hcr rotary version

TRANSCRIPT

The Future of America’s Health Care

Presented by Ed McClements, CLU, ChFCVentura Rotary Meeting, Sept. 1st 2010

Health Insurance Coverage , 2008

Uninsured15%

Medicaid/Other Public

13%

Medicare14%

Private Non-Group5%

Employer-Sponsored Insurance

52%

NOTE: Includes those over age 65. Medicaid/Other Public includes Medicaid, SCHIP, other state programs, and military-related coverage. Those enrolled in both Medicare and Medicaid (1.9% of total population) are shown as Medicare beneficiaries. SOURCE: Kaiser Commission on Medicaid and the Uninsured/Urban Institute analysis of March 2009 CPS

Total = 300.5 million

BIG PICTURE – REDUCE UNINSURED

Current Uninsured - 45 millionEstimated Uninsured in 2019… Without Reform – 54 million With Reform, estimated Uninsured 23 million* * Source: Congressional Budget Office, 2009

GOOD NEWS FOR UNINSURED – Anyone who wants insurance will be able to get it

BAD NEWS FOR EMPLOYERS AND MOST PEOPLE WITH CURRENT COVERAGE – Costs are predicted to go up and bureaucracy will increase

Can THEY LEGALLY DO THAT?Already 20 states have filed suitAlabamaArizonaColoradoFloridaGeorgiaIdahoIndianaMichiganMississippiNebraska

NevadaTexasUtahLouisianaSouth CarolinaPennsylvaniaVirginiaWashingtonSouth DakotaNorth Dakota

What is in the Reform Package?

This is sweeping health insurance reform, significant public program expansion with a dose of health care reform Marketplace (Underwriting, Profitability and Sales) Reforms

Creation of Government Supervised Insurance Exchanges Creation on “Essential Benefit” Levels Creation of Non-Profit Cooperatives Individual Mandates to Purchase Insurance Potential Employer Mandates to Provide Insurance or Pay a

Fine Employer Reporting and Compliance Mandates Creation of New Regulatory Agencies Changes to Existing Tax Law on Dependents Age, HSAs,

FSAs, HRAs, etc. Medicaid Expansion to 133% of Federal Poverty Level Medicare Changes (notably the closure of the Rx donut

hole) Creation of a National Insurance Program to Address Long

Term Care Demonstration projects for Medical Liability Reform Restrictions on Doctors ownership of Medical Facilities Demonstration projects for Preventative Health Care

Basic HCR Timeline

Enact-ment3/23/10•Small Business Tax Credits

First 90 Days•Temporary Reinsurance for Retirees•National High Risk Pool

Plan Years Starting 6 months after Enactment

•Deps to age 26•No Pre-Ex for Kids•No Lifetime Limits•Limited Use of Annual Limits•Preventative covered 100%

2011-2012•Limits on Medical Loss Ratios•Uniform Explanation of coverages

2014•Guarantee Issue•Individual Mandate•Rating Reforms•State Exchanges•Employer Play or Pay

Best Parts: Preventative Care 100% coverage (no deductibles nor copay

%) in all plans starting with new plan years after 9/23/2010

Creates a Prevention and Public Health Fund ($500M in 2010 scaling up to $2B in 2015) for national investment in preventative care

Grants for $240 million in 2011 and 2012 to educate and train providers in preventive medicine, health promotion, chronic disease management and evidence based medicine

Localized programs targeting obesity, smoking, and mental health

Best Parts: Supporting Primary Care

Nationwide, local Community Clinic revenues will increase dramatically (potentially about 800%) once reforms are fully implemented

Doctors treating Medicaid (aka Medi-Cal in Calif.) patients will get at least as much as MediCare doctors

Loan repayment programs for Primary Care Doctors and Nurses

Incentives for practicing in “Health Professional Shortage Areas”

Increased funding of National Health Services Corps

Small Employer Wellness Programs

$200 million in grants to eligible Small Employers for creating comprehensive wellness programs for employees

▪ Less than 100 employees▪ Work an average of 25+ hours per week

▪ Not already (as of 3/23/2010) providing a wellness programFor Years 2011

-2015

Help NOW for Uninsurable Folks Pre-Existing Condition Insurance Programs

(PCIPs) are opening up nationwide (21 run by HHS / 29 state organized)

