hidden potential of your occupancy costs: how jll’s corporate finance team can help

TRANSCRIPT

Tapping Into

Hidden Potential

Using the balance sheet to lower your occupancy cost

April 2014

To Lease or to Own?

Driving Value

2

Determinants of Corporate Real Estate Value

Lease Terms and Conditions

Lease Term

Rent Escalations

Corporate Guarantee

Master vs. Individual Leases

Structural Obligation

Early Termination

ROFO/ROFR

Assignment/Subleasing

Lease Term

Rent Escalations

Corporate Guarantee

Master vs. Individual Leases

Structural Obligation

Early Termination

ROFO/ROFR

Assignment/Subleasing

202015 years15 years 202015 years15 years

FixedFixedCPICPI FixedFixedCPICPI

YesYesNoNo YesYesNoNo

Master LeaseMaster LeaseIndividual LeaseIndividual Lease Master LeaseMaster LeaseIndividual LeaseIndividual Lease

BondableBondableNNNNNN BondableBondableNNNNNN

NoNoYesYes NoNoYesYes

NoneNoneYesYes NoneNoneYesYes

NoneNoneTenant ControlledTenant Controlled NoneNoneTenant ControlledTenant Controlled

Minimizes ValueMinimizes Value Maximizes ValueMaximizes Value

Lease Terms and Conditions

Lease Term

Rent Escalations

Corporate Guarantee

Master vs. Individual Leases

Structural Obligation

Early Termination

ROFO/ROFR

Assignment/Subleasing

Lease Term

Rent Escalations

Corporate Guarantee

Master vs. Individual Leases

Structural Obligation

Early Termination

ROFO/ROFR

Assignment/Subleasing

202015 years15 years 202015 years15 years

FixedFixedCPICPI FixedFixedCPICPI

YesYesNoNo YesYesNoNo

Master LeaseMaster LeaseIndividual LeaseIndividual Lease Master LeaseMaster LeaseIndividual LeaseIndividual Lease

BondableBondableNNNNNN BondableBondableNNNNNN

NoNoYesYes NoNoYesYes

NoneNoneYesYes NoneNoneYesYes

NoneNoneTenant ControlledTenant Controlled NoneNoneTenant ControlledTenant Controlled

Minimizes ValueMinimizes Value Maximizes ValueMaximizes Value

Lease Structure Gross Bondable

Purchase Option Yes No

HIGHEST CAP RATE LOWEST CAP RATE

Location

Property Condition

Lease Term

Tenant Credit

Property Class

25 years 0 years

Investment-Grade Speculative

Class C Class A

Tertiary Market Primary Market

Poor Excellent

Value Deterrents Positive Value Drivers

Lower Your Occupancy Costs The Right Tool, The Right Opportunity, The Right Investor

Tool Lease Term Lease Rent Credit

Worthiness

Balance

Sheet

Vacancy Discount

Rate

Acquisition

Long-Term Sale

Leaseback

Acquisition Sale

Leaseback

Lease Buy Down

Tenant Led Build-

to-Suit

Short-Term Sale

Leaseback

Deal Packaging

Identifying your company’s leverage points can help determine which capital markets

tools can help tap into hidden value in your real estate portfolio.

3

Potential to acquire at low basis

Absolute control over property

Reset depreciation of Leasehold Improvements

Cease costly rental obligations

NPV benefits if low cost of capital

Points of Leverage

Lease Term Lease Rate Credit

Worthiness Balance Sheet Vacancy Discount Rate

Short Remaining

Lease Term Excess Capital

Low Discount

Rate

Acquisition Purchase a currently leased asset

Considerations Benefits

Asset goes on balance sheet

Debt goes on balance sheet

Not always most efficient use of capital

Potential for losses if company no longer needs

building in the future (residual risk)

4

$21.4 Million Purchase Price

$200K NPV Benefit

$700K Annual Earnings Benefit

Acquisition Purchase a currently leased asset

Client Situation

$1.1 Million Annual Cost Savings

While each acquisition is different, a

recent acquisition yielded significant

savings for our client. The

transaction contemplated a 100K SF

asset with a net rent of $15 psf

purchased at a 7.00% cap rate.

