i c euromax resources - denver gold group · initiation: timing is everything - august 13, 2015 2...

TRANSCRIPT

Find CIBC research on Bloomberg, Reuters, firstcall.com

and ResearchCentral.cibcwm.com CIBC World Markets Inc., P.O. Box 500, 161 Bay Street, Brookfield Place, Toronto, Canada M5J 2S8 (416) 594-7000

INSTITUTIONAL EQUITY RESEARCH Leon Esterhuizen 44 (207) 234-6139 [email protected]

Arnold Van Graan 27 (11) 575-4935 [email protected]

Ben McEwen 44 (207) 234-6180 [email protected]

I N I T I A T I N G C O V E R A G E j

Euromax Resources

Initiation: Timing Is Everything

All figures in US dollars, unless otherwise stated.(C$1.3:US$1) 15-136716 © 2015

CIBC World Markets does and seeks to do business with companies covered in its research reports. As a result, investors

should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.

Investors should consider this report as only a single factor in making their investment decision. See "Important Disclosures" section at the end of this report for important required disclosures, including potential

conflicts of interest. See "Price Target Calculation" and "Key Risks to Price Target" sections at the end of this report,

where applicable.

August 13, 2015

Precious Metals

Stock Rating: S E C T O R O U T P E R F O R M E R –

S P E C U L A T I V E

Sector Weighting: M A R K E T W E I G H T

Key Ratios and Statistics

12-18 mo. Price Target C$0.70

EOX-V (8/12/15) C$0.36

Key Indices: None

3-5-Yr. EPS Gr. Rate (E) NM 52-week Range C$0.17-C$0.57

Shares Outstanding 116.8M

Float 116.8M Shrs

Avg. Daily Trading Vol. NM

Market Capitalization C$42.0M

Dividend/Div Yield Nil / Nil

Fiscal Year Ends December

Net Asset Value $0.58 per Shr

2015 ROE (E) NM

LT Debt $15.0M

Net Asset Value Common Equity NM

EPS 2013 2014 2015 2016

Current ($0.10A) ($0.13A) ($0.09E) ($0.07E)

Estimates (Dec. 31) 2013 2014 2015 2016 CF per Share-Curr ($0.06A) ($0.10A) ($0.09E) ($0.05E) Valuation (Dec. 31) P/E-Curr NM NM NM NM P/CF-Curr NM NM NM NM

Company Description Euromax holds the copper-gold Ilovica project located in Macedonia.

www.euromaxresources.com/

What's Changed

The mining scene is awash with stories of investment at the top of the cycle, delivering deeply negative returns and, in many instances, dead losses as assets are shut in the now much lower pricing

environment. The only way to make real returns in the commodity space is to be counter-cyclical. Buy and develop in low metals price environments so that the higher prices will eventually see significant returns delivered to the long-term investors who positioned early.

So here is Euromax with its Ilovica copper/gold project. With an IRR in the order of 8% at current spot metals prices, a market cap of $40 million and some $500 million in capital needed to build the

mine... Run for the hills?

Implications

NO - this is, in our view, exactly the kind of development that must

be supported: Low cost ($800/oz. gold equivalent AISC), long life (over 20 years), well-funded (some $400 million in funding already secured through streaming and project finance debt that is guaranteed by the German government) and easy mining and

processing (0.7:1 strip right next to all infrastructure).

This project at the top of the cycle (gold at $1,900/oz. and copper at

$4.40/lb.) would have delivered an IRR in excess of 35% and would obviously have been built. Here now, these numbers indicate "potential," while the actual IRR of 8% proves it still viable - perfect

for positioning and building for real solid returns when the market eventually turns up from here again. Furthermore, the stated strategy to pay out all free cash flows from this mine as dividends certainly adds more sparkle to the already good optionality.

Valuation

Euromax has a solid project in Ilovica, has secured most of the funding and is building when most are closing down - the perfect

mix, in our view, for proper long-term returns. One could decide to wait for an opportunity closer to the realisation of production, but that may also mean foregoing the possible premium that could be

unlocked in a takeout scenario. As of August 13, we initiate with a Sector Outperformer (Speculative) rating and a price target of C$0.70/share (including a $100 million equity raise in 2016 at

C$0.40/share).

Initiation: Timing Is Everything - August 13, 2015

2

Source: Company reports and CIBC World Markets Inc.

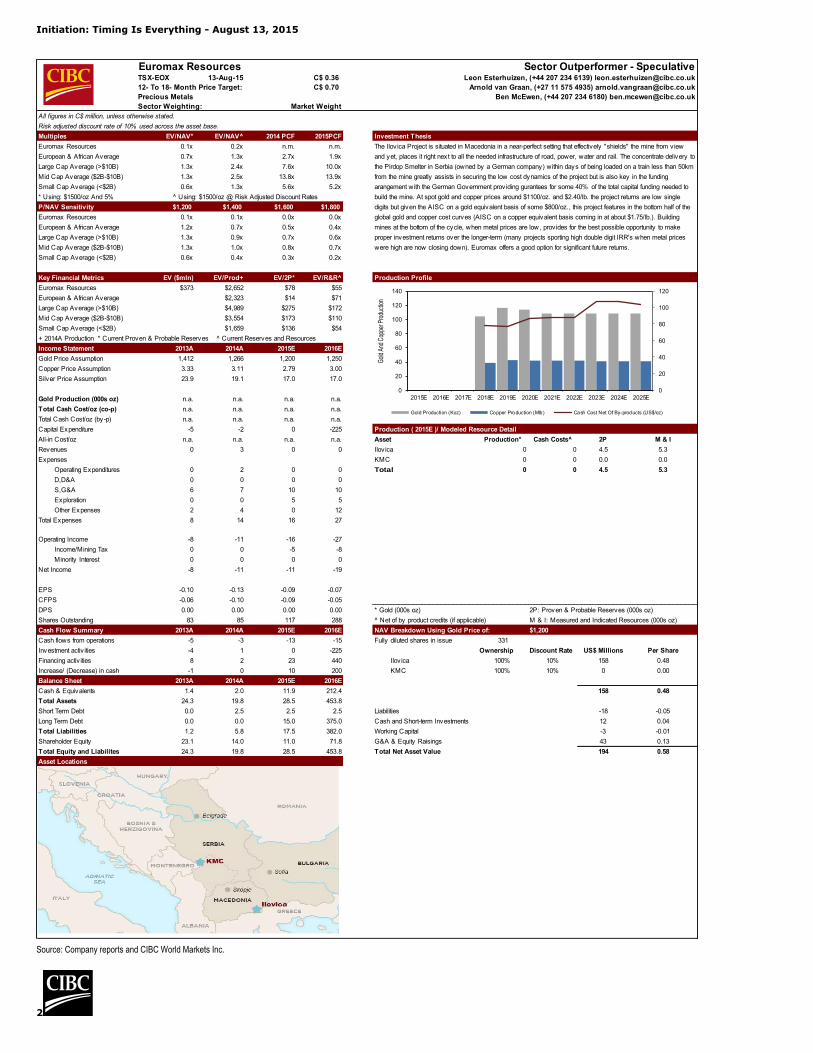

Euromax Resources Sector Outperformer - SpeculativeTSX-EOX 13-Aug-15 C$ 0.36 ###### Leon Esterhuizen, (+44 207 234 6139) [email protected]

12- To 18- Month Price Target: C$ 0.70 Arnold van Graan, (+27 11 575 4935) [email protected]

Precious Metals Ben McEwen, (+44 207 234 6180) [email protected]

Sector Weighting: Market Weight

All figures in C$ million, unless otherwise stated.

Risk adjusted discount rate of 10% used across the asset base.

Multiples EV/NAV* EV/NAV^ 2014 PCF 2015PCF

Euromax Resources 0.1x 0.2x n.m. n.m.

European & African Average 0.7x 1.3x 2.7x 1.9x

Large Cap Average (>$10B) 1.3x 2.4x 7.6x 10.0x

Mid Cap Average ($2B-$10B) 1.3x 2.5x 13.8x 13.9x

Small Cap Average (<$2B) 0.6x 1.3x 5.6x 5.2x

* Using: $1500/oz And 5% ^ Using: $1500/oz @ Risk Adjusted Discount Rates

P/NAV Sensitivity $1,200 $1,400 $1,600 $1,800

Euromax Resources 0.1x 0.1x 0.0x 0.0x

European & African Average 1.2x 0.7x 0.5x 0.4x

Large Cap Average (>$10B) 1.3x 0.9x 0.7x 0.6x

Mid Cap Average ($2B-$10B) 1.3x 1.0x 0.8x 0.7x

Small Cap Average (<$2B) 0.6x 0.4x 0.3x 0.2x

Key Financial Metrics EV ($mln) EV/Prod+ EV/2P* EV/R&R^ Production Profile

Euromax Resources $373 $2,652 $78 $55

European & African Average $2,323 $14 $71

Large Cap Average (>$10B) $4,989 $275 $172

Mid Cap Average ($2B-$10B) $3,554 $173 $110

Small Cap Average (<$2B) $1,659 $136 $54

+ 2014A Production * Current Proven & Probable Reserves ^ Current Reserves and Resources

Income Statement 2013A 2014A 2015E 2016E

Gold Price Assumption 1,412 1,266 1,200 1,250

Copper Price Assumption 3.33 3.11 2.79 3.00

Silver Price Assumption 23.9 19.1 17.0 17.0

Gold Production (000s oz) n.a. n.a. n.a. n.a.

Total Cash Cost/oz (co-p) n.a. n.a. n.a. n.a.

