gains and pains from contract research: a transaction cost ... · gains and pains from contract...

TRANSCRIPT

Gains and Pains from Contract Research:

A Transaction Cost and Resource-Based Perspective

Abstract

Determining the research and development (R&D) boundaries of the firm has frequently

been characterized as a major challenge for firms to secure their innovative capabilities. This

paper investigates the driving forces of external technology sourcing through contract

research based on arguments from transaction cost theory and the resource-based view of the

firm. Moreover, it relates a firm’s engagement in contract research to innovation performance

and suggests that in-house and contract R&D are complements. However, firms may ‘over-

contract’ and hence dilute the uniqueness of their resource portfolio. Using a comprehensive

data set of innovating firms from Germany our findings suggest that environmental

uncertainty, contractual experience and openness to external knowledge sources motivate the

choice for engaging in contract research activities. Moreover, we find our hypotheses on the

complementarities between in-house and contract R&D as well as on ‘over-contracting’ to be

confirmed, which generates important implications for the strategic management of

innovation.

Keywords: Contract research, innovation, transaction cost theory, resource-based view of the

firm

JEL-Classification: O32, C24

1

1 Introduction

Determining the research and development (R&D) boundaries of the firm has attracted

considerable attention in the literature because of its central role in the management of

innovation. As the institutional loci of new technology can be diverse there is a high

probability that at least from time to time firms need to source technology externally (Teece,

1986, 1992). Apart from in-house R&D, firms may choose from a multitude of options

through which they can acquire technology externally, including collaborative R&D or

strategic alliances (e.g., Cassiman and Veugelers, 2002; Belderbos et al., 2004; Villalonga and

McGahan, 2005; Rothaermel et al., 2006) and acquisitions (e.g., Cassiman et al., 2005;

Graebner, 2004). Most of the existing research has focused on aspects related to knowledge

spillovers, access to complementary knowledge, co-development or cost- and risk-sharing in

innovation projects. A third option available to the firm is the outsourcing of R&D (e.g.,

Cassiman and Veugelers, 2006; Nagarajan and Mitchell, 1998; Pisano, 1990; White, 2000).

Even though R&D, just like production, has been characterized as a core ‘high-value

function’ of the firm (Leiblein et al., 2002; Leiblein and Miller, 2003), R&D activities have

frequently become subject to outsourcing, offshoring or both (Arnold, 2000; Doh, 2005; Jahns

et al., 2006).

While offshoring refers to the relocation of R&D activities which could still be carried out

by the same firm, outsourcing implies a move beyond a firm’s boundaries to R&D

contractors. In this sense, contract research can be defined as the contractually agreed, non-

gratuitous and temporary performance of R&D tasks for a client by a legally and

economically independent contractor where the research outcomes are transferred to the client

with all specific exploitation rights upon completion of the task (Teece, 1988). Existing

research has most prominently focused on two lines of thought to explain why contract

2

research occurs. A first key argument for outsourcing R&D can be traced back to transaction

cost theory (Williamson, 1975). It suggests that an efficient governance of R&D activities is

achieved by markets unless this leads to transaction costs that exceed the costs of

organizational arrangements (Brockhoff, 1992; Cassiman and Veugelers, 2006; Gooroochurn

and Hanley, 2007; Veugelers and Cassiman, 1999). R&D cooperation, strategic alliances and

firm acquisitions lead to both transaction and organization costs as they comprise a

contractual relationship as well as the setup of organizational interfaces. In their effort to

optimize the innovation process, however, firms also need to find organizational arrangements

for those tasks which encompass virtually no interaction with partners and hence cause only

minimal organization costs. Moreover, there are tasks that can be characterized as an ‘ad-hoc

problem solving’ (Winter, 2003), i.e. they require a quick reaction on a closely contoured

research project for which time or resources are not available internally.

While transaction cost theory hence puts emphasis on the most cost efficient governance for

technology development, another argument to explain contract research has been put forward

by the resource-based view (RBV) of the firm (e.g., Wernerfelt, 1984; Barney, 1991). Given

the common belief that firms largely differ in their resource endowment and capabilities,

contract research provides an opportunity to access external resources which may be joined

with internal resources to create a unique and valuable combination (Barthélemy and Quélin,

2006; Kogut and Zander, 1992; Leiblein and Miller, 2003). In other words, in-house and

contract research are complementary activities (Cassiman and Veugelers, 2006).

Transaction cost and resource-based theory hence provide strong arguments for the ‘gains’

from contract research. Little research has been done, however, to elucidate the ‘pains’ that

come with contracting out R&D to external organizations. Contract research has been shown

to account for a substantial share of total innovation expenditure in a large number of firms

(Eurostat, 2004). Gaining a more detailed understanding of the downsides of contract research

3

will thus provide an indication whether innovation expenditures are better spent elsewhere. In

fact, in this paper we suggest that firms might ‘over-contract’ which leads to a dilution of the

firm’s resources, making them less unique, easier to imitate and, as a result, less valuable.

This ‘over-contracting’ might offset the benefits expected from complementarities between

in-house and contract research and hints at the importance of carefully balancing internal and

external technology development modes.

We aim at contributing to the literature by clarifying the role played by contract research in

a two-step approach, integrating the choice for contract research with its performance

implications. Specifically, we first study firms’ decision to engage in contract research and

then analyze the effects that this engagement has on innovation success. Like several other

studies in the field (e.g., Arnold, 2000; Mayer and Salomon, 2006; White, 2000), we make

use of the complementary character of transaction cost and resource-based theory and provide

a conceptual framework that outlines the factors influencing a firm’s propensity to engage in

contract research. Our econometric tests are based on a comprehensive data set of more than

1,000 German firms.

The remainder of this study is organized as follows: Section 2 gives a short overview of the

motivation for contracting out R&D activities, while Section 3 presents our conceptual

considerations and the hypotheses. Section 4 describes our empirical strategy to test the

hypotheses. Estimation results are presented in Section 5. We discuss our findings in Section

6. Section 7 concludes.

2 Motives for engaging in contract research

Technological change, as well as the geographic and organizational dispersion of expertise,

has led to a wide array of organizational arrangements for the generation and acquisition of

4

knowledge. Traditionally, outsourcing had been largely used for rather specialized activities

or repetitive tasks like logistics or facility management. Over time other value chain activities

closely related to the core of the firm – like R&D and production – have become subject to

outsourcing decisions as well (Leiblein et al., 2002; Leiblein and Miller, 2003). A prominent

example is the automotive industry, where a whole model series of cars could be assembled

by contract manufacturers. Contract research as the outsourcing of R&D activities basically

follows the same logic in that it is directed at exploiting certain advantages associated with the

nature and purpose of contract research organizations, whether they may be private firms,

universities or research centers. The idea of contracting research to external firms or research

institutes is not new. In fact, the consulting firm Arthur D. Little roots back to the year 1886

with the offering of “investigations for the improvement of processes and the perfection of

products” (Kahn, 1986). Several potential benefits for firms engaging in contract research can

be identified.

A first group of advantages centers on a reduction of costs compared to the same R&D

activities being performed in-house. Cost advantages may be achieved by specialization of the

contract research organization or by cost sharing in a joint commissioning of more than one

client. Moreover, fixed costs may be reduced and R&D time and budgets better controlled

(Tapon and Thong, 1999). Apart from cost aspects, quality advantages through contract

research may be possible since the contract research organizations can employ specialized

know-how, equipment and infrastructure. Using external sources may also foster creativity

within internal R&D since new research methods and perspectives are brought in. Another

advantage of contract research relates to timing issues and the undivided attention that the

project may receive by the contractor. This can especially be important if the outcontracting

firm tries to catch up with competitors in an area of technology where no or little competence

is available internally (Tapon and Cadsby, 1994). Firms may also choose to deliberately

5

install competition to stimulate internal R&D. Such forms of competition may also prove to

be helpful in overcoming internal resistance to innovation projects. Finally, firms may get

access to public R&D funding more easily when they involve public contract research

organizations like universities or research institutes (David and Hall, 2000) or when the R&D

activities are carried out in particular regions (Tapon and Cadsby, 1994).

Despite these ‘gains’ there are also several ‘pains’ associated with the external provision of

R&D services: intellectual property rights (IPR) as a result of such activities might be difficult

to allocate. Moreover, the contractual relationship involves information asymmetries in that

potential contractors might lack the required expertise they declared to deliver (Love and

Roper, 2002). Contracting firms may also encounter considerable steering, controlling and

confidentiality problems associated with the contracted research. They lose the opportunity to

learn which leads to a situation where firms may critically depend on the contract research

organization. Likewise, contract research might trigger a ‘not invented here’ syndrome which

may lead to a reluctance of in-house R&D to adopt external technology (Katz and Allen,

1982; Veugelers and Cassiman, 1999). Contracting out those R&D projects that appear to be

of high strategic relevance hence constitutes a risky strategy. Using a transaction cost

framework, Teece (1988) consequently explains the reluctance of firms to rely heavily on

external knowledge with contractual uncertainty, cumulative knowledge acquisition and a

limited transferability of research outcomes. Similar arguments are put forward by Pisano

(1990) and Brockhoff (1992). After all, knowledge produced by a contract research

organization might not be unique since potential competitors may equally benefit from the

organization’s expertise. Unique knowledge, however, has been characterized as the most

important asset of the firm for achieving competitive advantage (Grant, 1996). Moreover,

Kotabe (1990) finds that firms may lose relevant manufacturing process knowledge which

6

may cost the firm the opportunity to improve their manufacturing technology in a rapidly

changing technological environment.

According to the above mentioned arguments for and against contract research, transaction

cost theory suggests that markets are more efficient than hierarchies unless the costs of

transacting with contract research organizations make the relationship less favorable. In this

respect, firms facing a given set of transactional attributes will in equilibrium reach the same

conclusion regarding the governance mode of their R&D activities. Several examples,

however, show that this proposition does not hold in the real world, for example in the fashion

industry, where some firms rely on a vertically integrated structure while other firms confine

themselves to design and marketing activities. Instead, a firm’s specific history, existing

portfolio of transactions as well as other firm-specific assets and capabilities could exert a

substantial influence on the decision to outsource R&D activities (Leiblein and Miller, 2003).

