global industry analysis and the quest for comparability philadelphia, pa december 2, 2003 andrew b....

TRANSCRIPT

GLOBAL INDUSTRY ANALYSIS AND THE

QUEST FOR COMPARABILITY

Philadelphia, PADecember 2, 2003

Andrew B. Williams, CFA PresidentPhiladelphia International Advisors, LP

2

Total Return Analysis - MSCI EAFE Value Versus MSCI EAFE

(December 31, 1974 through September 30, 2003)

Since 1974, a valuation based approach has provided alpha in international markets

Cumulative Total Return

(December 1974=$100)

$4,450

$2,599

$1,413

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

74 76 78 80 82 84 86 88 90 92 94 96 98 00 02

MSCI EAFE Value MSCI EAFE MSCI EAFE Growth

Historical 12-Month Returns

MSCIEAFEValue

MSCIEAFE

MSCIEAFE

GrowthAnnualized Return 14.1% 12.0% 9.6%Maximum Return 109.1% 103.7% 100.2%Minimum Return -24.2% -28.3% -37.9%

Standard Deviation 22.4% 22.5% 23.3%Negative Return Frequency 24.0% 26.9% 29.9%Average Negative Return -9.1% -10.6% -12.7%

Avg Return/St Dev 0.63 0.53 0.41

3

Historically, international value stocks have outperformed growth stocks 73% of the time.

Relative 12-Month Total Returns(December 31, 1975 through September 30, 2003)

Sources: FactSet, MSCI EAFE (based on monthly US dollar equivalent returns), and PIA Investment Research

4.0%

4.3%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

19751977197919811983198519871989199119931995199719992001

Rela

tive

12

-Mon

th R

etu

rn

25/75 Percentiles10/90 Percentiles5/95 Percentiles

Median

Historical International Value versus Growth Analysis

4

International Equity ResearchStandard Analysis Options

Restate all figures to some comparable basis - US GAPP or local GAAP

Focus on cash flow and create DCF based valuation comparisons

Analyze valuations locally, ignoring the differences between countries

5

6

Non-synchronized economies

Capital market disparities - inflation, interest rates, valuation, tax

Accounting standards - earnings and balance sheet distortions

– Goodwill/acquisition accounting– Depreciation - term and rates vary– Inventory valuation - LIFO/FIFO– Forex gains/losses– R&D treatment– Asset revaluation– Pension liability disclosure– Special expenses & revenue

Non-uniform disclosure (annuals vs interim's)

It’s a big job - EAFE has 1000 companies and MSCI All World ex US has 1700!

Alternative #1

Global Sector Equity Analysis

7

Alternative #2

DCF-Based Approach

Where: FCF Yr1: Free cash flow year 1, etc. R: WACC TY: Terminal year of forecasting period G: Free cash flow growth rate in perpetuity

Advantages:

Conceptually accurate

Eliminates accounting issues: Free cash flow is free cash flow

Firm Value = FCF Yr1 + FCF Yr2 + FCF Yr3…..(FCF TY+1)/(R - G) (1+R)^1 (1+R)^2 (1+R)^3 (1+R)^TY

