german business network (gbn) - webcast – mexico

TRANSCRIPT

German Business Network (GBN) Webcast – Mexico: Supercharged for the futureJuly 5, 2016

Page 2

German Business Network (GBN)

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

► Mario has been with EY for 27 years and worked as an Audit Partner since 2002

► He is Leader of the German Business Center (GBC) Mexico and Central America Mining & Metals Leader

► Mario is in charge of the audit of one of the most representative German companies, Siemens

Background

Mario ArregoytiaPartnerLeader German Business Center (GBC) Mexico

Phone: +52 55 1101 6451Mail: [email protected]

► Marcellus is an experienced Certified Public Accountant within EY’s International Audit and Advisory Services Practice in Mexico-City

► Marcellus is a vital and reliable source of information to support EY’s efforts in Emerging Markets

Background

Marcellus A. van EckExecutive DirectorCoordinator German Business Center (GBC) Mexico

Phone: +52 55 5283 1364Mobile: +52 55 6873 4039 or +49 160 939 14490Mail: [email protected]

Page 3

Your hosts today

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Dirk EgbersPartnerGlobal Leader of the German Business Network (GBN)

Phone: +49 211 9352 18500Mobile: +49 160 939 18500Mail: [email protected]

Marcellus A. van EckExecutive DirectorCoordinator German Business Center (GBC) Mexico

Phone: +52 55 5283 1364Mobile: +52 55 6873 4039 or +49 160 939 14490Mail: [email protected]

Francisco Bautista PlancartePartnerGlobal Trade and Investment, Incentives

Phone: + 52 55 5283 1454Mail: [email protected]

Julian Vega GreggSenior ManagerClimate Change and Sustainability

Phone: +52 55 5283 3342Mail: [email protected]

Juan Ignacio AriasPartnerTAX

Phone: +52 222 237 9922 ext. 2138Mail: [email protected]

Page 4

Webcast: Mexico – Supercharged for the futureAgenda

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

I. General overview: Market development in MexicoMarcellus van Eck

II. A holistic approach to an investment in MexicoFrancisco Bautista

III. Renewable Energies in MexicoJulian Vega Gregg

IV. Taxes in MexicoJuan Ignacio Arias

V. Q & A/Wrap-Up

Page 5

I. General overview: Market development in Mexico

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Page 6

General overview: Market development in MexicoExecutive summary

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

• Mexico’s economy will continue to rise at an annual rate between 2.5 and 3.0% through 2016 and 17 (Q116= 2.8%). Recovery in the upcoming months is expected to include an upturn of industrial output in the US; depreciation of the peso; continued expansion of employment; higher real wages resulting from lower inflation; an increase in remittances in pesos in real terms; and the gradual effects of recent structural reforms.

• Meanwhile, the government has continued to treat the oil shock as a permanent one and has proposed an austere budget for 2016, which foresees a 1.9% cut in spending (in real terms) and a fiscal deficit of 3% of GDP.

Investment climate

• Structural reforms in the telecommunications and energy sectors will help to boost FDI. • On 30 September 2015, the second package of Mexico's First Oil Bidding Round was awarded and includes

shallow water fields with proven resources. The next phase of 26 fields has been awarded on 15 December 2015. Further packages (including natural- and shale gas) are scheduled for the 2nd half of 2016.

Key investment drivers

Sectors overview

Mexico economic census

• Investment spending has shown modest dynamism fueled by the private sector, while oil output has rebounded from the April 2015 lows (although it remains on a downward trend).

• In 2015, Mexico received US$28.4 billion (PY: US$22.8 billion ) in foreign direct investment (FDI).• Announcements of FDI by US, Japanese and German Automotive companies such as BMW, Ford,

Mercedes Benz, and Bosch illustrate that exports may increase considerably in the next few years.

Economic environment

• The manufacturing industry remains one of the most attractive in the country (especially, the automotive sector), followed by financial services, mass media, commerce and construction, as they received the greatest amount of FDI in 2015.

• Recent reforms have captured the attention of investors due to Mexico’s growth potential in some of its key sectors. These reforms should increase participation by the private sector in industries such as energy, telecom, consumer products, automotive, retail, real estate, banking and tourism.

