hkicpa and ftms module d taxation module...

TRANSCRIPT

1

HKICPA and FTMS

Module D – Taxation

Module Preparation Seminar

Patrick Ho

LL.B, LL.M, MBA, MCS, FCPA, FCCA, FTIHK, PCLL

Author of “Hong Kong Taxation and Tax Planning”

Principal Lecturer, FTMS Training Systems (HK) Ltd,

13 April 2012

2

Agenda

Major or Difficult Syllabus Topics (Part I)

• Salaries tax:

- Office, employment and pension

- Employment benefits

- Termination payments

• IRD letters

3

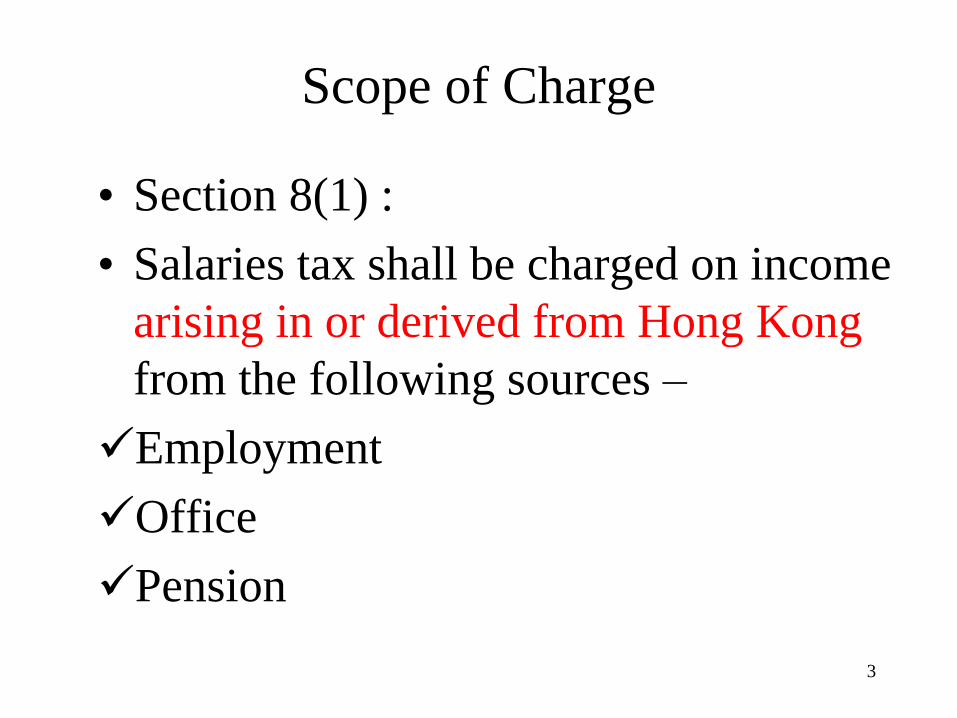

Scope of Charge

• Section 8(1) :

• Salaries tax shall be charged on income

arising in or derived from Hong Kong

from the following sources –

Employment

Office

Pension

4

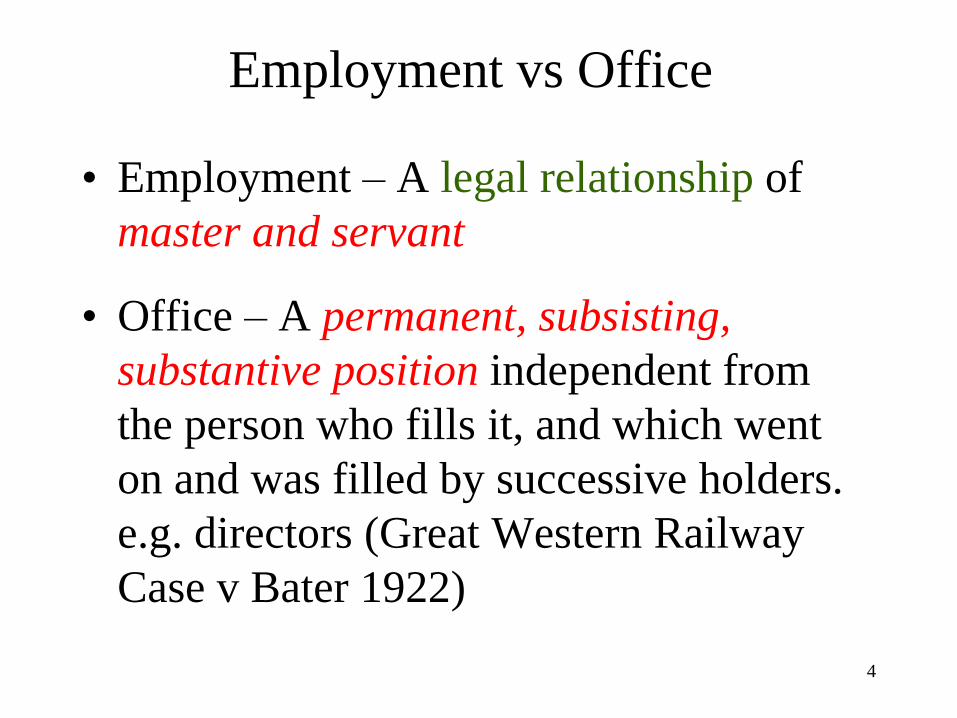

Employment vs Office

• Employment – A legal relationship of

master and servant

• Office – A permanent, subsisting,

substantive position independent from

the person who fills it, and which went

on and was filled by successive holders.

e.g. directors (Great Western Railway

Case v Bater 1922)

5

Employment vs Office

• Employment – income includes salary,

bonus, commission etc.

• Office – major income is direct fee and

includes fringe benefits.

6

Who is an office holder?

• Trade officer

• Marketing director

• Tax director

• Director

• Chief executive officer

• Executive director

• Managing director

7

Arising In or Derived From

• Applies the Territorial Concept

• Need to Determine Hong Kong Sourced

Office, Employment and Pension

• Otherwise, Not Taxable

8

Source of Office

• Place where legal office exists

• Practical concern is where the company

is centrally managed and controlled

(McMillan V Guest, D123/02)

• Place where board of directors holds

meeting for making policy decision

• Irrespective of place of residence and

work

9

Example on Office

• A director of a Hong Kong based company draws $500,000 in 2009/2010 but never comes to Hong Kong and performs any duties.

• Is director’s fee assessable to salaries tax?

10

Pension vs Retirement Lump Sum

• Pension : a periodic payment made after retirement – with a separate source of income different from employment and office.

• Retirement Lump Sum : A lump sum payment made at the time of retirement – it is a part of employment income with the source rule of employment.

11

Source of Pension

• The source of pension is at the place where the pension fund is managed.

• If a pension fund is managed outside Hong Kong, the pension is 100% exempt from salaries tax. If a pension fund is managed in Hong Kong, only the portion of pension attributable to Hong Kong service is taxable.

12

Contract of Service vs Contract for Service

Contract of Service

• A person is under an employment

• Also referred as “being employed”

• Income chargeable under salaries tax

Contract for Service

• A person runs his own business

• Also referred as “self-employed”

• Income chargeable under profits tax

13

Tests for Distinguishing

Contract of Service and Contract for Service

• Control test

• Integration test

• Economic reality test

14

Source of Employment

• Two-tier Test :

3 factors in DIPN 10

Totality of facts approach

15

Source of Employment

• 3 Factors in DIPN 10 :

Where the contract is negotiated /

concluded / enforceable

Place of residence of employer

Where employee’s remuneration is paid

16

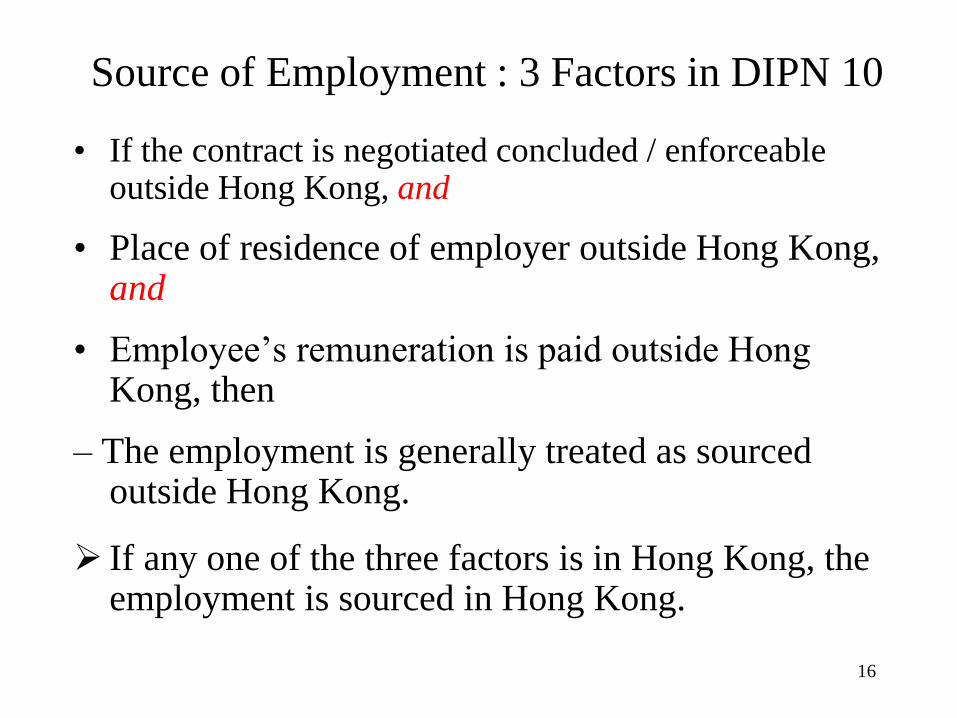

Source of Employment : 3 Factors in DIPN 10 • If the contract is negotiated concluded / enforceable

outside Hong Kong, and

• Place of residence of employer outside Hong Kong, and

• Employee’s remuneration is paid outside Hong Kong, then

– The employment is generally treated as sourced outside Hong Kong.

If any one of the three factors is in Hong Kong, the employment is sourced in Hong Kong.

17

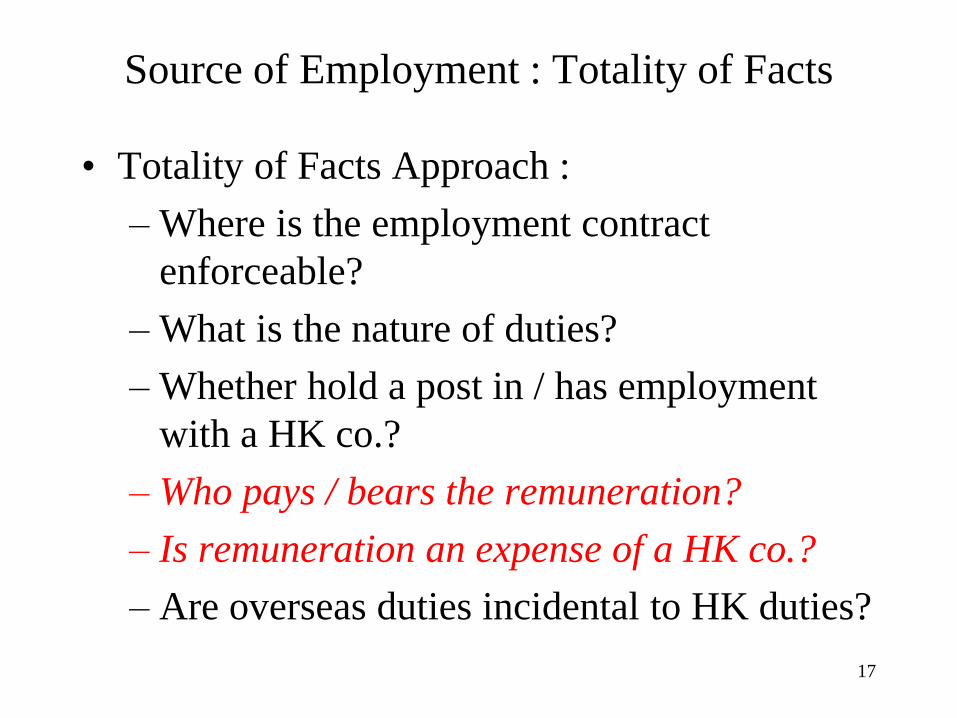

Source of Employment : Totality of Facts

• Totality of Facts Approach :

– Where is the employment contract

enforceable?

– What is the nature of duties?

– Whether hold a post in / has employment

with a HK co.?

– Who pays / bears the remuneration?

– Is remuneration an expense of a HK co.?

– Are overseas duties incidental to HK duties?

18

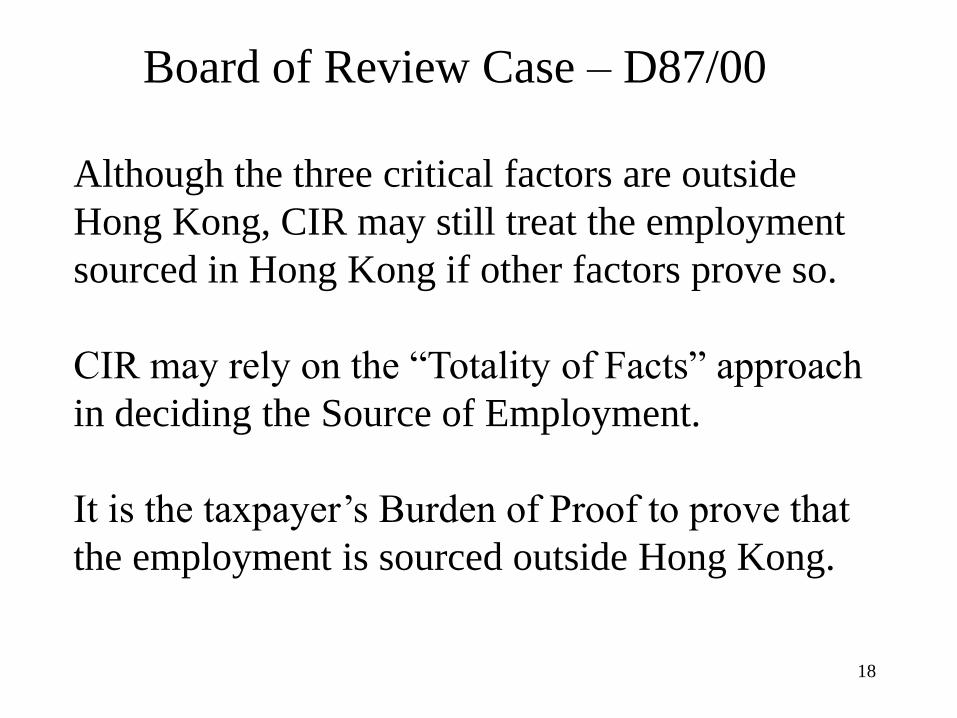

Board of Review Case – D87/00

Although the three critical factors are outside

Hong Kong, CIR may still treat the employment

sourced in Hong Kong if other factors prove so.

CIR may rely on the “Totality of Facts” approach

in deciding the Source of Employment.

It is the taxpayer’s Burden of Proof to prove that

the employment is sourced outside Hong Kong.

19

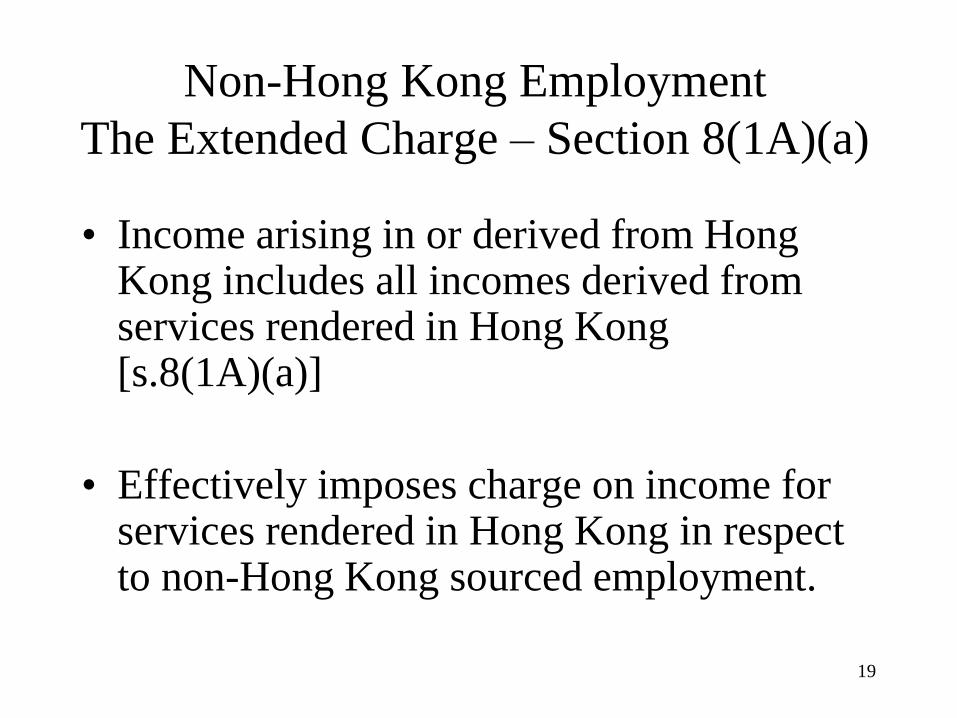

Non-Hong Kong Employment

The Extended Charge – Section 8(1A)(a)

• Income arising in or derived from Hong Kong includes all incomes derived from services rendered in Hong Kong [s.8(1A)(a)]

• Effectively imposes charge on income for services rendered in Hong Kong in respect to non-Hong Kong sourced employment.

20

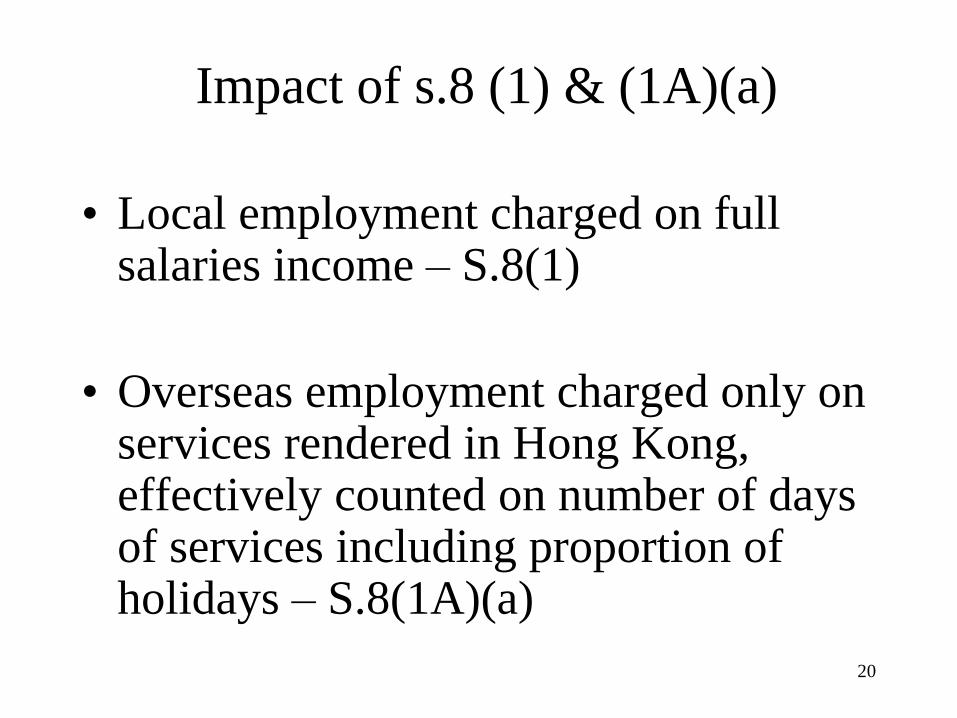

Impact of s.8 (1) & (1A)(a)

• Local employment charged on full salaries income – S.8(1)

• Overseas employment charged only on services rendered in Hong Kong, effectively counted on number of days of services including proportion of holidays – S.8(1A)(a)

21

Employment : Exemption from Salaries Tax

• when all services are rendered outside

Hong Kong, or

• 60-day rule of visit (i.e. an individual

stays in Hong Kong for 60 days or

lessin a year of assessment)

22

Visits

• Normally no permanent base in Hong

Kong

• Not with the intention to stay for work

on a continuous basis

23

Employment : Exemption from Salaries Tax

• Exemption of all services outside Hong

Kong and 60-day rule of visit NOT

APPLIED to:

• Office (i.e. director)

