globalization and the automotive industry: is indonesia ... · 1 globalization and the automotive...

TRANSCRIPT

1

Globalization and the Automotive Industry:

Is Indonesia missing out?

Abstract

International trade in automotive and auto parts has grown rapidly during the last two decades but

Southeast Asia largest economy, Indonesia, is lagging behind in its export performance. This paper uses

comparative perspective in examining Indonesia's role in automotive production networks in the context of

the contemporary debate on opportunities for reaping gains from economic globalization through

engagement in global production sharing. Panel data regression on all countries for period 1988-2007 is

applied to analyse factors affecting a country’s participation in global production networks. The regression

result suggests that a country's ability to gain from global production sharing depends more on the service

link factors than production cost factors. Indonesia is indeed left behind in export side but not on the

import side of the global production network. The major factors which affect Indonesian condition are the

costly business practice and low quality of institutions and legal certainty which discourage foreign

investor

Keywords: automotive, auto parts, globalization, product fragmentation, global production networks,

Indonesia, Thailand.

Moekti P. Soejachmoen

PhD Candidate

Arndt-Corden Department of Economics

Crawford School of Economics and Government

Australian National University

9 June 2011

2

I. Introduction

International trade in automotive and auto parts is growing rapidly in the last two decades where

the growth of automotive production reached the highest annual growth during the period 1989-

2000 with almost 5% growth per annum. There is a shift in a global production pattern from the

North America and European countries dominance in 1960 to Japanese dominance in 1970s and

1980s. And for the last twenty years some developing countries increased their production shares in

global market.

The participation of developing countries in automotive industry was made possible by the

technology development and innovations in telecommunication and transportation, which enable

automotive industry to fragment the production process into smaller segments in which

components of productions or assemblies can be relocated to different places based on cost

advantages. The relocation of segmented production process creates global production networks.

However Indonesia as the largest economy in Southeast Asian seems to miss out the opportunity to

reap gains from the globalization in the automotive industry.

This paper examines from a comparative perspective Indonesia's role in automotive production

networks in the context of the contemporary debate on opportunities for reaping gains from

economic globalization through engagement in global production network. Automotive industry is

considered as vital ingredients in national economic development strategies therefore government

involvement in automotive industry is quite intense. Therefore it is necessary to evaluate the role of

government policies in Indonesia on the development of the industry. Analysis on the dynamics of

Indonesian automotive industry is important to ascertain the impacts of government regulation on

the industry and determine Indonesian position in the global automotive industry.

A pooled panel data regression is undertaken to determine the factor affecting countries'

participation in production network in the automotive industry which has become increasingly

globalized over the past two decades. The regression result suggests that a country's ability to gain

from global production sharing depends crucially on labour cost as well as the quality of institutions

and legal certainty. Trade facilitation, procedures to start a new business and certainty in enforcing

the contract affect the participation more than production cost and market size factors. On the

import side, real exchange rate (RER), tariff and market size are the determinants of the

participation in the global production networks. A comparison with Thailand, which has became a

major hub of automotive production for the regional and global markets, suggests that Indonesia is

missing out because most of these preconditions were not present in the Indonesian economy.

This paper is structured as follows: Section 2 discusses the globalization in the automotive industry

started with the overview then further discusses the development of global production network in

the automotive industry. Section 3 discusses the product fragmentation theory as a basic theory in

3

explaining the global production networks. Section 4 describes Indonesian automotive industry and

its position on global automotive production and trade. Section 5 presents the analytical framework

which includes model specification, variable constructions and data, and estimation method. Section

6 reports the result and discussion. Section 7 concludes.

II. Globalization in Automotive Industry

The automotive industry is one of the biggest in the world and employs more than eight million

people making the vehicles directly, and more than forty million people indirectly through related

manufacture and services sectors (OICA, 2007). In principle, the automotive industry is an assembly

industry, where more than a thousand parts and components are produced by independent

industries. Dicken (2003) categorized the major processes in the automotive industry prior to the

final assembly process into the manufacture of bodies, of components and of engines (as shown in

Figure 1).

Figure 1:

The automotive industry has experienced a transformation from its inception in the late 19th

century, when France and Germany were the largest automotive producers but with small domestic

markets (Simarmata, 2007). The first transformation began at the beginning of the 20th century

with the introduction of Fordist mass production in the US. Fordist mass production is a moving

MAJOR

SUPPLYING

INDUSTRIES

Bodies

Components

1. Manufacture of mechanical and electrical

components (e.g. Instruments, carburettors,

braking systems, steering components, etc)

2. Manufacture of wheels, tyres, seats,

windscreens, exhaust systems, etc.

Engines and transmissions

Consumer

Market

Final

Assembly

Manufacture

and stamping of

body panels

Body

assembly

and painting

Forging and

casting of

engine and

transmissions

components

Machining

and assembly

of engines

and

transmission

Steel and other

metals

Rubber

Electronics

Plastic

Glass

Textiles

Source: Dicken, 2003

4

assembly line developed by Henry Ford in 1913. During the 1920s the US car production contributed

84% of world car production and in 1929 it started to export 10% of its production, which

accounted for 35% of the world market. The expansion of the US production urged the European

governments to protect their domestic car producers and promote their national automotive

industries.

The second transformation occurred at the end of 1950s with the implementation of the General

Agreement of Tariff and Trade (GATT). The significant reduction in tariffs integrated the markets

and enabled the European automotive producers to expand their markets with their specialization

on small cars which were energy-efficient. At the beginning of the 1980s the US’s domination of the

world’s automotive producers started to decline, while European production increased.

The third transformation occurred in the 1970s when Japan started to penetrate the world market

with their new lean production system. This new system enabled Japan to produce automotive more

efficiently compared to the US and Europe, with far fewer employees and a “just-in-time” system

compared to the “just-in-case” system operating in the US. The expansion of the Japanese automotive

industry threatened domestic production in the US and Europe and urged the US and European

governments to apply interventionist policies such as import quotas, tariffs and Voluntary Export

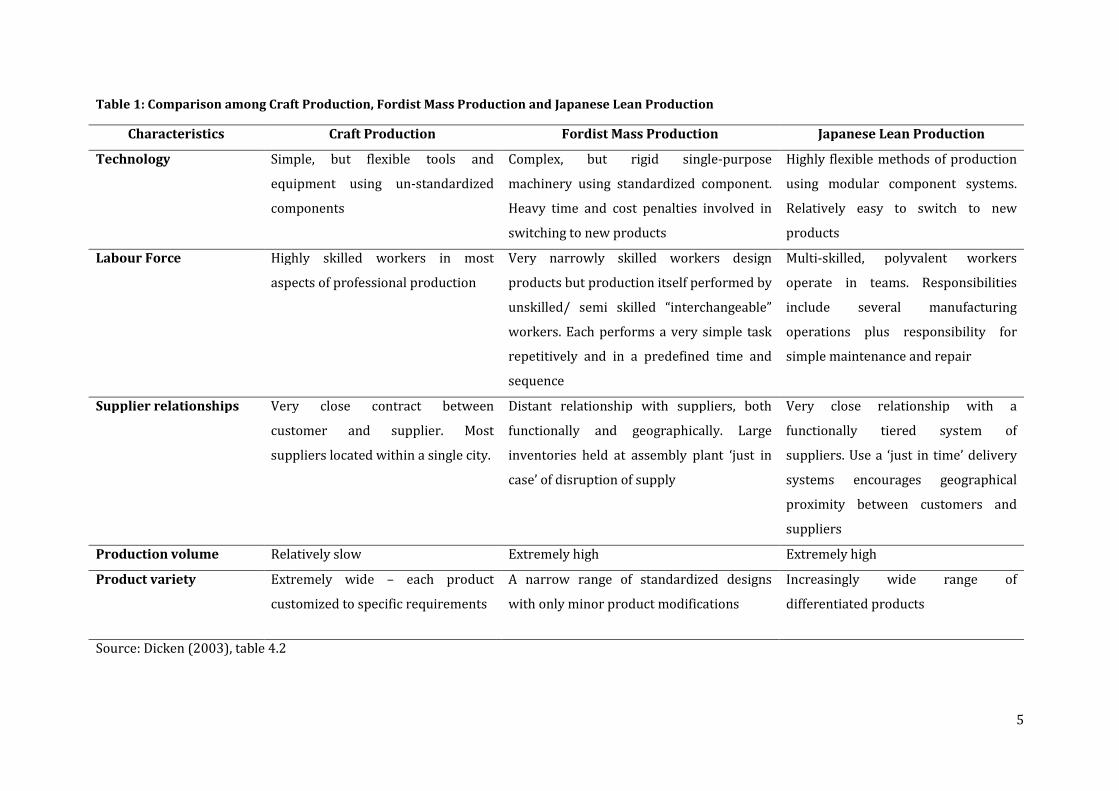

Restriction (VER). The differences between craft production, Fordist mass production and Japanese

lean production is summarized in Table 1.