• According to INEGI, as of 2014, 95.4% of the businesses in Mexico are small (0‒10 employees).• The average income of the businesses (or establishments) nationwide indicates that for every MX$100

earned, MX$71 are used for current operating expenses, MX$8 for payment of salaries and the remaining MX$21 for taxes, royalties, etc.

Continued on next slide.

Page 7

General overview: Market development in MexicoExecutive summary (continued)

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

► Macroeconomic stability► Steady post-recession economic growth► Political stability► Close proximity to the US and Canada► Highest number of free trade agreements in the region► Extensive and growing domestic market► Strong manufacturing sector► Stable and well-capitalized banking system► Abundant natural resources► Sophisticated production and export base► Attractive destination for FDI► Favorable trends in demographics

► Weak governmental control in certain areas► Lack of accountability from elected state officials► Security► Income inequality► High costs and low graduation rates in educational system► Large dependence on US export market► High dependence on global automotive industry► Low wage growth► Rising current-account deficit► Doubling of state-level debt between 2008 and 2015► Increasing dependence on imported energy resources

Highlights10th most populous country in the world according the UN; almost 80% live in urban areas, including Mexico City, the largest urban area in the Western Hemisphere

15th largest economy in the world as measured by GDP in current prices (IMF) and the 11th largest by purchasing power parity

14th largest country in the world as measured by geographic area

2nd largest FDI recipient in Latin America and the Caribbean

Sovereign risk rated as investment grade (S&P, Fitch and Moody’s)

Financial reserves more than twice the size of the country’s external debt

Signatory of the Kyoto Protocol

More than 100 government and industry R&D centers

Largest exporter of trucks and 8th of cars. The 7th largest producer of motor vehicles globally

Top exporter of home appliances to Latin America; 5th exporter globally

About 25% of power generation capacity fueled by renewable energy; 4th largest producer of geothermal energy in the world

9th largest producer and 13th largest exporter of crude oil

Strong transportation network of highways, railroads, ports and airports

Largest exporter of several key agricultural products in demand worldwide, including organic coffee, tomatoes, avocados and mangos

Largest global exporter of beer

Manufacturing costs and cost of doing business 20–25% lower than US

Opportunities

Impediments

Page 8

General overview: Market development in MexicoSolid long-term growth outlook on the back of structural reforms, increasingly strong consumer spending and favorable demographics

Mexico

Economy: Oil is an important source of revenue and accounts for around 20% of fiscal revenues, 5% of exports and about 5% of GDP

Main exports: Exports are mostly related to the automotive sector and other activities related to the manufacturing and livestock sectors

President: Enrique Peña Nieto (next elections in July 2018)

Demographics:66 inhabitants/km²

Deteriorating security Labor shortages in highly

skilled professions Large informal labor market Fall of global oil prices

Country risks

Strong demand for goods exports

Declining unemployment Positive long-term GDP growth

due to structural reforms

Macroeconomic outlook

Higher household spending Bidding rounds for oil fields Strong manufacturing sector Attractive FDI destination

Major opportunities

With 10 free-trade agreements signed with 45 countries, Mexico has been able to trade with partners that make up 60% of the world’s GDP.

Around 80% of the country’s 121 million people are living in urban areas. Mexico is the 14th-largest country in the world in terms of surface area.

F= ForecastSource: Oxford Economics, May 2016.

