hmf product possibilities - rhlf · 2015-07-09 · 1 hmf product possibilities: using hmf to...

TRANSCRIPT

11

HMF PRODUCT POSSIBILITIES:Using HMF to promote housing, job creation, and

sustainable human settlements, and more borrowing

RHLF Annual Client Workshop25 October 2012

Leriba Lodge, Centurion

Kecia [email protected]

www.housingfinanceafrica.org

22

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

Outline

� Understanding affordability & circumstance

� Understanding local economies & sustainable livelihoods

� Understanding communities

� Understanding HMF

Housing

Job creation

Sustainable human

settlements

Borrowing

Product possibilities

Positioning the HMF loan

product in the housing

delivery chain

Key issues in South Africa

33

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

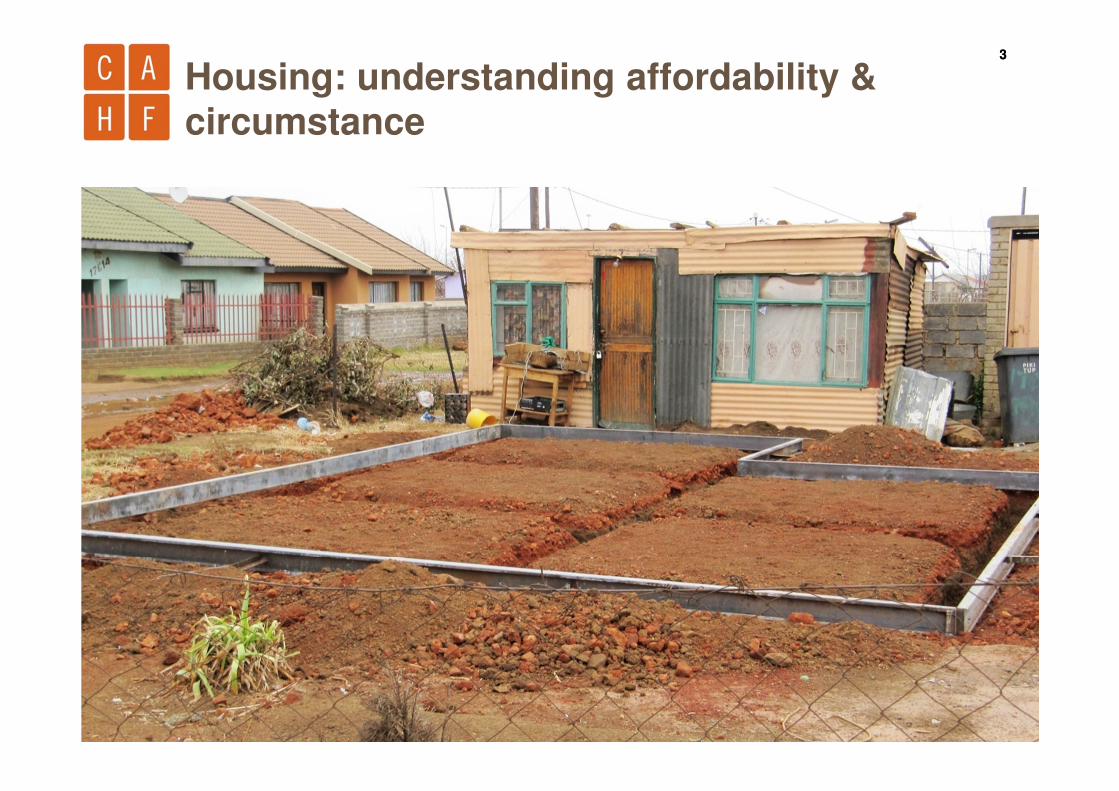

Housing: understanding affordability & circumstance

44

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

Affordability constraints limit the potential of

mortgage markets across Africa

According to the World Bank, only 3% of the population in Africa has an income sufficient to support a mortgage

36.5% of Africa’s population earn less than US$ 2,00 per day. This is the international poverty line.

