gruh finance limited loans (rs. in crores) as at sept. 30, 2017 as at sept. 30, 2016 amount % amount...

TRANSCRIPT

GRUH Finance LimitedGRUH Finance Limited(A Subsidiary of HDFC Limited)(A Subsidiary of HDFC Limited)

Sept 2017

1

GRUH PROFILEGRUH PROFILE

2 2

• Promoted by HDFC & AKFED on July 21, 1986

• Commenced operations in 1988 from Ahmedabad

• A subsidiary of HDFC - Since June 2000A subsidiary of HDFC Since June 2000

• Regulated by National Housing Bank (NHB) – Wholly

owned subsidiary of Reserve Bank of India (RBI)

• Recognized by NHB for Refinance facility• Recognized by NHB for Refinance facility

3

As on Sept. 30, 2017

• Cumulative Housing Units Financed – 3,87,764

• Cumulative Disbursement of Rs. 25,459 Cr.

• Cumulative Disbursement in Rural Areas(*) – Rs. 11,736 Cr.

• Retail Network of 187 offices across 11 States & one UT• Retail Network of 187 offices across 11 States & one UT

• Consistent track record of Dividend Payout

(*) Rural Areas are locations where populations is less than 50,000

4

As on Sept. 30, 2017

• LoanDisbursementduring the period – Rs.2,483Cr.g p ,

• AverageLoanPer Unit onDisbursementduring the Period–Rs. 9.34Lac

• OutstandingLoanAssets of Rs 14 304 CrOutstandingLoanAssets of Rs. 14,304 Cr.

• AverageLoanOutstanding Per Unit – Rs. 6.51Lac

GrossNPAs Rs 95 55 Cr 0 67%of OutstandingLoanAssets of Rs 14 304Cr• GrossNPAs Rs. 95.55 Cr– 0.67%of OutstandingLoanAssets of Rs. 14,304Cr.

• Net NPAs – 0.07% (PY– 0.29%)

5

Ratingsg• Public Deposits :

– ‘MAAA’ by ICRA and– ‘FAAA’ by CRISIL

• Non-Convertible Debentures : ‘AAA (Stable)’ by ICRA and CRISILand CRISIL

• Subordinated NCD: ‘AAA (Stable)’ by ICRA and CRISIL• Commercial Paper : ‘A1+’ by ICRA and CRISILCommercial Paper : A1+ by ICRA and CRISIL

“These rating indicates high safety with regard to timely t f i t t d i i l”payment of interest and principal”

6

GRUH PERFORMANCEGRUH PERFORMANCE

7 7

Disbursements(Rs. in Crores)

2500

3000

2,483

2000

1000

1500

960

500

0Sept'12 Sept'13 Sept'14 Sept'15 Sept'16 Sept'17

88

Loan Assets(Rs. in Crores)

