harnessing global growth - supply chain...

TRANSCRIPT

© 2008 Rolls-Royce plcThe information in this document is the property of Rolls-Royce plc and may not be copied or communicated to a third party, or used for any purpose other than that for which it is supplied without the express written consent of Rolls-Royce plc.This information is given in good faith based upon the latest information available to Rolls-Royce plc, no warranty or representation is given concerning such information, which must not be taken as establishing any contractual or other commitment binding upon Rolls-Royce plc or any of its subsidiary orassociated companies.

Harnessing Global Growth

Addressing four global markets

A global 20 year market opportunity for products and services worth around US$2 trillion

DefenceAerospace(US$480 billion)

Energy

(US$120 billion)

Marine

(US$350 billion)

Civil Aerospace(US$1,250 billion)

Investing in technology and capability and infrastructure£11 billion over 10 years

£0.88bn£0.93bn

£1.05bn

£1.30bn

£1.45bn

2003 2004 2005 2006 2007

Gross R&D11% of turnover in 2007

A Global Company

Turnover

R&T

Employees

New Programmes

70%

30%85%

15%

100%

100%

93% 60%

50%50%

40%

1987 2007

UK Rest of World

68%

32%

Rolls-Royce is privatised

Bergen Diesels

F136 for JSF

AE 2100

LiftFan for JJF

Trent 500

AE 3007

TP400

Trent 900

MT30

Tay 611C Trent 1000

AE 1107C

Trent XWB

RB282

RR300

1987

2007

Broadening our portfolio

Trent 700

Trent 800

BR710

Industrial Trent

BR715

1998 2007 1998 2007 1998 2007

£5.0bn

£12.7bn

£4.7bn

£12.9bn

£2.9bn

£20.3bn

Americas Asia and Middle EastEurope

Growing our market share and installed base globally

12% Compound

growth

Americas

11%Compound

growth

Europe

24%Compound

growth

Asia and Middle East

Compound growth of order book 15% and increased global reach

CHENGDU●

●●●

●XIAMEN

GUANGZHOUKUNMING

ACI: 13 x Boeing 757

CYH: 3 x Boeing 767

CSN: 20 x Boeing 757

CXA: 5 x Boeing 757

Improved Market Access- Rolls-Royce Powered Aircraft in China - 1997

Total: 41 Aircraft

● URUMQI

CHENGDU●

BEIJING●

●●

●●●

●SHANGHAI

NANJING

XIAMEN

GUANGZHOU

KUNMING

WUHAN

CXJ: 13 x Boeing 757

CAA: 13 x Boeing 757

CYH: 3 x Boeing 767 –

CSN: 16 x Boeing 757CSN: 24 x A330 CSN: 6 x Emb 145

CXA: 9 x Boeing 757

CKK: 2 x Tu204

CES: 10 x Emb 145

CKK: 3 x Tu204CAA: 14 x A330

CES: 5 X A340-600

CSN: 5 x A380

CSC: 5 x Emb 145

CHH: 7 x A330

CES: 20 x A330

●XIAN

TIANJIN ●CHH: 50 x Emb 145

CAA: 15 x Boeing 787

Total: 504 Aircraft

CAA: 6 x A330

CAA: 13 x A320

CSN: 127 x A320

CSC: 40 x A320

CSN: 13 x MD90

CES: 9 x MD90

Rolls-Royce Powered Aircraft in China - 2010

CHH(HK): 20 x A330

CHH: 3 X A340-600

●CHONGQING

CGQ: 3 x A320

CES: 30 x A320

CHH: 20 x A319

Balanced business portfolio

Civil: 19%Marine: 13%

Defence: 10%

Energy: 3%

Aftermarket services: 55%(£4.3 bn)

Original equipment: 45%(£3.5bn)