8

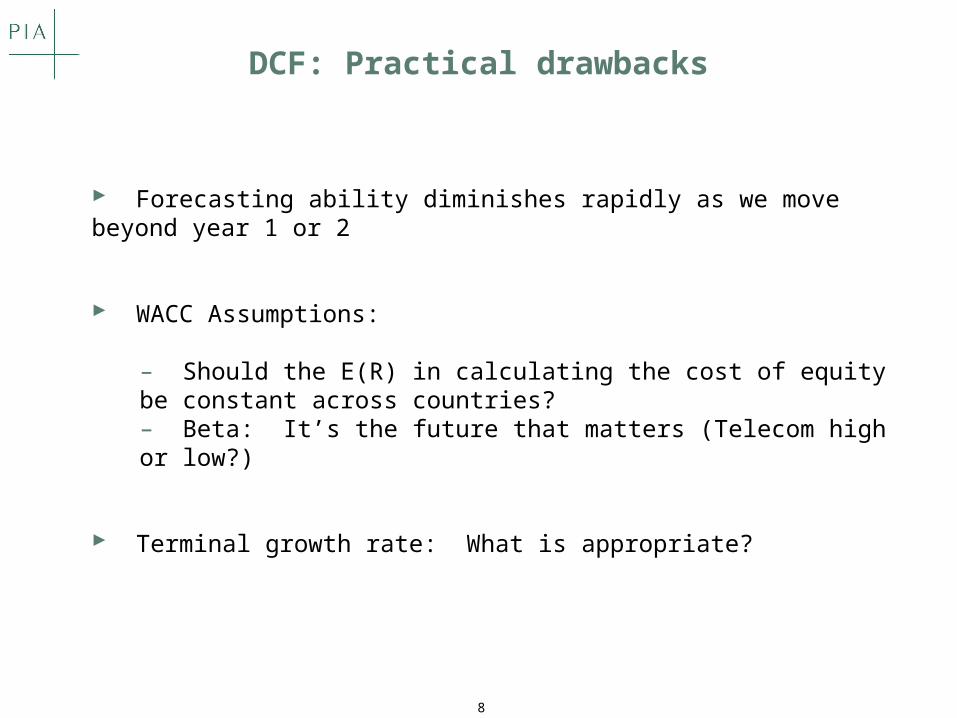

DCF: Practical drawbacks

Forecasting ability diminishes rapidly as we move beyond year 1 or 2

WACC Assumptions:

– Should the E(R) in calculating the cost of equity be constant across countries?– Beta: It’s the future that matters (Telecom high or low?)

Terminal growth rate: What is appropriate?

9

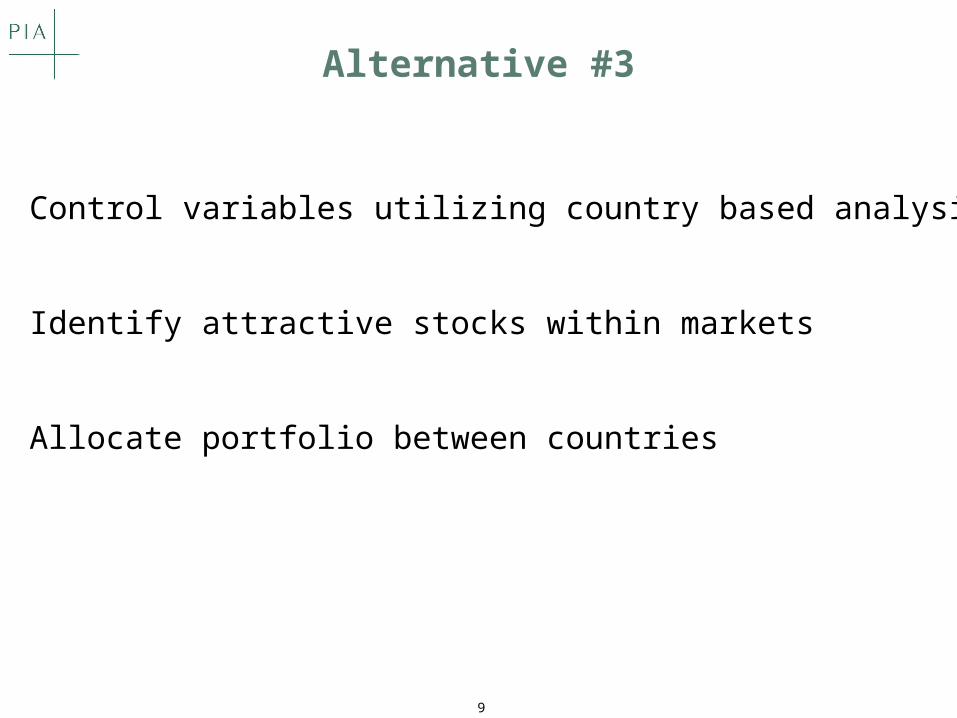

Alternative #3

Control variables utilizing country based analysis

Identify attractive stocks within markets

Allocate portfolio between countries

10

Top Quintile Versus Average Stock Performance

Monthly Returns From September 1991 through September 2003

MSCI EAFE

AverageExc/Def Return/Return St Dev Risk

Dividend Yield 0.73 2.43 0.30Price to Earnings 0.63 2.70 0.23Price to Book Value 0.66 3.22 0.21Price to Cash Flow 0.65 2.43 0.27Price to Sales 0.40 2.25 0.18

