expertquote hcr slides

TRANSCRIPT

2/23/2015

1

Presented by Ophelia Y., MBA, SPHR, GPHR, SHRM-SCP

HEALTH CARE REFORM AND ITS EFFECTS ON YOUR BUSINESS

AGENDA

Background & History

The Past: Previously Implemented HCR Provisions

The Present: Current & Pending HCR Provisions

The Near-Future: HCR Provisions on the Horizon

Cheat Sheets

Wrap Up/Questions and Answers

2/23/2015

2

• US History of Healthcare

Reform

• Patient Protection and

Affordable Care Act

• Education Reconciliation Act

BACKGROUND & HISTORY

THE PAST: PREVIOUSLY IMPLEMENTED PROVISIONS

• Lactation Breaks

• Summary of Benefits and

Coverage

• Notice of Exchanges and

Subsidies

LACTATION BREAKS

• Requires almost all employers to provide

reasonable break times for an employee

to express breast milk for her nursing child

• Only applicable up to one year after the

birth of her child

• Exemptions for small employers (less than

50) if able to demonstrate undue hardship

• Amends the Fair Labor Standards Act (FLSA)

2/23/2015

3

SUMMARY OF BENEFITS & COVERAGE

• A uniform template pre-filled with the important

provisions of a specific health insurance plan

• Creates an “apples to apples” approach to

comparing and contrasting health plans

• Must be included with open enrollment materials

each year and to all new enrollees during the plan year

2/23/2015

4

NOTICE OF EXCHANGES & SUBSIDIES

• Purpose: To inform employees of the existence of Health

Insurance Exchanges (Health Insurance Marketplaces) and

potential federal subsidies available to them

• Applies to virtually all employers, regardless of size

• Must be provided to each new employee within 14 days of

the employee’s start date

NOTICE OF EXCHANGES & SUBSIDIES

• Federal Department of Labor has released two model notices

(one for organizations that sponsor a health plan, and one for

organizations that do not)

• No penalties for noncompliance at this time

THE PRESENT: CURRENT/PENDING HCR PROVISIONS

90-Day Waiting Period

Small Business Tax Credits – 2014 Increase

Health Insurance Exchanges

New COBRA Notice Language

Tax Treatment: Individual Plan Reimbursements

W-2 Reporting – 2014 W-2s

2/23/2015

5

THE PRESENT: CURRENT/PENDING HCR PROVISIONS

Employer Mandate

Employer Mandate Reporting

90-DAY WAITING PERIOD

• As of 1/1/14, no more than a 90-day waiting period for coverage for new

employees

• For all plans renewing on or after 1/1/14

• Applies to all group health plans, regardless of group size

• Applies to both Grandfathered and Non-Grandfathered Plans

• Current guidance does not allow “first of the month following 90-day” waiting

period

SMALL BUSINESS TAX CREDITS

2014 and beyond: 2014 and beyond: 2014 and beyond: 2014 and beyond: Up to 50% 50% 50% 50% Tax Credit on

Employer-Paid Premiums

(35% for nonprofits)

Tax credit, not a deduction

2/23/2015

6

SMALL BUSINESS TAX CREDITS

To Be Eligible:

• Must contribute at least 50 percent of the cost of health care single coverage,

• Must pay average annual wages below $50,000,

• Must purchase coverage through the state SHOP exchange; and

• Must have less than the equivalent of 25 full-time employees

To Be Eligible for Full Amount:

• Must pay average annual wages below $25,000, and

• Must have less than the equivalent of 10 full-time employees

STATE HEALTH CARE EXCHANGES

Each state has one. Some set up by federal

government, some by the state and some are hybrids

Virtual/competitive marketplace offering

health plans

Individuals and small employers (fewer than 50

FTEs) may shop in exchanges – Some states currently allow groups of fewer

than 100

Starting in 2016, all SHOPs will be open to employers

with up to 100 full time equivalents

States have some flexibility regarding the set up of the

exchange(s) and participation requirements

STATE HEALTH CARE EXCHANGES

Two Parts to the State Health Care Exchange:Two Parts to the State Health Care Exchange:Two Parts to the State Health Care Exchange:Two Parts to the State Health Care Exchange:

1)1)1)1) Marketplace Marketplace Marketplace Marketplace – Individual health plans

2)2)2)2) SHOP SHOP SHOP SHOP – Small Group Health Plans

(Small Business Health Options Program)

2/23/2015

7

STATE HEALTH CARE EXCHANGES: THE MARKETPLACE

• Open Enrollment for 2015:

11/15/14 11/15/14 11/15/14 11/15/14 –––– 2/15/15 2/15/15 2/15/15 2/15/15

• Forfeit the employer health insurance contribution, but may be eligible

for federal premium subsidy

• No payroll deduction available for Marketplace Plans

STATE HEALTH CARE EXCHANGES: THE SHOP

• For groups with less than 50 employees

• May shop with or without a broker, cost is the same to the employer

• Small business tax credit onlyonlyonlyonly available for plans purchased through

the SHOP

STATE HEALTH CARE EXCHANGES: THE SHOP

• Employers may enroll at anytime during the year

• If the employer enrolls by the 15th of the month, coverage may begin as soon as

the 1st of the next month

• Must offer plan to all full-time employees working 30+ hours/week

• In many states, at least 70% of the full-time employees must enroll in the SHOP

plan to maintain eligibility. (Employers who apply for SHOP coverage from 11/15 -

12/15 can enroll without meeting this requirement.)

• States that set up their own Exchanges have some

flexibility in the features

2/23/2015

8

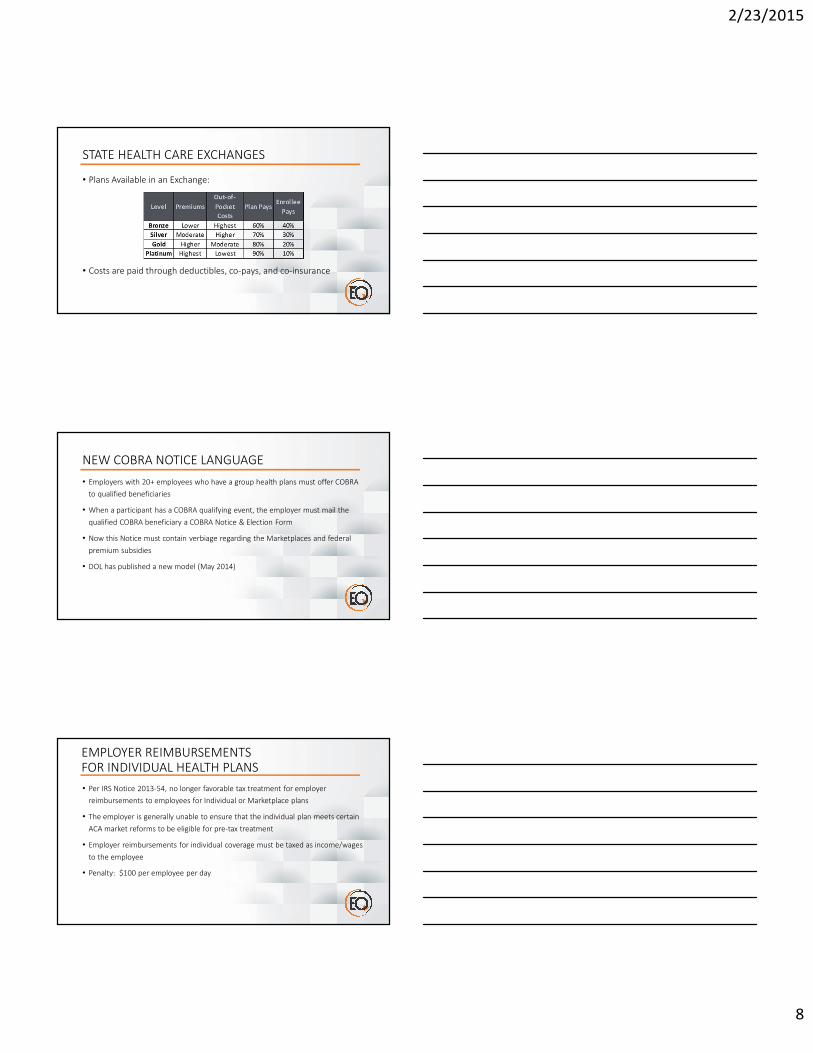

STATE HEALTH CARE EXCHANGES

• Plans Available in an Exchange:

• Costs are paid through deductibles, co-pays, and co-insurance

NEW COBRA NOTICE LANGUAGE

• Employers with 20+ employees who have a group health plans must offer COBRA

to qualified beneficiaries

• When a participant has a COBRA qualifying event, the employer must mail the

qualified COBRA beneficiary a COBRA Notice & Election Form

• Now this Notice must contain verbiage regarding the Marketplaces and federal

premium subsidies

• DOL has published a new model (May 2014)

EMPLOYER REIMBURSEMENTS FOR INDIVIDUAL HEALTH PLANS

• Per IRS Notice 2013-54, no longer favorable tax treatment for employer

reimbursements to employees for Individual or Marketplace plans

• The employer is generally unable to ensure that the individual plan meets certain

ACA market reforms to be eligible for pre-tax treatment

• Employer reimbursements for individual coverage must be taxed as income/wages

to the employee

• Penalty: $100 per employee per day

2/23/2015

9

W-2 REPORTING

• Large employers (issuing more than 250 W-2s in the previous tax year)

must report the “aggregate cost” of employee-sponsored health plans

on the W-2

• Applies to both grandfathered and non-grandfathered plans

• Does not change tax treatment of plans

• For most plans, the “aggregate cost” includes both employee and

employer contributions

W-2 REPORTING

Who is required to report the cost of healthcare on the

2014 W-2’s?

THE PRESENT: NEW FOR 2015

Employer Mandate

Employer Mandate Reporting

2/23/2015

10

EMPLOYER MANDATE DELAYED

Employer must offer health insurance to full-time employees (30 hours/week) according to the

following table:

Full Time Equivalents –Including Control Groups

Employer Mandate Penalties Begin

Margin of Error

100+ 1/1/2015 30% in 2015 and 5% thereafter

50 -99 1/1/2016** 5%

Less than 50 N/A N/A

** Delay to 2016 applies only if:** Delay to 2016 applies only if:** Delay to 2016 applies only if:** Delay to 2016 applies only if:

1) The employer did not reduce its workforce to get below the 99 employee

threshold without a bona fide reason

2) The employer did not materially reduce its health care plan

EMPLOYER MANDATE: FULL TIME EQUIVALENT EMPLOYEES (FTES)

• Look-back period

____ Part-time Employee Equivalents(Total Monthly Part-Time Hours/120)

+ ____ Full-time Employees (30 hours/week or more)

Owners (Sole proprietors, Partners in a Partnership, Members of LLCs

- ____ Taxed as a Partnership, and Shareholders who own two percent or more in an S

Corporation)

= ____ Full-time Equivalent Employees

EMPLOYER MANDATE: PENALTIES

•Calculation:Calculation:Calculation:Calculation:•$2,000 annually for each full-time employee, excluding the first 30 (80 in 2015) employees•{the total number of employees in the firm (subsidized and unsubsidized) minus 30 or 80} x {$2,000}

A Penalty: A Penalty: A Penalty: A Penalty: When a plan that meets minimum

coverage requirements is not offered

• Calculation:Calculation:Calculation:Calculation:• $3000 annually for each employee who actually receives a federal

premium subsidy

B Penalty: B Penalty: B Penalty: B Penalty: When minimum coverage is provided but it is not

affordable

• Overall Penalty: Overall Penalty: Overall Penalty: Overall Penalty: The lesser of A Penalty or B Penalty

