how incentives shape strategy: the role of cmo and ceo ... · role of chief marketing officers...

TRANSCRIPT

“How Incentives Shape Strategy: The Role of CMO and CEO Equity Compensation in

Inducing Marketing Myopia” © Martin Artz and Natalie Mizik; Report Summary © 2018

Marketing Science Institute

MSI working papers are distributed for the benefit of MSI corporate and academic members

and the general public. Reports are not to be reproduced or published in any form or by any means, electronic or mechanical, without written permission.

Marketing Science Institute Working Paper Series 2018 Report No. 18-105

How Incentives Shape Strategy: The Role of CMO and

CEO Equity Compensation in Inducing Marketing Myopia

Martin Artz and Natalie Mizik

Report Summary

Myopic management is a serious problem and a threat to firms because it entails inefficient

decision making, which leads to a decline in future firm performance. In this study, Martin Artz

and Natalie Mizik examine the role personal compensation incentives of CMOs and CEOs play

in inducing myopic marketing management.

They combine data from multiple sources (ExecuComp, Center for Research in Security Prices

[CRSP], Compustat, and Thomson Reuters Insider Filing Data Feed). Their sample covers all

public firms in these databases from 1993-2014. Their analyses use multiple methods designed to

identify causal effects (e.g., inverse probability weighted regression adjustment, Heckman

selection bias correction, endogenous treatment effects, control function, difference-in-

differences), which allows for a causal interpretation of findings.

Findings

CEO equity incentives are largely unrelated to the incidence and severity of myopic marketing

management. CMO equity compensation, on the other hand, is highly predictive of the incidence

and severity of myopic marketing management.

Contrary to the arguments that the presence of a CMO in the organization can help maintain

customer focus and support for marketing departments, CMOs not only fail to prevent myopia,

but further exacerbate the problem as the market-based (i.e., equity) portion of their personal

compensation increases.

Further, consistent with the CMO’s personal enrichment motivation, CMOs take advantage of

artificially inflated stock valuation by exercising more stock options and selling more of their

personal equity holdings in the years when myopic marketing management occurs and is more

severe.

Implications

In contrast to a popular pessimistic view in the marketing literature questioning the ability of

CMOs to influence firm strategy, these findings suggest CMOs have a significant influence on

marketing budgets and firm strategy. However, this study also challenges the belief in the CMO

as a central force to mitigate marketing resource misallocation and as the dominant advocate for

a long-run-focused marketing strategy.

On the contrary, these findings suggest that CMOs enable myopic marketing management and

seek to derive personal gain when it occurs. They highlight the pitfalls and limitations of

overreliance on equity in managerial compensation packages: Equity compensation can create

perverse incentives for managers in their functional domain to engage in myopic practices.

What are the solutions to the myopic management problem? One proposal suggests firms should

pay their executives based on stock price performance but defer the payout until after the

executive’s retirement in order to reduce the effects of equity compensation and provide optimal

investment incentives during the latter part of the CEO’s tenure. Another proposal calls for tying

executive compensation to long-run-oriented performance metrics (e.g., customer satisfaction or

Marketing Science Institute Working Paper Series 1

brand equity). Yet another proposal advocates expanding disclosure of value-relevant non-

financial performance indicators to curtail myopic management.

In April 2015, the SEC issued a “pay versus performance” proposal (it has just been moved from

the 2017 SEC rulemaking agenda to the long-term action list by the new administration) to

require greater disclosure on compensation and to draw a direct link to performance

(http://www.sec.gov/news/pressrelease/2015-78.html). Under this proposal, companies would be

required to disclose the relationship between executive pay and a company’s financial

performance and to report executive compensation relative to their financial performance and

relative to their peer group of firms. Will this solution help remedy the problem? The answer

remains to be seen.

Martin Artz is Associate Professor of Management Accounting and Control at the Frankfurt

School of Finance & Management, Germany. Natalie Mizik is Professor of Marketing and J.

Gary Shansby Endowed Chair in Marketing Strategy, Foster School of Business, University of

Washington.

Acknowledgments

The authors thank seminar participants at Goethe University, INSEAD, Northwestern University,

Marketing Science Conference (Atlanta), Marketing Strategy Meets Wall Street Conference

(Singapore), Theory + Practice in Marketing Conference (Kellogg School of Management),

University of Georgia, University of Mannheim, University of Washington, and Washington

State University for helpful comments. The first author gratefully acknowledges support from

the Julius-Paul-Stiegler Memorial Foundation at the University of Mannheim.

Marketing Science Institute Working Paper Series 2

INTRODUCTION

The economic crisis of 2008 put a bright spotlight on executive compensation and its effects on the

behavior of top management teams (TMTs). The critics have pointed to the unprecedented escalation

in executive compensation, drawing a direct link to deteriorating business ethics, widespread excesses

and abuses of power, and the lack of regard for customers’ and shareholders’ welfare (Ferguson,

Beck, and Bolt 2010). Executive pay has quickly become the subject of public and media attention

and heated debates in the US Congress. In 2010, the Dodd-Frank Wall Street Reform and Consumer

Protection Act was signed into law. It included several important new rules to govern executive pay at

large public companies, for example, requiring large public companies to give shareholders a vote on

executive pay.

There has also been an explosion of research on managerial incentives and behavior in

academic literature. Research in marketing and accounting has documented that under certain

conditions, firms engage in earnings management (through accounting accruals and real activity

manipulation) to temporarily inflate earnings, and such manipulation has significant negative

consequences for the firm (Cohen and Zarowin 2010; Kothari at al. 2016, Bereskin et al. 2018).

Standard economic models suggest that private managerial incentives play a significant role in

inducing such behaviors. Specifically, theoretical models show that an overemphasis on stock price in

managerial evaluation and compensation can induce myopic management and/ or accounting

manipulation (e.g., Bizjak, Brickley, and Coles 1993; Croker and Slemrod 2007).

Accounting research has seen a surge of interest in studying the links between executive

compensation and accounting “irregularities” (i.e., accrual-based earnings manipulation). These

studies find support for the conclusions from the theoretical economic models: equity incentives

motivate executives to manipulate accounting information (Cheng and Warfield 2005; Bergstresser

and Philippon 2006; Jiang, Petroni, and Wang 2010).

Marketing Science Institute Working Paper Series 3

In the marketing literature there has also been an increased interest in studying the effects of

executive compensation (e.g., Bansal et al. 2016; Currim at al. 2012; Chakravarty and Grewal 2016).

Some authors have suggested that executive equity compensation might serve to reduce myopic

management such as cutting marketing spending to artificially inflate earnings (Currim at al. 2012;

Luo et al. 2012; Chakravarti and Grewal 2016). We investigate this proposition in detail. Further, the

role of chief marketing officers (CMOs) in preventing (or inducing) marketing myopia and the impact

of CMO compensation on myopic marketing management are unknown. These two key aspects—the

CMO compensation–myopic marketing management link and the relative role of CMOs in inducing

marketing myopia—are the focus of our study.

Specifically, we examine the role personal compensation incentives of a CMO and CEO play

in inducing myopic marketing management. We find that CEO equity incentives are largely unrelated

to the incidence and severity of myopic marketing management. CMO equity compensation, on the

other hand, is highly predictive of the incidence and severity of myopic marketing management.

Contrary to a common belief articulated in the marketing literature that the presence of a CMO in the

organization helps maintain customer focus, support funding for marketing departments, and ensure

consistent marketing strategy, we find CMOs not only fail to prevent myopia, but further exacerbate

the problem as the market-based (equity) portion of their personal compensation package increases.

Our analyses utilizing multiple methods designed to identify causal effects (e.g., inverse probability

weighted regression adjustment, Heckman selection bias correction, endogenous treatment effects,

control function, difference-in-differences) allow for a causal interpretation of these findings. Further,

we find that CMOs seek to benefit financially and take advantage of inflated equity valuation.

Consistent with the CMO’s personal enrichment motivation we find that CMOs exercise more stock

options and sell more of their personal equity holdings in the years when myopic management takes

place (i.e., when stock valuation is artificially inflated).

Marketing Science Institute Working Paper Series 4

EXECUTIVE COMPENSATION AND STRATEGIC BEHAVIOR

The Evolution of Academic Thought on Managerial Compensation

Economic research on managerial compensation has focused on the need to align managers’

incentives with those of the firm owner’s. The trajectory of the theoretical thought on the topic

closely parallels the contemporary issues and economic problems of the particular era.

In the 1980s and early 1990s, academics, shareholders, and activist groups pointed to the fact

that the pay practices established in the United States in the 1960s and 1970s were unsuitable for the

new economic reality and the dynamics of the 1980s and 1990s as the shareholder value creation

became more dependent on the organizational embrace of innovation and entrepreneurship. Most

academic and practitioners’ criticism of executive pay structure at the time emphasized the lack of

meaningful rewards for superior performance and penalties for failure. Both academics and

practitioners argued for the need to establish a closer link between pay and performance and to create

incentives to mitigate managerial risk aversion (Murphy 1999). This notion resulted in calls for tying

executive pay directly to changes in shareholder wealth to increase the sensitivity of executive pay to

stock price performance. The proliferation of the stock-based and stock options compensation

followed.

Equity-based compensation provides a direct link between managerial rewards and appreciation

of share price. Because the value of options increases with stock price volatility, executives holding

stock options have greater incentives to undertake riskier investments. Analytical models show that

option plans reduce agency costs because they incentivize long-term focus and mitigate executives’

risk aversion (Hirshleifer and Suh 1992). Empirical research confirms this finding—managers who

receive more stock-based compensation invest more in risky projects (Gormley, Matsa, and Milbourn

2013; Rajgopal and Shevlin 2002).

Early empirical studies investigating the effects of introducing equity incentives in executive

pay showed a significant positive effect on firm performance. For example, Brickley, Bhagat, and

Marketing Science Institute Working Paper Series 5

Lease (1985) reported a 2.4% abnormal stock return in the event study of firms adopting stock-based

compensation plans. Similarly, DeFusco, Johnson, and Zorn (1990) reported a .68% return for a two-

day event window and a 4.0% positive abnormal return when they included the potential leakage

period prior to the event in the analysis.

Yermack (1997) also reported that stock price increases tend to coincide with executive stock

option grants, even when these grants are not publicly announced. All these findings are consistent

with the predictions of the economic theory: tying managerial compensation to stock market

performance improves managerial incentives and reduces agency costs. Yermack (1997), however,

points out an alternative, more sinister, explanation that is also consistent with these findings:

executives push stock-based compensation through before positive news become public or before

they engage in manipulation of the stock price (also see Aboody and Kasznik 2000).

