guidance for champs - hong kong institute of certified...

TRANSCRIPT

STU

DEN

TS’ S

ECTI

ON

Students’ Section

THE HONG KONG ACCOUNTANT MARCH 200342

Guidance for champsDear Registered Student,

In this edition of Hong Kong Accountant I should like to offer you some tips tohelp you study like a CHAMP!

Cultivate good study habits: in order to do that, you need to study consistently andproactively. Spread your studies over a period of time. Plan your study strategy asopposed to last minute cramming, spreading out your study load helps you retainknowledge longer. This is why the QP has workshops which involve students inactive learning and serve as revision milestones to assist in exam preparation.

Heightening concentration: go to a library, classroom or a quiet place when youseriously intend to study. Have a regular place to study. Ensure that your studyenvironment has the minimum distraction - turn off the TV, stop chattering, turnoff the music and remove chairs that are too comfortable if they are not helpingyou to concentrate.

Aim high: if you just aim to pass, the chances of failing are higher than if you wereto aim to score high marks or get a medal.

Mind over matter: If daydreaming is a problem, rein in your wandering mind bymaking notes or recall important points. Inject enthusiasm into your study. Activestudy is more effective than passively reading the text. Study when you are most alert. Avoid heavy meals before studying. If youfind studying on your own boring, form a study group and work together! Peer learning is a wonderfully effective way to learnand encourage teamwork

Practise and revise. Understand what you are studying. Passing professional examinations these days is about applying what youhave learnt and not regurgitating the facts from books. For open-book examinations, prepare as if you were taking a closedbook examination. It is a mistake to think that you would have enough time during the examination to look up referencebooks. Therefore a well-organised file of key references condensed for examination purposes is as far as you should go. If youdon't know how to identify issues and apply the concepts to the facts of the case, you have not understood your subject matterwell enough yet. So practise and revise. Do more reserach on the topic if needed. Use past examination questions to practiseand test your understanding. Finally, do mock examinations to polish your examination techniques.

I hope the above tips can help you in your studies and I wish you all every success in your examinations.

Examination ResultsThe examination results for modules A and C have been released. Those who passed deserve our congratulations. For thosewho failed the examination this time, take an audit of the reasons for failing. It is important to adopt a positive attitude whenwe fail and use it as a lesson for future success. Apart from the study tips mentioned above, do read through the Examiner’sComments from page 45, which will be available at the online QP Learning Support Centre.

Continuing Professional Development (CPD)As a prospective professional accountant, you are highly encouraged to participate in the CPD programmes organised by theSociety. Although they are organised for our members, registered students are entitled to avail themselves of these technicaland accounting related updates at member’s rates. What’s more, some of the programmes are offered in e-Learning mode, foryour convenience. For details of the upcoming CPD programmes, please go to www.hksa.org.hk/membership/cpd/index.php.

CPD has become an international standard for the professionals to keep abreast of the latest developments in theirrespective professions. Many professional bodies have made it compulsory to ensure that their members continuously enhancetheir ability to provide quality advice and services to their clients in the ever-changing business environment. In accountancy,the International Federation of Accountants (IFAC), of which the Society is a member, advocates the importance of CPD. In itsrecent Exposure Draft on CPD, it proposes to make CPD a standard for all its member bodies. Please read page 18 for details ofthe proposals made by the IFAC and the views of the Society.

Yours truly,Georgina ChanDirector of Education & Training

Director’s Message

STU

DEN

TS’ S

ECTI

ON

Students’ Section

THE HONG KONG ACCOUNTANT MARCH 200344

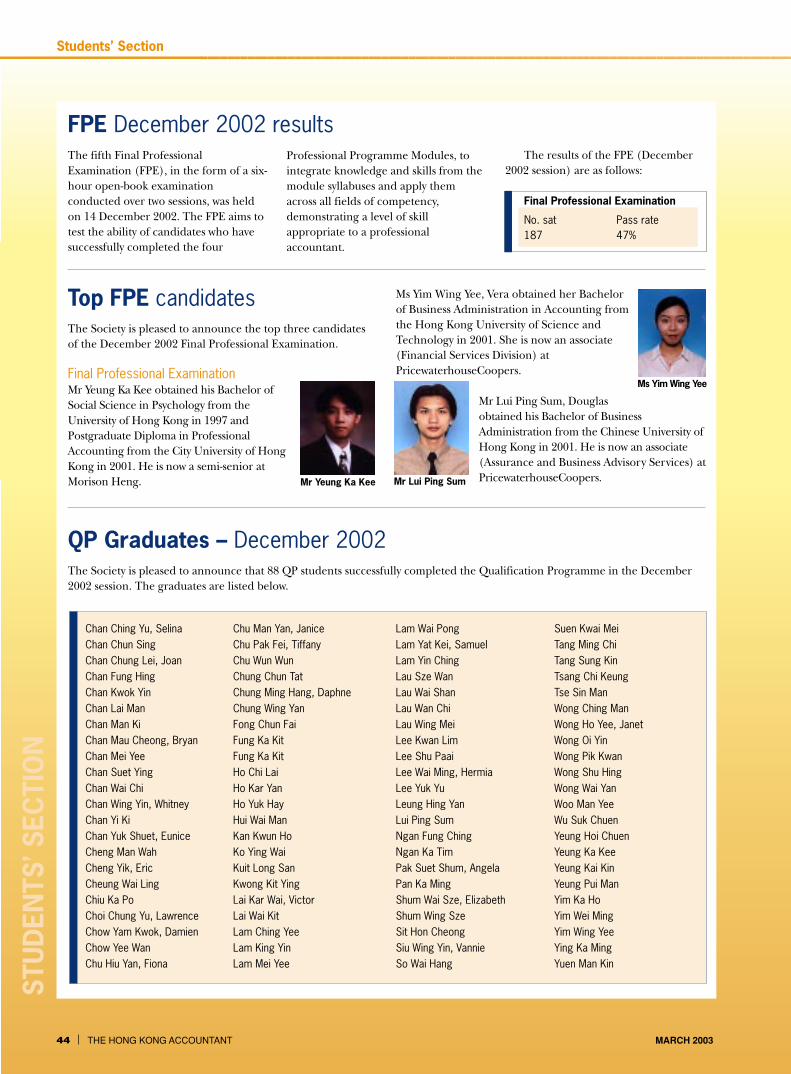

The fifth Final ProfessionalExamination (FPE), in the form of a six-hour open-book examinationconducted over two sessions, was heldon 14 December 2002. The FPE aims totest the ability of candidates who havesuccessfully completed the four

Professional Programme Modules, tointegrate knowledge and skills from themodule syllabuses and apply themacross all fields of competency,demonstrating a level of skillappropriate to a professionalaccountant.