24% earn US$2 -$4 per day

9% earn US$4 - $10 per day

10.8% earn US$10 - $20 per day

18.8% earn above US$20 per day

In most cases, subsidies don’t bridge affordability to buy a new house. In others, they cause new affordability challenges.

Source: AfDBReport on the middle class, 2011Served

UnderservedUnserved

55

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

0,07 0,07 0,16 0,21 0,39 0,5 0,5 0,5 1 1,1 1,2 1,3 1,6

2,3 2,3 2,51

3,94

12 12,2

16,9

19,6

0

2

4

6

8

10

12

14

16

18

20

Sene

gal (

2010

Hof

inet

)

Cent

ral A

frican

Rep

ublic

(200

5 W

B)

Burk

ina Fa

so (2

010 W

B)

Tanz

ania

(201

2 re

spon

se fr

om N

HC Tan

zani

a)

Niger

ia (2

008 W

B)

Cam

eroo

n (2

005 W

B)

Gha

na (2

012 re

spon

se fr

om H

F Ba

nk, G

hana

)

Malaw

i (20

07 W

B)

Egyp

t (20

11 H

ofin

et)

Uga

nda (2

011)

Zim

babw

e (2

012 re

spon

se fr

om C

ABS)

Alge

ria (2

009 W

B)

Buru

ndi (

2011

WB)

Rwan

da (2

010 W

B)

Botswan

a (2

009 W

B)

Keny

a (2

010 W

B)

Seyc

helle

s (20

10 W

B)

Tuni

sia (2

010 Ho

finet

)

Mau

rius

(201

2 re

spon

se fr

om M

HC)

Mor

occo

(201

1 W

B)

Nam

ibia

(201

1 Ho

finet

)

Sout

h Af

rica (e

nd 2

011,

own

analys

is)

Pe

rce

nt

Mortgages as a percent of GDP

Source: World Bank data from Simon Walley; email correspondence from country-level prac oners; Hofinet; own analysis.

Affordability constraints limit the potential of mortgage markets across Africa

26,4

66

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

8 177 850

2 180 760

915 397

905 885

1 464 370

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Households

>R16 000

R10 000 - R16 000

R7000 - R10 000

R3500 - R7000

<R3500

Monthly household income distribution (Housing White Paper 1994)

5,720,000

1,440,000

1,150,000

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Households per income band

>R3501

R1500-R3500

<R1500

8,3m households in SA in 1994 14,7m households in SA (2011)

Monthly hh income distribution (Housing White Paper 1994)

Monthly hh income distribution (General Household Survey 2011, StatsSA)

Affordability constraints (&housing costs) also limit the potential of mortgage markets in SA

77

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

In South Africa, housing affordability and circumstance are not necessarily related

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

R 0-R 3,500 R 3,500 -

R7,000

R 7,000 –

R10,000

R 10,000 -

R15,000

R 15,000 –

R20,000

R 20,000+ Total

Other (% hh)

Hostel (% hh)

Tradi onal dwelling - rented or owned (% hh)

Backyard dwelling - rented or owned (% hh)

Informal se lement - rented or owned (% hh)

Formal - rented, plus room/flatlet not in

backyard (% of hh)

Formal - owned (% of hh

Source: Household income data is based on data modeled by the Department of Economics at the University of Stellenbosch, utilising the Community Survey of 2007. Analysis by Shisaka Development Management Services, prepared for the Finance and Fiscal Commission, 2012

88

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

Housing: understanding affordability & circumstance

99

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

According to the World Bank, only 3% of the population in Africa has an income sufficient to support a mortgage

36.5% of Africa’s population earn less than US$ 2,00 per day. This is the international poverty line.

18.8% earn above US$20 per dayBuild in

opportunities for housing

microfinance & shift housing

finance potential for low-income

earners.