A new perspective on the equity-based compensation emerged at the turn of the 21st century: it

was now blamed for excessive risk-taking (Bebchuk and Fried 2006). The highly publicized

accounting scandals of the early 2000s further reinforced this perception and a new trend emerged—a

shift away from the stock options and toward restricted stock grants and cash bonuses. The Economist

(April 15, 2004, p.71) noted that the shareholders have finally “woken up to the perverse effects on

executive behavior of corporate pay, and especially of stock options,” and reported that the proportion

of compensation from stock options in 2004 reached its lowest level in seven years.1

Recently, however, some researchers have suggested that equity-based compensation may be

beneficial not only because it discourages risk aversion, but also because it may curb executive

opportunism and reduce myopic management (Currim et al. 2012; Luo et al. 2012). We seek to

investigate this proposition in detail. In the following section, we review relevant arguments in the

economic theory related to managerial compensation.

1 The use of stock options has further declined since that report, primarily due to the change in the accounting regulations that required expensing of the stock options starting in June 2005, which made options more costly for the firms to use in compensation.

Marketing Science Institute Working Paper Series 6

Compensation Effects in Incomplete Information Markets

In the theoretical models with standard assumptions of efficient markets and rational expectations, if

managers care about stock prices, they act in the best interests of the shareholders and make firm

value–maximizing business decisions. Standard efficient market models advocating equity-based

compensation relied on the assumption of perfect information, that is, full observability of managerial

actions, and the investors and managers having identical information. However, with the introduction

of information asymmetries into the standard model, the predictions and implications of equity-based

compensation for shareholder welfare change dramatically. Managers with private information about

the firm that is not available to the stock market or managers able to take unobservable actions may

engage in misreporting (i.e., accounting manipulation) or myopic management (i.e., real activity

manipulation) to maximize their personal compensation rather than to maximize firm value. That is,

under imperfect information, stock-price-based compensation contracts may create perverse

incentives for the managers.

(1) Myopic management: models and evidence. Hidden action models demonstrate the phenomenon

of myopic management (e.g., Narayanan 1985; Stein 1989). They start with the basic assumptions of

rationality, efficient markets, earnings persistence, and managerial utility function depending on the

stock price. Under these four assumptions, managers make efficient decisions and act in the best

interests of the owners (shareholders). Then, Stein (1989), for example, allows managers to take

actions (shift future income into the present, at some cost) that are not perfectly observable by the

owners. The owners can observe the distorted earnings but cannot decompose them into the “true”

and “borrowed” components. Under these conditions, managers have a higher discount rate than that

justified by cost-of-capital considerations (as it would be in the absence of asymmetric information).

This higher discount rate leads to an overemphasis on immediate performance outcomes. Stein (1989)

shows that the extent of myopia increases with the importance managers place on the current-term

stock price.

Marketing Science Institute Working Paper Series 7

Bizjak, Brickley, and Coles (1993) and Benmelech, Kandel, and Veronesi (2010) develop

private information models in which managers have better information about the value of the firm’s

investment opportunities. The investment choices managers make affect cash flows in the future. The

market does not have the same information as the managers about the value of the projects when the

project is undertaken. But by observing the future cash flows or dividends as they materialize

following an investment, the market eventually learns and becomes fully informed about investment

value. In this setting, an overemphasis on current stock price can prompt managers to manipulate the

market’s inferences about firm prospects through observable (however suboptimal) investment

choices. Bizjak et al. (1993) show that managers are more likely to engage in myopic manipulation as

the significance they attach to the current stock price (relative to future profits and future stock price)

increases. Benmelech et al. (2010) similarly find that managers facing equity-based compensation

incentives forego profitable investment opportunities in order to inflate current dividends. However,

because this myopic strategy cannot be maintained forever, at some point in the future, the true state

is revealed and the stock price declines sharply. Both models show that the more managerial

remuneration depends on current stock price, the more likely myopic behaviors are to occur.

Empirical research in marketing and accounting has documented that myopia indeed occurs in

practice (Roychowdhury 2006), can take various forms (Ahearne et al. 2016; Chapman and

Steenburgh 2010; Moorman et al. 2012; Wies and Moorman 2015), and has significant negative

performance consequences (Cohen and Zarowin 2010; Kothari et al. 2016; Kurt and Hulland 2013;

Mizik 2010). The role of the CMO and of the CMO personal compensation in inducing marketing

myopia, however, has not been examined.

Firms can artificially inflate earnings through accounting manipulation (mis-reporting) and/ or

real activity manipulation (myopic management). Because research into the drivers of myopic

management is rather scarce, we turn to a related and well-established stream of literature on financial

mis-reporting for insights.

Marketing Science Institute Working Paper Series 8

(2) Misreporting performance data: models and evidence. Bar-Gill and Bebchuk (2002), Crocker

and Slemrod (2007), and Goldman and Slezak (2006) model managerial incentives to truthfully report

firm performance. They show that performance-based compensation can induce managers to

misreport performance by engaging in accounting manipulation. Numerous empirical studies

examining the role of equity compensation find that it is significantly associated with accounting

earnings manipulation. For example, Cheng and Warfield (2005) report a positive association

between stock-based compensation and the magnitude of abnormal accruals (i.e., discretionary

components in reported earnings). They also find earnings are less informative (i.e., viewed by the

market as being less predictive of the future) in firms with higher stock-based executive

compensation. Bergstresser and Philippon (2006) find the use of discretionary accruals to manipulate

reported earnings is more pronounced in firms in which CEO compensation is tied to stock-based

incentives.

In sum, both the theoretical and the empirical evidence on accounting-based earnings

manipulation suggest that the extent of manipulation increases with the portion of market-based (i.e.,

equity) compensation in executive pay packages.

The Role of Different Members on the Top Management Team

Most of the empirical studies have focused on the role of CEO compensation, but more recent

research is turning its attention to the other members of the TMT. Several authors have argued that

the lower-level officers can be more influential in their domain than the CEOs. The incentives of the

CFOs, for example, may play a more prominent role in decisions requiring advanced financial

expertise. Jiang, Petroni, and Wang (2010) argue that because the CFO’s primary responsibility is

financial reporting, CFO equity incentives should play a stronger role than those of the CEO in

inducing accounting-based earnings management. Consistent with this argument, the authors find that

the accruals and the likelihood of beating analyst forecasts (i.e., two alternative proxies for

accounting-based earnings management) are more sensitive to CFO than to CEO equity incentives.

Marketing Science Institute Working Paper Series 9

Similarly, Kim, Li, and Zhang (2011) report that the sensitivity of the CFO’s portfolio value to stock

price changes is more strongly associated with the risk of future stock price crash (i.e., evidence of

potential stock price manipulation, Benmelech et al. 2010) than that of a CEO.

The empirical evidence on the link between equity incentives and myopic marketing

management is lacking, and CMOs have not received attention in research investigating the effects of

compensation structure on TMT behavior and firm strategy. The economics literature of incomplete

information unequivocally predicts a greater extent of myopic behaviors as managers’ interest in the

current stock price increases, and extending the logic of Jiang, Petroni, and Wang (2010) to marketing

domain would suggest that CMOs might have greater responsibility than other executives for myopic

marketing management. This logic, however, runs contrary to the views on the role and power of

CMOs dominant in the marketing literature.

THE ROLE OF THE CMO

CMO Power and the Scope of Responsibilities

One popular (pessimistic) view contends that the influence of marketing within organizations is

waning. Supporters of this view refer to an often-cited SpencerStewart study (Welch 2004) reporting

that CMO tenures typically last about 23 months.2 Most notably, Webster, Malter, and Ganesan

(2005) declare that the marketing function is in steep decline in many organizations. They highlight

(a) the inability of marketers to document marketing’s contribution to the bottom line, (b) an

emphasis on short-term revenues, market share, and stock price, and (c) a shift in channel power as

the primary causes for this trend. The authors argue the question now is not how to rebuild a

marketing center, but rather how to disperse marketing competence across the organization. They call

for building a “small [marketing] ‘center of excellence’” and argue this center “should not be

responsible for developing or implementing marketing strategies,” but rather “it should be the

repository for expert knowledge about the customers and it should manage process for developing and

2 Our data show the average CMO tenure at 5.4 years (about 65 months), just a year shorter than that of a COO.

Marketing Science Institute Working Paper Series 10

disseminating that knowledge” (pp. 42, 43). Under this view, the CMOs are unrelated to myopic

management because they are neither responsible for nor capable of directly influencing firm strategy.

In sharp contrast to this view, an alternative (optimistic) view (e.g., Aaker 2008; Jaworski 2011;

Feng, Morgan, Rego 2015) touts the rising power of the CMOs. Marketers’ credibility and power

comes from owning customer knowledge and market intelligence, and with the ever-increasing

market complexity, the influence of marketing is only bound to increase. Understanding, managing,

and responding to market complexity requires highly specialized capabilities and skills, which are

outside the scope of competency of generalist marketers at the SBU (strategic business unit) level.

Supporters of this view advocate building and strengthening the central marketing group with the key

responsibility of overseeing marketing strategy, and they put the CMO at the center of this structure.

Aaker (2008) views the CMO as the central force to mitigate marketing resource misallocation, create

more coherent and linked marketing strategies, leverage success, and improve communication and

cooperation within organization. He argues that without a centrally driven discipline, internal resource

allocation is driven by politics, and firm resources are often diverted to the largest, rather than the

most promising, areas and markets. Under this view, CMOs are directly responsible for and capable

of preventing myopic marketing management.

Practitioners tend to support the optimistic view. Dahlstrom et al. (2014) note a proliferation of

C-suite titles that include a component of marketing, and argue that the role of CMOs has been

elevated in recent years. Neff (2010) too trumpets the increasing power of the CMOs. He finds the

new crop of CMOs is centralizing control over communications, brand-building, PR, design, market

research, and digital. He argues these new-generation CMOs are leading a significant change and are

becoming far more prevalent, successful, and powerful than their predecessors.

Empirical Evidence on the Role and Effects of CMOs

Most academic studies of CMOs focus on the effect of CMOs on firm performance and typically

report that it is positive (e.g., Germann at al. 2015). Several studies examined the CMO characteristics

Marketing Science Institute Working Paper Series 11

(origin, education, marketing and industry experience) and report their impact on firm value (Wang et

al. 2015), likelihood of external funding for new ventures (Homburg et al. 2014), and show how the

effect varies depending on environmental and firm-specific factors (Nath and Mahajan 2008, 2011;

Boyd et al. 2010).

