german business network (gbn) - ey.com has been with ey for almost 30 years and worked as an audit...

TRANSCRIPT

German Business Network(GBN)

Webcast – Mexico:Demanding challenges, big opportunitiesNAFTA, US Tax Reform, and more

March 6, 2018

Page 2

German Business Network (GBN)

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

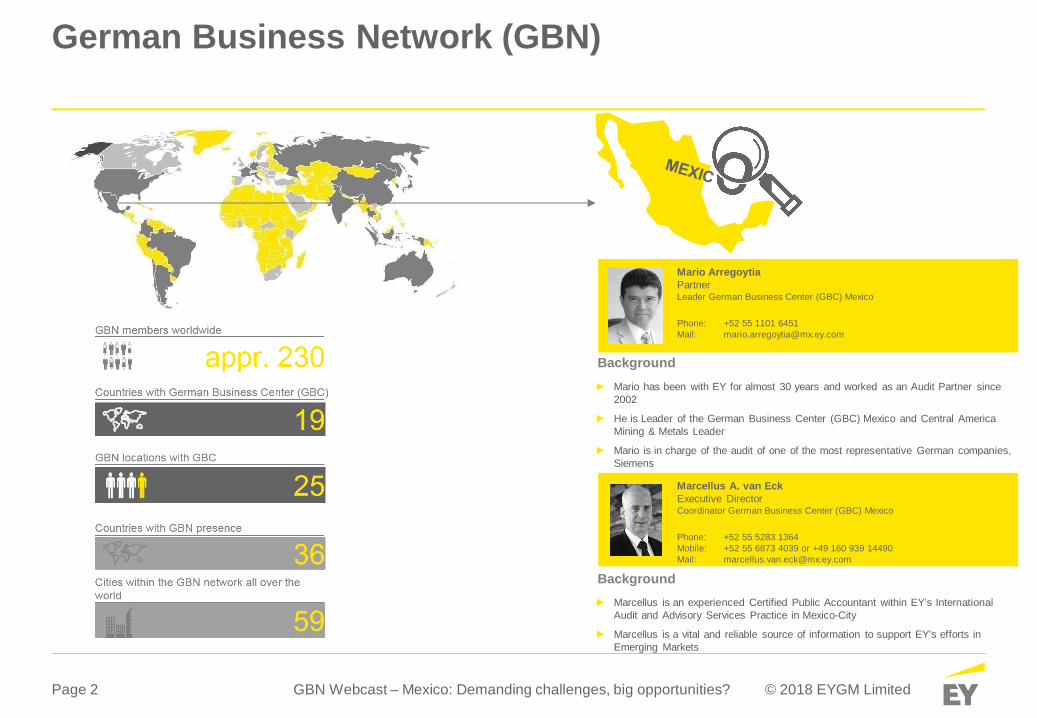

► Mario has been with EY for almost 30 years and worked as an Audit Partner since2002

► He is Leader of the German Business Center (GBC) Mexico and Central AmericaMining & Metals Leader

► Mario is in charge of the audit of one of the most representative German companies,Siemens

Background

Mario ArregoytiaPartnerLeader German Business Center (GBC) Mexico

Phone: +52 55 1101 6451Mail: [email protected]

► Marcellus is an experienced Certified Public Accountant within EY’s InternationalAudit and Advisory Services Practice in Mexico-City

► Marcellus is a vital and reliable source of information to support EY’s efforts inEmerging Markets

Background

Marcellus A. van EckExecutive DirectorCoordinator German Business Center (GBC) Mexico

Phone: +52 55 5283 1364Mobile: +52 55 6873 4039 or +49 160 939 14490Mail: [email protected]

