growth focus discipline - eon.com · upper end of guidance +58% yoy. leverage target of 3.9x...

TRANSCRIPT

Creating the future of energy

March 13th, 2018

DisciplineFocusGrowth

http://www.energyfortomorrow.de/

• Focus: Europe’s first energy player with exclusive downstream focus

• Unique downstream footprint: RAB and customer numbers rise >60%1

• Earnings quality: network EBIT share rises to ~80%1

• Strong synergies: fading nuclear earnings overcompensated by €600-800m synergies

• Attractive dividends: aiming to deliver absolute annual dividend growth

• EPS accretion: from second year after closing

• Solid capital structure: high commitment to strong BBB rating

• Limited cash impact: acquisition of RWE‘s 76.8% in innogy via asset exchange; attractive offer to minority shareholders

2

FutureE.ON

~371, 3

EngieIberdrolaEnelNat. Grid

~501

IberdrolaEngieEnelFutureE.ON

Regulated Asset Base (RAB € bn)

Customer Numbers (m)

Iberdrola2Nat. Grid2Engie2Enel2

~51

FutureE.ON

EBIT (€ bn)

Creating the future of energy

1. Future E.ON pro-forma EBIT 2017 (innogy data based on public information), 2. Bloomberg Data, 3. RABs from different regulatory regimes are not directly comparable due to significant methodical differences.

Creating two focused energy companies

E.ON RWE

Future E.ON RWE16.67%

Target structure

Structure today~77% innogy

3

Acquisition of innogy via innovative asset exchange

innogy

76.8%(RWE)

23.2%(Min. share-

holders)

Total equity value: ~€22bn16.67% Stake in Future E.ON

(~€3.7bn)

E.ON & innogy Renewables&

Other Assets(~€13.5bn)1

Cash payment to E.ON (- €1.5bn)

Offer price and innogy dividend for 2017 and ’18 (~€5.2bn)

1. Acquisition of RWE‘s 76.8% stake in innogy via asset exchange

2. RWE to get in exchange:• 16.67% in new E.ON via 20% capital increase against

contribution in kind (authorized capital)• E.ON‘s and innogy‘s renewables businesses4

• Additional assets: E.ON’s minority stakes in two RWE operated nuclear power plants2, innogy’s gas storage business and minority participation in Kelag

3. RWE receives innogy dividends for 2017 and 20184. Net cash payment from RWE to E.ON of €1.5bn3

5. Attractive cash offer to minority shareholder in innogywith total value of €40.00 per share (offer price (€36.76) plus expected dividends of €3.24 per share for the two fiscal years 2017 & ’18 combined)

Asset exchange (limited cash impact)

Cash element

41. Equity value for transfer perimeter 2. Gundremmingen (25% stake) and Emsland (12.5% stake), 3. Payment to balance asset valuation. 4. Excludes 20% in Rampion and certain onshore capacity indirectly held by E.ON and innogy.

Innogy dividends (~€1.4bn)

Renewables11x EV/EBITDA

Upper end of guidance

+58% YoY

Leverage target of 3.9x achievedbefore monetization of Uniper

Payout ratio increased 2x since start of new E.ON

3-4% EBIT CAGR3

5-10% EPS CAGR3

Transacting from a position of strength

EBIT€3.1bn1

ANI€1.4bn1

END€19.2bn1

Dividend

Mid-term Growth

Group EBITDA

~€8bn2

Customer Solutions

>31mCustomers1

~50mCustomers2

Energy Networks

~€23bn RAB1, 4

~€37bn RAB2, 4

€5bn1

1. E.ON standalone 2017 reported, 2. Future E.ON pro-forma 2017 (innogy data based on public information), 3. 2018-2020 based on existing portfolio (E.ON standalone), 4. RABs from different regulatory regimes are not directly comparable due to significant methodical differences.

Regulated Non-regulated

E.ON today Future E.ON (’17)

5

E.ON today (’17)

E.ON standalone

Sweden1

~€4bn ~1m- ~7m1

NL/BE

- ~4m2

Germany3

~€20bn ~14m

CEE3

~€11bn4 ~13m

Turkey1

~€1bn ~9m

Unique downstream position across Europe

Energy Networks (RAB)

Customer Solutions (number of customers)

Southern Europe

- ~1m36

1. E.ON 2017 reported, 2. innogy2017 reported, 3. Future E.ON pro-forma 2017 (innogy data based on public information), 4. RABs from different regulatory regimes are not directly comparable due to significant methodical differences.

Excludes npower UK customers subject to transaction with SSE

UK

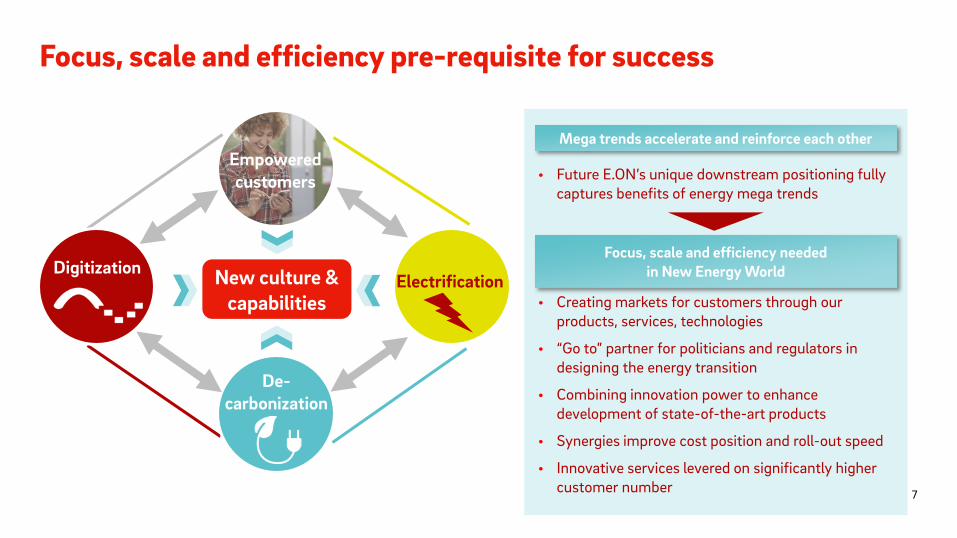

Focus, scale and efficiency pre-requisite for success

DigitizationElectrificationNew culture &

capabilities

Empoweredcustomers

De-carbonization

• Future E.ON’s unique downstream positioning fully captures benefits of energy mega trends