GDP nominal, 2015:US$ 1,144.2 billion

GDP per capita nominal, 2015:US$ 9.445 3,8 1,6 2,3 2,5 2,6 2,7 2,8 2,8 2,8

4,13,8

4,0

2,73,0 3,3

3,1 3,0 3,0

2012 2013 2014 2015 2016 F 2017 F 2018 F 2019 F 2020 F

Mexico's GDP Real, annual growth, % Inflation, consumer price index, % YOY

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Page 9

General overview: Market development in MexicoYoung population

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Source: INEGI

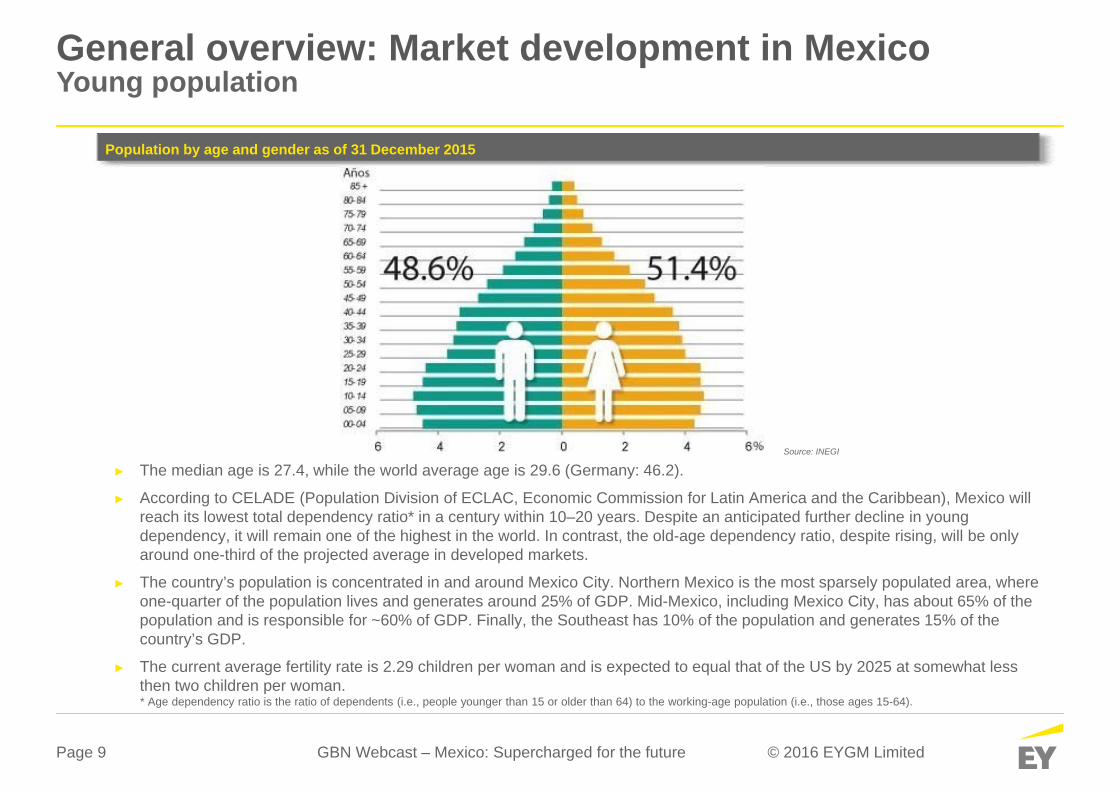

► The median age is 27.4, while the world average age is 29.6 (Germany: 46.2).

► According to CELADE (Population Division of ECLAC, Economic Commission for Latin America and the Caribbean), Mexico will reach its lowest total dependency ratio* in a century within 10–20 years. Despite an anticipated further decline in young dependency, it will remain one of the highest in the world. In contrast, the old-age dependency ratio, despite rising, will be only around one-third of the projected average in developed markets.

► The country’s population is concentrated in and around Mexico City. Northern Mexico is the most sparsely populated area, where one-quarter of the population lives and generates around 25% of GDP. Mid-Mexico, including Mexico City, has about 65% of the population and is responsible for ~60% of GDP. Finally, the Southeast has 10% of the population and generates 15% of the country’s GDP.

► The current average fertility rate is 2.29 children per woman and is expected to equal that of the US by 2025 at somewhat less then two children per woman.

Population by age and gender as of 31 December 2015

* Age dependency ratio is the ratio of dependents (i.e., people younger than 15 or older than 64) to the working-age population (i.e., those ages 15-64).

Page 10

Mexico’s structural change story is barely in its initial stages. From 1994 to 2012, only five structural reforms were implemented; and during 2013, seven structural reforms were debated and approved. All of them are in the implementation phase, but not all are moving at the same pace due to the global economic environment.

General overview: Market development in MexicoImplementation of reforms to be reflected in the next several years

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Reform Status Aim Regulatory changes Assessment Update

Energy Approved

End state monopoly status of Pemex and encourage private investment in the energy sector

Power of existing regulators substantially strengthened

Bold reform but differences over extending production-sharing versus profit-sharing rights remain

A total of 169 oilfields will be available to investors during the first round of auctions According to the Ministry of Economy, there are 47 companies registered for round one and the winner of the bid is expected was announced in the third quarter of 2015

Fiscal ApprovedRaise revenues and close loopholes; expands fiscal deficit

None; however, the reform introduces universal pension/unemployment insurance

Does not expand the tax base or reach of VAT; does not reduce government reliance on Pemex revenues

