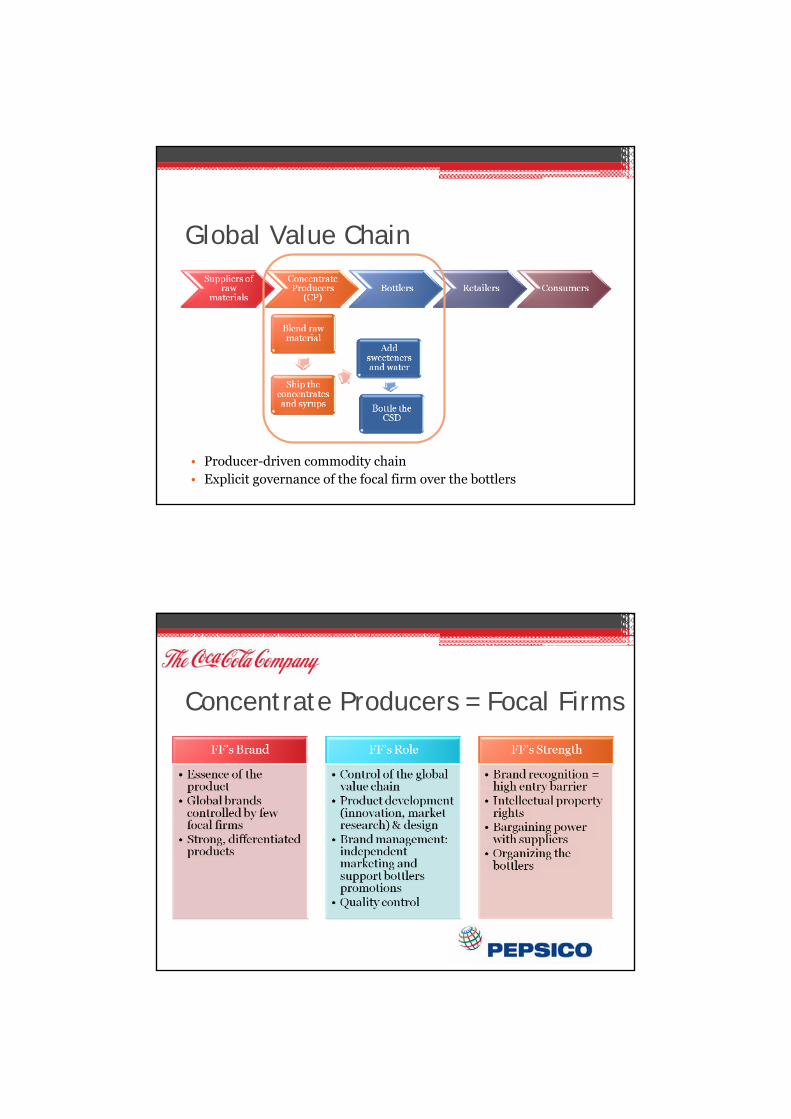

Global Value Chain

• Producer-driven commodity chain• Explicit governance of the focal firm over the bottlers