14000

16000

14,304

10000

12000

6000

8000

4,672

2000

4000

0Sept'12 Sept'13 Sept'14 Sept'15 Sept'16 Sept'17

99

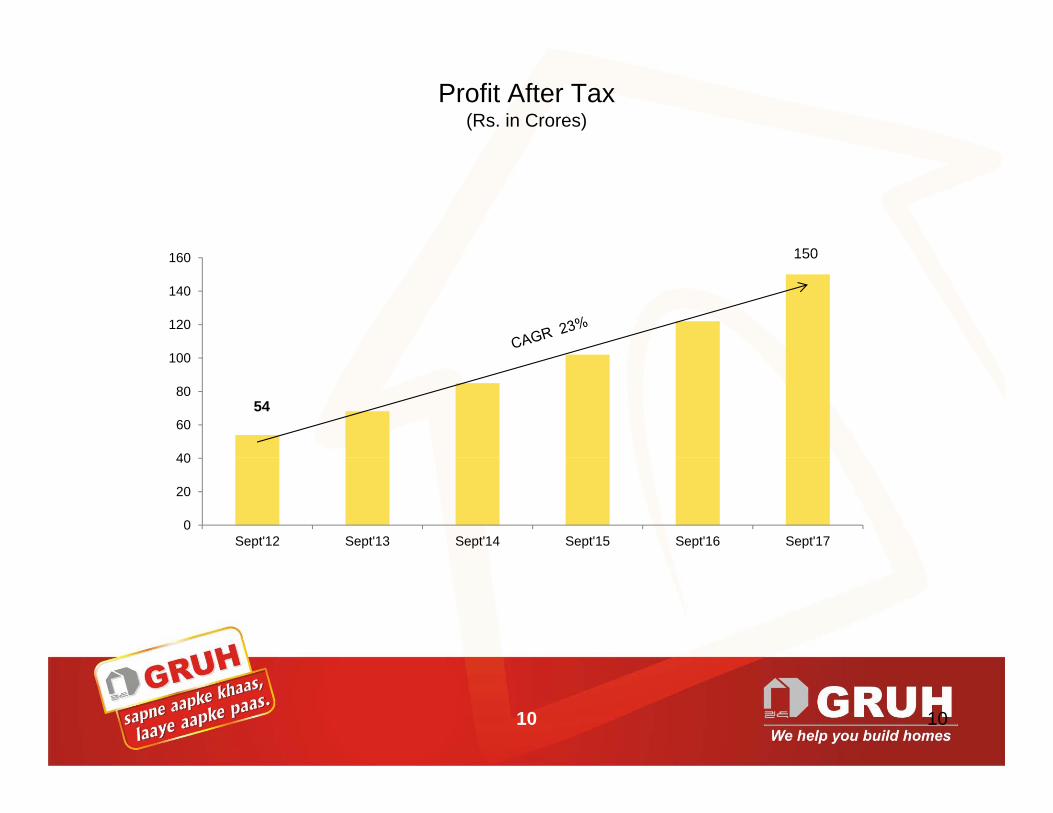

Profit After Tax(Rs. in Crores)