Bansal et al. (2016) and Kim at al. (2016) are the only studies we know to systematically

examine the determinants of CMO compensation and link it to firm performance. The authors find

that CMOs employed at firms with high advertising and R&D intensity, and operating in competitive

product markets, command larger amounts of total compensation and that a greater proportion of their

compensation is market-based. Bansal et al. (2016) also report that the absolute deviations in the

compensation elements of top marketing executives from their predicted level (which serves as the

authors’ proxy for optimal compensation) have a symmetric negative association with firm

performance as measured by contemporaneous ROA, earnings surprises, and annualized stock

returns. Kim et al. (2016), on the other hand, report a positive linear association between CMO equity

incentives and the market value of the firm.

The studies linking CMO compensation and myopic practices are lacking. Currim et al. (2012)

and Chakravarty and Grewal (2016) studies are, to the best of our knowledge, the only to examine the

effects of TMT compensation on firm marketing strategy.3 Specifically, Currim et al. (2012) examine

risk aversion as related to R&D and advertising spending. The authors find that increases in equity-to-

bonus compensation ratios of the top five TMT members have a positive association with increases in

risky and uncertain projects—advertising and R&D spending as a percentage of sales. This finding is

fully consistent with the predictions of economic theory: equity-based compensation reduces risk

3 Other marketing researchers have examined some marketing aspects related to TMT compensation. For example, Tavassoli, Sorescu, and Chandy (2014) examine total compensation packages of top executives and find that firms with strong brands pay their executives less than other firms and that this effect is stronger for CEOs and younger executives. O’Connell and O’Sullivan (2011) study the impact of customer satisfaction on CEO bonuses and equity compensation. Luo, Homburg, and Wieseke (2012) suggest the reverse link: equity-based CEO compensation is the driver of customer satisfaction because CEOs invest more in long-term relations with customers and internal employees.

Marketing Science Institute Working Paper Series 12

aversion. Based on their findings, the authors take a step further to suggest that equity-based

compensation schemes to incentivize long-term orientation may also mitigate myopic management of

resources. They argue that “equity-based compensation is a motivational tool that can encourage

longer-term orientation, discourage myopic management of resources or short-term opportunism” (p.

36). That is, executives’ equity pay may help decrease myopic marketing management. Chakravarty

and Grewal (2016) consider and find a positive moderating effect of the current-year bonus-to-equity

ratio in the CEO compensation (i.e., the inverse of the Currim et al. 2012 focal metric) on propensity

to cut advertising and R&D spending. Consistent with Currim et al. (2012) propositions, the authors

suggest that CEO bonus (rather than current-year equity award) induces short-term orientation and

increases propensity to myopically cut advertising and R&D.

In sum, the optimistic view on the role and power of CMOs has greater empirical support and

appears to dominate in more recent discussions. Under this optimistic view, CMOs are responsible for

and capable of directly influencing firm strategy and curtailing myopic marketing management.

Moreover, because it encourages long-term orientation, CMO equity compensation is argued to

motivate CMOs to reduce myopic marketing management.

HYPOTHESES

The CMO is a top firm executive with the primary responsibilities for overseeing the overall

marketing strategy in the organization, for gathering, analyzing, and disseminating market

intelligence, and for defining and shaping marketing philosophy and process (Aaker 2008; Court

2007; Jaworski 2011). All these responsibilities are the key inputs into the top decision-making and

strategy setting within the firm. As such, the mere presence of a CMO in TMT can potentially reduce

the extent of myopic marketing:

Hypothesis 1 (H1): The presence of a CMO in a firm reduces the extent of myopic marketing management.

Under the pessimistic view on CMOs there would be no effect of CMO presence because

CMOs have no power to affect strategy. But under the positive view of CMOs dominating marketing

Marketing Science Institute Working Paper Series 13

literature, CMOs are responsible for and capable of stemming myopic marketing management and,

therefore, this effect would be negative—that is, CMO presence would help curb marketing myopia.

Economic theory predicts that managers with high equity incentives are motivated to

artificially inflate earnings to increase stock price value and correspondingly their personal

compensation. They may do so by engaging in myopic marketing management:

Hypothesis 2 (H2): The more executive compensation depends on equity, the greater the extent of myopic marketing management.

CEOs have the greatest influence on strategic decisions and a final decision authority

(Finkelstein and Hambrick 1996). However, the CMOs have immediate control over and

responsibility for managing marketing budgets and assets. As such, they might be in a better position

than other members of the TMT, including the CEO, to affect myopic marketing management. This

argument suggests the following hypothesis:

Hypothesis 3 (H3): CMO equity incentives have a greater association with myopic marketing management than those of the CEO.

Under the standard economic theory, the effect of CMO compensation on the extent of myopic

marketing management would be positive—that is, CMO equity compensation would induce more

marketing myopia. Under the positive view on CMOs, the effect would be negative—that is, CMO

equity pay (reflecting CMO power) would curb myopia. These two views contrast the importance and

priority CMOs attach to the demands and responsibilities of their job (to oversee marketing strategy

and to advocate for and support marketing functions) versus their personal financial gain. If CMOs

are enabling myopic marketing management, their equity incentives would play a stronger role in

inducing myopic marketing management than those of other executives (e.g., CEOs).

Further, if we find evidence consistent with CMOs inducing myopic marketing management,

(i.e., H2 and H3 hold, and H3 effect is positive) we would also expect CMOs to try benefit financially

from this manipulation. If managers deliberately engage in myopic marketing management to inflate

firm valuation, then, anticipating an inevitable future decline in stock price, they would seek to

Marketing Science Institute Working Paper Series 14

capitalize on the situation. That is, CMOs would seek to take advantage of inflated stock prices and

sell more of their equity holdings in the years when earnings and firm valuation are artificially

inflated through myopic marketing management:

Hypothesis 4 (H4): The CMOs take advantage of artificially inflated equity valuations in the years when myopic marketing management occurs and sell more of their equity holdings than in other years.

Even if CMOs are not driving marketing myopia (i.e., H3 does not hold) we may still find

CMOs accelerating divesting of their equity holdings in the years when myopic marketing

management takes place. While CMOs may not be powerful and may not be able to affect firm

strategy, they might be better informed and/or they might have better insight about the future negative

consequences of marketing myopia than other members of TMT. This insight would motivate them to

opportunistically take advantage of the inflated equity valuation and sell their personal equity

holdings.

DATA SAMPLE AND MEASURES

Data Sources

We combine data from multiple sources for our study. Executive compensation and options exercise

data come from the ExecuComp database, stock returns from the Center for Research in Security

Prices (CRSP), accounting data from Compustat, and insider-trading data from the Thomson Reuters

Insider Filing Data Feed (IFDF). Our sample covers all public firms in these databases in the 1993-

2014 period. We limit the sample to firms reporting Net Income, SGA, R&D, and positive values for

Total Assets, Sales, Employees, and Book Value of Equity. We winsorize the data at the 1% level to

restrict the influence of outliers. We exclude firms in the utility (SIC 4400–5000), financial (SIC

6000–7000), and public administration (SIC 9000-9900) sectors because these firms operate in highly

regulated environment with accounting rules that differ substantially from those in other industries.

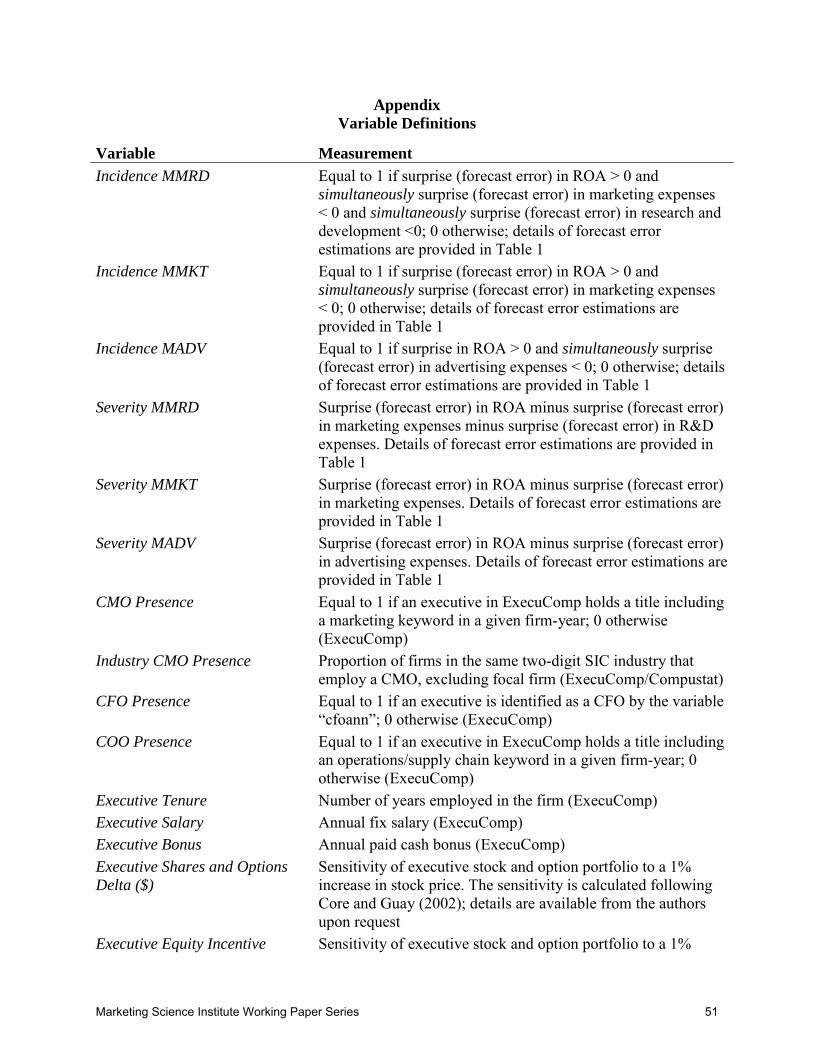

All variable definitions are in the Appendix. We describe key research constructs and their

measurement below.

Marketing Science Institute Working Paper Series 15

Measuring the Extent of Myopic Marketing Management: Incidence and Severity

(1) Identifying Myopic Marketing Management with Secondary Data

Myopic behaviors are not directly observable or measurable and as such require forming indicators

for inferring whether myopic management has occurred. Past research has established econometric

methods for identifying the incidence of myopic management (e.g., Kothari et al. 2016) and we

closely follow this literature. Incidence is a binary indicator reflecting whether or not a firm likely

engaged in myopic management in a given year. A firm is classified as potentially myopic if it shows

a positive earnings surprise (unexpectedly high earnings) and a simultaneous negative surprise

(unexpected cut) in marketing spending.