Mayer and Salomon (2006), for example, find that technological capabilities as well as

contractual hazards play a role in explaining outsourcing decisions. In fact, the RBV of the

firm provides an instrument to investigate the effect of firm capabilities on outsourcing

decisions (Barney, 1991; Barthélemy and Quélin, 2006; Leiblein and Miller, 2003; Mayer and

Salomon, 2006). The following section hence adopts a transaction and resource-based

perspective to determine factors that lead firms to actually engage in contract research. The

analysis then focuses on the question of how contract research translates into innovation

success.

7

3 Conceptual framework

3.1 Contract research in the light of transaction cost theory

A large body of literature has successfully employed transaction cost economics to describe

how the conditions of contractual relationships affect the optimal form of organization (e.g.,

Barthélemy and Quélin, 2006; Leiblein and Miller, 2003; Leiblein et al., 2002; Robbertson

and Gatignon, 1998). Transaction cost theory suggests that it is the cost associated with the

governance of such relations which is central to determining the choice for a particular form

of coordination of a transaction (Klein et al., 1978; Williamson, 1979). Hence, a firm will

select the form of coordination that is associated with the lowest level of cost (given the return

to the respective activity). Regarding the sourcing of technology, the choice is typically

between ‘market’, resulting in transaction costs, and ‘hierarchy’, resulting in organization

costs. In other words, firms choose between buying a technology at the market for research

services and performing the required R&D activities in-house. The resulting trade-offs

between internalizing and outsourcing firm activities have been analyzed in various settings

(e.g., Leiblein et al., 2002; Walker and Weber, 1984). Aside from these two poles, ‘hybrid’

forms of governance such as cooperative R&D arrangements or R&D alliances have been

widely used by firms (e.g., Belderbos et al., 2004; Brockhoff, 1992; Cassiman and Veugelers,

2002; Pisano, 1990). However, the setup of organizational interfaces in R&D cooperation

incurs organization costs. These need to be balanced with an entirely external provision of

R&D services through contract research which minimizes organization costs.

Due to the benefits of specialization in the marketplace, applications of transaction cost

theory generally assume that markets represent a more efficient governance mode than

hierarchy (Leiblein and Miller, 2003). There are situations, however, in which the costs of

market exchange may surpass the technical efficiencies of the market. More specifically,

8

contract research incurs costs to negotiate and write the contract as well as costs to monitor

and enforce the contractual performance (Williamson, 1975). Transaction cost theory hence

focuses on the identification of exchange characteristics that would be best reflected in a

market, hybrid or hierarchical organization. While transaction cost theory provides a useful

reference to study contractual relations, recent research has emphasized the simultaneous

adoption of alternative governance modes for R&D (e.g., Cassiman and Veugelers, 2006;

Lokshin et al., 2008; Veugelers and Cassiman, 1999; White, 2000). In other words, instead of

‘make or buy’, firms typically rely on ‘make and buy’ and even ‘make, collaborate and buy’,

depending on the specifics of the innovation project. Thus, the arguments raised in the

following have to be understood as an indication that contract research becomes more or less

likely at the firm level. It is not our intention to position contract research as an alternative to

other technology sourcing modes.

Adopting a rather abstract level of explanation, the two main factors driving the analysis

have been identified as uncertainty and asset specificity (Barthélemy and Quélin, 2006;

Williamson, 1985): transaction costs increase with increasing uncertainty and the necessity to

rely on transaction-specific assets (Englander, 1988; Williamson, 1979). In combination with

bounded rationality and opportunism, these attributes or dimensions hence largely determine

the transaction costs associated with contractual research arrangements (Brockhoff, 1992).

Uncertainty

Uncertainty in the present setting describes the degree to which unforeseen environmental

changes may influence and alter the conditions underlying a contractual arrangement

(Leiblein and Miller, 2003). Uncertainty raises transaction costs through a number of

channels. First, a higher number of expected contingencies raise the effort to set up and

enforce a contract. Second, uncertainty decreases the ability to assess the contribution of any

9

individual activity which in turn increases the risk of shirking (Demsetz, 1988). The impact of

an uncertain technology environment on the innovation process is widely acknowledged (e.g.,

Jansen et al., 2006; Miller and Friesen, 1983). Uncertainty about the technology employed in

an innovation project may be high when technological change is rapid, as it is related to two

fundamental risks in innovation: strategic blind spots and ‘betting on the wrong horse’. As a

result, a firm might suffer from technological lock-in effects. Moreover, uncertainty increases

when products and services together with their underlying technologies become obsolete fast,

i.e. they have a short product life cycle and the firm may be uncertain about potential

successor products or services. Uncertainty also increases when there is a high threat from

substitutability of the own product by competitor products as in this case the firm might not

be able to appropriate the returns from investments into contract research. Thus, the higher the

perceived environmental uncertainty the higher the transaction costs turn out to be and the

less likely the choice of contract research becomes. Our first hypothesis can be stated as:

Hypothesis 1: Environmental uncertainty increases transaction costs and thereby reduces the

propensity to engage in contract research.

Specificity of assets

The second driving factor of transaction costs is the specificity of assets employed in the

contractual relationship. It defines the degree to which the assets in a contractual research

arrangement are more valuable in their current application than in their second best use

(Leiblein and Miller, 2003). High levels of specific assets create opportunities for an

appropriation or ‘hold-up’ of quasi-rents by opportunistic contractors. The suppliers of

research services may be subject to a hold-up situation when the contracted research requires

buyer-specific investments resulting in few alternatives for the supplier (Williamson, 1985).

This will in turn motivate a more complex negotiation and a higher level of contractual

10

safeguards. Moreover, by deterring investments in other efficiency-improving assets fewer

opportunities for the appropriation of quasi-rents arise. In this context, Williamson (1979)

puts particular emphasis on ‘physical asset specificity’ and ‘human asset specificity’. With

respect to the innovation process, specificity increases with the extent to which in-house R&D

activities are specialized and related assets are focused on one or a few products as the main

outcomes of the R&D process. In this case, costly investments in physical and human assets

are required by the contract research organization to establish a productive relationship. As

these specific assets may not be easily used in other projects, contract research organizations

will presumably be reluctant to invest in them which in turn raises transaction costs. Our

second hypothesis hence reads:

Hypothesis 2: Specificity of assets increases transaction costs and thereby reduces the

propensity to engage in contract research.

While providing valuable insights, it has to be recognized that transaction cost economics

makes rather restrictive assumptions leading to some implications which cannot be justified in

reality. In this respect, we have outlined that differences in a firm’s R&D resource

endowment might influence the boundary decision to create valuable firm-specific

knowledge. Hence, the next section complements the arguments derived from transaction cost

economics by adopting a resource-based perspective.

3.2 Contract research in the light of resource-based theory

The RBV of the firm has frequently been used to study the effect of firm capabilities on

outsourcing decisions (Leiblein and Miller, 2003; Barthélemy and Quélin, 2006). Capabilities

are organizational processes which bundle strategic resources into unique combinations and

constitute superior performance themselves (Eisenhardt and Martin, 2000). This follows the

basic rationale that competitive advantage does not only arise from the possession of strategic

11

resources but also from the way in which they are used (Penrose, 1959). Two main aspects

have been put forward by the RBV. First, firms are heterogeneous with respect to their

resource and capability endowment. Second, valuable resources and capabilities are limited in

supply. Their creation is expensive and involves causal ambiguities (e.g., Barney, 1991).

Complementary to transaction cost theory which emphasizes the cost incurred by contractual

relationships, the RBV centers on the search for competitive advantage that stems from an

exploitation of unique firm attributes and R&D governance modes. Consequently, firms will

strive to choose the governance mode that leverages the value of existing capabilities or that

complements capabilities in a way that knowledge gaps can be bridged (Leiblein and Miller,

2003). This implies that firms need to be open to externally available knowledge resources.

Generally speaking, any firm-specific resource and capability may influence a firm’s

boundary decision in R&D. However, the RBV argues that particularly those activities are

carried out in-house where the firm possesses valuable and difficult-to-imitate capabilities

(White, 2000). Zollo and Winter (2002) describe the acquisition of such capabilities as a

continuous and deliberate learning process. This process depicts a firm’s systematic methods

for a modification of its operating routines. Such routines constitute stable patterns of

organizational behavior and reaction to internal or external stimuli (Nelson and Winter, 1982).

As a consequence, this process explains why some firms are over time more effective in

implementing specific governance structures than others. The two driving factors of the

analysis hence center on the concepts of contractual experience as well as openness to

external knowledge.

Contractual experience

At first glance, recurring transactions with R&D contractors have a direct influence on

transaction costs. Firms need to enter into contracts several times which requires negotiating

12

efforts and a constant monitoring of the relationships. Over time, however, firms should be

able to learn, to modify operating routines and, as a consequence, find efficient contractual

arrangements to deal with an increasing number of recurring transactions. In fact, relatively

high one-time costs upon establishment of a contractual relationship should enable firms to

economize on later transactions since possible sources of conflict can be foreseen and avoided

(Brockhoff, 1992). Moreover, firms may differ in their ability to select suitable contract

research organizations as well as to negotiate and monitor the contract (Leiblein and Miller,

2003). Those firms that have developed a refined contracting experience are presumably

particularly inclined to engage in outsourcing activities. In this respect, recurring transactions

foster a common understanding of routines, cultures, systems, and other firm characteristics

(e.g. Gulati and Singh, 1998) as they lead to the development of relational capabilities (Dyer

and Singh, 1998). Mayer and Argyres (2004) found that over time firms learn how to contract.

