gst opportunities and challanges for cma and challenges for cmaopportunities and challenges for cma...

TRANSCRIPT

Implementation of Goods Implementation of Goods Implementation of Goods Implementation of Goods and Service Tax (GSTand Service Tax (GSTand Service Tax (GSTand Service Tax (GST))))

in India in India in India in India

Opportunities and Opportunities and Opportunities and Opportunities and Challenges for CMAChallenges for CMAChallenges for CMAChallenges for CMA

CMA Rajesh ShuklaCMA Rajesh ShuklaCMA Rajesh ShuklaCMA Rajesh Shukla

At ICWA Chapter meet At ICWA Chapter meet At ICWA Chapter meet At ICWA Chapter meet

14141414thththth August 2015August 2015August 2015August 2015

AurangabadAurangabadAurangabadAurangabad

Present Indirect Taxation StructurePresent Indirect Taxation StructurePresent Indirect Taxation StructurePresent Indirect Taxation Structure

2

Background of GSTBackground of GSTBackground of GSTBackground of GST

Goods and Services

tax (‘GST’)

Broad based consumption tax

Unified tax on both on goods and

services

Levied at each stage

On value added to goods/ services at

each stage

Introduced with the objective to

‘eliminate tax cascades’

Integration of prevailing indirect taxes

to ensure uniformity

Preventing cascading effect of taxes

Simplified compliances

Credit available across goods and

services

Availability of credit even for inter-state

procurements

What is GST Why GST

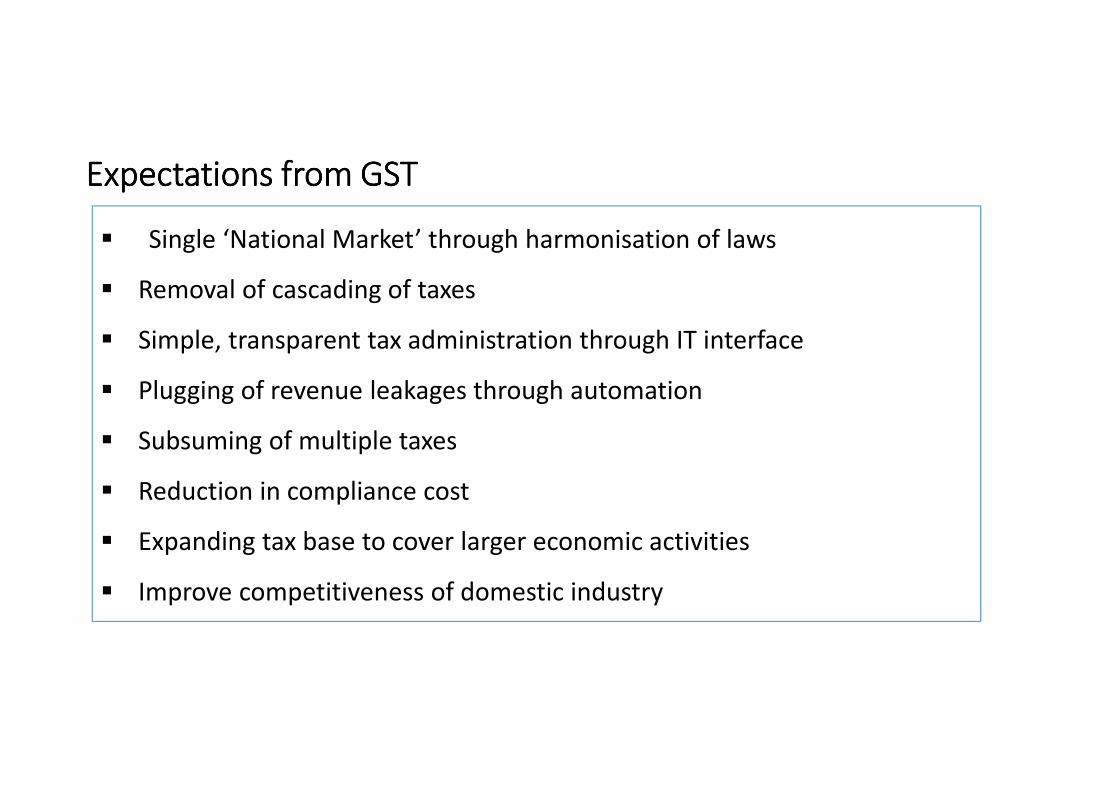

Expectations from GSTExpectations from GSTExpectations from GSTExpectations from GST