EV/EBITDA 0.46 2.07 0.22EAFE Equal Weighted 0.82 2.41 0.34

Sources: PIA Investment Research and FactSet (Alphatesting with MSCI EAFE constituents)

Within EAFE, all valuation metrics have identified investment opportunities

11

Valuation Factor Performance

Top Quintile* Versus Average Stock

1992 through September 2003 YTD

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003ytd

Highest P/E P/B P/B P/E Div Yld EV/EBITDA P/S EAFE P/E Div Yld Multifactor P/B

0.2% 73.0% 20.3% 20.7% 27.2% 6.7% 26.8% 27.3% 13.7% 8.8% 11.6% 57.2%

Div Yld P/E P/S Div Yld P/E Multifactor P/CF Div Yld Div Yld Multifactor P/E P/S

-1.1% 66.4% 20.0% 18.8% 27.0% 4.3% 23.8% 21.5% 13.2% 2.4% 10.0% 52.6%

EV/EBITDA Div Yld P/CF P/CF Multifactor EAFE EAFE P/B Multifactor P/E Div Yld Multifactor

-1.3% 59.0% 13.7% 15.6% 22.9% 2.1% 20.3% 21.1% 12.7% -2.4% 8.9% 46.2%

Multifactor P/CF Multifactor Multifactor EV/EBITDA P/CF P/B Multifactor P/CF P/B P/CF P/CF

-4.0% 58.2% 13.6% 15.5% 20.9% -1.8% 18.0% 21.1% 11.0% -3.2% 6.3% 46.1%

P/B P/S EV/EBITDA P/B P/B Div Yld Avg Stock P/CF P/B EV/EBITDA EV/EBITDA P/E

-5.1% 57.7% 12.6% 14.7% 16.3% -2.3% 15.2% 19.1% 11.0% -3.5% 4.9% 39.2%

Avg Stock Multifactor Avg Stock EAFE P/CF P/E Multifactor P/E P/S P/CF P/B EV/EBITDA

-6.2% 57.3% 10.4% 11.6% 16.2% -12.5% 15.0% 18.7% 6.9% -6.7% 2.3% 37.7%

P/S Avg Stock EAFE EV/EBITDA P/S P/S EV/EBITDA Avg Stock EV/EBITDA P/S P/S Div Yld

-9.4% 50.4% 8.1% 10.3% 9.0% -14.9% 13.9% 18.7% 1.9% -7.0% -4.2% 36.6%

P/CF EV/EBITDA P/E Avg Stock Avg Stock Avg Stock Div Yld EV/EBITDA Avg Stock Avg Stock Avg Stock Avg Stock

-10.4% 45.2% 6.6% 9.5% 9.0% -15.3% 10.7% 16.2% -2.8% -14.0% -9.2% 34.8%

EAFE EAFE Div Yld P/S EAFE P/B P/E P/S EAFE EAFE EAFE EAFE

Lowest -11.8% 32.9% 2.9% 8.0% 6.4% -25.0% 1.6% 15.0% -14.0% -21.2% -15.7% 18.8%

*Top Quintile returns are based on the equally-weighted total returns of the most attractively ranked stocks (top 20%) for each factor within a given year.

Source: FactSet (Alphatesting - MSCI EAFE Universe, monthly rebalancing, no transaction costs assumed)

Some value factors don’t work every yearMultifactor valuation models smooth out performance over time

12

Valuation Based Approach Effective in Individual Markets

Historical12-Month Returns Value Growth Difference Value Growth Difference Value Growth Difference Value Growth Difference Value Growth Difference

Average 13.6% 12.1% 1.5% 16.8% 14.3% 2.6% 11.4% 7.9% 3.5% 12.6% 6.1% 6.5% 10.6% 6.4% 4.2%

Maximum 57.8% 62.5% -4.6% 122.7% 112.9% 9.8% 163.1% 173.3% -10.1% 150.5% 151.5% -1.1% 108.4% 150.4% -42.0%Minimum -19.1% -41.2% 22.1% -31.0% -35.9% 5.0% -28.1% -52.6% 24.5% -37.4% -47.8% 10.5% -35.2% -75.7% 40.6%

