harvard endowment fund

TRANSCRIPT

HARVARDENDOWNMENT FUND

Tian LunDonavan Lim

Foo Wei ShingNg Wenying

The Endowment Model

Content

1 Background on Harvard & Yale Endowment

2 Harvard vs Yale

3 What went wrong in 2009?

4 Current Risk Environment and Harvard’s Changing Obligation

5 How Harvard Modified Swensen Model Post Crisis

6 Portfolio Optimisation Analysis and Recommendations

Background: Yale & Harvard Rivalry

• Yale and Harvard, rivals in the academic sphere, extended their rivalry to the sports and financial world.

• Yale pioneered a new endowment model that returned superior returns which resulted in many endowment fund seeking to emulate the Yale model.

• This became known as the Yale or Swensen model.• Not to be outdone, Harvard “pioneered” its Hybrid model.

1

Yale Harvard

Swensen Model Hybrid Model

• Named after David Swensen, chief investment officer of Yale University

• Swensen had steered Yale’s endowment 1985: US$1bn 2008: US$22.9bn

• Under Swensen, Yale pioneered an unconventional approach to managing its endowment Swensen Model

• In the model, significant investments were made in less efficient equity markets o private equity (venture capital and

buyouts),o real assets (real estate, timber, oil,

and gas), ando absolute-return investments (hedge

funds).

Background: Swensen Model1

History Principles

• Equities, whether publicly traded or private. He pointed out that equities are a claim on a real stream of income, as opposed to a contractual sequence of nominal cash flows (such as bonds)

• Diversification. In general, Yale believed that risk could be more effectively reduced by limiting aggregate exposure to any single asset class, rather than by attempting to time markets.

• Seek opportunities in less efficient markets

• Fourth, Swensen believed strongly in using outside managers for all but the most routine or indexed investments

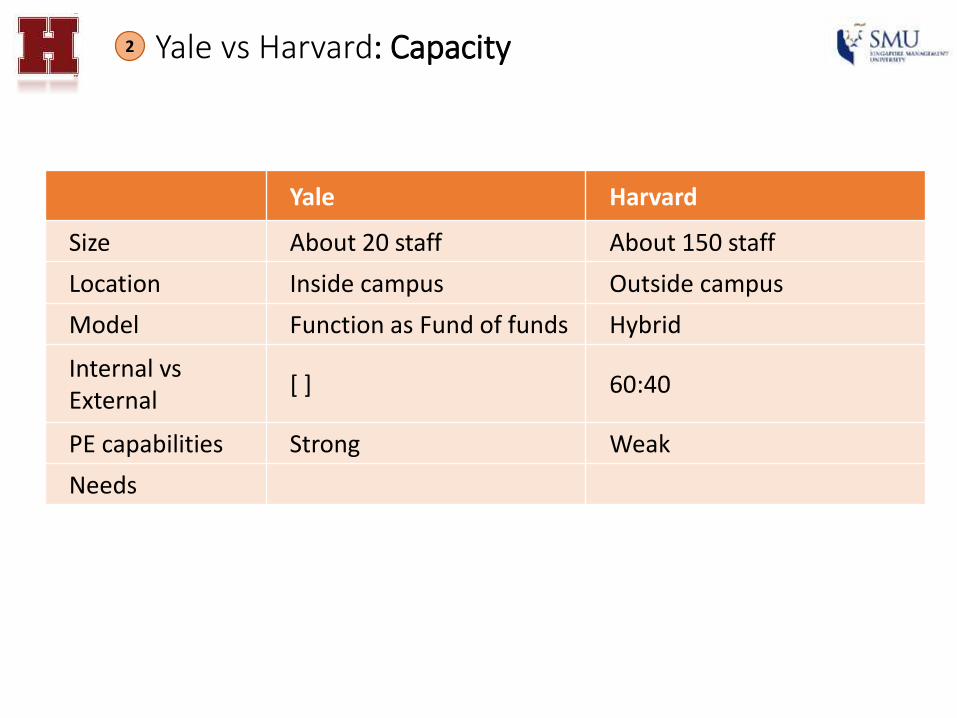

Yale Harvard

Size About 20 staff About 150 staff

Location Inside campus Outside campus

Model Function as Fund of funds Hybrid

Internal vs External

[ ] 60:40

PE capabilities Strong Weak

Needs

Yale vs Harvard: Capacity2

Return % 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Yale 41 9.2 0.7 8.8 19.4 22.3 22.9 28 4.5 -24.6 8.9 14.6