• Creating markets for customers through our products, services, technologies

• “Go to” partner for politicians and regulators in designing the energy transition

• Combining innovation power to enhance development of state-of-the-art products

• Synergies improve cost position and roll-out speed

• Innovative services levered on significantly higher customer number

Mega trends accelerate and reinforce each other

Focus, scale and efficiency needed in New Energy World

7

Spin-off Uniper& reset of E.ON

2016 2018 2020 and beyond

Position of strength

• Robust portfolio

• Strong financial & operational delivery

• Balance sheet headroom

Transition year

Acceleration of strategy execution

Unique strategic position

• Focus on high-performance regulated networks and state-of-the-art customer solutions

• Reduction of portfolio complexity

• Enhanced earnings quality: ~80% of EBIT1 is regulated

• Aiming to deliver absolute annual dividend growth

8

1. Future E.ON pro-forma 2017 (innogy data based on public information).

Potential for premium valuation

3

4

5

6

7

8

9

10

11

12

Value creation for shareholders

Instant redeployment of

capital

Renewables1

Platformfor high

Synergies (€600-800m)

Shareholder value

creation

91. Enterprise value (schematic).

Renewables11x EV/EBITDA

innogy acquisition at ~10x EV/EBITDA

Realization of valuation premium

Integration of innogy provides for strong synergy potential

2019 2020 2021 2022

Estimated synergies (€ m)2 Synergy focus1, 2

€600-800m

10

~55%

~25%

~5%

• Strong synergy potential of €600-800m

• 10-15% of controllable costs

• ~5000 FTEs affected (~7% of employee base)

Corporate Functions & IT

Energy Networks

Energy Sales & Customer Solutions

~100%

1. Synergy split (€ million), 2. Future E.ON pro-forma 2017 (innogy data based on public information).

~80%2

~65%1

Non-regulatedRegulated

E.ON today Future E.ON

Share of regulated network earnings (EBIT)

Attractive earnings & dividend profile secured long-term

11

Synergies to over-compensate fading nuclear earnings

0

1

2

3

4

5

6

E.ON stand-alone

EBIT development3

Enlarged E.ON

2018 2019 2020 2021 2022

1. E.ON 2017 reported, 2. Future E.ON pro-forma 2017 (innogy data based on public information), 3. Schematic illustration.

Future E.ON‘s key financials

12

EBITDA

EPS

EBIT

~€8bn1

~€5bn1

EPS accretion from second year after completion

DividendAiming to deliver absolute annual dividend growth

(fixed dividend for 2018: €0.433)

Customer Solutions

Energy Networks

Non-Core

~80% regulated2

1. Future E.ON pro-forma 2017 (innogy data based on public information), 2. Future E.ON pro-forma EBIT 2017 (innogy data based on public information), pie chart does not account for corporate functions & others, 3. Fixed for FY2018 (paid in 2019).

• Nuclear provisions: ~€0.9bn• AROs (Renewables): ~€0.9bn• Tax equity liabilities

(Renewables): ~€0.6bn• Pension provisions

(Renewables): ~€0.4bn

13

Pro forma economic net debt

Economic Net Debt 2017

~19.2

~10.6

~3.6

~5.0

E.ON today1 (€ bn)

Economic Net Debt 2017

~35

Asset-retirement obligationsProvisions for pensionsNet financial position

1. E.ON 2017 reported, 2. Future E.ON pro-forma 2017 (innogy data based on public information), 3. E.ON will address structural subordination post closing, 4. Nord Stream 1 stake.

~5+ Monetization of Uniper shares

+ Transfer of NS14 into CTA

Further deleveraging measures to be realized in ‘18 (€ bn)

Includes:• Acquisition of 23.2% minority shares • €1.5bn cash payment from RWE

Future E.ON2, 3 (€ bn)

~€2.8bn debt transferred to RWE

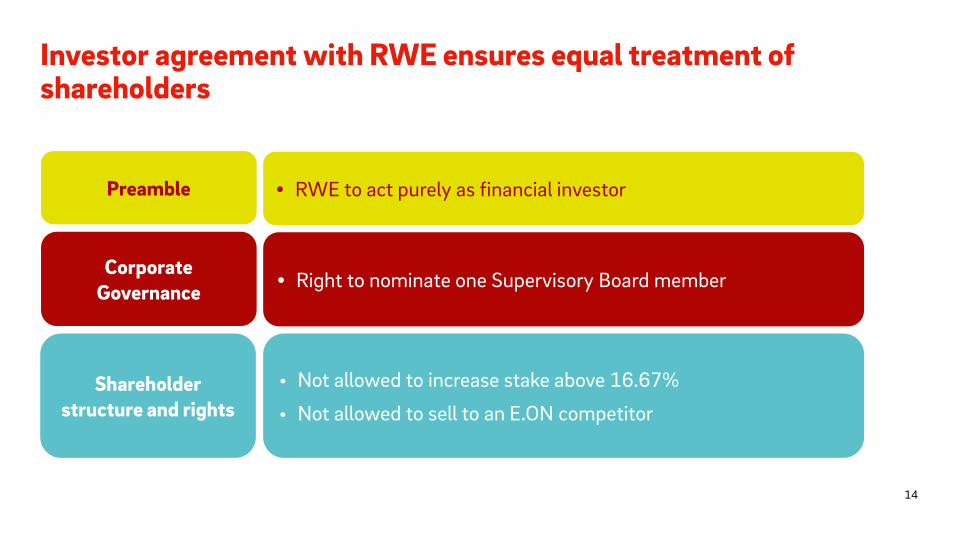

Investor agreement with RWE ensures equal treatment of shareholders

Preamble • RWE to act purely as financial investor

CorporateGovernance

Shareholder structure and rights

• Right to nominate one Supervisory Board member

• Not allowed to increase stake above 16.67%

• Not allowed to sell to an E.ON competitor

14

20192018 20212020

1. Payment to balance asset valuation, 2. Transfers of E.ON minority shares in the two RWE-operated nuclear power plants Gundremmingen (25% stake) and Emsland (12.5% stake) to RWE.