Standard Deviation 13.9% 19.1% -5.1% 22.5% 21.4% 1.1% 27.1% 31.8% -4.7% 31.8% 34.7% -2.9% 20.5% 31.7% -11.3%Negative Frequency 13.4% 19.2% -5.8% 21.7% 20.8% 1.0% 28.8% 35.9% -7.1% 31.0% 43.9% -12.9% 28.8% 34.4% -5.5%Average Negative -5.9% -13.7% 7.8% -8.2% -11.1% 3.0% -11.3% -14.6% 3.4% -15.1% -17.2% 2.1% -10.3% -16.4% 6.1%

Avg Return/ St Dev 0.98 0.64 0.34 0.75 0.67 0.08 0.42 0.25 0.17 0.40 0.18 0.22 0.52 0.20 0.32

Sources: Glenmede/ PIA Investment Research, based on monthly returns (US dollar equivalent) per FactSet and MSCI Value and Growth Indices

United States CanadaJapanGermanyUnited Kingdom

13.6%12.1%

Value Growth

16.8%

14.3%

Value Growth

11.4%

7.9%

Value Growth

12.6%

6.1%

Value Growth

10.6%

6.4%

Value Growth

1975 to 2002

13

Sources: PIA Investment Research and FactSet (Alphatesting with MSCI EAFE constituents)

Top Quintile Versus Average Stock PerformanceMonthly Returns From September 1991 through September 2003

JapanUnited Kingdom

AverageExc/Def Return/Return St Dev Risk

AverageExc/DefReturn St Dev

Return/Risk

Dividend Yield 0.71 2.98 0.24 Dividend Yield 0.52 2.50 0.21Price to Earnings 1.08 2.66 0.41 Price to Earnings 0.51 2.18 0.23Price to Book Value 0.42 2.79 0.15 Price to Book Value 0.73 3.23 0.23Price to Cash Flow 0.88 2.84 0.31 Price to Cash Flow 0.65 2.25 0.29Price to Sales 0.49 3.36 0.15 Price to Sales 0.32 3.39 0.10

EV/EBITDA 0.65 2.51 0.26 EV/EBITDA 0.41 2.31 0.18UK Equal Weighted 0.95 2.67 0.36 Japan Equal Weighted 0.74 2.25 0.33

Germany France

Average AverageExc/Def Return/ Exc/Def Return/Return St Dev Risk Return St Dev Risk

Dividend Yield 0.94 3.04 0.31 Dividend Yield 0.32 3.00 0.11Price to Earnings 0.57 3.47 0.17 Price to Earnings 0.36 2.62 0.14Price to Book Value 0.63 4.09 0.15 Price to Book Value 0.66 4.17 0.16Price to Cash Flow 0.34 3.76 0.09 Price to Cash Flow 0.48 3.23 0.15Price to Sales 0.40 3.99 0.10 Price to Sales 0.75 3.79 0.20

EV/EBITDA -0.04 3.66 -0.01 EV/EBITDA 0.15 2.83 0.05Germany Equal Weighted0.55 3.59 0.15 France Equal Weighted0.61 3.21 0.19

Valuation factor efficacy varies across markets

14

Cash Flow/Price RatioHistorical Factor Analysis

Alternative Holding Period Returns September 1991 to September 2003

Information RatioAverage Excess/(Deficit) Return Positive Frequency

Highest Quintile versus Average

12.57%

16.91%

.65%1.87%

3.46%

6.65%

%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1-M 3-M 6-M 12-M 24-M 36-M

Exc

ess/

(Def

icit

) R

etu

rn

Highest Quintile versus Average

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1-M 3-M 6-M 12-M 24-M 36-M

Info

rmat

ion

Rat

io

Highest Quintile versus Average

84% 85%

75%71%69%

64%

%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1-M 3-M 6-M 12-M 24-M 36-M

Pos

itiv

e F

req

uen

cy

Data Source: FactSet

Information RatioAverage Excess/(Deficit) Return Positive Frequency

Lowest Quintile versus Average

(.51)%(1.47)%

(2.90)%

(5.63)%

(15.15)%

(11.70)%

-16.0%

-14.0%

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

.0%

1-M 3-M 6-M 12-M 24-M 36-M

Exc

ess/

(Def

icit

) R

etu

rn

Lowest Quintile versus Average

(0.23)