Since 2000 China became one of the major car producers in the world and since 2008 it replaced

Japan’s position as the second largest car producer. India also shown significant growth in their car

production and its share in the global car production increased significantly from 1.5% in early 2000

to almost 5% in 2010.

Along with the continuous transformation, global automotive production experienced a change of

pattern as shown in Table 2. Global production of automobiles was dominated by North America and

European countries in 1960. North America contributed more than 50% of automotive production

while European countries shared almost 40% of global production or around 13 thousand units. The

US and Germany were the two main producers of automobiles during that period. During the 1970s

and 1980s Japan showed a dramatic development in the automotive production with an almost 55

fold increase in production and experienced 15% annual growth which increased its share of global

production increased from only 1.3% in 1960 to 28% in 1989. In the late 1990s, China started to

enter global automotive production with relatively high level of production at more than 2 million

units. This lowered the dominance of Germany, the US and Japan. The automotive production

reached its highest annual growth during the period 1989-2000, with almost 5% growth per annum.

However, in 2000, Canada, South Korea and Malaysia experienced higher growth compared to other

countries. This reflects the spread of technology from the US and Japan to surrounding countries.

5

Table 1: Comparison among Craft Production, Fordist Mass Production and Japanese Lean Production

Characteristics Craft Production Fordist Mass Production Japanese Lean Production

Technology Simple, but flexible tools and

equipment using un-standardized

components

Complex, but rigid single-purpose

machinery using standardized component.

Heavy time and cost penalties involved in

switching to new products

Highly flexible methods of production

using modular component systems.

Relatively easy to switch to new

products

Labour Force Highly skilled workers in most

aspects of professional production

Very narrowly skilled workers design

products but production itself performed by

unskilled/ semi skilled “interchangeable”

workers. Each performs a very simple task

repetitively and in a predefined time and

sequence

Multi-skilled, polyvalent workers

operate in teams. Responsibilities

include several manufacturing

operations plus responsibility for

simple maintenance and repair

Supplier relationships Very close contract between

customer and supplier. Most

suppliers located within a single city.

Distant relationship with suppliers, both

functionally and geographically. Large

inventories held at assembly plant ‘just in

case’ of disruption of supply

Very close relationship with a

functionally tiered system of

suppliers. Use a ‘just in time’ delivery

systems encourages geographical

proximity between customers and

suppliers

Production volume Relatively slow Extremely high Extremely high

Product variety Extremely wide – each product

customized to specific requirements

A narrow range of standardized designs

with only minor product modifications

Increasingly wide range of

differentiated products

Source: Dicken (2003), table 4.2

6

Table 2: Car production by country, 1960 - 2010

Production

(000 units)

World share

(%)

Production

(000 units)

World share

(%)

Production

(000 units)

World share

(%)

Production

(000 units)

World share

(%)

Production

(000 units)

World share

(%)

EU 5,092 39.17 13,267 37.42 15,761 27.00 15,587 24.17 12,990 16.74

France 1,175 9.04 3,409 9.62 3,348 5.74 3,666 5.68 2,228 2.87

Germany 1,817 13.98 4,564 12.87 5,527 9.47 5,570 8.64 5,906 7.61

Italy 596 4.58 1,972 5.56 1,738 2.98 1,142 1.77 857 1.10

Spain 43 0.33 1,639 4.62 3,033 5.20 3,012 4.67 2,388 3.08

Sweden 108 0.83 384 1.08 301 0.52 340 0.53 217 0.28

UK 1,353 10.41 1,299 3.66 1,814 3.11 1,857 2.88 1,393 1.80

North America 6,998 53.83 7,807 22.02 15,761 27.00 14,701 22.79 9,832 12.67

Canada 323 2.48 984 2.78 2,962 5.07 2,712 4.20 2,071 2.67

USA 6,675 51.35 6,823 19.24 12,800 21.93 11,989 18.59 7,761 10.00

Asia 165 1.27 10,018 28.26 17,113 29.32 22,535 34.94 38,616 49.76

China .. .. .. .. 2,069 3.54 5,234 8.12 18,265 23.53

India .. .. .. .. 801 1.37 1,511 2.34 3,537 4.56

Indonesia .. .. .. .. 293 0.50 408 0.63 705 0.91

Japan 165 1.27 9,052 25.53 10,141 17.37 10,512 16.30 9,626 12.40

Malaysia .. .. 94 0.27 283 0.48 472 0.73 568 0.73

South Korea .. .. 872 2.46 3,115 5.34 3,469 5.38 4,272 5.50

Thailand .. .. .. .. 412 0.71 928 1.44 1,645 2.12

South America 96 0.74 1,282 3.62 3,957 6.78 4,155 6.44 6,710 8.65

Argentina 30 0.23 112 0.32 340 0.58 260 0.40 717 0.92

Brazil 38 0.29 731 2.06 1,682 2.88 2,317 3.59 3,648 4.70

Mexico 28 0.22 439 1.24 1,936 3.32 1,577 2.45 2,345 3.02

Total 12,999 100.00 35,455 100.00 58,374 100.00 64,496 100.00 77,610 100.00

Notes: .. : data not available

Source: 1960 and 1989 data: Dicken (2003)

2000, 2005 and 2010 data: International Organization of Motor Vehicle Manufacturers

2010

Country

1960 1989 2000 2005

7

An important characteristic of the auto parts is that there are few fully generic parts and

components which can be used in a wide variety of final products without extensive customization

such as in the electronics industry. This characteristic limits auto parts firms in reaching economies

of scale in production and economies of scope in design. The relationship between auto parts

suppliers and car assemblers are typically captive and relational. Many components are relatively

heavy compares to electronics industry therefore relocation to close proximity is preferable to a

more distant location. This condition leads to agglomeration in the automotive industry.

Sturgeon et al (2008) argue that the dispersion of the automotive industry has a nested geographical

and organizational structure. Global integration occurred through buyer-supplier relationships,

especially between car makers and their largest suppliers. Production tends to organize regionally

or nationally, where parts and components which are bulky and heavy tend to locate in close

proximity with the assembler to ensure on-time delivery and to save transportation costs.

Meanwhile smaller, lighter and standardized parts and components can be located at a distance to

take advantage of lower labour cost and economies of scale. Vehicle development is concentrated in

a few design centres. As a result, local, national and regional production networks in automotive

industry are nested within the global organization and structures of the largest car maker firms.

There are three large regional clusters in the automotive industry: Europe, North America and Asia.

Within a region there is a tendency to shift investment locations to lower operating cost countries,

such as Mexico in North America, Spain and Eastern Europe in the European region and to Thailand

and China is Asia. Auto parts are more heavily traded within a region compared to the finished

goods. Within a country, production and employment are concentrated in a location which provides

better infrastructure and which in turn lowers the service link costs.

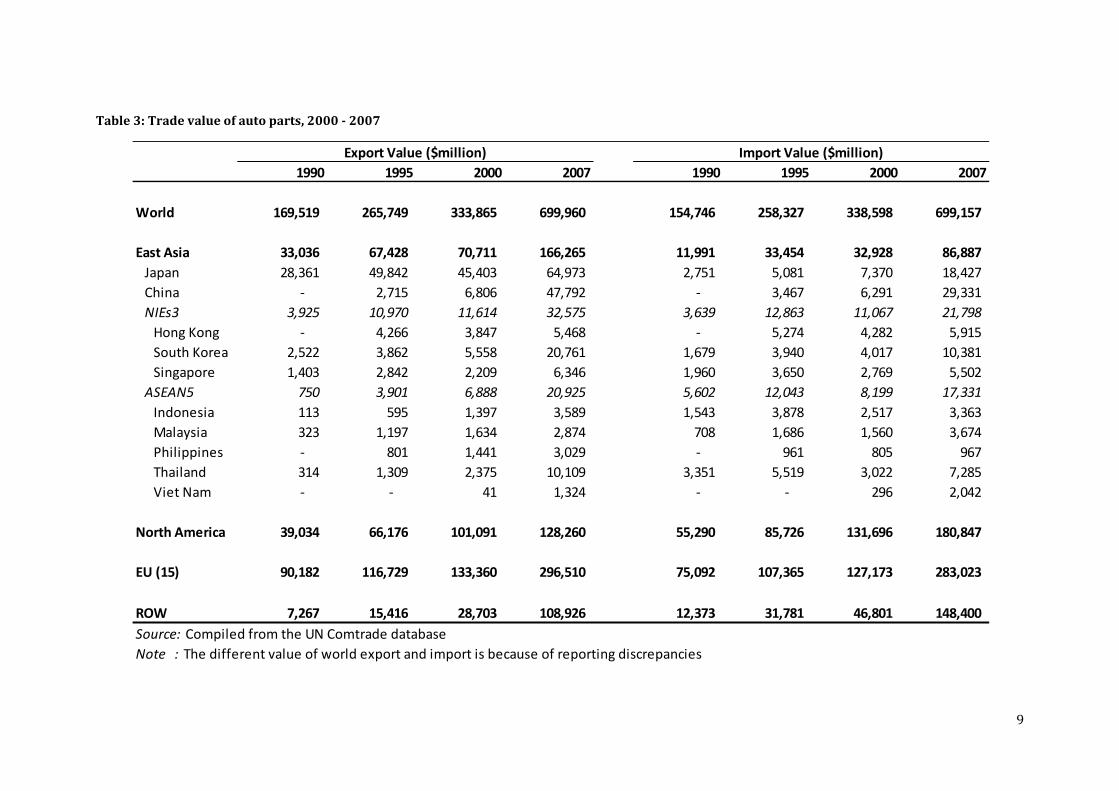

World’s auto parts trade increased significantly from $170 billion in 1990 to almost $700 billion in

2007, with an annual growth of 8.7% which reflects the higher intensity of global production

networks in the automotive industry (see Table 3). The world auto parts trade is dominated by the

EU(15) and North American countries. There is no significant change in the trend of auto parts trade

in the world during 1990-2007.

