global equities: risks and opportunities the advice exchange – national pd day dom giuliano...

TRANSCRIPT

Global equities: risks and opportunities

The Advice Exchange – National PD Day

Dom GiulianoPortfolio Manager

This presentation (‘Presentation’) has been produced by Magellan Asset Management Limited (‘Magellan’) ABN 31 120 593 946, AFS Licence No 304 301 and has been prepared for informational and discussion purposes only and does not constitute an offer to sell or a solicitation of an offer to purchase any security or financial product or service. Any such offer or solicitation shall be made only pursuant to a Product Disclosure Statement, Information Memorandum or other offer document (collectively ‘Offer Document’) relating to a Magellan financial product or service. A copy of the relevant Offer Document relating to a Magellan product or service may be obtained by calling Magellan on +61 2 8114 1888 or by visiting www.magellangroup.com.au. This Presentation does not constitute a part of any Offer Document issued by Magellan. The information contained in this Presentation may not be reproduced, used or disclosed, in whole or in part, without the prior written consent of Magellan.

Past performance is not necessarily indicative of future results and no person guarantees the performance of any Magellan financial product or service or the amount or timing of any return from it. There can be no assurance that a Magellan financial product or service will achieve any targeted returns, that asset allocations will be met or that a Magellan financial product or service will be able to implement its investment strategy and investment approach or achieve its investment objective.

Statements contained in this Presentation that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Additionally, this Presentation may contain “forward-looking statements”. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements.

Certain economic, market or company information contained herein has been obtained from published sources prepared by third parties. While such sources are believed to be reliable, neither Magellan or any of its respective officers or employees assumes any responsibility for the accuracy or completeness of such information. None of Magellan or any of its respective officers or employees has made any representation or warranty, express or implied, with respect to the correctness, accuracy, reasonableness or completeness of any of the information contained in this and they expressly disclaim any responsibility or liability therefore. No person, including Magellan has any responsibility to update any of the information provided in this Presentation.

Neither this Presentation nor the provision of any Offer Document issued by Magellan is, and must not be regarded as, advice or a recommendation or opinion in relation to a Magellan financial product or service, or that an investment in a Magellan financial product or service is suitable for you or any other person. Neither this Presentation nor any Offer Document issued by Magellan takes into account your investment objectives, financial situation and particular needs. In addition to carefully reading the relevant Offer Document issued by Magellan you should, before deciding whether to invest in a Magellan financial product or service, consider the appropriateness of investing or continuing to invest, having regard to your own objectives, financial situation or needs. Magellan strongly recommends that you obtain independent financial, legal and taxation advice before deciding whether to invest in a Magellan financial product or service.

Important Information

Agenda

01 United States

02 Interest rate risk

03 China

04 Europe

05 Tailwinds of growth

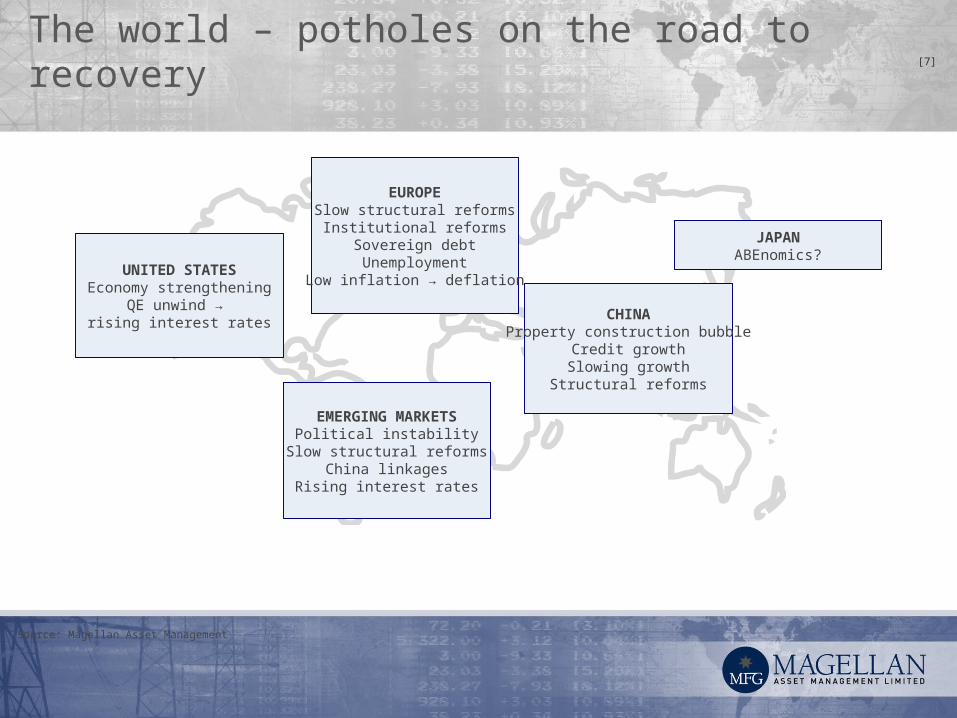

The world – potholes on the road to recovery

Source: Magellan Asset Management

[7]

UNITED STATESEconomy strengthening

QE unwind → rising interest rates

EMERGING MARKETSPolitical instability

Slow structural reformsChina linkages

Rising interest rates

EUROPESlow structural reforms

Institutional reformsSovereign debtUnemployment

Low inflation → deflation

CHINAProperty construction bubble

Credit growthSlowing growth

Structural reforms

JAPANABEnomics?