• Government employees

• Sailors, air crew or seafarers

24

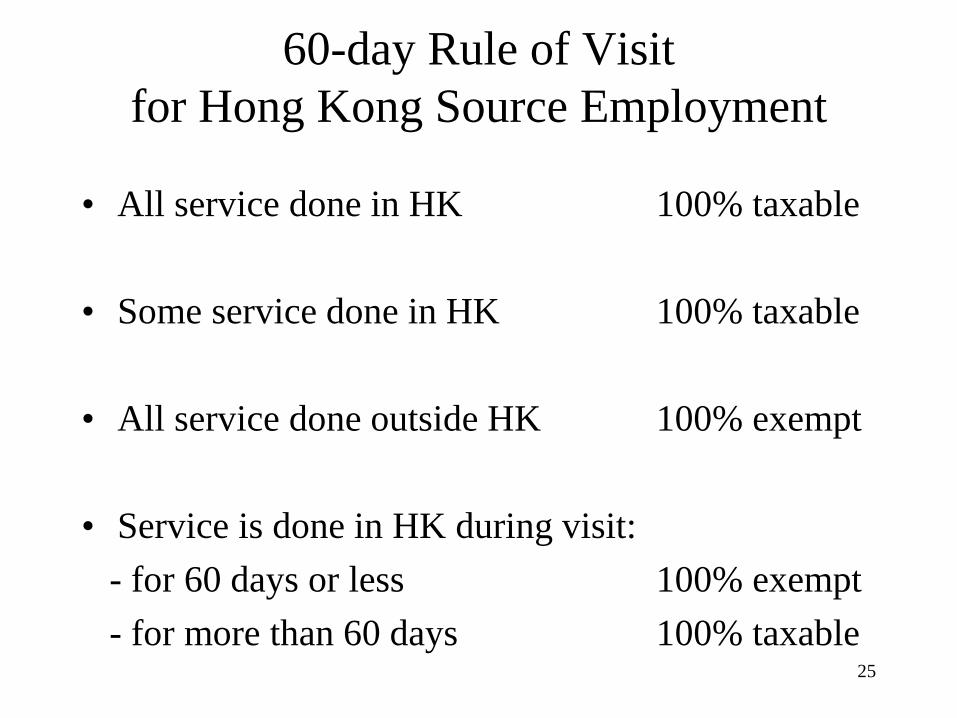

60-day Rule of Visit

Apply to both:

– Hong Kong source employment, and

– Non-Hong Kong source employment

25

60-day Rule of Visit

for Hong Kong Source Employment

• All service done in HK 100% taxable

• Some service done in HK 100% taxable

• All service done outside HK 100% exempt

• Service is done in HK during visit:

- for 60 days or less 100% exempt

- for more than 60 days 100% taxable

26

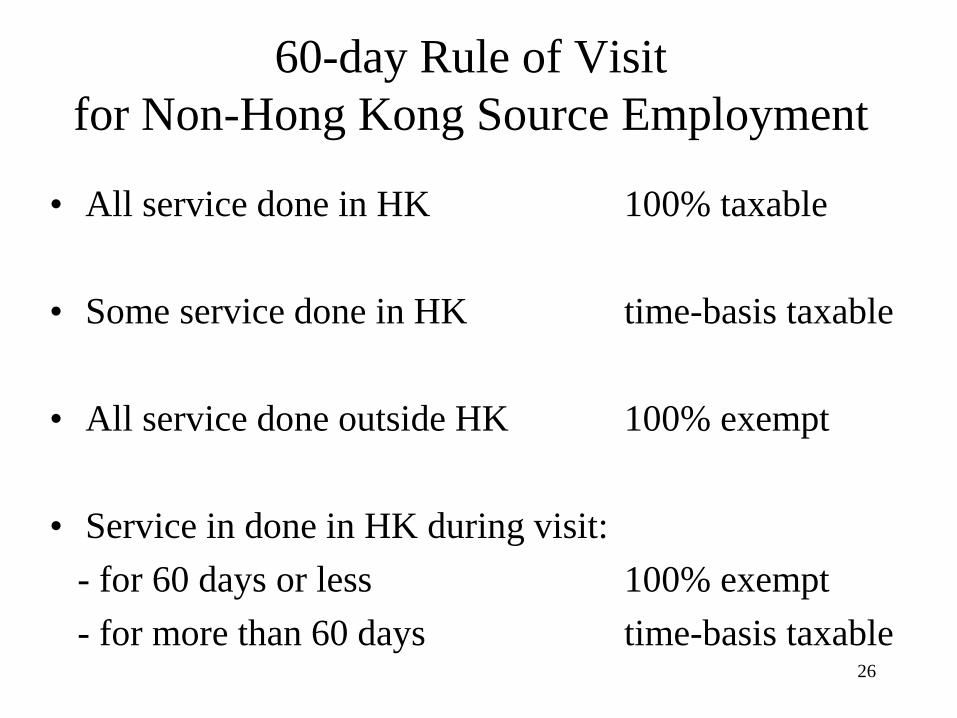

60-day Rule of Visit

for Non-Hong Kong Source Employment

• All service done in HK 100% taxable

• Some service done in HK time-basis taxable

• All service done outside HK 100% exempt

• Service in done in HK during visit:

- for 60 days or less 100% exempt

- for more than 60 days time-basis taxable

27

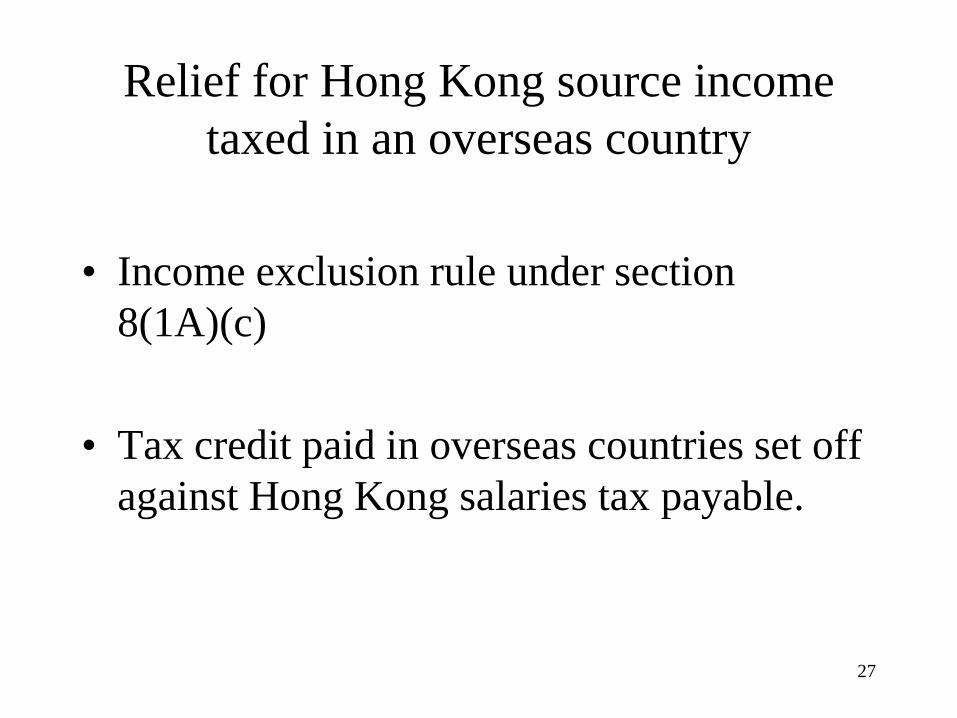

Relief for Hong Kong source income

taxed in an overseas country

• Income exclusion rule under section

8(1A)(c)

• Tax credit paid in overseas countries set off

against Hong Kong salaries tax payable.

28

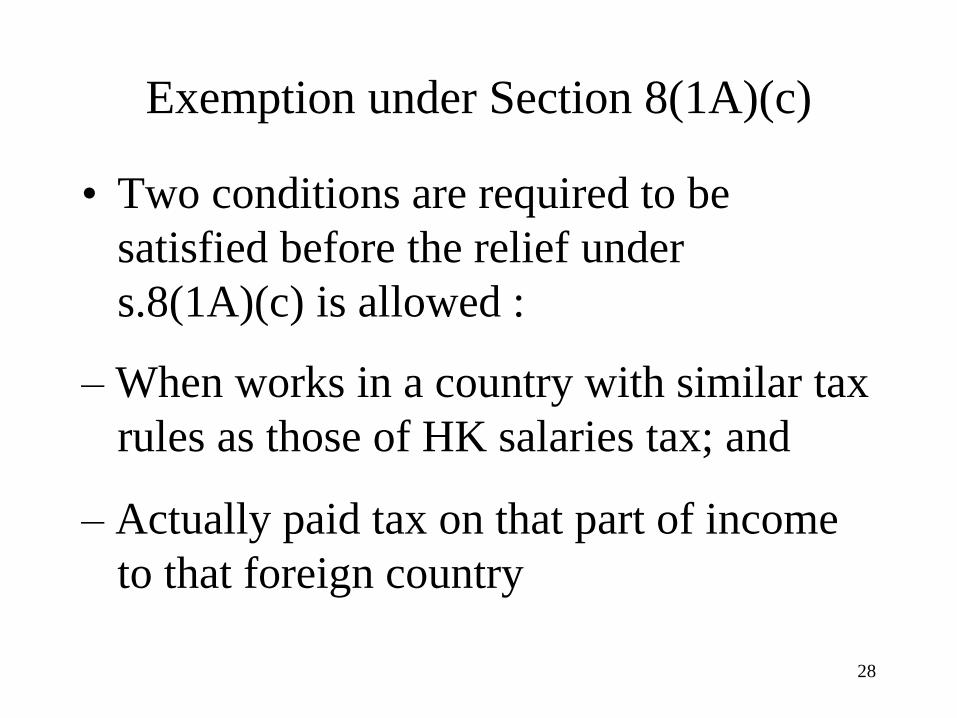

Exemption under Section 8(1A)(c)

• Two conditions are required to be

satisfied before the relief under

s.8(1A)(c) is allowed :

– When works in a country with similar tax

rules as those of HK salaries tax; and

– Actually paid tax on that part of income

to that foreign country

29

Dual Capacity

• Holds Office as well as Employment

• Divide remuneration between office

and employment

• Different rules apply

30

183-day Rule of

Anti-Double Tax Arrangement

• 183-day rule with non-residents

coming from countries or places

signed with a double taxation

arrangement with Hong Kong

31

183-day Rule of

Anti-Double Tax Arrangement

• This is different from 60-day rule of visit.

• Mainland Chinese is commonly used in examinations.

• The conditions for exemption are Mainland Chinese :

not employed by a Hong Kong company, and

staying in Hong Kong for 183 days or less in Hong

Kong in any continuous period of 12 months

commencing and ending in the year of assessment,

then, he or she is exempt from Hong Kong salaries tax.

32

183-day Rule of

Anti-Double Tax Arrangement

- Mainland Chinese stays in Hong Kong for 183 days or

less in Hong Kong in a continuous period of 12 months

commencing and ending in the year of assessment, he or

she is exempt from Hong Kong salaries tax if :

- he or she is not employed by a HK company, and

- his or her income is not finally borne by a HK company

33

Crews of Ship & Aircraft – S8(2)(j)

• Income not assessable if physical

presence in HK :

– Not more than 60 days in total in the year

of assessment, and

– Not more than 120 days in total for 2

consecutive years of assessment

34

Employment Income

Chargeable with Salaries Tax

Two Basic Principles:

• The receipt of income is derived from an

employment, and

• The income is in the consideration of

services performed in the past, present and

future.

35

Test of Income from Employment

• Is the receipt customarily expected?

• Is the receipt provided in the contract of

employment?

• Is the payment made for reasons other

than services rendered?

• Is it a gift or compensation?

36

Income Not Related to Employment

• If payment is remuneration for past,

present or future services, it is taxable.

• Voluntary payments for personal

reasons are generally not taxable.

• Compensation for loss of rights is

generally not taxable.

• A payment for agreeing to a restrictive

covenant is generally not taxable.

37

Example on Employer’s Voluntary Payment

• Employer gives an employee a lump

sum of $50,000 voluntarily in

recognition of the employee’s good

performance.

• Is this subject to salaries tax?

38

Example on Employer’s Voluntary Payment

• An employer gives a birthday gift of

$1,000 to the employee on his birthday.

• Is this subject to salaries tax?

39

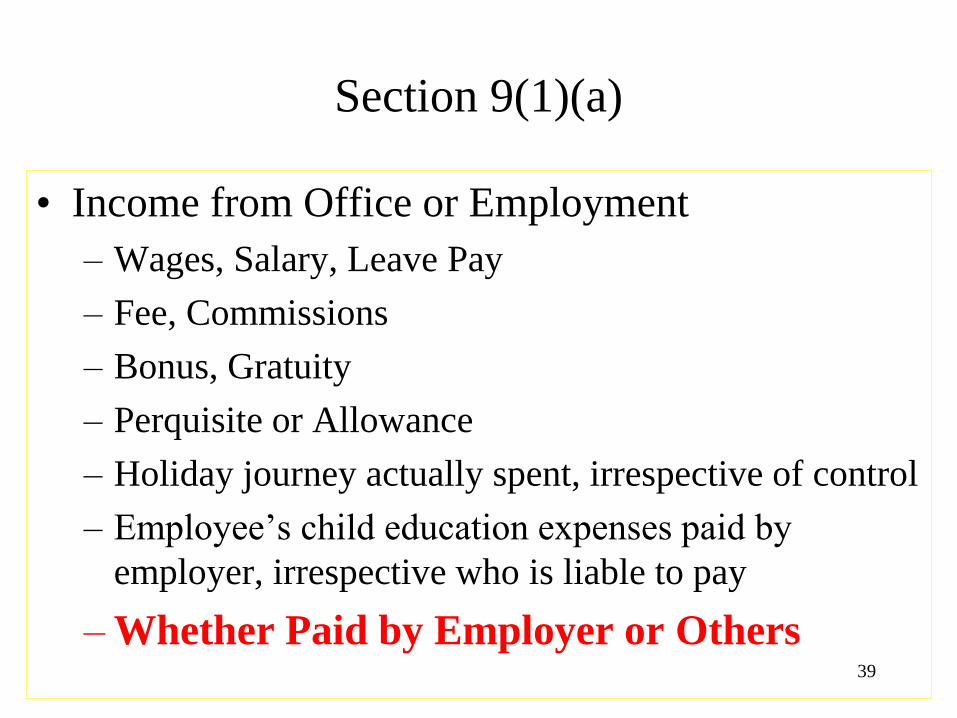

Section 9(1)(a)

• Income from Office or Employment

– Wages, Salary, Leave Pay

– Fee, Commissions

– Bonus, Gratuity

– Perquisite or Allowance

– Holiday journey actually spent, irrespective of control

– Employee’s child education expenses paid by

employer, irrespective who is liable to pay

– Whether Paid by Employer or Others

40

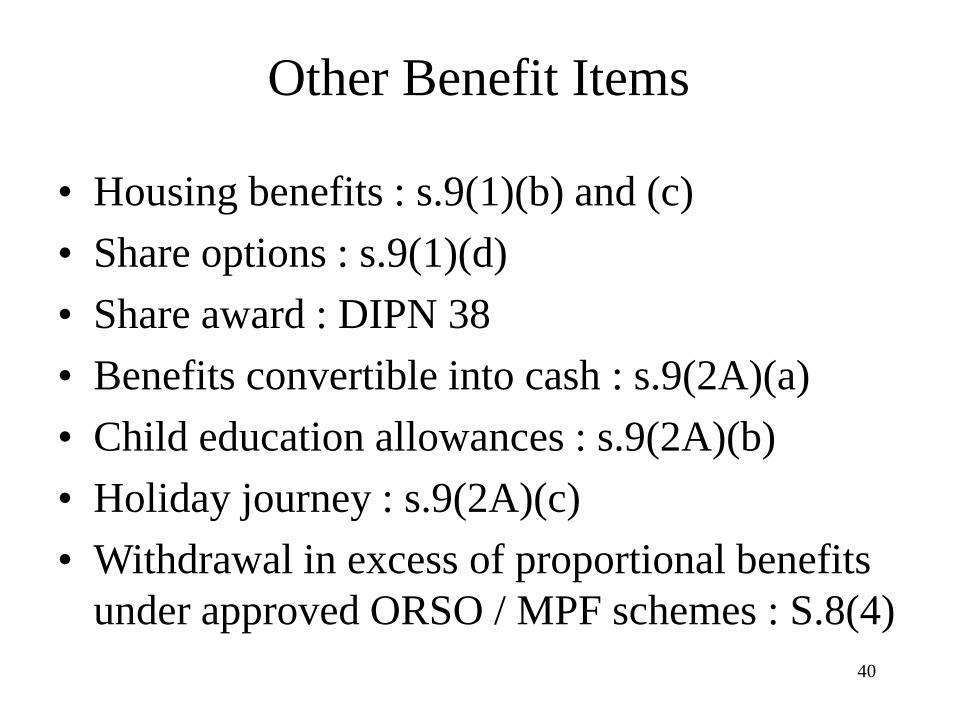

Other Benefit Items

• Housing benefits : s.9(1)(b) and (c)

• Share options : s.9(1)(d)

• Share award : DIPN 38

• Benefits convertible into cash : s.9(2A)(a)

• Child education allowances : s.9(2A)(b)

• Holiday journey : s.9(2A)(c)

• Withdrawal in excess of proportional benefits

under approved ORSO / MPF schemes : S.8(4)

41

Assessable Income

• That item of income which should be

included in the calculation of total income

for Salaries Tax purpose

• Should be the aggregate amount of income

accruing to a person from all services

42

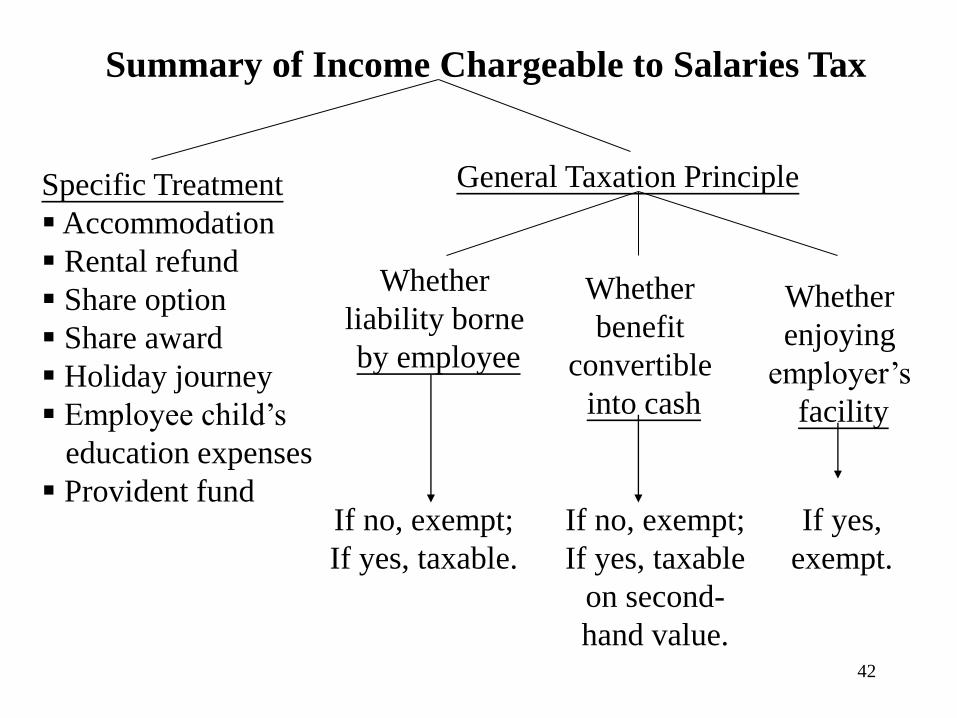

Summary of Income Chargeable to Salaries Tax

Specific Treatment

Accommodation

Rental refund

Share option

Share award

Holiday journey

Employee child’s

education expenses

Provident fund

General Taxation Principle

Whether

liability borne

by employee

Whether

benefit

convertible

into cash

Whether

enjoying

employer’s

facility

If no, exempt;

If yes, taxable.

If yes,

exempt.

If no, exempt;

If yes, taxable

on second-

hand value.