East Asian countries contribute less significantly in the auto parts trade compared to the electronics

parts and components trade. The share in the world auto parts trade is around 21-23% for the

period 1990-2007, which is much lower than the share in the electronics parts and components

trade (around 50% for export and 45% for import). Among East Asian countries, Japan, China, South

Korea and Thailand are the major players in the auto parts trade. Japan’s role is declining over time

with a decline in export share from 18% in 1990-1994 to 11% in 2000-2007, although it is still the

largest exporter of auto parts in Asia. Meanwhile China’s export share increased from a low 1.2% in

2000 to more than 4% in 2007. Other countries in Asia which experienced an increase in export

8

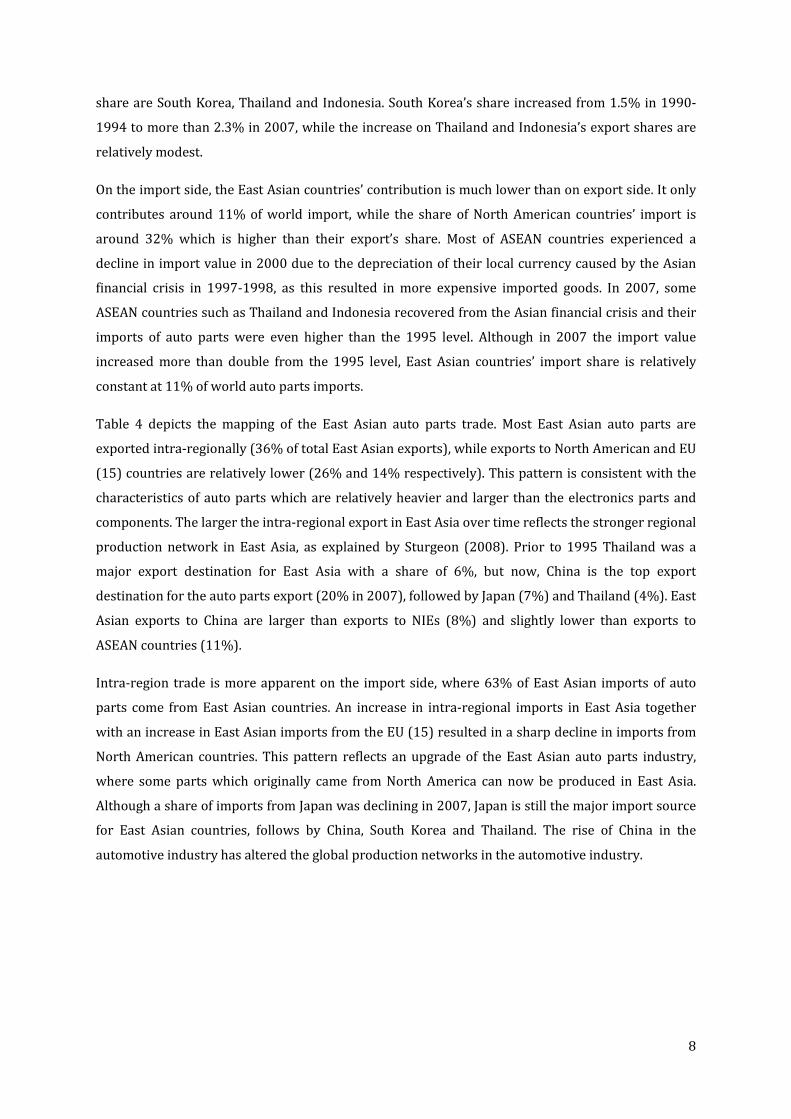

share are South Korea, Thailand and Indonesia. South Korea’s share increased from 1.5% in 1990-

1994 to more than 2.3% in 2007, while the increase on Thailand and Indonesia’s export shares are

relatively modest.

On the import side, the East Asian countries’ contribution is much lower than on export side. It only

contributes around 11% of world import, while the share of North American countries’ import is

around 32% which is higher than their export’s share. Most of ASEAN countries experienced a

decline in import value in 2000 due to the depreciation of their local currency caused by the Asian

financial crisis in 1997-1998, as this resulted in more expensive imported goods. In 2007, some

ASEAN countries such as Thailand and Indonesia recovered from the Asian financial crisis and their

imports of auto parts were even higher than the 1995 level. Although in 2007 the import value

increased more than double from the 1995 level, East Asian countries’ import share is relatively

constant at 11% of world auto parts imports.

Table 4 depicts the mapping of the East Asian auto parts trade. Most East Asian auto parts are

exported intra-regionally (36% of total East Asian exports), while exports to North American and EU

(15) countries are relatively lower (26% and 14% respectively). This pattern is consistent with the

characteristics of auto parts which are relatively heavier and larger than the electronics parts and

components. The larger the intra-regional export in East Asia over time reflects the stronger regional

production network in East Asia, as explained by Sturgeon (2008). Prior to 1995 Thailand was a

major export destination for East Asia with a share of 6%, but now, China is the top export

destination for the auto parts export (20% in 2007), followed by Japan (7%) and Thailand (4%). East

Asian exports to China are larger than exports to NIEs (8%) and slightly lower than exports to

ASEAN countries (11%).

Intra-region trade is more apparent on the import side, where 63% of East Asian imports of auto

parts come from East Asian countries. An increase in intra-regional imports in East Asia together

with an increase in East Asian imports from the EU (15) resulted in a sharp decline in imports from

North American countries. This pattern reflects an upgrade of the East Asian auto parts industry,

where some parts which originally came from North America can now be produced in East Asia.

Although a share of imports from Japan was declining in 2007, Japan is still the major import source

for East Asian countries, follows by China, South Korea and Thailand. The rise of China in the

automotive industry has altered the global production networks in the automotive industry.

9

Table 3: Trade value of auto parts, 2000 - 2007

1990 1995 2000 2007 1990 1995 2000 2007

World 169,519 265,749 333,865 699,960 154,746 258,327 338,598 699,157

East Asia 33,036 67,428 70,711 166,265 11,991 33,454 32,928 86,887

Japan 28,361 49,842 45,403 64,973 2,751 5,081 7,370 18,427

China - 2,715 6,806 47,792 - 3,467 6,291 29,331

NIEs3 3,925 10,970 11,614 32,575 3,639 12,863 11,067 21,798

Hong Kong - 4,266 3,847 5,468 - 5,274 4,282 5,915

South Korea 2,522 3,862 5,558 20,761 1,679 3,940 4,017 10,381

Singapore 1,403 2,842 2,209 6,346 1,960 3,650 2,769 5,502

ASEAN5 750 3,901 6,888 20,925 5,602 12,043 8,199 17,331

Indonesia 113 595 1,397 3,589 1,543 3,878 2,517 3,363

Malaysia 323 1,197 1,634 2,874 708 1,686 1,560 3,674

Philippines - 801 1,441 3,029 - 961 805 967

Thailand 314 1,309 2,375 10,109 3,351 5,519 3,022 7,285

Viet Nam - - 41 1,324 - - 296 2,042

North America 39,034 66,176 101,091 128,260 55,290 85,726 131,696 180,847

EU (15) 90,182 116,729 133,360 296,510 75,092 107,365 127,173 283,023

ROW 7,267 15,416 28,703 108,926 12,373 31,781 46,801 148,400

Source: Compiled from the UN Comtrade database

Note : The different value of world export and import is because of reporting discrepancies

Export Value ($million) Import Value ($million)