Total Cash Cost/oz (by-p) n.a. n.a. n.a. n.a.

Capital Expenditure -5 -2 0 -225 Production ( 2015E )/ Modeled Resource Detail

All-in Cost/oz n.a. n.a. n.a. n.a. Asset Production* Cash Costs^ 2P M & I

Revenues 0 3 0 0 Ilov ica 0 0 4.5 5.3

Expenses KMC 0 0 0.0 0.0

Operating Expenditures 0 2 0 0 Total 0 0 4.5 5.3

D,D&A 0 0 0 0

S,G&A 6 7 10 10

Exploration 0 0 5 5

Other Expenses 2 4 0 12

Total Expenses 8 14 16 27

Operating Income -8 -11 -16 -27

Income/Mining Tax 0 0 -5 -8

Minority Interest 0 0 0 0

Net Income -8 -11 -11 -19

EPS -0.10 -0.13 -0.09 -0.07

CFPS -0.06 -0.10 -0.09 -0.05

DPS 0.00 0.00 0.00 0.00 * Gold (000s oz) 2P: Proven & Probable Reserves (000s oz)

Shares Outstanding 83 85 117 288 ^ Net of by product credits (if applicable) M & I: Measured and Indicated Resources (000s oz)

Cash Flow Summary 2013A 2014A 2015E 2016E NAV Breakdown Using Gold Price of: $1,200

Cash flows from operations -5 -3 -13 -15 Fully diluted shares in issue 331

Investment activ ities -4 1 0 -225 Ownership Discount Rate US$ Millions Per Share

Financing activ ities 8 2 23 440 Ilov ica 100% 10% 158 0.48

Increase/ (Decrease) in cash -1 0 10 200 KMC 100% 10% 0 0.00

Balance Sheet 2013A 2014A 2015E 2016E

Cash & Equivalents 1.4 2.0 11.9 212.4 158 0.48

Total Assets 24.3 19.8 28.5 453.8

Short Term Debt 0.0 2.5 2.5 2.5 Liabilities -18 -0.05

Long Term Debt 0.0 0.0 15.0 375.0 Cash and Short-term Investments 12 0.04

Total Liabilities 1.2 5.8 17.5 382.0 Working Capital -3 -0.01

Shareholder Equity 23.1 14.0 11.0 71.8 G&A & Equity Raisings 43 0.13

Total Equity and Liabilites 24.3 19.8 28.5 453.8 Total Net Asset Value 194 0.58

Asset Locations

The Ilov ica Project is situated in Macedonia in a near-perfect setting that effectively "shields" the mine from v iew

and yet, places it right next to all the needed infrastructure of road, power, water and rail. The concentrate delivery to

the Pirdop Smelter in Serbia (owned by a German company) within days of being loaded on a train less than 50km

from the mine greatly assists in securing the low cost dynamics of the project but is also key in the funding

arangement with the German Government prov iding gurantees for some 40% of the total capital funding needed to

build the mine. At spot gold and copper prices around $1100/oz. and $2.40/lb. the project returns are low single

digits but given the AISC on a gold equivalent basis of some $800/oz., this project features in the bottom half of the

global gold and copper cost curves (AISC on a copper equivalent basis coming in at about $1.75/lb.). Building

mines at the bottom of the cycle, when metal prices are low, prov ides for the best possible opportunity to make

proper investment returns over the longer-term (many projects sporting high double digit IRR's when metal prices

were high are now closing down). Euromax offers a good option for significant future returns.

Investment Thesis

0

20

40

60

80

100

120

0

20

40

60

80

100

120

140

2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

Gol

d An

d C

oppe

r Pro

duct

ion

Gold Production (Koz) Copper Production (Mlb) Cash Cost Net Of By-products (US$/oz)

Initiation: Timing Is Everything - August 13, 2015

3

Investment Rationale And Recommendation

Solid IRR, Cash Flows – Proper Opportunity? Euromax’s (EOX–SO-Spec.) 100%-owned Ilovica Project is located in the

southeast of Macedonia (The Former Yugoslav Republic Of Macedonia) and is

forecast to produce 90 Koz. of gold and 16 Kt of copper per annum over an

initial life of mine of some 23 years. The project was initiated a couple of years

ago and, according to the project’s preliminary feasibility study (PFS) (using

$3.00/lb. copper and $1,250/oz. gold prices), it delivers a 19% internal rate of

return (IRR) pre-tax, and 16% IRR post-tax. This equates to a six-year pre-tax

payback or seven years post-tax payback on the $502 million initial capital

requirement.

Of course, the metals prices have fallen subsequently, leaving the pre-tax IRR at

approximately 8% (using $2.40/lb. copper and $1,080/oz. gold). Clearly then,

this is no “dripping roast” at current metals prices, but here’s the rub – if the

view is for a much better copper price in the near term (most market forecasts

point to the development of big copper deficits within the next year or two),

should this opportunity – to build a relatively low-cost mine that still shows

positive returns (albeit very low returns at current spot prices) – still be pursued

at this stage? In particular, given a three-year build (from here, with the actual

mine build some 18 months) that may put the mine into production at much

better copper (and gold?) pricing levels, is this not the ideal time to build?

The answer will, in our opinion, depend very much on an investor’s view on the

potential for higher copper and gold prices in the future, and on the funding

structure. The less the company is dependent on equity and the more it can

secure debt for funding, the better the chances of success. As we will show later,

Euromax already sports a significant amount of the capital needed, with only

some 20% of the remaining funding likely to come from equity.

Based on our calculations and forecasts, the project will produce 165 Koz. of

gold equivalent output per annum at AISC (all-in sustaining costs) of $800/oz.

on a gold-equivalent basis or just under $1.75/lb. on a copper-equivalent basis.

As such, and including an equity raising of $100 million in 2016 at an assumed

share price of C$0.40/share, we believe that the net asset value (NAV) (at 10%)

of C$194 million or C$0.70/share represents a well-discounted (or risked) value,

indicating a real possibility of a successful investment opportunity.

$500 Million Capex…? No Worries, Nearly Fully Funded The PFS capital expenditure forecast for Ilovica is some $502 million, clearly a

material number (including about $50 million for contingencies) given Euromax’s

current market capitalisation of some $40 million – the very typical problem of

any start-up company in the mining industry. So, does this imply material per

share dilution as the company is pushed towards raising equity finance to fund

this capital bill? Or, more bluntly, should we wait for others to fund the capital

and only look to come in later after this risk has been handled?

Well, a “massive” dilution event is unlikely, in our opinion, given the company’s

continued progress on alternative funding. In October 2014, the company

announced that it had agreed terms with Royal Gold (RGLD–SO) for a gold

stream worth $175 million, equivalent to 32% of the total PFS capex bill (at the

cost of 14% of its gold-equivalent output). Furthermore, in May 2015, Euromax

announced that it had entered into a debt financing agreement with a number of

Initiation: Timing Is Everything - August 13, 2015

4

European banks for $215 million (and backed by German government UFK

Eligibility – whereby the German government will guarantee funds in line with

the value of the metal that will be supplied to the German Smelter/Refiner for

processing). Concurrent with that announcement, the company also noted that it

had entered into an equipment financing facility for up to $25 million, bringing

the potential funding receipt to some $400 million, equivalent to 80% of the

total capex bill to build this mine.

This in itself is an astonishing achievement and speaks volumes about the

experience and acumen of the Euromax management team. Even more so given

that project numbers generally improve into the Feasibility Study (from the

wider margin of error associated with the pre-feasibility study). At the same

time we have seen clear declines in cost curves across the gold and copper

industries, the oil price is lower and there are likely to be some adjustments to

render the capital profile more efficient. The level of financing already secured

then, even on this pre-feasibility level, stands out as a very clear and noticeable

flag as to the quality of this project.

So, with regards to the remaining $100 million capital shortfall, management

will be seeking equity participation for the debt arrangements mentioned above,

at set debt/equity ratios. In other words, there will be an equity component to

this funding and its size is essentially “fixed” by the requirements of the debt

providers (and the total forecast capital expenditure budget, of course) –

pointing to all of the outstanding capital likely coming from equity. In our

modeling, we have included a $100 million equity issue at a share price of

C$0.40/share (currently trading at about C$0.36/share and likely higher

following the expected release of what will probably be a better feasibility

study). In other words, the equity issue price could well be much better than our

assumed C$0.40/share.

Stacking it up then: At a cost of some $800/oz. on a gold-equivalent basis (or

some $550/oz. on a by-product basis whereby all copper income is deducted as

a credit against the gold cost), the project sports very competitive AISC in both

the gold and copper sectors ($1.75/lb. AISC on a copper-equivalent basis); it

seems to already be very well funded off just the PFS numbers; and, it does not

present anything difficult in terms of mining and/or processing as all major

infrastructure needs are in the immediate vicinity. Outside of this, the financial

analysis points to value – maybe not a lot at current metals prices, but we

certainly believe that if the IRR is positive at this time, at what most consider to

be the bottom of the copper cycle, then the project will more than likely deliver

very good returns over many years in the future.

By our calculation, the average AISC for the global gold industry at the end of

H2/2015 is just under $1,100/oz. with the tail of that cost curve becoming VERY

flat between $900/oz. and $1,000/oz. – less than 25% of global gold production

will be making profits at a gold price below $900/oz. on our forecasts (most of

the “quality” senior producers are all guiding for AISC levels in the order of

$850/oz. to $900/oz. with most of the other major players squarely pegged

around the $1,000/oz. level).