43

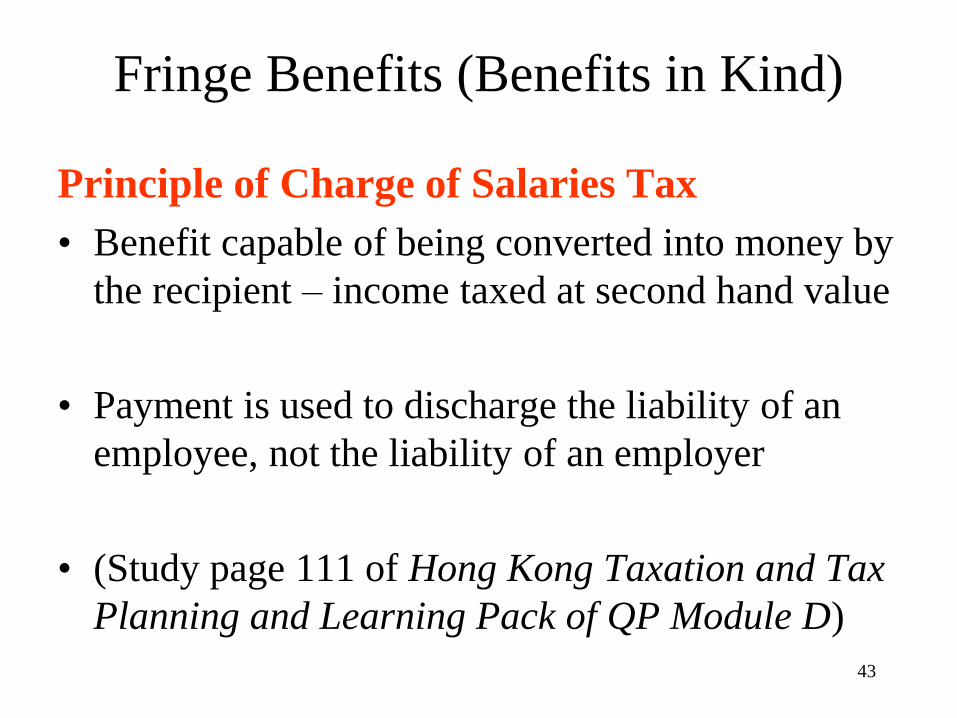

Fringe Benefits (Benefits in Kind)

Principle of Charge of Salaries Tax

• Benefit capable of being converted into money by

the recipient – income taxed at second hand value

• Payment is used to discharge the liability of an

employee, not the liability of an employer

• (Study page 111 of Hong Kong Taxation and Tax

Planning and Learning Pack of QP Module D)

44

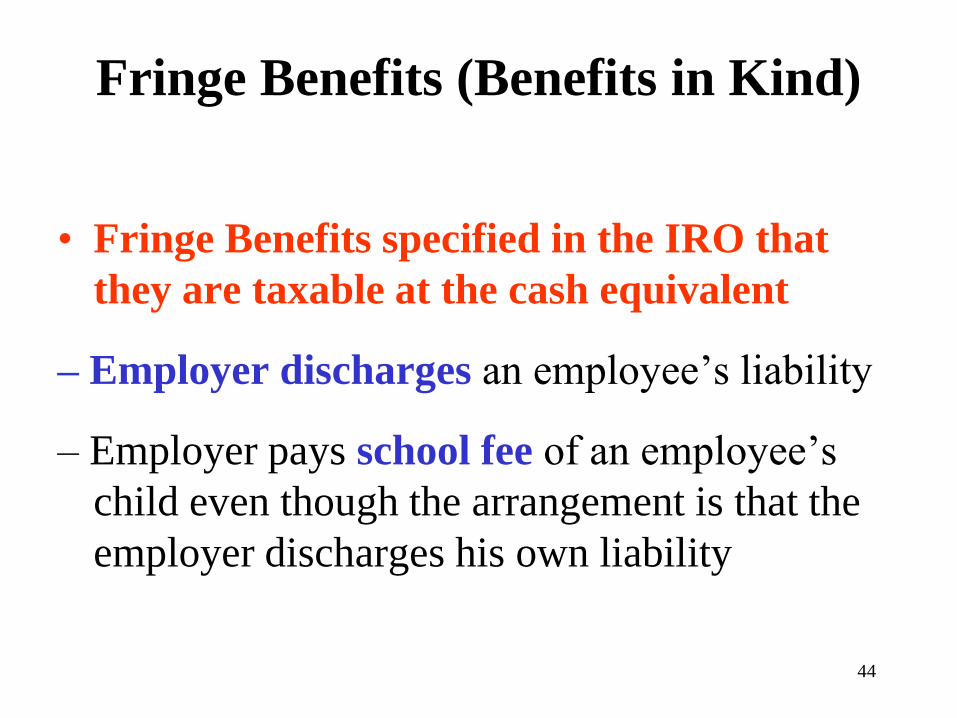

Fringe Benefits (Benefits in Kind)

• Fringe Benefits specified in the IRO that

they are taxable at the cash equivalent

– Employer discharges an employee’s liability

– Employer pays school fee of an employee’s

child even though the arrangement is that the

employer discharges his own liability

45

Fringe Benefits : Holiday Journey

• Fringe Benefits specified in the IRO that they are taxable at the cash equivalent

– Employer provides holiday journey (such as purchase of air ticket or holiday package, etc., for an employee) unless

a. the employer does not incur any additional cost in the provision of such benefit; or

b. an expatriate employee for the first time he came to Hong Kong to take up his or her post, or

c. his or her departure from Hong Kong after the employment has been terminated.

46

Section 9(1)(a)(iv)

• Payment by Employer to Third Party in discharge of Employee’s Primary Liabilities

• Identity of Liabilities is Crucial --

– If employee has no liability, not assessable

– If employee has liability or obligation to liability, assessable

47

DIPN 16 : Taxation of Fringe Benefits

For Benefits to be Included as Income

• Receipt of Cash or Cash Equivalent

• Convertible to Cash

• Discharge of Liabilities Committed by

Employee

48

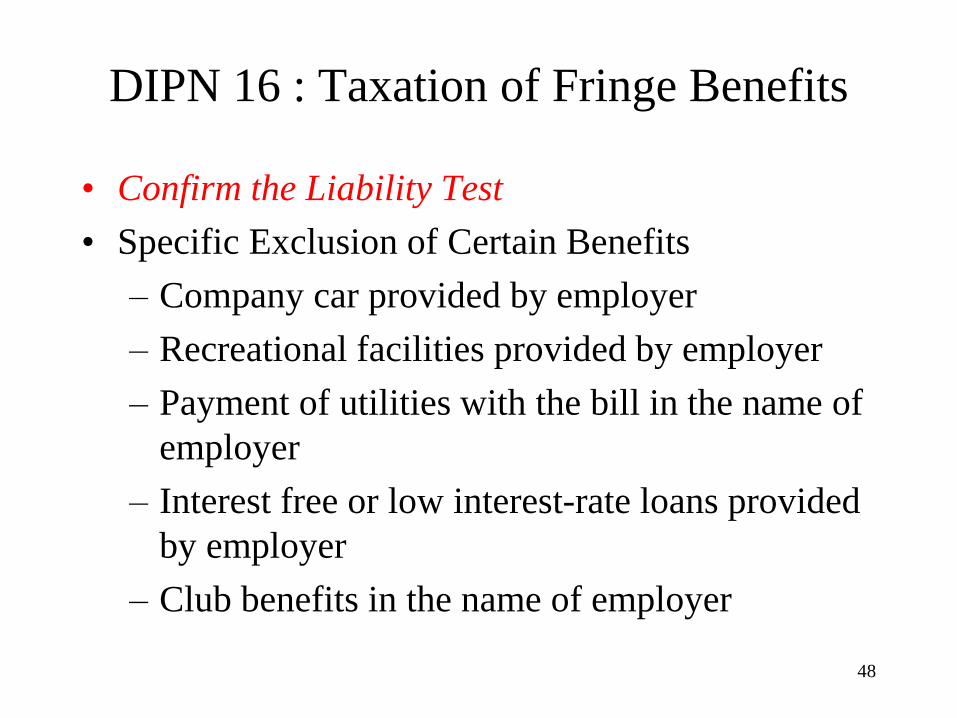

DIPN 16 : Taxation of Fringe Benefits

• Confirm the Liability Test

• Specific Exclusion of Certain Benefits

– Company car provided by employer

– Recreational facilities provided by employer

– Payment of utilities with the bill in the name of

employer

– Interest free or low interest-rate loans provided

by employer

– Club benefits in the name of employer

49

DIPN 16 : Taxation of Fringe Benefits

• Special Tax Treatment on Private Expenses Paid

with Employer’s Credit Card

• Although it is the liability of employer to settle the

monthly statements of the corporate credit card,

the benefit is chargeable to the employee’s salaries

tax liability based on Liability Test.

Reason :

• It is the employee’s primary liability to settle the

private expenses on the spot.

50

Housing Benefits

Three different kinds of housing benefits

• cash allowance / rental allowance

• provision of quarters free or at a

reduced rate

• reimbursement of rent with or without

charge to employee

51

Provision of Residence

• Section 9(1)(b)

• Residence provided rent free - calculated at

rental value as a percentage of income -

– 4% for one room in hotel or hostel

– 8% for two rooms in hotel or hostel

– 10% for other cases

• Must be private and feasible for family

accommodation

52

Excess of Rental Value

• Section 9(1)(c)

• Where residence is provided at a rent

less than the rental value

• Included as income that part of excess

of rental value

53

Reimbursement of Rent (Rental Refund)

• Where residence is provided in terms of

reimbursement of rent -

• General rule of convertibility to cash is

applied

• Sufficient Control must be exercised for

reimbursement amount

• Otherwise treated as cash receipts

54

What is Sufficient Control?

• Duly Stamped Rental Agreement –

Normally no direct relationship

• Rental terms and conditions are reasonable

• Monthly or periodic rental receipts

• Notification of changes required from

employee

• Employees’ integrity is normally assumed

55

CIR v P.L.Page (2003)

• Taxpayer contracted with employer with a term of housing reimbursement

• Employer paid the maximum amount without identifying the actual rent paid by employee

• Employee paid actual rents that were more than the capped maximum amount reimbursed by employer

56

CIR v P.L.Page (2003) (Con’t.)

• Held: the capped amount “paid back” to Page

was taxable

What did we learn?

• Terms of contract a starting point & a

weighty factor, but not the SOLE test

• Conducts of parties varied the terms of

contract

57

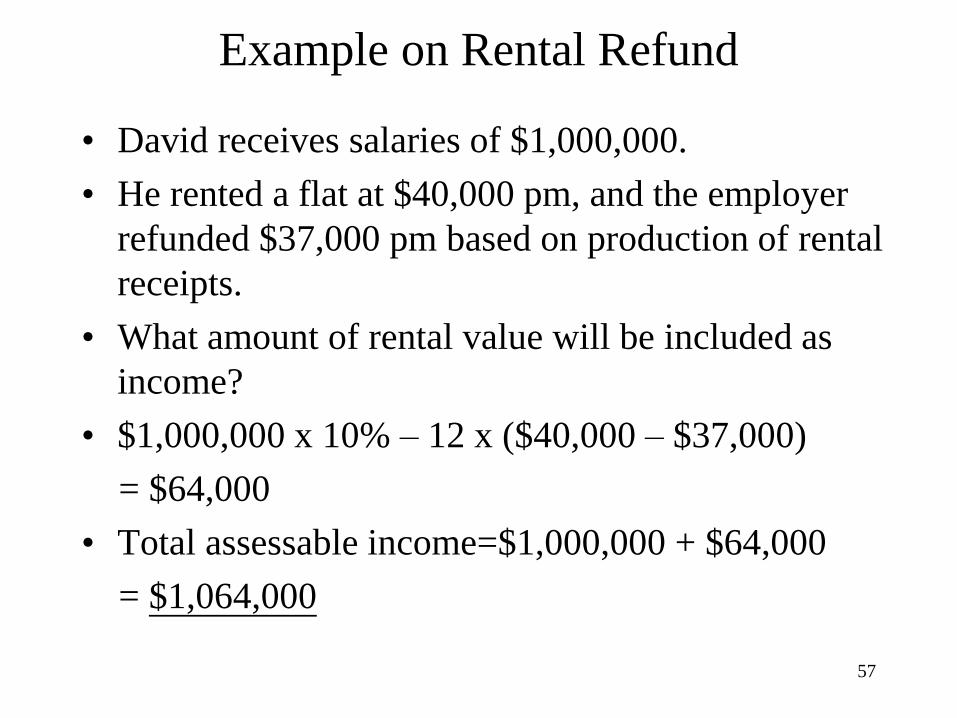

Example on Rental Refund

• David receives salaries of $1,000,000.

• He rented a flat at $40,000 pm, and the employer

refunded $37,000 pm based on production of rental

receipts.

• What amount of rental value will be included as

income?

• $1,000,000 x 10% – 12 x ($40,000 – $37,000)

= $64,000

• Total assessable income=$1,000,000 + $64,000

= $1,064,000

58

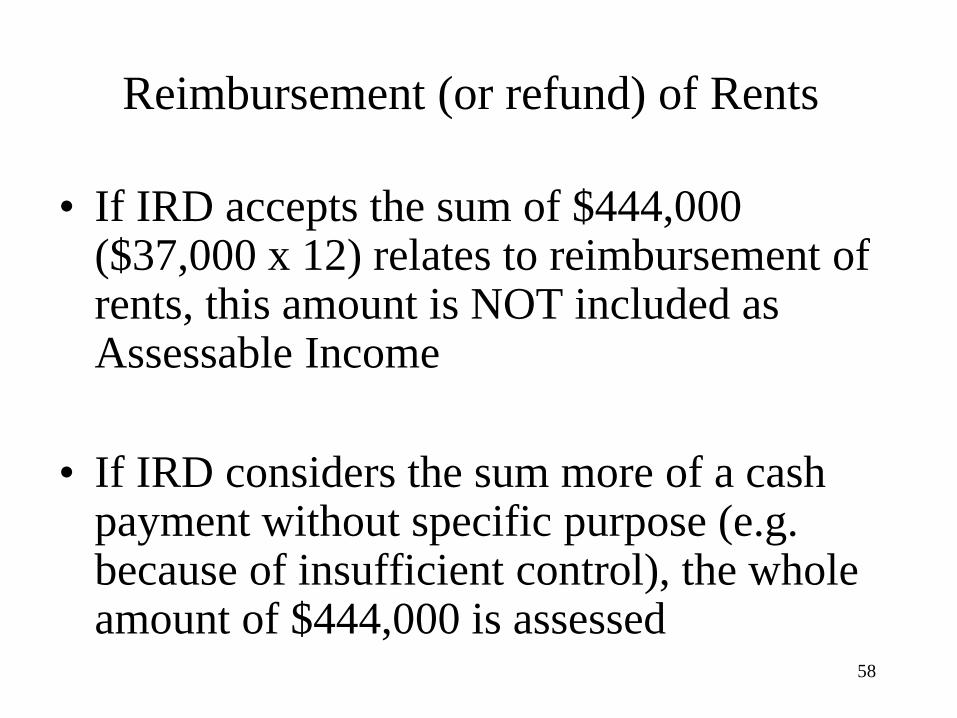

Reimbursement (or refund) of Rents

• If IRD accepts the sum of $444,000 ($37,000 x 12) relates to reimbursement of rents, this amount is NOT included as Assessable Income

• If IRD considers the sum more of a cash payment without specific purpose (e.g. because of insufficient control), the whole amount of $444,000 is assessed

59

Impact of Control on

Reimbursement of Rents

• Accept as Rental

Reimbursement:

• Salaries $1,000,000

• Rent Reimbursement

$444,000

• Total Assessable

Income $1,064,000

• View as Cash

Payment:

• Same data as in the left

hand side

• Total Assessable

Income :

• $1,000,000 + $444,000

• =$1,444,000

60

Different Tax Liabilities

with Same Gross Income

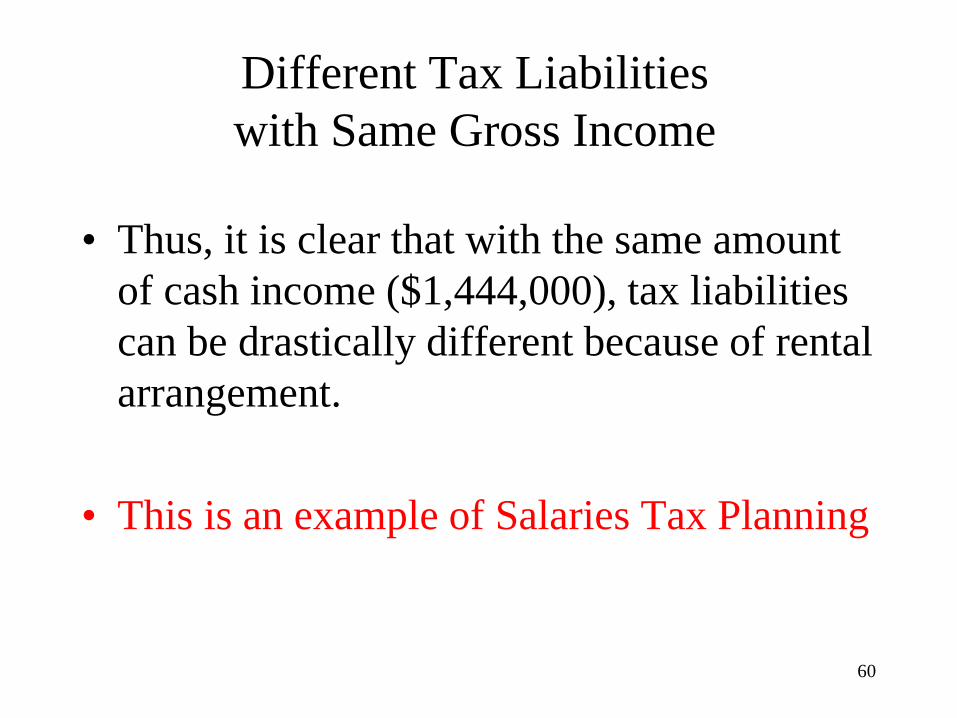

• Thus, it is clear that with the same amount

of cash income ($1,444,000), tax liabilities

can be drastically different because of rental

arrangement.

• This is an example of Salaries Tax Planning

61

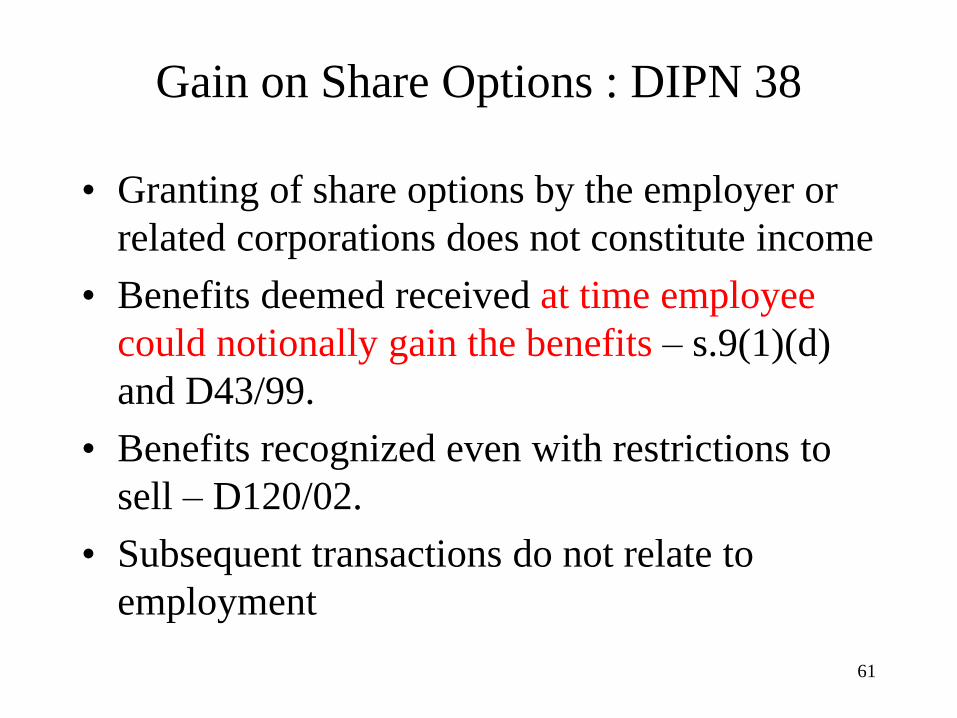

Gain on Share Options : DIPN 38

• Granting of share options by the employer or

related corporations does not constitute income

• Benefits deemed received at time employee

could notionally gain the benefits – s.9(1)(d)

and D43/99.

• Benefits recognized even with restrictions to

sell – D120/02.

• Subsequent transactions do not relate to

employment

62

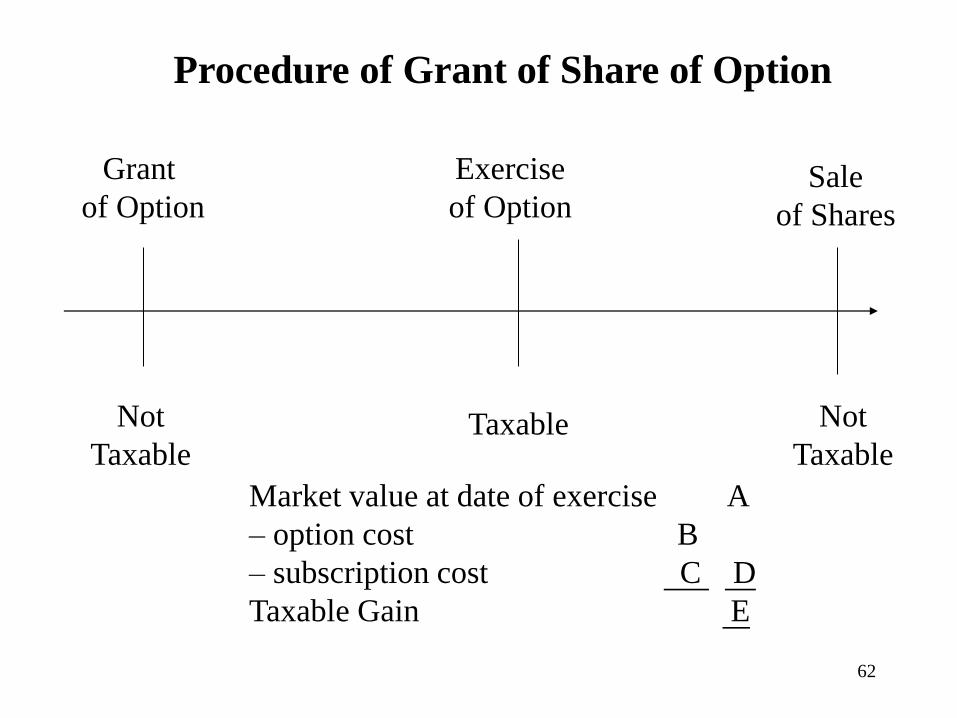

Grant

of Option

Exercise

of Option Sale

of Shares

Procedure of Grant of Share of Option

Not

Taxable Taxable Not

Taxable

Market value at date of exercise A

– option cost B

– subscription cost C D

Taxable Gain E

63

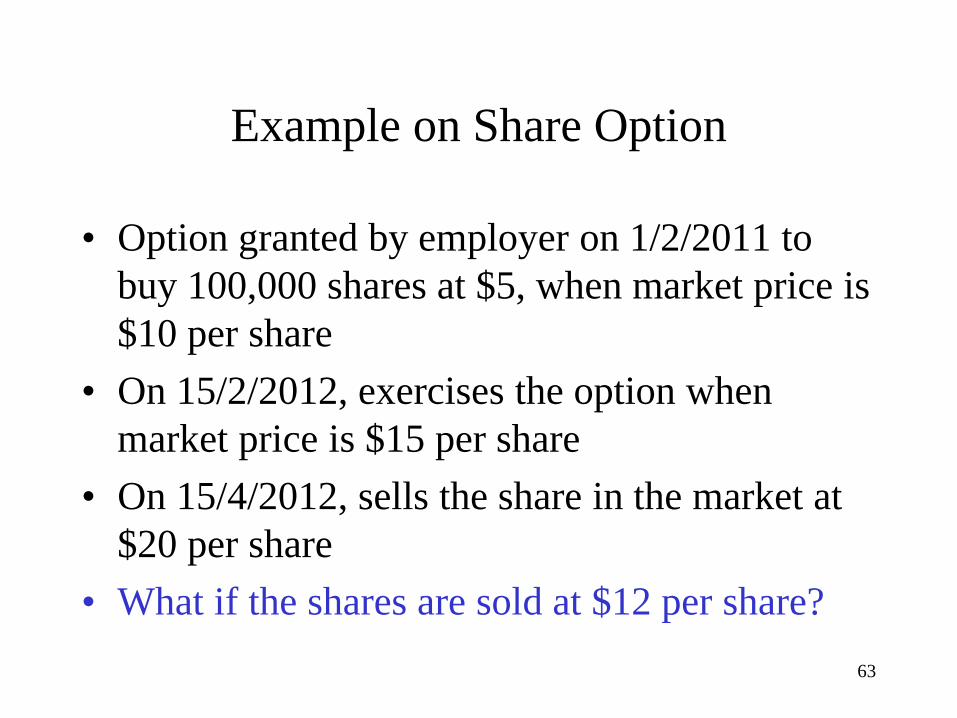

Example on Share Option

• Option granted by employer on 1/2/2011 to

buy 100,000 shares at $5, when market price is

$10 per share

• On 15/2/2012, exercises the option when

market price is $15 per share

• On 15/4/2012, sells the share in the market at

$20 per share

• What if the shares are sold at $12 per share?