Total sales: £7.8bn

0

0

10

20

30

40

50

2002 2003 2004 2005 2006 2007Europe Americas Asia and Middle East

A global order book*- More than doubled in less than 3 years

£bn

*Firm and announced

Orders totaling £6bn announced in 2008 to date

Meeting the challenges

Delivering on our customer commitments

− Demands improved performance

Leadership collaboration for environmental solutions

External headwinds pressure

− Material costs and USD

Volatile market and new levels of competition

Powering

a better world

Environmental report 2007

Facilities & Services Management

REVISED 22-02-08

TRAINING AREA750m 2

ATC OFFICE505 m 2

STREETAREA

OPEN PLANDINE AREA550 m 2

ATC MANUFACTURING

AND LABORATORIES

1000 m 2

ENERGYSTOREQUIET rm

FUEL STORE 500m2

FUEL PUMPS

STACK HORIZONTAL

FAN CASE

DESPATCH

FAN

05 MODULE

03 MODULE

MACHINE SHOP

04 MODULE

O2 MODULE FOOT PRINT

O8 MODULE FOOT PRINT

COMPLETED ENGINE STORE &

GSE

TEST BED No.1

TEST BED No.2

GANGWAY

GANGWAY

GANGWAY

GANGWAY

B EVERAGE AREA

GRO UN D FLOOR 25m2

TECHNICAL LIBRARY &

CERT. OFFICE

BEVERAGE AR EA

G RO UN D FLOOR 25m2

CONTROL ROOM

SHO

P FL

OO

R SU

PPO

RT

OFF

ICE

- GRO

UND

FLO

OR

(98

SEA

TS)

TR AININ G AREA75 0 m2

A T C OF F ICE50 5 m2

S T RE E TA RE A

O P E N P L A N

DI NE A RE A5 50 m 2

A T C M A NUF A CT URING

A ND L A B ORA T ORIE S

1 0 0 0 m 2

E NE R GYS TO REQU IE T r mFUEL STORE 500m2

FUEL PUMPS

SHO

P FL

OO

R S

UPPO

RT O

FFIC

E - F

IRST

FLO

OR

(98

SEA

TS)

BEVERAGE AR EA

GR OU ND FLOO R 25m 2

BEV

ERAG

E AR

EAGR

OUN

D FL

OOR

25m

2

SECURE DOCUMENT STORAGE

BAS

EMEN

T

Globalisation- Facilities of the future

Commonwealth of Virginia and Singapore assembly facilities –enabling future growth and “dollarisation”

Seletar Park,

Singapore (concept)

Ground Breaking (19th February) Seletar Park, Singapore

Crosspointe campus,

Virginia (concept)

Major Programmes

The A380 The A380 ……EIS!EIS!