Because a direct clean measure of marketing spending is not available in financial reports, we

undertake analyses using three different proxies for marketing myopia to test our hypothesis. The first

is a proxy for myopic marketing and R&D management (MMRD) introduced in Mizik (2010). The

second is myopic marketing management (MMKT) proposed in Mizik and Jacobson (2007). The

third is myopic advertising management (MADV). The three measures differ in how closely they

capture marketing-related spending and the CMO control over this spending:

(1) Myopic Marketing and R&D Management (MMRD) measure considers both marketing and R&D

cuts at the time of unexpectedly high earnings and, as such, reflects a more widespread myopic

behavior in the firm (Mizik 2010). While this measure fully captures marketing spending, it is broader

and captures more than myopic marketing management. Other TMT members, such as the CEO,

typically have greater control over R&D expenses and CMO influence is likely to be less pronounced.

As such, we might see greater association of CEO incentives and a weaker support for H3 with this

measure.

(2) Myopic Marketing Management (MMKT) measure only considers marketing spending and

earnings (i.e., does not consider R&D cuts) and, as such, is closer to better capturing the marketing-

related myopia (Mizik and Jacobson, 2007). It is based on selling, general, and administrative

Marketing Science Institute Working Paper Series 16

expenditures (SGA) minus R&D expenditures (MKT=SG&A-R&D). It covers all marketing

spending. While it is still broader than “pure” marketing (it includes non-marketing SGA items that

are outside of the CMO control), we might see stronger CMO findings with MMKT than with the

MMRD metric.

(3) Myopic Advertising Management (MADV) measure is based on advertising and is a very narrow

proxy for marketing-related spending. Clearly, marketing encompasses many other expense

categories, not just advertising. As such, a cut in advertising is a likely, but not a guaranteed, evidence

of myopic marketing management. A cut to advertising might occur when a firm is re-balancing its

marketing budget and shifting advertising dollars into other marketing expense categories (e.g.,

promotions, free sampling, loyalty programs, etc.) Under a re-balancing scenario, MADV might

indicate myopia, but MMKT would correctly indicate no myopia. Nevertheless, analyses of MADV

are insightful as we would expect a CMO to have tighter control over advertising compared to the

expense categories included in MMRD and in MMKT measures and would expect other executives to

have no or little effect on advertising-based myopic marketing management.

It is worthwhile examining all three measures for establishing confidence in our findings: While

no proxy is perfect, as a set, these three measures provide insights into the extent of myopic

marketing management and the scope of CMO association with it.

(2) Operationalization of the MMRD, MMKT, and MADV Proxies

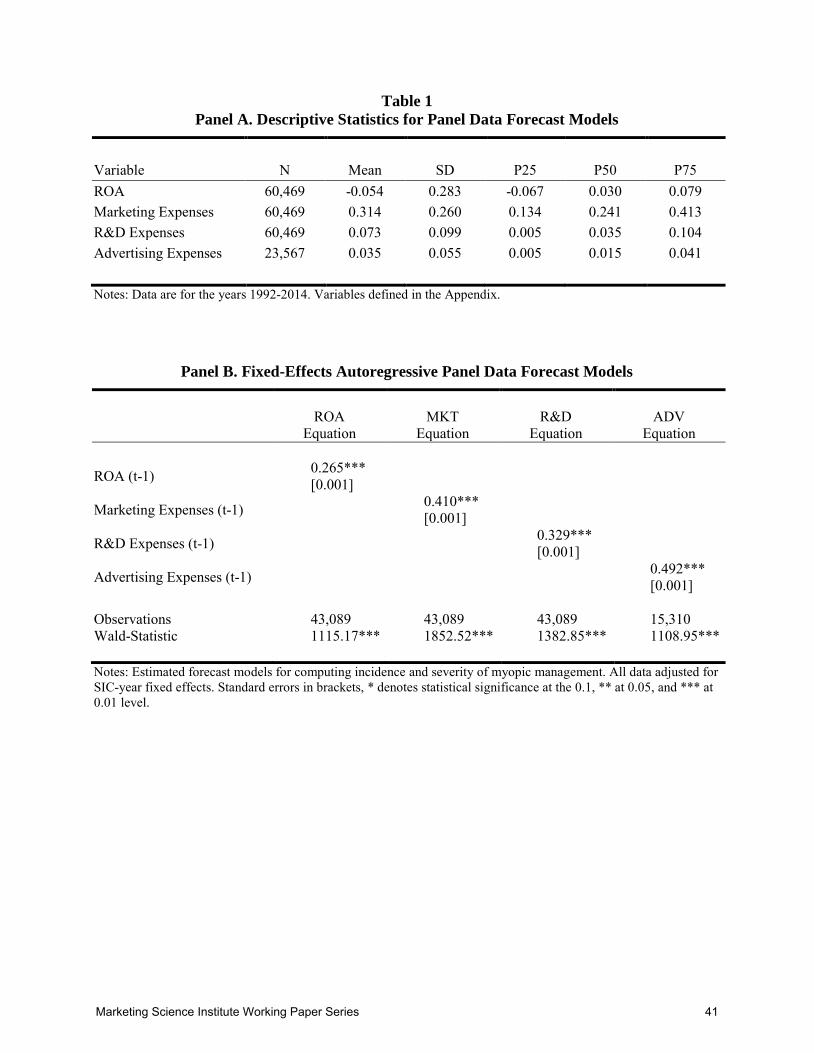

Following prior research (e.g., Kothari, et al. 2016) we use the following fixed-effects autoregressive

panel data forecast models to generate our proxies of myopic management. We use these models to

estimate next-period normal (expected) levels of profitability, marketing, R&D, and advertising

spending:

(1) 𝑅𝑅𝑅𝑅𝑅𝑅𝑖𝑖𝑖𝑖 = 𝛼𝛼𝑅𝑅𝑅𝑅𝑅𝑅,𝑖𝑖 + 𝜑𝜑𝑅𝑅𝑅𝑅𝑅𝑅 𝑅𝑅𝑅𝑅𝑅𝑅𝑖𝑖𝑖𝑖−1 + ∑δ𝑅𝑅𝑅𝑅𝑅𝑅,𝑠𝑠𝑖𝑖𝑠𝑠_𝑖𝑖 𝑆𝑆𝑆𝑆𝑆𝑆_𝑌𝑌𝑌𝑌𝑌𝑌𝑌𝑌𝑠𝑠𝑖𝑖𝑠𝑠_𝑖𝑖 + ε𝑅𝑅𝑅𝑅𝑅𝑅,𝑖𝑖𝑖𝑖;

(2) 𝑀𝑀𝑀𝑀𝑀𝑀𝑖𝑖𝑖𝑖 = 𝛼𝛼𝑀𝑀𝑀𝑀𝑀𝑀,𝑖𝑖 + 𝜑𝜑𝑀𝑀𝑀𝑀𝑀𝑀 𝑀𝑀𝑀𝑀𝑀𝑀𝑖𝑖𝑖𝑖−1 + ∑δ𝑀𝑀𝑀𝑀𝑀𝑀,𝑠𝑠𝑖𝑖𝑠𝑠_𝑖𝑖 𝑆𝑆𝑆𝑆𝑆𝑆_𝑌𝑌𝑌𝑌𝑌𝑌𝑌𝑌𝑠𝑠𝑖𝑖𝑠𝑠_𝑖𝑖 + ε𝑀𝑀𝑀𝑀𝑀𝑀,𝑖𝑖𝑖𝑖;

(3) 𝑅𝑅&𝐷𝐷𝑖𝑖𝑖𝑖 = 𝛼𝛼𝑅𝑅&𝐷𝐷,𝑖𝑖 + 𝜑𝜑𝑅𝑅&𝐷𝐷 𝑅𝑅&𝐷𝐷𝑖𝑖𝑖𝑖−1 + ∑δ𝑅𝑅&𝐷𝐷,𝑠𝑠𝑖𝑖𝑠𝑠_𝑖𝑖 𝑆𝑆𝑆𝑆𝑆𝑆_𝑌𝑌𝑌𝑌𝑌𝑌𝑌𝑌𝑠𝑠𝑖𝑖𝑠𝑠_𝑖𝑖 + ε𝑅𝑅&𝐷𝐷,𝑖𝑖𝑖𝑖;

Marketing Science Institute Working Paper Series 17

(4) 𝑅𝑅𝐷𝐷𝐴𝐴𝑖𝑖𝑖𝑖 = 𝛼𝛼𝑅𝑅𝐷𝐷𝐴𝐴,𝑖𝑖 + 𝜑𝜑𝑅𝑅𝐷𝐷𝐴𝐴 𝑅𝑅𝐷𝐷𝐴𝐴𝑖𝑖𝑖𝑖−1 + ∑δ𝑅𝑅𝐷𝐷𝐴𝐴,𝑠𝑠𝑖𝑖𝑠𝑠_𝑖𝑖 𝑆𝑆𝑆𝑆𝑆𝑆_𝑌𝑌𝑌𝑌𝑌𝑌𝑌𝑌𝑠𝑠𝑖𝑖𝑠𝑠_𝑖𝑖 + ε𝑅𝑅𝐷𝐷𝐴𝐴,𝑖𝑖𝑖𝑖,

where ROAit, MKTit, R&Dit, and ADVit, are the profitability (net income), marketing (SGA-R&D),

R&D, and advertising spending of firm i in year t scaled by total assets and ROAit-1, MKTit-1, R&Dit-1,

and ADVit-1, are their lagged values. SIC_Yearsic_t is the year-specific industry fixed effect.

Coefficient 𝛼𝛼𝑖𝑖 is the firm-specific constant and 𝜑𝜑s are the first-order autoregressive coefficient

estimates. To estimate these models, we use Arellano and Bond (1991) approach which allows for a

consistent estimation of these dynamic fixed effects models. Table 1 reports the descriptive statistics

for the data and the estimation results for models 1-4. Our descriptives and estimates are closely in

line with past research.

We use the deviations of the actual values from the forecasts (i.e., forecast errors) as the

measure of abnormal profitability (aROAit) and abnormal spending levels (aMKTit, aR&Dit, aADVit).

Firms simultaneously reporting greater-than-normal profitability (aROAit>0) and lower-than-normal

spending are more likely to have engaged in myopic marketing management than other firms. As

such, our measures of the incidence are defined as follows:

Myopic Mkt_RD Management: Incidence MMRDit =1 if aROAit>0 and aMKTit<0; aR&Dit<0, 0 otherwise.

Myopic Marketing Management: Incidence MMKTit =1 if aROAit>0 and aMKTit<0, 0 otherwise.

Myopic Advertising Management: Incidence MADVit =1 if aROAit>0 and aADVit<0, 0 otherwise.

A total of 20% of our sample observations are classified as potentially engaging in myopic

management with regard to both, MKT and R&D, 30% with regard to MKT, and 26% with regard to

advertising.