This competitiveness of the Ilovica ore body is also reflected in our cash flow

analysis. Exhibit 1 shows the numbers at the current spot metals prices of

$1,080/oz. for gold and $2.40/lb. for copper. Given the sharp decline across the

metals spectrum over the past month, the CIBC forecast scenario (long-term

gold at $1,200/oz. and copper at $2.75/lb.) now seems a bit rich, but with

Euromax showing the capacity to generate free cash at today’s very low spot

prices (gold at $1,080/oz. and copper at $2.40/lb.), any higher price scenario

naturally would make the numbers significantly better.

Initiation: Timing Is Everything - August 13, 2015

5

Exhibit 1. Spot ($2.40/lb. Copper And $1,080/oz. Gold) Cash Flow Excluding An Equity Issue (LEFT) And Including A $100 Million Equity Issue (RIGHT)

Source: Company reports and CIBC World Markets Inc.

Exhibit 2 demonstrates the $100 million equity issue being sufficient to see the

project through to full production and making a little bit of money, leading to a

drop in the debt burden. The current proposed debt deal requires no payback in

the first three years (interest only), but then amortizes over the remaining

nine years (a 12-year debt deal secured by a 10-year smelter offtake agreement

and the German government providing a guarantee for these funds over

12 years). We believe it highly likely that the debt would be re-financed once

strong cash flows are generated.

In terms of metals price sensitivity, once the $100 million equity portion is

funded, the company would be running very close to break-even, with just a

further 10% drop in prices pushing the company back into small losses.

However, a 20% increase in metals prices would see Euromax repaying the full

$100 million of equity finance within two years and at a 10% improvement in

the metals prices in just three years of the 23-year life of mine (Exhibit 2).

Exhibit 2. Spot ($2.40/lb. Copper And $1,080/oz. Gold) Cumulative Cash Balance With No Equity Issue (LEFT)

And With A $100 Million Equity Issue (RIGHT)

Source: Company reports and CIBC World Markets Inc.

-400

-300

-200

-100

0

100

200

300

2014A 2015E 2016E 2017E 2018E 2019E 2020E

Cum

ulat

ive

Cas

h B

alan

ce U

S$

Mill

ion)

-30% -20% -10% Spot +10% +20% +30%

Initiation: Timing Is Everything - August 13, 2015

6

This gearing to metals prices is very good and given the roughly 50/50 revenue

contribution split between gold and copper at current metals prices, Euromax

would be equally geared to rallies in gold and in copper. At a discount rate of

between 5% and 10% (given the 80% secured funding and the relatively low

position on the global cost curve, the lower discount should be more applicable),

we estimate the value at between about $0.05/share and $0.60/share

(C$0.07/share to C$0.80/share). Our operating NAV estimate at the current spot

metals prices comes in at about C$0.63/share, dropping to C$0.10/share at the

more aggressive 10% discount rate and after accounting for overheads, in line

with our project IRR estimate of about 8% at the operating level.

From Exhibit 3, given a current share price of C$0.36/share, and assuming a

10% discount rate, metals prices would need to increase by some 15% to justify

the current value. At a discount rate of 5%, of course, a 15% jump in metals

prices could increase the value to more than three times the current share price

(bear in mind that our values already include dilution assumed in an equity issue

of $100 million).

Exhibit 3. NAV Sensitivity At 5% (LEFT) And 10% (RIGHT) – Almost Equally Driven By Copper And By Gold BUT Challenging At Current Prices…

Source: Company reports and CIBC World Markets Inc.

Of course, many would look at the low to no NAV and the IRR of only 8% and

simply decide to walk away from this project at current metals prices. We would

add though that had this project come to market three or four years ago with an

IRR pushing above 30% the decision may well have been to invest, only to then

lose one’s shirt as the metals prices tumbled. Basically then, buying at the

bottom of the cycle implies some level of willingness to weigh a low NAV against

a much better option value. In our view, if a project such as Ilovica can show

positive free cash flows at these prices, it not only deserves a low discount rate

but certainly should be attracting attention as a good opportunity to secure

longer-term returns that are likely to be much higher over the current 23-year

life of mine.

The peak funding requirement seems set at about $100 million but could

increase if metals prices were to decline even further, driving the initial cash

flows lower. Exhibit 4 illustrates this position and makes it clear that current

spot pricing levels are really starting to push the fundamentals of this ore body.

It must be added that our numbers remain conservative while the feasibility

study that is due out at the end of October 2015 is highly likely to reflect better

capital and cost numbers.

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

-30% -20% -10% Spot +10% +20% +30%

NA

V/ S

hare

(US

$)

Gold Copper

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

-30% -20% -10% Spot +10% +20% +30%

NA

V/ S

hare

(US

$)

Gold Copper

Initiation: Timing Is Everything - August 13, 2015

7

Exhibit 4. Peak Funding – About $100 Million, Almost Regardless Of

Metals Prices, But Could Be 50% More If There Are Even Lower Metals Prices Over The Next Two To Three Years

Source: Company reports and CIBC World Markets Inc.

From a potential investment perspective, the standard question relates to buying

before the equity issue or waiting until the company is fully funded before

buying the stock. There is no doubt that the risk to investing after the equity

issue is significantly lower than what it is beforehand. However, bear in mind

here that some 80% of project funding is essentially already in place – the

equity investors will be bringing in only 20% of the required funding, to then

share in 100% of the upside. In a sense then, any investor buying in before the

equity issue is already buying into a reduced risk scenario.

Of course, once fully funded, the risk reduces markedly and the stock should

trade higher (dependent on metals prices and a smooth mine build, of course).

Waiting to invest after the equity issue will, thus, likely imply paying a lot more

for the share (as always, risk = reward). Naturally, buying before the equity

issue also covers the probability of another mining company considering the

very low value of Euromax versus the high quality of its project and deciding the

company may offer a good growth opportunity. In a sense then, the main risk

for investment before the equity issue boils down to the equity issue price.

In Exhibit 5, we illustrate the sensitivity to the NAV at 10% and at the CIBC

metals price forecast scenario ($1,200/oz. gold and $2.75/lb. copper). We model

an assumption of an issue price of C$0.40/share – implying an NAV of

C$0.70/share. Even if we dropped that issue price to just C$0.30/share, the NAV

would still be about C$0.60/share, compared to the current trading level of

C$0.36/share. We have to make the point that we’d be unsurprised (given very

little liquidity at present and given better Feasibility Study numbers expected in

October) if the equity issue next year transpired at a share price well above the

current C$0.36/share.

Initiation: Timing Is Everything - August 13, 2015

8

Exhibit 5. NAV/Share Sensitivity To Varying Equity Issue Prices

Source: Company reports and CIBC World Markets Inc.

Finally, it’s worth noting here the quite adamant position by the CEO and the

board that this asset will be built to then distribute ALL free cash flow to the

shareholders (with some cash buffer left in the company, of course). If there

comes a time for future growth or expansion capital, the same shareholder base

may be pushed for a rights issue but only if the capital requirement makes sense

in terms of adding value to the very investors who will be funding it and tapping

all the cash flow from it again.

We very much like this model of delivery as it not only significantly enhances the

optionality of the shares but adds a lot more credibility to delivering and

embarking on ONLY projects that are well scrutinized and approved (and then

funded) by the shareholders. Being underpinned by the first project that can

already sport a plus-20-year life is a very good position from which to build such

a longer-term real dividend vehicle – everything the market wants: low cost and

high optionality coupled to yield and growth. Perhaps the only remaining worry

would be fast-accumulating takeout bids! A problem worth having…

So, in our view, this investment scenario – getting in at the bottom of the cycle

with an “easy project” that is already very well-funded and showing a positive

IRR is really the ONLY way to secure proper longer-term investment returns

(much, much better than buying high IRRs at the top of the cycle!). The strategy

and goal to pay out all free cash flow simply underline that optionality. The

risk/reward balance in this situation is clearly very much tilted in favor of

reward. While there is no guarantee of success or even of high returns or

dividend yields, the way in which the project is set up, funded and run

maximizes that possible gain, which is all that any investor already bullish on

gold and/or copper can wish for. If the investor is a bear on either gold or

copper or both, this vehicle, in our opinion, would not be the preferred play at

this stage.

Let’s take a closer look at some of the other attributes that render this project

appealing enough to write this note and to recommend investment in Euromax.