They are able to retain contracts as ‘repositories for knowledge’ of how contractual

relationships should be shaped. Contracting experience hence supports the development of

organizational routines directed at an efficient collaboration with a variety of partners

(Leiblein and Miller, 2003). As a consequence, firms should be more likely to engage in

contract research. Our third hypothesis therefore is:

Hypothesis 3: Prior experience with contract research increases the propensity to engage in

contract research.

Openness to external knowledge

The RBV has made it clear that unique knowledge resources are the most valuable assets of

a firm for achieving competitive advantage (Grant, 1996; Liebeskind, 1996). Knowledge is

crucial for firm success as it provides a platform for decisions on what resources and

capabilities to deploy, develop or discard as the environment changes (Ndofor and Levitas,

13

2004). In this respect, recent literature has pointed at the merits of acquiring external

knowledge (Tsang, 2000) and moving from ‘research and develop’ towards ‘connect and

develop’ (Huston and Sakkab, 2006). The ‘open innovation’ model by Chesbrough (2003)

extends this perspective on how firms innovate. Firms following an open innovation approach

can hence be ascribed openness to external knowledge (Laursen and Salter, 2006; Tether and

Tajar, 2008). In this respect, shorter product life cycles as well as the growing complexity of

technologies and markets motivate firms to use external sources of knowledge. Moreover,

external sources have become more readily available as information and communication

technologies have improved. Being open in the innovation process should therefore trigger the

adoption of external knowledge and motivate firms to reach out to external actors. As a

consequence, openness should be reflected in a higher propensity to engage in contract

research. Our fourth hypothesis hence is:

Hypothesis 4: Openness to external knowledge increases the propensity to engage in contract

research.

3.3 Contract research and innovation performance

The effects from incorporating external knowledge from customers, suppliers, competitors

or universities into the innovation process have received considerable attention in the

literature. Such effects range from higher innovation success (Gemünden et al., 1992; Laursen

and Salter, 2006; Love and Roper, 2004) to an increased novelty of innovations (Landry and

Amara, 2002) as well as higher returns to R&D investments (Nadiri, 1993). While Lokshin et

al. (2008) study the effects from external R&D on labor productivity, relatively little is known

about the relationship between contract research and innovation performance, for example in

terms of new products introduced in the market. Cassiman and Veugelers (2006) provide the

only empirical evidence so far for the performance effect of several types of external R&D,

14

including outsourced R&D. Moreover, they find that internal and external R&D are

complements. While Cassiman and Veugelers (2006) can substantiate complementarity, they

can only do so on the rather abstract level of whether a particular make and/or buy strategy

had been chosen by the firm. Extending this perspective, innovation performance should,

however, to a substantial degree depend on the actual scale of outsourced R&D compared to

in-house R&D and other types of innovation activities. We have argued before that contract

research does not only result in ‘gains’ but also in ‘pains’. In this sense, firms might ‘over-

contract’ with contract research organizations which could be detrimental to innovation

performance. In the following, we attempt to clarify the complex relationship between

contract research and innovation performance by focusing on the two aspects of

complementarity in technology sourcing modes and ‘over-contracting’.

Complementarity in technology sourcing modes

Innovation outputs, i.e. new products or services that can be commercialized, require inputs

into the innovation process (e.g. Griliches and Mairesse, 1984). If complementarities exist

between in-house and contract research, combining both technology sourcing modes has a

more positive impact on innovation performance than spending on one activity only, even if

total expenditures are the same in both cases (Cassiman and Veugelers, 2006). In the effort to

optimize the innovation process, contract research might for example be an efficient way for

handling ad-hoc problems and for saving organization costs. In fact, the literature has pointed

at the importance of timing in innovation activities in the context of first mover and follower

advantages (e.g., Jensen, 2003; Lieberman and Montgomery, 1988; Shankar et al., 1998).

Obviously, the purchase of external R&D services through contract research is often easier

and faster to establish than other external knowledge sourcing, for example through R&D

collaborations. Thus, contract research can be a superior sourcing mode when a timely

reaction to a closely contoured research project is required. Resulting efficiency gains should

15

consequently lead to better innovation performance. It has to be acknowledged, however, that

being a good ‘buyer’ also requires being a good ‘maker’ (Cassiman and Veugelers, 2006;

Radnor, 1991; Veugelers and Cassiman, 1999). In other words, the absorptive capacities of

the firm come into play when complementarities between in-house and contract research are

to be realized (Cohen and Levinthal, 1989, 1990).

Absorptive capacity basically comprises a set of organizational routines (Zahra and George,

2002). It has three major components: the identification of valuable knowledge in the

environment, its assimilation into existing knowledge stocks and the final exploitation for

successful innovation. These continuous learning engagements increase the awareness for

market and technology trends, which can be translated into pre-emptive actions. Absorptive

capacity provides firms with a richer set of diverse knowledge which gives them more options

for solving problems and reacting to environmental change (Bowman and Hurry, 1993;

March, 1991). As a result, absorptive capacity enables firms to predict future developments

more accurately (Cohen and Levinthal, 1994). Cohen and Levinthal (1989, 1990) have argued

that absorptive capacity is closely linked to performing internal R&D activities. However,

some authors have defined it more broadly as a dynamic capability that refocuses a firm’s

knowledge base through iterative learning processes (Szulanski, 1996; Zahra and George,

2002). In effect, absorptive capacity enables firms to find and recognize relevant external

knowledge sources so that it can be combined, i.e. assimilated, with existing knowledge

(Todorova and Durisin, 2007). From this it follows that the effectiveness of contract research

critically depends on the firm’s in-house R&D capacity (Chatterji, 1996). Consequently, we

hypothesize that there is a complementary effect between in-house R&D and contract

research:

Hypothesis 5: There is a complementary relationship between in-house R&D and contract

research.

16

Over-contracting and resource dilution

Although we have argued that contract research is associated with higher innovation

performance, we also expect that firms might in fact ‘over-contract’. On the one hand, our

logic of ‘over-contracting’ follows the arguments provided by Katila and Ahuja (2002) as

well as Laursen and Salter (2006) who find that firms might ‘over-search’ their environment

for potential innovation impulses. In this respect, firms might be confronted with complex

external knowledge coming in from the contract research organization that needs to be

managed and absorbed despite a lack of internal absorptive capacity. Managerial attention is

needed to cope with the contractual relationships which could lead to neglecting other

relevant innovation activities (Ocasio, 1997).

On the other hand, building a competitive strategy around external knowledge is

challenging. Knowledge is by its very nature a public good that may ‘spill over’ to

competitors (Jaffe, 1986). Hence, knowledge from contract research organizations hardly

qualifies as a unique resource (Liebeskind, 1996). In order for knowledge resources to

become highly valuable, they need to be scarce, constitute a unique combination of external

and internal knowledge or be co-specialized with other assets of the firm (Teece, 1986).

Moreover, unique knowledge resources are difficult to imitate so that they can be exploited

for a period of time. In this respect, Kogut and Zander (1992) refer to ‘combinative

capabilities’ that serve to acquire and synthesize knowledge resources leading to new

applications from these resources. Using too much external knowledge resources hence

implies using resources that are probably not unique and not difficult to imitate. As a

consequence, there should be a diluting effect on the uniqueness of the firm’s own resource

base. In other words, resource dilution refers to the fact that a firm’s resources become less

unique and hence valuable the more rather generic external knowledge is incorporated. This

resource dilution argument suggests that there is a point at which contract research becomes

17

disadvantageous. Contract research in this sense extends and enhances the value of a firm’s

capabilities only if the firm succeeds in acquiring external knowledge and combining it with

internal knowledge to create new and unique knowledge resources. As a consequence, our last

hypothesis is:

Hypothesis 6: The relationship between contract research and innovation performance is

inversely U-shaped.

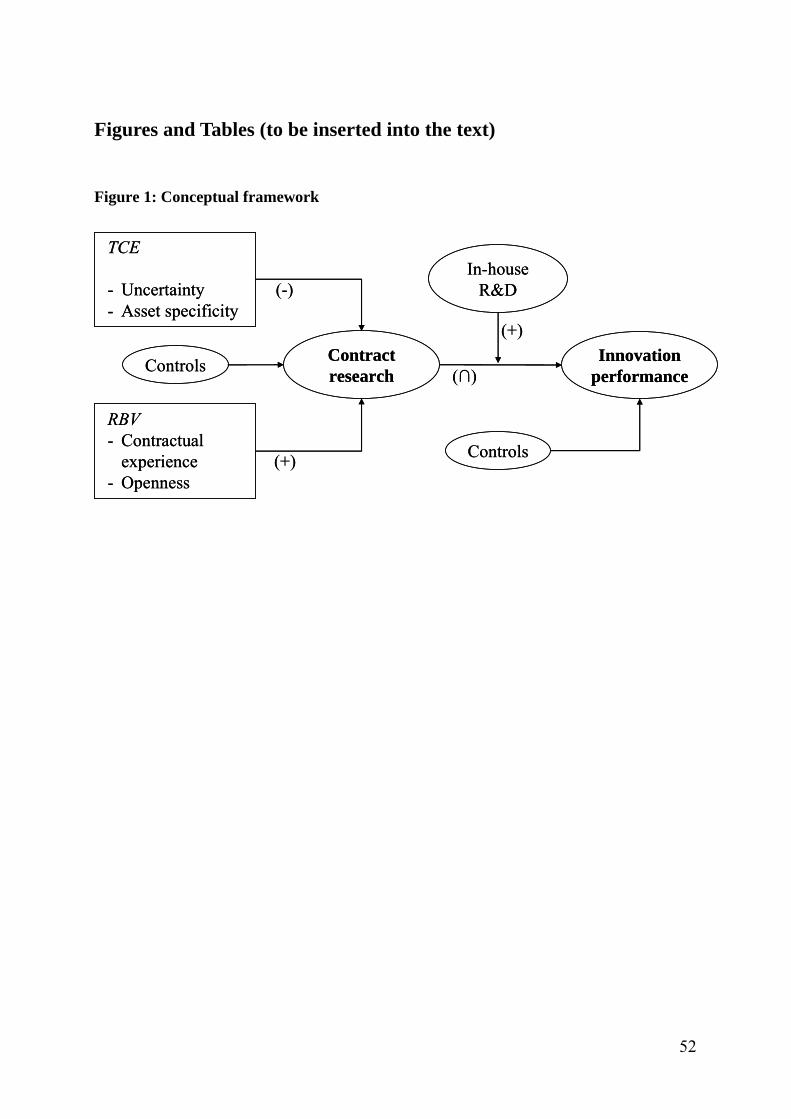

Figure 1 summarizes our theoretical considerations regarding both the transaction cost and

the resource-based factors influencing the decision to engage in contract research activities:

an increase in environmental uncertainty and asset specificity both increase transaction costs,

which in turn makes contract research less likely. In contrast, an increase in contractual

experience and openness to external knowledge both lead to an increase in the probability of

contract research. In a second step, contract research is hypothesized to have a complementary

relationship with in-house R&D for achieving innovation performance. Moreover, the logic of

‘over-contracting’ points at an inversely U-shaped relationship between contract research and

innovation performance. Both the outsourcing decision and innovation performance are

influenced by control variables.