• Penalties are Calculated Monthly – Paid Annually

2/23/2015

11

EMPLOYER MANDATE: IMMUNIZING THE PLAN

Minimum Essential Coverage

Affordable RateAll Full Time Employees

MINIMUM ESSENTIAL COVERAGE

• Health insurance plan design, notnotnotnot employer contribution to the plan

• Health insurance carrier must pay for at least 60% of treatment costs

(60% actuarial minimum value)

• “Bronze level” plan

AFFORDABLE RATE

• Exclusively refers to employee contribution

to the plan

• Misconception – Certain Contribution %

Required

• Coverage is considered “affordable” if

employee contributions for employee only

coverage do not exceed 9.5% of an 9.5% of an 9.5% of an 9.5% of an

employee’s household employee’s household employee’s household employee’s household incomeincomeincomeincome

There are three safe harbor methods for

determining affordability:

1)1)1)1) WWWW----2 Wages 2 Wages 2 Wages 2 Wages - 9.5% of an employee’s W-2

wages (reduced for salary reductions

under a 401(k) plan or cafeteria plan)

2)2)2)2) Rate of Pay Rate of Pay Rate of Pay Rate of Pay - 9.5% of an employee’s

monthly wages (hourly rate x 130 hours

per month)

3)3)3)3) Federal Poverty Level Federal Poverty Level Federal Poverty Level Federal Poverty Level - 9.5% of the

Federal Poverty Level for a single

individual

2/23/2015

12

FULL TIME EMPLOYEES

• Minimum essential coverage at an affordable rate must be offered to

all full time employees regularly working at least 30 hours30 hours30 hours30 hours per week

following the 90-day waiting period

• Also, it must be offered to their dependent children, but not spouses

• No requirement to offer insurance to part time employees – less than

30 hours

• Begins in 2015 tax year and only applies to employers with 50+ full-time equivalent

employees

• The forms must be filed for first time in early 2016 for the 2015 calendar year.

• Just like W-2’s, copies of the forms must be provided to employees by January 31st

and filed with the IRS by February 28th (paper) or by March 31st (electronic)

• Electronic filing required unless the employer will be submitting fewer than 250 1095-

C forms for the year

EMPLOYER MANDATE:

REPORTING REQUIREMENTS

Section 6056 of the Tax Code requires:Section 6056 of the Tax Code requires:Section 6056 of the Tax Code requires:Section 6056 of the Tax Code requires:

1) One Transmittal Form (IRS Form 1094-C)

2) Employee Statements (IRS Form 1095-C – top half only)

It may help you to think of the 1094-C as similar to the W-3 (a transmittal form) and

the 1095-C as similar to the W-2 (a separate return for each employee)

*Self-funded plans require additional reporting under Section 6055 Section 6055 Section 6055 Section 6055 of the Tax Code

EMPLOYER MANDATE:

REPORTING REQUIREMENTS

2/23/2015

13

2/23/2015

14

Three Methods of Reporting:Three Methods of Reporting:Three Methods of Reporting:Three Methods of Reporting:

1)1)1)1) General Method General Method General Method General Method – Required method for all large employers unless they qualify for reporting

relief provided by the two alternative methods. (See next two slides for data collection

requirements)

2)2)2)2) Qualifying Offer Method Qualifying Offer Method Qualifying Offer Method Qualifying Offer Method – To use this method the employer must offer a bronze level or higher

plan where the cost to the employee of employee-only coverage is less than about $1,100 in

2015. Also, plan must be offered to all family members. Provides relief from reporting

monthly, employee-specific health information.

3)3)3)3) 98% Offer Method 98% Offer Method 98% Offer Method 98% Offer Method – To use this method, the employer must offer a bronze level or higher plan

at an affordable rate to at least 98% of the company’s full time employees. Provides relief

from identifying which employees regularly work full-time hours.

EMPLOYER MANDATE:

REPORTING REQUIREMENTS

So What Information Do I Need to Track in 2015?So What Information Do I Need to Track in 2015?So What Information Do I Need to Track in 2015?So What Information Do I Need to Track in 2015?