Page 3

Your hosts today

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

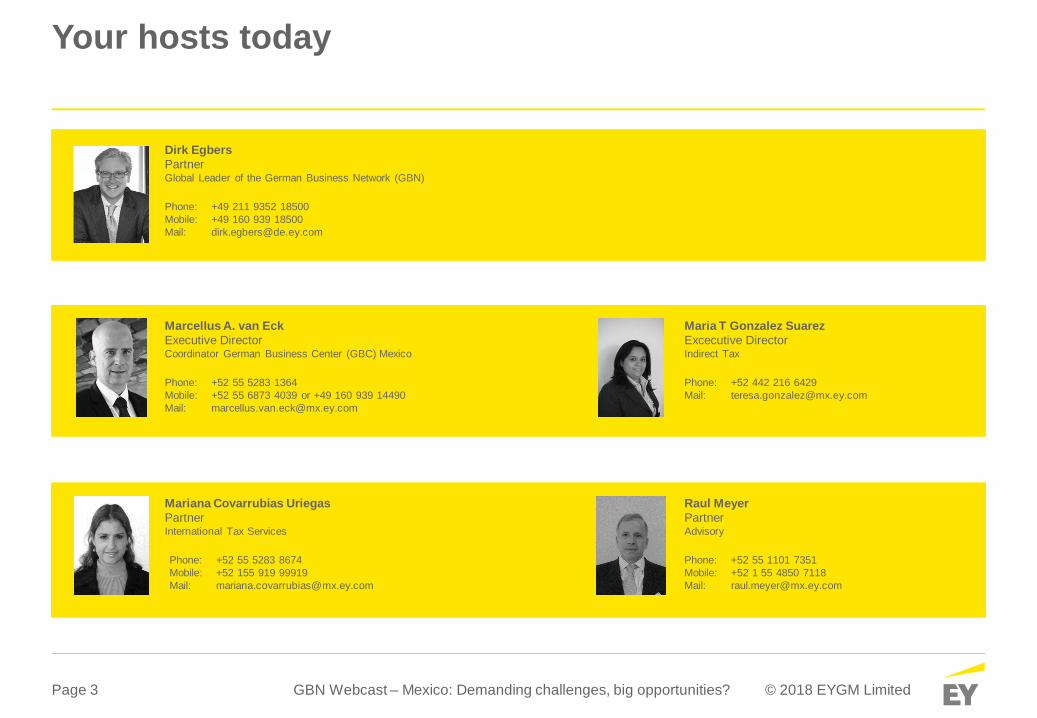

Dirk EgbersPartnerGlobal Leader of the German Business Network (GBN)

Phone: +49 211 9352 18500Mobile: +49 160 939 18500Mail: [email protected]

Marcellus A. van EckExecutive DirectorCoordinator German Business Center (GBC) Mexico

Phone: +52 55 5283 1364Mobile: +52 55 6873 4039 or +49 160 939 14490Mail: [email protected]

Maria T Gonzalez SuarezExcecutive DirectorIndirect Tax

Phone: +52 442 216 6429Mail: [email protected]

Mariana Covarrubias UriegasPartnerInternational Tax Services

Phone: +52 55 5283 8674Mobile: +52 155 919 99919Mail: [email protected]

Raul MeyerPartnerAdvisory

Phone: +52 55 1101 7351Mobile: +52 1 55 4850 7118Mail: [email protected]

Page 4

Webcast: Mexico – Demanding challenges, big opportunitiesAgenda

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

I. Country ProfileMarcellus van Eck

II. NAFTA negotiationsMaria T Gonzalez Suarez

III. Effects of the US Tax ReformMariana Covarrubias Uriegas

IV. Automotive Industry in MexicoDr. Raul Meyer

V. Q & A/Wrap-Up

Page 5

I. Country Profile

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

Page 6

Country ProfileCountry Overview

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

When it comes to doing business, Mexico continues to be a very attractive country for foreigninvestors. Low wages and improved logistics have been part of the draw for OEMs to invest in thecountry, but what has really tipped the scales is Mexico’s unrivaled trade relationships.

Mexico currently has a network of 12 FTAs with 46 countries (plus other trade deals in LatinAmerica and Asia Pacific, according to the government’s trade office). The pacts give exportersfrom Mexico duty-free access to markets that contain 60% of the world’s economic output.