1st Closing• E.ON becomes ≥76.8%

shareholder in innogy• RWE becomes 16.67%

shareholder in E.ON (20% capital increase)

• €1.5bn cash payment to E.ON1

• Transfer of other assets2

2nd Closing• Transfer of E.ON and innogy RES Assets• Transfer of Kelag participation and gas storage assets of

innogyVoluntary public

takeover offer (PTO)(ca. May – July)

Clear path to obtain full control, irrespective of PTO acceptance rate

Antitrust approvalsFull legal integration

Integration & synergies

15

Investment highlights

Starting from position of strength: Creating the future of energy

Unique downstream positioning with ~80% regulated earnings1Focus

Aiming to deliver absolute annual dividend growthGrowth

Renewables value crystallization and €600-800m synergiesHigh commitment to strong BBB rating Discipline

161. Future E.ON pro-forma 2017 (innogy data based on public information).

Standalone strength

Dr. Johannes Teyssen – CEO and Dr. Marc Spieker - CFOMarch 13th, 2018

DisciplineFocusGrowth

E.ON standalone

Delivering step by step – Strategy & Operations

Portfolio reset completed

• €3.8bn Uniper disposal: decision to accept Fortum’s offer

• De-risking: transfer of nuclear storage liabilities to government

• €0.2bn proceeds: successful IPO of Enerjisa’sdownstream business

• + ~500MW onshore wind in US in 2017

• + ~130k customer in Q4 ’171 – turn-around achieved

• €400m delivery of Phoenix performance program

• ~€0.6bn nuclear decommissioning savings secured

• ~€1bn total contract value in B2B new solutions (2017)

• ~200% sales growth in PV/battery: fastest growing solar company in Germany

• Innovation & digitization: successful launch of new products

• E-mobility: gaining traction

New culture & capabilities Operational excellence

1. Germany and UK. 18

E.ON standalone

Each pillar with focused and disciplined growth

Customer Solutions Energy Networks Renewables

• Grow & sustain RAB• Develop transformative platform• Drive adjacent businesses

+~€2-3bn

E.ON power RAB

2017 2020

~€19bn

~€21-22bn

• Energy sales: reinvent with profitable customer growth

• New solutions: rapidly scale up• Heat: leverage existing positions

+~2m

Total Customer #

2017 2025

~22m

~24m

• Onshore: grow at scale• Offshore: leverage existing

options

+~2GW

E.ON operated capacity

~6GW

~8GW

2017 2020

19

E.ON standalone

Attractive stand-alone profile

Dividend growth

+40%

2017 2018

€0.30

EPS growth

+5-10% CAGR

€0.60 –0.70

2018 2020

EBIT growth

5.3GW

~8GW

2017 2020

2018 2020

Group CAGR: +3-4%

€2.8 –3.0bn

€0.431

20

Aiming to deliver absolute annual dividend growth

1. Fixed for FY2018 (paid in 2019).

E.ON standalone

Core CAGR: +5-6%

Drive value creation Absolute annual dividend growth

Sustainable & resilient EPS growth

Customer-led Digitization Operational excellence

Capitaldiscipline

E.ON‘s guiding principles

21

E.ON standalone

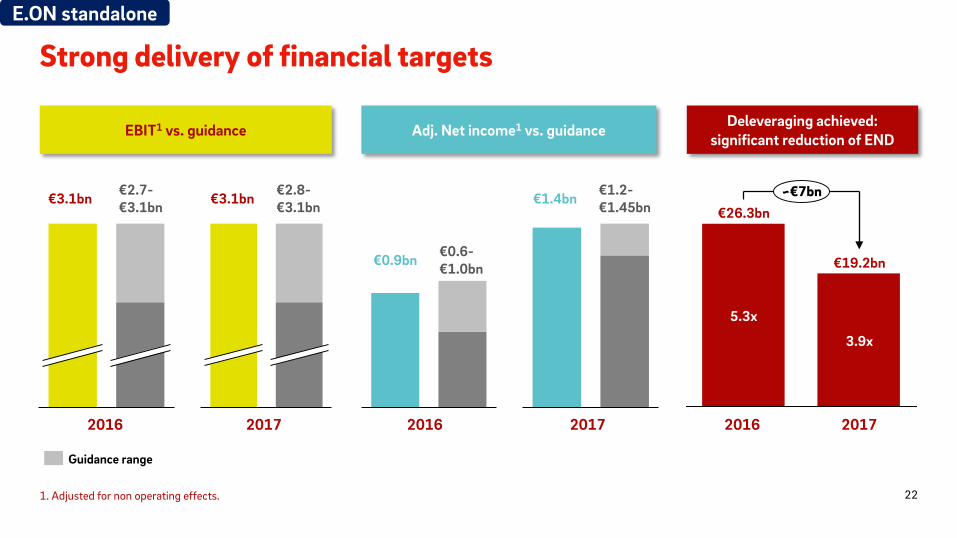

Strong delivery of financial targets

1. Adjusted for non operating effects.

2016 2017 2016 2017

~€7bn

€19.2bn

3.9x

€26.3bn

5.3x

2016 2017

€2.7-€3.1bn

€2.8-€3.1bn

€0.6-€1.0bn

€1.2-€1.45bn€3.1bn €3.1bn

€0.9bn

€1.4bn

EBIT1 vs. guidance Adj. Net income1 vs. guidance Deleveraging achieved:significant reduction of END