Source: AfDBReport on the middle class, 2011

9% earn US$4 - $10 per day

10.8% earn US$10 - $20 per day

24% earn US$2 -$4 per day

ServedUnderservedUnserved

HMF offers a staged financing process that is affordable to a wider population for both home improvement and housing development

1010

HMF can be affordable even at rates significantly above mortgage rates

Traditional Mortgage$10,000 Home Loan at 25% interest

Incremental HMF Loan5 x $2,000 Loans at 50% interest

The installment associated with a Traditional Mortgage Loan at 25% interest is still 55% greater than that of an Incremental HMF Loan at 50% interest.

1 2 3 4 5 6 7 8 9 10

Year

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

1 2 3 4 5 6 7 8 9 10

USD

Year

Principal paid

Interest paid

Principal outstanding

Cumulative borrowings

Monthly installment: $233Total repayment: $28,000

Monthly installment: $150Total repayment: $18,000

Source: Select Africa

Realising housing by understanding affordability: from whole house to step-by-step

1111

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

Original house –built around 1995

Three backyard rooms with water-borne sewerage: rental income

Container in the front yard for spaza shop – small business with cash flow for credit

Building materials for the next project

About 70% of small scale enterprises in Gauteng have a component of their business in the home

Job creation: understanding local economies & sustainable livelihoods

1212

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

Sustainable human settlements: understanding communities

A shop in the neighbourhoodmeans residents don’t have to take the bus for milk & bread.

A creche allows parents to work.

Small businesses diversify residential space and support sustainable human settlements

1313

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

Original house – access to good water, sewerage and electricity – taxes and services charges are affordable when the household has an income

Quality rental housing serves a housing need & stimulates the local construction sector

Sustainable human settlements: understanding communities

Small businesses diversify residential space and support sustainable human settlements

Property creates the demand for other local enterprises: burglar bars, ceilings, walling, gardens, etc. all stimulating the local economy

1414

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

More borrowing: understanding HMF

1515

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

Housing microfinance:

� Gives low-income earners an opportunity to improve their housing circumstances

� Enables lenders to extend lower down market, creating new clients for possible future cross-selling.

� Offers income generationopportunities to support sustainable livelihoods.

� Encourages home improvements and gentrification towards sustainable human settlements

� Borrow microloan

� Make improvements

� Accommodation for rent

� Small business

� Realise income

� Pay back microloan

� Improved housing asset

More borrowing: understanding HMF

1616

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

More borrowing: understanding HMF

Starter houseStarter houseStarter houseStarter house

Borrow micro

loan to improve

Improved house Improved house Improved house Improved house

with backyard with backyard with backyard with backyard

room (for rental)room (for rental)room (for rental)room (for rental)

Sell to buy…

Mortgaged Mortgaged Mortgaged Mortgaged

2222----room room room room

house with house with house with house with

backyard backyard backyard backyard

dwellingdwellingdwellingdwelling

Mortgaged Mortgaged Mortgaged Mortgaged

5555----room room room room

house with house with house with house with

granny granny granny granny

cottagecottagecottagecottage

Sell and buy…

2nd dwelling for business…

Income for retirement…

Once homeless, now an investor, providing housing to other low income earners

1717

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

Positioning the HMF loan product in the housing delivery chain

1818

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

Acquisition and

occupancy of the plot

Upgrading property tenure to

obtain security

• Maintain physical control of the plot

• Achieve secure tenure

• Obtain full legal title

Provision of basic

infrastructure & upgrading

Construction of the house structure &

improvements

Building community

institutions to combat insecurity

• Physically occupy the plot

• Pay for plot

• Starter infrastructure

• Construct an initial makeshift shelter

• Upgrading of basic infrastructure

• Provide adequate sanitation

• Improve and expand unit

• Add accessories and space for relatives and rental

• Form neighbourhood groups

• Local and international NGO support

• Partner with pubic and private sector

Finance

moment

Finance

moment

Finance

moment

Finance

momentFinance

moment

Positioning the HMF loan product in the housing delivery chain

Source: Housing Value Chain derived from Ferguson, as reported at HMF Regional Workshop, April 2010

Advocacy & networking: policy and regulatory

Issues

Services: Technical skills, supervision, admin support

Products: building materials, plans, etc.