Relevant Information● Area: 1,972,550 km2

● Population:127,540,423

● GDP Per Capita (US$):9,040

● PPP (US$): 17,274

Source(s): Oxford Economics, BMI Research, OEA, World Bank

Page 7

Country ProfileMacroeconomic Overview

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

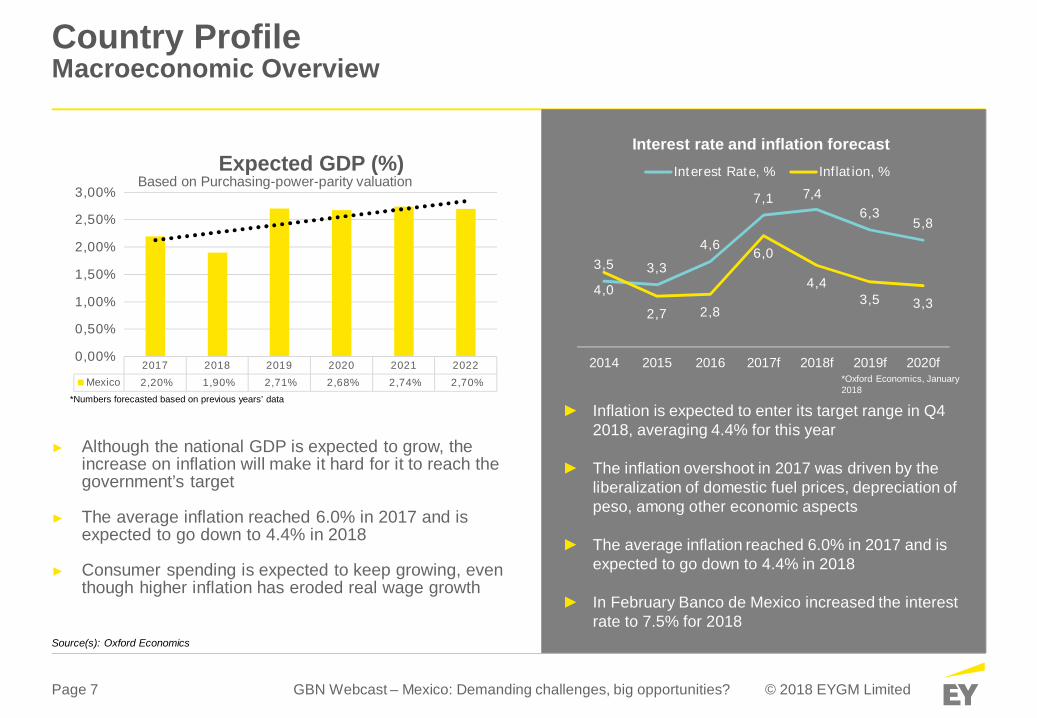

3,5 3,3

4,6

7,1 7,46,3

5,8

4,0

2,7 2,8

6,0

4,43,5 3,3

2014 2015 2016 2017f 2018f 2019f 2020f

Interest rate and inflation forecastInterest Rate, % Inflation, %

► Inflation is expected to enter its target range in Q42018, averaging 4.4% for this year

► The inflation overshoot in 2017 was driven by theliberalization of domestic fuel prices, depreciation ofpeso, among other economic aspects

► The average inflation reached 6.0% in 2017 and isexpected to go down to 4.4% in 2018

► In February Banco de Mexico increased the interestrate to 7.5% for 2018

► Although the national GDP is expected to grow, theincrease on inflation will make it hard for it to reach thegovernment’s target

► The average inflation reached 6.0% in 2017 and isexpected to go down to 4.4% in 2018

► Consumer spending is expected to keep growing, eventhough higher inflation has eroded real wage growth

2017 2018 2019 2020 2021 2022Mexico 2,20% 1,90% 2,71% 2,68% 2,74% 2,70%

0,00%

0,50%

1,00%

1,50%

2,00%

2,50%

3,00%

Expected GDP (%)Based on Purchasing-power-parity valuation

*Numbers forecasted based on previous years’ data

*Oxford Economics, January2018

Source(s): Oxford Economics

Page 8

Country ProfileMacroeconomic Overview

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

Despite the strong depreciation followingDonald Trump’s threats to end NAFTA,the Mexican Peso staged a strongrebound the last months of 2017

Private consumption is expected tokeep driving growth, even though itmight lose its momentum due to theeffect of the tight monetary andfiscal policy.

In 2017 the country had a 1.2%contraction in investment due to trade-

related uncertainty and thegovernment’s austerity drive. Oxford

Economics expects a 1.6% recovery in2018 and 2.8% in 2019.Source(s): Oxford Economics

3,6 4,0 5,1 5,3 4,2 3,4 4,1 3,8 4,0 2,7 2,86,0

4,4 3,5 3,3 3,1

0,1 0,22,1

21,1

-6,5

-1,5

5,7

-3,0

4,3

19,217,8

1,1

-3,8-2,70,0 1,1

Inflation y-y%

PesoAppreciation/Depreciation

App

reci

atio

nof

the

peso

Dep

reci

atio

nof

the

peso

Forecasts

Page 9

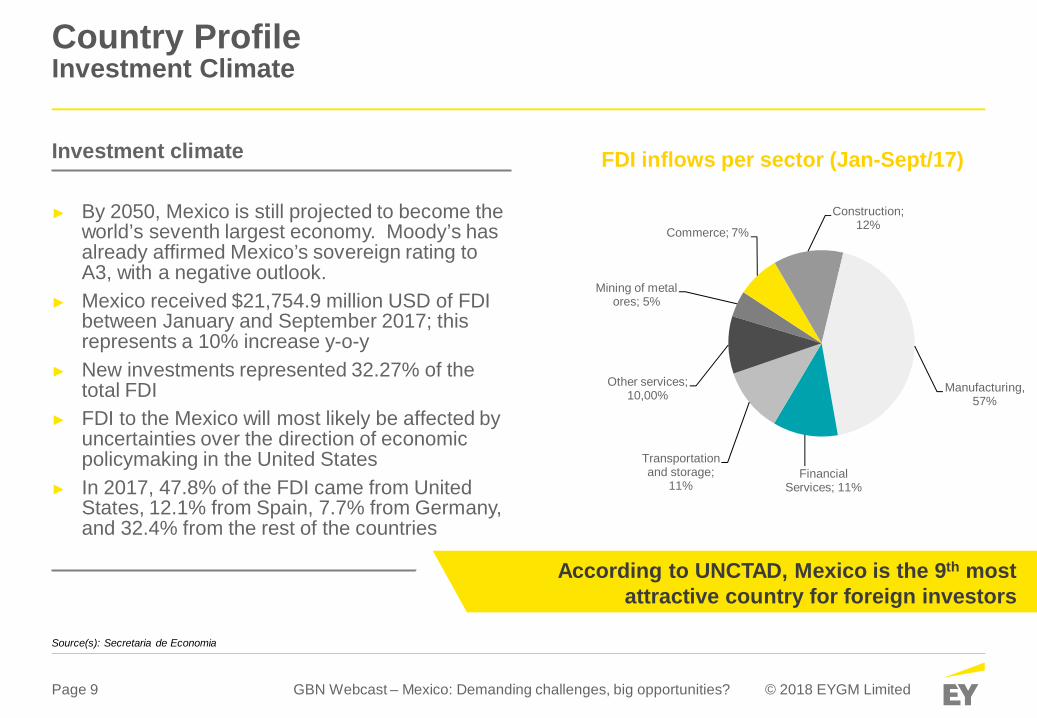

Country ProfileInvestment Climate

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

Investment climate

► By 2050, Mexico is still projected to become theworld’s seventh largest economy. Moody’s hasalready affirmed Mexico’s sovereign rating toA3, with a negative outlook.