The client expected to use the

building for 15+ years and had a

discount rate of 5.00%

Financial Impact

5

Points of Leverage

Lease Term Lease Rate Credit

Worthiness Balance Sheet Vacancy Discount Rate

Can Accept Long

Term

Investment

Grade

High Discount

Rate

Long Term Sale Leaseback Sell property for upfront proceeds, but retain long-term control

Preserve capital

Monetize asset to generate capital and redeploy

Remove assets from balance sheet

Structured to meet key objectives

Enhance occupancy flexibility

Transfer residual risk exposure

Considerations Benefits

Credit and lease term drive pricing

EBITDA Impact

NPV benefits greatest for companies with high

cost of capital

Strategic nature of asset

Need for future capital improvements

6

Earnings Neutral Transaction

Alleviate Residual Risk

$18 Million Day 1 Net Proceeds

$3.1 Million NPV Benefit

Long Term Sale Leaseback Sell property for upfront proceeds, but retain long-term control

Clients executing long term sale

leasebacks include Walgreens, Citi,

EDMC, and AT&T, among others.

Cap Rates on these types of

transactions are at historic lows,

making now an ideal time for

corporate occupiers to consider this

strategy

This example considers a 100K SF

asset leased for 15 years at a net

rent of $15 psf.

The client had a discount rate of

10.00%, an annual depreciation

expense of $5.33 psf and re-

deployed the proceeds at a 5.00%

return.

Client Situation Financial Impact

7

Points of Leverage

Lease Term Lease Rate Credit

Worthiness Balance Sheet Vacancy Discount Rate

Has Short Term,

Can Do Long

Term

Investment

Grade

High Cost of

Capital

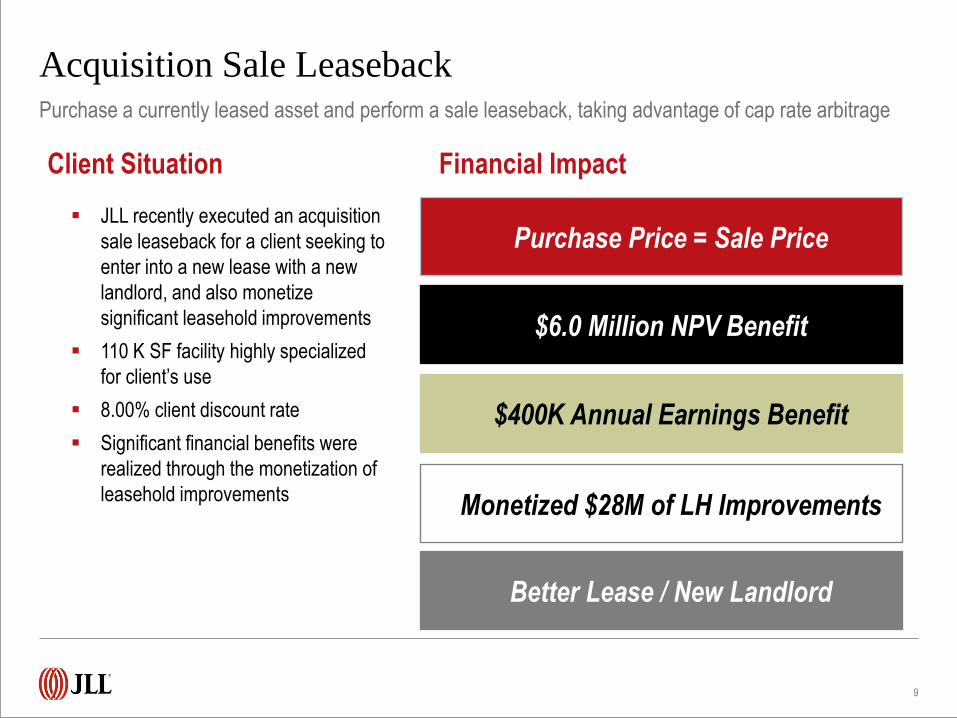

Acquisition Sale Leaseback Purchase a currently leased asset and perform a sale leaseback, taking advantage of cap rate arbitrage

Potential to acquire at low basis

Generate upfront proceeds or lower long term

occupancy costs by utilizing cap rate arbitrage

Choose new landlord

Utilize credit to drive down rent

Utilize credit to increase cash

Considerations Benefits

Prevents title from passing to tenant

Sale leaseback generally performed “off-market”

Less likely to receive tenant improvement

allowance than standard lease extension

Option to sell leasehold improvements

8

Better Lease / New Landlord

$400K Annual Earnings Benefit

$6.0 Million NPV Benefit

Purchase Price = Sale Price

Acquisition Sale Leaseback Purchase a currently leased asset and perform a sale leaseback, taking advantage of cap rate arbitrage