Harvard 32.2 -2.7 -0.5 12.5 21.1 19.2 16.7 23 8.6 -27.3 11.0 21.4

S&P 500 7.2 -14.8 -18 0.3 19.1 6.3 8.6 20.6 -15 -32 15 10.5

Wilshire 5000

9.5 -15.3 -16.6 1.3 21.2 8.4 10.2 21 -14 -32 18 10.5

Government bond index

7 9.6 8.8 20.2 -4.3 18.8 -7.3 5.9 12.4 7.7 11.9 9.5

Consumer price index

3.7 3.2 1.1 2.1 3.3 2.5 4.3 2.9 5.2 -0.4 1.9 3.7

Source: Bloomberg and Cases

Yale vs Harvard: Performance2

Source: Bloomberg and company documents

Asset Class (%)

Yale Harvard Yale Harvard

2008 2008 2010 2010Domestic equity

10.1 12.0 7.011.0

Foreign equity

15.2 22.0 9.922.0

Bonds 4.0 15.0 4.0 11.0Cash -3.9 -5.0 0.4 2.0Real assets 29.3 9.0 27.5 9.0Private equity 20.2 11.0 30.3 13.0Absolute return

25.1 18.0 21.016.0

Commodities 0.0 17.0 0.0 14.0High Yield 0.0 1.0 0.0 2.0

Yale vs Harvard: Asset Allocation2

What Went Wrong in 2009?3

2008 Sept: Lehman Brothers Holdings collapsed, precipitating an economic decline that had begun with the subprime mortgage crisis and setting off a global rout across financial markets.

The Dow Jones fell over 500 points (−4.4%) on a single day. Continue to decline through early 2009, whereupon it fell below 7,000 points – less than half of its 2007 high.

2009 June: Harvard University’s endowment fund manager booked losses of 27% and a staggering US$10.1 billion of its assets were wiped out.Yale: Lost 24.6% of assets (FY09)

Harvard underperformed Policy Portfolio (a smaller 25.2% loss)Harvard underperformed more than any other Ivy League school Cutbacks in capital spending & student services

Both Yale and Harvard were plagued by liquidity issue due to investment in alternative assets as market tanked Such assets take considerable time to unwind. Hedge fund even halted redemptions in 2008

Interest-rate swaps:Former President entered into series of Interest-rate swap to cap I/r on future debt issuance but required posting collateral when I/r declined

HMC lost more than US$550mn because of I/r decline

Capital Market conditions• Given high unemployment in the US and uncertain economic conditions , the equity markets pursued a strong

upward climb through the first months of 2010• Bond markets were functioning fairly normally for the most part, with reasonable liquidity and persistently low

rates. • High yield spreads declined, indicating that the risk of default was lessening• Long rates on US Treasuries were pushed lower as investors sought safe haven investments.

Current Environment: Capital Market4

Harvard Business School Considerations• Harvard’s need to Maintain the “vigour” and “Longevity” of the

endowment • Ongoing stagnation in median household income growth and

Federal Budget Cuts in education across the has put increasing pressure on grant aid expenditures ( The endowment now funds 35% of the total University budget. )

• As Private Equity landscape evolves and becomes more global, Challenge for Harvard to look for the best opportunities

• Close attention to liquidity, capital commitments and risk management ( avoid the mistake of 2009 )

Source: Harvard 2009 Annual Report

4 Current Environment: Harvard’s Obligations

4 Current Environment: Asset Correlations

Correlation of assets changes during times of crisis

4 Current Environment: Analysis of Asset Classes

Asset Class Suitability Optimality Diversification Illiquidity of Assets Potential Conflicts of Interest

Domestic EquitiesForeign EquitiesEmerging Markets

Suitable

Potentially High Returns

Emerging markets has tremendous opportunities due to both their greater inefficiencies and their

dynamic, growing economies

Overall portfolio risk can be diversified if managed

properly

Liquid(Marketable securities can be illiquid during

crisis?)

Collateral for short-term loans (security lending

agreement)

Money managers may tend to emphasize asset growth at the

expense of performance

Private Equity

Suitable**Investors cannot withdraw their invested capital whenever they

wish

Potentially High ReturnsWith high returns

attracting new investors who flooded money into the sector until returns

deteriorated

Diversification across General partners and

industriesIlliquid

Key principle was to select organizations in which the

incentives were properly aligned

Absolute Returns Suitable ** Potentially High Returns

Historically provided retunes largely

independent of overall market moves

IlliquidMoney managers may tend to emphasize asset growth at the

expense of performance

CommoditiesReal Estate

Suitable **

Potentially High ReturnsHigh and visible current

cash flow and opportunity to exploit inefficiencies

Sensitivity to inflationary force

Illiquid

Misalignment or conflicts of interest in external firm’s compensation motivation

Domestic BondsForeign BondsInflation-indexed Bonds

Suitable Low Returns

Relative low covariancewith other asset classes and

serves as a hedge against financial accidents or

periods of unanticipated deflation

LiquidIn situations of severe

liquidity shortages, Bonds can be used as

collateral for short-term loans

Post Crisis – How Harvard Modified Swensen?