Severity of myopic marketing management refers to the magnitude of myopia. Past research has

not considered the construct of severity of myopic management, and no metrics have been developed

for it. We propose measuring severity as a differential between the abnormal profitability and

abnormal spending (i.e., how much of a spending cut occurs at a given level of ROA increase). The

greater the cut and the higher the ROA surprise, the more severe is the myopia:

Marketing Science Institute Working Paper Series 18

Myopic Mkt_RD Management: Severity MMRDit = aROAit - aMKTit - aR&Dit;

Myopic Marketing Management: Severity MMKTit = aROAit - aMKTit;

Myopic Advertising Management: Severity MADVit = aROAit - aADVit.

These measures are highest when a firm has a positive earnings surprise and a negative surprise

in spending. It is lowest in case of a negative earnings surprise and positive surprise in spending

(indicating investment into marketing, R&D, or advertising and no myopic management taking

place).

Executive Compensation and Equity Incentives Measure

The ExecuComp database provides executive compensation for S&P500 companies. The information

is provided by the companies in accordance with the SEC rules on reporting executive compensation

and is compiled from 10-K reports and other public sources. We use data item CEOANN to identify

CEO data and restrict our sample to firms with CEOs. Because CMOs can have various titles, we

search the database item TITLEANN for marketing-related key words. We classify an executive as a

CMO if the job title includes keywords such as "marketing," "CMO," "customer," "brand," "channel,"

"product," "pricing," or "advertising." In the very few cases when multiple individuals are identified

in our search in a given firm-year, we select the one with the highest total compensation package for

our sample. CMO Presence is an indicator variable equal to one if a CMO is identified in a given

firm-year and zero otherwise. We are able to identify a CMO in 38% of observations in our data

sample.

We follow Bergstresser and Philippon (2006) in constructing a measure of executive equity

incentives that arise from stock-based compensation and stock ownership. This measure represents

the share of the executive’s total compensation that would arise from a 1% increase in the value of

stock price of his/ her company. The numerator is the dollar change in the value of an executive’s

stock and options holdings that would come from a 1% increase in the company stock price. The

denominator is the total amount of compensation the executive realizes in a given year under a 1%

Marketing Science Institute Working Paper Series 19

increase in stock price:

𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸 𝑆𝑆𝐼𝐼𝐼𝐼𝑌𝑌𝐼𝐼𝐸𝐸𝐸𝐸𝐼𝐼𝑌𝑌𝑗𝑗𝑖𝑖𝑖𝑖 = 𝐷𝐷𝐷𝐷𝐷𝐷𝑖𝑖𝐷𝐷 𝑆𝑆𝑖𝑖𝑆𝑆𝑠𝑠𝑆𝑆𝑠𝑠𝑗𝑗𝑗𝑗𝑗𝑗+𝐷𝐷𝐷𝐷𝐷𝐷𝑖𝑖𝐷𝐷 𝑅𝑅𝑝𝑝𝑖𝑖𝑖𝑖𝑆𝑆𝑝𝑝𝑠𝑠𝑗𝑗𝑗𝑗𝑗𝑗(𝑆𝑆𝐷𝐷𝐷𝐷𝐷𝐷𝑆𝑆𝑆𝑆𝑗𝑗𝑗𝑗𝑗𝑗+𝐵𝐵𝑆𝑆𝑝𝑝𝐵𝐵𝑠𝑠𝑗𝑗𝑗𝑗𝑗𝑗+𝐷𝐷𝐷𝐷𝐷𝐷𝑖𝑖𝐷𝐷 𝑆𝑆𝑖𝑖𝑆𝑆𝑠𝑠𝑆𝑆𝑠𝑠𝑗𝑗𝑗𝑗𝑗𝑗+𝐷𝐷𝐷𝐷𝐷𝐷𝑖𝑖𝐷𝐷 𝑅𝑅𝑝𝑝𝑖𝑖𝑖𝑖𝑆𝑆𝑝𝑝𝑠𝑠𝑗𝑗𝑗𝑗𝑗𝑗)

, where

𝐷𝐷𝑌𝑌𝐷𝐷𝐸𝐸𝑌𝑌 𝑆𝑆𝐸𝐸𝑆𝑆𝐼𝐼𝑆𝑆𝑆𝑆𝑗𝑗𝑖𝑖𝑖𝑖 is the sensitivity of executive j stock holdings to a 1% increase in stock price of his

company i in year t. It is equal to .01*Priceit*Sharesjit. Delta Optionsjit is the sensitivity of executive

j’s options holdings to a 1% increase in stock price (i.e., the amount of individual’s wealth created by

a 1% equity appreciation). Following Core and Guay (2002), we compute Delta Optionsjit using the

Black-Scholes options formula.4 This equity incentive measure differs fundamentally from

compensation measures in Chakravarty and Grewal (2016), Currim et al. (2012), and Bansal et al.

(2016) in that it reflects total compensation, including all executive’s shares and options from prior

year grants, and not just the current-year newly granted equity awards.

Executive Insider Trading Measures

We consider two measures of equity trading by executives: option exercises and shares trading. Our

first measure of selling activity, Share of Options Exercised, is based on ExecuComp data and is

defined as the ratio of options exercised in a given year to the total number of exercisable options an

executive holds that year (Erickson, Hanlon, and Maydew 2006). Because almost all executive stock

option exercises in the United States are followed by share sales, this measure reflects the intensity of

equity selling. Higher values indicate greater selling activity.

Our second measure of equity trading by executives is based on Thomson Reuters Insider

Filing Data Feed (IFDF) data. It tracks trading of securities (purchases and sales) by individuals with

access to non-public company information. Following Khan and Lu (2013), Net Trading is defined as

the difference of share purchases and share sales in a given year by an executive deflated by the total

number of firm shares outstanding. Positive values represent net insider purchases (accumulation) and

negative values reflect net insider sales (divesting).

4 A detailed description can be found in Core and Guay (2002), Bergstresser and Philippon (2006), and is available from the authors upon request.

Marketing Science Institute Working Paper Series 20

Descriptive Statistics

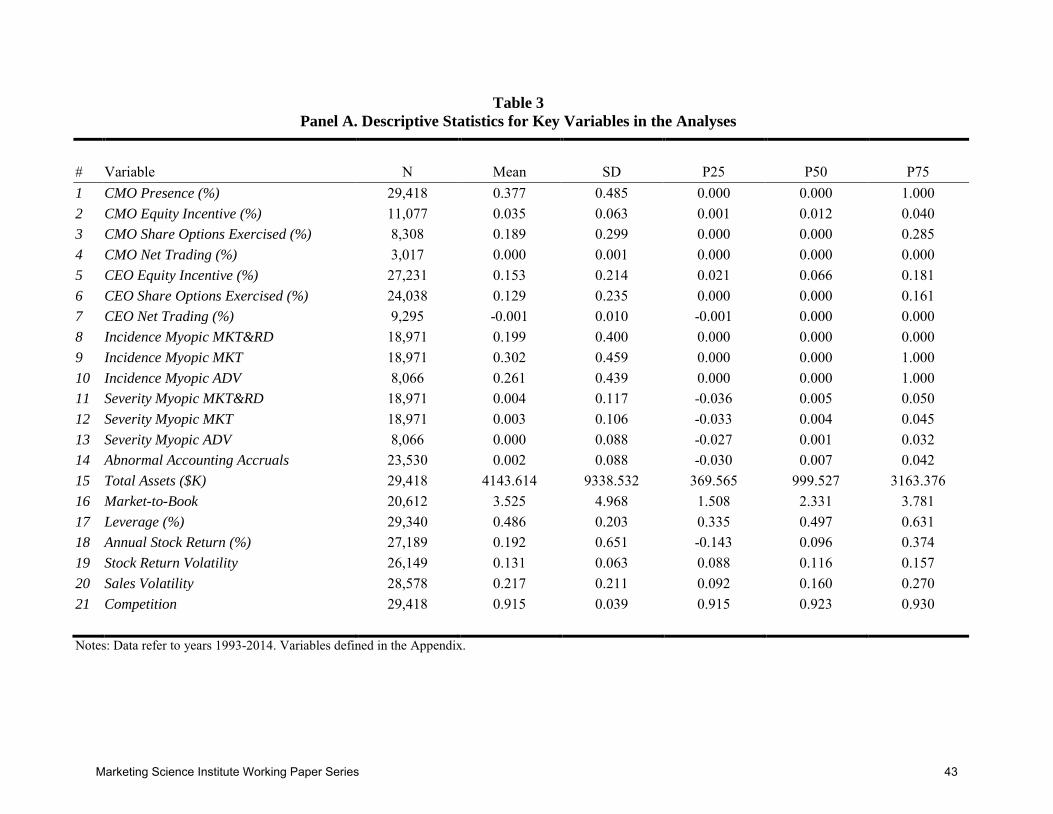

We summarize the definition and measurement for all control variables in the Appendix. We consider

a comprehensive set of control variables. This list includes controls used in prior research on

accounting misreporting and myopic management, executive compensation, insider trading, and

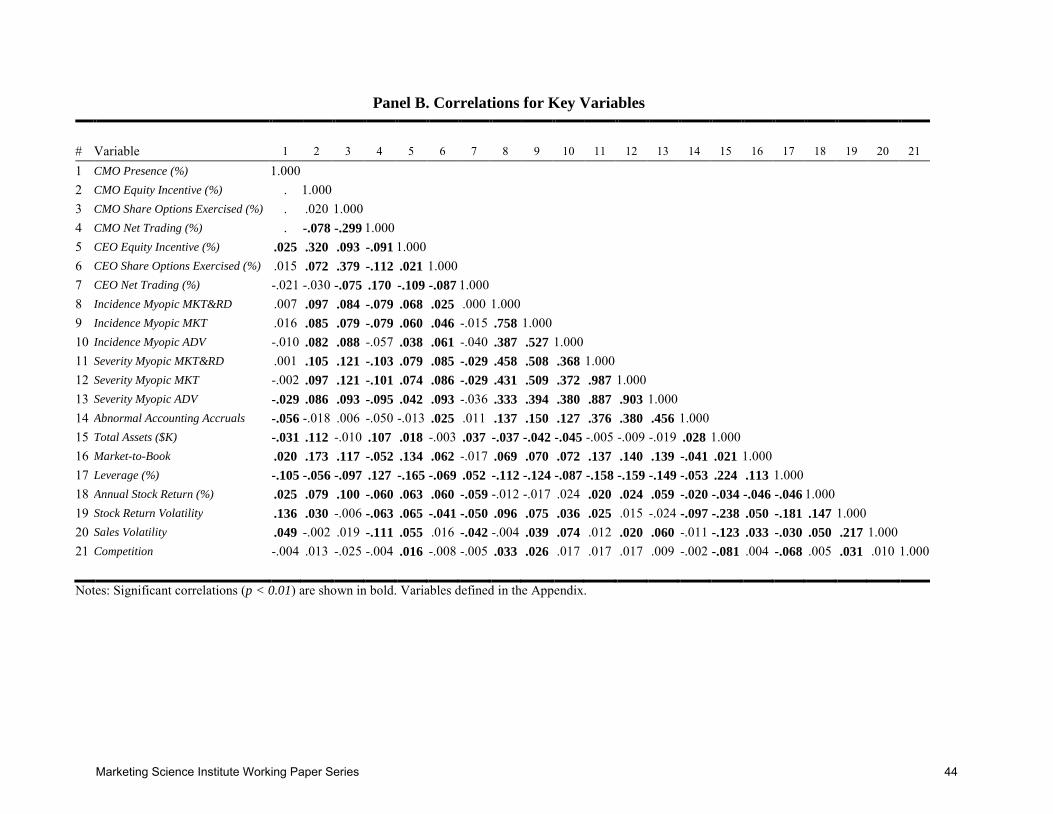

CMO characteristics. Tables 2 and 3 provide descriptive statistics for our sample and Table 3 Panel B

presents pairwise correlations. They show our sample characteristics are closely in line with those in

prior studies (e.g., Jiang, Petroni, and Wang 2010; Kim, Li, and Zhang 2011).