The results of the FPE (December2002 session) are as follows:

Final Professional Examination

No. sat Pass rate187 47%

FPE December 2002 results

Mr Yeung Ka Kee

Ms Yim Wing Yee

Mr Lui Ping Sum

Top FPE candidatesThe Society is pleased to announce the top three candidatesof the December 2002 Final Professional Examination.

Final Professional ExaminationMr Yeung Ka Kee obtained his Bachelor ofSocial Science in Psychology from theUniversity of Hong Kong in 1997 andPostgraduate Diploma in ProfessionalAccounting from the City University of HongKong in 2001. He is now a semi-senior atMorison Heng.

Ms Yim Wing Yee, Vera obtained her Bachelorof Business Administration in Accounting fromthe Hong Kong University of Science andTechnology in 2001. She is now an associate(Financial Services Division) atPricewaterhouseCoopers.

Mr Lui Ping Sum, Douglasobtained his Bachelor of BusinessAdministration from the Chinese University ofHong Kong in 2001. He is now an associate(Assurance and Business Advisory Services) atPricewaterhouseCoopers.

Chu Man Yan, JaniceChu Pak Fei, TiffanyChu Wun WunChung Chun TatChung Ming Hang, DaphneChung Wing YanFong Chun FaiFung Ka KitFung Ka KitHo Chi LaiHo Kar YanHo Yuk HayHui Wai ManKan Kwun HoKo Ying WaiKuit Long SanKwong Kit YingLai Kar Wai, VictorLai Wai KitLam Ching YeeLam King YinLam Mei Yee

Chan Ching Yu, SelinaChan Chun SingChan Chung Lei, JoanChan Fung HingChan Kwok YinChan Lai ManChan Man KiChan Mau Cheong, BryanChan Mei YeeChan Suet YingChan Wai ChiChan Wing Yin, WhitneyChan Yi KiChan Yuk Shuet, EuniceCheng Man WahCheng Yik, EricCheung Wai LingChiu Ka PoChoi Chung Yu, LawrenceChow Yam Kwok, DamienChow Yee WanChu Hiu Yan, Fiona

Lam Wai PongLam Yat Kei, SamuelLam Yin ChingLau Sze WanLau Wai ShanLau Wan ChiLau Wing MeiLee Kwan LimLee Shu PaaiLee Wai Ming, HermiaLee Yuk YuLeung Hing YanLui Ping SumNgan Fung ChingNgan Ka TimPak Suet Shum, AngelaPan Ka MingShum Wai Sze, ElizabethShum Wing SzeSit Hon CheongSiu Wing Yin, VannieSo Wai Hang

QP Graduates – December 2002The Society is pleased to announce that 88 QP students successfully completed the Qualification Programme in the December2002 session. The graduates are listed below.

Suen Kwai MeiTang Ming ChiTang Sung KinTsang Chi KeungTse Sin ManWong Ching ManWong Ho Yee, JanetWong Oi YinWong Pik KwanWong Shu HingWong Wai YanWoo Man YeeWu Suk ChuenYeung Hoi ChuenYeung Ka KeeYeung Kai KinYeung Pui ManYim Ka HoYim Wei MingYim Wing YeeYing Ka MingYuen Man Kin

STU

DEN

TS’ S

ECTI

ON

Students’ Section

45MARCH 2003 THE HONG KONG ACCOUNTANT

General commentsThe final professional examinationpaper tested candidates’ ability to applyknowledge in solving practicalproblems across technical areas, andcommunicate effectively.

Candidates were expected to showtheir competence in integratingprofessional skills and knowledge acrossall areas of accounting and related skills,including financial reporting, financialmanagement, auditing and informationmanagement, and taxation. Specialattention should be given to effectiveanalytical and communication skills.

In what areas did candidatesperform poorly?• Too hasty in reading the questions

and could not understand therequirements of the questions

• Weak in identifying the issuesrequired in the answers and couldnot focus on the key topics;answered with a lot of irrelevantpoints to a question

• Some candidates failed to use themarks allocated for each questionas a time allocation reference.Hence some answers were too long,while others were too short

• Only searched for the materials onhand (CLP, SSAPs) and bound bythem; not able to think analyticallyand critically and/or search forsome relevant points not found inthe case and in the materials onhand

• Failed to apply practical knowledgeto a single question and thinkcritically and systematically

In what areas did candidatesperform well?• Time management improved and

most candidates could answer allquestions

• Able to attempt all questions, even

QP Examination panelists’ report–FinalProfessional Examination (December2002 session)

though they might not understandhow to tackle them

Specific commentsPaper ISection A – Case studyThis case study formed acomprehensive testing of thecandidates’ skills and knowledge acrossseveral disciplines, including financialreporting, financial management,management accounting, and taxation.

Generally speaking, questions 2(a)and 3 were straight forward, andcandidates were able to perform well.However, the performance in the otherquestions was not satisfactory.

Individual questionsQuestion 1This question required candidates toapply and integrate their knowledge infinancial reporting in order to identifyall the financial accounting andreporting issues related to a businesscombination.

The candidates seemed to lackawareness of the many issues that mayarise, in particular:• Since the two companies are not

under common control before thetransactions, this businesscombination is not regarded as agroup reconstruction and thus SSAP27 is irrelevant

• SSAP 30 ‘Business Combinations’takes the position that, in allbusiness combinations, one of thecombining enterprises obtainscontrol over the other combiningenterprise, thereby enabling anacquirer to be identified

• This means that fair value of thecost of acquisition and identifiableassets and liabilities should beascertained and goodwill should becalculated and amortised throughthe income statement

Question 2This question tested candidates’knowledge of the treatment of the leasefor accounting and tax purposes withthe related ethical consideration. Theaccounting treatment of the leasearrangement was straightforward, butmany candidates did not bother tocalculate the figures or do any analysis.

Many candidates were unable tomention that the treatment of the leasefor tax purposes may differ from thatfor income statement purposes. In fact,the SSAP 14 did not change the taxtreatment of the lease. Most candidatesmentioned Section 39E of the InlandRevenue Ordinance which disallowsthe depreciation on leased plant andmachinery if the lease is used wholly orprincipally outside Hong Kong ‘by aperson other than the taxpayer’ andfailed to mention the DepartmentalInterpretation and Practice Notes(DIPN) 15 Part F which is required bythis question. The DIPN 15 Part F haslaid down what the IRD considers basicrequirements for all leases. Probablythe candidates did not read thequestion carefully and have notproperly addressed the tax implicationof classification of finance andoperating lease.