10

Table 4: East Asian auto parts trade: geographic composition, 1990 - 2007

Percentage 1990 1995 2000 2007

Export to

World 100.00 100.00 100.00 100.00

East Asia 20.97 32.20 28.36 35.59

Japan 0.94 2.15 4.32 6.58

China 0.96 6.12 5.97 9.88

NIEs3 7.35 9.19 7.83 7.84

Hong Kong 1.83 3.63 2.98 3.18

South Korea 3.03 2.59 2.83 3.23

Singapore 2.48 2.97 2.01 1.42

ASEAN5 11.73 14.74 10.24 11.29

Indonesia 3.49 3.94 2.79 2.89

Malaysia 2.06 3.20 2.51 2.55

Philippines 0.98 1.57 1.44 1.12

Thailand 5.16 5.81 3.01 3.79

Viet Nam 0.04 0.22 0.48 0.95

North America 43.37 35.00 35.88 25.88

EU (15) 16.92 15.69 16.95 14.41

Others 18.73 17.11 18.81 24.12

Import from

World 100.00 100.00 100.00 100.00

East Asia 56.03 59.36 59.29 62.82

Japan 48.29 43.89 32.18 23.24

China 0.72 5.08 10.95 18.88

NIEs3 3.96 5.50 6.38 7.93

Hong Kong 0.38 1.08 1.09 0.38

South Korea 2.23 2.23 3.09 6.39

Singapore 1.35 2.19 2.20 1.16

ASEAN5 3.07 4.89 9.78 12.77

Indonesia 0.21 0.51 1.66 2.83

Malaysia 1.30 1.99 2.53 1.64

Philippines 0.64 1.26 2.07 1.86

Thailand 0.92 1.10 3.12 5.37

Viet Nam 0.00 0.02 0.40 1.08

North America 16.70 14.26 15.89 9.15

EU (15) 21.52 18.59 17.36 20.99

Others 5.75 7.79 7.46 7.03

Source: Compiled from the UN Comtrade database

III. Product Fragmentation Theory

In the initial formulation, all production processes in the automotive industry were conducted in one

place as a single integrated prod

development together with innovations in telecommunication and transportatio

development of a fragmented production process which consists of more than one product

as shown in Figure 2(B). These production blocks are not independent, but are connected through

service links such as transportation, design, qua

others services. Several patterns of interdependence between production blocks and service links

can be envisaged. Figure 2(C) shows that an output of one production block can become an input for

another production block, while in Figure 2(D) a more complex relationship among production

blocks exists where there is a simultaneous operation of production blocks and the output of each of

these is assembled in the last production block. The degree of fragmen

the number of stages or production blocks. As the degree of fragmentation increases, so does the

importance of service links.

Figure 2: Production Network

Product Fragmentation Theory

, all production processes in the automotive industry were conducted in one

place as a single integrated production block as shown in Figure 2(A). However

development together with innovations in telecommunication and transportatio

development of a fragmented production process which consists of more than one product

(B). These production blocks are not independent, but are connected through

service links such as transportation, design, quality control, insurance, R&D, telecommunication and

others services. Several patterns of interdependence between production blocks and service links

can be envisaged. Figure 2(C) shows that an output of one production block can become an input for

production block, while in Figure 2(D) a more complex relationship among production

blocks exists where there is a simultaneous operation of production blocks and the output of each of

these is assembled in the last production block. The degree of fragmentation can be measured by

the number of stages or production blocks. As the degree of fragmentation increases, so does the

11

, all production processes in the automotive industry were conducted in one

2(A). However technology

development together with innovations in telecommunication and transportation promoted the

development of a fragmented production process which consists of more than one production block

(B). These production blocks are not independent, but are connected through

, R&D, telecommunication and

others services. Several patterns of interdependence between production blocks and service links

can be envisaged. Figure 2(C) shows that an output of one production block can become an input for

production block, while in Figure 2(D) a more complex relationship among production

blocks exists where there is a simultaneous operation of production blocks and the output of each of

tation can be measured by

the number of stages or production blocks. As the degree of fragmentation increases, so does the

Production network started in the

other industries such as sport footwear, automobiles, televisions and radio receivers, sewing

machines, office equipments, power and machine tools, camera and watches and printing and

publishing. One example of the global production network is Japanese car producers. Toyota, for

example, has an assembly centre for cars in Thailand. This assembly centre imports parts from

several countries in East Asia, assembles those parts and then exports the fin

other East Asian markets. Toyota also has another assembly centre for SUVs in Indonesia that

follows the same pattern where Toyota Indonesia imports parts and components from several

countries and then assemblies these parts and co

other East Asian markets.

Fragmentation theory was developed by Jones and Kierzkowski (1990). Product fragmentation is

the breaking down of the integrated process into separate stages of production (producti

which opens up new possibilities for exploiting gains from specialization. Their discussion focused

on the importance of service links in connecting fragmented production blocks.

Growth of a firm’s output level, increasing returns to scale and

encourage a firm to switch a production process from a vertically integrated process to fragmented

production blocks connected by service links. The service links include transportation,

telecommunications and various other

scale.

the electronics and clothing industries and then gradually spread into

other industries such as sport footwear, automobiles, televisions and radio receivers, sewing

machines, office equipments, power and machine tools, camera and watches and printing and

One example of the global production network is Japanese car producers. Toyota, for

example, has an assembly centre for cars in Thailand. This assembly centre imports parts from

several countries in East Asia, assembles those parts and then exports the finished cars to Japan and

East Asian markets. Toyota also has another assembly centre for SUVs in Indonesia that

follows the same pattern where Toyota Indonesia imports parts and components from several

countries and then assemblies these parts and components before exporting the SUVs to Japan and

Fragmentation theory was developed by Jones and Kierzkowski (1990). Product fragmentation is

the breaking down of the integrated process into separate stages of production (producti

which opens up new possibilities for exploiting gains from specialization. Their discussion focused

on the importance of service links in connecting fragmented production blocks.

Growth of a firm’s output level, increasing returns to scale and the advantages of specialization

encourage a firm to switch a production process from a vertically integrated process to fragmented

production blocks connected by service links. The service links include transportation,

telecommunications and various other coordination tasks, which are often subject to economies of

12

nics and clothing industries and then gradually spread into

other industries such as sport footwear, automobiles, televisions and radio receivers, sewing

machines, office equipments, power and machine tools, camera and watches and printing and

One example of the global production network is Japanese car producers. Toyota, for

example, has an assembly centre for cars in Thailand. This assembly centre imports parts from

ished cars to Japan and

East Asian markets. Toyota also has another assembly centre for SUVs in Indonesia that

follows the same pattern where Toyota Indonesia imports parts and components from several

mponents before exporting the SUVs to Japan and

Fragmentation theory was developed by Jones and Kierzkowski (1990). Product fragmentation is

the breaking down of the integrated process into separate stages of production (production blocks)

which opens up new possibilities for exploiting gains from specialization. Their discussion focused

the advantages of specialization

encourage a firm to switch a production process from a vertically integrated process to fragmented

production blocks connected by service links. The service links include transportation,

coordination tasks, which are often subject to economies of

When a firm’s output increases above Y

integrated production process Total Cost (TC

Cost (MC), or it can switch to a

flatter than TC1 because of trade

from an increased specialization of productive

caused by setting up new production blocks. With a fragmented production block, service links

emerge to connect the production blocks, therefore the total cost of the fragmented production

process increases to TC2’. Note that

cost is independent of output level. If service links cost is driven up by the level of output

is steeper than TC2.

Figure 3: Total Cost and Output

The process described in Figure

blocks and connecting service links as shown in Figure

combination of fixed cost and marginal c

declines with output. This rate of decline accelerate

When the production cost per se

production blocks becomes low enough

economic factors such as wage rates and income. Service link cost

technology in each industry.

When a firm’s output increases above Y1 as shown in Figure 3, a firm can choose either to stay at an

integrated production process Total Cost (TC1) which consists of some Fixed Cost (0A)

a fragmented production process with Total Cost of TC

because of trade-off between a lower MC and a higher FC. A lower MC is obtained

from an increased specialization of productive tasks and division of labour, while an increase in FC is

caused by setting up new production blocks. With a fragmented production block, service links

emerge to connect the production blocks, therefore the total cost of the fragmented production

’. Note that TC2 and TC2’ are parallel because we assume that service links

cost is independent of output level. If service links cost is driven up by the level of output

3 can be repeated to higher orders, creating a number of production

blocks and connecting service links as shown in Figure 4. For any degree of fragmentation the

combination of fixed cost and marginal cost within the production blocks ensures that average cost

declines with output. This rate of decline accelerates when the degree of fragmentation is higher.

per se drastically falls and the cost of the service links connecting t

production blocks becomes low enough, fragmentation will occur. Production cost relates to local

economic factors such as wage rates and income. Service link costs depend heavily on the nature of

13

, a firm can choose either to stay at an

) which consists of some Fixed Cost (0A) and Marginal

fragmented production process with Total Cost of TC2. Here, TC2 is

off between a lower MC and a higher FC. A lower MC is obtained

tasks and division of labour, while an increase in FC is

caused by setting up new production blocks. With a fragmented production block, service links

emerge to connect the production blocks, therefore the total cost of the fragmented production

’ are parallel because we assume that service links

cost is independent of output level. If service links cost is driven up by the level of output, then TC2’

can be repeated to higher orders, creating a number of production

For any degree of fragmentation the

ost within the production blocks ensures that average cost

when the degree of fragmentation is higher.