(0.35)(0.47)

(0.63)

(1.05)(1.00)

(1.2)

(1.0)

(0.8)

(0.6)

(0.4)

(0.2)

0.0

1-M 3-M 6-M 12-M 24-M 36-M

Info

rmat

ion

Rat

io

Lowest Quintile versus Average

40%34% 31%

22%

12% 15%

%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1-M 3-M 6-M 12-M 24-M 36-MP

osit

ive

Fre

que

ncy

Like good wines, value factor returns improve with age

15

January 1979 - December 2002

Data Source: FactSet and MSCI

Average 12-Month Return and Standard Deviation

8%

9%

10%

11%

12%

13%

14%

15%

16%

17%

10% 15% 20% 25% 30%

Standard Deviation

Ave

rag

e 1

2-M

on

th R

etu

rn

Average Excess Return and Information Ratio

-1%

0%

1%

2%

3%

4%

5%

6%

7%

(0.2) (0.1) 0.0 0.1 0.2 0.3 0.4 0.5

Information RatioA

vera

ge E

xcess

Retu

rn

Maximize IR

Equal-Weight

MSCI EAFE

P/E

P/CE

P/B

Yield

Rel P/E

Rel P/CE

Rel P/B

Rel Yield

Inexpensively Valued Markets Outperform

16

17

Alternative #3A“Belt and Suspenders”

Utilize country rankings

Evaluate equities within a regional sector basis

Blend inputs from country/sector analysis

Check behind the numbers

18

*Based on International Stocks of over $1 Billion Market Capitalization (US$ as of October 2003) in the MSCI EAFE Index

MSCI EAFE Large Cap Stocks*Average R-Squared for Country, Sectors and Macro

International Stock Prices continue to reflect Higher Correlations to Country Factors!

(Rolling 30-Month Stock Price Changes)

Sources: Philadelphia International Advisors with monthly stock prices from FactSet.

16.0%

6.7%

22.6%

0%

10%

20%

30%

40%

50%

10/034/0310/024/0210/014/0110/004/0010/994/9910/984/9810/974/9710/96R-S

qu

are

d (

Roll

ing

30

-Mon

th)

Country Sector Macro

Country Versus Sector Correlation Analysis

19

MSCI EAFE Large Cap Stocks*Average R-Squared for Country and Economic Sectors

(Rolling 30-Month Stock Price Changes)

Country Versus Sector Correlation Analysis

*Based on International Stocks of over $1 Billion Market Capitalization (US$ as of October 2003) in the MSCI EAFE Index

United Kingdom Germany

Japan Ireland

Sources: Philadelphia International Advisors with monthly stock prices from FactSet.

6.0%7.0%

0%

10%

20%

10/0310/0210/0110/0010/9910/9810/9710/96

R-S

qu

are

d (

Roll

ing

30

-Mon

th)

Country Sector

19.0%

7.0%

0%

10%

20%

30%

10/0310/0210/0110/0010/9910/9810/9710/96

R-S

qu

are

d (

Roll

ing

30

-Mon

th)

Country Sector

14.7%

10.7%

0%

10%

20%

30%

10/0310/0210/0110/0010/9910/9810/9710/96

R-S

qu

are

d (

Roll

ing

30

-Mon

th)

Country Sector

12.6%

2.8%0%

10%

20%

30%

10/0310/0210/0110/0010/9910/9810/9710/96

R-S

qu

are

d (

Roll

ing

30

-Mon

th)

Country Sector

20

Country Versus Sector Correlation Analysis

MSCI EAFE Large Cap Stocks*Average R-Squared for Country and Economic Sectors

(Rolling 30-Month Stock Price Changes)

*Based on International Stocks of over $1 Billion Market Capitalization (US$ as of October 2003) in the MSCI EAFE Index

Consumer Staples Industrials

Sources: Philadelphia International Advisors with monthly stock prices from FactSet.