Moreover, many candidates failed tomention that the directors of thecompany must look at the substance ofthe transaction instead of the legalform. Ethical considerations must begiven priority over the sole intention ofinflated reported profit figures.

Question 3This is a straightforward question.While most candidates performed wellin calculating the maximum licence feeas equivalent to what it is worth to thecompany, i.e. its net present value to thecompany at the company’s required rateof return, some candidates did notcompare the option to lease or topurchase.

Most candidates failed to mentionthat once the company decides toobtain the license to produce, thelicense fee becomes a sunk cost and

STU

DEN

TS’ S

ECTI

ON

Students’ Section

THE HONG KONG ACCOUNTANT MARCH 200346

thus irrelevant to the lease or purchasedecision. If the company is willing tolease instead of purchase, the presentvalue of the lease payment discountedat the required rate of return mustbe lower than the net cost of themachine (i.e. the original cost of themachine less the present value of theresale value).

Many candidates failed to makenote of the fact that depreciation ismerely an accounting method toallocate the original cost of an asset overits useful life. It is not an actual cashitem for discounting purposes. Besides,they failed to point out that fixedoverheads remain unchanged, bydefinition, whether the companydecides to undertake the project or notand thus they are irrelevant for netpresent value calculation.

Question 4This question tested candidates’ abilityto explain the advantages anddisadvantages of the various ways tofinance (other than the finance lease).Candidates performed well on thequestion if they could clearlydemonstrate the problems that thecompany encounters in choosingamong the various financing sources. Inparticular, to determine whether thecompany should borrow or issue shares,there are four key issues that thedirectors should consider, namely; risk,ownership and control, duration, anddebt capacity. Since the presentcontrolling shareholder may not want todilute its ownership and control, arights issue may be a better alternativethan issuing new shares to outsideparties.

Moreover, as dividends create cashoutflows, the company may want to cuttheir dividend payments to conservecash in order to invest in the newproject. However, dividend cuts arewidely regarded as the ultimate sign offinancial incompetence.

Most of the candidates failed tomention that the lower annual interestrate quoted for short-term debt gives lieto the common misapprehension that

short-term debt is cheaper than long-term debt. Since the company has topay the interest every 3-months, theeffective annual interest rate is (1 + 8per cent/4)4 = 8.243 per cent which ishigher than that for the 5-year long-term loan (8.125 per cent). Thus,short-term debt can be more expensivebecause of the difference in thecompounding period. This showscandidates’ inability to integrate theirknowledge and apply it to a practicalsituation.

Some candidates did not read thequestion carefully and thus they havespent time on discussing the financelease as an option to finance, which isexpressly excluded by the question.

Section B – EssaysThe overall performance of thecandidates was satisfactory. Comparedwith the previous two examinationsessions, students have improved a lot inanswering essay questions in thetaxation area.

More than 10 candidates did notanswer part 1(b) of the essay question.Even though this part only carries threemarks, it is important that candidatesallocate appropriate time to answerthem.

Several students mixed up the factsgiven in the essay; consequently theyscored no mark for the related analysis.For example, a student talked aboutwhether HK Ltd could deduct theconsultancy fee paid by WH Ltd;however the fees are paid to SG Ltd,not HK Ltd.

Several students misread therequirement of the question. Forexample, a student talked aboutwhether WH Ltd could deduct themarketing fees paid to HK Ltd.However, the question asked about thetaxability of the marketing fees receivedby HK Ltd.

Several students just recommendedfiling objection to the 2000/2001 profitstax assessments without specifyingwhich company/companies should fileobjection. Based on the answers of thecandidates, it appeared some of the

students wrote as if there was only oneobjection to be filed. In fact, thereshould have been two differentobjections to be filed, one for HK Ltdand the other one for WH Ltd.

Individual questionsQuestion 1(a)Most candidates could refer to therespective sections 14 and 16(1) indetermining the source of profits anddeductibility of expenses.

Whilst sections 61 and 61A hadbeen explicitly mentioned in thequestion, few candidates made anattempt to elaborate how the relevantstatutory provisions should be applied.Candidates are expected to brieflyexplain the meaning of ‘artificial orfictitious’ as it appears in section 61;and in respect of section 61A, they areexpected to make some generalcomments on the ‘seven factors’ asthey appear in section 61A(1)(a)-(g).By reference to the legal meaning ofthe statutory provisions, this questioncould be properly handled by puttingforward possible arguments that IRDshould not invoke sections 61 and 61Aand that deduction in respect of theconsultancy fee paid to SG Ltd shouldbe allowed.

Some candidates still made someconclusions without using the factgiven in the essay to support theiranswer. For example, they concludedthat HK Ltd carried on business inHong Kong without any analysis.Many candidates were able to identifythe relevant sections of the InlandRevenue Ordinance; however theyshould have performed more in-depthanalysis of the tax issues. For example,only a few candidates identified theseven factors specified in section61A(1) and applied them to the casesituation.

Question 1(b)Candidates had little difficulty inidentifying the respective charging andexemption provisions in section 8 inmaking their answers. Many of themwere able to apply properly the legal

STU

DEN

TS’ S

ECTI

ON

Students’ Section

47MARCH 2003 THE HONG KONG ACCOUNTANT

principles to the relevant facts indeciding that the employees of HK Ltdmost likely were chargeable to salariestax under section 8(1).

More in-depth analysis of thesalaries tax issues are needed.

Paper IISection A – Case studyIt is found that the performance ofcandidates is better on some commonand traditional questions, like generalauditing, financial reporting and SSAP(question 1a, 2 and 3b). However, theydo not seem to have sufficient generalknowledge of information technologyand system considerations.

Individual questionsQuestion 1(a)Most candidates performed well inidentifying the most commonprocedures that an auditor shouldperform during the client acceptanceprocess, like assessing the inherentrisk, management integrity, and theauditor’s own independence, andcarrying out the professional clearanceprocess. However, quite a number ofcandidates had totally missed out somecommon but ‘practical’ steps, i.e.performing a company search andlegal search, and obtaining the latestfinancial statements.

Question 1(b)The question specifically requested thecandidates to set out the audit workthat would be planned for thisparticular client. However, a numberof candidates only set out the normalaudit work, which could be generallyapplied for all clients, which are notspecifically suitable for this particularclient.

Although some candidates couldsuggest relevant audit work for thosequalified areas, the work they suggestedmight not be totally tailored for thequalification. Some observations arelisted out as follows:(i) Impairment tests are commonly

suggested for property but nottrademark;

(ii) Some candidates mistakenly appliedSSAP 13 on investment in propertiesunder development.

Question 2The question covered several areas inrespect of investments from accounting,auditing and tax perspectives.Candidates generally performed well ontaxation and audit procedures oninvestments. However, some candidatesdid not perform well on investmentaccounting. They only discussed thegeneral requirements in investmentaccounting but did not address thespecific issues of the case.