United States

SECTION: 01

Note: Data as at 5/9/14

Source: Federal Reserve; Bureau of Labour Statistics; Dept. of Commerce; ISM; US Census Bureau; Bloomberg; US

Treasury

US economic indicators are strengthening

Indicator Latest 1 year ago

Unemployment 5.8% 7.2%

Non-farm payroll employment (last 6 month avg.) 235k 205k

House starts 1.0m 0.9m

Industrial production (yoy growth) 4.3% 3.4%

Bank loans & leases (yoy growth) 6.5% 2.3%

Retail sales (yoy growth) 3.3% 2.5%

Capital goods new orders, ex defence & aircraft (yoy growth)

7.8% 7.7%

Auto sales (yoy growth) 7.9% 5.7%

ISM non-manufacturing PMI 57.1pts 55.1pts

Federal budget balance (% of GDP) -2.9% -3.8%

US RecoveryImprovement in the labour market is real

2006 2008 2010 2012 201462%

63%

64%

65%

66%

67%

0%

2%

4%

6%

8%

10%

12%

Participation rate (LHS)

Unemployment rate (RHS)

US labour market

Improvement in the labour market is

real

• US is creating 2.7m new jobs p.a.1

• 9.6m unemployed as at Aug.

2014, down from 15.4m peak in

Oct. 2009

• Employment only 0.2m below all

time high of 147m in Nov. 2007

• Falling participation is only part of

the story; much of this is

structural change with ageing.

1. Based on past six months of non-farm payroll data annualisedSource: BLS; Bloomberg; Magellan

Source: US Federal Reserve; Bureau of Economic Analysis; Magellan

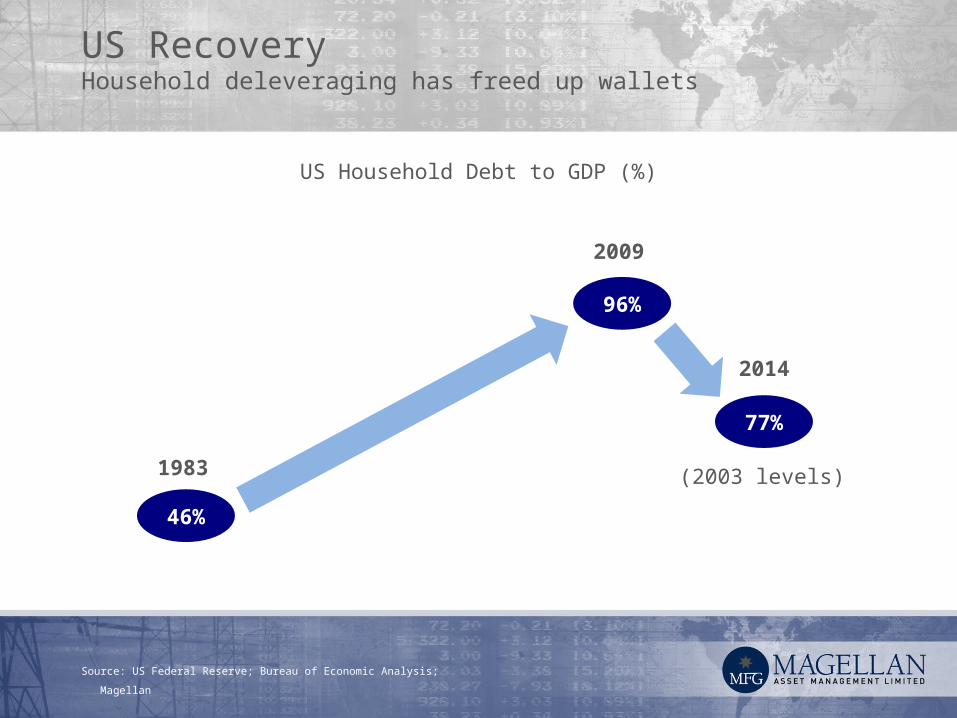

US RecoveryHousehold deleveraging has freed up wallets

96%

2009

46%

1983

77%

2014

(2003 levels)

US Household Debt to GDP (%)

US RecoveryHome building is heading back to ‘normal’

Note: Monthly data at a Seasonally Adjusted Annual Rate (SAAR)Source: US Department of Commerce; Bloomberg; Magellan