64

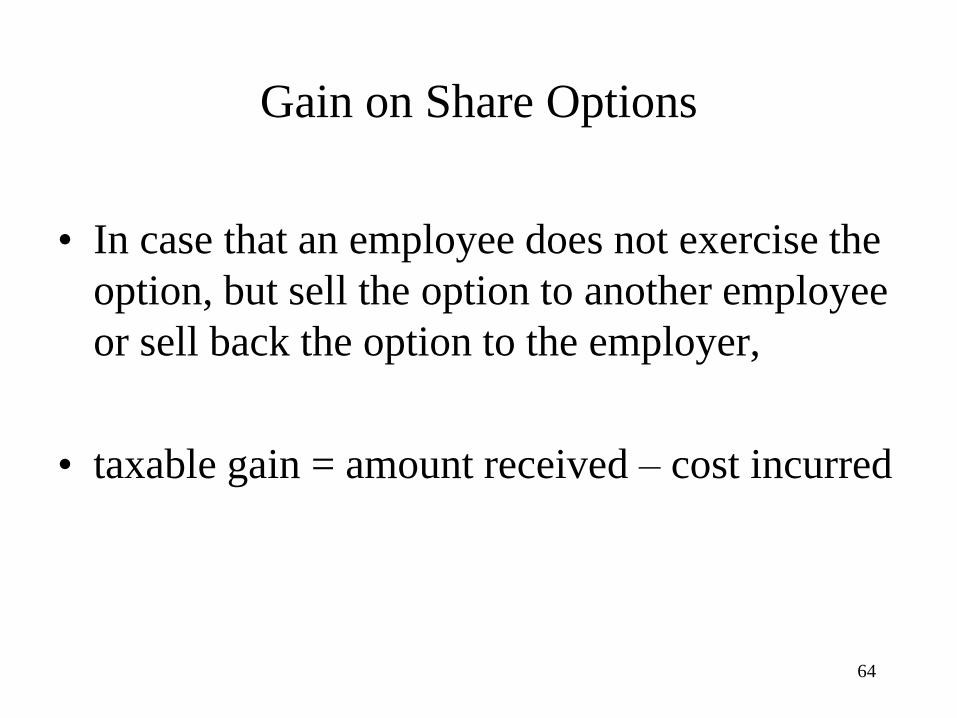

Gain on Share Options

• In case that an employee does not exercise the

option, but sell the option to another employee

or sell back the option to the employer,

• taxable gain = amount received – cost incurred

65

Valuation of Shares

Reference to :

• Open market value

• Restrictions on sale

• Quoted shares

• “Slump effect”

• Brokerage, stamp duty or other charges

• Unquoted shares

66

Share Option : Restrictions on Sale of Shares

• Share options are sometimes granted on the

condition that restrictions will apply in

relation to the disposal of any shares

acquired under the scheme (e.g. as to when

or to whom the shares can be sold).

• The restriction on disposal of the shares are

relevant in determining the amount “which

a person might reasonably expect to obtain

from a sale in the open market”.

67

Share Option : Restrictions on Sale of Shares

• This is a valuation exercise to be undertaken

in the light of the facts of each particular

case.

• See for example, D120/02, IRBRD vol. 18,

125, where a 25% discount was allowed to

reflect the five year restriction period

against alienation of the shares.

68

Valuation of Quoted Shares

• Where the shares are listed on a stock

exchange,

• the open market value of the shares

acquired can be taken as the closing

quotation value for shares of the same kind

on the date the option is exercised.

69

Valuation of Quoted Shares : Slump Effect

• In practice, the Department will consider a request

for downward adjustment of the quoted value if

there is evidence to suggest that,

• because of the number involved, a sale of the

shares obtained from exercising the option would

only be possible at a reduced price,

• i.e. a “slump effect” would be induced if the shares

in question were to be made available for sale.

• This practice reflects the decision of the Board of

Review in case D46/95, IRBRD, vol. 10, 308.

70

Shares Listed in HK and Overseas

• If the shares are listed in Hong Kong and

overseas at the same time, it is normal

practice for the Department to adopt the

price quoted on the Hong Kong Stock

Exchange.

• If the shares are listed on two non-Hong

Kong exchanges, the taxpayer may select

the more favourable price.

71

Notional Expenses For Quoted Shares

• Once the open market value of the shares is

ascertained, it is accepted that any

brokerage,

stamp duty or

other charges

• that would have been levied if the notional

sale had actually taken place.

72

Unquoted Shares

• For unquoted shares, if it is not possible to

say that for all such companies there is a

single valuation method, e.g. reference to;

• “dividend yield”,

• “earnings yield” or

• “asset backing”.

73

DIPN 38 : Example 1

• The taxpayer had a Hong Kong employment.

He was granted an unconditional right to

subscribe for shares. He ceased employment

and exercised his option after cessation of

employment.

74

Answer to DIPN 38 : Example 1

• Cessation of employment does not prevent the application of the share option provisions. As the taxpayer concerned had a Hong Kong employment at the time of grant of the right, the relevant income was derived from Hong Kong and accordingly is chargeable to Salaries Tax in the year of assessment in which the right is exercised.

• This approach has been endorsed in CIR v. Sawhney, Subhash Chander, HCIA 1/2006.

75

DIPN 38 : Example 2

• The taxpayer had a Hong Kong employment.

All services were rendered in Hong Kong

prior to and during the year the unconditional

grant of the right was granted to him.

• During the year of assessment in which the

right was exercised, the taxpayer rendered all

services outside Hong Kong in connection

with the same employment.

76

Answer to DIPN 38 : Example 2

• As the taxpayer had a Hong Kong employment, the gain would be treated as having been derived from Hong Kong.

• The gain would only be excluded from the charge to Salaries Tax by virtue of section 8(1A)(b)(ii), taking into account section 8(1B), if all services were rendered outside Hong Kong in the year of grant of the right.

77

Answer to DIPN 38 : Example 2 (Con’t.)

• The gain, calculated in accordance with section 9(4), would fall for assessment in the year of assessment in which the right was exercised.

• The fact that the taxpayer did not render any services in Hong Kong during the year of exercise would not in itself have any bearing on whether the gain would be chargeable to Salaries Tax, see D4/02, IRBRD, vol. 17, 400.

78

DIPN 38 : Example 3

• The taxpayer had a Hong Kong employment.

All services were rendered outside Hong

Kong in the year of assessment in which the

right was unconditionally granted, but

rendered inside Hong Kong during the year

of assessment in which the right was

exercised.

79

Answer to DIPN 38 : Example 3

• As the taxpayer rendered all services outside Hong Kong during the year of assessment in which the right was granted, and as it was granted on an unconditional basis which did not involve services being rendered in Hong Kong, it would be accepted that the gain on realization should qualify for exemption by virtue of section 8(1A)(b)(ii), taking into account section 8(1B), notwithstanding the fact that the taxpayer was rendering services in Hong Kong during the year in which the right was actually exercised.

80

DIPN 38 : Example 4

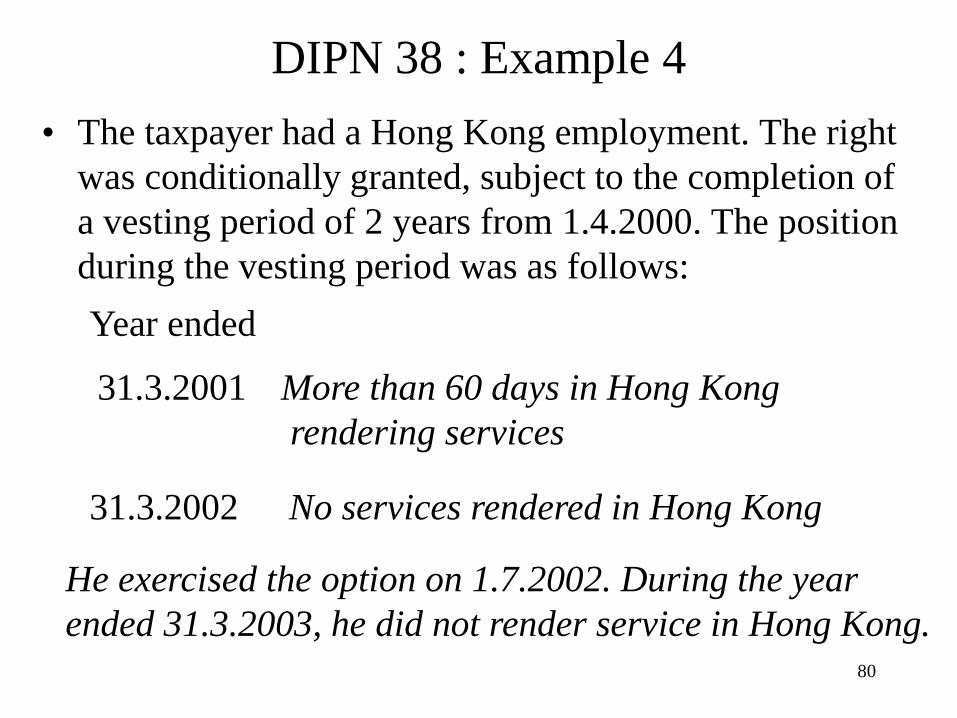

• The taxpayer had a Hong Kong employment. The right

was conditionally granted, subject to the completion of

a vesting period of 2 years from 1.4.2000. The position

during the vesting period was as follows:

Year ended

31.3.2001

31.3.2002

More than 60 days in Hong Kong

rendering services

No services rendered in Hong Kong

He exercised the option on 1.7.2002. During the year

ended 31.3.2003, he did not render service in Hong Kong.

81

Answer to DIPN 38 : Example 4

• The chargeability of any gain on exercise would not hinge on where (or if) the taxpayer was rendering services in the year of assessment in which the right was exercised.

• For a Hong Kong employment case, income can only be excluded from the charge to Salaries Tax if the taxpayer renders outside Hong Kong all the services in connection with his employment (taking into account the 60 days allowance provided under section 8(1B)).

82

Answer to DIPN 38 : Example 4 (Con’t.)

• Accordingly, having regard to the latter point in the previous paragraph, if during any year of assessment included in the vesting period, the taxpayer rendered services in Hong Kong during visits exceeding 60 days, all of the gain from the exercise of the option would be chargeable to Salaries Tax.

• On the other hand, if during each such year the taxpayer’s visits did not exceed a total of 60 days, no part of the gain would be treated as chargeable (section 8(1A)(b)(ii) and (1B) would apply).

83

Non-Hong Kong Employment

• Where a person has a non-Hong Kong employment at the time of grant, the gain will have a non-Hong Kong source and will not be chargeable to Salaries Tax unless it is derived from services rendered in Hong Kong.

• IRD will generally accept that no liability to Salaries Tax arises where a right is granted on an unconditional basis (or on completion of a vesting period of a conditional grant) prior to a person rendering any services in Hong Kong, notwithstanding that the right may be exercised after the person commences to render such services.

84

Non-Hong Kong Employment (Con’t.)

• Where a person with a non-Hong Kong

employment is granted the right subject to a

vesting period during which services are

rendered both in and outside Hong Kong,

• the gain can be partly attributed to services

in Hong Kong, the benefit should to some

extent be chargeable to Salaries Tax.

85

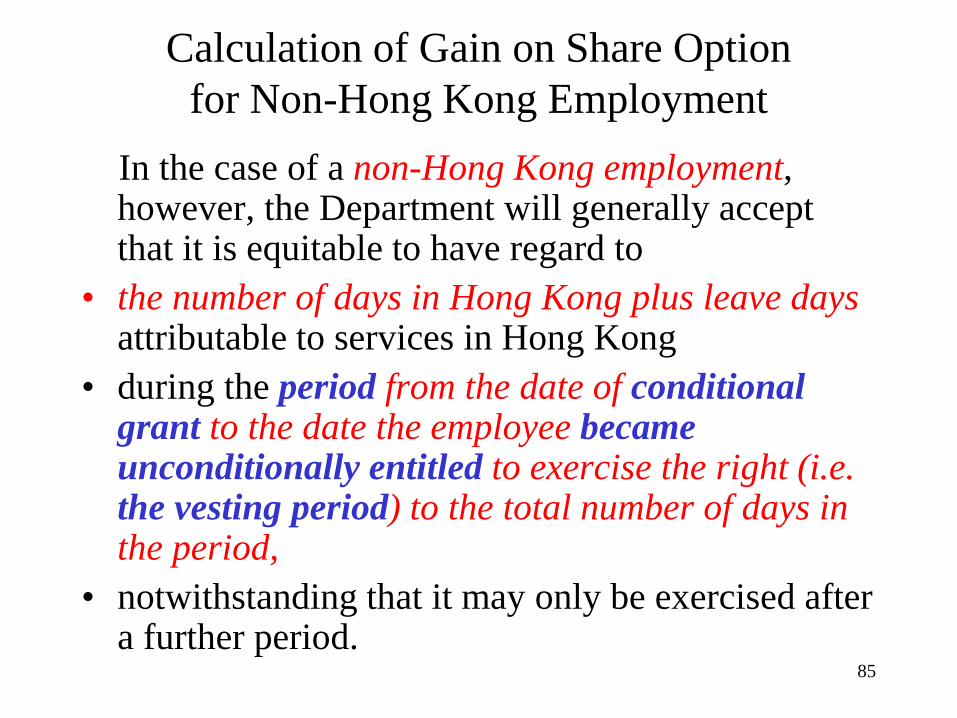

Calculation of Gain on Share Option

for Non-Hong Kong Employment

In the case of a non-Hong Kong employment, however, the Department will generally accept that it is equitable to have regard to

• the number of days in Hong Kong plus leave days attributable to services in Hong Kong

• during the period from the date of conditional grant to the date the employee became unconditionally entitled to exercise the right (i.e. the vesting period) to the total number of days in the period,

• notwithstanding that it may only be exercised after a further period.

86

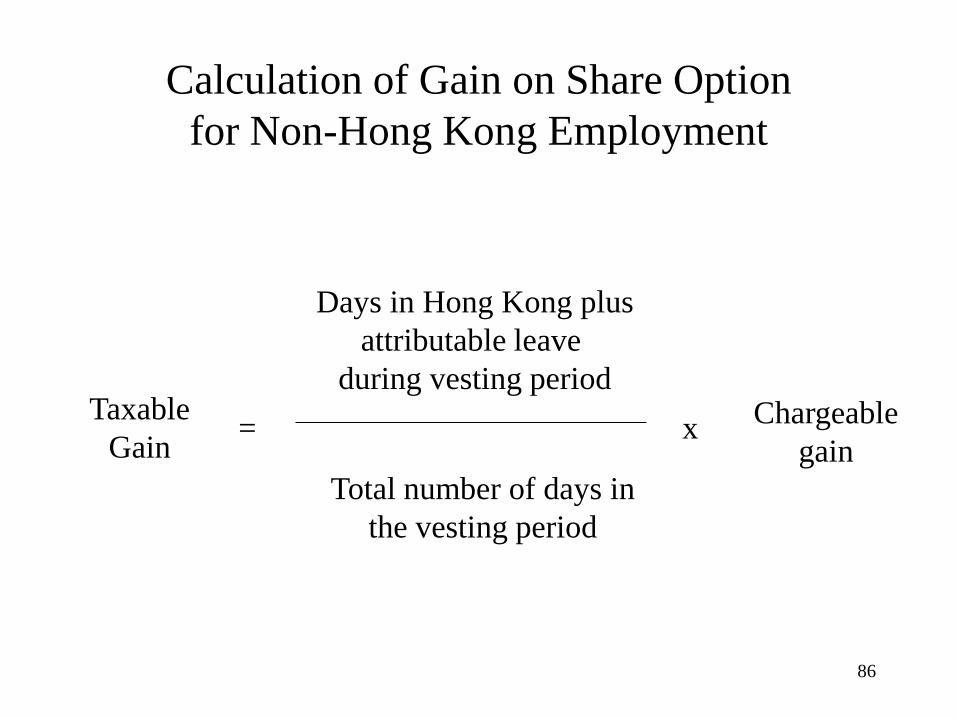

Calculation of Gain on Share Option

for Non-Hong Kong Employment

Taxable

Gain =

Days in Hong Kong plus

attributable leave

during vesting period

Total number of days in

the vesting period

x Chargeable

gain

87

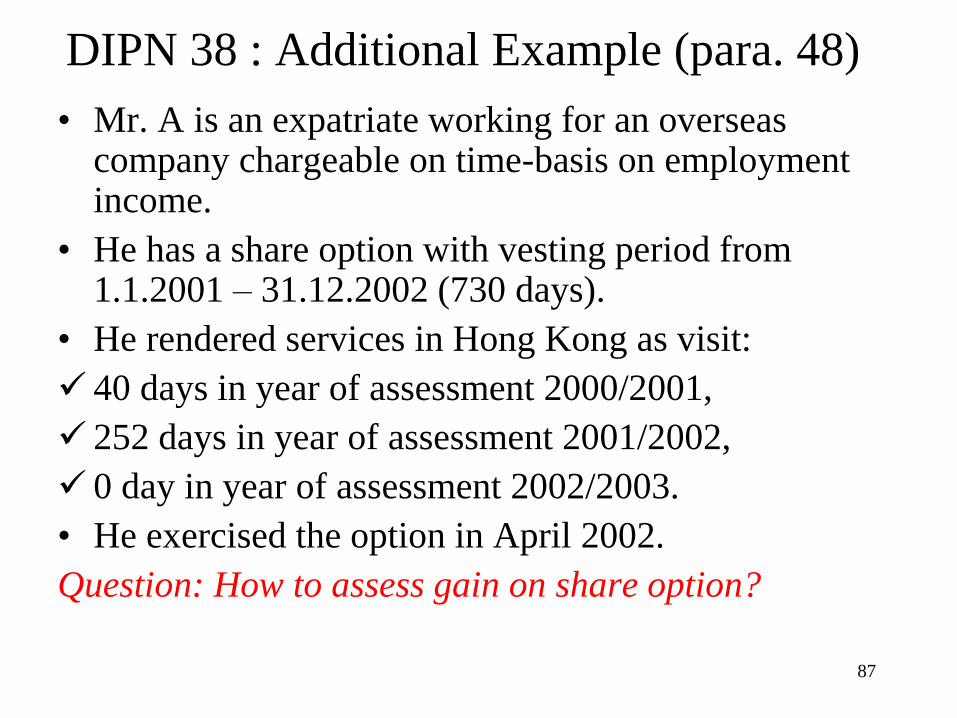

DIPN 38 : Additional Example (para. 48)

• Mr. A is an expatriate working for an overseas company chargeable on time-basis on employment income.

• He has a share option with vesting period from 1.1.2001 – 31.12.2002 (730 days).

• He rendered services in Hong Kong as visit:

40 days in year of assessment 2000/2001,

252 days in year of assessment 2001/2002,

0 day in year of assessment 2002/2003.

• He exercised the option in April 2002.

Question: How to assess gain on share option?