Candidates are required tocomment on the proposed accountingtreatment suggested by the financialcontroller given that the companyadopted alternative treatment.Candidates should still spend time ondiscussion of alternative treatmentagainst the benchmark treatment.

Some candidates had not carefullyread the SSAP 24 and could not identifythat paragraph 33 of SSAP 24 is onlyapplicable to investment securities underbenchmark treatment but not on otherinvestments under alternative treatment.

The prohibition from reclassificationof investments under alternativetreatment is generally addressed andcandidates did not sufficientlydemonstrate their arguments.

Question 3(a)Candidates generally performed well onthis question by applying SSAP 18.

Question 3(b)Candidates performed badly on thisquestion. It also demonstratedcandidates’ weakness in the areas ofinformation technology and generalsystem requirement.

To some extent, the unsatisfactoryperformance is because of thecarelessness of the candidates. They didnot carefully read the question. Forexample, some candidates answeredfrom the financial reporting perspectiveand with the revenue issues related toquestion 3a in this question. Some

candidates discussed the issues relatingto the operation of POS, but not theimplementation of POS. Somecandidates mentioned the control onPOS but not the responsibilities ofvendor and clients on POS.

Question 3(c)Candidates also performed badly onthis question; partially, because of thefact that the candidates could notunderstand fully the functions of apoint-of-sales system. However, a point-of-sales system has been widely used inretail business. Candidates generallycould not demonstrate their commonbusiness sense. Thus, they could notsuggest the auditor’s concerns and therelated audit procedures.

Section B – EssaysThe essay questions tested candidates’ability to apply their knowledge infinancial reporting, taxation, andgeneric skills in analysing a debtrestructuring situation. These situationsare known to have occurred in therecent poor economy in Hong Kong.

Candidates’ overall performance forthis essay was fair. They did well forquestion 1(c), but did poorly for 1(a)and 1(b).

Individual questionsQuestion 1(a)In general, candidates’ analyses werenot of sufficient depth. Many candidatesperformed poorly in this part. Many ofthem did not understand the nature ofdebt reduction and the relatedaccounting treatment. They consideredreduction of debt as an extraordinaryitem. A few candidates said the amountof debt reduced would be credited tothe Balance Sheet in a Capital Reserveaccount. Some candidates did not readcarefully the question and thus theyspent too much time on reporting theaccounting treatment and disclosure inthe balance sheet though the questionsasked for the disclosure in the incomestatement. Several candidates mixedup the facts given in the essay;consequently they scored no mark

STU

DEN

TS’ S

ECTI

ON

Students’ Section

THE HONG KONG ACCOUNTANT MARCH 200348

Online examination resultsQP students who have applied for a Student Login Account may view their resultsonline within two weeks from the official result release date. For those without a loginaccount, please visit http://www.hksa.org.hk/faq/ for information on how to obtainone.

Important dates Procedures

Week commencing Candidates will each receive an Examination5 May 2003 Attendance Docket (EAD) from the Hong Kong

Examinations Authority (HKEA) containing informationsuch as the name of the examination paper,examination centre, date and time of theexamination, desk number and student registrationnumber. It also serves as a personal identificationand entry permit to the examination centre.

Students should check and notify the Society’sEducation & Training Department immediately on2287 7063 or 2287 7046 if errors are found ontheir dockets.

16 May 2003 Candidates who have not received their EADs should(9:00 – 12:00 noon) contact the Society’s Education & Training

Department on 2287 7063 or 2287 7046 during thespecified period to obtain a duplicate copy.

26 May 2003 Examinations take place:Module B 9:30 am – 12:30 pmModule D 2:00 pm – 5:00 pm

QP Examination Attendance Dockets – February 2003 session(modules B & D)

Remarks

The HKEA only administers theexaminations on behalf of theSociety, students shouldcontact the Society directlyfor all enquiries regarding theEADs.

A duplicate copy of the EADmay not be issued to studentswho do not approach theSociety by the cut-off time.

for the related analysis. For example, acandidate talked about write-off oftrade debt by the company, rather thanwaiver of the company’s liabilities.

Question 1(b)Most of the candidates were unable toidentify 15(2) as the relevant section ofthe Inland Revenue Ordinance for thispart of the question. Only a fewcandidates discussed the need to reviewsource documents and accountingrecords to determine the exact nature

of a debt for the purpose of section 15(2). Similarly, only a few candidatesdiscussed the need to review therelevant documents, e.g. deed of release,to determine exact timing of effectingthe release of debt. Many of thecandidates failed to refer to the specificinformation in their analysis, i.e. thecompany gains as the banks agreed toreduce the loan and the creditor agreedto reduce the processing fee payable asmentioned in the facts of the question.Candidates should apply the facts in

their analysis rather than giving answersfor a general situation. Some candidatessimply answered yes or no withoutgiving an explanation in details.

Question 1(c)Candidates in general performed well inthis part of the question. However, only afew candidates discussed when it wouldbe most effective for a company to have adebt restructuring and what would bethe success factors of a debtrestructuring.

STU

DEN

TS’ S

ECTI

ON

Students’ Section

49MARCH 2003 THE HONG KONG ACCOUNTANT

Qualify as a Professional Accountantthrough the HKSA Qualification Programme

June 2003 CohortApplication Closing Date : 2 May 2003

Why encourage your colleagues and friends to choosethe Qualification Programme?• This programme is the ONLY professional qualification

programme offered by the Hong Kong Society of Accountants(HKSA), the statutory licensing body of professional accountantsin Hong Kong.

• It also offers the shortest route to qualify as a CPA, with nofurther examinations required.

• HKSA members who qualify through the Qualification Programmecan apply for membership of CPA Australia and/or ACCA*.

What is the Qualification Programme?The Professional Qualification Programme prepared and monitoredby the HKSA is specifically tailored to Hong Kong’s businessenvironment. It is synonymous with quality - a choice for studentswho seek to stand out from their peers. When finding a regular job istough, doors automatically open for those with a professionalqualification.

This Qualification Programme is not about just passing anotherset of exams. Rather than memorising text books and cramming, itbreaks the traditional mould by exposing students to simulatedbusiness situations. It encourages you to think independently. Atworkshops you will be given professional problems needing effectivesolutions. Of course, there are exams to pass. But much emphasisis placed on demonstrating your ability to make professionaldecisions, contribute through teamwork and be interactive whenworking as a group.

The Qualification Programme places strong emphasis on thepractical application of business, accounting, taxation, auditing andIT skills. This is not just another academic course. Through the mostup-to-date training methods, it prepares you for a career as a highlycompetent and ‘Forward Thinking Accountant’. It paves the wayfor a future in business.