� Single ‘National Market’ through harmonisation of laws

� Removal of cascading of taxes

� Simple, transparent tax administration through IT interface

� Plugging of revenue leakages through automation

� Subsuming of multiple taxes

� Reduction in compliance cost

� Expanding tax base to cover larger economic activities

� Improve competitiveness of domestic industry

Framework of Goods and Services tax in IndiaFramework of Goods and Services tax in IndiaFramework of Goods and Services tax in IndiaFramework of Goods and Services tax in India

FrameworkDual GST

IGST + AT*

CGST and SGST Intra-State transactions

IGST +AT*Inter-State Sales and

Branch Transfers

*Additional Tax only on goods

CoverageIndirect taxes to be subsumed

Indirect taxes to be continued

Basic Duty of Customs ����

Additional Duty of Customs and Cess on such duty ����

Central Excise ����

Service tax ����

VAT/ CST* ����

Entry tax not in lieu of Octroi ����

Octroi, LBT and Cesses ����

Municipal/ Property tax ����

State Excise on Liquor ����

Stamp duty ����

Motor Vehicles tax ����

Entertainment tax and Luxury tax ����

Entry tax in lieu of Octroi ����

Framework of Goods and Services tax in IndiaFramework of Goods and Services tax in IndiaFramework of Goods and Services tax in IndiaFramework of Goods and Services tax in India

Rate of taxGoods

Services

YearGoods

Standard Concessional

Year II

Year I

Year III

onwards

20 percent 12 percent

18 percent 12 percent

16 percent 16 percent

Services

16 percent

16 percent

16 percent

YearGoods

Standard Concessional

Year II

Year I

Year III

onwards

~27 percent?

Services

Framework of Goods and Services tax in IndiaFramework of Goods and Services tax in IndiaFramework of Goods and Services tax in IndiaFramework of Goods and Services tax in India

Cross Credits

Central GST (‘CGST’)

State GST (‘SGST’)

Inter-State GST (‘IGST’)

Credit Output Liability

IGST IGST, CGST, SGST

CGST CGST, IGST

SGST SGST, IGST

Framework of Goods and Services tax in IndiaFramework of Goods and Services tax in IndiaFramework of Goods and Services tax in IndiaFramework of Goods and Services tax in India

ThresholdThresholdThresholdThreshold

Following limits are under discussion. (lower limits for some states.)

Annual Financial Turnover Remarks

Up to Rs. 25 lakhs Exempt from GST

From Rs. 25 lakhs to Rs. 75 lakhs Composition option maybe given without ITC

Rs. 75 lakhs to Rs. 100 lakhsEntire GST including CGST, IGST to be monitored by State – No involvement of

Central Government

Above Rs. 100 lakhsUnits will be under dual authorities – CGST and IGST will be monitored by Central

Govt. and SGST to be monitored by State Govt.

GST : Summary of Business Impact

Current and Future

Investments

Human Resource

Procurement / Sourcing

Accounting

Sales & Marketing

Logistics ProfitabilityProduct Pricing

Distribution

Working Capital

GST

GST : Snap shot of Impacted Business Areas GST : Snap shot of Impacted Business Areas GST : Snap shot of Impacted Business Areas GST : Snap shot of Impacted Business Areas

GST : Summary of Business Impact

Sr.No. Business Area Impact

1 Procurement � Higher Tax Rate, But - Lower Cost of Tax

� Saving of CST, But incidence of 1% Additional Tax� Credit of all Taxes paid on procurement – Goods + Services

� Increase in Working Capital requirements

2 Distribution / Logistics � Rationalization of Tax Rate – Multiple to Single / Two rates� Saving of CST, But incidence of 1% Additional Tax� Sales from factory / through RSO will be at par� Logistics function will need relook

� Working Capital need of Channel Partners will increase.� After Sales Services – Increase in Tax Rates

3 Manufacturing � Area based exemption from excise duty is not likely to continue under GST.

� Need to get converted into “Refund” schemes – Hard Negotiations with Government required.