88

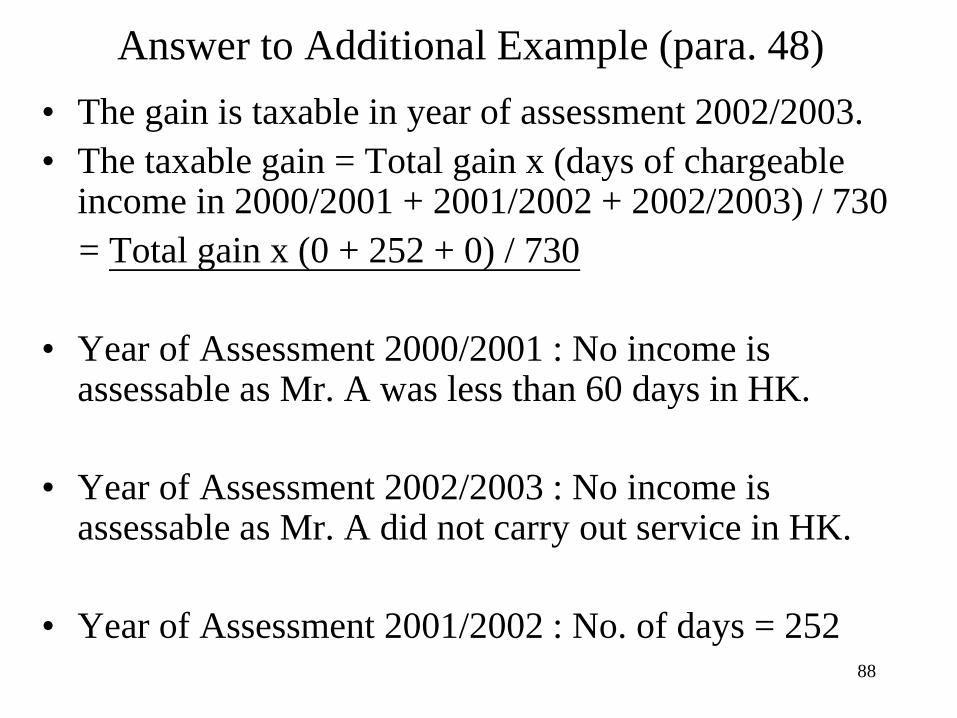

Answer to Additional Example (para. 48)

• The gain is taxable in year of assessment 2002/2003.

• The taxable gain = Total gain x (days of chargeable income in 2000/2001 + 2001/2002 + 2002/2003) / 730

= Total gain x (0 + 252 + 0) / 730

• Year of Assessment 2000/2001 : No income is assessable as Mr. A was less than 60 days in HK.

• Year of Assessment 2002/2003 : No income is assessable as Mr. A did not carry out service in HK.

• Year of Assessment 2001/2002 : No. of days = 252

89

DIPN 38 : Example 5

• The taxpayer had a non-Hong Kong

employment.

• All services were rendered outside Hong

Kong in the year of assessment in which the

right was unconditionally granted,

• but rendered inside Hong Kong during the

year of assessment in which the right was

exercised.

90

Answer to DIPN 38 : Example 5

• As the taxpayer rendered all services outside Hong Kong during the year of assessment in which the right was granted, and

• as it was granted on an unconditional basis that did not involve services being rendered in Hong Kong,

• the right would accordingly be recognised as having been derived from services rendered outside Hong Kong.

• As such, the gain on exercise of the right would not be chargeable to Salaries Tax.

91

DIPN 38 : Example 6

• The taxpayer had a non-Hong Kong employment.

• All services were rendered in Hong Kong during the year of assessment in which the right was unconditionally granted,

• but during the year of assessment in which the right was exercised, the taxpayer rendered all services in connection with the employment outside Hong Kong.

92

Answer to DIPN 38 : Example 6

• As the taxpayer rendered all services in

connection with the employment in Hong

Kong during the year of assessment in which

the right was granted, and as it was granted

on an unconditional basis which did not

involve services being rendered outside Hong

Kong,

• the gain on exercise would be fully

chargeable to Salaries Tax in the year of

exercise of share option.

93

DIPN 38 : Example 7

• The taxpayer had a non-Hong Kong

employment.

• Services were rendered inside and outside

Hong Kong :

during the year of assessment in which the

right was unconditionally granted and

during the year in which it was exercised.

94

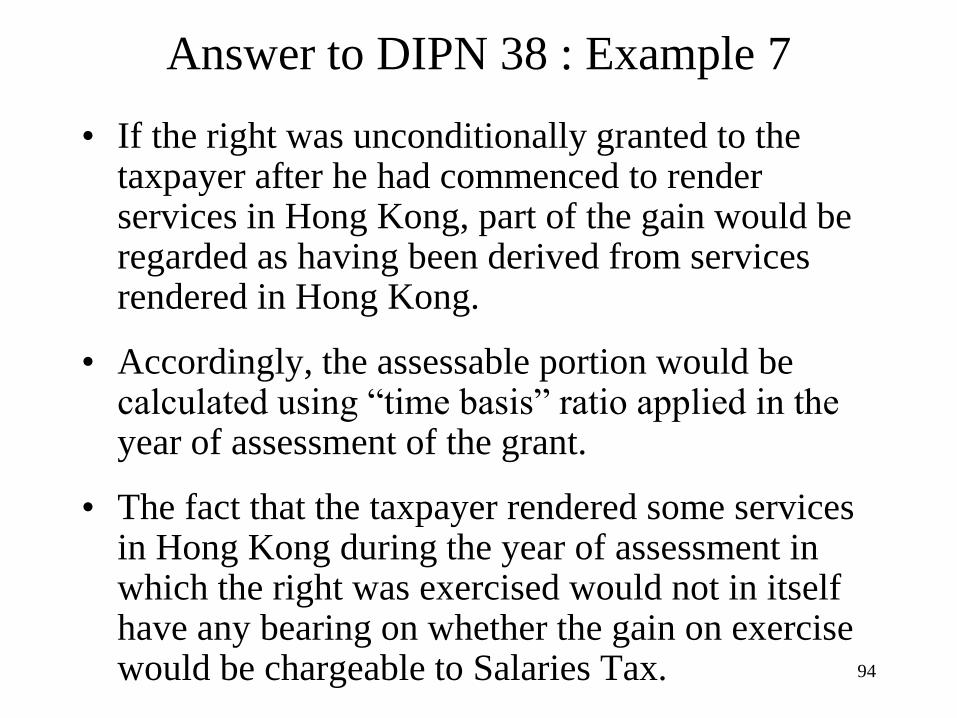

Answer to DIPN 38 : Example 7

• If the right was unconditionally granted to the taxpayer after he had commenced to render services in Hong Kong, part of the gain would be regarded as having been derived from services rendered in Hong Kong.

• Accordingly, the assessable portion would be calculated using “time basis” ratio applied in the year of assessment of the grant.

• The fact that the taxpayer rendered some services in Hong Kong during the year of assessment in which the right was exercised would not in itself have any bearing on whether the gain on exercise would be chargeable to Salaries Tax.

95

DIPN 38 : Example 8

• The taxpayer had a non-Hong Kong

employment.

• The right was conditionally granted subject to

the completion of a vesting period during

which services were rendered partly inside

and partly outside Hong Kong.

96

Answer to DIPN 38 : Example 8

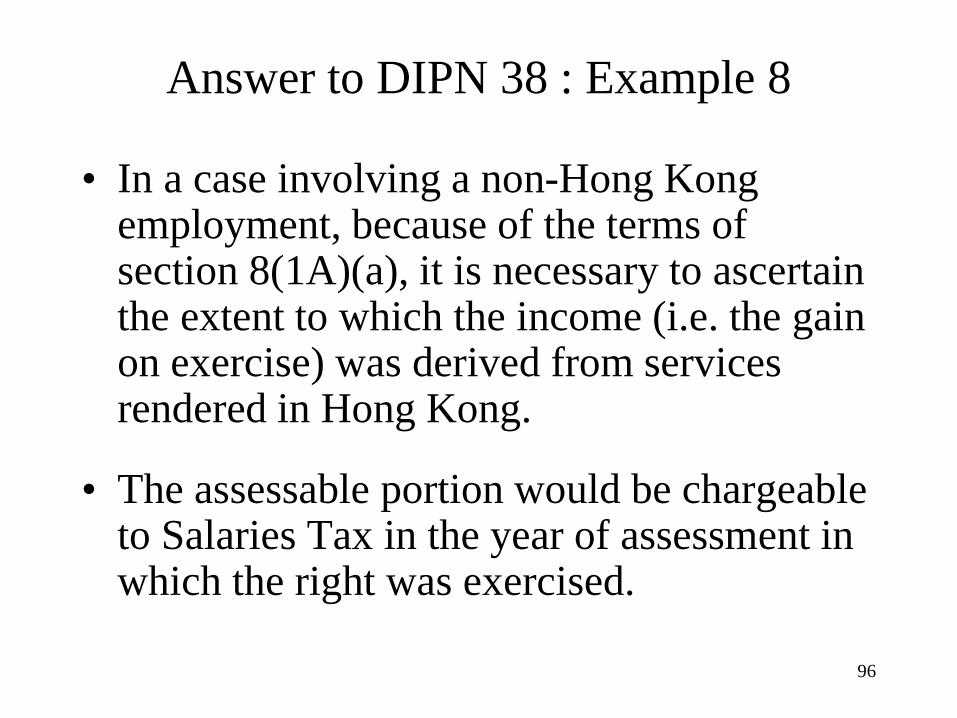

• In a case involving a non-Hong Kong employment, because of the terms of section 8(1A)(a), it is necessary to ascertain the extent to which the income (i.e. the gain on exercise) was derived from services rendered in Hong Kong.

• The assessable portion would be chargeable to Salaries Tax in the year of assessment in which the right was exercised.

97

DIPN 38 : Example 9

• The taxpayer had a non-Hong Kong employment at the time when the option was conditionally granted subject to the completion of a vesting period during which the taxpayer’s employment was changed to a Hong Kong employment within the same group of companies.

• Issue: How to handle changes from Hong Kong to non-Hong Kong employment or vice versa during vesting period

98

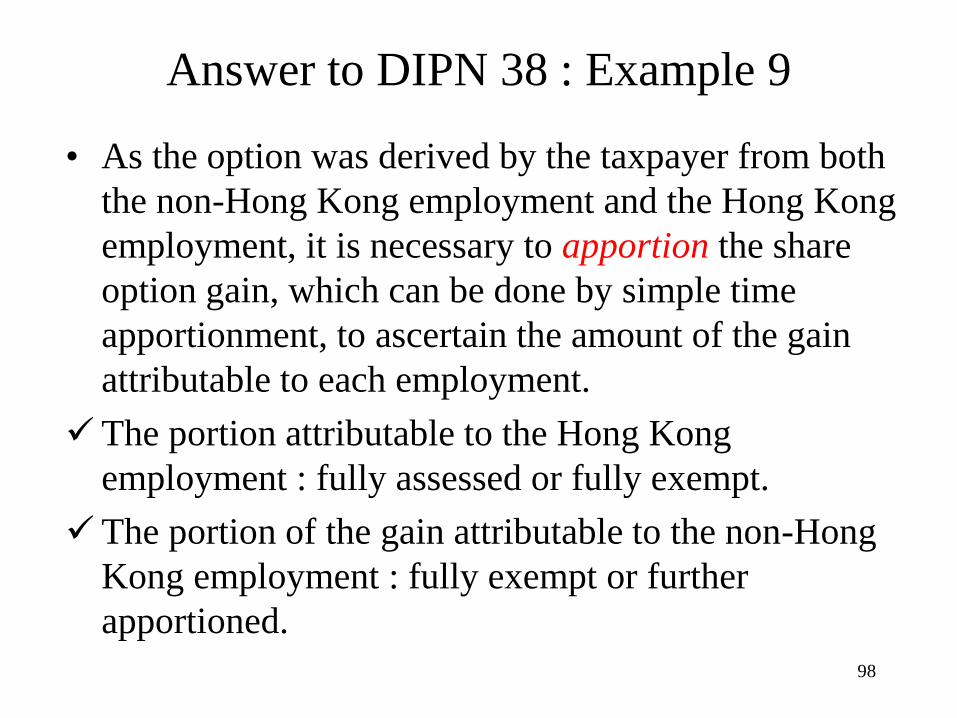

Answer to DIPN 38 : Example 9

• As the option was derived by the taxpayer from both

the non-Hong Kong employment and the Hong Kong

employment, it is necessary to apportion the share

option gain, which can be done by simple time

apportionment, to ascertain the amount of the gain

attributable to each employment.

The portion attributable to the Hong Kong

employment : fully assessed or fully exempt.

The portion of the gain attributable to the non-Hong

Kong employment : fully exempt or further

apportioned.

99

Share Award

While share or stock award plans vary in

details, the points which need to be

addressed are –

• When does the perquisite accrue to the

employee?

• What value should be attached to the

perquisite when it has accrued to the

employee?

100

When Share Award Taxable?

• The first question can be considered in the light of

section 11D(b) of the Ordinance, which provides

that income accrues to a person when he becomes

entitled to claim payment.

• While this section uses the term “entitled to claim

payment”, in the situation of share award, this

phrase is taken to mean “entitled to ownership of

the shares”.

101

Types of Share Award

• Upfront approach

• Back-end approach

• Phantom share scheme

102

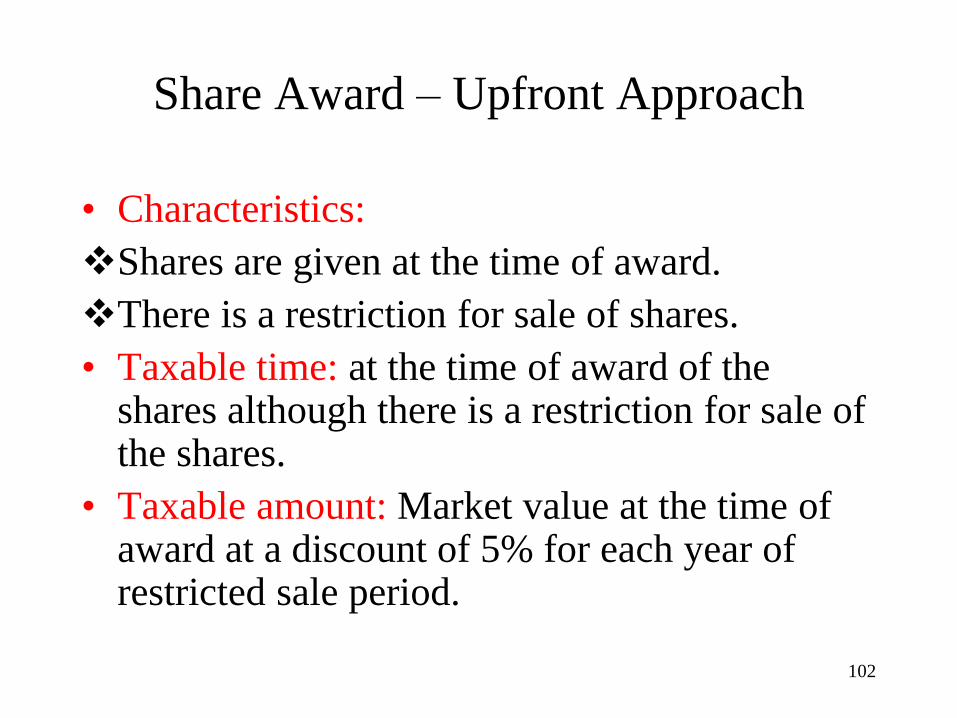

Share Award – Upfront Approach

• Characteristics:

Shares are given at the time of award.

There is a restriction for sale of shares.

• Taxable time: at the time of award of the shares although there is a restriction for sale of the shares.

• Taxable amount: Market value at the time of award at a discount of 5% for each year of restricted sale period.

103

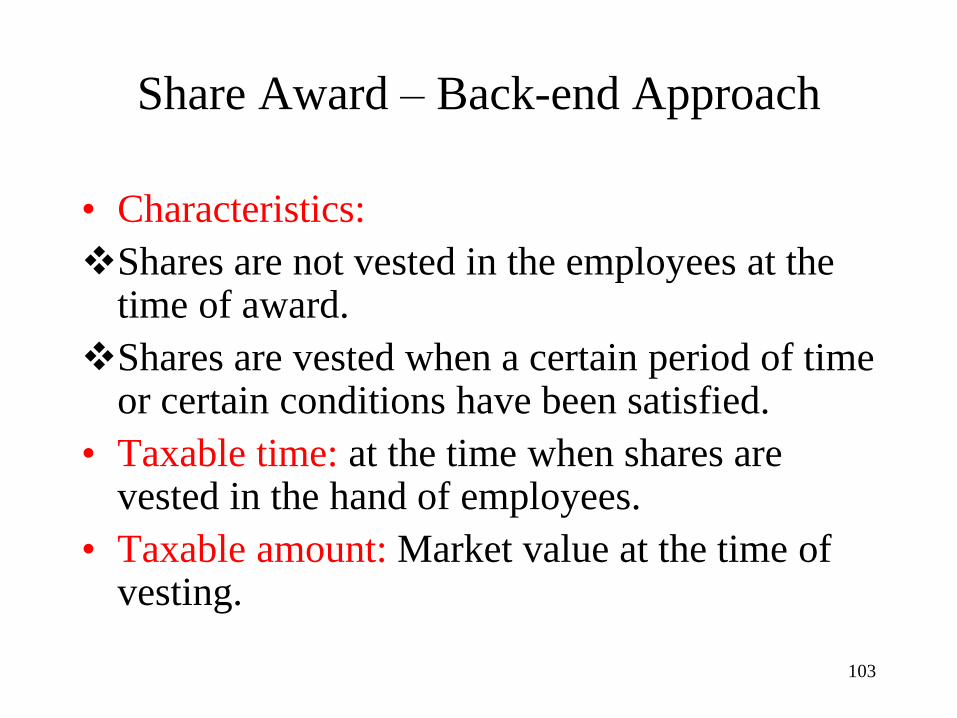

Share Award – Back-end Approach

• Characteristics:

Shares are not vested in the employees at the time of award.

Shares are vested when a certain period of time or certain conditions have been satisfied.

• Taxable time: at the time when shares are vested in the hand of employees.

• Taxable amount: Market value at the time of vesting.

104

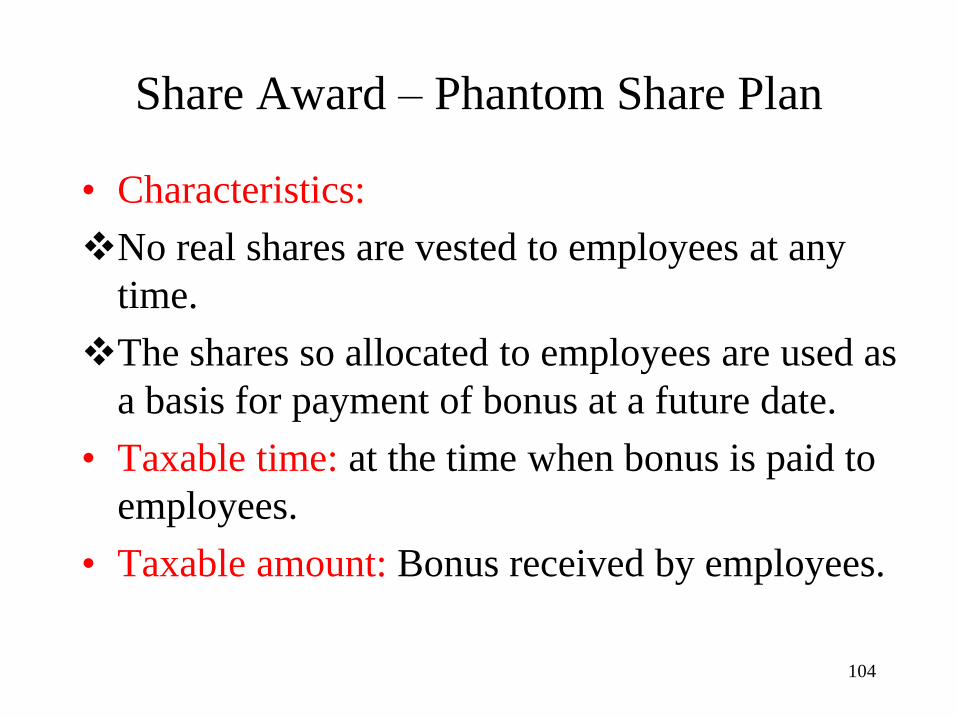

Share Award – Phantom Share Plan

• Characteristics:

No real shares are vested to employees at any

time.

The shares so allocated to employees are used as

a basis for payment of bonus at a future date.

• Taxable time: at the time when bonus is paid to

employees.

• Taxable amount: Bonus received by employees.