160 150

100

120

140

160 150

40

60

80

100

54

0

20

40

Sept'12 Sept'13 Sept'14 Sept'15 Sept'16 Sept'17

1010

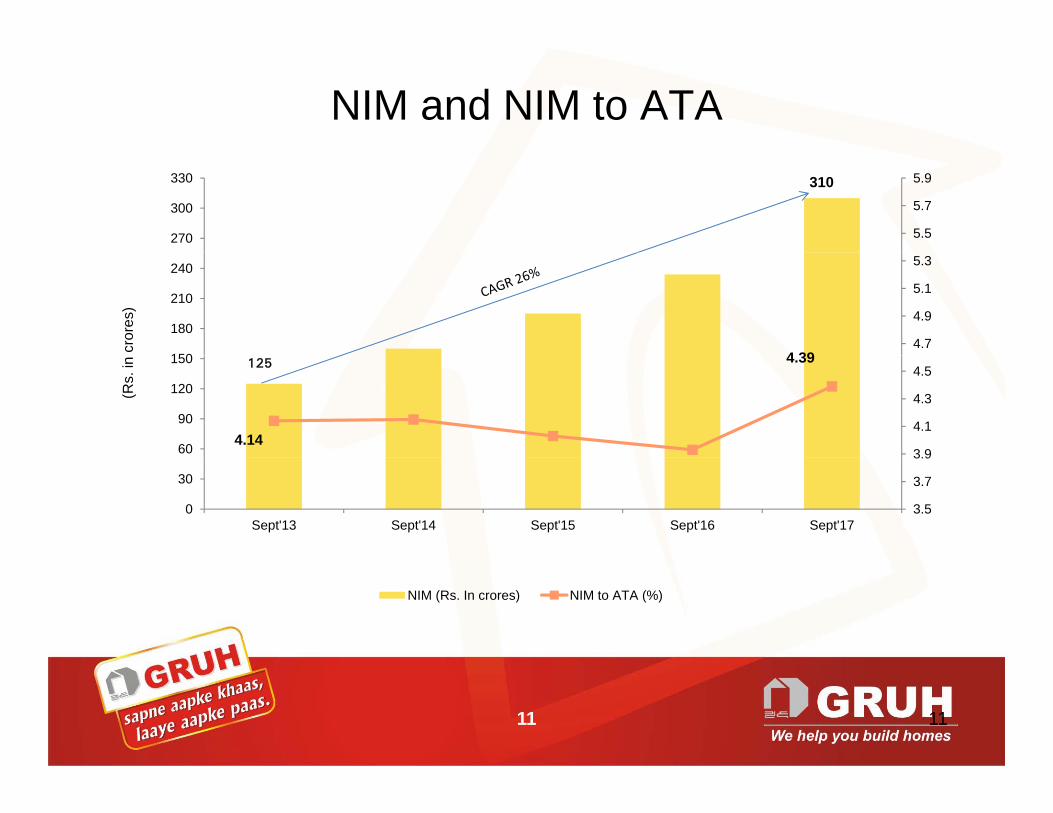

NIM and NIM to ATA

5.5

5.7

5.9

270

300

330 310

4.7

4.9

5.1

5.3

150

180

210

240

4 39cror

es)

3.9

4.1

4.3

4.5

60

90

120

150

4.14

4.39125

(Rs.

in

3.5

3.7

3.9

0

30

Sept'13 Sept'14 Sept'15 Sept'16 Sept'17

NIM (Rs. In crores) NIM to ATA (%)

1111

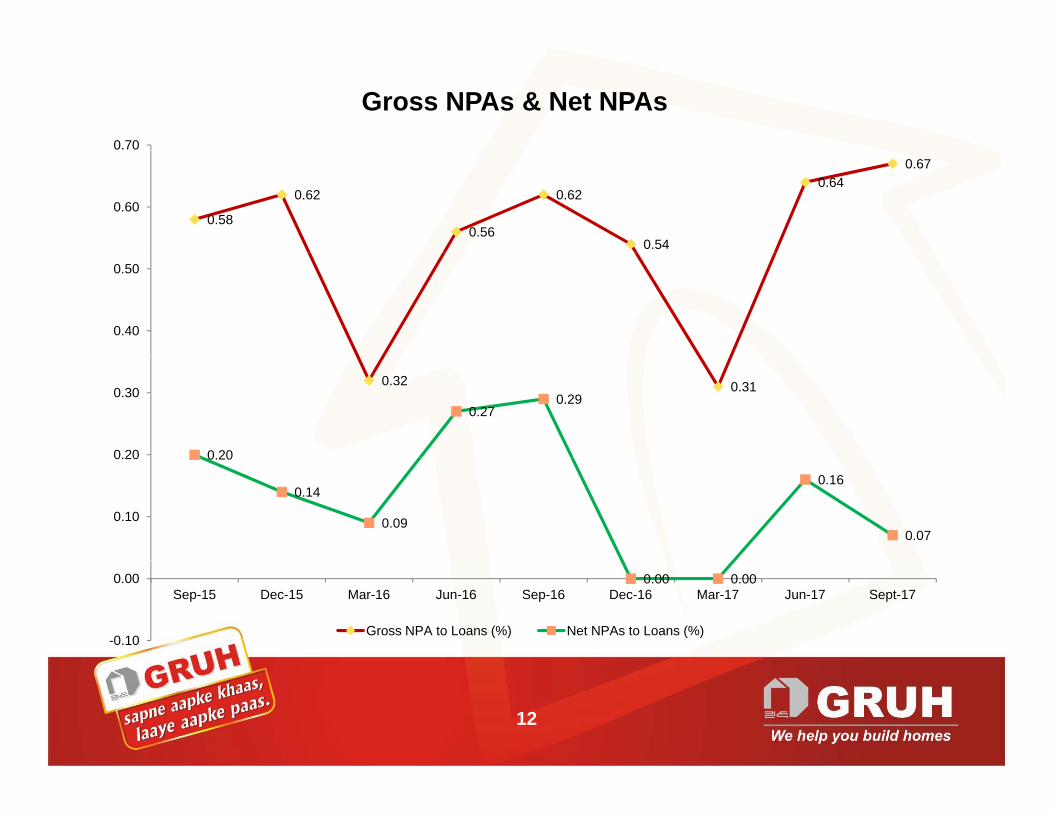

Gross NPAs & Net NPAs0.70

0.58

0.62

0.56

0.62

0.54

0.640.67

0.60

0.40

0.50

0.32 0.31

0 20

0.270.29

0.20

0.30

0.20

0.14

0.09

0.16

0.070.10

0.20

0.00 0.00

-0.10

0.00Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16 Mar-17 Jun-17 Sept-17

Gross NPA to Loans (%) Net NPAs to Loans (%)

12

Provisions & Contingencies 70 00

51.4453.90

56.7159.04

63.1364.63 65.56

52.55

61.6060.00

70.00

In C

rore

)

43.21

47.23

51.44

34.97

41.78

40.00

50.00

(Rs.