Stop-Gap solution until 2014 (when Guarantee Issue starts)

California already operates a High Risk Pool (known as the Major Risk Medical Insurance Board…MRMIB)

The NEW Federal program will be have “reasonable premiums” (apparently subsidized by Federal money)

Qualifications are strict minimum of 6 months without any insurance Proof of citizenship or legal presence

Calif.’s applications were supposed to become available 8/31/2010

www.pcip.ca.gov

Medicaid Expansion (MediCAL)

In 2014 Medicaid expands to all individuals under age 65 with incomes up to 133% of the FPL

This alone will potentially reduce uninsured by 1/3 (over 17 million people)

Federal Government will (for newly eligibles): Provide 100% of the funding 2014-2016 95% of the funding in 2017 94% of the funding in 2018 93% of the funding in 2019 And 90% of the funding in 2020

and beyond

Comparative Effectiveness Research

Patient-Centered Outcomes Research Institute

Establishes a private, non-profit corporation to assist providers, payers, and policy makers in making informed health decisions

Research conducted would be comparative clinical effectiveness research which evaluates health outcomes and clinical effectiveness, risks, and benefits of two or more medical treatments

The Legislation levies a $2 tax per participant per year ($1 in the first year of 2013) on both Insured and Self Insured plans for funding

12

Coverage of Adult Children (< age 26)

Adult Children to be eligible on parent’s plan up to age 26

▪ Regardless of School Status▪ Regardless of Married Status▪ Regardless of Dependent Status on Parents Taxes▪ Availability of other coverage is a factor in eligibility until

2014 Earliest it was supposed to go into effect was

October 1, 2010 (for plans with Oct. 1st start dates) The Obama Administration as asked health

insurers to comply in advance of the deadline - so that graduating high school and college students could be covered starting this summer

Most major health plans have said they will comply Those losing coverage can stay on Those WHO ALREADY LOST coverage can be

added at open enrollment

Biggest Issues Facing Employers

Simply trying to keep up with strategy & compliance issues No Annual or Lifetime benefit caps

Huge impact on some industries like agriculture (waivers for some?)

Community Rating/Pooling (no ability to medically underwrite ) Age Blending (rates will be limited to 1:3 ratio – youngest:oldest) “Essential” Benefit Levels richer than most current plans To Grandfather or not to Grandfather? Non-Discrimination Rules may apply (possible taxation of benefits) Seasonal Workers can only be excluded if they work 120 days or less No Exchange coverage permitted for Undocumented Workers Coming in 2014 - the Play or Pay Requirement

on Employers with over 50 employees

DON’T BE SURPRISED IF YOU ARE UNSURE – here are some helpful hints…

Is the Group over 100 employees? If so, they should be filing a 5500 annual benefit plan return to the IRS (check it for the defined plan year)

If the group is over 100 and isn’t filing a 5500, call in an expert

If the group is under 100, see if they have a Summary Plan Description ( a plan year should be defined in the SPD). All employers are supposed to have SPDs, but they commonly do not unless they are partially self insured

Call the current carrier and ASK THEM what they have in their records as the defined plan year for the client

If all else fails – define the plan year!

WHEN DOES MY PLAN YEAR START?

Special Cases – Plan Year Defined

Association Plans and Union Plans typically have their own plan year.

Western Growers Assurance Trust

▪ 7/1/2011United Agricultural Benefit Trust

▪ 1/1/2010

Grandfathering – Postponing the Inevitable

It isn’t about rocking chairs and fishing stories…

Pres. Obama’s promise “If you like what you have you can keep it”

Only applies to plans in existence as of 3/23/2010

Regulations (for keeping grandfather status) are onerous

Cannot increase coinsurance % Cannot make significant increases in deductibles , copayments

or out of pocket maximums Cannot increase employee premium share by more than 5%

Value of Grandfather status is highly questionable Almost every ”important” issue is a required change to BOTH grandfathered and non-grandfathered plans. Plus many of the issues that are eligible to be postponed are actually going to be decided FOR employers by the health insurance companies. The only significant issue is delaying discrimination testing of medical plans.