As reported in Table 2, CMOs are present among top paid executives in approximately 38% of

the observations in the sample (compared to CFOs in 88% and COOs in 52%). A closer analysis of

our data reveals an increase in CMO prominence over the years: whereas only about 27% of the firms

had a CMO on their TMT in 1993 (the first year of our data sample), CMO presence increases to and

hovers at about 41% in the 2000-2014 period. Further, we find that CMO salary, bonus, and equity

incentives are considerably lower than those of the CEOs, but are rather comparable to those of

CFOs. Contrary to an often cited statistic of CMOs having a short 23-months tenure, we find that an

average CMO tenure in our sample is 5.4 years (65 months), compared to 6.46 for COO, 7.74 for

CFO, and 8.26 years for CEO.5 In sum, we find CMOs are increasingly prevalent in TMTs and while

their compensation is lower than that of CEOs, it is rather comparable to that of other top executives.

Further, we find no evidence to support the claim that CMO tenures are very short.

RESEARCH DESIGN

Testing Hypothesis 1: CMO Presence

H1 suggests that CMO presence in an organization can reduce the extent of myopic marketing

5 The 23-months statement originates with the 2004, 2005, and 2006 SpencerStewart studies (e.g., Welch 2004). A follow-up CMO tenure study by SpencerStewart conducted in 2011 reported a 42-month average CMO tenure and attributed it to “the fact that CMOs have firmly established themselves among their peers in the C-suite" (SpencerStewart, May 24, 2011). The most recent estimate is again at 42-months (SpencerStewart, March 2017, https://www.spencerstuart.com/research-and-insight/chief-marketing-officer-average-tenure-drops-to-42-months). These estimates are clearly much lower than the 65-months average for the public US firms derived from the SEC filings.

Marketing Science Institute Working Paper Series 21

management. Results of basic regressions (logit for incidence, OLS for severity) with a dummy

variable for CMO presence suggest that CMO presence is not associated with either the incidence or

severity of myopia for any of our three myopia proxies. A concern with this basic approach is that

these models and their estimates might suffer from selection bias leading to erroneous inferences

about the effect.

Selection bias occurs when the potential outcome (myopic behavior) for those assigned or self-

selected to the “treatment group” (CMO present) differs in a systematic way from those who are

assigned or self-selected into the “control” or “no-treatment group” (Rossi 2017). Firm’s choice of

employing a CMO with a pay rate among its top-paid executives may be not random, but rather

driven by firm-specific and/or environmental factors. If the same factors are also associated with

myopic management, basic models ignoring this issue could suffer from selection bias.

A large stream of literature on causal inference in economics offers tools for dealing with

selection issues (Angrist and Pischke 2009; Imbens and Rubin 2015).6 One popular estimator for

addressing potential selection issues is the inverse probability weighted regression adjustment

(IPWRA). Imbens and Wooldridge (2009) specifically advocate combining propensity score

weighting with regression adjustment because of the desirable resulting properties of this estimator.

The method is consistent, asymptotically efficient, doubly-robust (i.e., only one of the two models,

the selection or the regression adjustment, must be correctly specified to consistently estimate the

treatment effects), and performs well in small samples (Busso et al. 2014; Imbens and Rubin, 2015).

Comparative tests of alternative treatment effects estimators tend to show IPWRA superiority over

IPW and over matching methods (Busso et al. 2014; Gordon et al. 2017).

The IPWRA approach models both, the outcome and the treatment (selection), and consists of

two steps. First, a selection model is developed to predict the likelihood of a firm employing a CMO.

6 We refer the reader to an excellent summary by Imbens and Wooldridge (2009) who review the foundations and recent advancements in the econometrics of causal effects estimation and offer practical recommendations to empiricists.

Marketing Science Institute Working Paper Series 22

Then, the outcomes are conditioned on the probability of CMO presence. That is, the observations on

the outcome variable are weighted by the inverse of the probability that it is observed. The inverse

probability weighting, in effect, adjusts the data to create a pseudo-population such that there is no

confounding on observables and the weighted averages reflect averages in the true population, thus

eliminating selection bias.

(1) Selection Model for CMO Presence. We follow Hirano and Imbens (2001) and Imbens and Rubin

(2015) for finding appropriate specification for the propensity score model. That is, we assemble a

large set of potentially relevant factors and use a logit specification (probit generates statistically

identical results) and a step-wise approach, setting the significance threshold at 10% with clustered

standard errors, to identify relevant factors.

We begin to assemble our set of potential explanatory factors for CMO Presence with the set of

factors reported in the CMO literature (e.g., Bansal et al. 2016, Nath and Mahajan 2008): Advertising,

R&D, Capital Expenditure, Size, Market-to-Book, Leverage, Stock Return Volatility, CEO Tenure,

Insider CEO, COO Presence, Firm Diversification, Competition, and Industry Use of CMO. Next, we

add variables that, in our opinion, logically complement the initial set. We add CFO Presence, CFO

Tenure, and COO Tenure to complete the initial set; and we add CMO Presence in the Prior Year

because we expect CMO Presence to persist over time. Finally, we include all variables potentially

affecting the outcomes we are investigating (myopia) that are entering the second stage of the

estimation (regression adjustment) and are not already included on the list above. Inclusion of all

second-stage variables is advised by Busso et al. (2014, p.897) who assess performance of various

estimators and specifications of treatment effects models and conclude that researchers should include

any covariates believed to influence the outcome variable (second stage) into the propensity score

model (first stage) because doing so provides “insurance against bad bias.” That is, our initial set also

includes the following factors explaining myopia from the second stage of the estimation: CEO

Equity Incentive, Abnormal Accruals, Annual Stock Return, Sales Volatility, and Year fixed effects.

Marketing Science Institute Working Paper Series 23

Only a few of the factors we consider for our CMO Presence (selection) model are relevant in

our sample. Our final selection model has the following form:

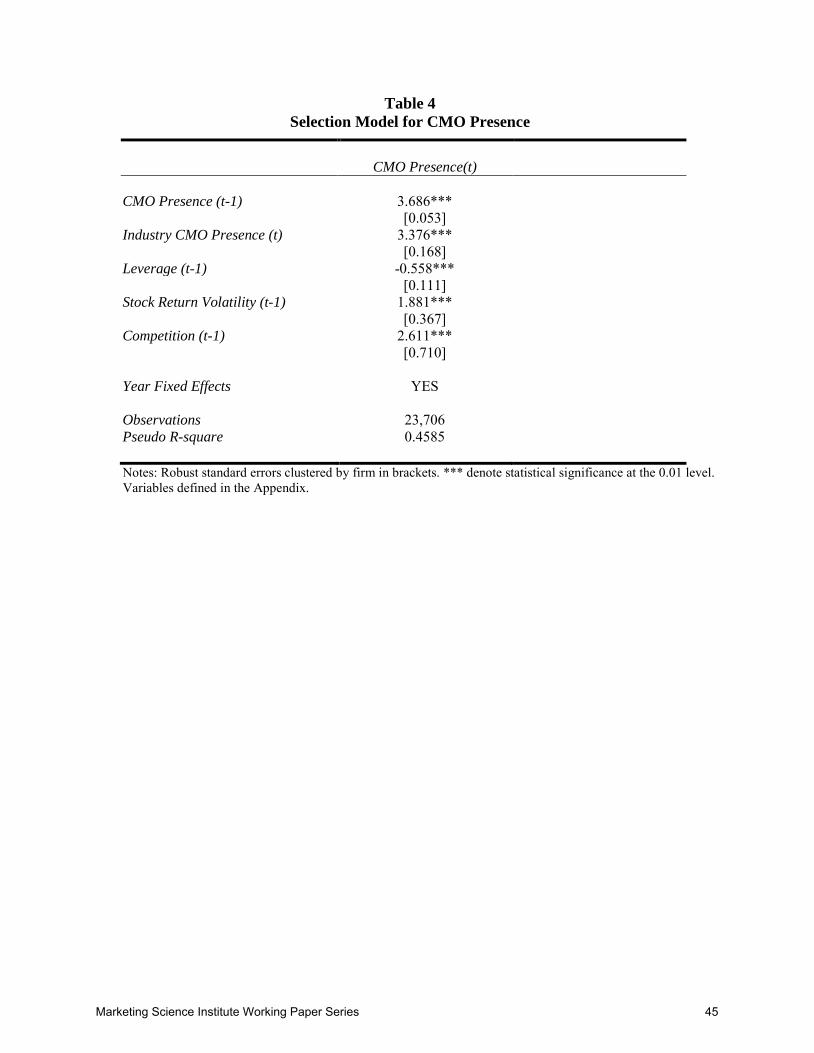

(5) CMO Presenceit = α0+ α1CMO Presenceit-1 + α2Industry CMO Presenceit + α3Leverageit-1

+ α4Stock Return Volatilityit-1 + α5Competitionit-1 + τtYeart + 𝜀𝜀𝑖𝑖𝑖𝑖.

Table 4 reports estimates of model 5. All included factors have expected signs. Consistent with

past research we find that Industry CMO Presence (the proportion of other firms in the same two-digit

SIC industry employing a CMO), Competition, and Stock Return Volatility have positive signs and

Leverage is negatively associated with CMO presence. We also find that our addition, CMO Presence

in the Prior Year, is positive and, by far, the most prominent factor accounting for most of the

explanatory power in the model. None of the other factors we consider are relevant in our sample.