--------------------------------

Insert Figure 1 about here

--------------------------------

18

4 Methods

4.1 Data

We use cross-sectional data from the German part of the fourth European Union’s

Community Innovation Survey (CIS-4) conducted in 2005 to test our hypotheses. The survey

is conducted annually by the Centre for European Economic Research (ZEW) on behalf of the

German Federal Ministry of Education and Research. It is designed as a panel survey

(Mannheim Innovation Panel, MIP) starting in 1993. The methodology and questionnaires

used by the survey, which is targeted at enterprises with at least five employees, complies

with the harmonized survey methodology prepared by Eurostat for CIS surveys. The 2005

survey collected data on the innovation activities of enterprises during the three-year period

2002-2004. About 5,200 firms in manufacturing and services responded to the German survey

and provided information on their innovation activities. We use this data to measure the

concepts presented above.

We use the 2005 wave of the MIP even though the MIP is a panel data set which in

principle allows us to control for unobserved firm-specific fixed effects. There are two

reasons why we use the 2005 wave only: (i) many variables central to our analysis were solely

collected in the 2005 survey and (ii) the MIP data is highly unbalanced, i.e. many firms

participate infrequently which does not help handling unobserved firm heterogeneity.

Nevertheless, the panel structure is exploited for our concept of contractual experience which

is presented in more detail below. CIS surveys are self-reported and largely qualitative which

raises quality issues with regards to administration, non-response and response accuracy (for a

discussion see Criscuolo et al., 2005). First, our CIS survey was administered via mail which

prevents certain shortcomings and biases arising in telephone interviews (for a discussion see

Bertrand and Mullainathan, 2001). The multinational application of CIS surveys adds extra

19

layers of quality management and assurance. CIS surveys are subject to extensive pre-testing

and piloting in various countries, industries and firms with regards to interpretability,

reliability and validity (Laursen and Salter, 2006; Tether and Tajar, 2008). Second, a

comprehensive non-response analysis of the German survey for more than 4,200 firms did not

indicate systematic distortions between responding and non-responding firms with respect to

their innovation activities (Rammer et al., 2005). In conclusion, the major advantages of CIS

surveys are that they provide direct, importance-weighted measures. On the downside, this

information is self-reported. Heads of R&D departments or innovation management are asked

directly if and how their company was able to generate innovations. This immediate

information on processes and outputs can complement traditional measures for innovation

such as patents (Kaiser, 2002; Laursen and Salter, 2006; Tether and Tajar, 2008).

We restrict the sample to firms with innovation activities and in particular to those with

product innovations. This restriction is necessary as most of our measures are based on

questionnaire items only answered by firms with product innovations.1 In total, we collected

1,156 observations without missing values for the decision to engage in contract research and

1,493 observations for the product innovation success equation.2

4.2 Measures

We use different measures in the models for the decision to engage in contract research and

for the implications of that choice for innovation performance. The questionnaire items for the

more complex measures in the choice model are listed in Table A-4 in the Appendix.

1 In a robustness check described in Subsection 4.3 we explicitly account for sample selection but find that our main estimation results remain qualitatively and quantitatively unchanged. 2 The difference in the number of observations is due to missing values in the explanatory variables, in particular lagged contract research experience.

20

Choice model

Dependent variable. We use a dummy variable indicating whether or not contract research

is used by the firm. Contract research organizations could be either private firms or

universities and other public research centers.

Uncertainty. A variety of measures for uncertainty has been identified in the literature (e.g.,

Leiblein and Miller, 2003). We will particularly focus on the impact of an uncertain

technology environment on the innovation process (e.g., Jansen et al., 2006; Miller and

Friesen, 1983). Uncertainty regarding the technology employed in an innovation project may

be high when the technological change is rapid or when products and services as well as their

underlying technologies become obsolete fast. Our measure for uncertainty is generated by a

factor analysis of two variables measuring whether or not technological change is rapid and

products and services become obsolete fast. Both variables are measured on a four-point

Likert scale. The scale reliability coefficient (Cronbach’s alpha) is 0.736. Our measure for the

uncertainty of the technology environment can hence be regarded as satisfactory and should

carry a negative sign in the model estimation according to Hypothesis 1.

Asset specificity. Various forms of specific assets have been analyzed in the literature,

ranging from customized physical assets to human capital. Specificity arises when these assets

are tailored to a specific need (Williamson, 1979). In a contract research relationship this may

involve the establishment of certain facilities, infrastructure and R&D teams for both

contracting partners. Respondents to the questionnaire were asked to indicate the product or

line of products that generates most of the sales. Moreover, they were asked to indicate the

share of sales that results from this particular product (line). We expect this share of sales to

be a reliable measure for asset specificity as it indicates the extent to which R&D activities,

human and physical assets, are focused on one particular product (line). The higher the degree

21

of specialization the lower the opportunities will be to use the assets for a different purpose.

The variable should therefore have a negative impact on the propensity to engage in contract

research activities as proposed by Hypothesis 2.

Contractual experience. We measure the contractual experience of a firm by accounting for

past engagements in contract research. Our measure is a dummy variable that is coded 1 if a

firm engaged in contract research in the period 1998 to 2003. The data we use is gathered

from three waves of the MIP conducted in 2001, 2003 and 2004 and merged with the MIP

data from 2005. We expect the coefficient of this measure to carry a positive sign as argued in

Hypothesis 3. A drawback of using additional data from previous years is that we encounter a

substantial decrease in the number of observations.

Openness. We follow Laursen and Salter (2006) as well as Tether and Tajar (2008) and

measure openness as the breadth of external innovation impulses used by the firm.

Respondents to the questionnaire were asked to indicate the importance of nine different

external sources for innovation impulses. These options include suppliers, customers,

competitors, consultancies, universities, public research institutions, conferences, scientific

journals and trade associations. All variables are measured on a four-point Likert scale from

0=not used to 3=highly important. Breadth is measured as the number of different sources

used (from 0 to 9), i.e. the number of variables that received at least a value of 1. We expect

our measure for openness to have a positive impact on the probability of engaging in contract

research as stated by Hypothesis 4.

Innovation performance model

Dependent variable. For the performance model we use the share of sales with products new

to the market as a dependent variable. The measure has frequently been used by related

studies in the field (e.g., Cassiman and Veugelers, 2006; Laursen and Salter, 2006; Tether and

22

Tajar, 2008). It provides direct information on the success of commercializing the firm’s

inventions and can thus be regarded as a success measure superior to patents since these

constitute an intermediary output of R&D activities.

Innovation inputs. We measure the extent to which firms are committed to in-house R&D

and contract research by using the investments into these activities. Both figures are part of

the total innovation expenditures of the firm as defined by the Oslo Manual of the OECD

(2005). Innovation expenditures that do not relate to either in-house or contract research

define the reference category. This refers, for example, to the expenditure for other external

knowledge, i.e. for the acquisition of patents or licensing-in of patents, the expenditure for

innovation-related investments, i.e. machinery, equipment or software, plus other innovation

related expenditure (marketing, testing, etc.). All variables are divided by total innovation

expenditure to yield a size-independent pattern of characteristic innovation inputs.

We estimate three different models to explain innovation success: first, a baseline model

(‘Model 1’) where we just include the linear terms for expenditures on in-house and on

contract research. Second, we augment our baseline specification by adding an interaction

term between the expenditure for in-house and contract research to test for complementarities

as stated by Hypothesis 5 (‘Model 2’). A statistically significant positive coefficient of the

interaction term indicates complementarities between the two innovation strategies. Third, we

extent our baseline model by including a squared term for contract research expenditure to

test Hypothesis 6 on ‘over-contracting’ (‘Model 3’).

Control variables

We control for a number of other factors that might be relevant in the two models. The first

model for the decision to engage in contract research controls for the absorptive capacity of

the firm. As absorptive capacities are closely related to in-house R&D activities we capture

23

their effects, in line with the literature (Cohen and Levinthal, 1990; Rothwell and Dodgson,

1991), through in-house R&D expenditures. The distribution of R&D expenditures is highly

skewed so that we take the natural logarithm of R&D expenditures. Since many firms do not

spend anything on R&D, taking logarithms is inappropriate for non-R&D spenders because it

generates missing values. In order to account for this discontinuity, we set the natural

logarithm for non-spenders to 0 and include a second variable to account for the difference

between R&D spenders and non-spenders. This variable is coded 1 if the respective firm has

positive R&D expenditures and 0 otherwise. That way, we can explicitly distinguish between

firms that invest in R&D and firms that do not. Moreover, we include a squared term of the

logarithm of R&D expenditure to allow for non-linearities. We also control whether the firm

had reported any type of innovation collaboration by including a dummy variable that is

coded 1 if the firm engaged in innovation collaboration and 0 otherwise. The questionnaire

lists suppliers, customers, competitors, consulting firms, universities or research centers as

potential partners in innovation cooperation. Finally, we control for regional differences

between East and West Germany, for firm size (number of employees in logs and in squared

terms to allow for non-linearities) and for industry effects (see Appendix A for details). Our

second model for the performance relationship includes control variables for regional

differences, firm size and industry effects.