The reform has impacted the corporate sector; however, the revenues resulting from the reform may not be enough and there could be some adjustments to the reform in 2017

Communications ApprovedIncrease competition in telecom and broadcasting

Two autonomous regulators: IFETEL (telecoms and broadcasting) and competition (CFCE)

Inexperienced regulators tackling powerful near-monopolies in both broadcasting and telecom sectors

New players are currently investing, including AT&T, and monopolies are still selling assets to competition

Banking Approved

Encourage more bank lending and streamline bankruptcy laws

Gives banking regulator power to punish banks that don’t lend enough; makes it easier for banks to collect bad loans

Needed but uncertain whether measures can significantly undermine the existing informal economy; does not mandate specific lending levels

Mexico continues to be among the countries with the lowest credit/GDP ratio in the world

Education Approved Improve teaching standards

Establishes autonomous regulator (INEE)

Need to avoid a protracted fight with teacher’s union

Changes still not reflected; controversy with teacher’s unions is still going

Page 11

General overview: Market development in MexicoKey areas of Business Activity

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Plants in Mexico per key sector

Automotive 4th largest exporter and 8th largest

producer of motor vehicles globally

Aerospace 6th supplier to the American

aerospace industry

Renewable energy Around 25% of total installed

capacity come from renewable sources

Electronic Leading exporter in Latin America

Oil & Gas Mexico’s potential for oil and gas

resources is high

Electric 2nd biggest producer in Latin

America

Source: ProMexico, figures as of December, 2014

Page 12

General overview: Market development in MexicoIndustry forecast: Top 10 sectors ranked by gross value added

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Source: Oxford Economics, December 2015.

Source: Latin American Cities and Regional Forecasts, Oxford Economics December 2015.

► Manufacturing output growth is forecast to be higher than GDP growth over the next decade. To 2024, manufacturing output is expected to grow on average by 3.5% a year.

► The three fastest growing sectors in manufacturing over the next five years will be motor vehicles; motor vehicle bodies & parts; and aerospace. The slowest growing sectors will be basic chemicals & fertilizers; man-made fibers; and pesticides & other agrochemicals.

2015 level(MX$ billion)

2015 percent annual change

Percent share of GDP

(Nominal terms)1. Manufacturing 2,374 2.8 13.1 2. Commerce 2,219 4.7 12.2 3. Real estate & property rental 1,674 2.4 9.2 4. Construction 1,045 3.4 5.8 5. Mining 947 - 6.1 5.2 6. Transport, post office & storage 831 3.5 4.6 7. Financial service & insurance 622 1.0 3.4 8. Government activities 514 2.6 2.8 9. Educational services 498 0.4 2.7 10. Information services 490 8.0 2.7 Top 10- Total 11,215 2.4 61.8

Page 13

General overview: Market development in MexicoAutomotive - OEM investments create opportunities for suppliers in upstream activities

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

1.59

1

1.56

1

2.11

5

1.89

8

2.80

8

3.39

3

4.29

9

5.85

8

2008 2009 2010 2011 2012 2013 2014 2015

Record FDI in 2015

Company 2007-10 2011 2012 2013 2014 2015 2016*Daimler 871 Toyota 1,000Ford 3,000 1,300 2,500 1,600Fiat/Chrysler 550 1,264Audi 1,300 VW 1,603 720 1,000GM 4,370 540 420 691 3,600Nissan 600 2,000 Mazda 500 120Honda 800 470MercedesBenz-Infiniti

1,240

BMW 1,000KIA 1,000Total 10,994 1,840 5,020 3,265 6,840 4,500 1,600

► Mexico’s competitive advantages, including low labor costs, continue to prove significant attractions to automakers.

► From 2007 to 2015, manufacturers announced investments of US$34 billion, primarily directed toward the construction of new plants and the purchase of new equipment.

► 81% of Mexican vehicle production was destined for export in 2015.

► According to ProMexico, there are market opportunities in processes with highest demand that lack of presence in Mexico like: stamping, foundry, forging and machining.