drastically falls and the cost of the service links connecting the

fragmentation will occur. Production cost relates to local

depend heavily on the nature of

Figure 4: Cost and Output under Fragmentation

Following the significant reduction

barriers, fragmentation is likely to occur first on a local or national basis and then spread to the

international market. Firms are able to take advantage of differences in technologies and factor

prices among countries in designing a more global production network. Figure

comparison between local production networks and global production networks

total cost (fixed and variable cost) when all production blocks are located in one country (Home) and

line H’ represents additional cost associated with

locate a production block in anoth

technologies available in that country. The home country has a lower marginal cost in the first

production block and the foreign country has a lower marginal cost in the second block. The cost

fragmented production with using a different location is represented in line M (Mixed)

first production block is located in the home country and second

the foreign country. Line M is flatter than line H du

links cost to connect the two production blocks allocated in the two countries is higher than the

domestic service link costs as shown by the higher fixed cost: AB (local production networks) is

lower than AC (international/global production networks). Therefore a firm will switch to an

international production network when its output level is higher than Y

: Cost and Output under Fragmentation

reduction to international coordination costs such as trade and regulatory

barriers, fragmentation is likely to occur first on a local or national basis and then spread to the

national market. Firms are able to take advantage of differences in technologies and factor

prices among countries in designing a more global production network. Figure

comparison between local production networks and global production networks

total cost (fixed and variable cost) when all production blocks are located in one country (Home) and

additional cost associated with local service links. Suppose now

locate a production block in another country in order to take advantage of factor endowments and

technologies available in that country. The home country has a lower marginal cost in the first

production block and the foreign country has a lower marginal cost in the second block. The cost

fragmented production with using a different location is represented in line M (Mixed)

first production block is located in the home country and second, the production block

the foreign country. Line M is flatter than line H due to lower marginal costs. However the service

links cost to connect the two production blocks allocated in the two countries is higher than the

domestic service link costs as shown by the higher fixed cost: AB (local production networks) is

(international/global production networks). Therefore a firm will switch to an

international production network when its output level is higher than Y2.

14

such as trade and regulatory

barriers, fragmentation is likely to occur first on a local or national basis and then spread to the

national market. Firms are able to take advantage of differences in technologies and factor

prices among countries in designing a more global production network. Figure 5 shows the

comparison between local production networks and global production networks. Line H represents

total cost (fixed and variable cost) when all production blocks are located in one country (Home) and

local service links. Suppose now that a firm can

er country in order to take advantage of factor endowments and

technologies available in that country. The home country has a lower marginal cost in the first

production block and the foreign country has a lower marginal cost in the second block. The cost of

fragmented production with using a different location is represented in line M (Mixed), where the

the production block, is located in

e to lower marginal costs. However the service

links cost to connect the two production blocks allocated in the two countries is higher than the

domestic service link costs as shown by the higher fixed cost: AB (local production networks) is

(international/global production networks). Therefore a firm will switch to an

Figure 5: Total Cost and Output: Effect of Foreign Service Links

The traditional theories of trade are still relevant in the product fragmentation theory.

of specialization according to comparative advantage is still a basis for a decision on the location of

production blocks. Both the Ricardian model on the variet

Heckscher-Ohlin model on factor prices and factor intensities provide explanations for trade within

production blocks. The results from comparative advantages add

and fragmentation as level of output increases.

complicates the analysis since it increases the number of products being traded from two products

in the traditional theory into six tradable items if each of the final products has tw

and components. The answer as

the standard considerations of comparative advantage in the production blocks, but also on the

relative cost and efficiency of service links b

2003).

Product fragmentation becomes important for a country, especially a developing country, because

first, fragmentation and component specialization eliminates the need to gain competency in all

aspects of productions and allows emerging countries to enter into the network of global production

sharing by focusing on the mastery of just one facet of the production process. Given the relative

factor endowments, a country may begin by developing compete

components of complex products and gradually move on to more capital and human

intensive activities. Moreover, by focusing on its factor endowments, it increases the industry

competitiveness as well as employment, o

access of scale economies is limited by volume of the end

: Total Cost and Output: Effect of Foreign Service Links

tional theories of trade are still relevant in the product fragmentation theory.

of specialization according to comparative advantage is still a basis for a decision on the location of

production blocks. Both the Ricardian model on the variety of factor productivities and

Ohlin model on factor prices and factor intensities provide explanations for trade within

production blocks. The results from comparative advantages add the gains from increasing returns

el of output increases. The introduction of cross-border fragmentation

complicates the analysis since it increases the number of products being traded from two products

in the traditional theory into six tradable items if each of the final products has tw

as to which country will specialize on which item depends not only on

the standard considerations of comparative advantage in the production blocks, but also on the

relative cost and efficiency of service links between any pair of countries (Kierzkowski and Arndt,

Product fragmentation becomes important for a country, especially a developing country, because

first, fragmentation and component specialization eliminates the need to gain competency in all

ects of productions and allows emerging countries to enter into the network of global production

sharing by focusing on the mastery of just one facet of the production process. Given the relative

factor endowments, a country may begin by developing competency in the more labour

components of complex products and gradually move on to more capital and human

intensive activities. Moreover, by focusing on its factor endowments, it increases the industry

competitiveness as well as employment, output and wages. When production is fully integrated, the

access of scale economies is limited by volume of the end-product. With fragmentation, volume will

15

tional theories of trade are still relevant in the product fragmentation theory. The principle

of specialization according to comparative advantage is still a basis for a decision on the location of

y of factor productivities and the

Ohlin model on factor prices and factor intensities provide explanations for trade within

from increasing returns

border fragmentation

complicates the analysis since it increases the number of products being traded from two products

in the traditional theory into six tradable items if each of the final products has two tradable parts

to which country will specialize on which item depends not only on

the standard considerations of comparative advantage in the production blocks, but also on the

etween any pair of countries (Kierzkowski and Arndt,

Product fragmentation becomes important for a country, especially a developing country, because

first, fragmentation and component specialization eliminates the need to gain competency in all

ects of productions and allows emerging countries to enter into the network of global production

sharing by focusing on the mastery of just one facet of the production process. Given the relative

ncy in the more labour-intensive

components of complex products and gradually move on to more capital and human-capital

intensive activities. Moreover, by focusing on its factor endowments, it increases the industry

utput and wages. When production is fully integrated, the

product. With fragmentation, volume will

16

rise whenever firms in one country supply not only their own industry, but foreign one as well. It is

no longer necessary for producers to master the entire production chains, therefore large and small

firms can save the learning cost and focus on component production

Based on production technology, the intensity of fragmentation depends on four factors (Lall, et.al,

2004): fist is the technical “divisibility” of the production process: not all production processes can be

divided into separate stages. Some industries have discrete stages of production and components

with different scale, skill and technology requirements which enable the stages then to be separated

and located at different locations and different ownership. Electronics and automotive

manufacturing are examples of these industries. On the other hand, the chemical industry, for

example, has continuous production process is not economically separable. Second, the factor

intensity of the process: the relocation of a production process to a low-wage site is economical only

if it is labour intensive and the reduced cost from labour is greater than the transportation and

coordination costs. Third, the technological complexity of each process: it is not always economical to

relocate a labour intensive process to a low-wage site unless the technology accompanying this

process is simple and stable enough to be conducted by low-wage countries. Finally, the value-to-

weight ratio of the product: the distance of relocation depends on the value-to-weight ratio of the

product. If the parts and components are light and of high value then the relocation of the process to

a further location in order to exploit cost differences is still economical. If the parts and components

are heavy and have low value then it is economic to relocate to proximate areas and encourage

agglomeration.

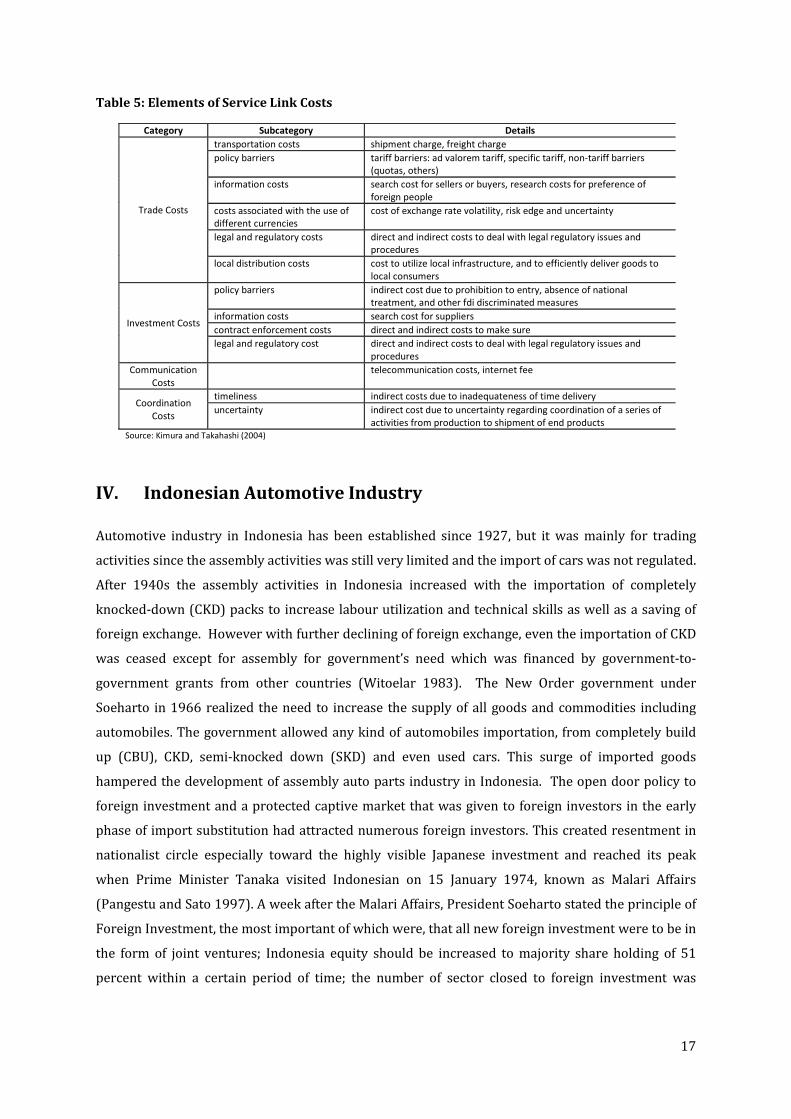

Service links are essential for production networks in order to connect production blocks into one