105

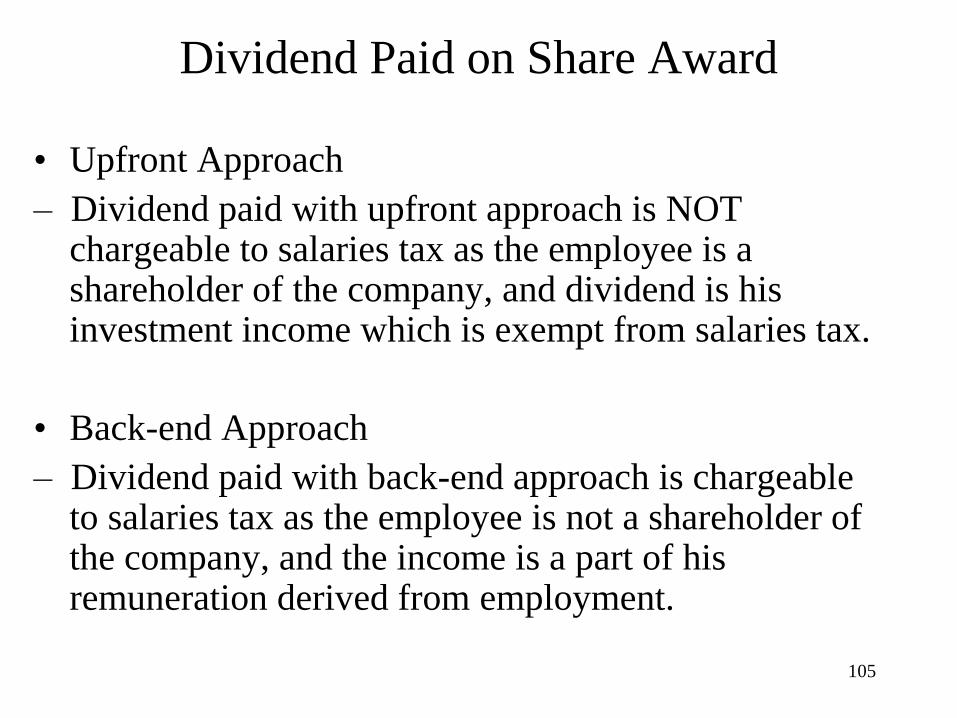

Dividend Paid on Share Award

• Upfront Approach

– Dividend paid with upfront approach is NOT chargeable to salaries tax as the employee is a shareholder of the company, and dividend is his investment income which is exempt from salaries tax.

• Back-end Approach

– Dividend paid with back-end approach is chargeable to salaries tax as the employee is not a shareholder of the company, and the income is a part of his remuneration derived from employment.

106

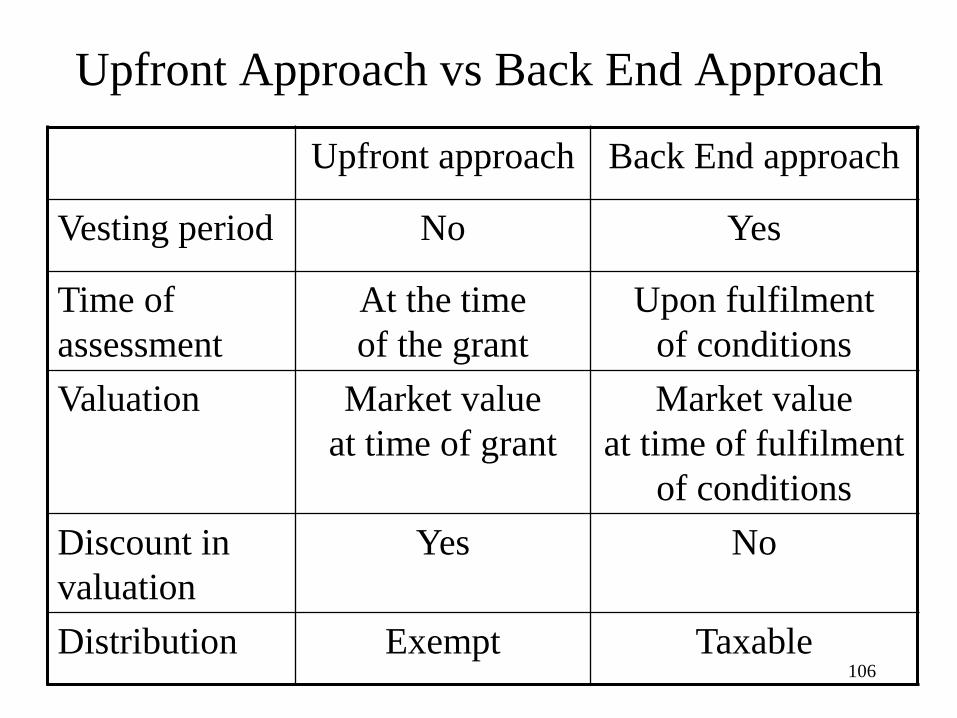

Upfront Approach vs Back End Approach

Upfront approach Back End approach

Vesting period No Yes

Time of

assessment

At the time

of the grant

Upon fulfilment

of conditions

Valuation Market value

at time of grant

Market value

at time of fulfilment

of conditions

Discount in

valuation

Yes No

Distribution Exempt Taxable

107

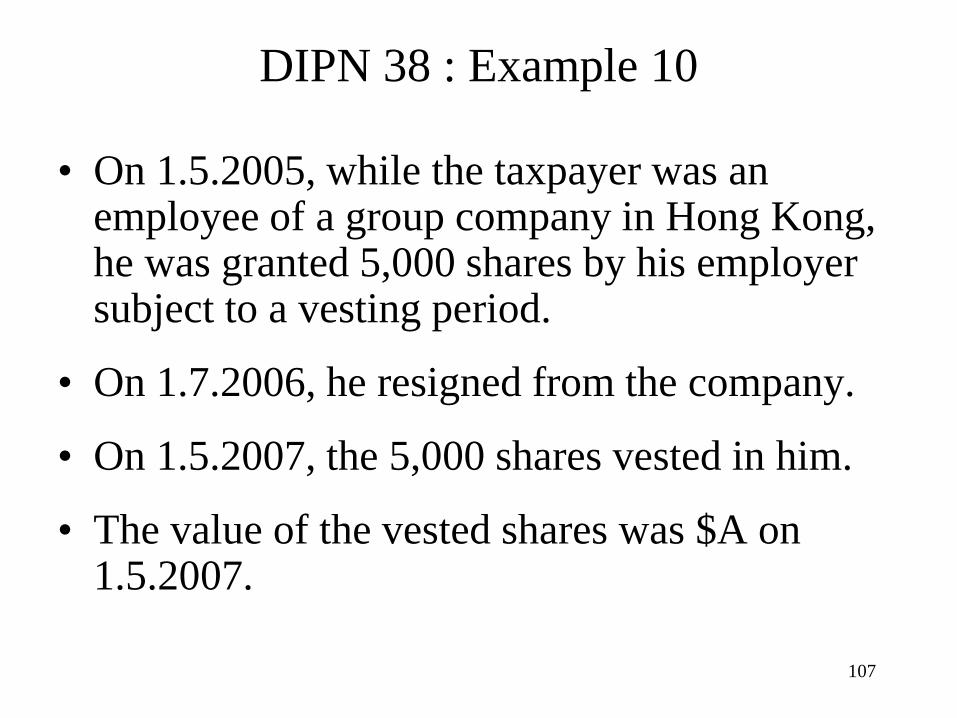

DIPN 38 : Example 10

• On 1.5.2005, while the taxpayer was an employee of a group company in Hong Kong, he was granted 5,000 shares by his employer subject to a vesting period.

• On 1.7.2006, he resigned from the company.

• On 1.5.2007, the 5,000 shares vested in him.

• The value of the vested shares was $A on 1.5.2007.

108

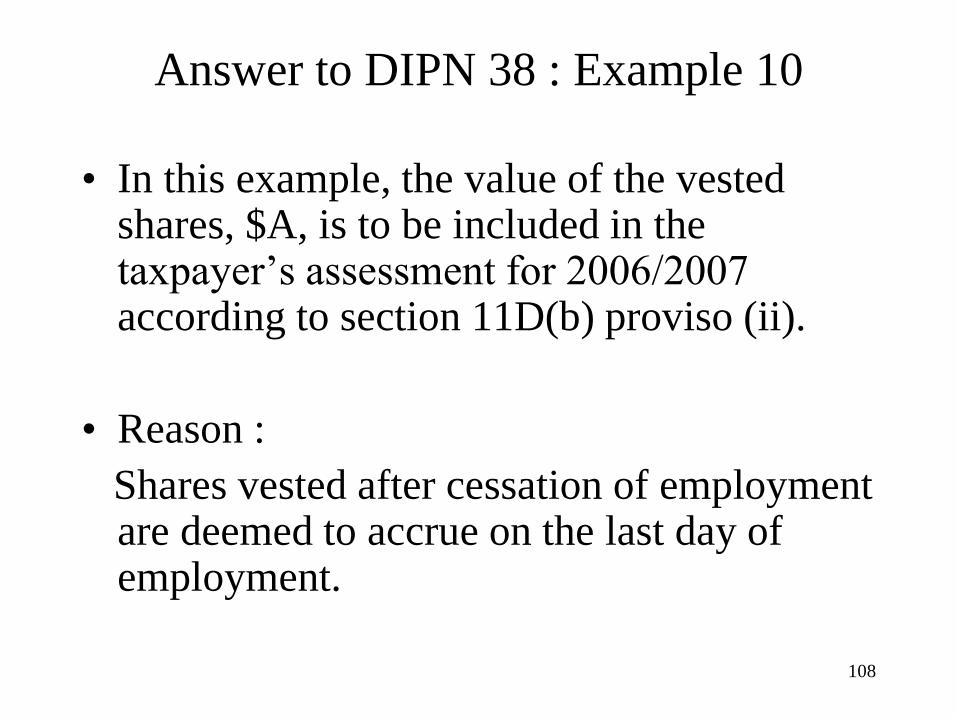

Answer to DIPN 38 : Example 10

• In this example, the value of the vested shares, $A, is to be included in the taxpayer’s assessment for 2006/2007 according to section 11D(b) proviso (ii).

• Reason :

Shares vested after cessation of employment are deemed to accrue on the last day of employment.

109

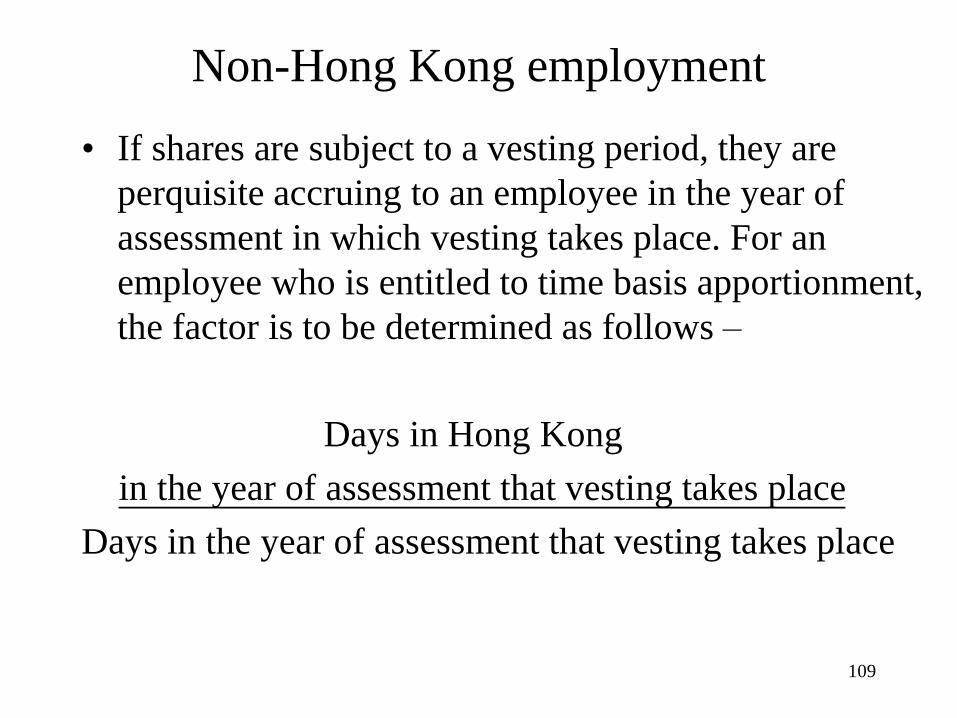

Non-Hong Kong employment

• If shares are subject to a vesting period, they are

perquisite accruing to an employee in the year of

assessment in which vesting takes place. For an

employee who is entitled to time basis apportionment,

the factor is to be determined as follows –

Days in Hong Kong

in the year of assessment that vesting takes place

Days in the year of assessment that vesting takes place

110

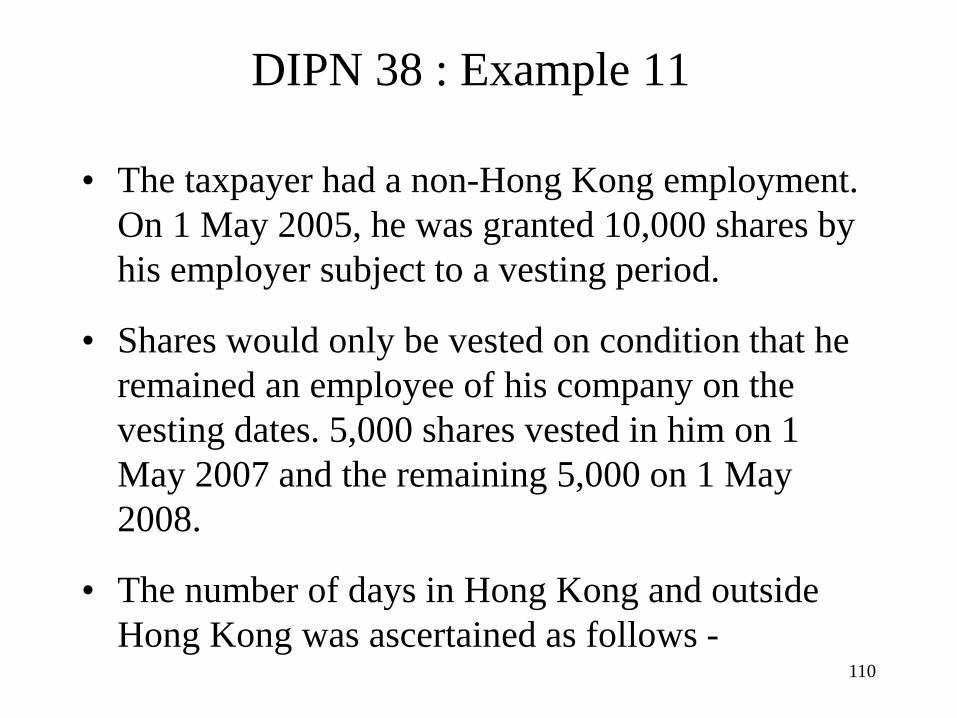

DIPN 38 : Example 11

• The taxpayer had a non-Hong Kong employment.

On 1 May 2005, he was granted 10,000 shares by

his employer subject to a vesting period.

• Shares would only be vested on condition that he

remained an employee of his company on the

vesting dates. 5,000 shares vested in him on 1

May 2007 and the remaining 5,000 on 1 May

2008.

• The number of days in Hong Kong and outside

Hong Kong was ascertained as follows -

111

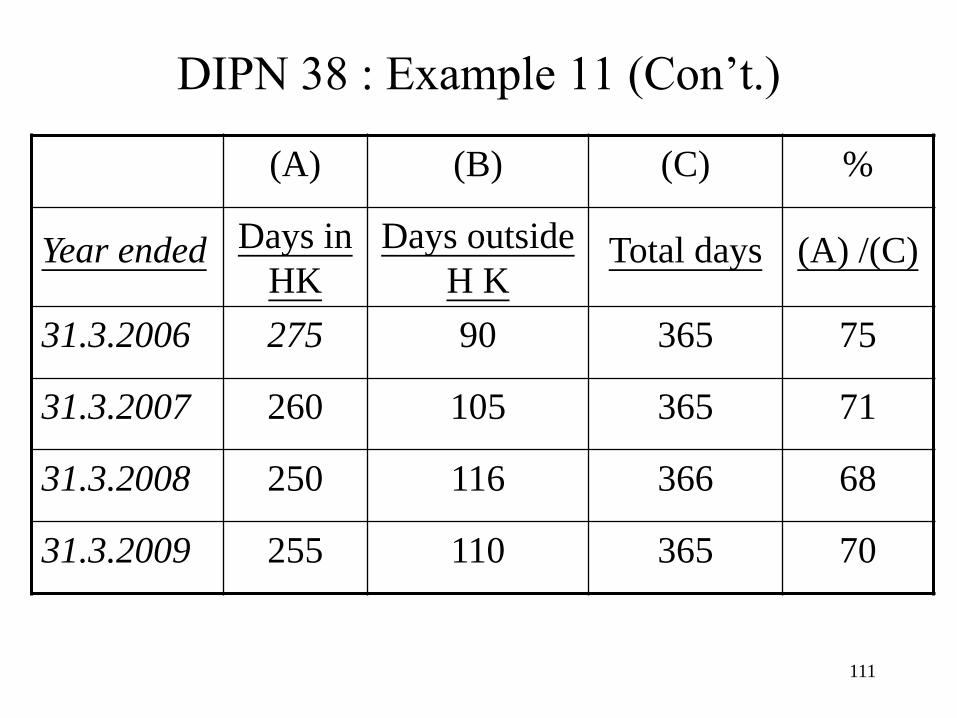

DIPN 38 : Example 11 (Con’t.)

(A) (B) (C) %

Year ended Days in

HK

Days outside

H K Total days (A) /(C)

31.3.2006 275 90 365 75

31.3.2007 260 105 365 71

31.3.2008 250 116 366 68

31.3.2009 255 110 365 70

112

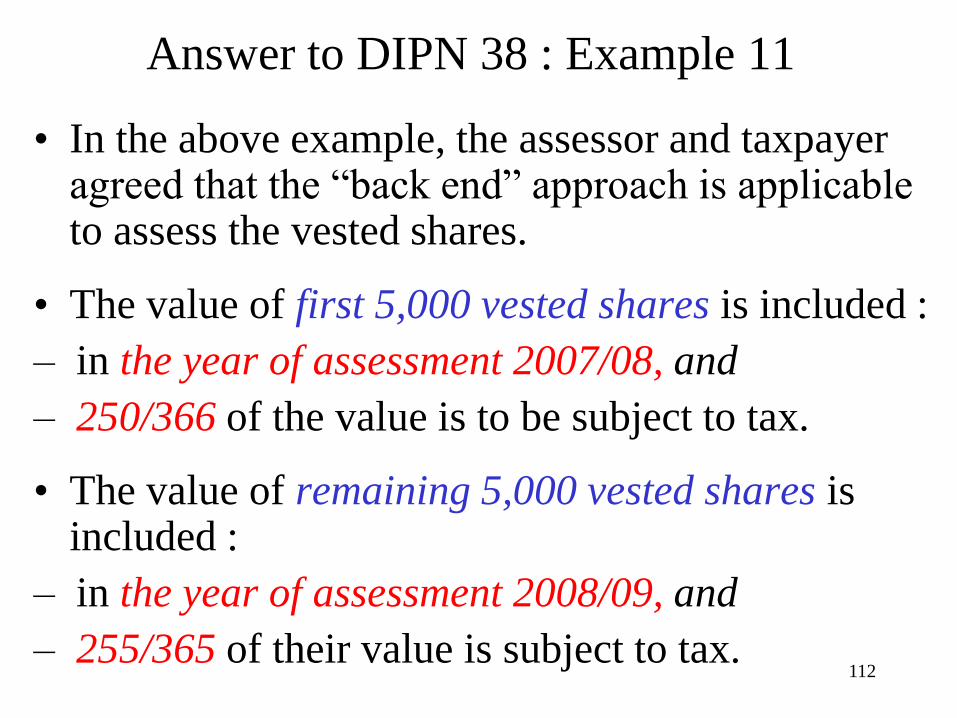

Answer to DIPN 38 : Example 11

• In the above example, the assessor and taxpayer agreed that the “back end” approach is applicable to assess the vested shares.

• The value of first 5,000 vested shares is included :

– in the year of assessment 2007/08, and

– 250/366 of the value is to be subject to tax.

• The value of remaining 5,000 vested shares is included :

– in the year of assessment 2008/09, and

– 255/365 of their value is subject to tax.

113

Inbound Employee Cases

• An employee holding a non-Hong Kong employment

may have been granted shares before he takes up his

employment or assignment in Hong Kong and such

shares are subject to a vesting period.

• If shares are vested in him after he takes up such

employment or assignment and the terms of the share

award clearly state that the vesting of the shares will

depend on a period of employment, IRD can agree to

exclude a portion of the gain on time apportionment

referable to the vesting period before the taxpayer’s

transfer to Hong Kong under the “Back End”

approach.

114

DIPN 38 : Example 12 – Inbound Employee

• On 1 September 2006, while the taxpayer was an employee of a group company outside Hong Kong, he was granted 10,000 shares by his employer subject to a vesting period.

• Shares would only be vested on condition that he remained an employee of the group on the vesting dates.

• On 1 August 2007, he was transferred to another company in Hong Kong within the group.

• The Department accepts that the taxpayer had a non-Hong Kong employment.