Effect of 1:3 Age Ratio on Rates

Net Pay PMPY Med

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

Males $9,348 $1,480 $916 $1,001 $1,399 $1,245 $1,144 $1,131 $1,368 $1,678 $2,036 $2,533 $3,548 $4,614 $5,887 $2,685 $2,315 $2,498

Females $8,736 $1,242 $801 $963 $1,557 $1,730 $1,959 $2,905 $3,263 $3,138 $3,165 $3,511 $4,121 $4,641 $5,482 $2,143 $2,057 $2,566

Ages < 1

Ages 1-4

Ages 5-9

Ages 10-14

Ages 15-17

Ages 18-19

Ages 20-24

Ages 25-29

Ages 30-34

Ages 35-39

Ages 40-44

Ages 45-49

Ages 50-54

Ages 55-59

Ages 60-64

Ages 65-74

Ages 75-84

Ages 85+

Source: Thompson-Reuters Market Scan Q12009 data

$1,144

$5,887

Younger Employees will be forced to subsidize Older Employees

1:5 ratio squeezed to

1:3

Qualifying Coverage Mandates

Essential Benefits: Ambulatory patient services Emergency services Hospitalization Maternity and newborn care Mental health and substance

abuse Prescription drugs Rehabilitative, habilitative

and devices Laboratory services Preventive and wellness

services Pediatric services, including

oral and vision care 100% coverage required for

preventive services, except to value-based insurance designs

19

No lifetime limits (within 6 months) or overall annual dollar limits on benefits (2014)

No waiting periods longer than 90 days

Secretary of HHS to determine the scope of essential benefits “equal to the scope of benefits provided under a typical employer plan”

Possible Designs

Initial indications are that the plan designs are going to be fairly similar, with only a varying level of cost-sharing on the first claim dollars per year as the differentiation. Keep in mind that such benefit formats can be applied to both HMO style and PPO style plans.

Next $12,500 Unlimited Benefits

$950

40% Share

BRONZE

Next $16,667 Unlimited Benefits

$950

30% Share

SILVER

Next $25,000 Unlimited Benefits

$950

20% Share

GOLD

Next $50,000 Unlimited Benefits

$950

10% Share

PLATINUM

Assuming SINGLE Coverage - Out of Pocket is $5,950 in all plans

Individual Mandates / Penalties If you make more than 133% of the Federal Poverty Level (about

$14,400 for a single person), you must have employer insurance or

buy your own in the open market or via an Exchange

Starting in 2014 there’s a penalty for not having health insurance

The penalty is non-deductible excise tax that is the HIGHER of…

Capped at no more than the average cost of the Bronze Level

benefit program21

2014 $95/person or 1% of income2015 $325/person or 2% of income2016 $695/person or 2.5% of income

Who is Eligible for Subsidy?

2010 Federal Poverty LevelsSize of family 100% of FPL 133% 400%

1 $10,830 $14,404 $43,320 2 $14,570 $19,378 $58,280 3 $18,310 $24,352 $73,240 4 $22,050 $29,327 $88,200 5 $25,790 $34,301 $103,160 6 $29,530 $39,275 $118,120 7 $33,270 $44,249 $133,080 8 $37,010 $49,223 $148,040

Government Subsidies given on premiums for individuals with incomes up to 400% of the federal poverty level (about $88,000 for a family)

Estimated to help 25 million low income folks pay for health care

HOW MUCH will Subsidies Help Lower Income Folks?

23

Single Coverage Family of 4 CoverageIncome Pay Per Yr. Pay Per Mo. % of Income Income Pay Per Yr. Pay Per Mo. % of Income

$14,404 $0 $0.00 0.00% $29,327 $0 $0.00 0.00%

$14,512 $444 $37.00 3.06% $29,547 $904 $75.33 3.06%

$21,660 $1,365 $113.75 6.30% $44,100 $2,778 $231.50 6.30%

$27,075 $2,180 $181.67 8.05% $55,125 $4,438 $369.83 8.05%

$32,490 $3,087 $257.25 9.50% $66,150 $6,284 $523.67 9.50%

$37,905 $3,601 $300.08 9.50% $77,175 $7,332 $611.00 9.50%

$43,320 $4,115 $342.92 9.50% $88,200 $8,379 $698.25 9.50%

Even AFTER the subsidy, Employees PAY THIS

Individual Mandates

Observations…

Mandates are meaningless to Undocumented Workers

Penalties are not huge – worst case scenario is that you have to pay an amount equal the premium on health insurance plan you were supposed to have

Drive is to change cultural mindset – being a responsible citizen means buying health insurance

Can Government successfully do that?