0.40

0.50

0.60

0.70

0.80

0.90

1.00

0.30 0.35 0.40 0.45 0.50 0.55 0.60

NA

V/ S

hare

Equity Issue Price (C$/share)

NAV/share (USD) NAV/share (CAD)

Initiation: Timing Is Everything - August 13, 2015

9

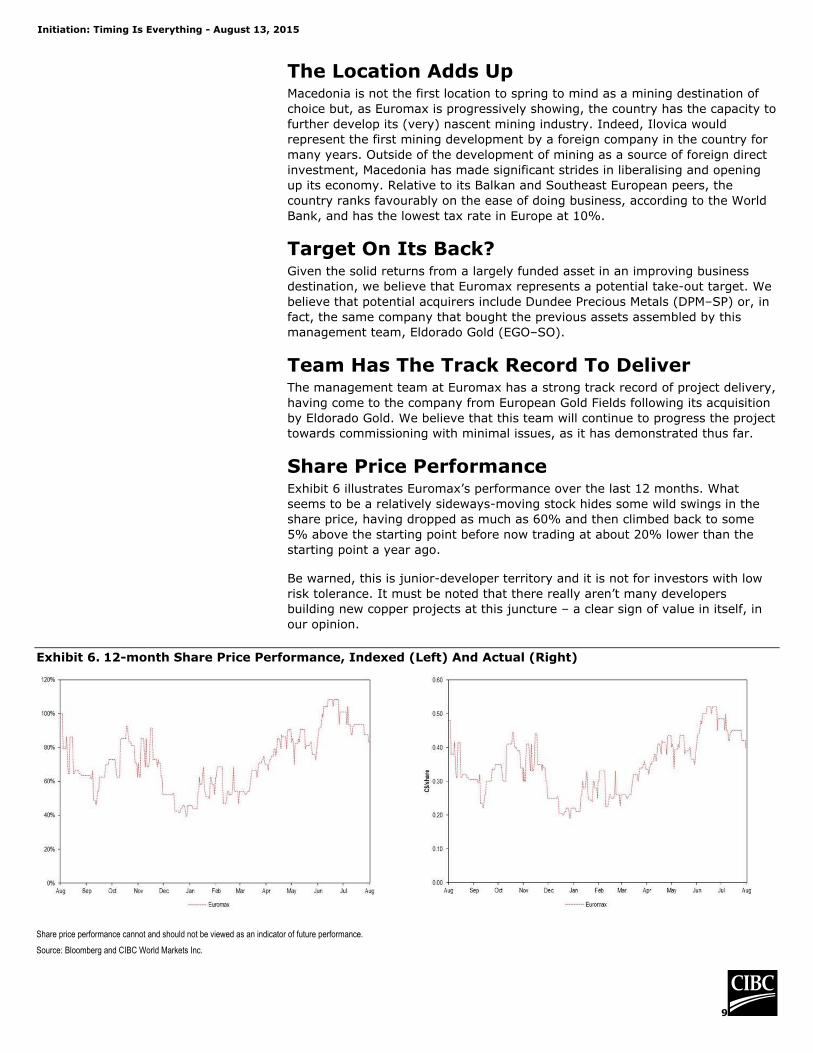

The Location Adds Up Macedonia is not the first location to spring to mind as a mining destination of

choice but, as Euromax is progressively showing, the country has the capacity to

further develop its (very) nascent mining industry. Indeed, Ilovica would

represent the first mining development by a foreign company in the country for

many years. Outside of the development of mining as a source of foreign direct

investment, Macedonia has made significant strides in liberalising and opening

up its economy. Relative to its Balkan and Southeast European peers, the

country ranks favourably on the ease of doing business, according to the World

Bank, and has the lowest tax rate in Europe at 10%.

Target On Its Back? Given the solid returns from a largely funded asset in an improving business

destination, we believe that Euromax represents a potential take-out target. We

believe that potential acquirers include Dundee Precious Metals (DPM–SP) or, in

fact, the same company that bought the previous assets assembled by this

management team, Eldorado Gold (EGO–SO).

Team Has The Track Record To Deliver The management team at Euromax has a strong track record of project delivery,

having come to the company from European Gold Fields following its acquisition

by Eldorado Gold. We believe that this team will continue to progress the project

towards commissioning with minimal issues, as it has demonstrated thus far.

Share Price Performance Exhibit 6 illustrates Euromax’s performance over the last 12 months. What

seems to be a relatively sideways-moving stock hides some wild swings in the

share price, having dropped as much as 60% and then climbed back to some

5% above the starting point before now trading at about 20% lower than the

starting point a year ago.

Be warned, this is junior-developer territory and it is not for investors with low

risk tolerance. It must be noted that there really aren’t many developers

building new copper projects at this juncture – a clear sign of value in itself, in

our opinion.

Exhibit 6. 12-month Share Price Performance, Indexed (Left) And Actual (Right)

Share price performance cannot and should not be viewed as an indicator of future performance.

Source: Bloomberg and CIBC World Markets Inc.

Initiation: Timing Is Everything - August 13, 2015

10

Key Catalysts We believe that there are a number of forthcoming catalysts for Euromax over

the next 12 to 24 months – all of which should be share price positive:

Reserve / Resource Update (September 2015);

Main Board Listing on TSX (September 2015);

Feasibility Study Completion (October 2015);

Final Offtake Term Sheet (October 2015);

Final Bank Funding Commitment (January 2016);

Receipt Of The Exploitation Permit (October 2016);

Mine Building Start (November 2016); and,

First Production (H2/2017).

The current cash position (about $10 million) is sufficient (given two $15 million

payments from the streaming agreement with Royal Gold to fund the feasibility

study) to take the mine plan through to the build decision. The anticipated

equity issue of $100 million will essentially mark the point at which all permitting

and funding is lined up for the build decision around mid-2016.

Valuation And Price Target Calculation As mentioned, our conservative analysis points to a reasonable chance of

success, in particular given the view that the copper price should be improving

in the future. In our evaluation, we also take account of a $100 million equity

issue, which we assume to be done at the current share price, while our costs

are slightly higher and the assumed build-out a little slower. We also believe

that the constant drift lower in the global cost curves, as well as slight tweaks to

the capital plan (which should deliver lower capex needs), should improve the

feasibility study numbers (when released before year-end 2015).

Being reasonably conservative, we derive a NAV at a 10% discount rate of some

$0.58/share or roughly C$0.70/share at the CIBC forecast metals price scenario.

Against this, using today’s very low spot metals prices, we see value to about

C$0.10/share (using a fairly aggressive 10% discount rate while at 5% that

value jumps to about C$0.75/share).

Mining is always about taking risk, and not least is having to take a view on

future gold and copper prices. However, if a mine can be built at these prices

(with gold and copper down close to 50% from their respective peaks in 2011)

and still make a case for some returns, then we believe it is set up perfectly for

when the cycle improves. Simply put, any low-cost mine should stand the test of

time through the cycle and the Ilovica Project seems to be squarely positioned

south of the mid-point on a copper and/or gold cost curve.

Given our conservative modeling approach, we opt to price the stock at a P/NAV

multiple of 1x, delivering a price target of C$0.70/share based on CIBC

estimates of long-term gold at $1,200/oz. and copper at $2.75/lb.

Initiation: Timing Is Everything - August 13, 2015

11

The Ilovica Project The 100%-owned Ilovica Project is located in the southeast of Macedonia,

approximately 15 kilometres to the west of the border with Bulgaria. As shown

in Exhibit 7, Ilovica is a porphyry copper-gold deposit, located in a

northwest-southeast-striking Tertiary magmatic arc that covers large areas of

Central Romania, Serbia, Macedonia, Southern Bulgaria, Northern Greece and

Eastern Turkey. The area comprises an undulating mountainous topography,

with moderately rugged steep slopes up to 30° and generally rounded mountain

tops, with flat valley floors. The PFS on the project anticipates annual production

of 95 Koz. of gold and 16 Kt of copper per annum.

Exhibit 7. Regional Location Map (Left) And Regional Geological Setting

Source: Company reports.

Solid Resource As noted above, Ilovica is a gold-copper porphyry with classic porphyry zonation

and minimal post mineral overprinting in the open-pit material. The project has

a pit-constrained measured and indicated mineral resource of:

237 Mt sulphide grading 0.33 g/t Au and 0.22% Cu; and,

36 Mt oxide grading 0.33 g/t Au.

From that resource, the PFS defined a Maiden Probable Mineral Reserve of:

209 Mt sulphide at 0.34 g/t Au and 0.20% Cu; and,

16 Mt oxide at 0.33 g/t Au.

Initiation: Timing Is Everything - August 13, 2015

12

The resource positioning is also very advantageous from a number of aspects,

including the readily available infrastructure that significantly enhances the

economics of the project. As we show in Exhibit 8, the mine itself will be

obscured from the nearby town of Ilovica by a deep valley next to the hill,

supplying ample capacity for life-of-mine tailings.

Exhibit 8. The Ore Body Is Very Well Positioned For Easy Access To All Needed Infrastructure, But Still Essentially Out Of Site – Even From The Nearby Village Of Ilovica

Source: Company reports and CIBC World Markets Inc.

Exhibit 9 summarizes the current Reserve / Resource Statement. We believe this

will see a significant amount of ounces reporting to the Proven Reserve category

when the next update is provided.

Ilovica Town In The Foreground – The Ore Body Sits In A Natural Amphitheatre Being Entirely Obscured From View By The Front Of This Hill

The Tailings Dam Will Sit In This Valley –Again, Not Visible From The Town, But With The Water Stream Diverted To Flow Past The Tailings Dam To The Users Down-Stream.

Ilovica Reservoir

Initiation: Timing Is Everything - August 13, 2015

13

Exhibit 9. Current Ilovica Reserve & Resource

Grade Contained Metal

Reserve Tonnage (Kt) Au (g/t) Cu (%) Au (Koz.) Cu (Klb.)

Sulphide Probable 208,650 0.34 0.20 2,276 905,100

Oxide Probable 16,230 0.33 0.0 172 0.0

Grade Contained Metal

Resource Tonnage (Kt) Au (g/t) Cu (%) Au (Koz.) Cu (Klb.)

Sulphide

Measured 18,440 0.34 0.22 200 88,677

Indicated 218,640 0.33 0.22 2,341 1,036,427

M&I 237,080 0.33 0.22 2,541 1,125,104

Inferred 19,850 0.36 0.22 226 96,942

Oxide

Measured 1,340 0.38 0.0 16 0.0

Indicated 35,540 0.33 0.0 365 0.0

M&I 35,880 0.33 0.0 381 0.0

Source: Company reports.

Though the latest Resource numbers should reflect improved levels of

confidence (Resource moving into Reserve), we would not expect there to be

much in terms of resource upside at this stage as drilling is essentially focussed

on delivering the required confidence for the feasibility study. As such,

Exhibit 10 shows two sections through the optimum pit shells that will likely

remain very much unchanged.