JLL recently executed an acquisition

sale leaseback for a client seeking to

enter into a new lease with a new

landlord, and also monetize

significant leasehold improvements

110 K SF facility highly specialized

for client’s use

8.00% client discount rate

Significant financial benefits were

realized through the monetization of

leasehold improvements

Client Situation Financial Impact

Monetized $28M of LH Improvements

9

Points of Leverage

Lease Term Lease Rate Credit

Worthiness Balance Sheet Vacancy Discount Rate

Above Market Speculative

Credit

Excess

Capital

Low Discount

Rate

Lease Buy Down Buy down the remaining rental obligation in an existing lease

Reduce rental cost to market rate

Hedge against the risk of a future impairment if the

facility becomes surplus

Decrease carrying cost of lease space in order to

facilitate subleasing at market

Deploy capital

Considerations Benefits

Utilize available, low-cost company capital to buy-

down an existing lease obligations where the

landlord’s return expectation is higher than the

company’s cost of capital

Buy Down payment against taxable income

Requires cash upfront which may increase

company debt

10

70.24 PSF Buy Down Payment

$28 PSF Earnings Benefit (10 years)

$6.91 PSF NPV Benefit

Reduced Rent $10 psf annually

Lease Buy Down Buy down the remaining rental obligation in an existing lease

The client in this example had sub-

investment grade credit but cash

available to deploy

8.75% discount rate

10 years of term at $20 psf

The rent was reduced $10 psf

annually

Based on an investor IRR

requirement of 7.00%, the buy down

payment was $70.24 psf

Client Situation Financial Impact

11

Points of Leverage

Lease Term Lease Rate Credit

Worthiness Balance Sheet Vacancy Discount Rate

Long Term Investment

Grade

Desire to Re-size

/ Re-locate

High Discount

Rate

Tenant Led Build-to-Suit Lease (Vs Developer Led) Leverage strong company credit and relationships to achieve optimal pricing while building a new facility

New facility designed to company’s standards

Reduce operating expenses through efficiencies

Densify to modern standards / reduce sf

Ability to fund entire project cost, including Tis

Potential to receive state or local incentives

Present value savings on lease payments

Considerations Benefits

Ability to manage incentive process

Ability to manage developer

Requires long term lease

Site selection can be difficult if developer

controlled

Lease classification scrutinized by underwriters

12

Points of Leverage

Lease Term Lease Rate Credit

Worthiness Balance Sheet Vacancy Discount Rate

Term will provide

higher sale price

Short Term Sale Leaseback Sell and lease a property back for less than 5 years

Generate higher sale price than vacant sale

Allows buyer to pass reduced stabilization costs to

seller through increased sale price

Minimize loss on assets where long term

occupancy is not anticipated

Maintain space flexibility

Considerations Benefits

Leaseback terms of five years or less are viewed

as a staged exit and price conservatively

Market dynamics and real estate fundamentals

effect pricing more than a long term SLB

Eye on the balance between deprecation and rent

Strategically developing a story around renewal

probability can significantly impact proceeds

13

Points of Leverage

Lease Term Lease Rate Credit

Worthiness Balance Sheet Vacancy Discount Rate

Mix of Long &

Short Flexibility

Investment

Grade

Under Utilized

Space

High Discount

Rate

Deal Packaging Enhance pricing and mitigate GAAP losses by packaging low yield plays with high yield plays

Generates sale proceeds and allows redeployment

of capital into core competencies

Control over allocations of gains and losses

Allows for disposition of unwanted space while

minimizing upfront GAAP losses

Right-size portfolio space, lower occupancy costs

Considerations Benefits

Need to sell dominant share of long term assets

to offset vacant and short term asset losses

Can be structured in a variety of ways to fit the

company’s needs and optimize the portfolio as a

whole

Individual property sale value must be at fair

market value

14

To Lease or to Own?

You Can Find the Answer with JLL’s Corporate Finance Team

© Copyright 2014 Jones Lang LaSalle

The full presentation includes updates on the

capital markets environment, additional financial

examples, further financial example detail, and

tips on how to identify opportunities to create

value in your real estate portfolio.

To View the Complete Presentation

Click Here

Bruce Westwood-Booth

Managing Director – Corporate Finance

Chicago, IL

+1 (312) 228-2966