growing unaffordability of health care: incremental vs. real health care reform

DESCRIPTION

Growing Unaffordability of Health Care: Incremental vs. Real Health Care Reform. John P. Geyman, MD Professor Emeritus- Family Medicine University of Washington, Seattle. Major Problems of Health Care System. Increased Costs Decreased Access Variable Quality Increased Fragmentation - PowerPoint PPT PresentationTRANSCRIPT

Growing Unaffordability of Health Care: Incremental vs.

Real Health Care Reform

John P. Geyman, MD

Professor Emeritus- Family Medicine

University of Washington, Seattle

• Increased Costs• Decreased Access• Variable Quality• Increased Fragmentation• Increased Administrative Burden• Technological Imperative• Medicolegal Liability• System Out of Control

Major Problems ofHealth Care System

Drivers of Health Care Costs

• 1.Technological advances

• 2. Aging of population

• 3.Increase in chronic disease

• 4.Inefficiency and redundancy of private insurers

• 5.Profiteering by investor‑owned companies, facilities and providers

• 6.Consumer demand

• 7.Defensive medicine

HEALTH CARE COSTS IN U.S.

• 16.5% of GDP

• $2.3 trillion per year

• Increased cost-shifting to individuals/families

• Incremental “reforms” ineffective

Escalating Costs of Care

• Double digit increases in health insurance

premiums

• Average family premium now over $15,000

per year

• 31% of total health costs are administrative

• HMO rates up by 11.7% in 2007 vs CPI

increase of 2-3%

GROWING UNAFFORDABILITYOF HEALTH CARE

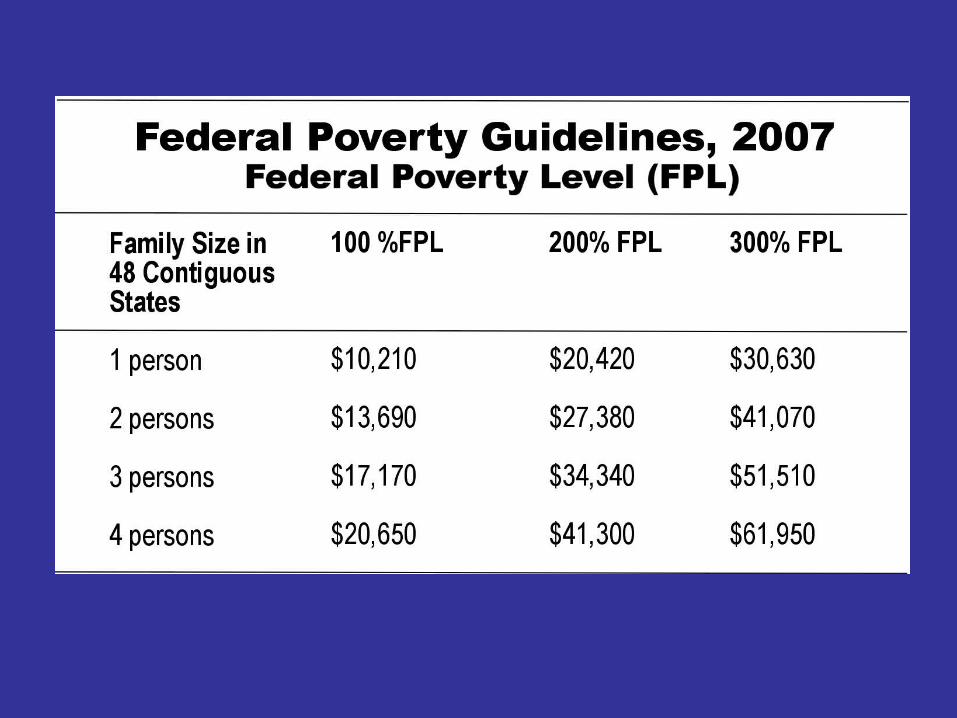

• “Medical divide” at about $50,000 annual income

• Median household debt over $100,000

• Median family income $41,000 a year

• Health insurance premiums to consume one-third of average

household income by 2010

CHANGE IN REAL FAMILY INCOME1979-2004

SOURCE: Bureau of the Census

Three Alternatives ForHealth Care Reform

1. Employer mandate

2. Individual mandate (Consumer‑driven health care)

3. Single‑payer system

Problems WithEmployer‑Based Approach

1. Only 59 percent of employers provide coverage

2. Trend toward part‑time work force

3. Defined contributions vs. benefits

4. Increasing cost‑sharing and unaffordability

5. Job lock problem

6. Competitive disadvantage in global markets

7. A failed track record (eg., Hawaii)

Consumer Choice(“Individual Mandate”)