Exhibit 10. Sections Through Optimum Pit Shells With Block Grades (Au equivalent)

Source: Company reports.

To provide a little more in terms of the lay of the land, Exhibit 11 shows some

views from the mine site, taken when we visited the site in early August 2015.

These pictures highlight that the ore body lies in a natural amphitheater that not

only “hides” the mining activity but crucially allows for a very low strip ratio of

just 0.7:1.

Initiation: Timing Is Everything - August 13, 2015

14

Exhibit 11. Panorama Around The Mine Site To Give An Indication Of The Lay Of The Land

Source: Company reports and CIBC World Markets Inc.

Mining Methodology And Sequencing The Ilovica mine site and facilities are based in two main areas, an Upper site

and Lower site. The Lower site has the run-of-mine pad and primary crusher

adjacent to the mine and pit exit around the 480 meter elevation. The haul truck

workshop and main fuel storage area are also adjacent around the 450 meter

elevation. The remaining facilities are located on an upper site around the

850 meter elevation. This upper site includes the crushed ore stockpile, process

plant, with gold room and product dispatch, and the ancillary facilities, including

the administrative and social building, stores and workshops.

The Ilovica PFS sees mining by conventional open pit using a large-scale mining

fleet. The mine will run at 10 million tonnes per annum (Mtpa), using 100 tonne

trucks, with leasing a possibility, although this is not incorporated into the PFS.

The initial stripping ratio at the mine will be 1.1:1, while the life-of-mine ratio is

forecast at 0.7:1. The early stripping requirements are high because of the

tailings dam construction.

Looking Back To Ilovica. The Mine Is Obscured From The Town

Crusher Site / Load PadConveyor Start To Plant

Natural High Wall Plant Site

Ore Body Lies In A Natural Amphitheatre (Low Strip)

Tailings Valley – Deep, Life Of Mine Capacity

Ilovica Rezervoir

Initiation: Timing Is Everything - August 13, 2015

15

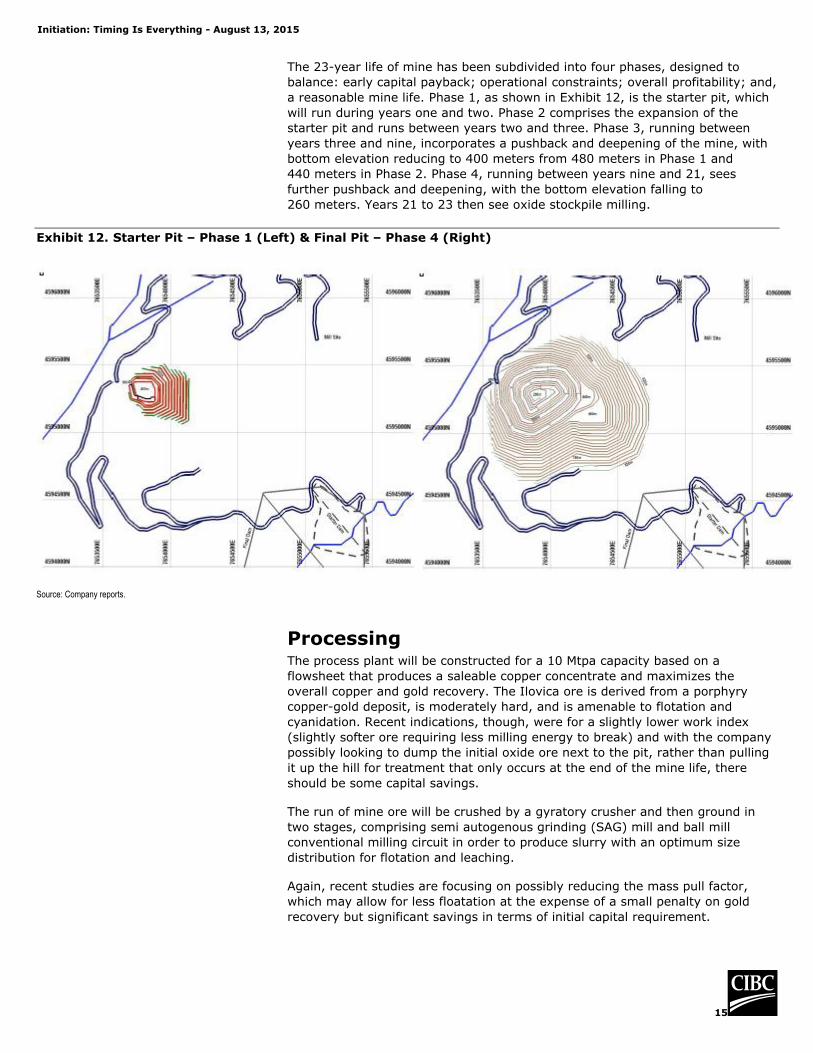

The 23-year life of mine has been subdivided into four phases, designed to

balance: early capital payback; operational constraints; overall profitability; and,

a reasonable mine life. Phase 1, as shown in Exhibit 12, is the starter pit, which

will run during years one and two. Phase 2 comprises the expansion of the

starter pit and runs between years two and three. Phase 3, running between

years three and nine, incorporates a pushback and deepening of the mine, with

bottom elevation reducing to 400 meters from 480 meters in Phase 1 and

440 meters in Phase 2. Phase 4, running between years nine and 21, sees

further pushback and deepening, with the bottom elevation falling to

260 meters. Years 21 to 23 then see oxide stockpile milling.

Exhibit 12. Starter Pit – Phase 1 (Left) & Final Pit – Phase 4 (Right)

Source: Company reports.

Processing The process plant will be constructed for a 10 Mtpa capacity based on a

flowsheet that produces a saleable copper concentrate and maximizes the

overall copper and gold recovery. The Ilovica ore is derived from a porphyry

copper-gold deposit, is moderately hard, and is amenable to flotation and

cyanidation. Recent indications, though, were for a slightly lower work index

(slightly softer ore requiring less milling energy to break) and with the company

possibly looking to dump the initial oxide ore next to the pit, rather than pulling

it up the hill for treatment that only occurs at the end of the mine life, there

should be some capital savings.

The run of mine ore will be crushed by a gyratory crusher and then ground in

two stages, comprising semi autogenous grinding (SAG) mill and ball mill

conventional milling circuit in order to produce slurry with an optimum size

distribution for flotation and leaching.

Again, recent studies are focusing on possibly reducing the mass pull factor,

which may allow for less floatation at the expense of a small penalty on gold

recovery but significant savings in terms of initial capital requirement.

Initiation: Timing Is Everything - August 13, 2015

16

The overall copper and gold recoveries are estimated at 84% and 88%,

respectively. The ground slurry, with a particle size of P80 = 75 μm, is fed into

flotation to produce a saleable copper concentrate. The copper concentrate, at

an expected copper grade of 24%, is dewatered in the concentrate thickener

and filter and shipped for smelting.

Exhibit 13. Process Plant Layout

Source: Company reports.

As it stands now, the flotation tails are fed into a pre-leach thickener and the

thickener underflow will then be pumped through Carbon in Leach (CIL) tanks.

Flotation tailings slurry will be leached in 16 CIL tanks, which utilize cyanide

leaching and recovery of the dissolved precious metals onto activated carbon.

The carbon is then pressure stripped with a hot caustic solution to elute the

precious metals into a pregnant solution, which, in turn, is treated by

conventional electrowinning to produce a gold sludge that is suitable for direct

smelting on site. Tailings from the process plant will be pumped to the Tailings

Management Facility (TMF).

Exhibit 14. Ilovica Process Flow Diagram

Source: Company reports.

Initiation: Timing Is Everything - August 13, 2015

17

The location of Ilovica offers the potential to export the concentrate product to

smelters in Bulgaria, Serbia or overseas via road or a combination of road and

rail transportation. Euromax’s preferred option is to export the concentrate to

the Pirdop refinery in Bulgaria. The company anticipates transportation costs of

$45 per tonne of concentrate from Ilovica to the Pirdop smelter. The concentrate

will travel 47 km along the paved road haul to the existing Petrich rail loading

depot on the European Rail Freight Corridor 7. There is forward rail

transportation directly to the Pirdop smelter. The close proximity of this smelter

provides a significant working capital benefit to Euromax as the delivery

essentially happens within a week of loading on the train – allowing for almost

“just-in-time” delivery to the smelter.

Exhibit 15. Pirdop Is An Important Key In Making This Project Viable – Assuring Low Cost and Securing Debt Guarantees From

Germany

Source: Company reports.

The company has been conducting a lot of work to determine the acid drainage

risks of various types of ore. In Exhibit 16 we show the current batches of

different ore types left exposed to the elements and monitored to define

leaching patterns and acid capacity. This will be very helpful in establishing the

tailings facility and for ensuring the natural water supply remains unaffected by

the mining activity. From a mining perspective, the transition from oxides to

sulphides is very pronounced (as seen in the picture of the core) and should

assist greatly in mine grade control.

Initiation: Timing Is Everything - August 13, 2015

18

Exhibit 16. Euromax Testing All Ore Types For Acid Drainage – Transition From Oxide To Sulphide Is Very Clear (Core On Right)

Source: Company reports and CIBC World Markets Inc.