FDI in automotive sector of Mexico (US$ million)

FDI announcements in Mexico by OEM (US$ million)Sources: Secretaría de Economia, 2016

* From January – May 2016Source: ProMexico 2016

2.022 2.103

1.508

2.2612.558

2.884 2.9333.220 3.399

1.613 1.6611.223

1.8602.143 2.355 2.423

2.643 2.759

500

1.500

2.500

3.500

4.500

2007 2008 2009 2010 2011 2012 2013 2014 2015

ProductionExports

Production vs exports of light vehicles, Mexico (‘000 units)

Source: Ministry of Economy with AMIA and ANPACT data, 2016

Page 14

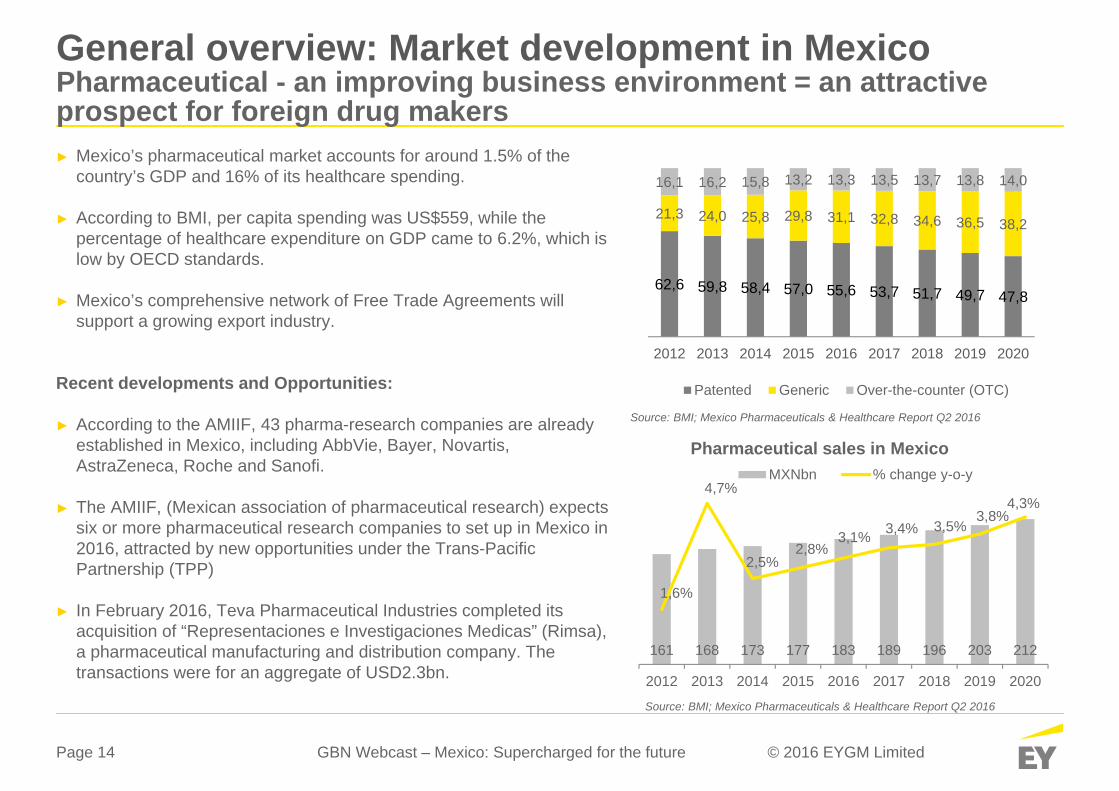

General overview: Market development in MexicoPharmaceutical - an improving business environment = an attractive prospect for foreign drug makers

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

62,6 59,8 58,4 57,0 55,6 53,7 51,7 49,7 47,8

21,3 24,0 25,8 29,8 31,1 32,8 34,6 36,5 38,2

16,1 16,2 15,8 13,2 13,3 13,5 13,7 13,8 14,0

2012 2013 2014 2015 2016 2017 2018 2019 2020

Patented Generic Over-the-counter (OTC)

► Mexico’s pharmaceutical market accounts for around 1.5% of the country’s GDP and 16% of its healthcare spending.

► According to BMI, per capita spending was US$559, while the percentage of healthcare expenditure on GDP came to 6.2%, which is low by OECD standards.

► Mexico’s comprehensive network of Free Trade Agreements will support a growing export industry.

Recent developments and Opportunities:

► According to the AMIIF, 43 pharma-research companies are already established in Mexico, including AbbVie, Bayer, Novartis, AstraZeneca, Roche and Sanofi.