The Qualification Programme’s comprehensive and professionaltraining curriculum is the key to the pursuit of excellence.

Programme StructureThe HKSA Qualification Programme comprises the ProfessionalProgramme and the Final Professional Examination.

Professional ProgrammeThe objective of the Professional Programme is to providecandidates with the opportunity, through the different modules ofthe programme and under the guidance of workshop facilitators, todevelop the necessary application skills and competencies, whichare essential for a professional accountant.

Professional Programme comprises four modules :Module A Financial ReportingModule B Financial ManagementModule C Auditing and Information ManagementModule D Taxation

Requirements for each module :• self-study for 15 weeks using study materials provided by the

HKSA• complete four workshops (approximately three hours each) led

by experienced practitioners• pass a two-hour open-book examination

Final Professional ExaminationAfter successful completion of the Professional Programmecandidates are eligible to take:• a six-hour open-book Final Professional Examination (to be

taken in two sessions of three hours each).

The Final Professional Examination will test the ability of candidatesto deal competently with professional type situations, involving theapplication of knowledge and skills from the ProfessionalProgramme Module Syllabus, across all areas of competencyappropriate to a competent practitioner.

To: HKSA Attn: Miss Juana Chan(Fax No. 2147 3293)

Name:

Telephone:

E-mail:

Highest educational qualification attained:

Website : www.hksa.org.hk/students Enquiries : 2287 7040/068Address : 4th Floor, Tower Two, Lippo Centre, 89 Queensway, Hong Kong

Need advice about enrolment? Attend our Information Sessions at the Society’scentrally located office. A brief introduction of the Qualification Programme will begiven at each session. More importantly, the session will provide opportunity forprospective students to obtain advice regarding admission to the QualificationProgramme and requirements for registration as a student of the Society.

To ensure individual attention is received, each information session accommodates amaximum of 20 prospective students. Bookings are made on a first-come-first-served basis.

* Other membership admission requirements will apply.

STU

DEN

TS’ S

ECTI

ON

Students’ Section

THE HONG KONG ACCOUNTANT MARCH 200350

Transitional Examinations (TE) December 2002 session resultsThe Society is pleased to announce the latest results of the Transitional Examinations (TE).

The results of each of the four papers are as follows:

Paper Examination pass rates

Paper I (Auditing and Information Management) 26%

Paper II (Financial Management) 31%

Paper III (Management Accounting) 33%

Paper IV (Taxation and Tax Planning) 25%

TE examiner’s report Paper I – Auditingand Information Management (December2002 session)

Overall CommentsThe poor results could be attributedto the lack of examination techniqueand poor time management of thecandidates. In general, the candidateswere careless in reading the facts ofthe questions. They were also weak ininterpreting the requirement of thequestions. They did not answerstrictly in accordance with therequirement. In addition, somecandidates failed to answer therequired number of questions, leavingone or even two questions totallyunattempted and thus no marks couldbe awarded.

Specific CommentsQuestion 1Most candidates failed to interpret therequirement of the question precisely.

They did not read carefully the whole‘required’ part of the question first.They were unable to distinguish theaudit procedures to be performedduring the physical inventory countand those to be performed after thecount. Some of the candidates alsomixed up audit procedures withclient’s internal controls. Overall thecandidates performed poorly in thisquestion.

Question 2Many candidates did not read the factsof the question carefully. They wereonly able to identify up to half of theweaknesses embedded in the question.Some of them were unable to suggestthe possible consequences and givemeaningful recommendations even ifthey could locate the weaknesses.

Question 3Most candidates did not read the factsand the requirement of the questioncarefully. They were unable todistinguish the difference betweencontrols, tests of control and substantiveprocedures. They also failed to see thelink between different parts of therequirement. They did not base theiranswers on the information given in thequestion and answer strictly inaccordance with the requirement.

Question 4This question was straight forwardbut the performance was not satisfactory.Although most candidates were able toidentify some risks facing the hospital,none of them were able to state clearlywhat business risk is. Some of thecandidates were also unable to defineaudit risk and its components. Mostcandidates lost marks in part (e) as theyfailed to suggest audit proceduresspecific to the hospital’s sales andcollection cycle. Some of them also didnot state the objectives of the auditprocedures as required by the question.

The Society is pleased to announce that 25 TE students successfully completed the Transitional Examinations in the December2002 Session. The graduates are listed below.

TE graduates – December 2002

Chan, Cheuk Wah

Chan, Mei Yuk

Chan, Lau Mei

Chiu, Suk Fun

Fung, Wai Man

Hui, Wai Ching

Hung, Cheung For

Kan, Wing Chi

Kwok, Po Yung

Kwok, Chun Lung

Lai, York Po, Alfred

Lam, Shui Ying, Anny

Leung, Kwok Keung

Leung, Kin Wa

Leung, Ho Lam

Leung, Kam Fai

Li, Chin Shan

Lui, Yuen Sze

Mak, Yuk Lin

Ng, Kin Lok, Eric

Pang, Kin Shing

Pun, Wing Cheung, Andy

So, Kin Wah

Wong, Ying Kiu

Yau, Nga Lai

STU

DEN

TS’ S

ECTI

ON

Students’ Section

THE HONG KONG ACCOUNTANT MARCH 200352

TE examiner’s report Paper II – FinancialManagement (December 2002 session)

Overall CommentsIn general, candidates’ overall examperformance is quite satisfactory.Compared to the June 2002 diet,candidates were much better preparedfor the exam.

Specific CommentsSection A: Compulsory questionsQuestion 1This question is related to the variouscapital budgeting techniques such as thepay-back, NPV, and IRR. Mostcandidates were generallyknowledgeable about thesefundamental concepts. However, somehad difficulties in calculating theinternal rate of return for a relativelystraightforward investment project. Inaddition, many candidates did notunderstand problems associated withthe pay-back method or the IRRmethod, especially when two investmentprojects are mutually exclusive.

Question 2This question tested candidates’ abilityto employ discounted dividend modelsto assess the fair market value of astock. Most candidates performed well

with the constant-growth model. Only afew candidates could apply the two-stage differential growth model in thecontext of stock valuation. Manycandidates also failed to demonstratethe sensitivity of the fair market price tosmall changes in either the dividendgrowth rate or the discount rate.

Question 3In attempting this question, about halfof the candidates demonstrated a fairunderstanding of risk and return, andthe Capital Asset Pricing Model(CAPM), while the other half showedlittle grasp of these important concepts.Most candidates did not fullyunderstand the meaning of the CAPM,especially in determining if a security ismispriced relative to its risk level asmeasured by beta.