► Mexico received $21,754.9 million USD of FDIbetween January and September 2017; thisrepresents a 10% increase y-o-y

► New investments represented 32.27% of thetotal FDI

► FDI to the Mexico will most likely be affected byuncertainties over the direction of economicpolicymaking in the United States

► In 2017, 47.8% of the FDI came from UnitedStates, 12.1% from Spain, 7.7% from Germany,and 32.4% from the rest of the countries

Mining of metalores; 5%

Commerce; 7%

Construction;12%

Manufacturing,57%

FinancialServices; 11%

Transportationand storage;

11%

Other services;10,00%

FDI inflows per sector (Jan-Sept/17)

According to UNCTAD, Mexico is the 9th mostattractive country for foreign investors

Source(s): Secretaria de Economia

Page 10

Country ProfileEase of Doing Business

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

56.45

58.11

60,76

58.56

72.27

69.41

69.45

0 20 40 60 80

Brazil

Argentina

India

Regional average (LatinAmerica & Caribbean)

Mexico

Peru

Colombia

90

87

92

99

6

62

115

63

41

31

0 50 100 150

Starting a business

Dealing with construction…

Getting electricity

Registering property

Getting credit

Protecting investors

Paying taxes

Trading across borders

Enforcing contracts

Resolving insolvency

►Mexico is ranked 49 out of 189 countries in terms of the ease of doingbusiness surveyed by the World Bank. This is a decrease over its 2017ranking (#47) but still higher than its regional average and otherdeveloping markets.

► Infrastructure (e.g. access to electricity) and administration (e.g.registering property and taxes) are areas in which Mexico needs themost improvement.

Ranking of Mexico on ease of doing business topics (2018)Ease of doing business ranking (2018)

Mexico ranks above the Regional averagebut still has a lot of room for improvement

in most of the areas evaluated

Source(s): Ease of Doing Business 2018

Page 11

II. NAFTA negotiations

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

Page 12

NAFTA negotiationsNegotiations Timeline

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

The deadline for the negotiations has changed from2017 to March 2018 due to the fact that there waslittle progress during the past 6 negotiation rounds

The sixth round of NAFTA negotiations between the United States, Canada, and Mexico began inJanuary 2018 in Montreal, Canada

March

Unsolved topics:► Rules of origin► Labor Rights► Sunset Clause

There has been progress onthe following key topics:► Anti-corruption► Intellectual property

Source(s): El Financiero, El Economista, Forbes

Page 13

NAFTA negotiationsWhat would be the consequences for the US?

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

President Trump hasto consider several

factors beforemaking the decision

of leaving NAFTA

Increases in tariffs

Mexico is America's second largestmarket for exported goods.

A 7.5% tariff would have a negativeeffect on the sales of American

products.

Decrease ofRepublican support

14.7% of US oil exports go to Mexico.

Mexico is the thirdlargest importer ofAmerican corn.

Most of the Southern States form part ofTrump’s Republican base and it would have anegative effect if the corn and oil sectors were

affected

Such tariff would hurt American firms which manufactureproducts and parts in Mexico and ship them back to the UnitedStated. The automotive sales impact would be 450,000units in the US.

Negative impact onAmerican firms

Trump has threatenedto impose a 35% tariffon imported goods from

Mexico.The Auto Parts Industry in United States couldpotentially lose around 50,000 jobs

Repercussionson theAutomotiveIndustry The $10 billion annual savings

for the auto industry in North Americawould be lost

Abandoning NAFTA would return Mexico-US trade relations to World Trade Organisation(WTO) rules. This would mean that the exports would be taxed according to the “mostfavoured nation” (MFN) tariffs, which would be higher for the US.