► The AMIIF, (Mexican association of pharmaceutical research) expects six or more pharmaceutical research companies to set up in Mexico in 2016, attracted by new opportunities under the Trans-Pacific Partnership (TPP)

► In February 2016, Teva Pharmaceutical Industries completed its acquisition of “Representaciones e Investigaciones Medicas” (Rimsa), a pharmaceutical manufacturing and distribution company. The transactions were for an aggregate of USD2.3bn.

Pharmaceutical sales in Mexico

Source: BMI; Mexico Pharmaceuticals & Healthcare Report Q2 2016

161 168 173 177 183 189 196 203 212

1,6%

4,7%

2,5%2,8%

3,1% 3,4% 3,5%3,8%

4,3%

2012 2013 2014 2015 2016 2017 2018 2019 2020

MXNbn % change y-o-y

Source: BMI; Mexico Pharmaceuticals & Healthcare Report Q2 2016

Page 15

II. A holistic approach to an investment in Mexico

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Page 16

Oil prices are still low but stabilizing

Automotive and Manufacturing continue to be Mexico´s main

driver

Labor cost among the most

competitive worldwide

Historic energy sector

liberalization, fundamental shift for the

hydrocarbons sector

Exchange rate will continue to show volatility

Federal Budget cuts through

2017

Government elections in June

2016

Foreign Direct Investments (FDI)

05

101520253035404550

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

US

D B

illio

nThe Bajío and

Northern regions

continue to lead FDI index

Trans Pacific Partnership

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

A holistic approach to an investment in MexicoMexico: What is expected for the future?

Page 17

Strategic decisions

Do I have a clear objective?

What are my capabilities and limitations?

How do I better use my resources?

Do I understand the risks involved?

Am I planning for the future?

Implementation

Hiring employees Location and

construction Setting up a company Importing my

machinery Fiscal structure and

compliance Legal compliance Avoid mistakes

“I don't know, what I don't know”

Operational aspects

Legal Customs duties Tax Labor and labor unions Government affairs Environmental Negotiations and

culture Quantifying the risks

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

A holistic approach to an investment in MexicoOptimize for today Build for tomorrow

Page 18

Labor/Expats

Costs and savings

Local practices and processes

Timing/long term desicions

Infrastructure

Suppliers reliabillty

Every state is differentGBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

A holistic approach to an investment in MexicoIssues to consider

Page 19

Attracting and retaining the talents

A broader risk perspective at the time of decision making and a stronger control framework during execution

Optimize the real estate portfolio through careful selection and hands on negotiation

Drive down cost and adapt more quickly to changes in the market

Optimize the tax scheme and incentives

Supply chain/logistics network modeling (inbound and outbound) and rough cut plant footprint model

Optimize the implementation of the project (HR, real estate, incentives, legal…)

Optimizing market reach and product/service mix to exploit new customer opportunities, achieve better returns and mitigate risk

Human capital

PMO

Real estate

Market reach

Location Analysis

Risk mgt.

Tax and incentives

Operational flexibility

Transfor-mation

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

A holistic approach to an investment in MexicoWhat is right for you?

Page 20

Phase 1

Location Screening and

in-depth analysis

Step 1

Strategic Assessment

Step 2

Location Screening

Step 3

Financial Analysis

Phase 2

Community evaluations,

negotiation, site selection and

agreement

Step 4

Community evaluations

Step 5

Incentives and site negotiation

Step 6

Legal structuring and purchase

agreement

Step 7

Compliance and on-going analysis

Interest in investing in Mexico

Success is accomplished when promises are fullfilled

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

A holistic approach to an investment in MexicoHow do you evaluate it?

Page 21

Operations

Tax/Treasury

R&D/ Technology

Sustainability

GeneralCounsel

Finance

Human resources

Government relations

Facilities/Real estate

Integrated Incentives Strategy

Federal authorities

State authorities

Municipal authorities

Government

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

A holistic approach to an investment in MexicoBuilding bridges with the Government

Page 22

Tax benefits Payroll tax subsidyAcquisition tax discountOwnership tax Licenses.