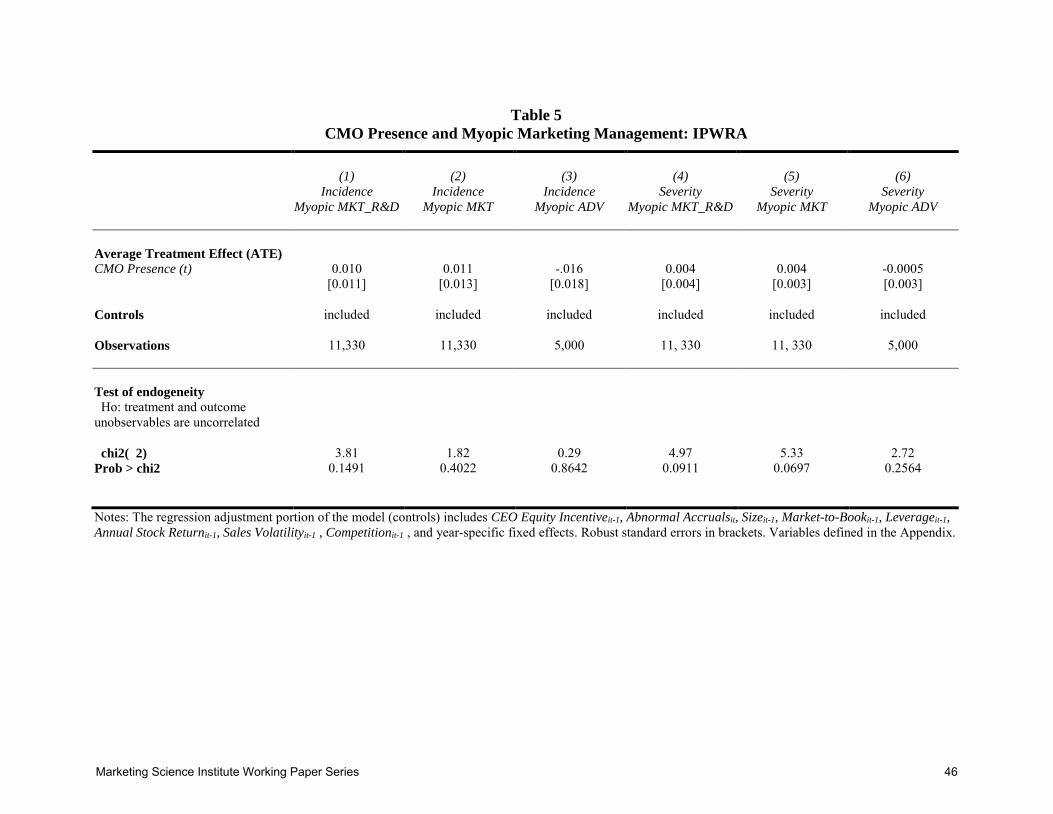

(2) IPWRA Models to Test the Effect of CMO Presence. We use propensity scores computed in step

one to weigh our observations in the regression models explaining the incidence and severity of

myopia. That is, each observation is weighted by the inverse probability that a CMO is present in the

TMT. We use logit specification for Incidence models and linear specification for Severity models.

Equation 6 summarizes our models for incidence and severity of myopia:

(6) Incidence/Severity Myopiait = β0+β1CMO Presenceit+β2CEO Equity Incentiveit-1

+β3Abnormal Accrualsit +β4Sizeit-1+β5Market-to-Bookit-1+ β6Leverageit-1

+β7Annual Stock Returnit-1 + β8Sales Volatilityit-1 + β9Competitionit-1 + τtYeart + 𝜀𝜀𝑖𝑖𝑖𝑖.

The key variable in our models is CMO Presence. Under H1, we would expect to observe a

significant negative estimate for CMO Presence in both the Incidence and Severity models. The

regression adjustment portion of the model includes a comprehensive set of controls. Prior work has

shown that certain firm- and market-specific characteristics affect earnings inflation (Armstrong et al.

2013, Chakravarty and Grewal 2011, Roychowdhury 2006), thus, we include them: firm size (Size),

growth opportunities (Market-to-Book), leverage ratio (Leverage), prior performance (Annual Stock

Return), volatility of sales (Sales Volatility), and the degree of competition (Competition). In addition,

Marketing Science Institute Working Paper Series 24

we also include Year fixed effects, CEO Equity Incentive, and Abnormal Accruals as controls.

The inclusion of these additional variables is motivated by the following considerations. Past

research has shown that equity-based managerial compensation affects accruals manipulation (Jiang

et al., 2010). We conjecture that CEO Equity Incentiveit-1 might also affect real activity manipulation,

because it is just an alternative strategy to achieve the same goal of earnings inflation, and include it

in our myopia models. We also include Abnormal Accrualsit (the amount that current accruals deviate

from their normal level) to control for the extent of accounting-based manipulation because accruals

and real manipulation (myopia) are driven by the same motivation to inflate earnings. Abnormal

Accruals are the difference between accounting accruals and expected accruals levels estimated using

the modified Jones model (Dechow et al. 1995). Year fixed effects capture general economic

conditions common across firms.

Except for Abnormal Accrualsit, all variables are lagged one year. This practice has been

established in compensation and earnings-inflation studies for two main reasons (Armstrong et al.

2013; Bergstresser and Philippon 2006): (1) to control for firm factors at the time managers actually

make strategic decisions, that is, at the beginning rather than the end of year; and (2) because

contemporaneous firm-specific factors can be affected by myopic management (e.g., myopic

management may affect firm size and the market-to-book ratio). The only contemporaneous measure

we include is Abnormal Accrualsit. We do so because current abnormal accruals represent the

contemporaneous accounting-based earnings manipulation and are presumably driven by some of the

same factors that motivate earnings inflation through real activity. Indeed, firms can achieve earnings

inflation through accounting accruals manipulation and/or myopic management. That is, Abnormal

Accrualsit proxy for common factors inducing earnings inflation.

Table 5 reports our estimation results. We find no significant effects for CMO Presence

across all six models. We undertake multiple tests to assess this non-finding.

(3) Alternative Models to Test Hypothesis 1. We follow Imbens and Wooldridge (2009), Busso et al.

Marketing Science Institute Working Paper Series 25

(2014) and Gordon et al. (2017) advice to use multiple methods to test our hypotheses. We find no

support for H1 and no evidence of CMO presence affecting either the incidence or severity of myopia

across all methods, models, and myopia proxies we use (all results available upon request). For

example, we tested H1 using Heckman approach for selection correction and various matching

estimators. We find no significant effects of CMO presence.

Heckman and matching methods are similar to IPWRA in that they require the conditional

independence assumption to hold (assume selection on observables). To assess the validity of this

assumption we test H1 using endogenous treatment effects models (control function approach,

Wooldridge 2015) and undertake direct tests of endogeneity between CMO presence and the

unobservables in our myopia models. We find no significant endogeneity (tests reported in Table 5),

suggesting IPWRA approach is preferred.7

Testing Hypotheses 2 and 3: Executive Compensation Effects

H2 predicts that executive equity compensation incentives induce myopic management. H3 predicts

that the CMO incentives have a greater association with the practice of myopic marketing

management than those of the CEO. We can assess these hypotheses by estimating models linking the

incidence and severity of myopia to the CMO and CEO equity incentives:8

(7) Incidence/ Severity Myopiait = γ0+γ1CMO Equity Incentiveit-1 +γ2CEO Equity Incentiveit-1

+β3Abnormal Accrualsit +β4Sizeit-1+β5Market-to-Bookit-1+ β6Leverageit-1

+β7Annual Stock Returnit-1 + β8Sales Volatilityit-1 + β9Competitionit-1 + τtYeart + 𝜀𝜀𝑖𝑖𝑖𝑖.

Following research on executive compensation (Armstrong et al. 2013), we measure

executives’ equity incentives one year prior to the measurement of our outcome variables (myopic

management). The lagged values for CEO and CMO Equity Incentive effectively represent the

7 In the two cases of MMRD and MMKT Severity proxies, where the endogeneity test p-values dip below .10, the estimated effects of CMO Presence from the endogenous treatment effects model are still insignificant, -.0009, p=0.749 and -.0012, p=0.651, respectively. 8 The models include all controls for myopic management discussed in the preceding section. As we later discuss in the Sensitivity Analyses section, we have also considered other controls and executives in addition to CEO and have found that our results are robust.

Marketing Science Institute Working Paper Series 26

"beginning-of-the-year" incentives to allow for these incentives to influence decisions made for that

year. Under H2, we expect the effects of equity compensation for both, the CEO and the CMO, to be

positive (i.e., to increase myopia). Furthermore, under H3 we would expect the CMO equity

incentives to have a greater impact than those of the CEOs.

Table 6 presents results of estimating model 7. We find CMO equity incentives are significantly

associated with the incidence and severity of myopia. Moreover, we find that CEO equity incentives

are unrelated to the incidence of myopia and become insignificant in the severity models (for MMRD

and for MMKT myopia proxies) when CMO equity incentives are included into the model. We

observe a consistent pattern of CMO equity incentives positively associated with the likelihood and

severity of myopia across all our proxies of myopic management. Wald tests reported in Table 6 show

that CMO equity incentives have a significantly stronger association with myopia than those of CEO

for incidence of MMRD and MMKT myopia and marginally so for incidence of advertising myopia

and all severity measures. As such, we find strong support for H2 and support for H3.

(1) Sensitivity Testing: Control Function Estimation. We undertook multiple tests to assess the

stability and validity of our findings. For example, we re-estimated model 7 with Heckman correction

(modeling the choice to issue equity to CMO in the first stage) and found our results are robust. We

also undertook tests to assess the validity of a causal interpretation for the results reported in Table 6

and tested for potential endogeneity in our models. For example, if there are some unobservable

factors affecting both, the compensation structure in the current year and the myopia in the following

year, our estimates in Table 6 could be biased. To address this concern, we undertook a control

function (CF) estimation of model 7.9

CF is closely related to instrumental variable (IV) estimation methods, but offers some

advantages. CF is a variable, such that adding it to a regression model renders an endogenous policy

9 We have also estimated model 7 using a traditional instrumental variable (IV) estimation. We used the exogenous variables CMO Equity Incentiveit-2, CEO Equity Incentiveit-2, Average CMO Equity Incentive in the Industryit-1 to create an instrument for CMO Equity Incentiveit-1. Consistent with CF results and no endogeneity, our IV estimation of model 7 generates results very similar to those reported in Table 6.