Guidance range

22

E.ON standalone

Deleveraging creates balance sheet headroom

Economic net debt

26.3

~4.4x EBITDA

~5.3x EBITDA

FY 16

21.5

FY 17Q2 17

~3.9x EBITDA

19.2

~5

1. Nord Stream 1 stake.

+ Nuclear fuel tax

+ Accelerated Book Build

+ Nuc. decommissioning cost savings

+ Additional measures

~2.9

~1.4

~0.6

~0.6

+ Monetization of Uniper shares

+ Transfer of NS11 into CTA

+ Nuc. decommissioning cost savings and additional measures

FY 17

19.2

~3.9x EBITDA

~3.0x EBITDA

Post deleveraging

headroom

~4.0xEBITDA

Mid-term target

Hybrid cancelled

Scrip dividendcancelled

€ bn

Achieved (€ bn) To be finalized (€ bn)

23

E.ON standalone

Disciplined capex drives EBIT growth

201920182017

EBIT driven up by additional capex (€ bn)

202020192018

New plan ~€9.5bn net capex1

~20%

1. Capex net of divestments.

EBIT flat within range (€ bn)

202020192018

2.8

3.1

2018 2019 2020

Group EBIT CAGR~3-4%

Core EBIT CAGR ~5-6%

Old plan ~€8bn net capex1

24

E.ON standalone

Capex split 2018-2020

Capex1 2018

1. Capex net of divestments.

1.0

1.0

1.5

RenewablesEnergy Networks Customer Solutions

~€ 3.5bn ~€ 9.5bn

Increase in capex drives the 5-6% EBIT growth target of the core business

Segments have to compete for capital and against other uses of funds

Strict adherence to return targets (ROCE 8-10%)

Growth

Focus

Discipline

25

E.ON standalone

Capex1 2018-2020

49%

26% 25%

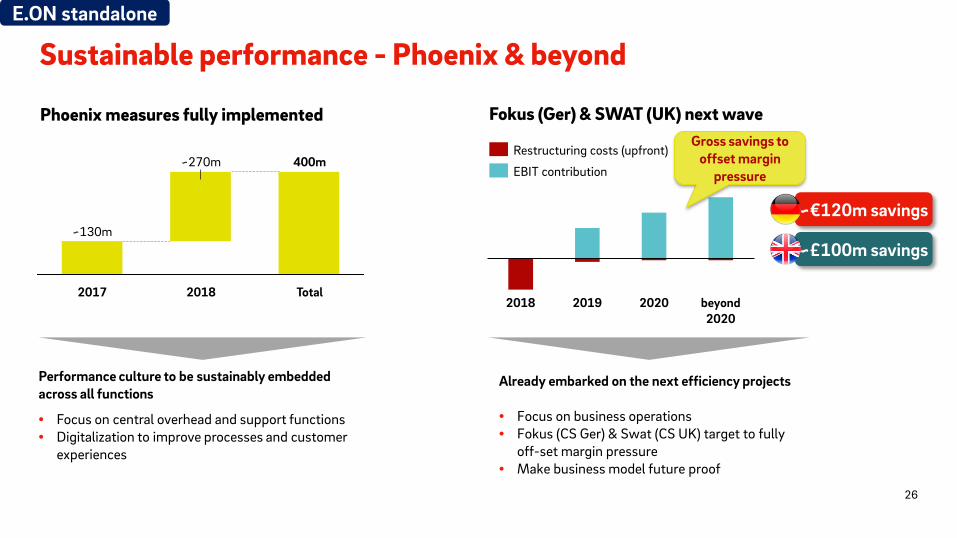

Sustainable performance - Phoenix & beyond

Fokus (Ger) & SWAT (UK) next wave

Already embarked on the next efficiency projects

• Focus on business operations• Fokus (CS Ger) & Swat (CS UK) target to fully

off-set margin pressure• Make business model future proof

202020192018 beyond 2020

Restructuring costs (upfront)

EBIT contribution

Gross savings to offset margin

pressure

~€120m savings

~£100m savings

Performance culture to be sustainably embedded across all functions

• Focus on central overhead and support functions• Digitalization to improve processes and customer

experiences

Phoenix measures fully implemented

2018

400m

~130m

Total2017

~270m

26

E.ON standalone

Group guidance FY 2018

EBIT 2017

Adj. Net Income 2017

1. Adjusted for non operating effects. 27

3.0

2.8

1.51.3

EBIT1 (€ bn)

Adj. Net Income (€ bn)

€3.1bn

€1.4bn

Includes ~€100m restructuring costs in Customer Solutions (UK, Germany)

2017

Act

uals

2018

Gui

danc

e

E.ON standalone

Guidance range

+ Offshore & Onshore: capacity additions– Onshore: subsidy expiries

+ Sweden: power tariff increase– Germany: reversal of regulatory effects, new

regulatory period gas, concession loss HH

+ Germany: Non-recurrence of a negative one-off effect in the prior year– Germany: restructuring costs– UK: competitive dynamics, restructuring costs, regulatory intervention

Segment EBIT guidance FY 2018Drivers for 20182018

Energy Networks

CustomerSolutions

Renewables

1. Adjusted for non operating effects, 2. Based on E.ON standalone EBIT 2017 pro forma figures, adjustments to reported figures: Turkey generation business reported under Non-Core (previously Energy Networks); German Heat business reported under Customer Solutions Other (previously Customer Solutions Germany); costs for digital products/services, innovative projects in Customer Solutions (previously Corp. Functions/Other).

Non-Core– PEL: lower hedged prices (-/+) Non-reoccurrence of one-off effects in 2017

EBIT1 2017€ bn

Pro forma2Actuals

1.9

0.5

0.5

0.5

2.0

0.5

0.5

0.4

28

E.ON standalone

Corp. Functions/ Other

+ Phoenix measures-0.3 -0.3

Attractive EBIT and EPS growth profile

Adj. EBITIllustrative

• Refinancing benefits of up to ~€200m1 (~2/3 effective in 2018)

• ~€4.5bn maturing bonds between 2018 –2020

5-10% p.a.

202020192018

Adj. Earnings per Share (EPS)

29

2019 20202018

Group EBIT CAGR~3-4%

Core EBIT CAGR ~5-6%

E.ON standalone

1. 2018 – 2020.