1919

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

Housing loans can be for various purposes: NACHU, Kenya

�Hatua New Housing Loan

�Huduma Infrastructure loan: install electricity, water and sanitation facilities, sewerage systems, fencing and roads

�Ploti resettlement loans: buy land for residential or commercial purposes

>100% growth between 2010-2011. Book value

is US$721 000

41% growth

94% growth

2020

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

Housing loans create demand for other services: KixiCredit, Angola

� KixiCredito (Angola’s first non-bank MFI) offers a housing microloan product: KixiCasa

� 36 month sequential loans up to $5000 per phase per house

� Raising further capital to grow loan book

� Development Workshop as developer

� Partnership with CLIFF to scale up: 3000 home, incremental housing project in Huambo. CLIFF provides infrastructure financing; KixiCasaend user finance

� HabiTec is a social enterprise supporting KixiCasa loans:

� HabiTerra provides settlement planning, land registration and land allocation services – support to provincial government with participatory urban planning

� AquaSan improves rural water supply, builds water systems

� Wood factory produces furniture & other goods for homes and schools

Examples from Angola, Malawi, Kenya, Tanzania, Zimbabwe, Uganda and elsewhere show real progress

2121

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

Market making by filling in the delivery chain: Malawi

Select Africa / Habitat for Humanity International

partnership

� Select (private sector MFI) provides HMF

� HfH provides construction technical assistance – cost

covered by Select

� 1900+ households served in Blantyre & Lilongwe –

40% of Select clients

� Plans to grow to other urban centres

� “site visits are an invaluable branding opportunity

for both Select and HfH”

� Future plans

� Refining overall cost model for CTA to increase capacity,

offer more services

� Getting to the client before they start construction

� Increase volume of site visits and inspectionsThe need to link HMF with the housing supply sector (through construction technical

assistance & other support) make this different from traditional microlending and supports a good housing outcome.

Off-site CTA• Technical information,

leaflets, sample plans

• Professional services &

training: meeting with

client regarding plans

On-site CTA• 3 levels relating to

complexity of project

and level of TA required

• Different professionals

for different tasks

• Multiple visits

2222

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

Using the delivery chain to innovate around origination

� Satellite HMF lending operations at building material stores

� Lendcor’s WozaniNonke interactive store terminals

� Lafarge Cement pilot in Zambia and Nigeria

2323

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

Market making by filling in the delivery chain

Housing microfinance needs

� A place to build (land): Access to securetenure on which households can begin toimprove their housing conditions rather thanwait for the State to intervene is critical.

� The skills and technical capacity to build (housing support services):

� Local municipal requirements

� Drawing & approval of appropriate & efficient plans

� Sourcing & costing of quality building materials

� Good quality builder / contractor

� Ongoing maintenance and longer term home improvements

� The permission to build (political support)

� Can microlenders be expected to provide the housing ingredients?

� Can the borrower?

� But without these ingredients, the housing process is less likely to be a quality one

� While microlendersgrow to scale, big challenge is growing housing support services to scale.