58 Bed

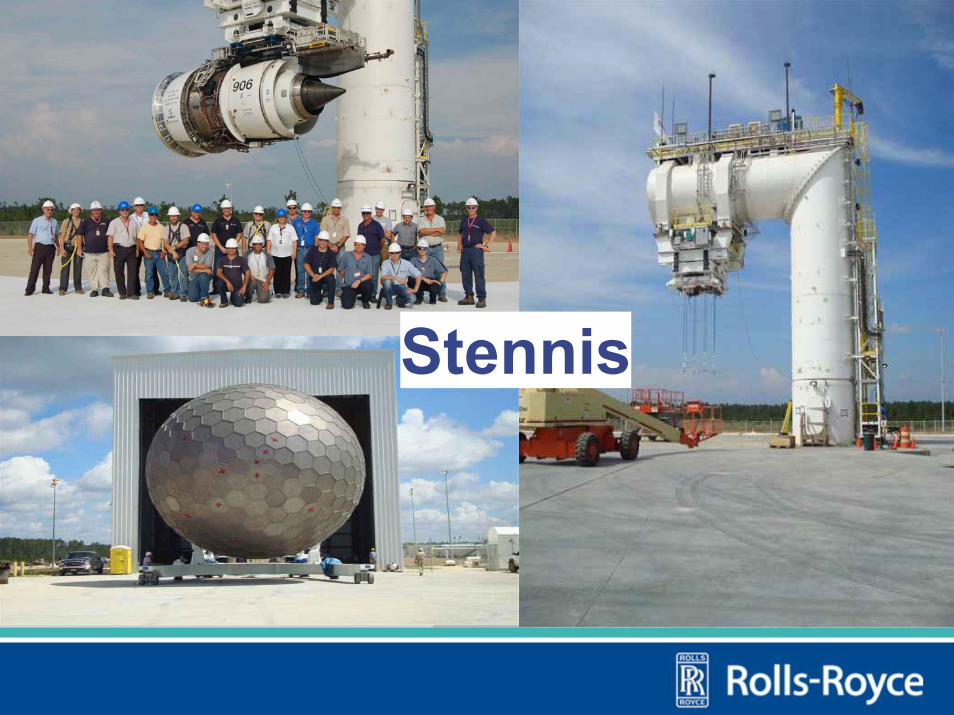

Stennis

© 2008 Rolls-Royce plcThe information in this document is the property of Rolls-Royce plc and may not be copied or communicated to a third party, or used for any purpose other than that for which it is supplied without the express written consent of Rolls-Royce plc.This information is given in good faith based upon the latest information available to Rolls-Royce plc, no warranty or representation is given concerning such information, which must not be taken as establishing any contractual or other commitment binding upon Rolls-Royce plc or any of its subsidiary orassociated companies.

Rolls-Royce data-strictly privateNot for internal or external distribution

The Purchasing

Journey to World Class

Visi

on

Stra

tegy

2008

BPD

world class global purchasing

organisation

peopleprocess

total coststrategic sourcing

relationshipscustomer satisfaction

enablers – relentlessly drive to deliver projects that will change our future

outputs – excellence in executing commitments and delivering business results

Mission

Best performing supply chain delivering m

utual competitive

advantage to Rolls-Royce, its customers and suppliers

A global team with a common vision

The Challenges Ahead

Unprecedented growth with new customers in new

markets

Growing customer expectations

Challenging economic conditions

Strong competition

Poor operational performance of the supply chain

Financial market crisis and access to capital

© 2008 Rolls-Royce plcThe information in this document is the property of Rolls-Royce plc and may not be copied or communicated to a third party, or used for any purpose other than that for which it is supplied without the express written consent of Rolls-Royce plc.This information is given in good faith based upon the latest information available to Rolls-Royce plc, no warranty or representation is given concerning such information, which must not be taken as establishing any contractual or other commitment binding upon Rolls-Royce plc or any of its subsidiary orassociated companies.

The Purchasing Mission, Vision and Strategy

We know our mission…“Best performing supply chain delivering mutual competitive advantage to Rolls-Royce, its customers and its suppliers”

..and we know our vision“World-class global purchasing organisation”

Stabilise the Supply Chain 2006 - 2008

Drive for World-Class

2007 - 2012

Meeting our Business

commitments

Transformational programmes

Immediate actions

Inputs Output

People CustomerSatisfaction

RelationshipsStrategicSourcing

TotalCost

Process

Transforming our business – six strategic themes

Visi

on

Stra

tegy

2008

BPD

world class global purchasing

organisation

peopleprocess

total coststrategic sourcing

relationshipscustomer satisfaction

enablers – relentlessly drive to deliver projects that will change our future

outputs – excellence in executing commitments and delivering business results

A global team with a common vision

Best performing supply chain delivering m

utual competitive

advantage to Rolls-Royce, its customers and suppliers

Mission

Our Vision, Mission, Strategy and BPD

© 2008 Rolls-Royce plcThe information in this document is the property of Rolls-Royce plc and may not be copied or communicated to a third party, or used for any purpose other than that for which it is supplied without the express written consent of Rolls-Royce plc.This information is given in good faith based upon the latest information available to Rolls-Royce plc, no warranty or representation is given concerning such information, which must not be taken as establishing any contractual or other commitment binding upon Rolls-Royce plc or any of its subsidiary orassociated companies.