integrated production process. Following Kimura and Takahashi (2004) elements of service link

costs can be categorized into four groups: trade costs, investment costs, communication costs and

coordination costs.

Trade costs are those costs related to the trade of parts and components among production blocks

whether it happened in the same firm or with other firms (arm’s length firm), both domestic and

international. Most of production blocks located in foreign countries conducted through Foreign

Direct Investment (FDI) therefore investment cost is one category in total service link costs.

Openness of FDI policies, especially in developing countries, is an important factor determining

participation in global production networks. The other two categories are communication costs and

coordination costs. Innovations in telecommunication have significantly reduced the communication

costs and encouraged the development of production networks. Timeliness as one aspect in

coordination costs becomes important as a firm realizes that to hold inventories is costly. “Just-in-

time” technology developed by Japanese production networks has proven effective in holding down

production costs. Therefore infrastructure development and institutional factors are crucial

prerequisites for global production network participation.

17

Table 5: Elements of Service Link Costs

IV. Indonesian Automotive Industry

Automotive industry in Indonesia has been established since 1927, but it was mainly for trading

activities since the assembly activities was still very limited and the import of cars was not regulated.

After 1940s the assembly activities in Indonesia increased with the importation of completely

knocked-down (CKD) packs to increase labour utilization and technical skills as well as a saving of

foreign exchange. However with further declining of foreign exchange, even the importation of CKD

was ceased except for assembly for government’s need which was financed by government-to-

government grants from other countries (Witoelar 1983). The New Order government under

Soeharto in 1966 realized the need to increase the supply of all goods and commodities including

automobiles. The government allowed any kind of automobiles importation, from completely build

up (CBU), CKD, semi-knocked down (SKD) and even used cars. This surge of imported goods

hampered the development of assembly auto parts industry in Indonesia. The open door policy to

foreign investment and a protected captive market that was given to foreign investors in the early

phase of import substitution had attracted numerous foreign investors. This created resentment in

nationalist circle especially toward the highly visible Japanese investment and reached its peak

when Prime Minister Tanaka visited Indonesian on 15 January 1974, known as Malari Affairs

(Pangestu and Sato 1997). A week after the Malari Affairs, President Soeharto stated the principle of

Foreign Investment, the most important of which were, that all new foreign investment were to be in

the form of joint ventures; Indonesia equity should be increased to majority share holding of 51

percent within a certain period of time; the number of sector closed to foreign investment was

Category Subcategory Details

Trade Costs

transportation costs shipment charge, freight charge

policy barriers tariff barriers: ad valorem tariff, specific tariff, non-tariff barriers

(quotas, others)

information costs search cost for sellers or buyers, research costs for preference of

foreign people

costs associated with the use of

different currencies

cost of exchange rate volatility, risk edge and uncertainty

legal and regulatory costs direct and indirect costs to deal with legal regulatory issues and

procedures

local distribution costs cost to utilize local infrastructure, and to efficiently deliver goods to

local consumers

Investment Costs

policy barriers indirect cost due to prohibition to entry, absence of national

treatment, and other fdi discriminated measures

information costs search cost for suppliers

contract enforcement costs direct and indirect costs to make sure

legal and regulatory cost direct and indirect costs to deal with legal regulatory issues and

procedures

Communication

Costs

telecommunication costs, internet fee

Coordination

Costs

timeliness indirect costs due to inadequateness of time delivery

uncertainty indirect cost due to uncertainty regarding coordination of a series of

activities from production to shipment of end products

Source: Kimura and Takahashi (2004)

18

extended; tax incentives were reduced; and the number of foreign personnel was restricted

(Pangestu 1996).

The major government policy that supports the development of auto parts industry was Deletion

Program in 1976. By Minister of Industry Decree no 307/1976, government schedules the gradual

deletion of specific components from the imported CKD packs used in the assembly of commercial

vehicles but not in passenger cars. One objective of deletion program is to stimulate technology

transfer from Japanese auto parts industry to local manufacturer through stable, durable and intense

subcontracting relationship between large car assembling firms and the local auto parts supplier

firms. However, in reality many of components intended to be made locally was actually assembled

from imported parts and components (Aswicahyono, Basri et al. 2000). Therefore government

intention to develop local auto parts manufacturer was not achieved.

The rapid development of assembly activities started in the early 1970s because of the oil boom.

Indonesian automotive market expanded strongly at the early 1970s because of oil boom with the

increase of makes and models. The large number of varieties create very segmented and small

market for auto parts industry and unable them to reach economies of scale. In 1983, government

attempted to rationalize the automotive industry by requiring car assembler to reduce the number

of car brands and models they assembled to achieve economies of scale. The objective was to have

larger market share for each brand and to increase efficiency and lower production cost. However

this regulation was not implemented effectively because of strong rejection from vested interests in

the industry. Another decree was stipulated in 1983 on compulsory use of locally made

components. However this decree was not successful due to the lack of technology, capital and skills

in technical areas of the small and medium scale manufacturers. It resulted on reluctance of foreign

car makers to invest heavily in locally small and medium manufacturer and created shallow, short

term and non-exclusive relationship between assemblers and auto parts manufacturers.

Since there was a little success of deletion program in fostering the development of auto parts

industry in Indonesia, in 1993 government terminated the deletion program and replaced it with the

Incentive program. In this program, assembler are not forced to use locally made auto parts, instead

they will receive an incentive in the form of lower import tariff for imported parts and components if

they increase the use of locally made components (local content). The maximum tariff for imported

parts and components was 40% but it becomes zero when the local content requirements achieved

or exceeded. Local content was measured by a formula of multiplying the percentage of value added

achieved with the given weighted percentage of the component parts. Until 1995, the components

were considered local if they used 40% locally made sub-components for passenger cars and 20%

locally made sub-components for commercial cars.

19

In 1996, Soeharto signed a shocking decree appointing the Timor Putra Nasional (TPN) company

(owned by his son) as the sole manufacturer of the national car, Timor. TPN did not have one single

auto plant, with a joint venture with KIA Motor from Korea, they started to build factory in

Indonesian and meanwhile the cars were produced wholly in Korea and exported to Indonesia in

CBUs. As a national car, it received pioneer status with exempting it from import duties and luxury

sales tax. This national car program was heavily criticized by Japan, the US and the EU and they filed

complaint to WTO which then ruled that the program was a violation to WTO rules. Although the

national car program only last for a while it has big impact on automotive industry in Indonesia.

After the financial crises in 1998, Indonesia has to sign Letter of Intent under the IMF which requires

Indonesia to rapidly liberalize the market. Indonesian government introduced harmonized system

under WTO system in 1999. In this harmonized system, the local content programs were removed

and Indonesia signed the “trade-related investment measures” (TRIMS). The protectionist policy

toward automotive industry was replaced by market liberalization program. The June 1999 tariff

reform has significantly reduced the import tariff for CBU and CKD imports, but it remains relatively

high.

A frequent change in policies toward automotive industry in Indonesia creates uncertainty for both

domestic and foreign investments which in turn hampered the development of automotive industry

especially auto parts manufacturer. Transfer of technology from Japanese car makers to domestic

small and medium enterprises did not occur as expected since Japanese car makers are reluctant to

transfer the technology because they are unable to secure majority of ownership.

Automotive production network in Indonesia has developed rapidly for the last twenty years with

the increase number of car and motorcycle parts producers by three fold and four fold respectively.

The stronger local production networks are due to policies set up by Japanese car makers to

optimize local procurement for cost efficiency and minimizing exchange rate risk. However high

dependency on Japanese car makers hamper the development of domestic auto parts makers since

they are bind to a cooperation agreement which sometimes prohibit them to have cooperation with

other companies.