Source(s): El Financiero, Bloomberg, Forbes, Automotive World

Page 14

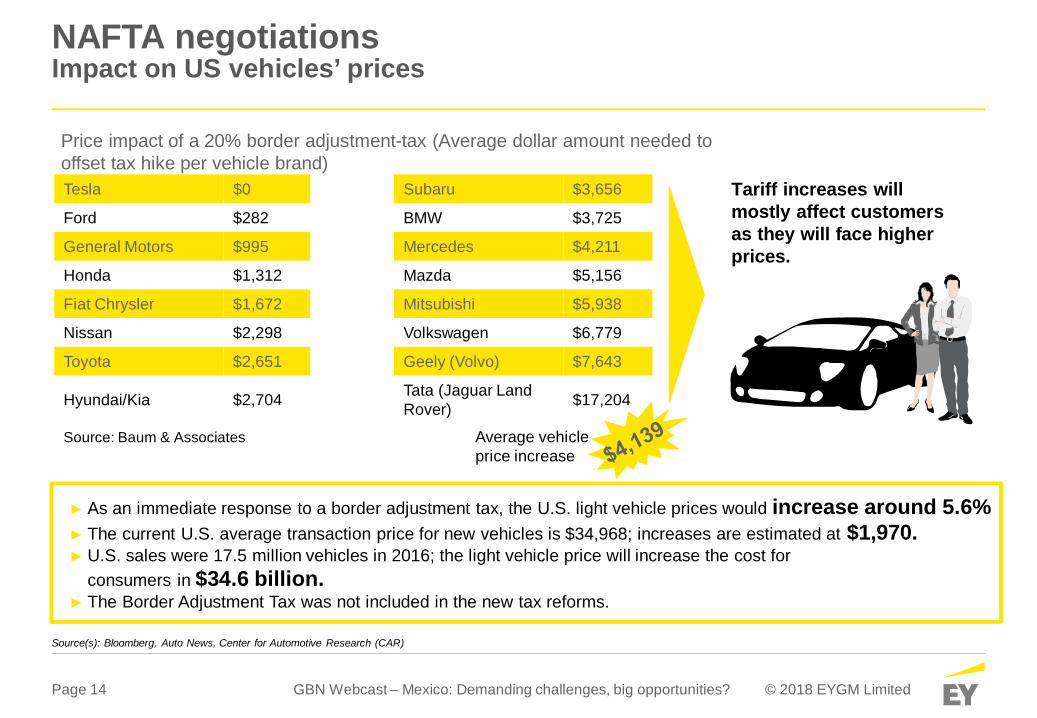

NAFTA negotiationsImpact on US vehicles’ prices

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

► As an immediate response to a border adjustment tax, the U.S. light vehicle prices would increase around 5.6%► The current U.S. average transaction price for new vehicles is $34,968; increases are estimated at $1,970.► U.S. sales were 17.5 million vehicles in 2016; the light vehicle price will increase the cost for

consumers in $34.6 billion.► The Border Adjustment Tax was not included in the new tax reforms.

Tesla $0 Subaru $3,656

Ford $282 BMW $3,725

General Motors $995 Mercedes $4,211

Honda $1,312 Mazda $5,156

Fiat Chrysler $1,672 Mitsubishi $5,938

Nissan $2,298 Volkswagen $6,779

Toyota $2,651 Geely (Volvo) $7,643

Hyundai/Kia $2,704 Tata (Jaguar LandRover) $17,204

Source: Baum & Associates

Price impact of a 20% border adjustment-tax (Average dollar amount needed tooffset tax hike per vehicle brand)

Tariff increases willmostly affect customersas they will face higherprices.

Average vehicleprice increase

Source(s): Bloomberg, Auto News, Center for Automotive Research (CAR)

Page 15

NAFTA negotiationsRisks around the elections

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

Rather than accelerating the NAFTA negotiations it seems that the political calendar is having theopposite effect. None of the three governments want to close a negotiation that might have anunpopular reaction among their voters.

June & OctoberOntario & Quebec’sprovincial elections

NovemberUS’ legislative

elections

JulyMexico’s presidential

elections

The latest polls show a tight three-way race for thepresidency.

Hard-left candidate Andrés Manuel López Obrador isleading the race with 34% of voting intention, followed byPAN’s leader Ricardo Anaya (27%) and the governingparty’s (PRI) former finance minister José Antonio Meade(18%).

Political Uncertainty

An AMLO presidency will likely break with Peña Nieto’sausterity but is unlikely to derail the country’s structuralreforms or threaten Banxico’s independence