We are told the IRS has plans or hiring 16,000 more agents

24

Yes

No further action required

Do you have 50 or more full-time equivalent employees?

Yes No

Do you offer a health plan with essential benefits coverage and meets at least a 60% actuarial value? You will pay a penalty fee of $2,000

annually for every FTE if at least one FTE receives income-based premium

assistance to purchase coverage through the exchange. Penalties do not

apply to the first 30 FTE’s.Do all of your employees have a total household income that exceeds

400% of Federal Poverty Level

Must offer a free choice voucher for employee to use to purchase coverage in the exchange. Cost will be equal to

greatest contribution offered by employer.

Is required employee contribution for health plan between 8%-9.5%* of total household income?

Yes

Employees not eligible for subsidy. No Employer penalty

Is required employee contribution for health plan >9.5% of total household income?

Yes

No penalty is required

No

No Individual Analysis

*Although the law currently states 9.8%, Mercer expects this to be adjusted to 9.5%

NoYes

You will pay the lesser of $3,000 times the number of FTE’s receiving income –based assistance; or $2,000 times the total number of full-

time employees; first 30 FTE’s not counted.

Employer Decision - Play or Pay Effective in 2014

Employer Analysis

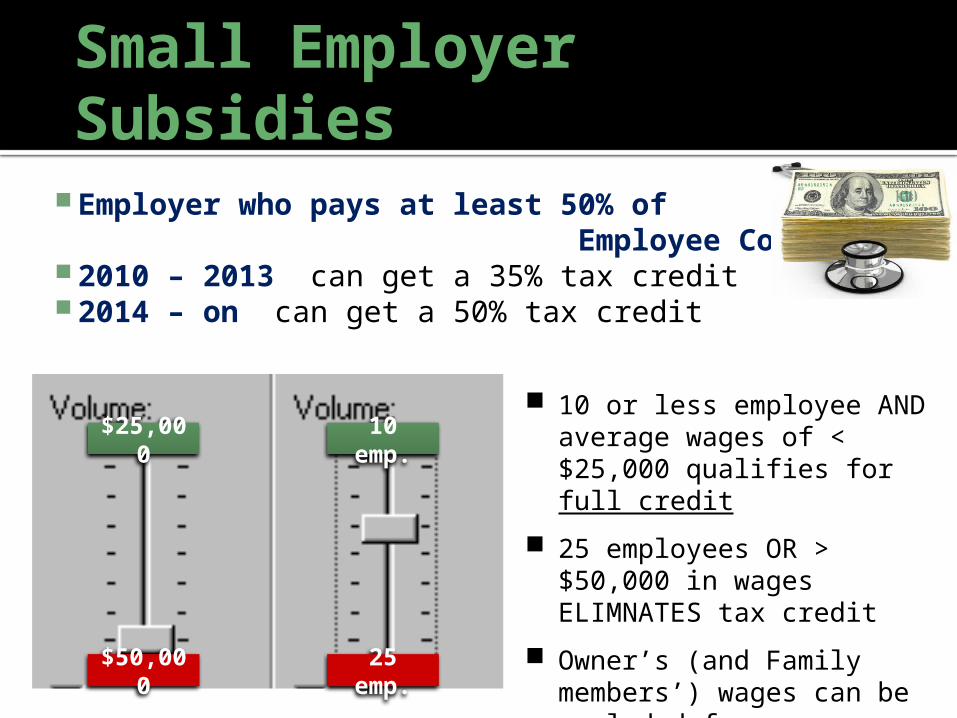

Small Employer Subsidies

Employer who pays at least 50% of Employee Cost…

2010 – 2013 can get a 35% tax credit 2014 – on can get a 50% tax credit

$25,000

$50,000

10 emp.

25 emp.