4.3 Econometric models

Model choice

We estimate two equations: a probit model for the decision to contract out R&D and a tobit

model for innovation success. Modeling the choice for contract research by a probit model

follows other authors who have employed binary choice models to assess the effect of a set of

covariates on the make-or-buy decision (e.g., Leiblein and Miller, 2003; Silverman et al.,

24

1997;). We use a tobit model to analyze innovation success since our measure for innovation

success is heavily left-censored as many firms do not have any market novelties and thus no

sales from this type of innovation. Tobit models adequately account for this specific feature of

our data by treating firms without market novelties differently from firms with market

novelties.

In contrast to OLS models, the coefficient estimates in probit and tobit models do not

directly translate into marginal effects, which is why we present our estimation results both in

terms of coefficient estimates and marginal effects. Marginal effects refer to the absolute

change in the dependent variable due to a one unit change in the explanatory variable.

Appendix B presents technical details of the two econometric models we estimate and also

discusses the calculation of the associated marginal effects. The marginal effects that our

models generate are firm-specific which is why we present marginal effects at the means of

the variables involved in the estimations.

Robustness checks

Manufacturing and services. Although our models control for industry differences,

manufacturing and services industries are lumped together in our main empirical analysis and

it is obviously questionable if results that hold for manufacturing also apply to services and

vice versa. We run separate regressions for each sector in order to investigate if combining

both sectors is appropriate.

Sample selection. The results presented in the choice model for contract research may be

subject to sample selection since they refer to innovating firms only. In a strict sense, this

implies that our results may not carry over to non-innovating firms which very well might

also invest into contract research. Hence, we re-estimate our regression and apply a

parametric correction for sample selection (Heckman, 1979), i.e. the model includes a

25

correction term (‘inverse of Mill’s ratio’). More precisely, Heckman (1979) proposes a two-

step estimator, where a selection equation is estimated in a first step and the equation of

interest is estimated in a second step, now including the inverse of Mill’s ratio which is

calculated based upon the first stage regression results. In this respect, the first stage model is

an equation for being innovative, i.e. having introduced either a new product or process. We

include the set of previously discussed control variables and three so-called ‘exclusion

restrictions’, i.e. variables that we assume to affect innovative activity but not the choice for

contract research. The first variable is a dummy variable indicating whether or not the firm is

rated as being credit worthy. Firms with financial constraints tend to drop innovative activity

altogether as shown by Bond et al. (2006) while the constraints are unlikely to affect sourcing

modes. Data are obtained from Creditreform, Germany’s largest credit rating agency, and

merged with the MIP. Moreover, we include a dummy variable from the MIP database that

indicates whether the firm is exporting. Exporting activity has been characterized as a main

driver for innovation (Bhattacharya and Bloch, 2004) but at the same time presumably

unrelated to the sourcing modes. Finally, we include the age of the firm in years, also obtained

from the Creditreform database, as younger firms tend to be more innovative than older firms

in order to successfully enter a market (Bhattacharya and Bloch, 2004; Rammer et al., 2005).

5 Results

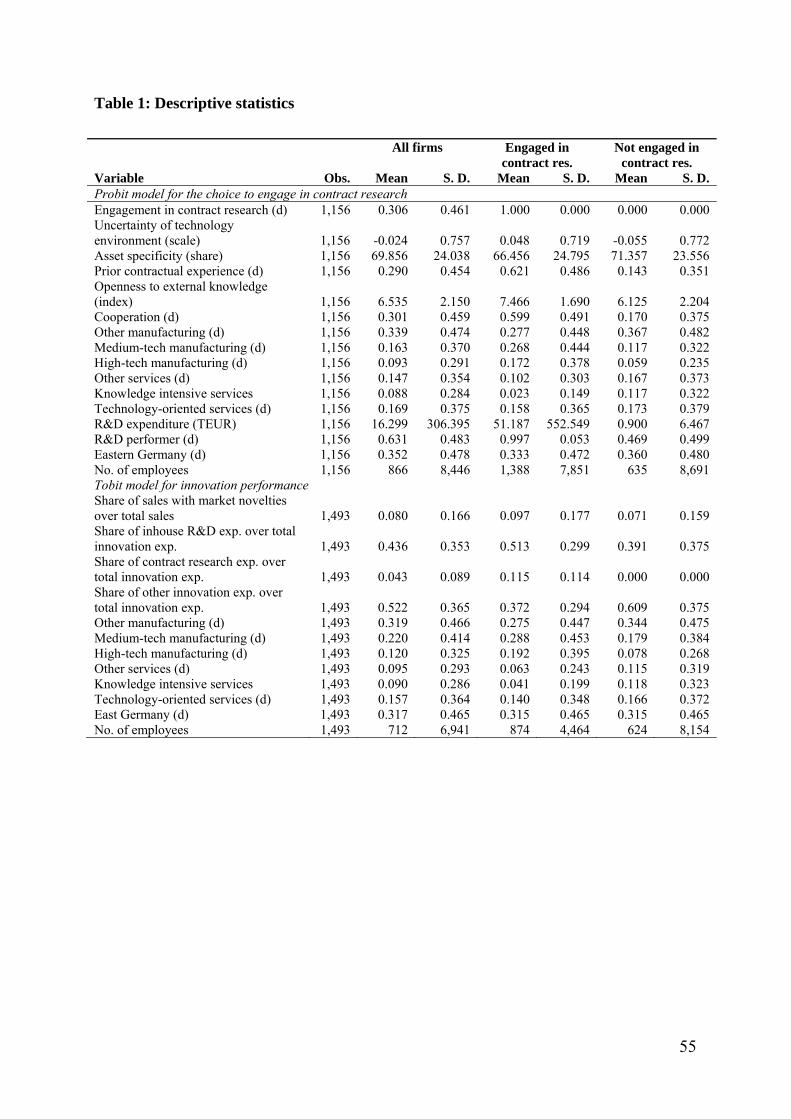

5.1 Descriptive statistics

Our results section starts with descriptive statistics of our dependent variables and our

explanatory variables displayed in Table 1. The upper part of the table refers to the choice

model to engage in contract research while the lower part relates to the innovation

performance model. We show descriptive statistics for all firms and additionally distinguish

26

between firms engaged and not engaged in contract research. Table 1 shows that 31 percent of

the firms in our data contract out research, our first dependent variable. The table also reveals

substantial differences between both groups of firms. These differences are also mostly

statistically significant (not shown in the table). It turns out that firms engaged in contract

research face on average a higher uncertainty of the technology environment and their assets

are slightly less specific. A higher share of firms has prior experience with contract research

and the firms are more open to external knowledge than those without contract research

activities. The lower part of the table shows that firms engaged in contract research achieve

around 2.6 percentage points higher sales with market novelties than firms without contract

research. Moreover, firms using contract research spend a higher share of their innovation

expenditure on in-house R&D compared to firms not engaged in contract research.

--------------------------------

Insert Table 1 about here

--------------------------------

Table A-2 and Table A-3 in the Appendix display correlation tables for both models. It turns

out that there is no indication for multicollinearity or even strong correlation between the

explanatory variables in either model. The mean variance inflation factors (VIF) are 1.31 and

1.18 and the condition numbers 15.08 and 4.88, respectively, which is well below the critical

values of 10 (VIF) and 30 (condition number) (Belsley et al., 1980).

5.2 Multivariate analyses

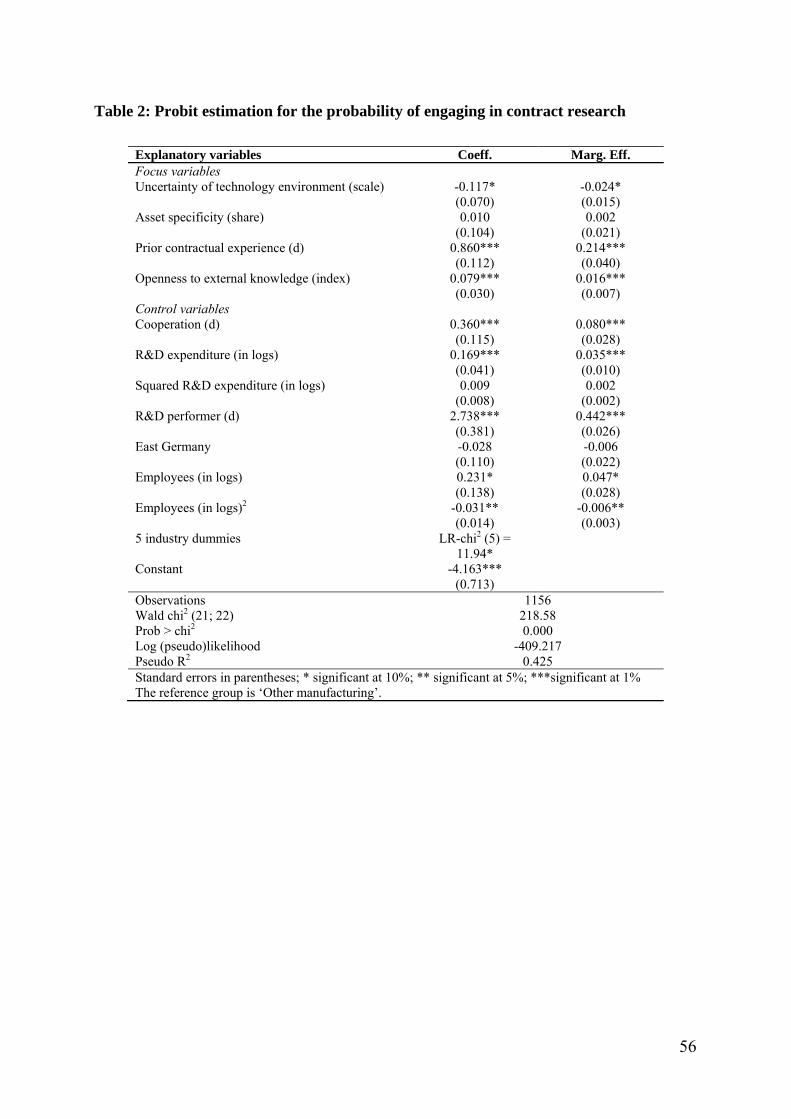

Table 2 shows probit estimation results for the probability of engaging in contract research.