23.96 23.96 23.9624.61

16 6319.45

22.92

20.00

30.00

13.6515.67

8.54

14.46 16.06 15.6316.63 16.63

10.00

20.00

0.00Sep- 15 Dec- 15 Mar- 16 Jun- 16 Sep- 16 Dec - 16 Mar - 17 Jun- 17 Sept- 17

Provision for NPAs Provision for Standarad Assets Provision for Contingencies

13

NIM & NIE to Average Total Assets

4.38 4.394 00

4.50

5.00

4.03 4.05 4.083.90 3.92

4.11 4.204.38

3.00

3.50

4.00

1.50

2.00

2.50

0.88 0.83 0.790.67 0.78 0.74 0.72 0.72 0.77

0 00

0.50

1.00

0.00Sep- 15 Dec- 15 Mar- 16 Jun- 16 Sep - 16 Dec - 16 Mar - 17 Jun - 17 Sept - 17

Net Interest Margin to Average Total Assets(%) Non-Interest Expenses to Average Total Assets (%)

14

PBT & PAT to Average Total Assets

3.20

3.15

3.51

3.11

3.53

3 13

3.22

3 00

3.50

4.00

2 0

2.36

2.05 2.372 09 2 12

3.06 3.09 3.13

2 00

2.50

3.00

2.112.07 2.05 2.04 2.09 2.12

1.00

1.50

2.00

0.00

0.50

S t 15 D 15 M 16 J 16 S 16 D 16 M 17 J 17 S t 17Sept- 15 Dec- 15 Mar- 16 Jun - 16 Sep - 16 Dec - 16 Mar - 17 Jun- 17 Sept- 17

PAT to Average Total Assets (%) PBT to Average Total Assets (%)

15

Cost to Income Ratio (%)

18.5120 00

25.00

19.5117.44

16.06

18.3516.68 15.87 15.46

16.3615.00

20.00

10.00

0.00

5.00

Sept- 15 Dec- 15 Mar- 16 Jun- 16 Sep - 16 Dec - 16 Mar- 17 Jun- 17 Sept- 17p p p

Cost to Income Ratio (%)

16

Loan DisbursementsLoan DisbursementsAs at

Sept 30 2017As at

Sept 30 2016Growth

(Rs. in Crores)

Sept 30, 2017 Sept 30, 2016

Amount Amount %

Home Loans * 1908 61 1474 05 29 48Home Loans * 1908.61 1474.05 29.48

Mortgage (LAP) Loans * 277.76 218.96 26.85

NRP Loans * 37 49 30 19 24 18NRP Loans * 37.49 30.19 24.18

Developer Loans 259.07 221.61 16.90

T t l 2482 93 1944 80 27 67Total 2482.93 1944.80 27.67

(*) Individual Loans

17

Outstanding Loans (Rs. in Crores)

As at Sept. 30, 2017 As at Sept. 30, 2016

Amount % Amount %

Suraksha Home Loans 7320.55 51.18 6332.64 52.38

Suvidha Home Loans 4282.61 29.94 3430.49 28.38

S j t R i L 122 18 0 85 57 66 0 48Sajavat Repair Loans 122.18 0.85 57.66 0.48

Total Home Loans * 11727.41 81.99 9820.79 81.23

Mortgage (LAP) Loans * 1593.03 11.14 1385.18 11.46g g ( )