Initiation: Timing Is Everything - August 13, 2015

19

Operating Cost Forecasts Per the PFS, the sulphide mining cost will be $1.72/t, the oxide mining cost

$1.96/t (including re-handle) and the waste mining cost $1.59/t (excluding

pre-strip). The total process plant operating cost has been estimated based on

the process design work and the reagent consumptions estimated based on the

prefeasibility study test work results. Per this work, the estimated process plant

operating cost is $6.50 per tonne, the split of which is shown in Exhibit 17.

Exhibit 17. Operating Costs (Left) And Processing Cost Split (Right)

US$/t

Mining Costs

Mining - Oxide 1.96

Mining – Sulphide 1.72

Mining – Waste 1.59

Conveyor 0.10

Processing Costs

Oxide Processing 5.23

Sulphide Processing 6.50

Infrastructure Opex 0.29

G&A 1.00

Source: Company reports and CIBC World Markets Inc.

Based on our analysis, these $/t costs equate to $/oz. cash costs of about

$500/oz. over the life of mine, with lower costs during the initial stages of

operation, a function of higher-grade throughput. On an AISC basis the number

comes to $800/oz. on a gold-equivalent basis. These costs would place Euromax

squarely in the bottom half of the international gold cost curve.

Consumables, $1.97

Reagents, $2.09

Power, $2.19

Labour, $0.11

Maintenance & Spares, $0.14

Initiation: Timing Is Everything - August 13, 2015

20

Infrastructure Requirements As previously noted, the mine site and facilities are based in two main areas, an

Upper site and Lower site; the layout of the mine and associated infrastructure

are shown in Exhibit 18. Aside from the mining and processing assets, we

provide details of the other infrastructure requirements below.

Exhibit 18. Surface Infrastructure Overall Layout

Source: Company reports.

Logistics

The upper and lower sites will be connected to the existing highway M6 by a

newly constructed paved road. The new intersection at M6 is presently proposed

for construction between Turnovo and Sekirnik. A network of internal

gravel-covered roads will connect the site facilities.

Water

Identifying a sustainable water supply for the project is currently considered to

be the most critical issue. A number of options for water supply were considered

in the PFS. Current options include: 1) supernatant water from the tailings,

supplemented by inflows into the pit, run-off from the tailings/waste rock facility

and rain/snow falling within the catchment of the overall mine site; 2) make-up

water from the Turija reservoir via the Turija Canal to the Ilovitza reservoir,

which could supply some 2 million to 3 million m3/year; and, 3) a borehole field

around the uphill side of the open pit. Water supply options will be further

investigated during the feasibility study and the impacts assessed as part of the

Environmental Impact Study (EIA) in a way that evaluates impacts to the water

supply of third parties and impacts on other environmental or social receptors.

Initiation: Timing Is Everything - August 13, 2015

21

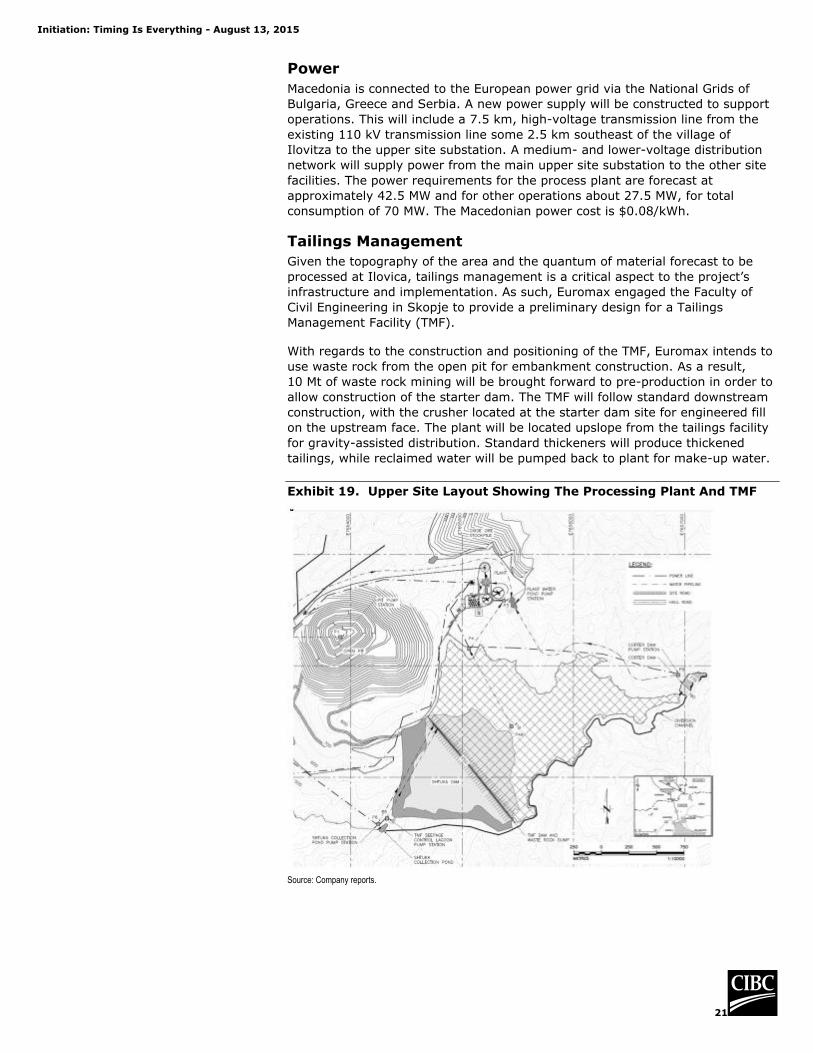

Power

Macedonia is connected to the European power grid via the National Grids of

Bulgaria, Greece and Serbia. A new power supply will be constructed to support

operations. This will include a 7.5 km, high-voltage transmission line from the

existing 110 kV transmission line some 2.5 km southeast of the village of

Ilovitza to the upper site substation. A medium- and lower-voltage distribution

network will supply power from the main upper site substation to the other site

facilities. The power requirements for the process plant are forecast at

approximately 42.5 MW and for other operations about 27.5 MW, for total

consumption of 70 MW. The Macedonian power cost is $0.08/kWh.

Tailings Management

Given the topography of the area and the quantum of material forecast to be

processed at Ilovica, tailings management is a critical aspect to the project’s

infrastructure and implementation. As such, Euromax engaged the Faculty of

Civil Engineering in Skopje to provide a preliminary design for a Tailings

Management Facility (TMF).

With regards to the construction and positioning of the TMF, Euromax intends to

use waste rock from the open pit for embankment construction. As a result,

10 Mt of waste rock mining will be brought forward to pre-production in order to

allow construction of the starter dam. The TMF will follow standard downstream

construction, with the crusher located at the starter dam site for engineered fill

on the upstream face. The plant will be located upslope from the tailings facility

for gravity-assisted distribution. Standard thickeners will produce thickened

tailings, while reclaimed water will be pumped back to plant for make-up water.

Exhibit 19. Upper Site Layout Showing The Processing Plant And TMF

Source: Company reports.

Initiation: Timing Is Everything - August 13, 2015

22

Permitting

Mining Concession Approved

On July 21, 2012, pursuant to Article 33 of the Law on mineral raw materials,

Euromax was granted a 30-year Exploitation Permit & Mining Concession over

the Ilovica Project Area, by way of a 30-year lease for peppercorn rent to the

Ministry of Forestry (all state Forestry land). The granting and gazetting of the

concession was formally endorsed by the Ministries of Forestry, Agriculture,

Transport & Communications and Culture and ratified for approval by the

Ministry of Environment under the EIA.

Local EIA Approved

The Ilovica Project EIA was approved and gazetted by the Ministry of

Environment on September 27, 2012, pursuant to Article 87 paragraph 1 of the

Law on Environment. The approval provides for the mining and processing of up

to 20 Mtpa within the conceptual footprint of the project. The approval followed

local and national public consultation and was formally enacted into Macedonian

Law without any comment or objection.

Construction Permit

The Exploitation Permit requires the commencement of construction in Q4/2016

and, to achieve such, the Main Mining Project, a document confirming

development within the EIA approval and detailed to FEED level, must be lodged

for confirmatory approval by June 30, 2016. Euromax is preparing these

documents to the exact standards required to ensure, to the extent possible, the

granting of final approvals about 60 days after submission at the end of June.

Exhibit 20. Financing Running In Tandem With Mine Design And

Permitting

Source: Company reports.

Initiation: Timing Is Everything - August 13, 2015

23

Offtake / Debt

The Main Mining Project submission requires the timely finalization of a number

of other issues, thereby positioning Euromax to start constructing the mine by

the time the Main Mining Project is approved. Part and parcel is the final signing

of the offtake contract with Pirdop, as well as the bank debt commitments and

term sheets – all running in tandem with the mine design and permitting

process.

Given the need to be in position to build the mine once the Main Mining Project

is signed off (around the end of August/beginning of September 2016), Euromax

will have to ensure all funding is in place before then – possibly placing the

timing of the equity issue at around April 2016, by our estimation.

Capital Expenditure Requirements Per the PFS, initial capital expenditure has been estimated at $501.8 million,

with sustaining capital expenditure $236.1 million. The split of these capital cost

estimates is shown in Exhibit 21.

Exhibit 21. Ilovica Capital Expenditure Split ($ mlns.)

Item Initial Capex Sustaining Capex Processing Items Initial Capex

Mining Fleet $34.8 $128.0 Primary Equipment Cost $69.9

Processing Plant 249.5 (in opex) Indirect Capital Costs 125.8

Owners Costs 10.0 0 Site Prep & Construction Management

29.4

Infrastructure 103.8 30.6 Plant Mobile Equipment Cost 6.7

Tailings (incl. pre-strip) 58.1 47.5 Coarse Ore Stockpile Cost 14.4

Reclamation 0.0 30.0 Elution & Gold Room Package 3.4

Sub-Total 456.2 236.1 Total Processing Capital Costs 249.5

Contingency (10%) 45.6 0

Total 501.8 236.1

Source: Company reports and CIBC World Markets Inc.