Hypothesis 1, which states that environmental uncertainty increases transaction cost and

hence reduces the propensity to engage in contract research, receives statistical support. With

respect to Hypothesis 2, which refers to asset specificity, we do not find statistically

27

significant effects on the propensity to engage in contract research. The hypothesis thus has to

be rejected. Prior contractual experience is shown to increase the propensity to engage in

contract research as suggested by Hypothesis 3. In fact, contractual experience turns out to

have both an economically and statistically highly significant effect on R&D contracting. As

stated by Hypothesis 4, openness to external knowledge increases the probability to engage in

contract research. This effect is measured with high precision. In conclusion, three of our four

hypotheses receive statistical support which suggests that both, transaction cost and resource-

based arguments, are well suited to explain firms’ choice for contract research.

The results for our control variables can be summarized as follows: engaging in R&D

cooperation spurs the engagement in contract research. R&D cooperation hence appears to be

a complementary strategy to R&D contracting. Investments in in-house R&D activities

increase the probability of engaging in contract research which suggests that absorptive

capacity matters very much in the decision for contract research. Moreover, there is an

inversely U-shaped effect of firm size on the probability of contract research with a maximum

reached at 42 employees. The control variable for regional differences does not have a

statistically significant effect.

--------------------------------

Insert Table 2 about here

--------------------------------

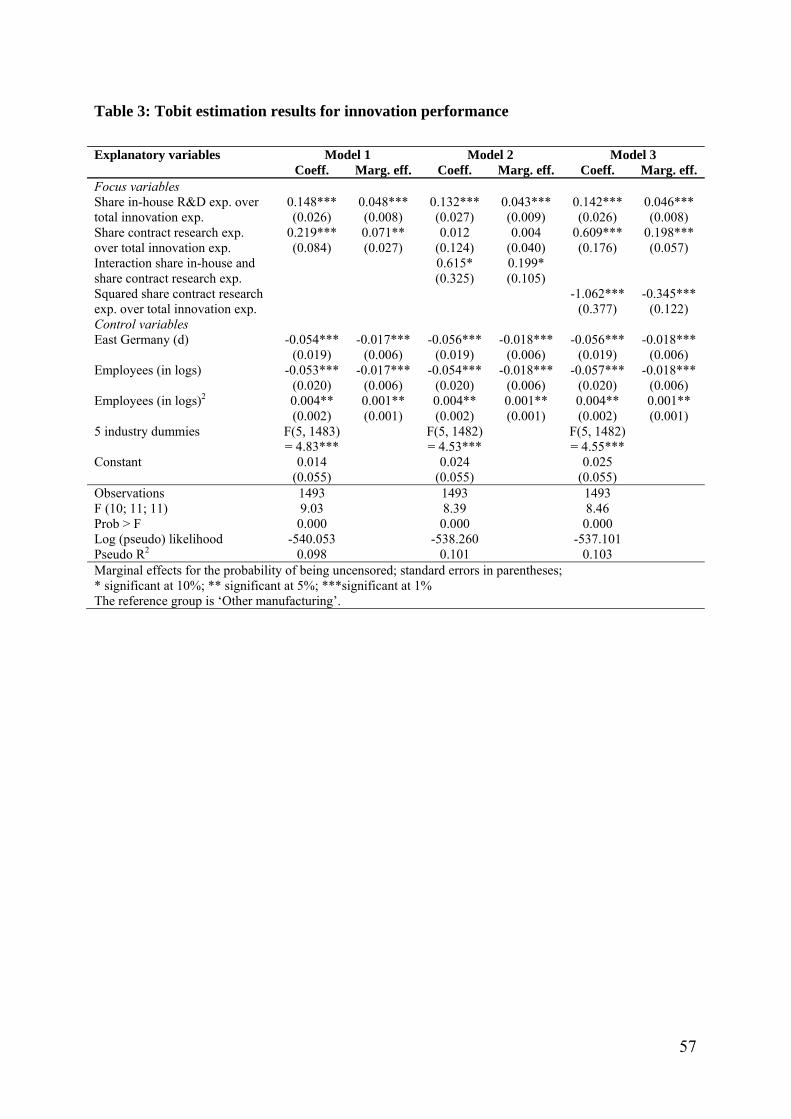

Table 3 displays our estimation results of the tobit model for innovation success. The

findings of our baseline case, Model 1, indicate that both in-house and contract research

contribute positively to innovation performance. This result is, however, qualified when

Model 2 and Model 3 are considered. It turns out that there is a complementary relationship

between in-house and contract R&D as indicated by the positive and significant interaction

28

effect. In other words, the extent to which an increase in in-house R&D or an increase in

contract research matters for innovation performance depends on the value of the respective

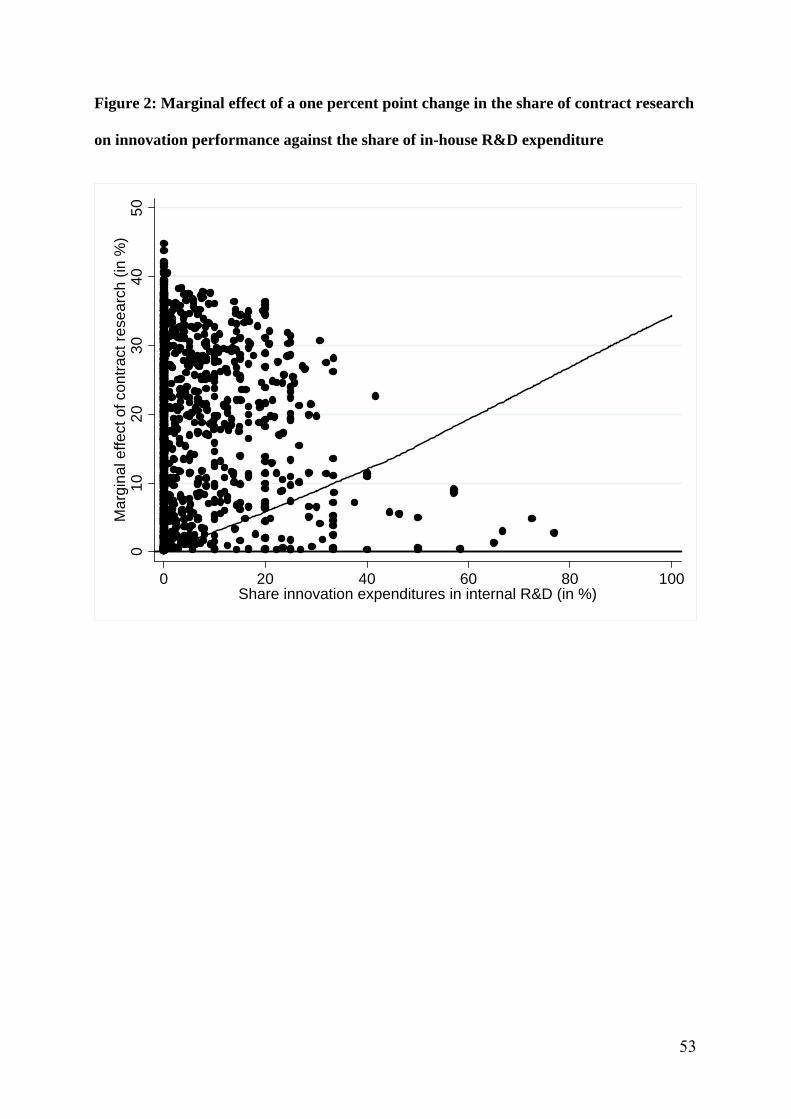

other variable. Hypothesis 5 thus receives full statistical support. Figure 2 presents a graphical

exposition of the mutual dependencies of in-house R&D and contract research. The figure

plots the marginal effect of contract research against the share of in-house R&D in total

innovation expenditure. It clearly chows that there is a positive link between the two

variables.

--------------------------------

Insert Figure 2 about here

--------------------------------

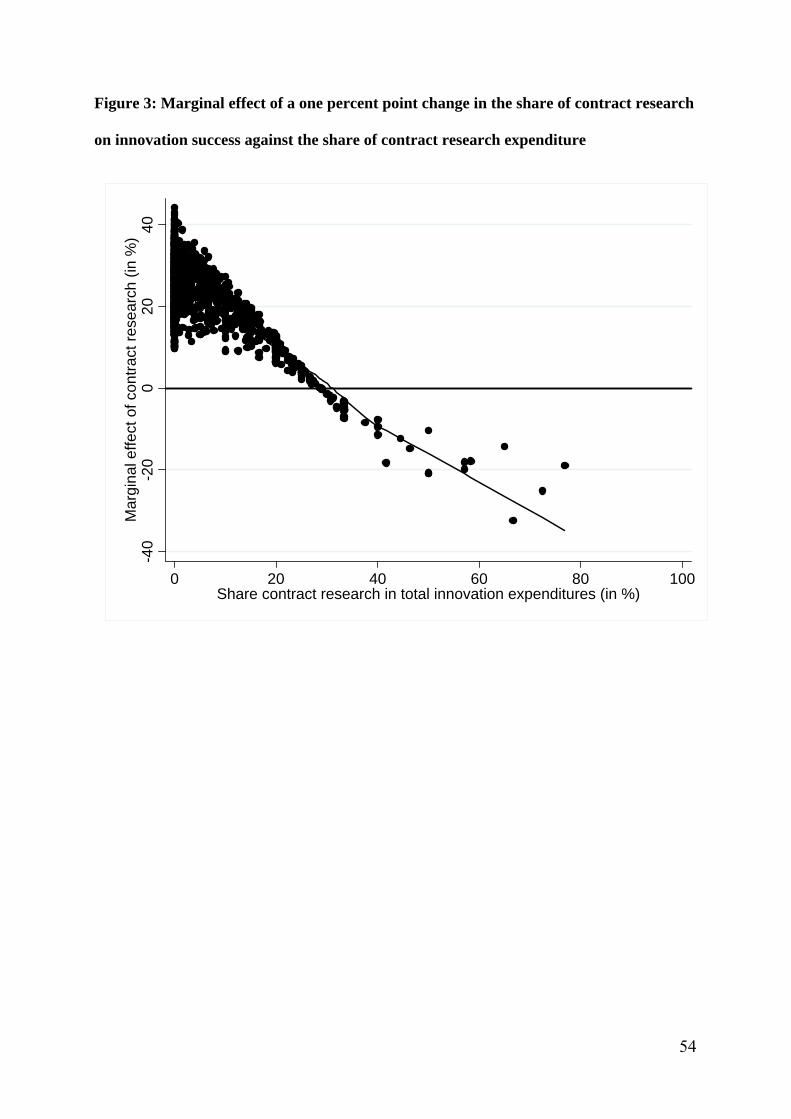

Model 3 shows that there is indeed an inversely U-shaped relationship between contract