NRP Loans * 412.53 2.88 382.00 3.16

Developer Loans 573.15 4.01 501.16 4.15

Total 14304.25 100.00 12089.13 100.00

(*) Individual LoansLoan Asset Growth of 18%

18

Loan Portfolio-wise NPLAs at Sept. 30, 2017 As at Sept. 30, 2016

Amount % Amount %

H L * 69 27 0 59 49 43 0 50Home Loans * 69.27 0.59 49.43 0.50

Mortgage (LAP) Loans * 19.03 1.19 15.70 1.13

NRP Loans * 7.25 1.77 9.45 2.47

Developer Loans 0.00 0.00 0.00 0.00

Total 95.55 0.67 74.57 0.62

(*) Individual Loans

19 19

Assets Profile

1.05%%

1.43%

1.41% 1.54% 1.09%

0.09% 0.11% 0.17%

98%

99%

100%

1.05%1.12%

96%

97%

97.45% 97.23% 97.31%

93%

94%

95%Fixed Assets Current Assets Investments Loan Assets

91%

92%

93%

90%

Sept 17 Sept 16 Sept 15

20

Sources of Borrowingg47%

45%

50%

34%

29%

33%

30%30%

35%

40% NHB

Bank Loans

Public Deposits

Others

23%

19%

23%

15%

23%

20%

25%

11%13%

15%

5%

10%

15%

0%Sept‐17 Sept‐16 Sept‐15

21

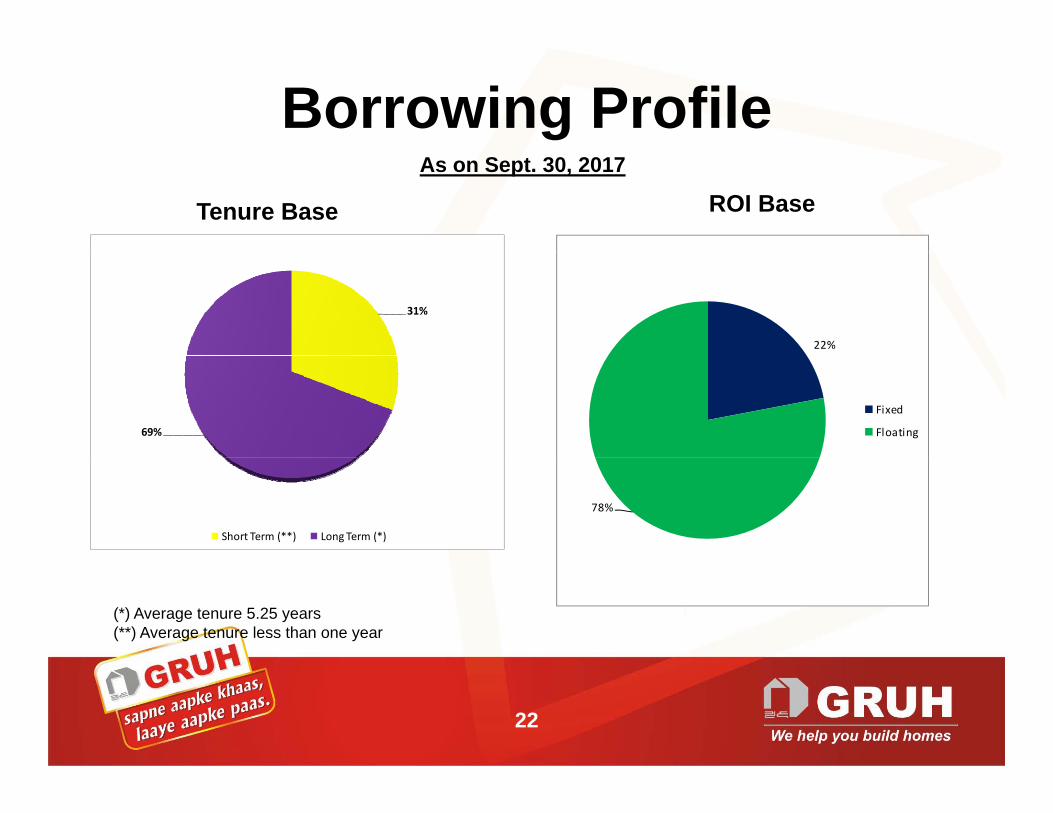

Borrowing Profile As on Sept. 30, 2017

ROI Base Tenure Base

31%

22%

69%

Fixed

Floating

Short Term (**) Long Term (*)