1993 2003 20130.0

0.5

1.0

1.5

2.0

2.5

Anticipated demand = 1.3-1.4m

US Housing Units Started (millions annualised)

Interest rate risk

SECTION: 02

Source: Bloomberg; Magellan

US Treasury and Bund yields are near record lows

1998 2000 2002 2004 2006 2008 2010 2012 20140%

1%

2%

3%

4%

5%

6%

7%

US Treasuries avg 2008-2014: 2.8%

US Treasuries avg 1998-2007: 4.9%

Treasuries

10 year US Treasury and German Bund yields

Fed announces QE

Bunds

Italian and Spanish yields are also at record lows

Source: Thomson Reuters

1991 1996 2001 2006 20110%

2%

4%

6%

8%

10%

12%

14%

16%

Spain

Italy

5/9/14Italy: 2.3%Spain: 2.0%

10 year Italian and Spanish sovereign yields

In 1994, the US Federal Reserve raised interest rates 250bps after ~1.5 years on hold

Sep-07

Sep-08

Sep-09

Sep-10

Sep-11

Sep-12

Sep-13

Sep-14

$0b

$1,000b

$2,000b

$3,000b

$4,000b

$5,000b

US Federal Reserve assets

Source: US Federal Reserve; Magellan

US Treasury securities

Mortgage-backed securities

Other

~25% of US

GDP

5x

‘Quantitative Easing’ has taken us into unchartered waters

Orderly exit

• Steady US recovery; gradual increase in credit

• US short term interest rates ~2-3%

• US 10 year Treasury yields ~4.5-5.5%

• Elevated market volatility; dramatic repricing of some assets

Disorderly exit

• Sharp US recovery; strong demand for credit

• Market loses faith in Federal Reserve’s ability to exit QE

• US 10 year Treasury yields ~8-10%

• Large & rapid falls in asset prices

• Potential emerging markets & Eurozone crisis

Most likely

‘Fat tail’

Two scenarios

China

SECTION: 03

Credit has exploded since 2008

31 Dec 2008 31 Dec 20130%

50%

100%

150%

200%

250%

128%

217%

+89% pts

China credit to GDP Dollar value of credit growth

equivalent to US banking system

Debt service ratio 30% of GDP p.a.

Central and local govt debt 56% of

GDP

Source: Fitch; Economist; Societe Generale; Magellan Asset Management

Credit has helped fuel a housing boom

Note: Demand estimate assumes normalised completions increase with income and household formation.Source: National Bureau of Statistics

2001 2006 2011 20160.0

0.5

1.0

1.5

2.0

2.5

China housing completions

Billion sqm

?

Rapid credit growth since

GFC

~3-4 years excess supply

Anticipated housing demand

Estimated housing

vacancy rate: 22%

China’s economy is slowing

Source: National Bureau of Statistics; Bloomberg; CEIC; Magellan

Average growth p.a. 2000-2008

2009-2013

2014

Real GDP growth 8.9% 9.0% 7.5%

Credit growth (Financial institution domestic currency loans)

14.0% 19.0% 13.4%

Steel production 15.0% 10.8% 4.4%

Electricity production 10.9% 12.0% 5.3%

Cement production 10.7% 10.5% 5.3%

Housing floor space sold 20.6% 15.3% -9.4%

Europe

SECTION: 04

EuropeChallenging economic backdrop

• “Too much debt” remains a problem for banks, households, governments

• Country level reforms occurring at varying paces

• Fighting to prevent deflation

• Russia has added to the difficulties

• ECB has underpinned markets with its “do whatever it takes” rehetoric….and now a European version of QE.

Themes and stocks that present opportunities

Data and Device Explosion

Cashless Society

Internet/eCommerce

Emerging Market Consumer

US Housing Recovery

Rising US Interest Rates

Key Investment Tailwinds

2013 % of Sales from Emerging Markets

2013 Emerging Markets growth rate (YOY)

Yum! Brands 60%* -18%***

Unilever 56.7% 8.7%

Danone 53% 10%**

Coca-Cola 40%** 6%**

Nestle 44% 9%

Growing Emerging Market Consumption

Source: Company filings & Magellan estimates. *% of operating profit. ** Magellan estimates. *** China business impacted by Avian Bird Flu scare and poultry supply concerns

Quality multinationals are already embedded

Magellan investment opportunitiesTechnology and payments 31% of Magellan’s portfolio

Huge and growing online

audience

Device innovation enabling

connectivity and mobility

E-commerce / payments

Advertising

Technology enabled

enterprises

Magellan Global Fund Portfolio As at 30 June 2014

Consumer Defensive; 17.6%

Mass-Market Retail; 14.5%

Health Care; 7.7%

Internet & eCommerce; 6.3%Information Technology; 12.2%

Consumer Discretionary; 7.2%

Payments; 11.9%

Financials; 12.7%

Media Content and Distribution; 5.5%

Cash; 4.4%

Questions?