1

Objective: Increase flexibility, reduce leverage and explore attractive investment themes foreseen emerging after the crisis.

Decrease uncalled capital commitments by roughly $3 Billion

2 Increased the depth and breadth of talents in the investment team - in fixed income/Asian markets, in equity arbitrage, in real estate and in externally managed funds

3 Continuation of the Hybrid Model• No change to the mix of internal and

external managers (as it would allow access to best strategy for each asset class)

• To give the portfolio the breath and depth.

• Look to increase the share of internally managed assets instead

‒ Added a COO from Pimco, a new CFO and CTO, other restructuring within investment team

5

4 Continue to emphasize on having risk tolerance as critical factor in asset allocation decisions.

5 Re-engineered the Policy Portfolio

Greater concentration in areas where HMC has unique competitive strengths such as fixed income and real assets

Fewer distinctions among the finely tuned asset classes to encourage greater collaboration among our teams in exploring investment themes

Rigorous reassessment of the fit between the endowment’s risk profile and the University’s needs.

Spectrum of Horizon introduced; short term, medium term, long term.

Post Crisis – How Harvard Modified Swensen?5

6 Integrate Risk management, liquidity and leverage management with portfolio management:o Risk: Wider range of stress tests, Buying of Insurance as protection instead of cutting exposure which may

reduce flexibility• However stress test results were subjected to accuracy of information on external manager’s

position which are often lagged, infrequent and impreciseo Asset allocation: Usage of optimal portfolio analysis, reexamining assumptions such as the range of

historical data used to reflect more current market conditions, reexamining inter-asset assumptions used to produce the efficient frontier• However the limitations of the efficient frontier is that it is very sensitive to the relative structure of

input assumptions particularly with 12 asset classes involved

7 Actions by External Managerso A subset of our external hedge fund managers, changed their investors’ ability to redeem capital,

ostensibly to protect their funds’ remaining assets.

Post Crisis – How Harvard Modified Swensen?5

Harvard’s Modification – Is it Enough?

Remaining Issues:• Liquidity position:

o Will Harvard meet liquidity needs? o Should there be a liquidity benchmark in addition to policy portfolio benchmark?o With endowment spending accounting for more than one third of total university

budget, what should change?• Asset allocation:

o Will alternative investments continue to provide high return in future?

5

Portfolio Optimization Analysis: Inputs6

• Optimize the Policy Portfolio with benchmark indexes being proxies.

• Mean-variance approach. Follow the original asset allocation of the policy portfolio. Allow permissible range of 5%.

• Take into consideration that the increasing correlation pattern during crisis time.

• Adjust asset allocation in line with Harvard’s liquidity needs, risk tolerance, etc.

Portfolio Optimization Analysis: Benchmarks6

• 10-year-long time horizon. Fully captured a complete economic cycle.

• Monthly return, 120 neutralized data points.

Portfolio Optimization Analysis: Return & StdDv6

Portfolio Optimization Analysis: Increases Correlations

6

1999-2009 “Pre-Crisis” Correlation “In-Crisis” Increased Correlation

Exp. Return: 7.10%Sharpe Ratio: 0.59

Portfolio Optimization Analysis: Results6

• Monthly review of liquidity position vs Annual review• Forecast spending (Yale uses a forecast model)• Given the difference in absolute return between top tier and other fund managers,

applying Yale’s strategy of employing more Private Equity in their portfolio may not work for all Harvard should focus on assets where they have a niche; Equity

• Use of high illiquidity hurdle rates to enter illiquid investments

Other Recommendations6

Liquidity Premium Benchmarking

Source: Columbia Business School

Other Recommendations

HARVARDENDOWNMENT FUND

Tian LunDonavan Lim

Foo Wei ShingNg Wenying

APPENDIX

Source: Columbia Business School

Appendix: Private Equity7

• Another is the focus on hunting for the best hedge funds, private-equity managers and stock pickers it's impossible for every institution to have the best managers.

• By definition, many institutions end up hiring managers who are below average. Consequently, many of them would be better off investing in index funds rather than finding themselves on the wrong side of the wide gulf that separates the performance of the best and worst managers.

Appendix7

• The Policy Portfolio is a theoretical portfolio allocated among asset classes in a mix that is judged to bemost appropriate for Harvard University from both the perspective of potential return and risk over thelong term.

• The Policy Portfolio differs from a traditional stock/bond portfolio, including allocations to less-traditional and less-liquid asset categories, such as private equity, real estate, and absolute returnstrategies.

• The Policy Portfolio provides us with a guide as to the actual allocation in the investment portfolio andalso serves as a measuring stick against which we judge the success of our active investmentmanagement activities.

Appendix: Policy Portfolio7

Appendix: Policy Portfolio7