• Increasingly popular pro-market “solution”

• Shifts responsibility for coverage from employers to consumers

• Assumes a free market in health care

• Assumes adequate information and options for consumers

• Current examples:

privatizing of Medicare

health savings accounts

Problems With Option 2

• Less service for more cost

• Serves for-profit insurance industry

• Coverage by risk selection

• Limited choice for consumers

• “Bad plans can drive out the good ones”

• Is still the most politically popular and likely

Why Incremental "Reforms” Keep Failing

1. Favorable risk selection by insurers

2. High administrative costs and profiteering

3. No mechanisms to contain costs

4. Fragmentation of risk pools

5. Decreasing access to necessary care

6. Lack of accountability for value and quality

"In America, the over reliance on market logic and marketing institutions is ruining the health care system. Market enthusiasts fail to tabulate all the costs of relying on market forces to allocate healthcare-the fragmentation, opportunism, asset rearranging, overhead, underinvestment in public health, and the assault on norms of service and altruism. They assume either a degree of self-regulation that the health markets cannot generate, or farsighted public supervision that contradicts the rest of their world view. Health care now consumes fully one-seventh of our entire national income. There is no realm of our mixed economy where markets yield more perverse results.”

Robert Kuttner - Everything for Sale: The Virtues and Limits of Markets

Incremental Change and U.S. Health Care

By John Jonik

Option 3: Single Payer System

• Socialized insurance, not socialized medicine

• Universal coverage through National Health

Program

• Eliminates private health insurance industry

• Hospitals and nursing homes with global budgets

• Physicians reimbursed by fee-for-service

• Blend of federal and state government roles

Fundamental Features of a Universal Healthcare System

• Everyone included

• Public financing

• Public stewardship

• Global budget

• Public accountability

• Private delivery system

What Would a NHP Look Like?

• Everyone receives a health care card assuring payment for all necessary care

• Free choice of physician and hospital• Physicians and hospitals remain independent

and non-profit, negotiate fees and budgets with NHP

• Local planning boards allocate expensive technology

• Progressive taxes go to Health Care Trust Fund• Public agency processes and pays bills

Advantages of National Health Program

• • Assured access for all AmericansAssured access for all Americans

• • Cost savings ($200 billion/year)Cost savings ($200 billion/year)

• • Administrative simplicityAdministrative simplicity

• • Decreased overhead (Medicare 3% vs private Decreased overhead (Medicare 3% vs private

insurance 15%-26%)insurance 15%-26%)

• • Distributes risk and responsibility to finance Distributes risk and responsibility to finance

carecare

• • Improves access, costs, and quality of careImproves access, costs, and quality of care

Growing Support for NHI

Physicians (egs., PNHP, ACP, AMWA, APHA)

2008: 59% national study2006: 64% Minnesota 2002: 62% Massachussetts1999: 57% of Deans, faculty, residents, and medical

students

Nurses (eg., CNA)Labor (egs., AFL-CIO and Working America)Mayors of 25 Cities (egs., Austin, Baltimore, Boston,

Chicago, Detroit, San Francisco, Louisville)Public: average 60-65% over many years