Delivering step by step – Attractive dividends

Absolute dividend growth 2018: Fixed Dividend

FY 2018Dividend

€0.431

FY 2017Dividend

€0.30

FY 2016 Dividend

€0.21

30

Aiming to deliver absolute annual dividend growth

1. Fixed for FY2018 (paid in 2019).

E.ON standalone

ReturnROCE1

8 – 10 %

E.ON FOCUS – medium-term framework Our basis for steering the company

1. Based on EBIT (= pre-tax), 2. OCFbIT divided by EBITDA, 3. Adjusted for non-operating effects, FY 2018 guidance range as basis for medium-term outlook 2018-2020, 4. Total Shareholder Return, 5. Fixed for FY2018 (paid in 2019).

CashCash conversion rate2

≥ 80 %

Executive CompensationClosely linked to EPS target achievement and relative TSR4 (in addition: share ownership obligations)

EPS3,4

Group+ 5-10%

Absolute dividend growth

Dividend Payout

Fixed dividend: €0.435EBIT3

Group+ 3-4%

31

Capital StructureStrong BBB/Baa

E.ON standalone

Investment highlights

From deleveraging to focused and disciplined growth

Management team with strong shareholder focusFocus

Deliver sustainable EPS growth andaiming for absolute annual dividend growthGrowth

Strict capital discipline and high-performance cultureDiscipline

32

E.ON standalone

Appendix

Energy Networks

DisciplineFocusGrowth

E.ON standalone

Energy Networks - The heart of E.ON

Power and gas business

Power business only

CEE &Turkey€8.5bn3

Sweden€4.0bn

Germany€10.7bn

~€23.1bn2

Regulated asset base 20171

CEE &Turkey€0.4bn

Sweden€0.5bn

~€1.9bn

Germany€1.1bn

EBIT4 2017

19 25 3212

71

27

Germany CEE & Turkey5Sweden

Market share (%)

349137

490

260

Germany Sweden

45

CEE & Turkey

Power Gas

Grid length (‘000 km) 1

∑ Grid length: 976

∑ Grid length: 107

1. 100% view for Slovakia and Turkey, 2. Differences may occur due to rounding, 3. In Hungary the RAB has been increased in 2017 by €2.8bn due to a system change towards replacement costs. It was €1.5bn before, 4. Adjusted for non operating effects, 5. Arithmetic average.

~75% of group core

35

E.ON standalone

Energy Networks - Higher capex leads to power RAB growth

2017 2020 2017 2020 2017 2020

Czech RepublicSwedenGermany

+6-10% +11-15% +12-16%

~€1.4bn~€3.8bn~€8bn

Power RABPower RABPower RAB

36

E.ON standalone

Multi-decade RAB growth engine

• Main driver is additional replacement investments

• Conservative assumptions on Renewables and E-mobility roll-out

• Acceleration of Renewables build-out• Smart meter• E-mobility• Electrical heating• Digital layer & fully digital equipment

Cautious planning

Potential upsides to “new normal”-level

+€300m –€400m

€1.4bn

2016 2017

€1.4bn

€1.7 – 1.8bn

Beyond 2020“New normal”

Disciplined & gradual ramp-up

Energy Networks capex1

371. Excluding Slovakia and Turkey.

E.ON standalone

Major transformation in Energy Networks

38

Single layer infrastructure (energy)

Physical linear network

Centralized system

Infrastructure ecosystem

Decentral, connected multi-layer infrastructure

More (semi-) autonomous local energy systems

Energy Network player

Energy network operatorFrom

Holistic system providerTo

Phys

ical

la

yer

Dig

ital l

ayer

Com

mun

i-ca

tion

laye

r

Data centerEMS Platforms

Network control center

Smart Home

Asset control systems

VPP

Local grid control

Smart Meter

Cloud

AntennaWifi

Block chain

Future energy network system will need to combine different layers of infrastructure

E.ON standalone

Turkey with extraordinary high RAB growth

Established in 3 high-growth regions

Leading electricity network operator: − 10.5 m connections− 220,000 km network length

(20% of market)

Constructive regulatory environment:− Allowed WACC for 2016-2020

regulatory period has been increased to 13.6% from 11.9% (pre-tax, real)

− Incentives to outperform capex, opex, and theft & loss allowances

High network investment due to:− Strong power demand growth of

>4% p.a.− Need for significant network

modernization

in bn TL, nominal

Regions

Target to more than double 2016 RAB by 2020

Downstream Business Market & Regulation RAB development

Strongly growing market with highly attractive returns

AnkaraIstanbul

Adana

>2x

3.8

5.3

2016 2017 2020

39

E.ON standalone

Operational excellence – digitization in practice

Transparent and effective capex allocation Providing a smooth user experience

Asset replacement decisions Digital workforce

Data driven decisions to prioritize replacement

activities

Low double digit million € added value p.a. potential after full roll-out

Expert judgement and local experience

Predictive maintenance Conventional approach

6-12 % productivity gains

Introduce digital application used by every field worker comprising all functionalities necessary in the daily work

Tool

Impa

ct

40

E.ON standalone

Aspiration to develop the platform for energy transition

41

Further decentralization and

fragmentation lead to a need for

local rebalancing

Transformative Platform

P2PTrading

Flex-Markets

LocalEnergy System

RegionalEnergySystem

Increasing system responsibility assumed by regional or local network operator

Energy transition is and will be happening essentially at the DSO-level

E.ON standalone

Opportunities in adjacent businesses - Broadband

42

Growing from existing assets

E.ON's existing fiber-optic infrastructureE.ON's new fiber-optic infrastructure

A

Local transformer station

Fiber-optic cables in every street and to every household

Network operations center

Business building

Mobile cell tower

Telco X'sbackbone

Enterprise customer's data center

Point of Presence (Switch between backbone and access network)

Extension of existing business

Entering Fiber-to-the-Home (FttH) marketB

New business concept in development

E.ON standalone

• Lower allowed returns reflect lower bond yields

• Benefits from maturing legacy bonds to be attributed to Energy Networks driving EPS growth

EBIT outlook – Stability despite two major regulatory reviews

43

German pension cost pass through

Positive one-off

2017 2018 2019 2020

€1.9bn

Lower allowed returns

Higher RAB

+5-10% p.a.