research and innovation performance. Obviously, it is the actual scale of contract research that

matters for innovation performance. Our findings substantiate a negative effect from ‘over-

contracting’ which is why our last hypothesis 6 can be confirmed. To illustrate this finding,

Figure 3 plots the marginal effect of contract research against the share of contract research

expenditure. The figure shows that investments into contract research become less efficient in

excess of around 30 percent of total innovation expenditures.

--------------------------------

Insert Figure 3 about here

--------------------------------

Regarding the control variables it turns out that firms located in East Germany exhibit a

lower performance. Moreover, smaller firms in terms of the number of employees tend to

have a higher innovation performance although there is a turning point at a firm size of 753

employees from where innovation performance tends to increase.

29

--------------------------------

Insert Table 3 about here

--------------------------------

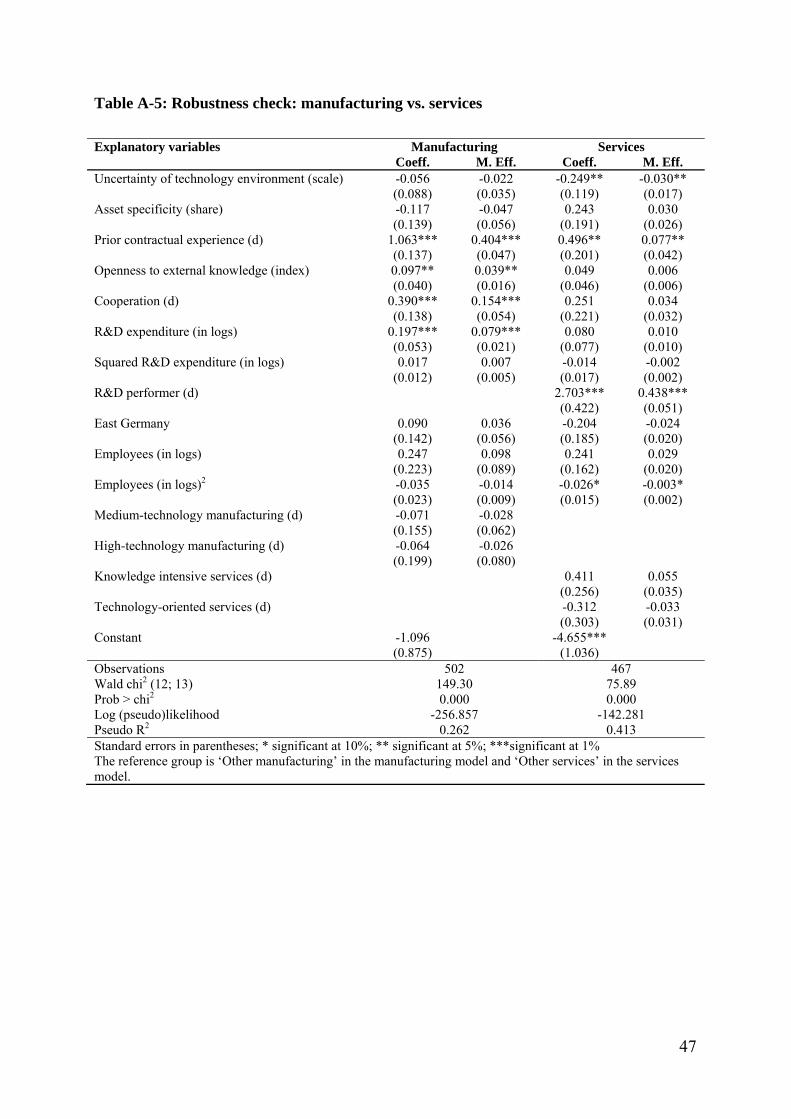

5.3 Robustness checks

The estimation results for our robustness checks are shown in Appendix A. Our first

robustness check relates to the difference between manufacturing and services in the choice

model.3 The results show that there are indeed differences between the sectors which are,

however, merely quantitative rather than qualitative in nature. None of the coefficients change

signs. These findings are similar to the results for the related performance model. This implies

that we can stick to the interpretation of our main results since our interest is in the

qualitative, not the quantitative effects. We believe that the relative imprecision with which

we estimate our coefficients once we split up the sample is due to the substantial reduction in

the number of observations.4

Correcting for sample selection does not change any of our results qualitatively or even

quantitatively. The correction term is statistically insignificant in the probit model for external

R&D. It is, however, statistically significant in the tobit model. The coefficients of interest

remain unchanged even in that case. We hence conclude that there is indeed some evidence

for sample selection but that sample selection does not affect our main estimation results.

3 The robustness checks were performed for the tobit performance model as well. Since the results for the robustness checks for the performance model are qualitatively the same as for the choice model, we display estimation results for the latter model only. Results for the performance model can be obtained from the authors upon request. 4 Note that the dummy variable for performing R&D activities at all drops out of the model for manufacturing industries. The reason is that all firms in this subsample have R&D expenditures and the terms hence become perfectly collinear.

30

6 Discussion

This paper provides comprehensive insights on the determinants and effects of contract

research. We investigate a firm’s decision to engage in contract research based on transaction

cost and resource-based arguments and analyze the interplay of contract research with a firm’s

absorptive capacity to achieve innovation success. Regarding the choice for contract research,

our results show that both transaction cost and resource-based factors matter considerably.

First of all, following a number of related studies (e.g., Robbertson and Gatignon, 1998;

Leiblein et al., 2002; Leiblein and Miller, 2003) we identify uncertainty and asset specificity

as important drivers in a firm’s boundary decision. Our estimation results indeed support our

hypothesis that increased uncertainty with respect to the technology environment decreases

the propensity to engage in contract research as predicted by transaction cost theory. Our

results do not, however, support that asset specificity has a similar effect, although it should

be mentioned that this negative finding might be related to how well our empirical proxy

describes asset specificity. Our transaction cost arguments are hence partly supported.

Second, it has been noted in literature that not only transaction-level effects determine the

decision to engage in contract research but that a critical role is also played by the specific

history, capabilities and resource endowments of a firm (Leiblein and Miller, 2003). As firms

strive to choose the governance mode that complements their capabilities in a way that

knowledge gaps can be bridged, our study focuses on contractual experience and the openness

to external knowledge to account for such factors. Both of our RBV-based hypotheses are

supported by the data. This underlines the great importance of firm-specific factors in

explaining the choice to engage in contract research as a way to get access to externally

available resources. First, firms appear to learn to contract (Mayer and Argyres, 2004),

thereby supporting the development of organizational routines directed towards an efficient

31

collaboration with a variety of partners (Leiblein and Miller, 2003) and thus increasing the

likelihood of repeating such an interaction. Second, our results show that openness to external

knowledge sources also increases the propensity for contract research. It is the breadth of

innovation sources that triggers contract research activities. Hence, the more diverse the

spectrum of knowledge sources the more likely it is that a firm engages in contract research.

This behavior reflects the open innovation model of ‘connect and develop’ (Chesbrough,

2003).

The second step of our analysis focuses on the performance implications of engaging in

contract research. We find positive as well statistically and economically significant effects

for both in-house and contract research expenditures. Moreover, our results strongly suggest

that both technology sourcing modes are complementary to one another, confirming previous

findings (Cassiman and Veugelers, 2006). Adding to the existing literature, we show that

firms may actually ‘over-contract’, i.e. incorporate too much external knowledge into the

innovation process, which we attribute to a resource dilution effect as the resulting bundle of

knowledge resources will be less unique and hence valuable. It is therefore important for

firms to balance in-house R&D with contract R&D carefully to achieve superior innovation

performance.

Our research extends and contributes to the literature particularly in two ways. First, we

extend the findings of Cassiman and Veugelers (2006) by accounting for the actual scale of

in-house versus contract research expenditures. In this respect, we are able to derive concise

information to what extent an increase in in-house R&D expenditure increases the marginal

returns of contract R&D (and vice versa). Contract research obviously fills a gap in a firm’s

sourcing strategy for technological knowledge in that it provides a comparably quick access to

such knowledge without engaging into a collaborative agreement with a partner. In this

32

context, contract research could serve as an instrument for an ‘ad-hoc problem solving’

(Winter, 2003), i.e. it provides a timely reaction to a closely contoured research project.

Second, we are able to examine the relationship between contract research and innovation

performance in more detail by putting forward the argument that firms might ‘over-contract’

or, put differently, under-invest in in-house R&D activities. Hence, while our research

generally underlines the importance of contract research in pursuing an open innovation

strategy, we qualify this finding and suggest that firms might dilute the uniqueness and hence

the value of their resource base. The descriptive statistics indicate that, while a substantial

share of firms is engaged in contract research, the innovation budget allocated to these

activities is quite low. Our results suggest that making more intensive use of contract research

actually increases innovation performance. The efficiency of contract research starts to

decrease, however, if the share exceeds around 30 percent of total innovation expenditures.