GrantsInfrastructure grantsCash grantsLand donation or free-use agreementsMachinery and equipment grantsInvestment promotion programs

Labor grantsJob trainingScholarshipsLabor grants

Federal programsINADEM fund (entrepreneurship)CONACYT fund (R&D)Sectorial fundsInnovation fundsProsoft (software)Proind (productivity)Proiat (technology)Prologyca (logistics)

Cost AbatementsInfrastructure support, land preparation and other costs

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

A holistic approach to an investment in MexicoIncentives Opportunities

Page 23

Choose the right partner

7 July 2015

Focus on your objectives

Understand the risks

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

A holistic approach to an investment in MexicoConclusion

Page 24

III. Renewable energies in Mexico

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Page 25 GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Ranking RECAI

Macro vitals

► Economic stability

► Investor climate (ease of doing business)

► Security & supply

► Clean energy gap

► Affordability

► Political stability► Support for

renewables

► Energy market access

► Infrastructure (&distributed generation)

► Finance (cost, availability & transaction liquidity)

► Natural resource► Power offtake

attractiveness► Political support► Technology

maturity► Forecast growth &

pipeline

Onshore windOffshore windSolar PVSolar CSPBiomassGeothermal Small hydroMarine

Energy imperative

Policy enablement

Project delivery

Technology potential

Renewable energies in MexicoMethodologyWhat makes a market attractive?

Page 26 GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Increased attractiveness compared to previous index

Decreased attractiveness compared to previous index

United States

1

China

2India

3Ch

ile4

Germany

5

Brazil

6

Mexico

7

France

8

Canada

9

Australia

10

South Africa

11

Japan

12

United Kingdo

m

13

Morocco

14

Denm

ark

15

Egypt

16

Argentina

18

Turkey

19

Belgium

20

Nethe

rland

s

17

Renewable energies in MexicoWhat’s the actual ranking?

Page 27 GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

2014 2015 2016

Q1 Q2 Q3 Q1 Q2 Q3 Q1

Issued RECAI‘s

Mexico’s tendency

Mexico jumps from position 30 to 27, thanks to energy market reforms.

High electricity prices, strong project pipelines and planned capacity auctions led Mexico up to the 25th place.

Mid-June saw Mexico officially enact its energy reform package

High electricity prices, strong project pipelines and planned capacity auctions led Mexico up to the 22th place.

New legislation appears in order to set out a detailed road map for achieving 35% clean energy by 2024.

The Government announced that it will move ahead with US$3.5b of investment in new wind capacity over the next three years.

The country’s first power auction marks the opening up of a multi-billion dollar market for developers and investors worldwide.

2725

2422

2019

7

Renewable energies in MexicoMexico in RECAI

Page 28 GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

EY’s second study on institutional investors’ views regarding nonfinancial reporting by issuers (publicly traded companies).

What is it?

Key 2015 findingsThis second report involved more than 200 institutional investors around the world. Some of the key findings of the 2015 study are the following:

- A majority of investors (61.5%) consider nonfinancial data to be relevant to all industrial sectors today.

- With the impact of environmental and social changes on commercial enterprises accelerating 37.0% of investors today use a structured, methodical approach to analyzing nonfinancial information.

- Investors are enthusiastic about the benefits of integrated reporting; 70.9% see integrated reports as essential or important, ranking them second in usefulness behind only companies’ annual reports.

- A noteworthy 59.1% of respondents consider corporate social responsibility (CSR) reports to be essential or important to investment decisions.

“The evidence shows that once you start producing nonfinancial reports, you start managing these issues more effectively, and you save a significant amount of money.“

Renewable energies in MexicoTomorrow’s Investment Rules 2.0

Page 29 GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Renewable energies in MexicoTomorrow’s Investment Rules 2.0: Investor interest in nonfinancial information spans all sectors

Page 30

IV. Taxes in Mexico

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Page 31

Country MexicoStatutory corporate

income tax ("CIT") rate 30%

Alternate Minimum Tax None

Capital Gains Tax rate 25% with no deductions allowed or 35% on the net gain provided that certain requirements are met

Loss carryforward 10 years

Withholding Tax rates

Dividends 10% or 40% on payments to Tax Heavens

Interest Regular rate: 35% or 40% on payments to Tax Heavens (special rates: 4.9%, 10%, 15% and 21%)

Royalties 25% or 40% on payments to Tax Heavens

Services 25% (services paid by foreign residents, without PE, might be exempted under certain conditions)

Operating leases 25% on leasing of movable and real property

VAT/Sales Tax 16% ; 0% for certain foods and medicines as well as exportations

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Taxes in MexicoTax Overview at a Glance