€0.60 –0.70

2018 2020

EPS growth

E.ON standalone

Customer Solutions

DisciplineFocusGrowth

E.ON standalone

Energy sales is the anchor of customer solutions

1. Excluding Turkey, 2. Total Contract Value, 3. Adjusted for non operating effects, 4. B2C customers in Germany and UK.

E.ON’s market positions

Customer

B2B

B2C

B2M

Customer focused portfolio

Heat &New

Solutions

EnergySales

EBIT3 2017 €526m Energy Sales EBIT4

B2C ~75%

B2B~25%

Energy Sales is the anchor business

High customer loyalty

Customer tenure4

> 5y

< 2y

2-5y

B2M/Heat: 10% market share in Germany & Sweden

B2B Solutions: ~€1bn TCV2 in 2017

Top 3

Top 2

Top 3

Top 3Top 3

Top 3

Top 10

Top 3

Energy Sales: 22m1 customers in 8 countries

45

E.ON standalone

7

6

5

4

Q4 17Q3 17Q2 17Q1 17Q4 16Q3 16Q2 16Q1 16

UK B2C customersUK SVT customers

2013 2014 2015 2016 2017

6

8

4

2

UK

E.ON is leading the transformation of energy sales

4646

Standard tariff customer numbers declining

Cust

omer

ac

coun

tsin

m

2016 year of peak margins1

% m

argi

n Rigorous cost focusReduce cost to acquire and cost

to serve dramatically

Attractive productsInnovative and green tariffs

complemented by smart meter rollout

Focused sales channels

Protecting revenues

Turnaround in customer numbers

Increasing EBIT into

next decade

6.3m

1. Final figure for 2017 not yet available: ~5%.

E.ON standalone

Increase customer attraction while reducing cost to acquire

Physical channel Digital channel

Product offering and selection of sales channels lead to…

…at the same time reducing costs to acquire

…increase in customer numbers…

2017 2025

Sale

s ch

anne

lsTa

riff i

nnov

atio

ns

200k innovative tariffs sold since June 2017

> 5,000 E.ON Plus products (devices as add-on to tariffs) sold

18% of our customer base with add-on services

+100% value-add services contracts in 2017

Scale sales cooperations with big retailers (e.g. Lidl) • Innovative tariff offering• Focus on earning customers’ loyalty

Sales push in digital• From broker site to own website e.g. GER, UK, SWE

Home move journey as acquisition channel

~22m

~24m

47

E.ON standalone

Closing the gap - Cost to serve to be reduced dramatically

48

Components of cost to serve1

Other

Metering & Installation

Debtresolution

Servicingand

Backoffice

SWAT

Fokus

Smart Meter Rollout

E.ON ambitionE.ON

~€120m savings

€/customer account

~£100m savings

Cost to serve ambitionEfficiency programsMeasures to reduce cost to serve

1. Example UK.

Tackling cost to serve and overall cost efficiencies to support earnings

E.ON standalone

Re-inventing our customer business with the digital attacker

Cost efficiency

Superior services

Innovative proposition

<€ 10Market Leading

Cost to Serve

Synergiesacross regions

1-clickCustomer

journey

+50 NPS1

Quick response &

accurate billing

Singleplatform for

tariff innovations

Datadriven

propositions

Fasttime to market

Selflearning

functionality

Market leading

cost of change

Gradual replacement of legacy systems – customer focused with proven stability

1. Net Promoter Score. 49

E.ON standalone

New Solutions - Strive for leadership with innovative products

1. Adjusted for non operating effects.

B2B B2M B2C

PV + battery

Smart home

Smart meter

E-mobility

Prod

uct o

ffer

ing

Am

bitio

n 20

25

EBIT1 ~€250-300 m EBIT1 ~€200 m EBIT1 >~€50 m

EBIT margin > 10%

District heating

City quarter solutions

Integrated city energy solutions

Decentral generation

Energy efficiency

Flexibility & storage

Digital energy solutions

50

E.ON standalone

~>2 x

2025

~2 x

2016 2020…2017

Become a leading Energy Service Company

B2B - E.ON to become a leading Energy Service Company in Europe

Ambitious organic growth of TCV1 … …to translate into EBIT2 over time

1. Total Contract Value, 2. Adjusted for non operating effects.

Decentral generation

Energy efficiency

Flexibility & storage

Digital energy solutions

~ €250-300m

51

2016 2017 2020 2025

~+25% CAGR

E.ON standalone

B2M – E.ON is a reliable partner for cities and communities

52

E.ON to benefit from market trends and investments

1. Germany, Sweden, UK, 2. Capex net of divestments, including investments for Högbytorp, 3. Adjusted for non operating effects.

Investments with low risk and high return

Capex2 2018-2020ROCE > 10%

Stable (long-term) earnings

15-20 year contracts

2025

~€200m

2017

UKGermanySweden

Heat EBIT3 €m

~€ 800m

ectogrid™

Högbytorp, Stockholm

> €250m capex project close to Stockholm, COD 2019

100 MW CHP district heating network extension and biogas as part of a circular economy project

Can provide heating and cooling for an entire city, optimising excess heating and cooling