Similar to Katila and Ahuja (2002) as well as Laursen and Salter (2006), who point at the

threats from ‘over-searching’ the knowledge environment, we focus on the consequences for a

firm’s resources when ‘too much’ external knowledge is brought into the innovation process.

The benefits and risks of contract research need to be reflected by the management when

organizing for innovation. Managers should not regard contract research primarily as a cost-

saving way of buying research results at the market for research services. Contract research

needs to be carefully balanced with other types of technology sourcing modes that the firm

pursues, e.g the portfolio of R&D alliances established by the firm. Contractual relationships

require managerial attention and its limits need to be taken into account when there is an

intention to increase contract research activities (Ocasio, 1997). After all, the management

needs to take care of the required capacity to absorb the external knowledge. This includes the

development of practices and training for the R&D team to overcome a potential ‘not

invented here’ syndrome (Katz and Allen, 1982).

33

Moreover, the screening and evaluation of potential research partners remains critical for

successfully contracting-out research services. Universities and public research institutes have

increased their supply of such services, but firms may be concerned about IPR issues.

Although universities provide access to cutting-edge knowledge they may be reluctant to

transfer all required IPR to the contracting firm and instead offer a licensing contract to secure

royalties. Another problem might be university researchers’ incentives to publish research

results in scientific journals prior to patent protection. This makes a strong case for evaluating

the chances to appropriate the rents from contract research activities carefully before

increasing the expenditure for it.

7 Conclusion and further research

Our research sheds new empirical light on firms’ decision to engage in contract research and

hence contributes to a more detailed understanding of the phenomenon of outsourcing high

value functions. Moreover, our findings underline that there are limits to the extent to which

firms can benefit from such outsourcing in the sense that contract research may lead to a

dilution of the firm’s resource base. In this respect, we have emphasized the crucial role of a

firm’s absorptive capacity in utilizing external knowledge. Our research focuses on one

important mode for technology sourcing that needs to be balanced with the other modes

available to the firm. Apart from in-house R&D and contract research, firms frequently

engage in R&D alliances, firm acquisitions or licensing for technology development.

Although we acknowledge that discussing all these options in a unified theoretical framework

and taking the related hypotheses to data is a highly complex task, future research should

therefore aim at moving towards an integrative theory of technology development. Our

findings for contract research suggest that this theory needs to consider both transaction-level

and firm-specific factors. In this sense, transaction cost theory and the resource-based view

34

may serve as building blocks for understanding the complex decision processes of firms on

how to balance different sourcing modes and the respective performance implications.

The challenges arising from contract research at offshore locations are another aspect that

we have neglected in our study. On the one hand, transaction costs can be expected to be

higher as contractual relations become more complex. On the other hand, the production costs

of knowledge might be much lower due to differences in wages. In this respect, countries like

India with a skilled workforce may succeed in attracting these high value functions.

Moreover, the open innovation logic suggests that offshore locations provide more diverse

knowledge which in turn may increase the value of a firm’s resources.

Finally, future research should address the need to change a firm’s innovation model over

time. This calls for a panel data analysis to uncover the underlying forces that influence firms

to change their technology sourcing modes. Particular attention should be paid to possible

complementary and substitutive effects between the different sourcing modes. Such a

longitudinal approach would also elucidate and qualify our understanding of the open

innovation model.

35

References

Arnold, U. (2000). ‘New Dimensions of Outsourcing: A Combination of Transaction Cost

Economics and the Core Competencies Concept’. European Journal of Purchasing

and Supply Management 6, 23-29.

Barney, J.B. (1991). ‘Firm Resources and Sustained Competitive Advantage’. Journal of

Management 17, 99-120.

Barthélemy, J. and B.V. Quélin (2006). ‘Complexity of Outsourcing Contracts and Ex Post

Transaction Costs: An Empirical Investigation’. Journal of Management Studies 43,

1775-1797.

Bhattacharya, M. and H. Bloch (2004). ‘Determinants of Innovation’. Small Business

Economics 22, 155-162.

Belderbos, R., M. Carree and B. Lokshin (2004). ‘Cooperative R&D and Firm Performance’.

Research Policy 33, 1477-1492.

Belsley, D.A., E. Kuh and R.E. Welsh (1980). Regression Diagnostics: Identifying Influential

Data and Sources of Collinearity, New York.

Bertrand, M. and S. Mullainathan (2001). ‘Do People Mean What They Say? Implications for

Subjective Survey Data’. American Economic Review 91, 67-72.

Bond, S., D. Harhoff and J. Van Reenen (2006). ‘Investment, R&D and Financial Constraints

in Britain and Germany’, forthcoming in Annales d’Économie et de Statistique.

Bowman, E.H. and D. Hurry (1993). ‘Strategy through the Option Lens: An Integrated View

of Resource Investments and the Incremental-Choice Process’. Academy of

Management Review 18, 760-782.

Brockhoff, K.K. (1992). ‘R&D Cooperation between Firms: A Perceived Transaction Cost

Perspective’. Management Science 38, 514-524.

36

Cassiman, B., M.G. Colombo, P. Garrone and R. Veugelers (2005). ‘The Impact of M&A on

the R&D Process. An Empirical Analysis of the Role of Technological- and Market-

Relatedness’. Research Policy 34, 195-220.

Cassiman, B. and R. Veugelers (2002). ‘R&D Cooperation and Spillovers: Some Empirical

Evidence from Belgium’. American Economic Review 44, 1169-1184.

Cassiman, B. and R. Veugelers (2006). ‘In Search of Complementarity in the Innovation

Strategy: Internal R&D and External Knowledge Acquisition’. Management Science

52, 68-82.

Chatterji, D. (1996). ‘Accessing External Sources of Technology’. Research Technology

Management 39, 48-56.

Chesbrough, H.W. (2003). Open Innovation: The New Imperative for Creating and Profiting

from Technology. Boston.

Cohen, W.M. and D.A. Levinthal (1989). ‘Innovation and Learning: The Two Faces of

R&D’. The Economic Journal 99, 569-596.

Cohen, W.M. and D.A. Levinthal (1990). ‘Absorptive Capacity: A New Perspective on

Learning and Innovation’. Administrative Science Quarterly 35, 128-152.

Cohen, W.M. and D.A. Levinthal (1994). ‘Fortune Favors the Prepared Firm’. Management

Science 40, 227-251.

Criscuolo, C., J.E. Haskel and M.J. Slaughter (2005). Global Engagement and the Innovation

Activities of Firms, NBER Working Paper No. 11479, Cambridge, MA.

David, P.A. and B.H. Hall (2000). ‘Heart of Darkness: Modeling Public–Private Funding

Interactions inside the R&D Black Box’. Research Policy 29, 1165-1183.

Demsetz, H. (1988). ‘The Theory of the Firm Revisited’. Journal of Law, Economics, and

Organization 4, 141-162.

Doh, J.P. (2005). ‘Offshore Outsourcing: Implications for International Business and Strategic

Management Theory and Practice’. Journal of Management Studies 42, 695-704.

37

Dyer, J.H. and H. Singh (1998). ‘The Relational View: Cooperative Strategy and Sources of

Interorganizational Competitive Advantage’. Academy of Management Review 23,

660-679.

Eisenhardt, K.M. and J.A. Martin (2000). ‘Dynamic Capabilities: What Are They?’. Strategic

Management Journal 21, 1105-1121.

Englander, E.J. (1988). ‘Technology and Oliver Williamson's Transaction Cost Economics’.

Journal of Economic Behavior & Organization 10, 339-353.

Eurostat (2004). Innovation in Europe. Results for the EU, Iceland and Norway. Luxembourg.

Gemünden, H., M. Heydebreck and R. Wijnberg (1992). ‘Technological Interweavement: A

Means of Achieving Innovation Success’ R&D Management 22, 359-376.

Gooroochurn, N. and A. Hanley (2007). ‘A Tale of Two Literatures: Transaction Costs and

Property Rights in Innovation Outsourcing’. Research Policy 36, 1483-1495.

Grant, R.M. (1996). ‘Toward a Knowledge-Based Theory of the Firm’. Strategic

Management Journal 17, 109-122.

Graebner, M. (2004). ‘Momentum and Serendipity: How Acquired Leaders Create Value in

the Integration of Technology Firms’. Strategic Management Journal 25, 751-777.

Greene, W.H. (2003). Econometric Analysis. Upper Saddle River, NJ.

Griliches, Z. and J. Mairesse (1984). ‘Productivity and R&D at the Firm Level’. In Z.

Griliches (Ed.), R&D, Patents and Productivity: 339 - 374. Chicago: University of

Chicago Press.

Gulati, R. and H. Singh (1998). ‘The Architecture of Cooperation: Managing Coordination

Costs and Appropriation Concerns in Strategic Alliances’. Administrative Science

Quaterly 43, 781-814.

Heckman, J.J. (1979). ‘Sample Selection Bias as a Specification Error’. Econometrica 47,

153-161.

38

Huston, L. and N. Sakkab (2006). ‘Connect and Develop’. Harvard Business Review 84, 58-

66.

Jaffe, A.B. (1986). ‘Technological Opportunity and Spillovers of R&D: Evidence from Firms’

Patents, Profits, and Market Values’. American Economic Review 76, 984-1001.

Jahns, C., Hartmann, E. and L. Bals (2006). ‘Offshoring: Dimensions and Diffusion of a New

Business Concept’. Journal of Purchasing and Supply Management 12, 218-231.

Jansen, J.J.P., F.A.J. Van Den Bosch and H.W. Volberda (2006). ‘Exploratory Innovation,

Exploitative Innovation, and Performance: Effects of Organizational Antecedents and

Environmental Moderators’ Management Science 52, 1661-1674.