Energy Technology

8.9%

24.0%

0%

10%

20%

30%

10/0310/0210/0110/0010/9910/9810/9710/96

R-S

qu

are

d (

Roll

ing

30

-Mon

th)

Country Sector

17.7%

2.1%0%

10%

20%

30%

10/0310/0210/0110/0010/9910/9810/9710/96

R-S

qu

are

d (

Roll

ing

30

-Mon

th)

Country Sector

17.6%

13.3%

0%

10%

20%

30%

10/0310/0210/0110/0010/9910/9810/9710/96

R-S

qu

are

d (

Roll

ing

30

-Mon

th)

Country Sector

10.8%

23.2%

0%

10%

20%

30%

10/0310/0210/0110/0010/9910/9810/9710/96

R-S

qu

are

d (

Roll

ing

30

-Mon

th)

Country Sector

21

Japanese Sector - Selected Valuation FactorsTop Quintile Versus Average Stock Performance

Monthly Returns From August 1996 through September 2003

Average AverageExc/Def Return/ Exc/Def Return/Return St Dev Risk Return St Dev Risk

Price to Earnings 0.67 3.67 0.18 Price to Earnings 0.83 3.45 0.24Price to Book 0.55 3.36 0.16 Price to Book 0.87 5.03 0.17

Price to Cash Flow 0.80 3.62 0.22 Price to Cash Flow 0.92 4.23 0.22Dividend Yield 0.30 3.54 0.09 Dividend Yield 1.02 4.28 0.24EV to EBITDA 0.69 3.19 0.22 EV to EBITDA 0.23 3.57 0.06

Price to Sales 0.26 4.51 0.06 Price to Sales 0.70 4.73 0.15

Equal Weighted Mix 1.10 2.89 0.38 Equal Weighted Mix 1.14 3.43 0.33

Average AverageExc/Def Return/ Exc/Def Return/Return St Dev Risk Return St Dev Risk

Price to Earnings 0.48 3.58 0.13 Price to Earnings 0.90 4.38 0.21Price to Book 0.71 4.59 0.15 Price to Book 0.59 3.91 0.15

Price to Cash Flow 1.10 2.65 0.42 Price to Cash Flow 0.28 5.99 0.05Dividend Yield 0.68 4.02 0.17 Dividend Yield 1.28 4.13 0.31EV to EBITDA 0.17 2.95 0.06 EV to EBITDA 0.47 3.62 0.13

Price to Sales 0.28 5.77 0.05 Price to Sales 0.12 6.06 0.02Equal Weighted Mix 0.98 3.02 0.32 Equal Weighted Mix 0.84 3.76 0.22

Sources: PIA Investment Research and FactSet (Alphatesting with MSCI EAFE constituents)

Discretionary Sector Materials Sector

Industrials Sector Staples Sector

22

Average AverageExc/Def Return/ Exc/Def Return/Return St Dev Risk Return St Dev Risk

Price to Earnings 1.10 3.62 0.30 Price to Earnings 0.89 2.44 0.36Price to Book 0.72 3.20 0.23 Price to Book 1.03 3.38 0.30

Price to Cash Flow 0.85 3.25 0.26 Price to Cash Flow 0.64 2.76 0.23

Dividend Yield 0.88 3.16 0.28 Dividend Yield 0.91 2.99 0.30EV to EBITDA 0.76 3.44 0.22 EV to EBITDA 0.44 2.43 0.18

Price to Sales 0.72 3.62 0.20 Price to Sales 1.00 3.26 0.31

Equal Weighted Mix 1.00 3.17 0.32 Equal Weighted Mix 1.08 2.63 0.41

Average AverageExc/Def Return/ Exc/Def Return/Return St Dev Risk Return St Dev Risk

Price to Earnings 1.04 2.57 0.41 Price to Earnings 0.77 3.41 0.23Price to Book 0.54 2.89 0.19 Price to Book 0.41 3.49 0.12

Price to Cash Flow 0.29 3.36 0.09 Price to Cash Flow 0.86 4.52 0.19Dividend Yield 0.90 2.78 0.32 Dividend Yield 1.32 2.51 0.52EV to EBITDA 0.54 2.35 0.23 EV to EBITDA 0.30 3.39 0.09