Where we are today

Significant challenges Huge opportunitiesPurchasing’s significance is increasing Purchasing is becoming increasingly global

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

0 0 0 0 0 0 0 0 0Year

£M B U

YM

A K

E

66% Buy 72% Buy

Whilst the significance of Purchasing continues to grow

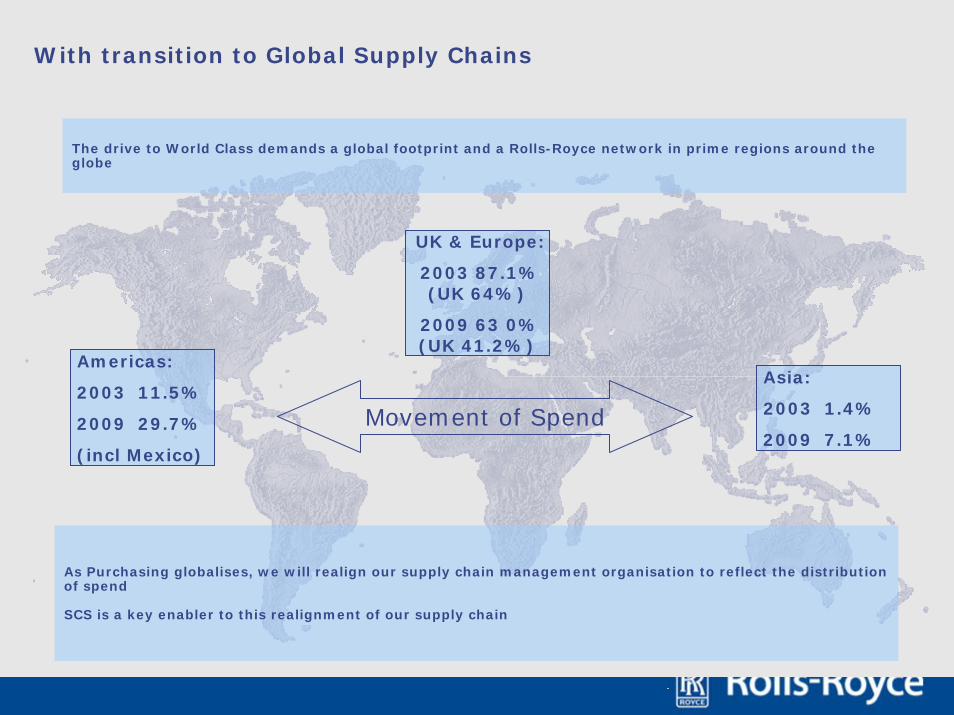

With transition to Global Supply Chains

Americas:

2003 11.5%

2009 29.7%

(incl Mexico)

UK & Europe:

2003 87.1% (UK 64%)

2009 63 0% (UK 41.2%)

Asia:

2003 1.4%

2009 7.1%Movement of Spend

As Purchasing globalises, we will realign our supply chain management organisation to reflect the distribution of spend

SCS is a key enabler to this realignment of our supply chain

The drive to World Class demands a global footprint and a Rolls-Royce network in prime regions around the globe

© 2008 Rolls-Royce plcThe information in this document is the property of Rolls-Royce plc and may not be copied or communicated to a third party, or used for any purpose other than that for which it is supplied without the express written consent of Rolls-Royce plc.This information is given in good faith based upon the latest information available to Rolls-Royce plc, no warranty or representation is given concerning such information, which must not be taken as establishing any contractual or other commitment binding upon Rolls-Royce plc or any of its subsidiary orassociated companies.

Where we need to get to World Class

Efficiency

Effec

tive

nes

s

Purchasing.