Source(s): El Financiero, El Economista, Forbes

Page 16

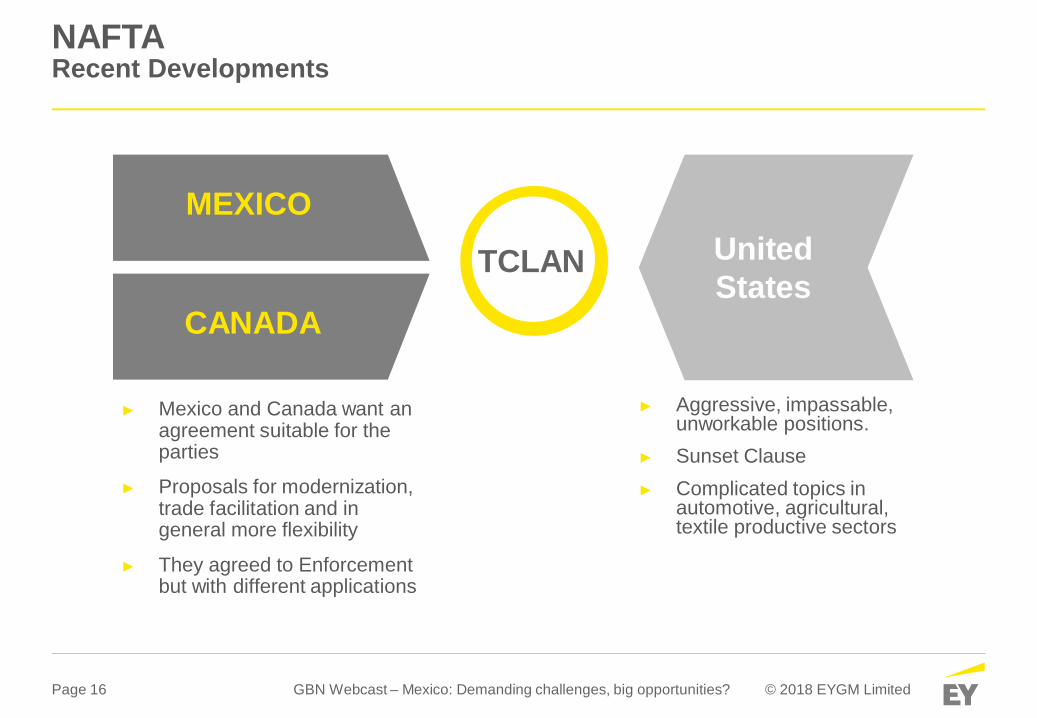

NAFTARecent Developments

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

► Mexico and Canada want anagreement suitable for theparties

► Proposals for modernization,trade facilitation and ingeneral more flexibility

► They agreed to Enforcementbut with different applications

► Aggressive, impassable,unworkable positions.

► Sunset Clause► Complicated topics in

automotive, agricultural,textile productive sectors

MEXICO

•CANADA

UnitedStates

TCLAN

Page 17

NAFTACanadian Ideas

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

IntellectualProperty

Mexico is now working on consolidating all these ideas

The idea is to change the methodology for calculating the regionalvalue content, including:

New investmentson facilities or

production lines

Steel andaluminium thatcome from theNAFTA region

Page 18

NAFTA7th Round of Negotiations

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

► Automotive Rules of originwill be negotiated into anintersessional conference► US government is now

working with the threeAutomotive Terminals

► Steel and Aluminumsafeguard could be imposedby US government to allcountries including Mexicoand Canada.

Page 19

III. Effects of the US Tax Reform

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

Page 20

Effects of the US Tax ReformKey business tax provisions

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

Corporate tax rate andcorporate AMT

►21% tax rate, effective1/1/18

►Eliminates corporate AMT

FDII

►Domestic corporationsallowed a deductionagainst foreign-derivedintangible income (37.5%deduction initially,reduced to 21.875% fortax years beginning after12/31/25),

►In general, the provisionincludes sale of goodsand rendering of services

Expensing►Allows immediate write-off of

qualified property placed inservice after 9/27/17 andbefore 2023. The increasedexpensing would phase-down starting in 2023 by 20percentage points for each ofthe five following years.Eliminates original userequirement. Qualifiedproperty excludes certainpublic utility property andfloor plan financing property.Taxpayers may elect to apply50% expensing for the firsttax year ending after 9/27/17

ParticipationExcemption

►Domestic corporationsallowed a 100%deduction for the foreign-source portion ofdividends received from10% owned (vote orvalue) foreignsubsidiaries. (Deductionnot available for capitalgains or directly-earnedforeign income)

Page 21

Effects of the US Tax ReformKey business tax provisions

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

Net Operating Losses(NOLs)

►Limits NOLs to 80% oftaxable income for lossesarising in tax yearsbeginning after 2017.Repeals carrybackprovisions, except forcertain farm and propertyand casualty losses;allows NOLs to be carriedforward indefinitely

Interest ExpenseDeduction

►Limits deduction to netinterest expense thatexceeds 30% of adjustedtaxable income (ATI).Initially, ATI computedwithout regard todepreciation,amortization, ordepletion. Beginning in2022, ATI would bedecreased by thoseitems. Regulated utilitiesgenerally excepted