10 or less employee AND average wages of < $25,000 qualifies for full credit

25 employees OR > $50,000 in wages ELIMNATES tax credit

Owner’s (and Family members’) wages can be excluded from averages above

Exchange Programs

Exchanges are meant to assist Individuals and Small Employers find the right coverage in the marketplace

Only U.S. Citizens and Legal Immigrants can access the Exchanges

Beginning as of July 2010 States must develop Information portals

for consumers to access information on coverage options to include:▪ Private Insurance▪ High Risk Pool ▪ CHIP (Healthy Families in Calif.)▪ Medicaid (Medi-CAL in Calif.)▪ Etc.

Beginning as of January 2014 States required to have Exchange established and operational

or HHS is required to establish and operate an Exchange in a non-compliant state (directly or through a not-for-profit entity)

27

Think of

Exchanges as transitional

employment for all the

insurance agents you’ve ever met!

Tax Increases on High Income Earners - over $200,000 for individual taxpayers and $250,000 for married couples filing jointly the Employee’s share of Medicare Part A

(hospital insurance) tax rate on wages goes up by 0.9% (from 1.45% to 2.35%) on earnings

The Medicare tax will also now apply to investment income (at 3.8%) such as rents, dividends, interest earnings, etc.

Levy a $2 per employee per year tax on all health plans for fund “Comparative Effectiveness Research” This tax is $1 per employee in the first year (2013)

Revenue Generation

Various Changes to FSAs / HSAs / HRAs Prohibits reimbursement of over-the-counter

drugs through an HRA or health FSA or on a tax-free basis through an HSA or Archer Medical Savings Account. (Effective January 1, 2011)

Increase tax on distributions from an HSA or Archer MSA that are not used for qualified medical expenses to 20% (from 10% for HSAs and from 15% for Archer MSAs). (Effective January 1, 2011)

Limits amount of contributions to an FSA for medical expenses to $2,500 per year increased annually for COLA. (Effective January 1, 2013)

29

Revenue Generation

Creates Health Care Industry Fees/Taxes: Medical Device Manufacturers…

2.3% excise tax on revenue starting in 2013

On the Drug Companies… Starting at $2.8 billion in 2012 and rising to $4.1 billion in 2018

On the Health Insurers… Starting at $8 billion in 2014 and rising to $14.3 billion in 2018

30

Revenue Generation

CIGNA

2009 Profits$12 billion in

2009

Other Notable Provisions

Adds language to the Fair Labor Standards Act that allows employees to get “whistle-blower protections” if they claim employer is non-compliant with the law

Limits deductible compensation of Insurance Executives to $500,000 Creates Minimum Loss Ratios of 85% for large group plans and 80% for small group

plans (effectively capping non-claims costs at 15% and 20% respectively) Includes new Medicare fraud and abuse provisions Going forward, limits doctor ownership of hospitals Governmental oversight and limitation of loss/premium ratios and reporting; Establishes a Health Insurance Reform Implementation Fund within the Department of

Health and Human Services and allocate $1 billion to implement health reform policies Allocates $250 million to help State Insurance

Departments police health plan rate increases Creates a 10% tax on indoor tanning salons

31

Greatest Opportunity – Self Funding & Preventative Care

Self Funded Employers avoid COMMUNITY RATING

Maximum exposure limited via Stop-Loss Insurance

Get more access to claims data (within HIPAA)

You control Plan Design (to a degree) You can create its own PPO or EPO Network Possible that Co-operative Medical Services

could be created to service our employees Concentrate on Prevention Consider HRA rather than a Health Insurance

Plan (at least until 2014, when Employer Play or Pay kicks in)

Low cost health care High quality health care

Your TOP PRIORITIES

Be mindful of YOUR Plan Year

Figure out if Small Employer Tax Credit can be of use

Figure out if you could reduce employees to 50 or less

Look Into Self Funding & Preventative Care Options

Stay Informed, but DO NOT MAKE SUDDEN CHANGES

For More Detailed Analysis…

www.healthcare.govwww.kff.orgwww.chcf.orgwww.hhs.govwww.cms.govwww.dol.gov www.irs.gov/newsroom/article/0,,id=220839,00.

html

THANK YOU!

721 South A Street

Oxnard, CA 93030

(805) 483 – 1995Dept. of Ins. #

0B75139www.barkleyins.c

om