Although local production network in Indonesia is relatively strong, Indonesia’s position in regional

and global automotive production network is still weak. Indonesian export and import of auto parts

are relatively low compares to other countries in South East Asia. Most developing countries in East

Asia experienced an upgrade in their auto parts industry which is reflected in the change of trade

composition, especially on the export side. For example, Thailand started its export with a labour-

intensive product (wire harness) and then moved to more technology intensive products (other auto

parts and accessories), China from the assembly of radio receiver to electrical accumulator and then

to, and the Philippines from wire harness to other auto parts and accessories. Meanwhile, Malaysia

20

and Indonesia are relatively caught at assembling the same products such as radio-broadcast

receivers and resource based products, i.e. tyres. This condition reflects that Indonesia has been

relatively left behind in the automotive global production network compared to other ASEAN

countries, although it has potentials such as abundant labour and a relatively large market size.

V. Analytical Framework

The empirical model employed in this paper is based on Jones and Kierzkowski (1990)

fragmentation theory which states that fragmentation will occur when production cost per se

drastically falls and the cost of the service links connecting the production blocks become low

enough. The aim is to answer two research questions; the first is on the determinants of a country’s

participation in the global production network, and the second question is whether Indonesia is left

behind in the global production networks compared to other countries.

This research provides new contribution to the empirical studies on the global production network.

While the existing studies focused on selected countries and group of countries, this research covers

all countries in the world and cover long period from 1988 to 2007. One reason to include all

countries in this research is to enable comparison between developed and developing countries as

well as between regions. It also avoids selection bias problem which would occur if countries are

selected based on the trade value or regions.

The existing empirical studies has separately analysed the determinants of the global production

networks. Jones et al (2005) and Golub (2007) focused on the role of service link in the global

production network. Lowering of service link costs promotes fragmentation and outsourcing of

output. The first study uses the business telephone charges as a proxy of service link cost. They

compare three regions: East Asia, EU 15 and NAFTA for period 1990-2000. The result supports the

theory that lowering of business telephone charges increases the trade of parts and components.

The second study uses the index of service link quality and costs as a proxy of service links. They

construct the index consisting of consisting of transport, communications, and electric power

reliability and costs using data from around 2004. The result also supports the theory that lower

service links costs indeed improve the trade of parts and components as well as trade of final goods

and FDI inflows.

Other determinants of the global production networks are exchange rate and relative wages. Arndt

and Hummer (2004) use quarterly data for bilateral trade between the U.S. and Mexico from the first

quarter of 1989 to the fourth quarter of 2002 to examine the effect of cross-border production

sharing on the sensitivity of trade to the exchange rate and GDP. They found that the sensitivity of

exports and imports to the real exchange rate should decline when cross-border fragmentation

expands and when the share of trade associated with production networks rises.

21

Athukorala and Yamashita (2006) use the gravity model to examine the extent, trends and patterns

of the global production networks. They found that relative wage differentials are a significant

determinant of cross border trade in components (as well as the related final products).

In summary, the existing empirical studies find that global production network is explained by cost

differences among countries which consist of production cost and service links costs. The decision

on which country will specialize on which item depends not only on the comparative advantage bust

also on the relative cost and efficiency of service links.

V.1 Model Specification

The empirical model employed in this research is based on Jones and Kierzkowski (1990)

fragmentation theory which states that fragmentation will occur when production cost per se

drastically falls and the cost of the service links connecting the production blocks become low

enough. The decision on which country will specialize on which item depends not only on the

comparative advantage bust also on the relative cost and efficiency of service links. Therefore the

explanatory variables in the model can be grouped into production cost and service link costs. The

dependent variable is fragmentation index which is represented by the trade of parts and

components.

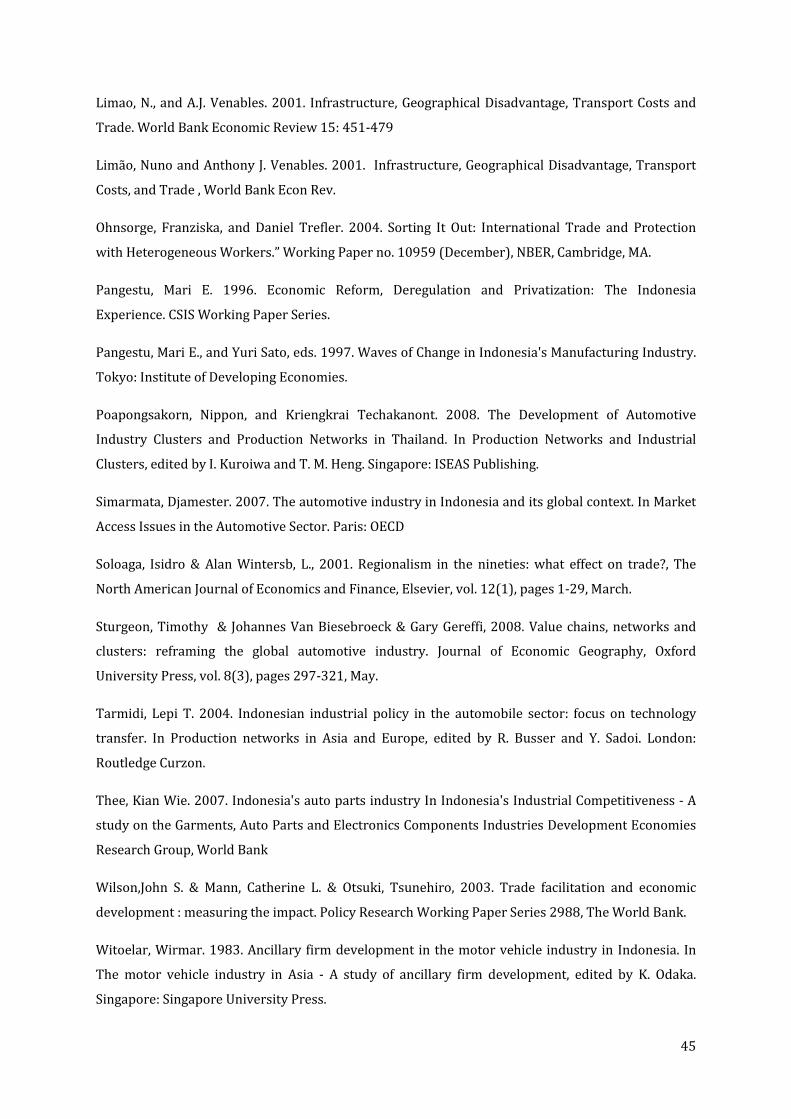

Production Costs

Production cost in this model consists of three variables: labour cost, quality of labour and

competitiveness. In the ideal model, the production cost should include capital cost as well.

However, capital cost is not included in the model because it is difficult to find comparable variable

for capital cost for all countries in the world.

Labour cost

As suggested by the standard international trade theory, comparative advantage is still relevant in

the fragmentation trade. Labour cost (RWages) is crucial in determining the location of production

block in product fragmentation. A country with lower labour cost will attract more production

blocks and will increase the fragmentation index. Therefore the expected sign for labour cost is

negative (Egger and Egger, 2005). However, the expected sign for developed countries is positive

since higher labour cost is associated with higher labour productivity and developed countries is

more conducive location for product fragmentation (Görg, 2000).

Quality of Labour

In addition to labour cost, quality of labour also determines the level of fragmentation in a country.

The heterogeneity of labour quality may determine the pattern of international specialization among

22

countries with similar aggregate factor endowments can explain the trade across industry

(Grossman and Maggi, 2000; Ohnsorge and Trefler, 2004). A country with higher technology

intensity is expected to attract more production blocks and will increase the fragmentation index.

Competitiveness

Traditionally, the appreciation of domestic currency raises import and lowers exports. However in

the production networks the relationship can reverse. The response of a country’s exports to the

exchange rate should decline as the share of imported components for use in the manufacture of its

export rises. Therefore the impact of relationship between changes in exchange rate (RER) and

trade will be negative in the presence of production networks. Moreover, as suggested by Arndt and

Hummer (2004), the sensitivity of trade to exchange rate will decline with the more intensive

fragmentation trade among countries. Then the exchange rate would not be significant in

determining the global production networks.

Service links costs

Besides the production costs listed above, the fragmentation index depends highly on service links

which connect the production blocks and ensure that the production blocks interact in the proper

manner. Basically, goods and services are traded among the production blocks both domestically

and across the border. Therefore it is possible to categorize service link cost into two types of trade

barriers, one is at-the-border trade barriers and another is behind-the-border trade barriers.

At-the-border trade barriers

Across-the-border trade barriers are barriers that affect the flow of goods and services across

countries (borders) which include freight cost and tariff and non tariff barriers.

Freight costs

One explanation of the rise in the international trade is a decline in the international transportation

costs (Hummels, 2007). The decline in the cost is associated with the innovations in transportation

and telecommunication. Mode of transportation depends on the characteristics of the goods. The

bulk commodities such as oil and petroleum products, iron ore, coal, and grains are shipped almost

exclusively via ocean cargo. Oh the other hand, commodities with high value-to-weight ratio will

choose air transportation. Nowadays, air transportation is more preferable than ocean

transportation because of the sharp decline in the relative cost of air transport.