Section B: A choice of two out ofthreeQuestion 4Most candidates attempted thisquestion, which was concerned withinitial public offerings (IPOs), IPOunderpricing, and long-term debt anddebt covenants. In general, they did

well in discussing advantages anddisadvantages of going public. Somecandidates could not clearly explainIPO underpricing and its causes. Mostcandidates showed little understandingof debt covenants.

Question 5Again, most candidates attempted thisquestion, which tested theirunderstanding of the Modigliani-Miller(MM) propositions with regards to capitalstructure. Many candidates seemed tounderstand the consequences of the useof debt on firm value, cost of equity, andweighted average cost of capital in theMM world without any taxes. However, indiscussing the various costs associatedwith the use of debt, most candidates didnot distinguish the agency costof (outside) equity from the agency costof debt.

Question 6The concept of Efficient MarketHypothesis (EMH) was tested in thisquestion. Only a few candidatesattempted this question, with verylimited success. In general, they coulddefine the EMH and identify its threeforms. They had difficulties inapplying the EMH concept and indescribing empirical evidenceuncovered so far as is consistent withthe weak-form and/or semi-strongform market efficiency.

Question 5This question was poorly performed.Most candidates were not aware of theprocedures to be performed duringchange of auditors and clientacceptance. They also failed to

understand the rationale behind thoseprocedures.

Question 6Only one third of the candidatesattempted this question. In general

this question was badly performed.Most candidates clearly did not knowhow to apply the generalised auditsoftware and the audit tests that couldbe conducted using the generalisedaudit programme.

TE examiner’s report Paper III –Management Accounting (December 2002session)

Overall CommentsOverall, candidates’ performance waspoor in the examination. Candidates

demonstrated satisfactory timemanagement in the examination sincethey tried very hard and finished most

of the questions. The commonweakness of the candidates was theydid not read the questions andrequirements carefully enough toproduce good answers. They tended toput down memorised facts that werenot relevant to the questions. Somecandidates were not well prepared forthe examination. In general,candidates performed better in

STU

DEN

TS’ S

ECTI

ON

Students’ Section

53MARCH 2003 THE HONG KONG ACCOUNTANT

TE examiner’s report Paper IV – Taxationand Tax Planning (December 2002 session)

Overall CommentsCandidates did well in the first twoquestions on salaries tax and profits taxcomputation, but the performance forthe other questions was not satisfactory.However, it is good to note thatcandidates did not avoid answering anyparticular optional question in Section

B. Each question in Section B wasattempted by more or less the samenumber of candidates. Candidatesshould put more effort intounderstanding the tax laws and on howto apply them in answering essay typequestions in the examination.

The result of this paper showed

that candidates had a betterknowledge of the preparation ofsalaries tax and profits taxcomputation while the knowledge oftax administration, stamp duty andestate duty was very poor. Usually thegood performance of questions 1 and2 on salaries tax and profits taxcomputation helps many candidatesto get a pass for the overall paper. Ifcandidates did not perform well onthese two questions, they would likelyfail in the examination.

handling straight forward calculationsthan analytical essay-type questions.The application of knowledge andconcepts in practical situations wasweak.

Specific commentsSection A – Compulsory questionsThe overall performance in Section Awas poorer than that in Section B. Thequestions required interpretation andanalytical skills to understand andorganise diverse information. Allquestions were related to coremanagement accounting concepts andapplications. The candidates wereweak in presentation skills in writingboth qualitative answers andcalculations suitable for reading bymanagement. In general, theirperformance demonstrated that theydid not fully understand the questionsand/or requirements in eachquestion.

Question 1The general performance was weak.While most candidates had no problemin answering parts (a) and (b) onperformance evaluation, they lost markson parts (c) and (d). Most candidatestried to discuss ‘what’ non-financialmeasures instead of ‘why’. Somecandidates were able to integrate the‘what’ and ‘why’ together and creditswere therefore given. It meant that pure‘what’ was inadequate. In addition,candidates had difficulties in identifyingthe characteristics of good performancemeasures in part (d).

Question 2The general performance was poor.Part (a) of the question relates to theanalysis of relevant costs to determinewhether a project should proceed. Theperformance indicated that they hardlyidentified relevant and irrelevant costsin making the right decision. Somemight have misunderstood theinformation in the question due to poorlanguage skills. In part (b), it indicatedthat candidates were unable to write inclear and simple English to define andexplain the basic terms.

Question 3The general performance was fair. Themajor weaknesses were identified inparts (a) and (d) where conceptualunderstanding of cost-based andnegotiated transfer prices with qualitativeanswers were required. For thequantitative parts of (b) and (c), mostcandidates performed well as it involvedhard calculations instead of soft analysis.

Section B – A Choice of two out ofthree questionsThe overall performance in Section Bwas generally better than that in SectionA. However, as common in similarpublic examinations, candidatesperformed better in quantitative ratherthan qualitative questions. Very fewcandidates chose to attempt question 6,which is a pure essay-type question onactivity-based costing (ABC).

Question 4The general performance was fair.

Candidates did well in part (a) whichinvolved the calculation of standardcosts. For part (b), most candidatesmisread the question and justexplained the roles of the threedifferent people ‘in general’ instead oftheir ‘specific roles’ in developingstandards. Some candidates were notwell prepared as they were unable toexplain the ideal and attainablestandards clearly in part (c) since theseare basic understandings in thestandard costing topic.

Question 5The general performance was good.Most candidates scored above averagemarks in this question, which related tothe optimal allocation of constrainedresource among multiple productsdemanding the same resource. Theperformance indicated that candidatesworked well with typical straightforward calculation questions.

Question 6The general performance was verypoor. Only a small proportion ofcandidates chose to answer thisquestion, which required acomprehensive understanding anddiscussion of the ABC system. Theperformance indicates that candidateswere not well prepared for thisincreasingly important topic in thesubject. They also had difficultiesorganising the relevant points and ideasin their answers for each of the issuesraised by the production director in thequestion.

STU

DEN

TS’ S

ECTI

ON

Students’ Section

THE HONG KONG ACCOUNTANT MARCH 200354

In order to further improveperformance in the examination oftaxation, candidates should pay moreattention to tax compliance, stamp dutyand estate duty. All these three areas oftax law are very important and practical.Questions on these areas of law willappear frequently in examinationpapers.

Specific commentsSection A – Compulsory questionsQuestion 1This question required candidates toprepare a salaries tax computation, aproperty tax computation, a personalassessment tax computation, and designa remuneration package. Mostcandidates got very high marks for thisquestion. The result showed thatcandidates prepared well for this type ofquestion.