78%

(*) Average tenure 5.25 years(**) Average tenure less than one year

22

Balance SheetAs on Sept. 30, (Rs. in Crores)

2017 2016 Growth (%)

Sources of Funds

Share Capital 73.08 72.78 -

Reserves & Surplus 1086 61 889 56 22Reserves & Surplus 1086.61 889.56 22Borrowings 12965.16 11092.03 17Current Liabilities & Provisions 430.31 313.29 37Deferred Ta Liabilit (Net) 123 84 65 29 90Deferred Tax Liability (Net) 123.84 65.29 90

14679.00 12432.95 18

Application of Funds

Loan Assets 14304.25 12089.13 18Investments 153.60 138.94 11Current Assets 207.20 190.84 9Fixed Assets 13.95 14.04 (1)

14679.00 12432.95 18

23

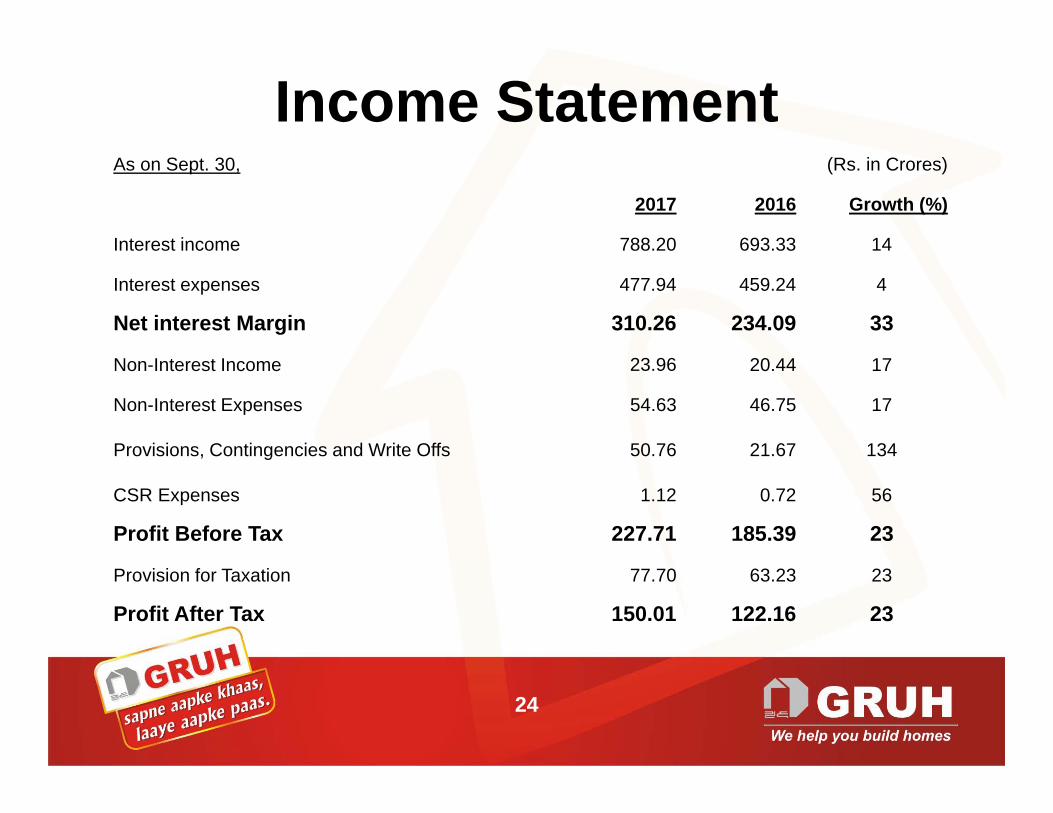

Income StatementAs on Sept. 30, (Rs. in Crores)

2017 2016 Growth (%)

Interest income 788.20 693.33 14

Interest expenses 477.94 459.24 4

Net interest Margin 310.26 234.09 33

Non-Interest Income 23.96 20.44 17

Non-Interest Expenses 54.63 46.75 17

Provisions, Contingencies and Write Offs 50.76 21.67 134, g

CSR Expenses 1.12 0.72 56

Profit Before Tax 227.71 185.39 23

Provision for Taxation 77.70 63.23 23

Profit After Tax 150.01 122.16 23

24

Risk Profile Loan Assets & NPAs

As on Sept. 30, (Rs. in Crores)