Some studies found that trade is more sensitive to the transportation cost than import tariff. With

the more trade negotiation among countries, the trade barriers from tariffs became less important

therefore the contribution of transportation cost into total cost is rising.

23

Transportation costs co-vary with distance and it well explains the reason of countries trade with

their neighbours first. However distance is not a perfect measurement for the transportation cost

since it does not reflect the change in the quality of transportation. With the declining of air

transport cost and the technology development which enables parts and components to be relocated

in the smaller structure, long distance trade is relatively more attractive.

Therefore the expected sign of freight cost and value of trade can be either positive or negative

depends on the type of traded commodities.

Tariff

Vertical trade is more sensitive to tariff changes compares to final trade (Yi, 2003). Parts and

components are subject to a tariff every time they cross the border. Therefore any reduction in the

parts and components tariff will reduce the production cost, and the level of this reduction will

depend on how many times the fragmented product crosses the border. However, most of

production blocks are located in Special Economic Zone which might include Free Trade Zones

(FTZ), Export Processing Zones (EPZ), Free Zones (FZ), Industrial Estates (IE), Free Ports, Urban

Enterprise Zones and others. Therefore it is expected that the sign of Tariff is negative although it

might not be significant. Another type of trade barrier is Non-Tariff Barriers which are commonly

used by a country as a substitute of the abolishment of tariff barriers and are sometimes more

protective than the tariff barriers. Unfortunately the data on NTB is not widely available for all

countries; therefore it is not included in the model.

Behind-the-border trade barriers

Behind-the-border trade barriers refer to a variety of barriers that operate inside countries rather

than at the border, but that nonetheless can restrict trade. They include trade facilitation and

business and regulatory environment.

Trade Cost

Trade facilitation is generally defined as an improvement of efficiency in logistics and related trade-

enhancing infrastructure at ports and trade customs for the movement of goods in international

trade (Wilson et al, 2003). Administration burdens faced by the exporter and importer at the port

affect the transaction cost of trade flows in a country. Number of documents to be signed and the

time to finish the administration will affect the cost of exporting and importing. Therefore the

expected sign is negative. However, there is a possibility of endogeneity problem between trade

facilitation and trade flows. The higher trade flows made the role of export and import in the GDP

higher and increase the power of exporter and importer to lobby the government to improve the

trade facilitation which in turn will decrease the trade cost.

24

Business and regulatory environment

Most of the production blocks located in foreign countries conducted through Foreign Direct

Investment (FDI), therefore business and regulatory environment related to the FDI is important

factor determining participation in global production networks (Jongwanich,2009). FDI openness is

crucial in the automotive industry because with the possibility of having full foreign ownership in a

country, foreign car maker is willing to bring the latest technology and improve managerial practices

and close supervision of assembly/production by bringing in foreign technicians and managers. It is

expected that the more open the FDI policies in a country the higher the participation in a global

production network, then the expected sign of FDI_Openness is positive.

Institutional quality is relevant in the process of production fragmentation which involves

establishing a complex relationship between two parties engaging in specific investment

relationship. Expansion of production fragmentation will be limited if the quality of institutional is

low. Two indicators are used in the model to represent quality of institutions in a country; fist is the

cost of starting a new business (Buss_Cost) and second is the cost of enforcing a contract

(Contract_Cost). Long and expensive process in attaining a license for new business will discourage

not only foreign investors but also domestic investors in establishing production blocks in a country.

Meanwhile the efficiency of the judicial system in resolving a commercial dispute also affects

investment decision in a country, especially in the automotive industry where most investment is

capital intensive. The expected signs of these variables are negative.

Other variables

Market size

Trade of parts and components depends on market size of export destination and import source

countries. With a larger market size, it is expected that the trade flow of parts and components

increased. Therefore the expected sign for market size (Market) is positive.

Dummy variables

Two dummies variables are included in the model. First, the country dummy variables (C) are

included to capture the unobserved country differences such as geographical location and historical

involvement in production networks. Second, the year dummy variables (T) are included to control

for time-varying factors relating to auto parts such as technological and price changes.

Based on the discussion of the variables above, the full specification of the model can be written as

follows:

25

titi

iiti

ititi

titititi

CTMarket

CostContractCostBussOpenFDI

CostTradeTariff

TechRERRWagesFragIndx

,,10

98,7

6,5,4

,3,2,1,

___

_Distanceln

lnlnln

εϕβ

βββ

βββ

βββα

++∂++

+++

+++

+++=

where subscript i represents the i-th country, i = 1,2, .., 200, and t represent the year, t = 1988,

1989,… , 2007. The variables are listed and defined below with the expected sign of the coefficient

for independent variables in parentheses:

Frag_Indx Fragmentation Index – dependent variable

RWages Labour cost (-)

Tech Quality of labour (+)

RER Real exchange rate (-)

Distance Freight cost (+/-)

Tariff MFN tariff (-)

Trade_Cost Trade cost (-)

FDI_Open FDI openness (-)

Buss_Cost Cost for starting new business (-)

Contract_Cost Cost of enforcing the contract (-)

Market Market size (+)

T A set of time dummy variables

C A set of country dummy variables

α A constant term

V.2 Variable construction and Data

The model covers 201 countries listed in the UN database (see Appendix 1 for the list of the

country). The auto parts which are categorized into three groups based on the factor intensity using

the classification by Helg (1999) namely: (i) unskilled labour intensive, (ii) human capital intensive

and (iii) technology intensive.

The data set was assembled from four different databases: the UN Comtrade , the ILO Labosta and

Index of Doing Business and the World Development Indicators (WDI) by the World Bank . The

initial point is 1988, because it is the first year of the UN Comtrade database started reporting under

SITC Revision 3, for which the commodity listing of parts and components in this study is based on.

26

The end point is 2007, since this was the latest year for which data for most of variables are available

and data for 2008 – 2009 are susceptible from global financial crisis.

Fragmentation Index (dependent variable)

Dependent variable is the real value of export and import of parts and components. The trade data

are sourced from the UN Comtrade database1 and the data is originally expressed in the nominal

US$. The real value is derived using the US import price index collected from the US Department of

Labor2. The automotive industry uses one import price index for the three groups, i.e. the import

price index for automotive Parts & Accessories.

The Athukorala 2009 list is with some modification by including other parts and components which

are considered as auto parts by the Japan Auto Parts Industries Association (JAPIA) and the

Indonesian Automotive Parts and Components Industries Association (GIAMM). Additional parts and

components include tyres, safety glass, electronics parts for automotive, brakes, and safety airbags.

Production Cost

Labour cost

Labour cost is represented by real wage which is calculated from the nominal wages of each country

in US$ deflated by the US Wholesale Price Index (WPI). Nominal wage from the ILO-Laborsta3

database is expressed in the country’s currency therefore it should be converted into US$ using

nominal exchange rate for each country sourced from the WDI website4. However, only 113 of 200

countries have wages data.

USPe

wageRWages

*=

Wherewage denotes nominal wage in domestic currency for each country, e denotes the nominal

exchange rate in the US$ and USP denotes the US Wholesale Price Index as a deflator.

Quality of Labour

Quality of labour is represented by the ratio of high technology export to manufacture export. High-

technology exports are products with high R&D intensity, such as in aerospace, computers,

1 The trade data is collected from UN Comtrade database website, http://comtrade.un.org/db/default.aspx 2 The price indexes are available at Bureau of Labour Statistics, the US Department of Labour ‘s website, http://www.bls.gov/web/ximpim/beaimp.htm 3 The wage data is collected from the ILO – Laborsta, http://laborsta.ilo.org/STP/guest 4 Others data is collected from the World Development Indicator, the World Bank, http://data.worldbank.org/indicator

27

pharmaceuticals, scientific instruments, and electrical machinery. This ratio is available from the

WDI for 173 countries.

Real Exchange Rate

The real exchange rate (RER) is calculated by the following conventional formula:

e

w

eP

ePRER =

Where e denotes the nominal exchange rate measured in terms of foreign currency, wP is an index

of foreign price and dP is an index of domestic price. The producer (wholesale) price index is used

as proxy of wP and, the GDP Deflator is a proxy for dP .

RER based on the price index is not appealing in a pure cross-sectional context because the data only

reflect changes relative to the base year of the index used, with no indication of overvaluation or

undervaluation of a given currency. The alternative measurement is to use the deviation between

RER and the mean of RER over the period with the assumption that the mean of RER is the long-term

equilibrium of the RER (Soloaga and Winters, 2001).

Service links costs

Freight Cost

Some empirical models use distance (Distance) as a proxy of freight cost. Since this model use

unilateral trade instead of bilateral trade, the determination of distance (Distance) is not as

straightforward as in the gravity model. Therefore the distance is calculated between a country and

its major exporter and importer countries. First the major partner is determined for each region and

then each country in the region is assumed to have the same major partner. If a county is also a

major partner for the particular region then the distance is measured by the distance between that