As shown in Exhibit 21, within the processing cost capex estimates, the larger

components include primary equipment costs and indirect capital costs. Of these

indirect capital costs, there is $21 million for civils, $16.8 million for structural

steel, $24.5 million for piping and valves, $28 million for electrical and

instrumentation, $21 million for transport and $10.5 million for erection of

items. Within the infrastructure capex estimates, the largest component is

power supply and distribution at $50.6 million, with all other components

sub-$10 million.

Funding The Capex Spend We anticipate material capital expenditure to be incurred from 2017 (post

anticipated receipt of the construction permit in Q3/2016), with one and a half

years of construction before commissioning. We believe that the majority of the

capital will be incurred in year one of the build. However, given that Euromax

has about $10 million in cash, how does it propose to fund the $500 million

capital forecast?

First, the company has put in place an agreement worth $175 million with Royal

Gold. Euromax will receive within one year of the agreement two tranches

totaling $15 million and a third tranche of $160 million toward construction. This

cash from Royal Gold will fund 32% of the PFS construction capex and is in

exchange for selling 25% of gold produced at Ilovica at 25% of the prevailing

spot gold price, representing 14% of gold equivalent production.

Initiation: Timing Is Everything - August 13, 2015

24

Second, in May 2015, Euromax announced that it had received UFK in-principle

eligibility, the German Untied Loan Guarantee Scheme (UFK – Garantien für

Ungebundene Finanzkredite), to provide cover for a project finance facility on

the assumption that a copper concentrate offtake agreement is entered into with

a German-owned smelter. In association, the company executed a Mandate

Letter and Term Sheet with a number of European banks to provide up to

$215 million of Senior Secured Project Finance, subject to due diligence and all

necessary approvals. The company has also executed a Mandate Letter and

Term Sheet with Caterpillar Financial (CAT–NYSE) to arrange an equipment

financing facility for up to $25 million to finance any Cat equipment purchased

for the project.

Payback Period The PFS’ economic evaluation of the Project using discounted cash flow was

prepared on a pre-tax and a post-tax basis. For the 23-year mine life, 225 Mt

total throughput, operating at 10 Mtpa and using $3.00/lb. copper and

$1,250/oz. gold, the PFS returned the following financial results:

18.6% IRR pre-tax, 16.5% IRR post-tax;

6.3 years pre-tax payback, 6.8 years post-tax payback on $501.8 million

initial capital;

$675 million pre-tax Net Present Value (NPV) at a 5% discount value; and,

$558 million post-tax NPV at 5% discount value.

Naturally, these returns are a lot lower given today’s much lower metals prices,

with the cash flow sensitivity in Exhibit 22 indicating the project approaching

break-even around current metals prices (and based on pre-feasibility numbers,

which should improve somewhat once the feasibility numbers are provided).

Exhibit 22. Forecast Cash Position (At Spot $1,120/oz. Gold And

$2.40/lb. Copper) – Essentially Just A Little Better Than Break-even After Assuming $100 Million In Equity Funding

Source: Company reports and CIBC World Markets Inc.

-400

-300

-200

-100

0

100

200

300

2014A 2015E 2016E 2017E 2018E 2019E 2020E

Cum

ulat

ive

Cas

h B

alan

ce U

S$

Mill

ion)

-30% -20% -10% Spot +10% +20% +30%

Initiation: Timing Is Everything - August 13, 2015

25

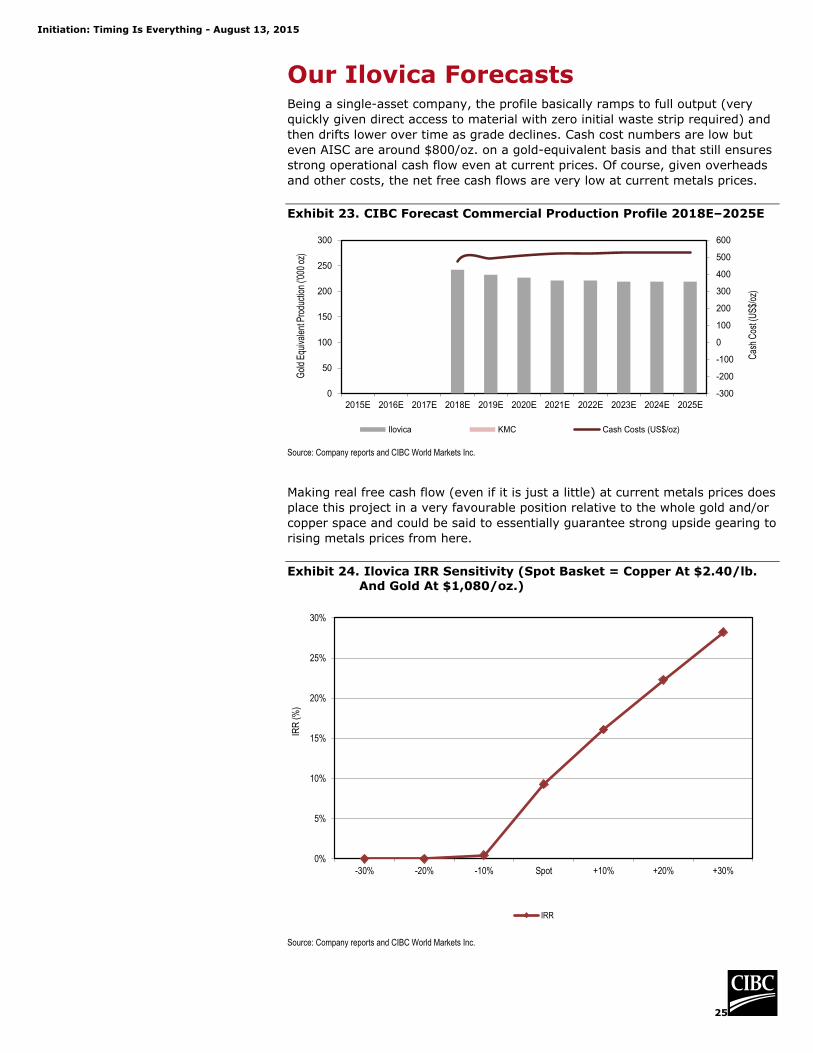

Our Ilovica Forecasts Being a single-asset company, the profile basically ramps to full output (very

quickly given direct access to material with zero initial waste strip required) and

then drifts lower over time as grade declines. Cash cost numbers are low but

even AISC are around $800/oz. on a gold-equivalent basis and that still ensures

strong operational cash flow even at current prices. Of course, given overheads

and other costs, the net free cash flows are very low at current metals prices.

Exhibit 23. CIBC Forecast Commercial Production Profile 2018E–2025E

Source: Company reports and CIBC World Markets Inc.

Making real free cash flow (even if it is just a little) at current metals prices does

place this project in a very favourable position relative to the whole gold and/or

copper space and could be said to essentially guarantee strong upside gearing to

rising metals prices from here.

Exhibit 24. Ilovica IRR Sensitivity (Spot Basket = Copper At $2.40/lb.

And Gold At $1,080/oz.)

Source: Company reports and CIBC World Markets Inc.

-300

-200

-100

0

100

200

300

400

500

600

0

50

100

150

200

250

300

2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

Cas

h C

ost (

US

$/oz

)

Gol

d E

quiv

alen

t Pro

duct

ion

('000

oz)

Ilovica KMC Cash Costs (US$/oz)

0%

5%

10%

15%

20%

25%

30%

-30% -20% -10% Spot +10% +20% +30%

IRR

(%

)

IRR

Initiation: Timing Is Everything - August 13, 2015

26

Exhibit 25 illustrates the sensitivity of our Ilovica NAV estimate to metals prices,

costs and capital expenditure inputs.

Exhibit 25. Ilovica NAV Sensitivity At 5% (LEFT) And 10% (RIGHT)

Source: Company reports and CIBC World Markets Inc.

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

-30% -20% -10% Spot +10% +20% +30%

NA

V/ S

hare

(US

$)

Gold Copper

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

-30% -20% -10% Spot +10% +20% +30%

NA

V/ S

ha

re (

US

$)

Gold Copper

Initiation: Timing Is Everything - August 13, 2015

27

The KMC Project The KMC project is located in southwest Serbia, about 200 kilometres from the

capital, Belgrade. The licence covers 23.6 square kilometres and was renewed

for an additional two years on March 20, 2014. KMC’s mineralisation includes

thick sequences of gold-copper skarns, gold skarns, zinc-lead-copper-gold

skarns and volcanic-hosted, gold-mineralised silica breccias. We believe that

Euromax will continue to prioritise capital towards Ilovica, rather than KMC, as

indicated by the decision to suspend exploration expenditure at KMC during

2014. A possible sale of the asset is highly likely, in our opinion.

Exhibit 26. KMC Gravity Anomaly Map (Left) And Cross-section Through Medenovac Prospect

Source: Company reports.

Initiation: Timing Is Everything - August 13, 2015

28

Company Management Chief Executive Officer: Steve Sharpe

Steve Sharpe was appointed as President and Chief Executive Officer and a

director in May 2012. He is also an Honorary Board Member of Macedonia 2025,

a group dedicated to enhancing business opportunities and the economic

development of Macedonia.