1) Employer name, address, and Tax ID

2) Name and phone number of employer’s contact person responsible for health insurance (this

may be either an employee or agent of the employer)

3) Calendar year for which the information is reported

4) Certification as to whether the employer provided minimum essential coverage to full-time

employees and their dependents by calendar month

5) Months minimum essential coverage was available to each full-time employee

EMPLOYER MANDATE:

REPORTING REQUIREMENTS

So What Information Do I Need to Track in 2015 (cont.)?So What Information Do I Need to Track in 2015 (cont.)?So What Information Do I Need to Track in 2015 (cont.)?So What Information Do I Need to Track in 2015 (cont.)?

6) Each full-time employee’s monthly cost for employee-only coverage under the employer’s least

expensive minimum value plan (bronze level or higher plan)

7) Number of full-time employees employed each month in the calendar year

8) Name, address, and tax ID of each full-time employee employed during the calendar year

9) Months each employee was covered on the group health plan during the year

** Self-insured plan sponsors must collect additional information

EMPLOYER MANDATE:

REPORTING REQUIREMENTS

2/23/2015

15

THE NEAR FUTURE: HCR PROVISIONS ON THE HORIZON

• Non-Discrimination

• Automatic Enrollment

NON-DISCRIMINATION

Per IRS, delayed until at least 2015

“Similar” to current regulations for self-insured plans

Grandfathered plans excluded

When implemented will most likely prohibit:

• Management Carve-Out Plans

• Higher % contributions to HCI’s

• Executive Health Plans

AUTOMATIC ENROLLMENT

Employers with more than 200 full-time employees required to automatically enroll new employees

Employees may still opt out

Automatic Enrollment Rules delayed until at least 2015, probably longer

Federal Department of Labor has not yet issued guidance on this issue

2/23/2015

16

CHEAT SHEETS

Provisions by Employer Size

CHEAT SHEET #1

1) Notice of Exchanges and Subsidies

2) Lactation Breaks

3) No Favorable Tax Treatment for Individual or Marketplace Plan

Reimbursements

Provisions for Small Employer (fewer than 50 employees) with no Provisions for Small Employer (fewer than 50 employees) with no Provisions for Small Employer (fewer than 50 employees) with no Provisions for Small Employer (fewer than 50 employees) with no Health Health Health Health

Insurance Plan:Insurance Plan:Insurance Plan:Insurance Plan:

CHEAT SHEET #2

1) Notice of Exchanges and Subsidies

2) Lactation Breaks

3) Small Business Tax Credits (If less than 25 employees)

4) Summary of Benefits and Coverage

5) New COBRA Notice Language

6) 90-Day Waiting Period

7) Non-Discrimination – if non-grandfathered (delayed)

Provisions for Provisions for Provisions for Provisions for Small Small Small Small Employer Employer Employer Employer (fewer than 50 (fewer than 50 (fewer than 50 (fewer than 50 eeeemployeesmployeesmployeesmployees) with a ) with a ) with a ) with a Health Health Health Health

Insurance Plan:Insurance Plan:Insurance Plan:Insurance Plan:

2/23/2015

17

CHEAT SHEET #3

1) Notice of Exchanges and Subsidies

2) Lactation Breaks

3) W-2 Reporting (if issue more than 250

W-2s)

4) Summary of Benefits and Coverage

5) New COBRA Notice Language

6) 90-Day Waiting Period

7) Employer Mandate – Effective 1/1/15 for

100+ employees and 1/1/16 for 50 – 99

employees.

8) Employer Mandate Reporting

9) Non-Discrimination – if non-

grandfathered (delayed)

10) Automatic Enrollment – 200+ employees

(delayed)

Provisions for Large Employer (50+ Provisions for Large Employer (50+ Provisions for Large Employer (50+ Provisions for Large Employer (50+ employeesemployeesemployeesemployees) with a ) with a ) with a ) with a Health Health Health Health Insurance PlanInsurance PlanInsurance PlanInsurance Plan::::

Questions?