Interest ExpenseDeduction

►Dividend ReceivedDeduction

►Domestic productionDeduction

►Others

Page 22

Effects of the US Tax ReformOther key international provisions

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

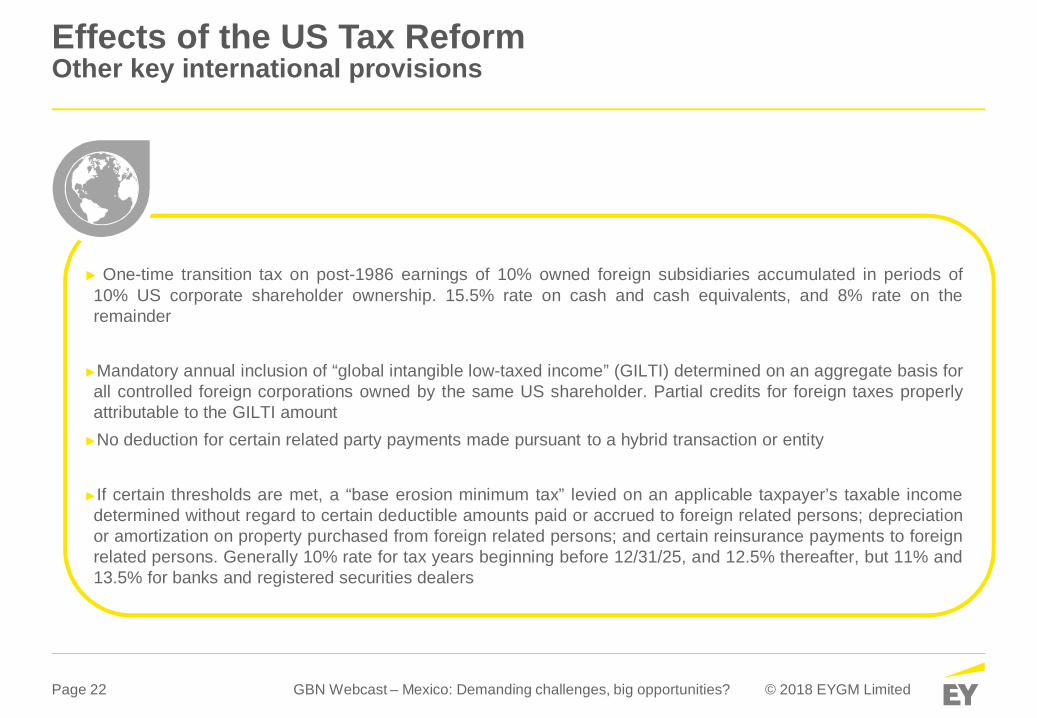

► One-time transition tax on post-1986 earnings of 10% owned foreign subsidiaries accumulated in periods of10% US corporate shareholder ownership. 15.5% rate on cash and cash equivalents, and 8% rate on theremainder

►Mandatory annual inclusion of “global intangible low-taxed income” (GILTI) determined on an aggregate basis forall controlled foreign corporations owned by the same US shareholder. Partial credits for foreign taxes properlyattributable to the GILTI amount

►No deduction for certain related party payments made pursuant to a hybrid transaction or entity

►If certain thresholds are met, a “base erosion minimum tax” levied on an applicable taxpayer’s taxable incomedetermined without regard to certain deductible amounts paid or accrued to foreign related persons; depreciationor amortization on property purchased from foreign related persons; and certain reinsurance payments to foreignrelated persons. Generally 10% rate for tax years beginning before 12/31/25, and 12.5% thereafter, but 11% and13.5% for banks and registered securities dealers

Page 23

IV. Automotive Industry in Mexico

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

Page 24

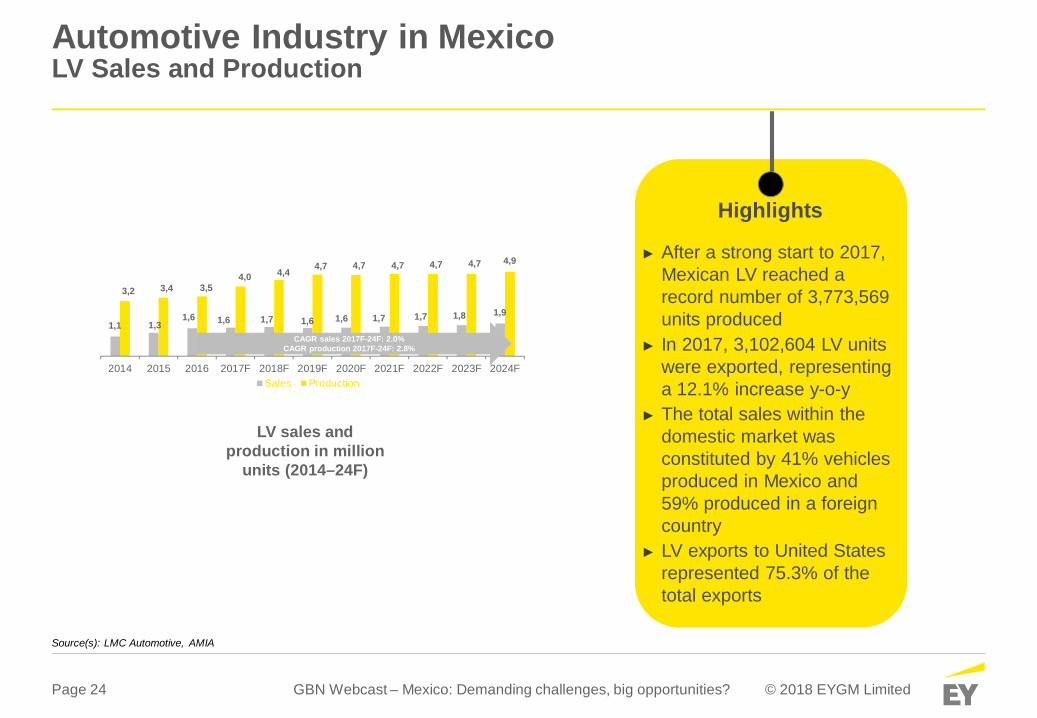

Automotive Industry in MexicoLV Sales and Production

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

LV sales andproduction in million

units (2014–24F)

Highlights

► After a strong start to 2017,Mexican LV reached arecord number of 3,773,569units produced

► In 2017, 3,102,604 LV unitswere exported, representinga 12.1% increase y-o-y

► The total sales within thedomestic market wasconstituted by 41% vehiclesproduced in Mexico and59% produced in a foreigncountry