Concentrate Producers = Focal Firms

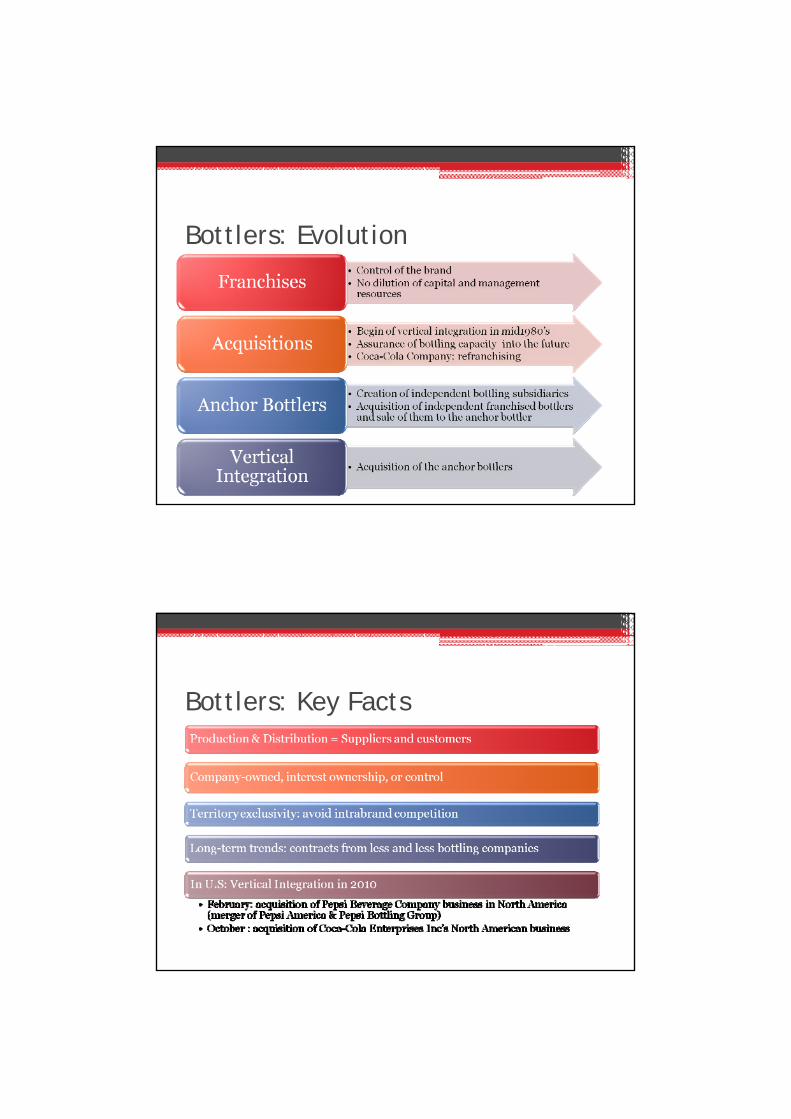

Bottlers: Evolution

Bottlers: Key Facts

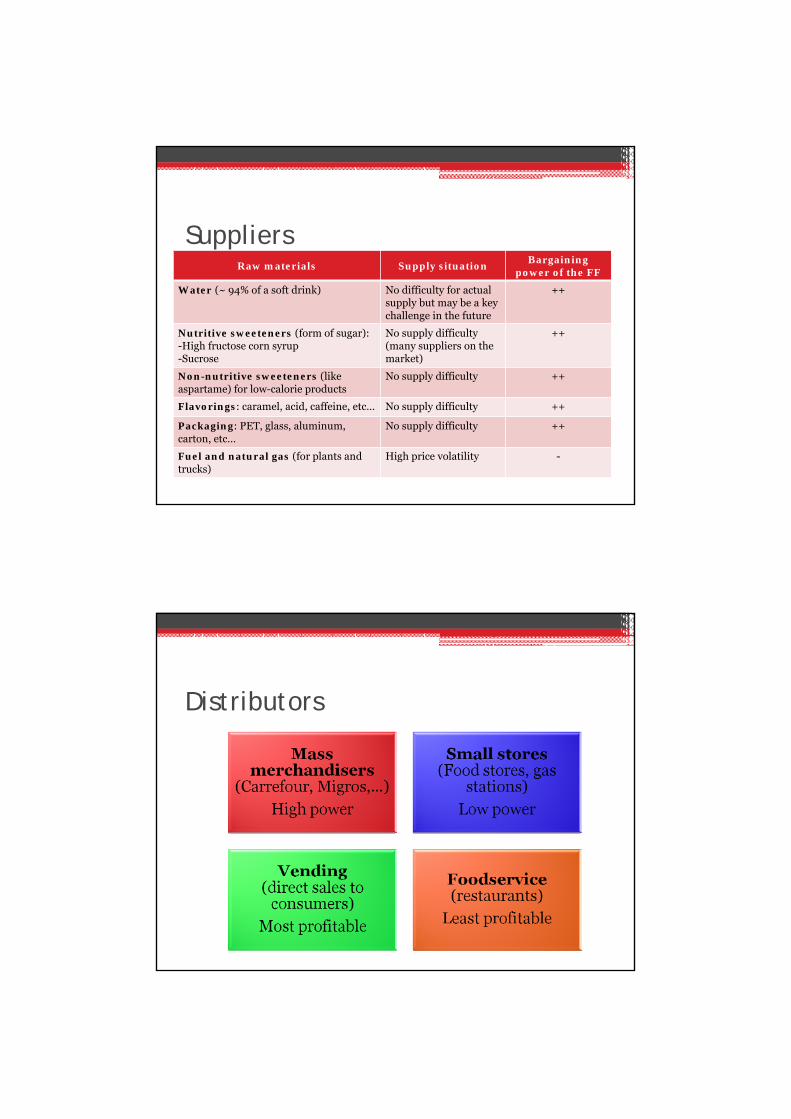

SuppliersRaw materials Supply situation

Bargaining power of the FF

Water (~ 94% of a soft drink) No difficulty for actual supply but may be a key challenge in the future

++

Nutritive sweeteners (form of sugar): -High fructose corn syrup-Sucrose

No supply difficulty (many suppliers on the market)