115

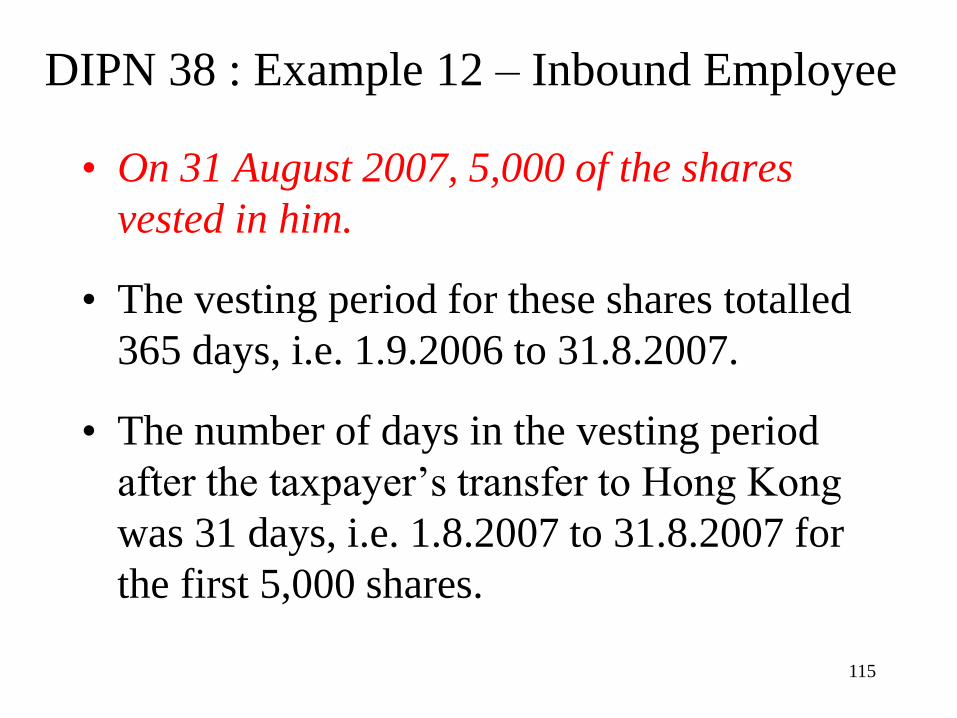

DIPN 38 : Example 12 – Inbound Employee

• On 31 August 2007, 5,000 of the shares

vested in him.

• The vesting period for these shares totalled

365 days, i.e. 1.9.2006 to 31.8.2007.

• The number of days in the vesting period

after the taxpayer’s transfer to Hong Kong

was 31 days, i.e. 1.8.2007 to 31.8.2007 for

the first 5,000 shares.

116

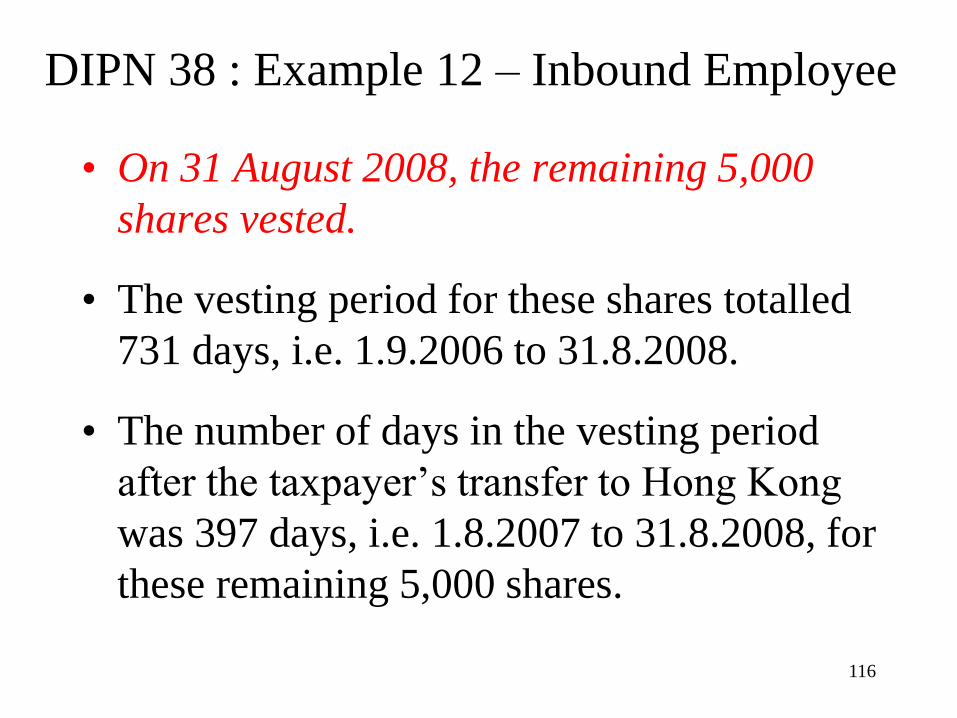

DIPN 38 : Example 12 – Inbound Employee

• On 31 August 2008, the remaining 5,000

shares vested.

• The vesting period for these shares totalled

731 days, i.e. 1.9.2006 to 31.8.2008.

• The number of days in the vesting period

after the taxpayer’s transfer to Hong Kong

was 397 days, i.e. 1.8.2007 to 31.8.2008, for

these remaining 5,000 shares.

117

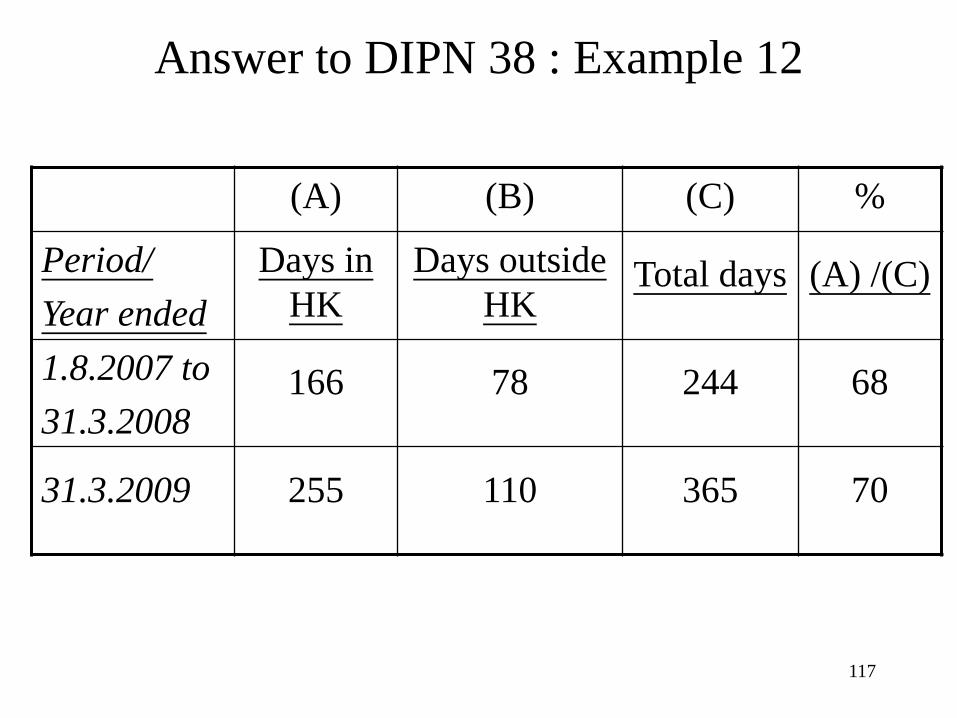

Answer to DIPN 38 : Example 12

(A) (B) (C) %

Period/

Year ended

Days in

HK

Days outside

HK Total days (A) /(C)

1.8.2007 to

31.3.2008 166 78 244 68

31.3.2009 255 110 365 70

118

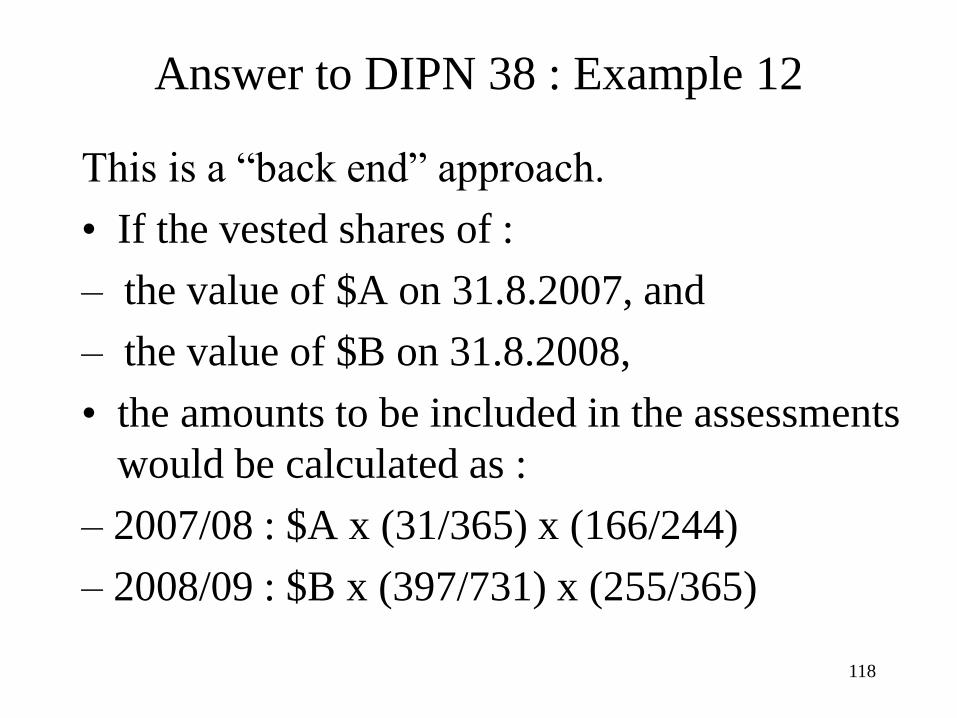

Answer to DIPN 38 : Example 12

This is a “back end” approach.

• If the vested shares of :

– the value of $A on 31.8.2007, and

– the value of $B on 31.8.2008,

• the amounts to be included in the assessments

would be calculated as :

– 2007/08 : $A x (31/365) x (166/244)

– 2008/09 : $B x (397/731) x (255/365)

119

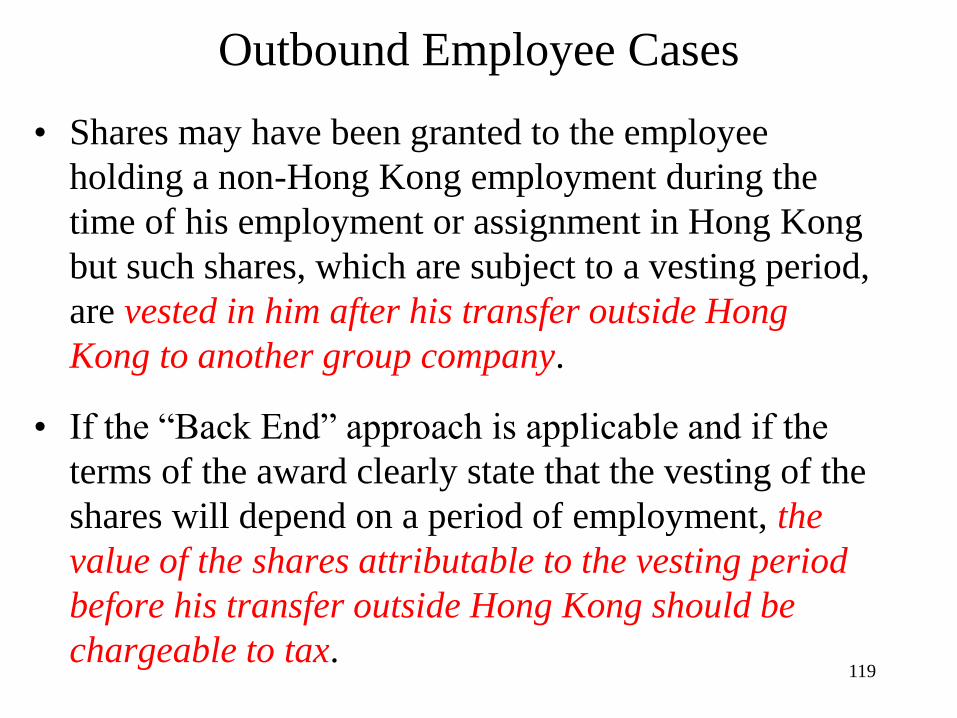

Outbound Employee Cases

• Shares may have been granted to the employee

holding a non-Hong Kong employment during the

time of his employment or assignment in Hong Kong

but such shares, which are subject to a vesting period,

are vested in him after his transfer outside Hong

Kong to another group company.

• If the “Back End” approach is applicable and if the

terms of the award clearly state that the vesting of the

shares will depend on a period of employment, the

value of the shares attributable to the vesting period

before his transfer outside Hong Kong should be

chargeable to tax.

120

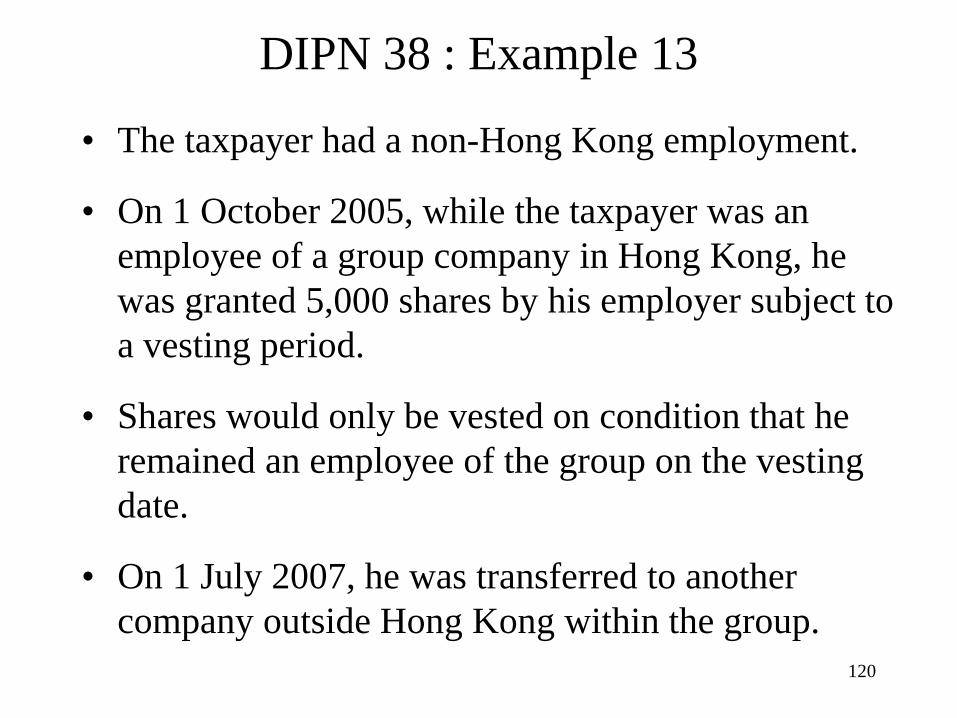

DIPN 38 : Example 13

• The taxpayer had a non-Hong Kong employment.

• On 1 October 2005, while the taxpayer was an

employee of a group company in Hong Kong, he

was granted 5,000 shares by his employer subject to

a vesting period.

• Shares would only be vested on condition that he

remained an employee of the group on the vesting

date.

• On 1 July 2007, he was transferred to another

company outside Hong Kong within the group.

121

DIPN 38 : Example 13

• On 1 October 2007, the 5,000 shares vested

in him.

• The vesting period for these shares totalled

730 days, i.e. 1.10.2005 to 30.9.2007.

• The number of days in the vesting period

before the taxpayer’s transfer outside Hong

Kong was 638 days, i.e. 1.10.2005 to

30.6.2007 for the 5,000 shares.

122

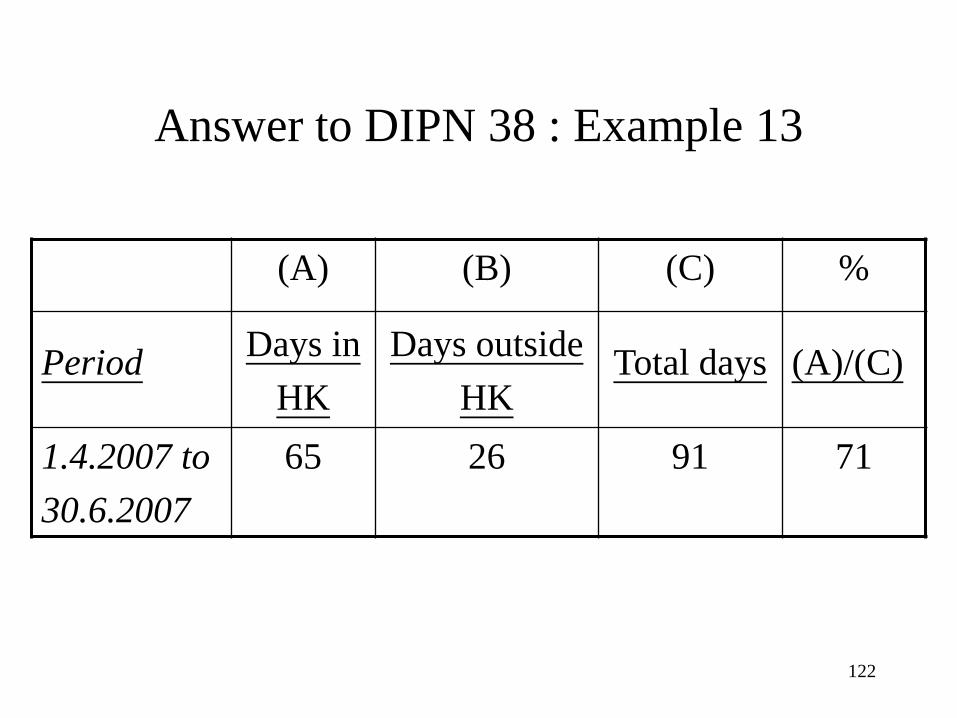

Answer to DIPN 38 : Example 13

(A) (B) (C) %

Period Days in

HK

Days outside

HK Total days (A)/(C)

1.4.2007 to

30.6.2007

65 26 91 71

123

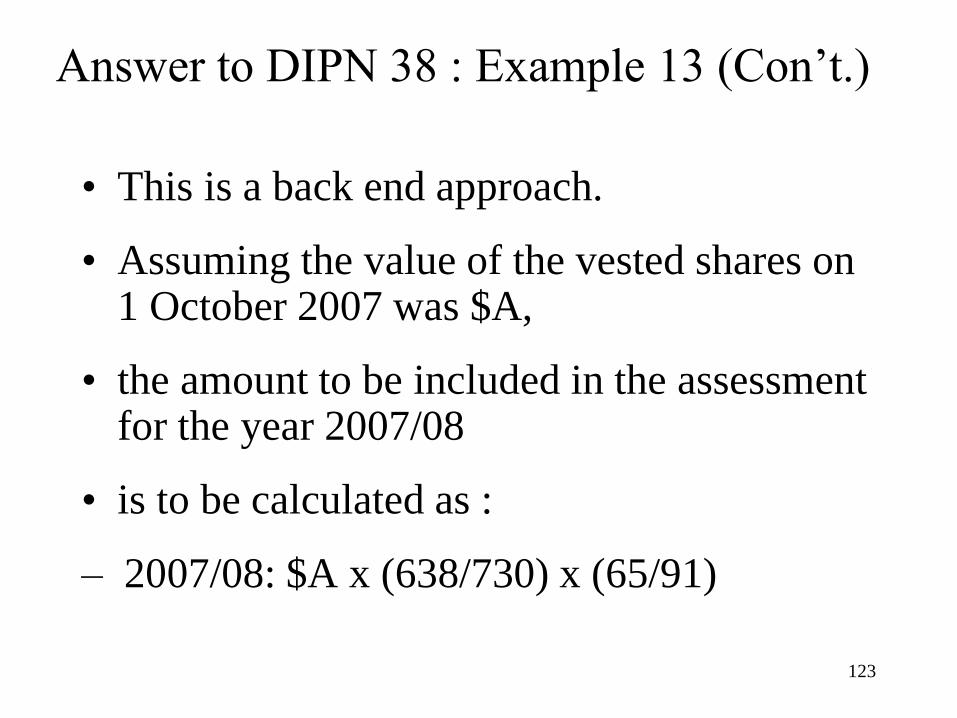

Answer to DIPN 38 : Example 13 (Con’t.)

• This is a back end approach.