2424

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

Nachu, Kenya

Product possibilities: Emerging practice in Africa

� Establishing a housing loan product

� Cooperative savings and loans for housing

� Scaling up capacity for growth

� Offering housing support services

� Broadening institutional actors

� The use of cheap and effective building technology

� Services products: solar, water, sanitation

� Guarantee finance

� Collaboration

� “pay as you go” slum upgrading

Ugafode, Uganda

Faulu, Kenya

KixiCredito, Angola

Nachu, Kenya

Kuyasa Fund, South Africa

Habitat for Humanity, Malawi / Ghana / Uganda

Centenary Bank, Uganda

Mchenga, Malawi

Mchenga Fund, Malawi

WAT, TanzaniaNachu, Kenya

Tanzania HMF WG TAFSUS, Tanzania

Select Africa

UNHabitat Ghana & Tanzania

Mwanza, Tanzania

Select Africa

Planet Finance

Izwe, South Africa

Zinahco, Zimbabwe

Alitheia Capital, Nigeria

2525

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

Key issues for HMF in South Africa

• RDP housing• Informal

settlements • Housing

supply & debt

2626

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

RDP Housing

All these dots represent 24% of the residential property market in SA

2727

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

RDP Housing: Johannesburg

� 135 000 registered subsidized units have

been built in Johannesburg since 1994, or

about 20% of the city’s registered

housing stock. (It is noted that a

significant number of subsidised housing

units have not been registered)

� House size: 40m2 maximum: Home

improvements / extensions

� Stand size: 250m2 (older properties):

Backyard rental, home based

enterprises

Legend

� Green: Discount benefit scheme

� Pink: RDP project-linked subsidy

� Grey: either DBS or RDP

Location of registered subsidised housing in Johannesburg: to September 2010

300 estimate

1994

1066

2001

2628

2010

• Nationally 10 shack fires each day, over 200 deaths p.a.

• 7% HIV annual incidence rate - 1.8% in urban formal areas

• Diarrhoea-related infant mortality up to 10 times higher than urban

formal areas

• Official estimates over 40% unemployment compared to 26%

national average

Informal settlements are an EMERGENCY

Source: Steve Topham, National Upgrading Support Programme.Presentation to Planning Africa 2012, 18 September 2012

Response: participatory upgrading at scale

• Outcome 8 Delivery Agreement national

target: 400 000 households in well-located

informal settlements to receive basic services

and secure tenure by 2014

• Cabinet Lekgotla 2011: Integrated upgrading

programmes in 45 municipalities

• National Planning Commission Vision 2030:

expand upgrading programme, create new

instruments for tenure & regularisation

• NDHS & Presidency 2012: Detailed project

plans for 1 800 informal settlements

• ALL to be produced by participatory planningSource: Steve Topham, National Upgrading Support Programme. Presentation to Planning Africa 2012, 18 September 2012

• 125 694 serviced sites delivered by provinces by June 2012

(31.3% of 2014 target) (Eastern Cape, Free State &

Limpopo figures outstanding)

• 7 metros have overall upgrading strategies in place, 6 to be

assisted with detailed settlement level plans – Cape Town,

Johannesburg, Tshwane, Buffalo City, Ethekwini, Ekurhuleni

• 13 Municipalities have housing plans (part of IDP) in place –

ISU portion however requires additional support

• Remaining 29 Municipalities have not upgrading strategies –

but will be assisted with mapping & categorisation of IS as a

first step: Limpopo complete, Free State underway

Progress – delivery and technical assistance

Source: Steve Topham, National Upgrading Support Programme. Presentation to Planning Africa 2012, 18 September 2012

3131

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

Rising debt levels coupled with declining housing supply…

� Annual supply has plummeted since 2007, but starting to recover

� Small house category the leading performer

� Debt levels are serious: 9.22 million consumers have impaired records (47% of 19.6 million credit active consumers)

So

urc

es:

NC

R C

redit

Bure

au M

onit

or

Q2 J

une

2012 /

A

BS

A R

esid

enti

al B

uil

din

g S

tati

stic

s 16 F

ebru

ary 2

012

3232

Kecia Rust ▪▪▪▪ Centre for Affordable Housing Finance in Africa - a division of the FinMark Trust

… creates other opportunities to shift towards productive HMF lending

� Limitations in housing supply may have precipitated a rise in pension-backed and unsecured lending.

� The rise in unsecured lending in SA can also be attributed to the absence of anything else to buy / invest in.

� Melzer has shown how unsecured lending locks the borrower in for years…

� And, the housing subsidy has also put upward pressure on housing prices, reducing affordability

� A wider population is joining the HMF target market, if incremental housing systems can be designed