� Inter unit transfers to cost 1% additional non-vatable tax

4 Finance(Profitability ,Working Capital ,

Tax compliance, accounting, investment decisions)

� Product Cost / Pricing will go under change � Future Products / Investment decisions needs to be revisited.

� Working Capital requirement will increase� Change in Accounting and reporting

� Indirect Tax compliance.

5 Information Technology � ERP System will need revamp / re-implementation.

GST : Snap shot of Impacted Business Areas GST : Snap shot of Impacted Business Areas GST : Snap shot of Impacted Business Areas GST : Snap shot of Impacted Business Areas

Invoicing under GSTInvoicing under GSTInvoicing under GSTInvoicing under GST

12

Impact on Supply Chain Impact on Supply Chain Impact on Supply Chain Impact on Supply Chain –––– Manufacture & Sale / ExportManufacture & Sale / ExportManufacture & Sale / ExportManufacture & Sale / Export

13

GST RegistrationGST RegistrationGST RegistrationGST Registration

Salient Features

►Separate registration for each State

►15-digit (alpha-numeric) PAN-based GSTIN

►Fully online registration process with no

physical documentation / inspection of

business premises involved

►Flexibility to use existing registration data in

one State as template for further registrations

►Option to authorize representative during

Registration

►Amendments of non-core fields of registration

data on self-service basis

► Migration of existing dealers

► Dual Jurisdiction mechanism

► Single vs Multiple registration within a State

► No clarity on how Input Service

Distribution (ISD) mechanism will work

► Extent of State specific fields in the

Registration Form

Open Points

GST Return

Salient Features

►Monthly return filing for all Regular

taxpayers

►Self-assessment of tax liability (for one

tax period only)

►Common e-Return for CGST, SGST,

IGST and Additional Tax (for each

registration)

► Upload of B2B supply invoice

information is must before filing of return;

Procurement list (B2B) to be generated

automatically by GSTN

►Annual Return to include reconciliation

statement with the audited financial

statements of the taxpayers

► Place of Supply rules and its implications on Return filing

► Destination State wise aggregation of B2C inter-State supply details

► Capturing and processing of

information pertaining to non-eligibility / partial eligibility of credit

(including capital goods)