Price to Sales 0.12 3.36 0.04 Price to Sales 0.23 3.75 0.06

Equal Weighted Mix 0.99 2.89 0.34 Equal Weighted Mix 0.78 3.64 0.21

Sources: PIA Investment Research and FactSet (Alphatesting with MSCI EAFE constituents)

Industrials Sector Staples Sector

Monthly Returns From August 1996 through September 2003

Discretionary Sector Materials Sector

European Sector - Selected Valuation FactorsTop Quintile Versus Average Stock Performance

23

Country Versus Sector Correlation Analysis

October 2003

SectorMaterials

Consumer DiscretionaryConsumer StaplesIndustrialsTechnologyEnergyFinancialsHealth CareCommunicationsUtilities

*Based on International Stocks of over $1 Billion Market Capitalization (US$ as of October 2003) in the MSCI EAFE Index

Source: PIA Investment Research (Based on rolling 30-month sector and country r-squareds from monthly stock prices from FactSet)

CountrySector CountrySector CountrySector CountrySector

51% 49% 72% 28% 69% 31% 77% 23% 70% 30% 85% 15% 84% 16% 88% 12% 20% 80% 38% 62% 35% 65% 44% 56% 74% 26% 88% 12% 86% 14% 90% 10% 31% 69% 52% 48% 49% 51% 59% 41% 20% 80% 39% 61% 36% 64% 45% 55% 67% 33% 83% 17% 81% 19% 86% 14% 38% 62% 61% 39% 58% 42% 67% 33% 19% 81% 37% 63% 34% 66% 43% 57% 16% 84% 32% 68% 29% 71% 37% 63%

United Kingdom Germany Spain Japan

24

25

P/E Calculated on Stated Earnings

#1

#2

#3

Heineken Interbrew Asahi

Net Sales 9011 6992 1375267Cost of Goods Sold * 4196 3403 956827Depreciation & Amortization 486 5.4% 641 9.2% 51545 3.7%Gross Profit 4329 2948 366895SG & A 3047 2171 297551Operating Profit 1282 777 69344Interest Expense-Net 146 147 4172Extraordinary Charges 0 -96 -25072non-Operating Inc/ Exp 85 131 7614Pre-Tax Income 1221 665 32486Tax 364 162 21197Minority Interest 62 36 3468Other Income 0 0 0Net Income 795 467 14757

EPS 2.03 1.08 28.91

Trailing 2002 P/ E, excluding special charges 15.5x 16.1x 12.0x

Interbrew looks relatively expensive - but what about depreciation?

26

P/E Calculated on Adjusted Earnings

Heineken Interbrew Asahi

Net Sales 9011 6992 1375267Cost of Goods Sold * 4196 3403 956827Depreciation & Amortization 486 5.4% 377 5.4% 74264 5.4%Gross Profit 4329 3212 344176SG & A 3047 2171 297551Operating Profit 1282 1041 46625Interest Expense-Net 146 147 4172Extraordinary Charges 0 -96 -25072non-Operating Inc/ Exp 85 131 7614Pre-Tax Income 1221 1025 9767Tax 364 30% 275 27% 3613 37%Minority Interest 62 36 3468Other Income 0 0 0Net Income 795 714 9622

EPS 2.03 1.66 18.87

Trailing 2002 P/ E, excluding special charges 15.5x 12.7x 18.8x#3

#2

#1

Interbrew is cheapest after adjustments

27

Coming soon…….IASInternational Accounting Standards Board

Mandates convergence of various standards closer to U.S. GAAP, but differences will remain.

Investor friendly reforms will facilitate global sector analysis and company comparisons.

European Union adoption 1/1/05.

Accounting Standards Board of Japan (ASBJ) has not agreed to converge.

To state compliance with IAS standards, a company must comply with all provisions.

28

Summary

Fundamental valuation analysis can exploit pricing inefficiencies in international stocks

Multi factor approach raises return, lowers risk

Country and sector based approaches are both effective

Effectiveness of country and sector models varies across regions and sectors

Further “hands-on” analysis can add insight beyond database

IAS will facilitate cross border analysis, but issues remain

29