Nevertheless, I would like to drawcandidates’ special attention to thefollowing items:• ground rent and interest expenses

are not deductible under propertytax;

• do not mix up interest paid for anincome-producing property withinterest paid on a home loan; and

• not familiar with how to preparepersonal assessment taxcomputation (the income put in thepersonal assessment taxcomputation are net assessablevalue, net assessable income andassessable profit, it is wrong torepeat every item in the propertytax computation and salaries taxcomputation in the personalassessment tax computation)

Question 2This question required candidates toprepare a profits tax computation for apartnership business, and prepare apersonal assessment allocation forpartners. Many candidates got a goodpass for this question although they didnot know how to calculate the personalassessment allocation.

However, the following points wereoverlooked by many candidates:

• rent paid to partners is deductibleagainst the assessable profits of apartnership business;

• contribution to the mandatoryprovident fund paid for partners isdeductible against the assessableprofits of a partnership business;

• not knowing how to handlerefurbishment; and

• treatment of prescribed fixed assets

Question 3This is a common question in taxationexaminations, but very few candidatesgot a pass mark for this question. Thisquestion is divided into two differentparts. Part (a) required candidates tostate the six badges of trade, and part(b) required candidates to apply theknowledge in part (a) to a scenariogiven.

Part (a) was made up of 15 marks,and candidates were expected to use 27minutes to answer this part. Merelyputting down the names of the sixbadges of trade was not sufficient toearn a pass mark. Brief explanation oneach badge was required. Part (b)required candidates to apply the law toa problem, but many candidates werenot able to handle such a question.

Section B – A choice of two out ofthree questionsQuestion 4This question is divided into two parts.Part (a) asked candidates’ estate dutyknowledge, but the overall result wasvery poor. It was found that candidateshad little knowledge of estate duty. Part(b) asked candidates to distinguishadditional assessment under section 60(1) and additional tax assessment undersection 82A. Very few candidates wereable to understand their differences.The performance of this question wasthe poorest, and no candidates got apass mark for it. It showed that mostcandidates did not care about taxadministration.

Question 5This question is divided into four parts.Part (a) was on the source of profit and

other parts were on stamp duty. Thepurpose of breaking the question intosmall parts was to help candidates tohave a better understanding of therequirements of each part of thetaxation knowledge being asked.

Part (a) asked candidates how todetermine the source of profitderived from the sale and purchase ofcommodities under profits tax. As onlysix marks were allocated to that part, abrief and direct answer to the questionwould be sufficient. It was not requiredto state the three conditions ofsection 14 on the charge of profits tax.Some candidates wasted time on that.That part also required candidates tomention how to apply the decisionmade in the Magna case besides thecontract effected test, but very fewcandidates touched on theMagna case.

Parts (b), (c) and (d) askedcandidates how to stamp a sale andpurchase of Hong Kong, immovableproperty and Hong Kong stock, and alease of Hong Kong immovableproperty. Those were the basicconcepts of stamp duty, but very fewcandidates got a pass mark for thoseparts. This reflected that mostcandidates did not prepare well forstamp duty questions.

Question 6A scenario was provided in thisquestion, and candidates were requiredto have the taxation knowledgeinvolved in the deduction of revenueor capital payments under profits tax,and apply it to the scenario given. Inaddition, candidates were requiredto write an objection letter tothe Commissioner of InlandRevenue.

Although the performance of thisquestion was not as good as questionsone and two in Section A, yet this wasthe one which most candidates wereable to get a higher score than inquestions four and five in Section B.Most candidates got a pass mark for thisquestion.

STU

DEN

TS’ S

ECTI

ON

Students’ Section

55MARCH 2003 THE HONG KONG ACCOUNTANT

The Transitional Examinations (TE)are offered to former JointExamination Scheme (JES) studentswho have passed or are exempted fromnine or less JES papers. The TE havebeen specially designed for such JESstudents, as an alternate route to meetQP admission requirements.

The TE will be offered for threeyears in 2002, 2003 and 2004. Twosessions will be held each year, namelyin June and December. The fourpapers of the TE are:• Auditing and Information

Management• Financial Management• Management Accounting• Taxation and Tax Planning

Rules• To be eligible to sit the TE, the

former JES students must haveeither sat and passed a minimum oftwo JES papers or be exemptedfrom or passed at least 6 papers.Application for exemptions, i.e. tosatisfy the 6-paper benchmark canbe made after the cessation of theJES, but within the duration of theTE, similar to JES exemptionpolicy, procedure and deadlines.

• Under the JES, the two papers (M1& M2) passed under the MatureStudent Entry Route (MSER) arecounted as ‘Exemption’ fromPapers 1 & 3 and not as ‘Pass’.

• A maximum of four papers can betaken at any diet.

Transitional Examinations

• Papers can be taken in any order.• A person can only apply for TE if

he/she is a registered student of theSociety and has paid his/hercurrent annual subscription fee andthe required fee for the TE.

• Exemptions of up to three papersmay be granted by application fromthose who have completed seven tonine papers under the JES.

• Examinations must be completed bythe December 2004 diet.

Important dates• The closing date for exemption

applications for the June 2003session is 31 March 2003

• The deadline for entry to the June2003 session is 15 April 2003

June 2003 session examination timetable

Paper I (Auditing & Information Management) Thursday 12 June 2003 2:00 pm – 5:00 pm

Paper II (Financial Management) Friday 13 June 2003 2:00 pm – 5:00 pm

Paper III (Management Accounting) Monday 16 June 2003 2:00 pm – 5:00 pm

Paper IV (Taxation and Tax Planning) Tuesday 17 June 2003 2:00 pm – 5:00 pm

TE exemption policy table

Transitional Examination Papers Paper passed/exempted under JES

Auditing and Information Management Paper 5 (Information Analysis) +Paper 6H (Audit Framework) orPaper 10H (Accounting and Audit Practice)

Financial Management Paper 3 (Management Information) +Paper 8 (Managerial Finance) orPaper 14 (Financial Strategy)

Management Accounting Paper 9 (Information for Control and DecisionMaking) +Paper 12 (Management and Strategy)

Taxation and Tax Planning Paper 7H (Tax Framework - HK) orPaper 11H (Tax Planning - HK)

Fees• Exemption/Examination Fee: $400

per paper

Application and syllabusApplication forms for enrolment andexemption claim, as well as detailedsyllabuses and recommended readinglists for each of the TransitionalExamination papers can be obtainedvia the following means:• www.hksa.org.hk/students/• the Society’s counter• by fax: 2528 9000

STU

DEN

TS’ S

ECTI

ON

Students’ Section

THE HONG KONG ACCOUNTANT MARCH 200356

Price List for QP Q&A booklets

Module A Module B Module C Module D Final ProfessionalFinancial Financial Auditing & Information Taxation Examination

Reporting Management Management

Pilot Paper $45 $45 $45 $45 $45

September 1999 session $45 – $45 – –

March 2000 session – $45 – $45 –

September 2000 session $45 – $45 – –

December 2000 session – – – – $45

March 2001 session – $45 – $45 –

June 2001 session $45 – $45 – $45

October 2001 session – $45 – $45 –

December 2001 session – – – – $45

March 2002 session $45 – $45 –

June 2002 session – – – – $45

June 2002 session* $45 $45

* New release

Q&A bookletsNew releases of the Question and Answer (Q&A) booklets are as follows:

Qualification ProgrammeModule B (June 2002 session)Module D (June 2002 session)

Practising CertificateOctober 2002 Diet PC papers (including PC-Law and PC-Tax Planning) cost HK$45 each.