2017 2016Loan Assets (Rs.) 14304.25 12089.13

Provision for Standard Assets (Rs.) 65.56 56.71

Gross NPAs (Rs ) 95 55 74 57Gross NPAs (Rs.) 95.55 74.57

Provision for NPAs (Rs.) 23.96 16.06

Provision for Contingencies 61.60 22.92

Net NPAs (Rs.) 10.00 35.59

RatiosGross NPA as % to Loans 0.67 0.62

Net NPA as % to Loans 0.07 0.29

Net NPA to Net worth 0.86 3.70

25

Quarterly Financial ResultsAs on Sept 30, (Rs. In Crore)

Q2-CY Q2-PY Q1-CY YOY CY YOY PY1. Operating Income 414.05 367.43 398.12 1585.79 1382.971. Operating Income 414.05 367.43 398.12 1585.79 1382.97

2. Total Income 414.05 367.43 398.12 1585.79 1382.97

3. Interest and Other Charges 241.49 235.14 236.45 938.32 877.73

4 Non interest Expenses 29 56 26 59 24 77 99 01 85 894. Non-interest Expenses 29.56 26.59 24.77 99.01 85.89

5. Depreciation 0.77 0.74 0.66 2.81 3.01

6. Provisions, Contingencies & Write Offs 22 84 9 13 27 92 61 33 24 35Write Offs 22.84 9.13 27.92 61.33 24.35

7. Total Expenditure 294.66 271.60 289.80 1101.47 990.98

8. Profit Before Tax 119.39 95.83 108.32 484.32 391.99

9. Tax Expenses 41.62 33.85 36.08 159.82 128.27

10. Profit After Tax 77.77 61.98 72.24 324.50 263.72

26

Key Financial RatiosAs on Sept. 30,

2017 2016 2015

Net Interest Margin / ATA (%) 4.39 3.92 4.03

Non Interest Expenses / ATA (%) 0 77 0 78 0 88p ( ) 0.77 0.78 0.88

PBT/ATA (%) 3.22 3.11 3.20

PAT/ATA (%) 2 12 2 05 2 11( ) 2.12 2.05 2.11

Cost to Income Ratio (%) 16.36 18.35 19.51

Return on Equity (%) 26.40 27.18 26.74q y ( ) 26.40 27.18 26.74

ATA = Average Total Assets

27

Key Financial RatiosKey Financial Ratios

Particulars Sept. 30, 2017 Sept. 30, 2016

Book Value Per Share 32 26

Earnings Per Share 4.11 3.36

Market Capitalization (Rs. In Crore) 17,965 11,923

28 28

Key Financial RatiosKey Financial Ratios

As on Sept. 30,

2017 2016 2015C it l Ad R ti (%)Capital Adequacy Ratio (%) 17.48 18.26 15.73

Tier – I 16.07 16.65 14.33

Ti IITier –II 1.41 1.61 1.40

29

Productivity RatiosProductivity RatiosAs on Sept. 30,

2017 2016 20152017 2016 2015

Average No. of Employees 668 637 593

Average No. of Retail offices 184 176 160

Profit After Tax Per Employee (Rs. in Lakhs) 45 38 34

Total Assets Per Employee ( Rs. in Lakhs) 2199 1952 171899 1952 1718

30

Rural Focus(Rural location is a location where population is less than 50000.

A state is divided into districts and each District cover 10-15 Talukas and each Taluka is a cluster of 80-100 villages)

• Loan Disbursement in Rural Areas during the Period – Rs. 1,064 Cr.

• Cumulative Rural Disbursement of Rs 11 736 Cr• Cumulative Rural Disbursement of Rs.11,736 Cr.

• Disbursed 2,13,938 cases in rural segment

P i 127 Di t i t f 11 St t• Presence in 127 Districts of 11 States

• Servicing customers in 1,174 Taluka places in 11 States

31

Thank You