Booz l Allen l Hamilton and Hackett findings

Upper Quartile

Upper Quartile

World

Class

The Drive to World Class demands both Efficiency and Effectiveness Global Key Performance Indicators

2004 2008 World Class

Delivery Below 50% Below 50% 100%

QualityInbound defects at

1000 ppmInbound defects at

700 ppmZero inbound defects

Material Cost Price reduction Annual inflationOngoing annual cost improvements and

avoidance

High staff to spend ratio

Improving staff to spend ratio

Lean staff to spend ratio

World-class aero: 30 FTEs / $b spend

(Peer: 60-80 FTEs / $b spend)

Effectiveness

Operational Cost

Efficiency

Functional ExcellenceSupporting our drive for efficiency

Functional Excellence focuses on improving efficiency and eliminating waste intelligently and sustainably through:− Industry and internal benchmarking− Functional workstreams that look at standardising

and simplifying, such as:− Global role standardisation − Better understanding work drivers− Shared services− Addressing spans and layers

Efficiency

Effec

tive

nes

s

Purchasing.

Booz l Allen l Hamilton and Hackett findings

Upper Quartile

Upper Quartile

World

Class

Changing to become World Class

2007 201270%

60%Core Non-Core

30%

40%

Oper

atio

nal

Str

ateg

ic

Enablers

40%

80%Core Non-Core

Oper

atio

nal

Str

ateg

ic

60%

Finance

HROperational & TransactionalSupplier Development

Business Development

Process DevelopmentCommodity Management

New Product Introduction

Legacy

Production

NPI

2007

Legacy

Production

NPI

2012

Current Future

Business Development

Process DevelopmentCommodity Management

New Product Introduction

Finance

HROperational & TransactionalSupplier Development

Strategic Supplier Development Strategic Supplier Development

© 2008 Rolls-Royce plcThe information in this document is the property of Rolls-Royce plc and may not be copied or communicated to a third party, or used for any purpose other than that for which it is supplied without the express written consent of Rolls-Royce plc.This information is given in good faith based upon the latest information available to Rolls-Royce plc, no warranty or representation is given concerning such information, which must not be taken as establishing any contractual or other commitment binding upon Rolls-Royce plc or any of its subsidiary orassociated companies.

How we get there

Fix the basicsStrengthen and standardise global functionTransform the Business and Deliver the business planStrengthen supplier relationshipsGlobalize

The Improvement Journey – FIX the Basics

Maturity

3. Process FlowEfficient Processes that flowIdentifying and eliminating waste to reduce lead-time and cost

Perf

orm

ance

1. Process BasicsDefine the process and be compliantProcess basics must be the first stepIn early stages of maturity, basics give the greatest improvement in performance

2. Process ControlCapable Processes in control in a stable environmentProcess Control embeds the basics so a standard is established and performance is sustained

4. Process CapabilityMeasuring and eliminating variation increases process reliability and predictability

Processes achieving zero defects

Processes

Visual Management provides clear visibility of overall Supplier performance Customer Satisfaction

Ongoing and robust delivery and quality visual management process – across all regions and sectors

Monitoring the way we work together allowing for targeted improvement activity

Finance Finance

Human Resources Human Resources

Quality Quality

Global Supply Chain Organisation

Commodity Purchasing

Operational Purchasing

Manufacturing Eng

Supply ChainPlanning & Control

Engineering Engineering

Operations

Gen

era

l M

ach

inin

g

Co

ntr

ols

Inst

allati

on

s

Tra

nsm

issi

on

s S

tru

ctu

res

& D

rives

Co

mb

ust

ion

& C

asi

ng

s

Ro

tati

ves

Fan

s

Co

mp

ress

ors

Tu

rbin

es

Co

mp

on

en

t S

erv

ices

Ris

k &

Reven

ue S

hari

ng

(C

ivil A

ero

)

Invest

men

ts &

Serv

ices

En

erg

y

Mari

ne

Ind

ian

ap

olis

Op

era

tio

ns

Cross-functional global organization to strengthen and standardize roles, processes, and measurements