► LV exports to United Statesrepresented 75.3% of thetotal exports

Source(s): LMC Automotive, AMIA

1,1 1,31,6 1,6 1,7 1,6 1,6 1,7 1,7 1,8 1,9

3,2 3,4 3,54,0 4,4 4,7 4,7 4,7 4,7 4,7 4,9

2014 2015 2016 2017F 2018F 2019F 2020F 2021F 2022F 2023F 2024FSales Production

CAGR sales 2017F-24F: 2.0%CAGR production 2017F-24F: 2.8%

Page 25

Automotive Industry in MexicoKey Industry Megatrends

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

1

2

3 4

5

6

Connectivity► Digitalization on the

value chain► Robotics

Retailtransformation► New business

models► Digital strategy

Supply chainand advancedmanufacturing► Increase in

complexity► Focus on flexibility

New mobilitymodels► Car Sharing► Car Pooling► Collaborative

consumptionBig Data► Analytics to

improve customerexperience andbusinessprocesses

AutonomousVehicles► Increasing

investment onautonomousvehicles

Page 26

Automotive Industry in MexicoKey Challenges

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

Accelerating paceof disruptive

competition andinnovation

Battling to ownrelationships

in a digitalmarketplace

“Digitalization”across the value

chain

Unprecedentedscrutiny

Securingresources for

businesscontinuity

Diversesources of

unpredictability

EY’s recent analysis of the automotiveC-suite’s agenda showed that most of theorganizations are not prepared in terms ofexecution and resource alignment in orderto enable a faster innovation and change

Page 27

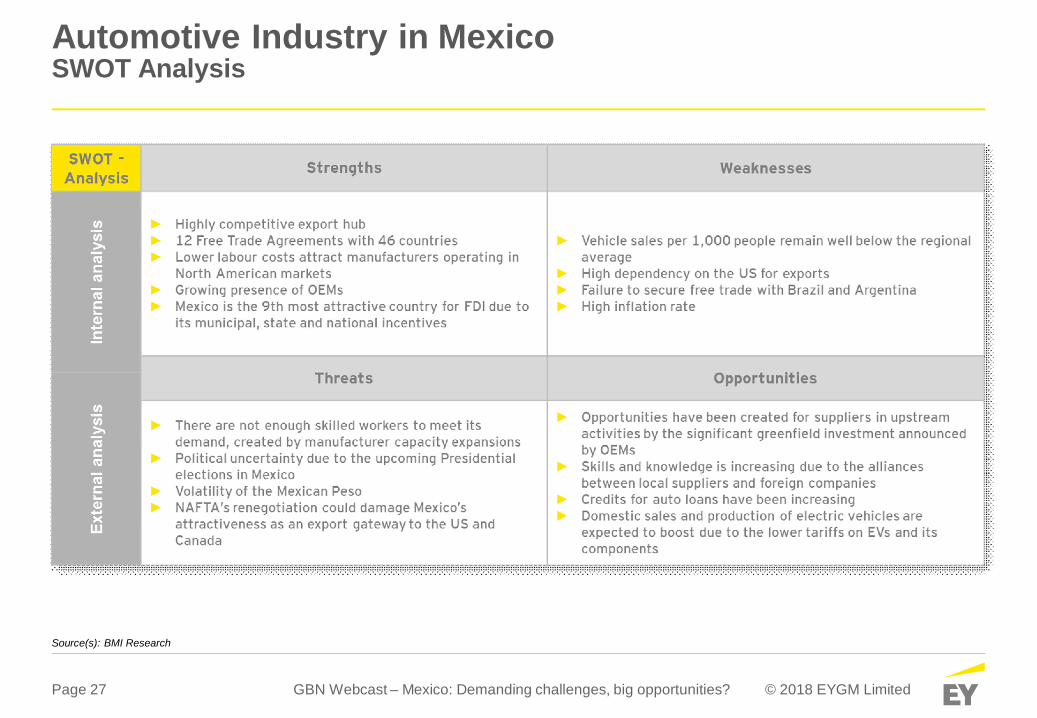

Automotive Industry in MexicoSWOT Analysis

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

Source(s): BMI Research

Page 28

V. Q & A/Wrap-Up

GBN Webcast – Mexico: Demanding challenges, big opportunities? © 2018 EYGM Limited

Thank you!

Page 30

EY | Assurance | Tax | Transactions | Advisory

About the global EY organization

The global EY organization is a leader in assurance, tax, transaction and advisory services. Weleverage our experience, knowledge and services to help build trust and confidence in the capitalmarkets and in economies the world over. We are ideally equipped for this task — with well trainedemployees, strong teams, excellent services and outstanding client relations. Our global purposeis to drive progress andmake a difference by building a better working world — for our people, for our clients and for ourcommunities.

The global EY organization refers to all member firms of Ernst & Young Global Limited (EYG).Each EYG member firm is a separate legal entity and has no liability for another such entity’s actsor omissions. Ernst & Young Global Limited, a UK company limited by guarantee, does notprovide services to clients.

For more information, please visit www.ey.com.

© 2018 EYGM LimitedAll Rights Reserved.

ED None

This material has been prepared for general information purposes only and is not intended to berelied upon as accounting, tax, or other professional advice. Please refer to your advisors forspecific advice.

www.ey.com