Q&A booklets for all recent diets are also available at the Society’s library.Friends or relatives may purchase pilot papers and booklets on the students’ behalf by presenting either the student’s StudentRegistration Card or a copy of the card.

ObjectiveThis 21-hour revision course, to be offeredby the Hong Kong Baptist University(HKBU), is targeted for those QPcandidates intending to sit for the June2003 FPE. The objective of the course is toassist QP candidates to better prepare forthe FPE. The focus will be placed onimproving candidates’ analytical skills/techniques in handling the FPE questions,

Revision course for QP candidates takingthe June 2003 Final ProfessionalExamination (FPE)

rather than go through the subjectmatters of the FPE syllabus in detail.However, the course includes a briefupdate of knowledge in financialreporting, financial management,auditing and information managementand taxation. Lectures of the course willalso provide comments to participantson their performance on an optionalmode examination.

Course StructureTopics to be covered are as follows:• Case analysis techniques with an

emphasis on how to handle the FPEquestions

• How to handle case questions offinancial reporting and a briefupdate of the knowledge infinancial reporting (Module A)

• How to handle case questions ofauditing and informationmanagement and a brief update ofknowledge in auditing andinformation management(Module C)

• How to handle case questions oftaxation and a brief update of

STU

DEN

TS’ S

ECTI

ON

Students’ Section

57MARCH 2003 THE HONG KONG ACCOUNTANT

Code 205 – Workshop on practical profits tax computation for partnership businesses

Objective:To enable participants to understand how to prepare profit taxcomputation and complete profits tax return for the year ofassessment 2002/03.

Target participants:Commercial accountants, auditors and tax professionals with atleast two years’ relevant experience.

Contents:• New profits tax treatments and requirements for the year of

assessment 2002/03• How to complete 2002/03 profit tax return with special

emphasis on partnership businesses• Easily overlooked items in the preparation of profits tax

return and computation• How to prepare personal assessment allocation for

Practical training functions

knowledge in taxation (Module D)• How to handle case questions of

financial management and abrief update of knowledge infinancial management (financialmanagement field of Module B)

VenueThe Wing Lung Bank Building forBusiness Studies, Hong Kong BaptistUniversity (Shaw Campus), 34 RenfrewRoad, Kowloon Tong.

Course fee: HK$1,750

Enrolment quota: 40

Notes to applicants:1. Application form has been sent to

QP candidates eligible for the June2003 FPE. Duly completedapplication form, together with acheque for HK$1,750 payable to‘Hong Kong Society of Accountants’(with your full name and studentregistration number written on theback of the cheque), must reach theSociety’s Education & TrainingDepartment by post on or before 11April 2003.

2. Applicants accepted for the coursewill receive a confirmation slip before

23 April 2003 whilst those who areunsuccessful will receive a rejection slipand their returned cheque. Studentsmust bring the confirmation slip whenattending the classes.

3. Applicants who have not receivednotification of enrolment by 25 April2003 should call the Society’sEducation & Training Department(2287 7063 or 2287 7046).

4. The Society reserves the right to changethe venue and lecturers of the course ifdeemed necessary. The course fee willbe refunded to the applicant in case thecourse is full or cancelled.

Schedule of Lectures

Session Date & Time Topic Lecturer

1 9:30am – 12:30pm Case analysis techniques Dr Lau Tze Yiu, Peter4 May 2003 FPE marker since Dec 2001;

QP workshop facilitator since Sept 2000

2 2:00pm – 6:00pm Taxation Mr Ho Hoi Ki, Daniel4 May 2003 QP workshop facilitator since Mar 2000

3 9:30am – 12:30pm Financial Reporting Mr Lam Chi Yuen, Nelson11 May 2003 FPE marker since Dec 2001;

QP workshop facilitator since Sept 2000

4 2:00pm – 6:00pm Auditing & Information Dr Lau Tze Yiu, Peter11 May 2003 Management FPE marker since Dec 2001;

QP workshop facilitator since Sept 2000

5 9:30am – 12:30pm Financial Reporting Mr Lam Chi Yuen, Nelson18 May 2003 FPE marker since Dec 2001;

QP workshop facilitator since Sept 2000

6 2:00pm – 6:00pm Financial Management Dr Lau Tze Yiu, Peter18 May 2003 FPE marker since Dec 2001;

QP workshop facilitator since Sept 2000

STU

DEN

TS’ S

ECTI

ON

Students’ Section

THE HONG KONG ACCOUNTANT MARCH 200358

Fee concessions for group enrolmentTo promote enrolment in practical training functions, a 10 per cent discount for groups of two or more people will be offered. This discountis only applicable to students enrolling in the same programme. Each student should submit separate application forms and cheques;however, the forms should be submitted together. Students are also required to indicate on the application form the name(s) of theperson(s) they are enrolling with to qualify for the discount. Applicants will not be entitled to the group discount if forms are submittedseparately.

Code 205 – Workshop on practical profits tax computation for partnership businesses (cont)

partnership business• How to handle loss of a proprietor, partnership and

corporation• How an assessor would examine a taxpayer’s profits tax

return

Training method:Lecture, instructor-led discussion and attendees’ activeparticipation. Simulated tax cases will be used.

Enrolment quota: 70

Medium of instruction:Cantonese supplemented with English

Speaker:Mr. Patrick Ho, tax training director, Deloitte Touche Tohmatsu

Date & time: 6:30 pm – 9:30 pm,Monday, 5 May 2003

Venue: General Purpose Hall (Basement),Methodist House, 36 Hennessy Road,Wanchai, Hong Kong.

Enrolment fee:HK$220 – 10 per cent discount (i.e. HK$198 per student) forgroup enrolment of two or more students. For details, pleaserefer to the ‘Fee Concession for Group Enrolment’ below.

Application deadline: 23 April 2003