Transforming our business with Pace

Wo r l d

Cl ass

2006 2007 2008 2009 2010 2011 2012

Strategic Transformation

Tactical Change

ConsolidationBasic Standards & Processes

Critical Supplier Support

Supply Chain Simplification

Organisational Strength & Capability

Supplier Collaboration

Commodity & Supply Chain globalisation

Total Cost Management System and e.Business

Lean Enterprise

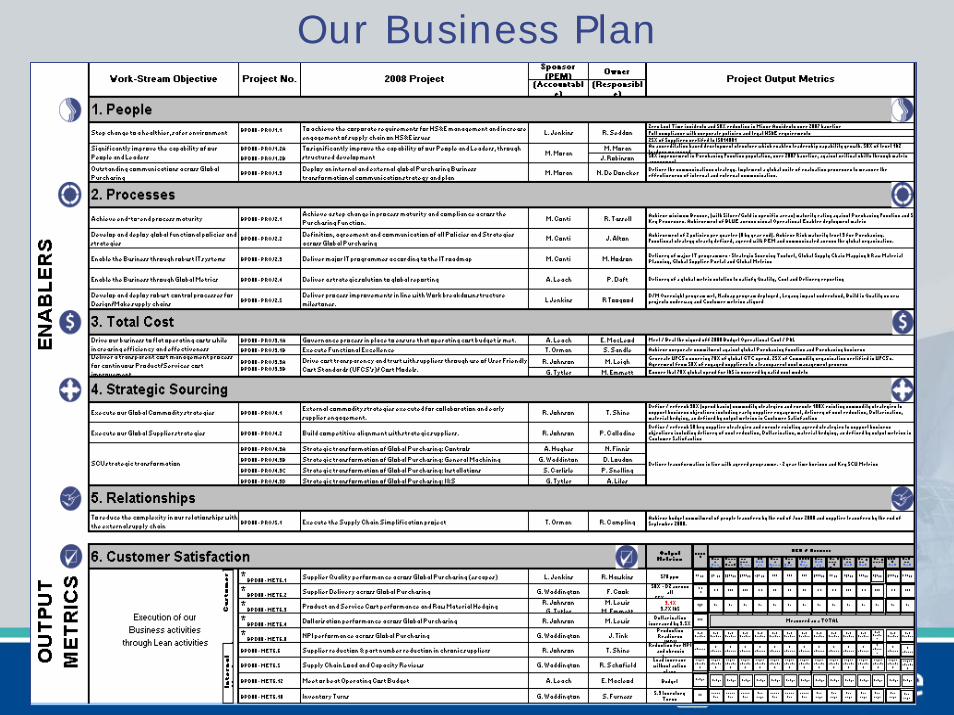

Our Business Plan

Trent 1000

75 Suppliers Total

Future engine vision

25 first tier suppliers

40 suppliers total

Strengthen and develop strategic relationships

0

100

200

300

400

500

600

1970s 1990s 2002 2006 2008 2012

Sup

plie

r cou

nt p

er e

ngin

e

Strategic Sourcing

We expect…Flawless DeliveryZero defect QualityClass leading Cost

Enabled by…Lean Manufacturing Effective supply chain managementContinuous improvement

Customer Satisfaction

Our expectations of Rolls-Royce suppliers:

The Shift to Globalisation Strategic Sourcing

Capability, Structure, Dollarization

JapanChina

(Singapore)

Russia

India+2423 (+71%)

+128 (+60%)

-3708 (-10%)

-159(-24%)

+1285

+31

Rolls-Royce Plants

Supply Chain Offices (SCO’s)Future Plants

In Summary, We must meet our commitments through Relentless Execution and…….Drive for World ClassWe are…

Redefining and restructuring our supply chain to address globalization and dollarizationDeploying our global purchasing strategy through our business planDriving robust processes to manage and control our supply chainResponding to and planning for the future market conditions

Increasing the pace is critical to our future success