Page 32

Country Mexico

Employee profit sharing10% of the adjusted taxable income of the business (Is not a deductible expense,

but reduces taxable income)

Thin capitalization rules 3:1

Other relevant taxes

Real Estate Transfer Tax (acquisition) raging from 2% to 4% Real Estate Property Tax raging from 0.4% to 1% of the property´s unitary value Payroll Tax ranging from 1% to 3% depending on the state where employee

carries on the work Social security contributions: individual pays 2.935%% of his salary and employer

pays 29.53% of the employee's salary

Tax treaties Over 50 tax treaties

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Taxes in MexicoTax Overview at a Glance (continued)

Page 33

► Tax and Legal Model reflecting Business Model

For Manufacturing: e.g. Toll Manufacturer, Toll Manufacturer under Maquila Regime, Contract Manufacturer, Licenced Manufacturer, Fully Fledge Manufacturer

For Distribution: e.g. Market Support, Agent, Limited Risk Distributor, Licensed Distributor, Fully Fledge Distributor.

For other operations e.g. R&D, Procurement, SSC, services, etc

► Customs duties and VAT implications of the models► Contractual Framework► Holding Structure► Fixed or Variable Capital► Financing Scheme► Permanent establishment risk► Convenience of an APA► Deduction of start-up costs► Employee profit sharing model► Tax efficient employee compensation► Social security

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Taxes in MexicoKey Tax Considerations when Operating in Mexico

Page 34

► Multiple sources of information: Electronic Accounting, Tax Return and TP Informative Return, Voluntary Statutory Tax Report (i.e., Dictamen Fiscal), Form 76 (Relevant Transactions), Contemporaneous TP documentation, Industry parameters/statistics, etc.

► Wide range of tax sophistication (local Secretary of Finance vs Federal Tax Authorities)

► How prepared are you? Tax health check, defense file, APA, archiving procedures, internal resources, etc.

► Main claims of tax administration:

Existence and substance of cross border payments Strictly indispensable expenses (e.g. business purpose and benefits of the transactions) Characterization of payments Entitlement to treaty benefits Unique to Mexico: Pro-rata Expenses -Domestic Law (non-deductible) – Art 28 Income tax Law Arm´s length? Tax/Business restructures Sufficiency of the evidence

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Taxes in MexicoCorporate tax audits

Page 35 GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Taxes in MexicoCorporate tax audits (continued)

Page 36

The tax audit usually lasts 12 months. After the aforementioned period has elapsed, the observation letter (Preliminary Assessment) is notified. Afterwards, the

taxpayer has 20 legal days to refute the findings of the authority. Once the observations letter has been issued, the tax authorities have up to 6 months to issue a Final Tax Assessment

(“Crédito Fiscal”). Taxpayers have an alternative to request a settlement (“Solicitud de Acuerdo Conclusivo”) before the Tax Ombudsman

(“Prodecon”). This procedure interrupts the 6 months period for issuing the Final Tax Assessment. Should the negotiations fail, the taxpayer can opt for an Administrative Appeal. After the Administrative Appeal, and

subject to a financial guarantee, it can opt for the Nullity Trial. The chart below depicts the process:

Chances to settle in Prodecon 20% (based on 2014 info 138/673) Chance to win Nullity Trial 45% (based on last 5 years SAT won 259,043/468,499)

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Taxes in MexicoCorporate tax audits (continued)

Page 37

V. Q & A/Wrap-Up

GBN Webcast – Mexico: Supercharged for the future © 2016 EYGM Limited

Thank you!

Page 39

EY | Assurance | Tax | Transactions | Advisory

About the global EY organization

The global EY organization is a leader in assurance, tax, transaction and advisory services. We leverage our experience, knowledge and services to help build trust and confidence in the capital markets and in economies the world over. We are ideally equipped for this task — with well trained employees, strong teams, excellent services and outstanding client relations. Our global purpose is to drive progress and make a difference by building a better working world — for our people, for our clients and for our communities.

The global EY organization refers to all member firms of Ernst & Young Global Limited (EYG). Each EYG member firm is a separate legal entity and has no liability for another such entity’s acts or omissions. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

For more information, please visit www.ey.com.

© 2016 EYGM LimitedAll Rights Reserved.

ED None

This material has been prepared for general information purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

www.ey.com