• Assuming the value of the vested shares on 1 October 2007 was $A,

• the amount to be included in the assessment for the year 2007/08

• is to be calculated as :

– 2007/08: $A x (638/730) x (65/91)

124

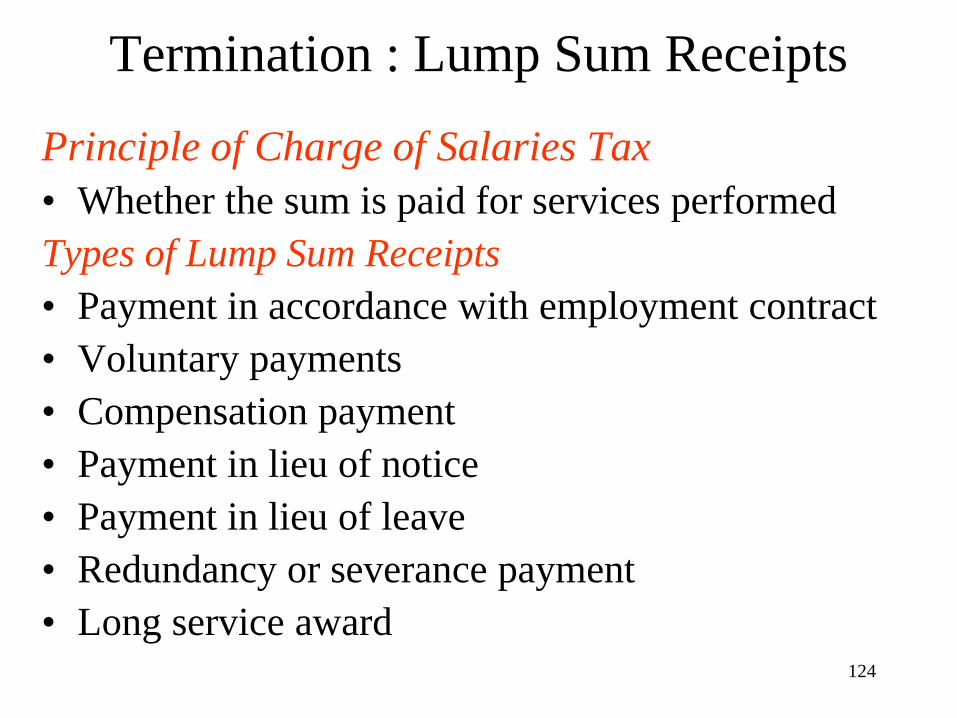

Termination : Lump Sum Receipts

Principle of Charge of Salaries Tax

• Whether the sum is paid for services performed

Types of Lump Sum Receipts

• Payment in accordance with employment contract

• Voluntary payments

• Compensation payment

• Payment in lieu of notice

• Payment in lieu of leave

• Redundancy or severance payment

• Long service award

125

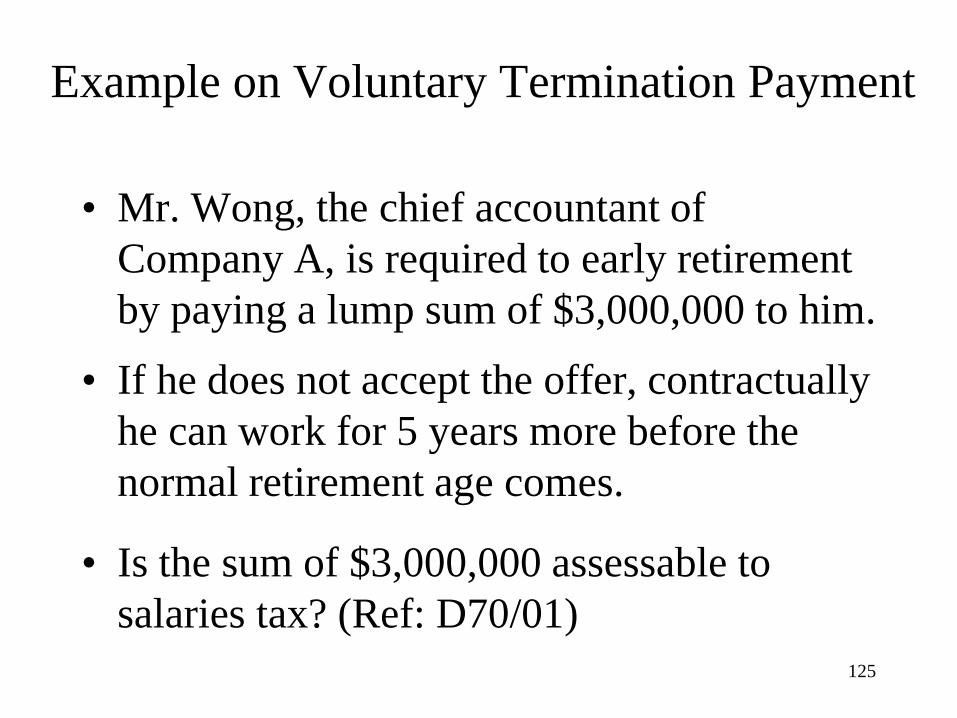

Example on Voluntary Termination Payment

• Mr. Wong, the chief accountant of

Company A, is required to early retirement

by paying a lump sum of $3,000,000 to him.

• If he does not accept the offer, contractually

he can work for 5 years more before the

normal retirement age comes.

• Is the sum of $3,000,000 assessable to

salaries tax? (Ref: D70/01)

126

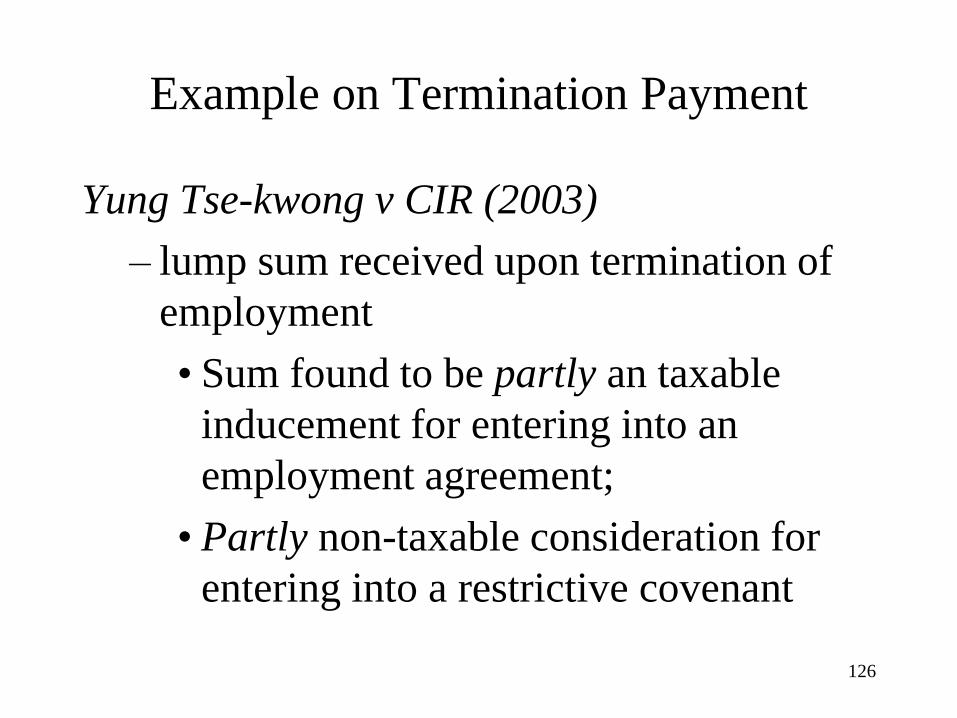

Example on Termination Payment

Yung Tse-kwong v CIR (2003)

– lump sum received upon termination of

employment

• Sum found to be partly an taxable

inducement for entering into an

employment agreement;

• Partly non-taxable consideration for

entering into a restrictive covenant

127

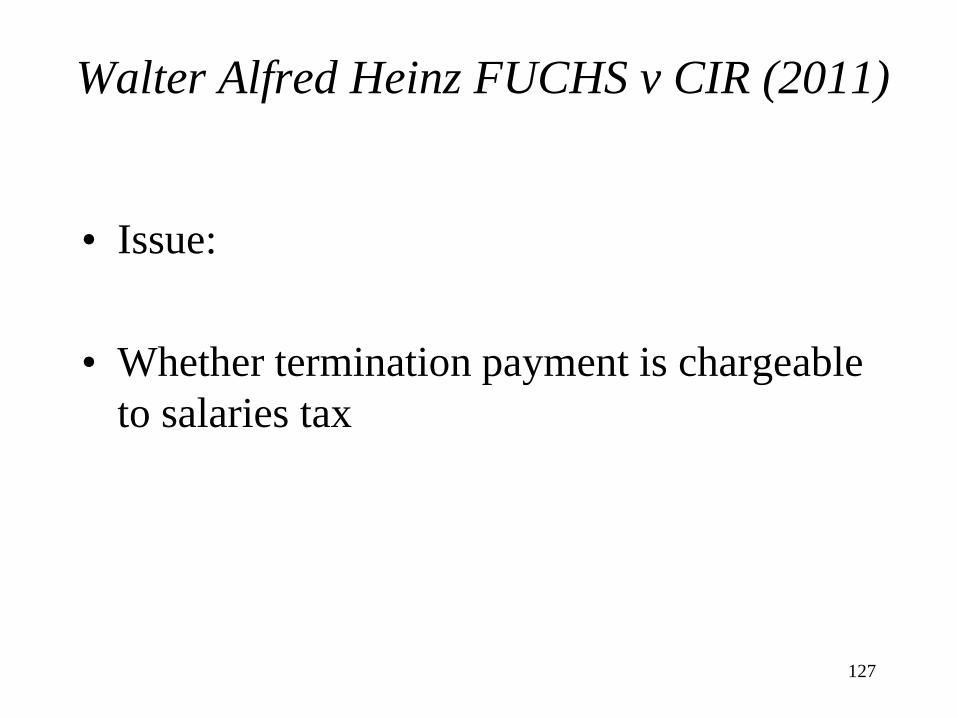

Walter Alfred Heinz FUCHS v CIR (2011)

• Issue:

• Whether termination payment is chargeable

to salaries tax

128

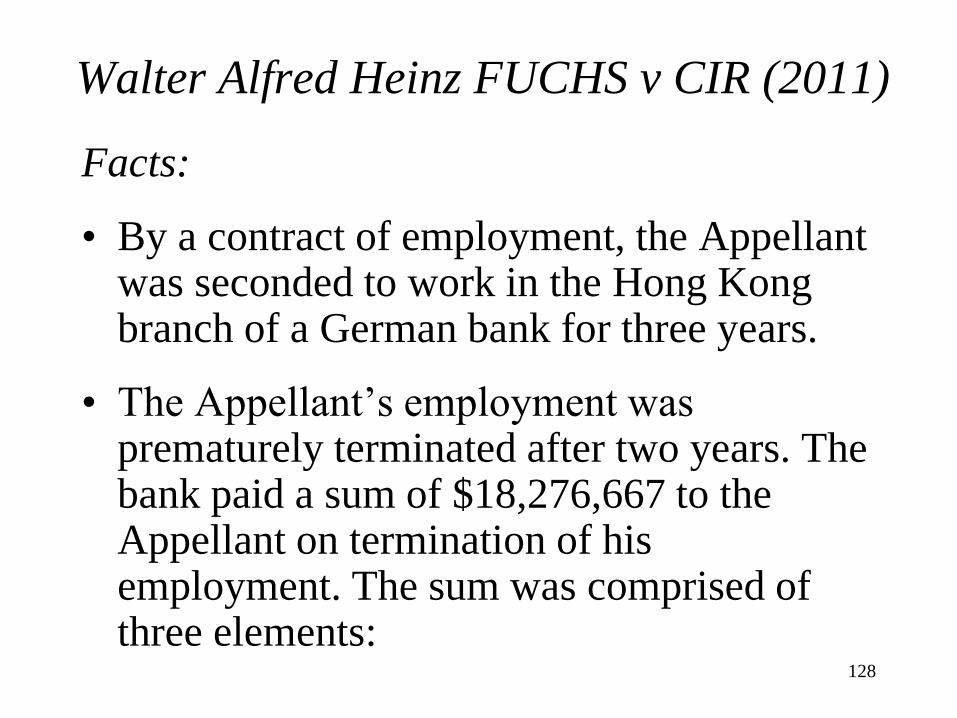

Walter Alfred Heinz FUCHS v CIR (2011)

Facts:

• By a contract of employment, the Appellant was seconded to work in the Hong Kong branch of a German bank for three years.

• The Appellant’s employment was prematurely terminated after two years. The bank paid a sum of $18,276,667 to the Appellant on termination of his employment. The sum was comprised of three elements:

129

Walter Alfred Heinz FUCHS v CIR (2011)

Facts (Con’t.):

(a) $3,120,000 being a sum equivalent to the Appellant’s salary for the remaining term of the employment contract (12 months) (“Sum A”);

(b) $6,240,000 being “two annual salaries for duration of service with the bank”(“Sum B”); and

(c) $8,916,667 being “the average amount of the bonuses paid in the 3 previous years” (“Sum C”).

130

Walter Alfred Heinz FUCHS v CIR (2011)

Facts (Con’t.)

• A term in the employment contract

• In the event that the employer terminates … this agreement … the employer shall pay to the employee (i.e. taxpayer) as agreed compensation or liquidated damages :

– 2 annual salaries (Sum B)

– an average amount of the bonuses paid in the 3 previous years of your employment with the Bank (Sum C).

131

Walter Alfred Heinz FUCHS v CIR (2011)

Facts (Con’t.):

• The assessor conceded that Sum A was non-

taxable but maintained the assessment in

respect of Sums B and C.

• By a determination, the Deputy

Commissioner confirmed the assessment.

132

Walter Alfred Heinz FUCHS v CIR (2011)

Decision of Court of Final Appeal

• Sum A was non-taxable

• Sums B and C taxable

133

Walter Alfred Heinz FUCHS v CIR (2011)

Reasons for the Decision :

• Payments made “in return for acting as or being an employee” or “as a reward for past services or as an inducement to enter into employment and provide future services” are income chargeable to tax under section 8(1).

• A payment is assessable as income from employment where the sum is plainly an entitlement under the contract of employment.

134

Walter Alfred Heinz FUCHS v CIR (2011)

Reasons for the Decision (Con’t.):

• Describing a payment as “compensation for

loss of office”does not displace liability to

tax.

• Where a payment is made in consideration

of the employee agreeing to surrender or

forgo his pre-existing contractual rights, the

payment is not taxable.

135

Walter Alfred Heinz FUCHS v CIR (2011)

Reasons for the Decision (Con’t.):

• Sums B and C were paid in satisfaction of the rights which had accrued to the Appellant, rather than in consideration of the abrogation of his rights, under the employment contract. Sums B and C accordingly come within the charge to salaries tax contained in section 8(1).

136

Payment in Lieu of Notice

• NOT Chargeable to Salaries Tax

• Reason

• It is not paid in consideration for services

rendered, but payment in compliance of the

Employment Ordinance.

137

Redundancy or Severance Payment

• Generally – NOT chargeable to salaries tax if

paid according to the provision of the

Employment Ordinance

• Excess over the requirements of the

Employment Ordinance may be assessable to

salaries tax (Advance Ruling Case No. 25)

138

Long Service Award

• By the general taxation principle, the sum is paid in consideration for the past services of an employee, and it is chargeable to salaries tax.

• However, the method of calculation of long service award and redundancy payment is similar under Employment Ordinance. Thus, as a matter of concession, CIR will charge salaries tax on the excess payable over the requirement of the Employment Ordinance.

139

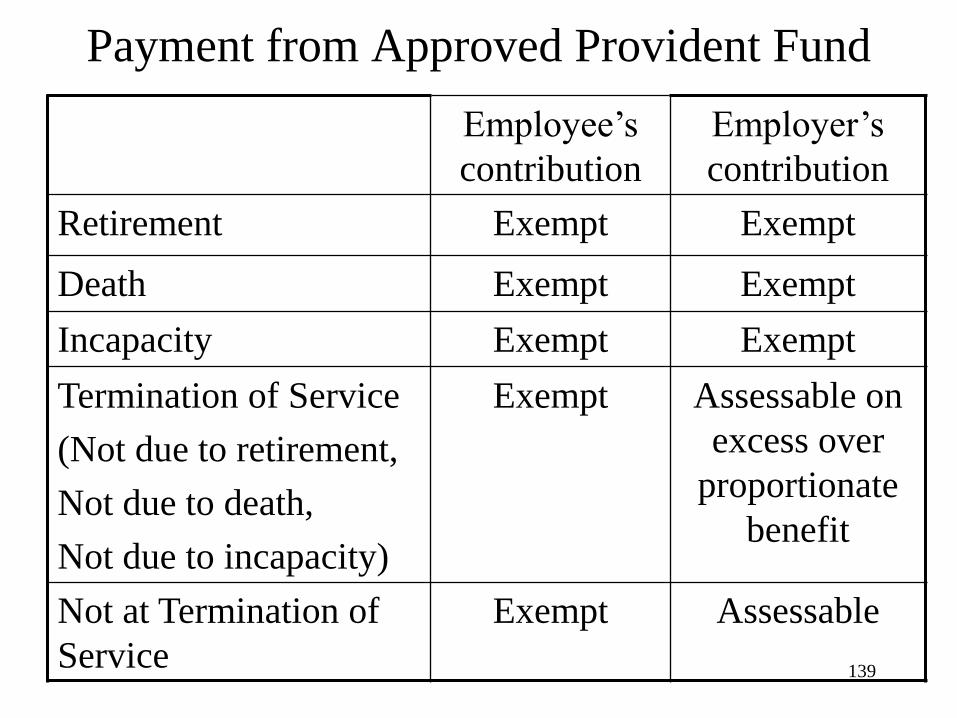

Payment from Approved Provident Fund

Employee’s

contribution

Employer’s

contribution

Retirement Exempt Exempt

Death Exempt Exempt

Incapacity Exempt Exempt

Termination of Service

(Not due to retirement,

Not due to death,

Not due to incapacity)

Exempt Assessable on

excess over

proportionate

benefit

Not at Termination of

Service

Exempt Assessable

140

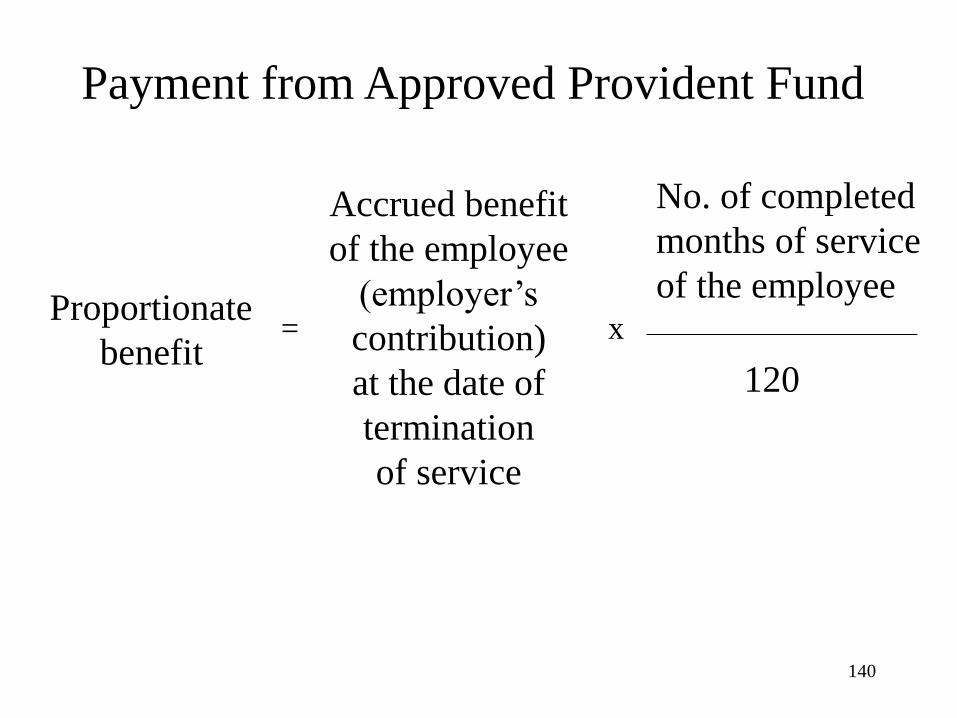

Payment from Approved Provident Fund

Proportionate

benefit

Accrued benefit

of the employee

(employer’s

contribution)

at the date of

termination

of service

No. of completed

months of service

of the employee

120

= x

141

Contract Gratuity

May be related back

Shorter of Contract / Employment Period

or 36 months

• A taxpayer has the right to elect or not

to elect for spreading over the gratuity.

142

Types of Correspondence / Letters to IRD

• Replying to an IRD enquiry

• Lodgment of objections against incorrect

assessment

• Lodgment of s.70A claim for correction of

an error or omission in a tax return or

statement

• Application for holdover for provisional

profits tax

143

Replying to an IRD Enquiry

Points to pay attention to :

• Whether the information is relevant and

sufficient

• Tables and appendices with proper indexes

• Present information in a logical and

professional manner

144

Replying to an IRD Enquiry

• As a quality control measure, the draft reply is

reviewed by a senior officer of CPA firm

before the draft is sent to the client for review

• Allow sufficient time for the client’s review

and before the final reply is sent to IRD

• Follow up actions to ensrue that the client’s

tax position is agreed with IRD without delay

145

Objection Letter to IRD

Points to pay attention to :

• Note the time limit for objection and appeal

• Draft the grounds for objection and seek

client’s agreement

• Enclose audited accounts if it is a section

59(3) estimated assessment in the absence

of return

• Any possible grounds for late objection

146

S.70A Claim for Correction of Error / Omission

• Note the time limit for claim of correction

of error or omission under section 70A :

– within 6 years after the end of a year of

assessment, or

– within 6 months after the date on which the

relative notice of assessment was served,

• whichever is the later.

147

Holdover for Provisional Profits Tax

• Note the grounds for holdover of provisional profits

tax – especially the 90% rule of the profits of the

previous year of assessment

• Note the time limit for application of holdover for

provisional profits tax :

– not later than 28 days before the payment due date, or

– not later than 14 days after the date of the issue of the

notice of payment of provisional profits tax

• whichever is the later.

148

Study and Practice for Drafting Letters to IRD

• Chapters 11 of Learning Pack

• Sections 5.1 to 5.4

149

Question and Answer

For further details, please refer to the book

“Hong Kong Taxation and Tax Planning” written by Patrick Kin Wai HO

and

Module D Learning Pack (2nd edition)

(and supplement for June 2012)

150

Thank You