How Physicians Win with NHI

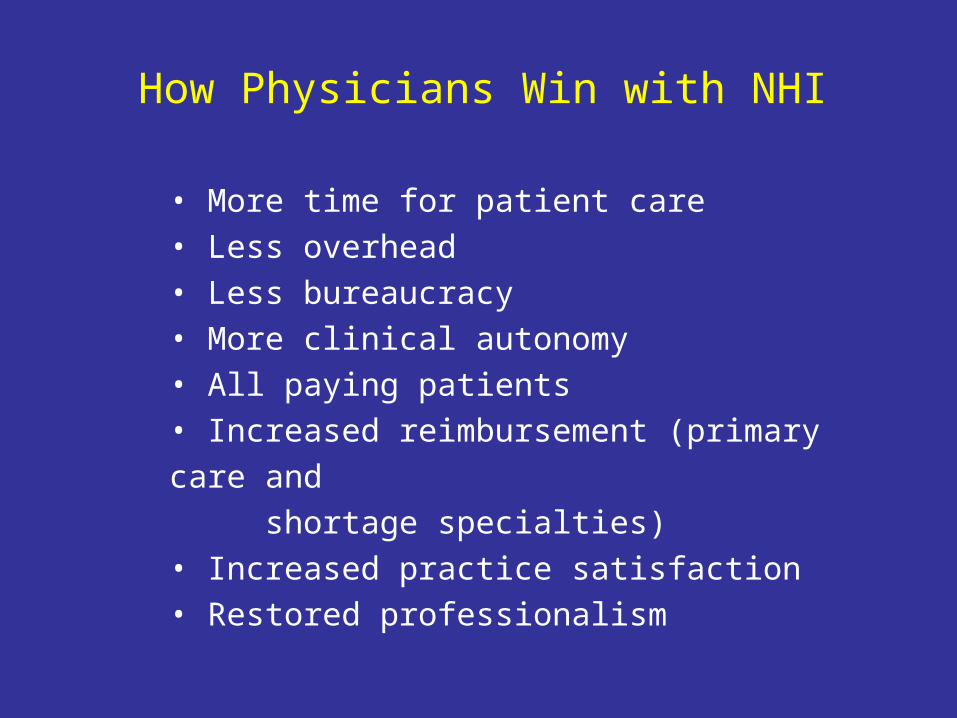

• More time for patient care

• Less overhead

• Less bureaucracy

• More clinical autonomy

• All paying patients

• Increased reimbursement (primary care and

shortage specialties)

• Increased practice satisfaction

• Restored professionalism

Problems with Option 3

• Political acceptance• Lobbying by special interest stakeholders• Disinformation by media coverage• Philosophic concerns about “big government”• Denial of ineffectiveness of market-based

system

Why Private Health

Insurance is Obsolete

・ Inefficiencies vs public-financing

・ Fragments risk pools by medical underwriting

・ Increasing epidemic of underinsurance

・ Excessive administrative and overhead costs

・ Profiteering ム shareholders trump patients

・ Pricing itself out of the market

・ Unsustainable and resists regulation

Annual Health Insurance Premiums And Household Income, 1996-2025

SOURCE: Reprinted with permission from Graham Center One-Pager. Who will have health insurance in 2025? Am Fam Physician 72(10):1989, 2005

1. Single-payer national health insurance (NHI)

2. Evidenced-based coverage process

3. Reimbursement reform

4. Strengthening of primary care

5. Quality improvement

6. Transition from for-profit to not-for-profit system

7. Rebuild the capacity of government

8. Malpractice liability reform

Basic Building Blocks

For Health Care Reform

Alternative Scenarios for 2020

Alternative Scenarios for 2020

Principle of Social Justice

The medical profession must promote justice in the health care system, including the fair distribution of health care resources. Physicians should work actively to eliminate discrimination in health care, whether based on race, gender,socioeconomic status, ethnicity, religion, or any other social category.

SOURCE: Project of the ABIM Foundation. ACP.-ASIM Foundation and EuropeanFederation of Internal Medicine. Medical professionalism in the new

millennium:A physician charter. Ann Intern Med 136(3):244, 2002.

“The evidence is conclusive that our people do not yet receive all

the benefits they could from modern medicine. For the rich and

near-rich there is no real problem since they can command the

very best science has to offer. - - - Among the majority of the

population, however, there are great islands of untreated or

partially treated cases - - - Although it is a principle of far-reaching

and, perhaps, of revolutionary significance, I think there are few

who would deny that our ultimate objective should be to make

these benefits available in full measure to all of the people.”

Ray Lyman Wilbur, M.D.Chairman of the Committee on the Costs of Medical Care, 1932 Report

First Dean of Stanford Medical School and President of Stanford University (1916-1943)