handout 4q - philippine individual income tax return sample problems

TRANSCRIPT

San Beda College AlabangAlabang Hills VillageAlabang, Muntinlupa CityIntegrated Basic Education (High School) That In All Things, God May Be Glorified

Social Studies IV Handout – Individual Income Tax Return Sample Problems

Name: Date: Section: Teacher:

Problem 1

Mrs. Jolie Sy is employed as a sales manager. Her husband is unemployed for three years now. They have four children; the eldest is 25 years old, the second is 20 years old, the third is 18 years old and the youngest is 15 years old. Compute for the annual income tax return for the taxable year 2011 given the following additional information:

Monthly salary 18,000Monthly allowance 3,000Annual Commission 120,000Withholding Tax 60,000

Solution:

Amount Explanation/Calculation

I. Gross Compensation Income 372,000(monthly salary x 12 months) + (monthly allowance x 12 months) + annual commission

II. Less: Personal Exemption Additional Exemptions

50,00075,000

Compensation for Married Individuals3 dependents x 25,000 per dependent

III. Total Exemptions 125,000 Total of Section II

IV. Taxable Income 247,000 Section I – Section III

V. Tax Due 49,250Over 140,000 but not over 250,00022,500 + 25% of excess over 140,000

VI. Less: Tax Withheld 60,000 Given in the problem

VII. Tax Payable/Tax Refundable (10,750)Section V – Section VITAX REFUND

Tax Due Calculation:

Taxable Income 247,000 Over 140,000 but not over 250,00022,500 + 25% of excess over 140,000

Tax Due = 22,500 + (247,000 – 140,000) x 0.25= 22,500 + 26,750= 49,250

Problem 2

Mr. Herrera is unmarried with two legal dependents. The following information is used to determine his income tax. Compute for his annual income tax return for the year 2011:

Monthly salary 20,000Monthly overtime pay 1,500Monthly gas and food allowance 3,500Withholding Tax 35,000

Solution:

Amount Explanation/Calculation

I. Gross Compensation Income 300,000(monthly salary x 12 months) + (monthly allowance x 12 months) + (monthly overtime pay x 12 months)

II. Less: Personal Exemption Additional Exemptions

50,00050,000

Compensation for Head of the Family2 dependents x 25,000 per dependent

III. Total Exemptions 100,000 Total of Section II

IV. Taxable Income 200,000 Section I – Section III

V. Tax Due 37,500Over 140,000 but not over 250,00022,500 + 25% of excess over 140,000

VI. Less: Tax Withheld 35,000 Given in the problem

VII. Tax Payable/Tax Refundable 2,500Section V – Section VITAX PAYABLE

Tax Due Calculation:

Taxable Income 200,000 Over 140,000 but not over 250,00022,500 + 25% of excess over 140,000

Tax Due = 22,500 + (200,000 – 140,000) x 0.25= 22,500 + 15,000= 37,500

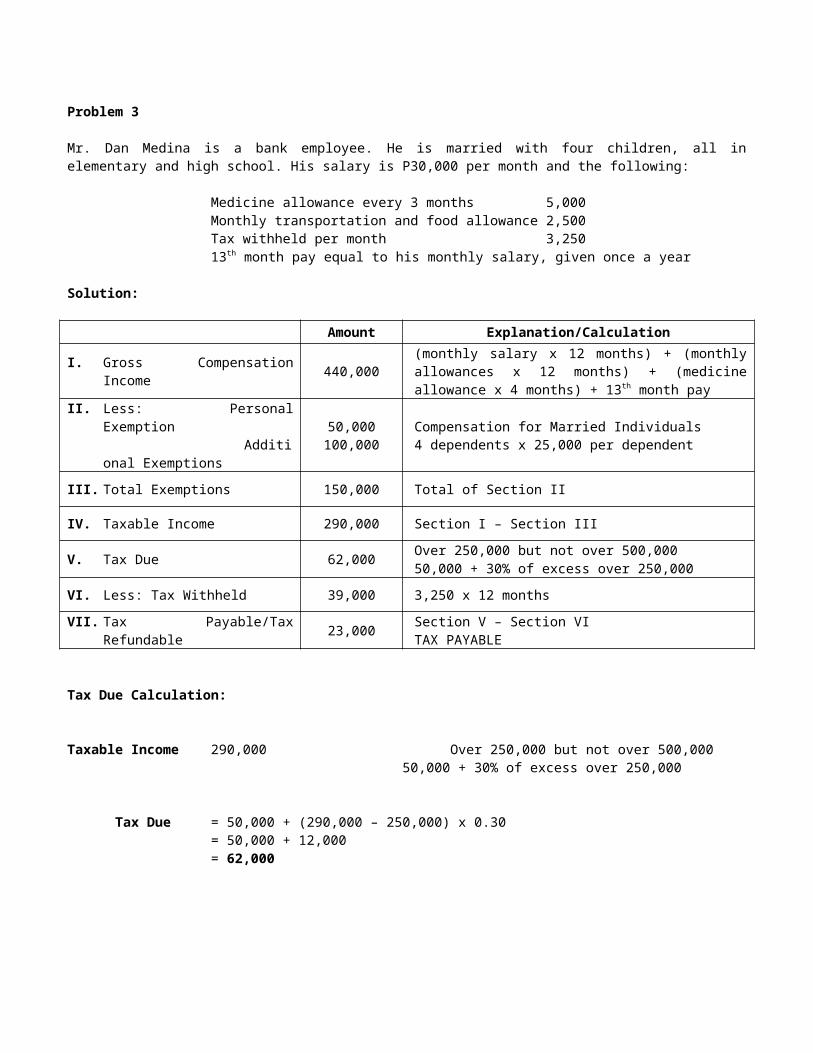

Problem 3

Mr. Dan Medina is a bank employee. He is married with four children, all in elementary and high school. His salary is P30,000 per month and the following:

Medicine allowance every 3 months 5,000Monthly transportation and food allowance 2,500Tax withheld per month 3,25013th month pay equal to his monthly salary, given once a year

Solution:

Amount Explanation/Calculation

I. Gross Compensation Income 440,000(monthly salary x 12 months) + (monthly allowances x 12 months) + (medicine allowance x 4 months) + 13th month pay

II. Less: Personal Exemption Additional Exemptions

50,000100,000

Compensation for Married Individuals4 dependents x 25,000 per dependent

III. Total Exemptions 150,000 Total of Section II

IV. Taxable Income 290,000 Section I – Section III

V. Tax Due 62,000Over 250,000 but not over 500,00050,000 + 30% of excess over 250,000

VI. Less: Tax Withheld 39,000 3,250 x 12 months

VII. Tax Payable/Tax Refundable 23,000Section V – Section VITAX PAYABLE

Tax Due Calculation:

Taxable Income 290,000 Over 250,000 but not over 500,00050,000 + 30% of excess over 250,000

Tax Due = 50,000 + (290,000 – 250,000) x 0.30= 50,000 + 12,000= 62,000