First ectogrid under construction in Lund, Sweden

Patented global solution - available to be sold and integrated in other cities

Project examples

E.ON standalone

B2C - E.ON drives the electrification of the home and mobility

PV + batteryE.ON SolarCloud

E.ON Plus + smart meters

E-mobilitysolutions

Home heating

Example: PV + battery growth story

Translating into decent EBIT in the next decade

beyond2025

~€50m

2017

E.ON product offering for the electrification of home

201720162015

~3x

~5x

2025…

EBIT1 €m

PV + battery units sold

E.ON – the fastest growing solar

company in Germany

1. Adjusted for non operating effects. 53

E.ON standalone

Temporary high investments for smart meter & IT

Disciplined investment plan to support growth opportunities

Capex1 2018-2020 €2.4bn

1. Capex net of divestments, 2. Adjusted for non operating effects.

€526mHeat &

New Solutions

2025…20202018

Restructuringcharges

2017

Customer Solutions EBIT2 2017-2020

Medium-term EBIT development

Energy Sales

Heat & B2B projects

Smartmeter

IT &efficiency

Other

E-mob

Partially temporary

Asset-backedinvestments

54

E.ON standalone

Renewables

DisciplineFocusGrowth

E.ON standalone

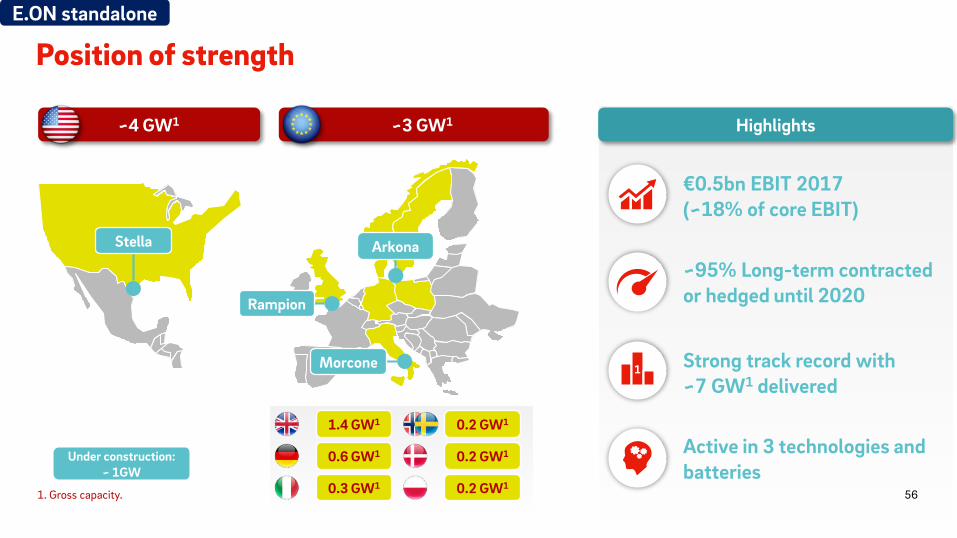

Position of strength

~4 GW1 ~3 GW1

Arkona

Rampion

Morcone

Under construction:~ 1GW

1.4 GW1

0.6 GW1

0.3 GW1

0.2 GW1

0.2 GW1

0.2 GW1

Stella

€0.5bn EBIT 2017(~18% of core EBIT)

~95% Long-term contracted or hedged until 2020

Strong track record with ~7 GW1 delivered

Active in 3 technologies and batteries

1

Highlights

561. Gross capacity.

E.ON standalone

Growth trend unbroken – RES to dominate global power generation

7 GW17 GW

CCGT

38 GW

Utility-scale PV

59 GW

Onshore

44 GW

Offshore Nuclear

Capacity additions forecastAnnual build rate avg. 2018-’301

~300 turbines per week

Strong cost decrease

Industry trends Bid prices per technology(EUR/MWh)

55

201720162015

103109

66

43

20162015 2017

Offshore Onshore

merchant2Decarbonization

571. Bloomberg New Energy Outlook 2017, 2. German Power Baseload forward 2019 (08.03.2018).

E.ON standalone

E.ON aims to grow at scale in Onshore

2017 2020

Onshore

+20-25%

Capitalize on attractive ~8 GW pipeline

~5 GW1

2017 2020

Offshore

+40%2

Leverage existing options in Europe

~1 GW1

1. Operated capacity 2. ~400MW net capacity addition. Gross capacity addition: 800MW.

• From boutique to industrial

• Capex light

Solar PV

58

E.ON standalone

High share of contracted revenues provides stability and visibility

2017 2018 2019 2020

• High earnings stability

• Secure long-term stable off-take agreements for new investments

• Revenue optimization for assets at the end of support scheme (rolling 3 year hedging)

• Active commercial risk management/value optimization incl. congestion hedging, day-ahead/intra-day optimization

Long-term contractedMerchant Hedged

High earnings stability and visibility Clear guiding principles

~75% long-term contracted1

~95% hedged or long-term contracted1

591. Average 2017 – 2020.

E.ON standalone

Integral part of E.ON - Modular value crystallization

Develop & Sell & (Operate) Build & Sell & Operate Build & Keep

• Rapid monetization of value• Capex light • Additional value from long-term

O&M services

• Reduce exposure in certain geographies

• Additional value from long-term O&M services

• Resilient long-term cash flows• Strong operational capabilities ensure

E.ON being an efficient asset owner

AftonMagic Valley 12

Amrumbank

Deal value: ~$100m1

Year: 2016Sold: 100%Cap.: 50 MW

Deal value: ~$650mYear: 2014Sold: 80%Cap.: 405 MW

Capex: ~€1bnCOD: 2015Cap.: 302 MW

Case

stu

dies

Wildcat 13

601. InfraRed Capital Partners, 2. Magic Valley 1: 203MW, 3. Wildcat 1: 202MW.

E.ON standalone

Technical/digital excellence to drive down LCOE1

Extension of life-time

Improved load factors and availability

Transparent and effective capex and opex allocation

1

Predictive maintenance roll-out

2017 2018 2019 2020

10%60%

Self-learning algorithms to optimize

wind park layout in order to increase

production and reduce wake effects

Array layout optimizer

Turbine selection tailored to site conditions

Data driven investment decision

Single digit yield increase

61

E.ON standalone

1. Levelized cost of electricity.

Play at scale in Onshore - Attractive pipeline in Tier 1 geographies

Gross capacity additions 2018-2020 (MW) Onshore pipeline

~5.9 GW

100% PTC

80% PTC

Other

Onshore pipeline

~1.8 GW

∑~2GW

UK

Nordic

Other EU

COD2016

COD2017

COD2018

COD2019

COD2020

Onshore Offshore1, 2 New Projects(Pre- FID pipeline)

621. 2018 COD: Rampion (Gross delivery: 400 MW, EU Offshore), Stella (Gross delivery: 201 MW, US Onshore) 2. 2019 COD: Arkona(Gross delivery: 385 MW, EU Offshore), Morcone (Gross delivery: 57 MW, EU Onshore).