++

Non-nutritive sweeteners (like aspartame) for low-calorie products

No supply difficulty ++

Flavorings: caramel, acid, caffeine, etc… No supply difficulty ++

Packaging: PET, glass, aluminum, carton, etc…

No supply difficulty ++

Fuel and natural gas (for plants and trucks)

High price volatility -

Distributors

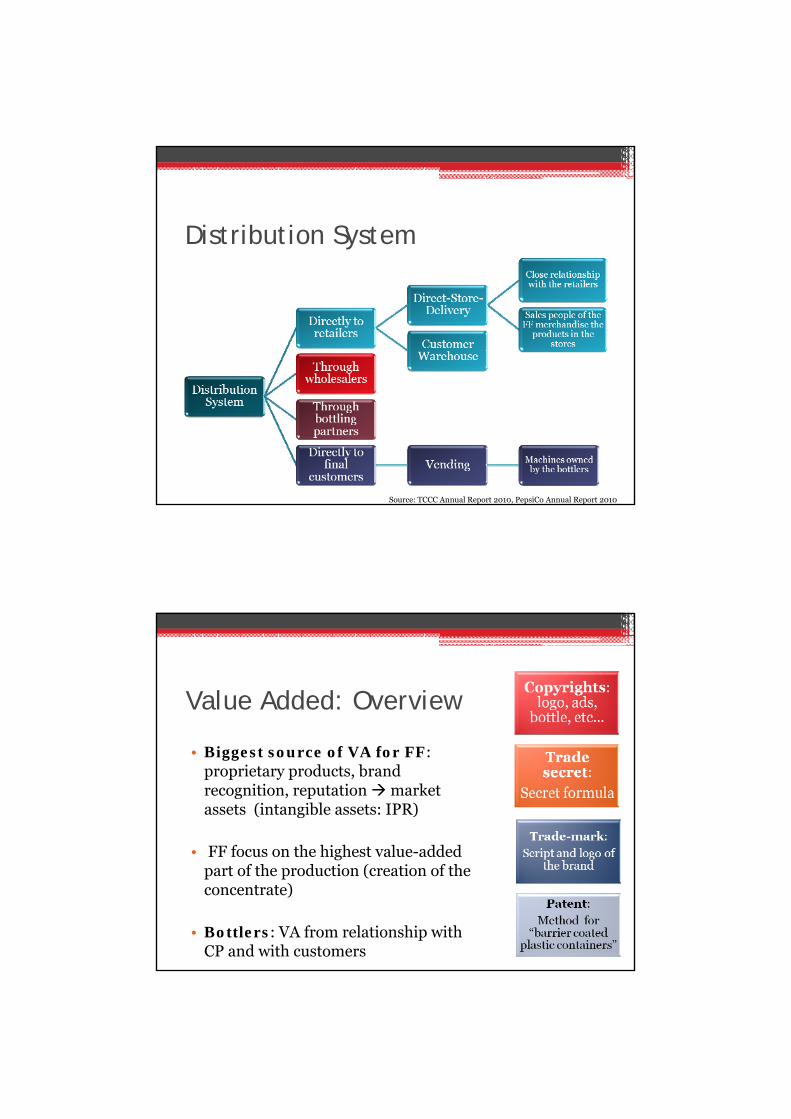

Distribution System

Source: TCCC Annual Report 2010, PepsiCo Annual Report 2010

Value Added: Overview

• Biggest source of VA for FF: proprietary products, brand recognition, reputation market assets (intangible assets: IPR)

• FF focus on the highest value-added part of the production (creation of the concentrate)

• Bottlers: VA from relationship with CP and with customers

VA: Comprehensive Income (TCCC) In millions USD 2010 %

Net operating revenues

35,119

- Cost of goods sold - 12,693 36.14% of net operating revenues

= Gross profit = 22,426

- Selling, general and administrative expenses

- 13,158 2.88%22.17%29.65%45.29%

Stock-based compensationAdvertisingBottling and distributionOther operating expenses

- Other operating charges - 819

= Operating income 8,449

Income before income taxes

14,243

Net income 11’859 33.77% of net operating revenues

Source: TCCC Annual Report 2010

VA: Calculation

Finished products% of total

salesEffective amount Value creation

Net operating revenues 49% 17,247 mio USD 0.49 USD/ liter

Cost of goods sold 36.14% 6.233 mio USD 0.18 USD / liter

Volumes 24% 34.79 billion liter

These figures include all TCCC’s products, not only Coke (impossible to indentify Coke’s sales)!

Conclusion

* Evolution of consumption of Coca-Cola products 2010 vs 2009

Thank you for your attention!

Questions?