Marketing Science Institute Working Paper Series 27

variable exogenous. As a result, a model including CF “provides consistent estimation of the causal

effect of a policy variable” (Wooldridge 2015, p. 420). Wooldridge (2015) offers a thorough review

of CF methods and their use in applied econometrics. We follow Wooldridge (2015) in implementing

our CF estimation. That is, we first estimate the following reduced form regression of CMO Equity

Incentiveit-1 on a set of exogenous instruments:

(8) CMO Equity Incentiveit-1 = δ0+ δ1CMO Equity Incentiveit-2 + δ2CEO Equity Incentiveit-2

+ δ3Average CMO Equity Incentive in the Industryit-1 + τtYeart +νit-1.

The estimated residuals νit-1 become our CF and are added to model 7. In the CF approach, νit-1

is viewed as an additional explanatory variable. If CMO Equity Incentiveit-1 is endogenous (correlated

with unobservables) in model 7, we can re-write model 7 errors (𝜀𝜀𝑖𝑖𝑖𝑖) as 𝜀𝜀𝑖𝑖𝑖𝑖= ηνit-1+ eit. Then,

including νit-1 in model 7 generates a new error term eit which is uncorrelated with CMO Equity

Incentiveit-1. That is, νit-1 is proxying for the factors in CMO Equity Incentiveit-1 that are correlated

with 𝜀𝜀𝑖𝑖𝑖𝑖 and including it into the model effectively controls for the potential endogeneity in CMO

Equity Incentiveit-1. One benefit of CF over IV is that it produces a direct test of potential endogeneity

between CMO Equity Incentiveit-1 and the unobservables in model 7. Including νit-1 generates a

heteroscedasticity-robust Hausnam test of OLS versus 2SLS and CMO Equity Incentiveit-1 actually

being exogenous (H0: η=0). These heteroscedasticity-robust Hausman specification tests of OLS

versus 2SLS are reported in the last row of Table 6. In our data, we cannot reject the null that CMO

Equity Incentiveit-1 is exogenous and as such, the OLS estimates (reported in Table 6) are preferred.

(2) Alternative Models to Test Hypotheses 2 and 3: Difference-in-Differences. To offer further

evidence and support for a causal interpretation of our findings, we undertake a differences-in-

differences (DID) analyses. We exploit a quasi-natural experiment created by the enactment of

regulation FAS 123R which changed the accounting treatment of stock options: it eliminated firms’

ability to expense options at their intrinsic value and required expensing options-based compensation

at a higher “fair” value. FAS 123R created an exogenous shock to the costs of options-based

Marketing Science Institute Working Paper Series 28

compensation while leaving the underlying economic benefits unaffected (Hayes et al. 2012). The

implementation of FAS 123R in 2005 effectively increased the costs and decreased the usage of

option-based compensation. The decline in the use of stock options owing to FAS 123R for

management compensation has been well documented in the accounting and finance literature (e.g.,

Brown and Lee 2011; Hayes et al. 2012). We follow prior literature leveraging FAS 123R in DID

analysis to structure our tests (e.g., Bakke et al. 2016).

We select a balanced window of 2003 to 2007 around the 2005 enactment of FAS 123R.

Restricting our analysis to the 2003-2007 isolates the effect of FAS 123R from two other major

exogenous shocks—the implementation of the Sarbanes-Oxley Act in 2002 and the beginning of the

financial and economic crisis in 2008. We select all firms offering stock options to their CEOs prior

to 2005 and divide them into two groups based on whether the CMO received (treatment group) or

did not receive (control group) stock options prior to 2005. Our sample consists of 910 firm-year

observations, including 807 treatment and 103 control observations. Firms granting options to their

CMOs prior to 2005 reduce or eliminate option grants after the implementation of FAS 123R and

therefore reduce incentives for myopic marketing management. FAS 123R has no effect on CMO

incentives in the “no-options-for-CMO” (control) group. As such, we expect the FAS 123R to reduce

myopic practices in the treatment relative to the control group in the post-2005 period. We estimate

the following DID regression design (Angrist and Pischke 2008):

(9) Incidence/ Severity Myopiait = ϕ1CMO with Optionsit+ ϕ2Post_FAS123Rit

+ ϕ3CMO with Options*Post_FAS123Rit + κkControlskit + 𝜀𝜀𝑖𝑖𝑖𝑖,

where CMO with Optionsit takes the value of one for the treatment firms and zero for the control

group of firms, Post_FAS123Rit is equal to one for firm-years after FAS 123R implementation in

2005 and is zero otherwise, and the set of k control variables (Controlskit) includes all variables from

equation 7. The key coefficient of interest is on the interaction term (ϕ3). It represents the difference-

in-differences estimate and shows the effect of implementing regulation FAS 123R on myopic

Marketing Science Institute Working Paper Series 29

management (Post_FAS123R) for firms granting stock options compared to firms not granting options

to CMOs prior to 2005. We expect ϕ3 to be negative and significantly different from zero.

Table 7 Panel A reports our findings. In line with our expectations, ϕ3 is negative in all and is

significant in five of our six models. That is, we document a decrease in myopic marketing

management after 2005 for firms compensating their CMOs with options. Table 7 also shows

significant positive main effect of treatment (ϕ1), which is consistent with our finding in Table 6:

firms granting options to their CMOs show greater extent of myopic management.

One core assumption underlying the DID estimation is that in the absence of the treatment,

both treated and control firms would experience similar trends in the outcome variable. In other

words, if FAS 123R did not occur, our estimate of ϕ3 would equal zero. This assumption cannot be

directly tested. But we can perform a placebo test suggested by Roberts and Whited (2013): we

falsely assume that a treatment occurs at a different point in time. We maintain the same treatment

and control groups, but use years 2004 and 2007 as alternative focal points. In both placebo tests the

estimated treatment effect is statistically insignificant for all six measures of myopia. This result

supports the argument that decline in myopic marketing management in treatment firms stems from

changes due to FAS 123R in 2005 and is not due to general time trends. In sum, our DID analysis

supports our key results and causal interpretation of the link between CMO equity incentives and

myopic marketing management.

We have undertaken a similar analysis to assess the role of CEO option grants on myopic

marketing management. Unlike CMOs, almost all of the CEOs in our sample are compensated with

stock options. As such, we structure our test as follows: we identified a set of firms in the 2004-2007

period that did not grant options to CMOs or did not have a CMO in the TMT and divided it into two

groups based on whether the CEO equity incentives were above (treatment group) or below (control

group) the median equity incentives in their respective industry (defined by 2-digit SIC code) in the

pre-FAS123R period. Our sample consists of 423 firm-year observations, including 152 treatment and

Marketing Science Institute Working Paper Series 30

271 control observations. If CEO equity incentives drive marketing myopia, we would expect to see a

significant decline in in myopic practices after 2005 for our treatment firms (i.e., ϕ3 < 0 in the

equation 10 below):

(10) Incidence/ Severity Myopiait = ϕ1CEO with High Equity Incentivesit + ϕ2Post_FAS123Rit

+ ϕ3CEO with High Equity Incentivesit *Post_FAS123Rit + κkControlskit + 𝜀𝜀𝑖𝑖𝑖𝑖,

where CEO with High Equity Incentivesit takes the value of one for the treatment firms and zero for

the control group of firms, Post_FAS123Rit equals one for firm-years after FAS 123R implementation

in 2005 and is zero otherwise, and the set of k control variables (Controlskit) includes all variables

from equation 7. Again, the key coefficient of interest is on the interaction term (ϕ3).

Table 7 Panel B reports our findings. We find no significant effects in CEO DID model.

Interestingly, we also do not find significant main effect of high CEO equity incentives on our

myopic marketing measures. As a sensitivity analysis, we have replicated our DID tests with the top

and bottom 25% of the CEO equity incentive groups and found that our results are stable with

alternative definitions of treatment and control groups.

In sum, we find full support for H2 and evidence to support a causal interpretation: CMO

equity incentives drive myopic marketing managements. Further, we find support for the argument

that CMO equity incentives have a stronger association with myopia than those of CEOs. We find no

support for the arguments of the positive and anti-myopia role of equity compensation advanced in

marketing literature: equity incentives of CMOs do not reduce myopic marketing management but

rather increase its incidence and severity.

Testing Hypothesis 4: CMO personal equity trading

H4 suggests that executives will seek to exploit the opportunity and will sell more of their equity

holdings and/ or exercise more options at the time when firm valuation is artificially inflated through

myopic marketing management. A univariate analysis of our data reveals that a significantly greater

portion of exercisable options is exercised in years when myopic management takes place. Across our

Marketing Science Institute Working Paper Series 31

three incidence proxies, CMOs sell on average 23.6 percent of their exercisable options in myopic

years, versus 17.9 percent in non-myopic years. The differences for all three proxies are highly

significant (p<0.001).

We can formally test H4 by contrasting executive equity trading in myopic versus non-

myopic periods and based on the severity of myopic marketing management by estimating the

following model:

(11) CMO Equity Tradingit= 𝜒𝜒0+ 𝜒𝜒1Incidence/Severity Myopiait + 𝜒𝜒2CEO Equity Tradingit

+ 𝜒𝜒8Abnormal Accrualsit + 𝜒𝜒3Sizeit-1+ 𝜒𝜒4Market-to-Bookit-1 + 𝜒𝜒5Stock Returnit-1

+ 𝜒𝜒6Stock Return Volatilityit-1 + 𝜒𝜒7R&D Intensityit-1 + 𝜒𝜒9CMO Equity Holdingsit-1 + τtYeart + 𝜀𝜀𝑖𝑖𝑖𝑖,

where CMO Equity Tradingit is one of our equity-trading measures (options-based, Share of Options

Exercised, or share-holdings-based, Net Trading) for CMO of firm i in year t. Our estimate of interest

is 𝜒𝜒1. It captures the association between our myopia proxies and CMO trading. Under H4 we expect

CMOs to exercise a larger share of their stock options (𝜒𝜒1 >0, i.e., greater portion of exercisable

options exercised) and to sell more of their equity holding (𝜒𝜒1 <0, i.e., overall declining personal

share holdings, shares sales exceeding purchases) in years when myopia occurs and is more severe.

Our CMO trading model includes factors explaining insider trading identified in prior

research: Sizeit-1, because managers in larger firms tend to sell rather than purchase equity compared

to managers in small firms (Seyhun 1986); Market-to-Bookit-1 and Annual Stock Returnit-1, because

insiders are contrarian investors and buy (sell) stock with high (low) valuation (Jenter 2005) and with

poor (good) past performance (Lakonishok and Lee 2001); Stock Return Volatilityit-1, as greater

volatility is associated with fewer early exercises because it increases the cost of exercising options

early (Burns and Kedia 2008); R&D Intensityit-1, because R&D activities increase information