E.ON standalone

Financial Appendix

DisciplineFocusGrowth

E.ON standalone

Highly stable business profile

Business profile

High share of regulated and long-term contracted earnings (~3/4 of EBITDA)

Predominantly quasi-regulated or contracted earnings in heat operations and RenewablesRemaining merchant exposure in Renewables and PreussenElektra largely hedged

Operations in Energy Networks under stable, well established frameworks in low risk markets with strong regulatory track record

FY EBITDA 20171

~3/4 from regulated/long-term contracted businesses2

1. Adjusted for non operating effects, representation in pie charts excluding Corporate Functions/ Other; total figure including Corporate Functions/ Other, 2. Including Energy Networks and a portion of Renewables and Heat.

15%

16%

56%

13%

Renewables

PreussenElektra (non-core)

Customer Solutions

Energy Networks

€5.0bn

64

E.ON standalone

E.ON today – Regulated Energy Networks at the heart

Key financials2017

Group EBIT1

Adj. Net Income1

€1.4bn

€3.1bn

Customer Solutions

€1.9bn€0.5bn €0.5bn

1. Adjusted for non operating effects, 2. Percentage as of Group EBIT.

Core EBIT1 2017 Share of regulated/long-term contracted

businesses2

Energy Networks Renewables

Regulated/contracted

Merchant

Strong pillars with Customer Solutions and Renewables

65

E.ON standalone

2017 yet another year of strong delivery

Highlights Key Financials1

€ m

1. Adjusted for non operating effects.

EBIT Adj. Net Income

Economic Net Debt

26.3

FY 2016 FY 2017

19.2

-7.1

EBIT and Adj. Net Income at the upper end of the guidance range

Adj. Net Income + 58% versus FY 2016

Economic net debt reduced to €19.2bn

Dividend 2017 of €0.30/share confirmed

€ m

€ bn

Guidance range EBITDA €2.8-3.1bn, Adj. Net Income 1.2-1.45bn

FY 2016 FY 2017

3,112 3,074

904

FY 2017FY 2016

1,427

+58%

66

E.ON standalone

E.ON Investor Relations contacts

T +49 (201) 184 [email protected]

Alexander Karnick T+49 (201) 184 28 38Head of Investor Relations [email protected]

Martina Burger T +49 (201) 184 28 07Manager Investor Relations [email protected]

Dr. Stephan Schönefuß T +49 (201) 184 28 22Manager Investor Relations [email protected]

Andreas Thielen T +49 (201) 184 28 15Manager Investor Relations [email protected]

67

Financial calendar & important links

Financial calendar

May 8, 2018 Quarterly Statement: January – March 2018

May 9, 2018 2018 Annual Shareholders Meeting

May 14, 2018 Dividend Payment

August 8, 2018 Half-Year Financial Report: January – June 2018

November 14, 2018 Quarterly Statement: January – September 2018

March 13, 2019 Annual Report 2018

Important links

Presentations https://www.eon.com/en/investor-relations/presentations.html

Annual Reports https://www.eon.com/en/investor-relations/financial-publications/annual-report.html

Interim Reports https://www.eon.com/en/investor-relations/financial-publications/interim-report.html

Shareholder Meeting https://www.eon.com/en/investor-relations/shareholders-meeting.html

Bonds / Creditor Relations https://www.eon.com/en/investor-relations/bonds.html

68

Transaction Website: http://www.energyfortomorrow.de/

DisclaimerThis presentation contains information relating to E.ON Group (“E.ON") that must not be relied upon for any purpose and may not be redistributed, reproduced,published, or passed on to any other person or used in whole or in part for any other purpose. By accessing this document you agree to abide by the limitations set outin this document.This document is being presented solely for informational purposes. It should not be treated as giving investment advice, nor is it intended to provide the basis for anyevaluation or any securities and should not be considered as a recommendation that any person should purchase, hold or dispose of any shares or other securities. Thispresentation is in particular neither an offer to purchase nor a solicitation of an offer to sell shares in innogy SE. The final terms and further provisions regarding thetakeover offer by E.ON Verwaltungs SE to the shareholders of innogy SE will be set forth in the offer document which will be published upon approval of its publicationby the German Federal Financial Supervisory Authority. Investors and shareholders in innogy SE are strongly recommended to read the offer document and allannouncements and documents published in connection with the takeover offer, since they will contain important information.The information contained in this presentation may comprise financial and similar information which is neither audited nor reviewed and should be consideredpreliminary and subject to change.Some of the information presented herein is based on statements by third parties. No representation or warranty, express or implied, is made as to, and no relianceshould be placed on, the fairness, accuracy, completeness or correctness of this information or any other information or opinions contained herein, for any purposewhatsoever.This announcement may contain statements about E.ON or innogy SE that are or may be “forward-looking statements”. Forward-looking statements include, withoutlimitation, statements that typically contain words such as “anticipate”, “target”, “expect”, “estimate”, “intend”, “plan”, “believe”, “hope”, “aims”, “continue”, “will”,“may”, “should”, “would”, “could”, or other words of similar meaning. By their nature, forward-looking statements involve risks and uncertainties because they relate toevents and depend on circumstances that may or may not occur in the future. E.ON cautions you that forward-looking statements are not guarantees of the occurrenceof such future events or of future performance and that in particular the actual results of operations, financial condition and liquidity, the development of the industry inwhich E.ON and innogy SE operate and the outcome or impact of the proposed acquisition on E.ON and/or innogy SE may differ materially from those made in orsuggested by the forward-looking statements contained in this announcement. Any forward-looking statements speak only as at the date of this announcement.Neither E.ON nor any respective agents of E.ON undertake any obligation to provide the recipient with access to any additional information or to update thispresentation or any information or to correct any inaccuracies in any such information.

69