► Mechanism for auto reversal of credit; revision of submitted invoice

information and its impact on counter-party

Open Points

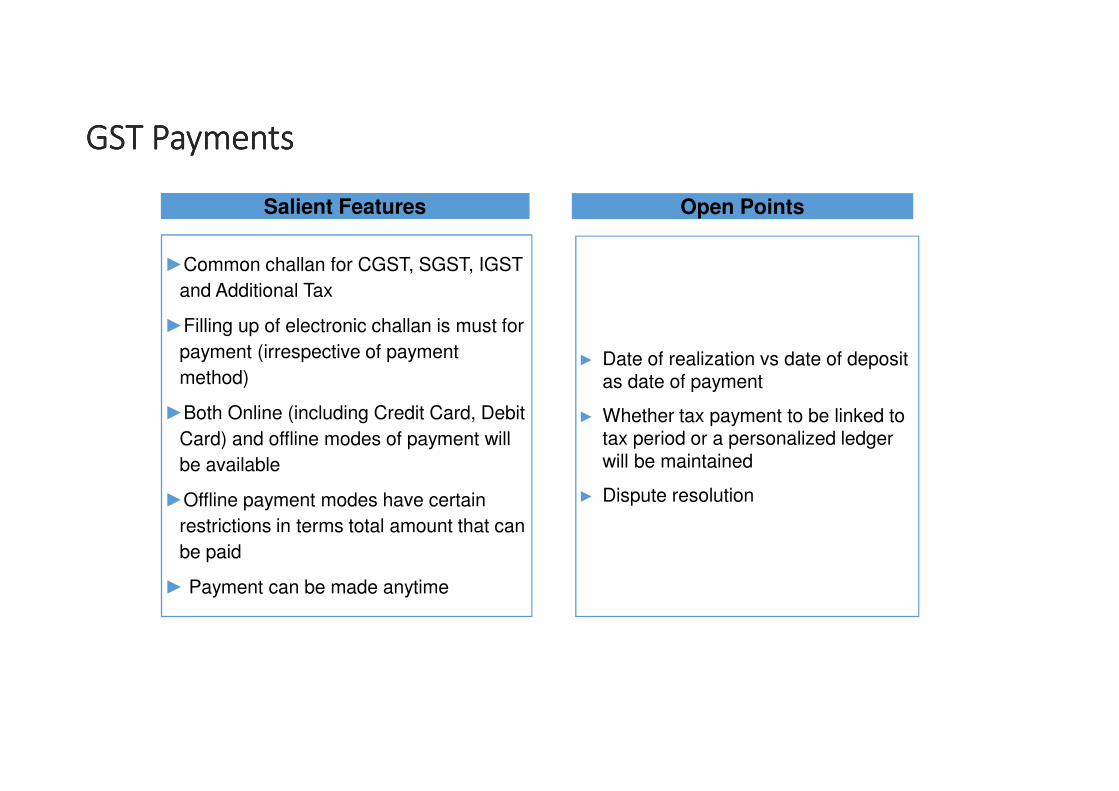

GST PaymentsGST PaymentsGST PaymentsGST Payments

Salient Features

►Common challan for CGST, SGST, IGST

and Additional Tax

►Filling up of electronic challan is must for

payment (irrespective of payment

method)

►Both Online (including Credit Card, Debit

Card) and offline modes of payment will

be available

►Offline payment modes have certain

restrictions in terms total amount that can

be paid

► Payment can be made anytime

► Date of realization vs date of deposit as date of payment

► Whether tax payment to be linked to tax period or a personalized ledger

will be maintained

► Dispute resolution

Open Points

Illustrative Return filing stepsIllustrative Return filing stepsIllustrative Return filing stepsIllustrative Return filing steps

► Upload of B2B supply invoice level details

► Auto-drafting of counter-party purchase register based on such uploaded supply invoice details

► Acceptance of auto-drafted purchase register by counter-party dealer

► Generation of draft return

► Payment of due tax

► Submission of Return

Key

Stake-

holders

Framework and key

decisionsState Finance

Ministry / VAT

Departments

CBECMinistry of

Commerce

State Industries

DepartmentGST Council

Empowered

Committee

State level levies and

procedures

GST implementation

Central incentives Central levies and procedures

State incentives

GST : Government Departments involved in implementation

Consensus between Centre & State on

power sharing

Agreement on the

Constitutional

Amendment Bill

(CAB)

Agreement on Taxing framework, more

specifically Place of Supply Rules

Industry feedback & finalization of Act &

Rules

Formation of GST Council

and Issue of draft

regulations & GSTN

framework

State fears on

loss of revenue &

compensation framework

Passing of the CAB

Roll - out

GST : GST : GST : GST : Progress and Roadmap from Government sideProgress and Roadmap from Government sideProgress and Roadmap from Government sideProgress and Roadmap from Government side

POWERS OF GST COUNCILPOWERS OF GST COUNCILPOWERS OF GST COUNCILPOWERS OF GST COUNCIL

�Taxes to be subsumed.

�Rate Structure

�Exemptions

�Threshold limits

�Model GST Law

�Principles of levy

�Apportionment of IGST

�Place of supply

�Special schemes for NE & Developing States

�Dispute Resolution Mechanism.

Open Issues Open Issues Open Issues Open Issues

► Fiscal Autonomy Vs Harmonization

► Tax Rates

► Tax Base

► Taxes to be subsumed

► Compensation to States

► Consensus in GST Council

► Dispute Resolution

Opportunities and challenges for CMA Opportunities and challenges for CMA Opportunities and challenges for CMA Opportunities and challenges for CMA

► Opportunities

► Expansion of scope – increase in number of assesse

► Equal opportunity – evolving tax law

► Supporting business for cost effective business model

► Participation in development of Systems, process and controls

► Tax Credit reconciliations

► Challenges

► Enhancement of Skills – Subject Knowledge / Presentation

► Gain visibility in organization - demonstrate passion / ownership of issue

► Build Reputation in Government - to get statutory recognition

23

THANK YOU