Mr. Sharpe was previously Senior Vice President, Business Development at

European Goldfields Limited from July 2010 until March 2012, where he focused

on raising the profile of the company in the European and North American

market and developing the optimum financing solution for the advancement of

the company’s gold assets. Prior to that, he was Managing Director in Structured

Finance. He has over 25 years of investment banking experience, focused on the

mining sector.

Chairman: Martyn Konig

Martyn Konig was appointed as Non-Executive Chairman and a director in

May 2012 and is Chairman of the Compensation Committee.

Mr. Konig has 30 years of experience in investment banking and the commodity

markets. Until February 2012, he was Executive Chairman and President of

European Goldfields Limited. He has extensive experience in the natural

resource sector, which includes senior management responsibility in resource

finance and commodity trading operations at various international investment

banks.

Project Manager: Pat Forward

Pat Forward was previously VP, Projects & Exploration at European Goldfields,

where he was responsible for the development of the Skouries and Olympias

projects in Greece and the Certej project in Romania through feasibility work,

basic engineering and financing. In addition, Mr. Forward was responsible for

European Goldfields’ exploration properties in Romania, Greece and Turkey and

the growth and compliance of that company’s resource and reserve base.

In the early 1990s, he managed exploration projects in Europe, Ghana and

Venezuela before spending some five years in Burkina Faso managing

exploration programs. Mr. Forward is also specialised in geological due diligence,

resource estimation, the application of GIS systems to exploration projects, and

deposit evaluation, and is a Qualified Person with respect to NI 43-101

reporting.

Initiation: Timing Is Everything - August 13, 2015

29

Political Risk And Mining In Macedonia Macedonia is not the first location to spring to mind as a mining destination of

choice but, as Euromax is progressively showing, the country has the capacity to

further develop its (very) nascent mining industry. Indeed, Ilovica would

represent the first mining development by a foreign company in the country for

many years, although there remain a few other foreign-held development

assets, with Reservoir Minerals (RMC–SP) retaining the Konjsko and Dvoriste

exploration concessions in the country.

Outside of the development of mining as a source of foreign direct investment,

Macedonia has made significant strides in liberalising and opening up its

economy. Indeed, relative to its Balkan and Southeast European peers, the

country ranks favourably on the ease of doing business, according to the World

Bank, as shown in Exhibit 27.

Exhibit 27. World Bank – How Macedonia, FYR And Comparator

Economies Rank On The Ease Of Doing Business

Source: World Bank.

As shown in Exhibit 28, in terms of the World Bank’s ratings, the country

features very favorably in terms of the ability to start a business, the ability to

pay taxes, protecting minority investors, resolving insolvency and getting credit.

Unfortunately for Euromax, two critical areas of mining project development do

not feature so well, as dealing with construction permits and getting electricity

are the two worst-scoring components of doing business in the country.

However, it should be noted that even these represent low relative scores and

both components are still in the top half of global rankings.

Initiation: Timing Is Everything - August 13, 2015

30

Exhibit 28. Components Of Doing Business In Macedonia

Rankings On Doing Business Topics (Scale: Rank 189 Center, Rank 1 Outer Edge)

Distance To Frontier Scores On Doing Business Topics (Scale: Score 0 Center, Score 100 Outer Edge)

Source: World Bank.

A new tax regime became effective in Macedonia as of January 1, 2009,

whereby the base for income tax computation was shifted from the “profit before

tax” concept to the “profit distribution” concept. As per the Macedonian

Corporate Income Tax (CIT) Law, tax is calculated and payable at a rate of 10%

on two components, and both components are taxed separately from each

other:

Component 1: Expenses not recognized for tax purposes and understated

revenues; and,

Component 2: Profit distribution.

The tax rate on both components is currently set at 10% and, as such, the PFS

applied this rate to the financial model with no tax holiday. The PFS estimates

that the total tax payable for the life of the project is $193 million. The PFS has

also applied a state royalty at 2% of the net smelter return (NSR). This is

estimated as an average annual cost of $4.3 million during full production from

sulphide ore. The total royalty payable is $92.7 million for the LOM.

Initiation: Timing Is Everything - August 13, 2015

31

Exhibit 29. Macedonia – Keen To Catch Up And Become Part Of EU

Source: Company reports and CIBC World Markets Inc.

Conclusion Euromax is a developing junior miner with a solid project in a solid setting and

sporting low costs that should see it deliver through-the-cycle value. This view is

backed by some 80% of funding that has already been secured, with the 20%

equity portion likely lining up in H1/2016.

The project reflects low-single-digit IRRs at current metals prices, implying that

it is not without risk, but given the low cost profile, chances are certainly higher

than average that this will be a good long-term investment that will also pay out

a very good dividend stream based on management’s strategy to spin out all the

free cash from this mine.

Lining up to build a mine is never without risk and investors with a low risk

appetite should probably hold off until the metal is flowing. For those

longer-term-focused investors, we would advocate buying sooner than later.

Initiation: Timing Is Everything - August 13, 2015

32

Valuation

Price Target Calculation The Ilovica Project is essentially a very low-risk project. The mining is easy and

implies low costs, providing good through-the-cycle potential. The funding is

already 80% secured and the offtake agreement with the nearby smelter adds

significantly to the favorable cost dynamics. Given management’s undertaking to

pay out all free cash flow generated from the project, the dividend potential

remains high and essentially secures an even better potential slice for investors

when or if metals prices were to rise again.

Still, given pre-development status, we apply a 10% discount rate to reach an

NAV of $0.58/share or roughly C$0.70/share at CIBC metals price forecasts

(gold at $1,200/oz. and copper at $2.75/lb.). Then, given the low-risk nature

explained above, we apply a full 1x NAV multiple to derive a price target of

C$0.70/share with a Sector Outperformer (Speculative) rating.

Key Risks To Price Target The key risks to our price target for Euromax are as follows:

Project Execution: Management has demonstrated a strong track record

in delivering projects to commissioning but risk remains in the execution of

Ilovica.

Country Risk: The company’s activities are materially focused in

Macedonia. As such, there is the potential for further negative impacts from

political and social unrest on the company’s assets and projects.

Resource Nationalism And Taxation: This is not a risk particular to

Euromax but to the entire natural resource and silver mining industry. As

with other producers, Euromax is susceptible to changes in taxation and

royalty regimes in the countries in which it operates.

Commodity Prices: Euromax is an unhedged producer of gold and copper

and, as such, is fully exposed to the spot prices.

The CIBC analyst(s) who cover this company visited the Ilovica Project site in

Macedonia on August 4 and 5, 2015, with Euromax providing accommodation

and meals and CIBC carrying the full cost of all transportation to and from

Macedonia.

Initiation: Timing Is Everything - August 13, 2015

33

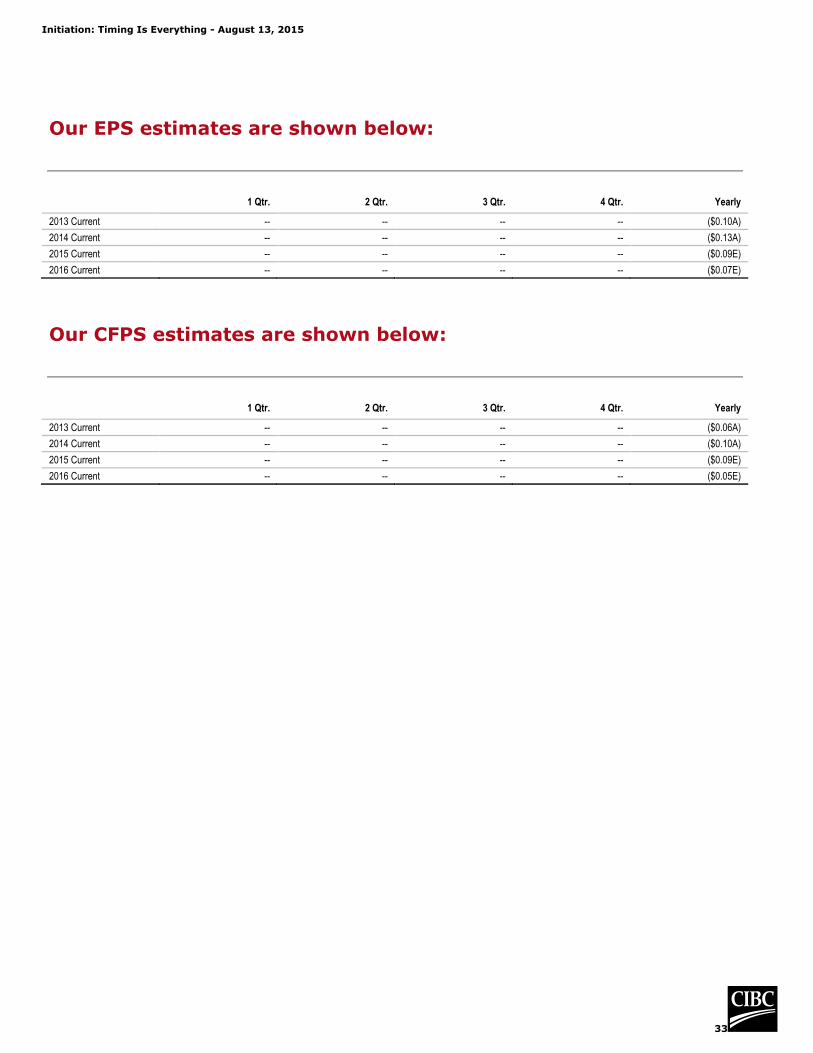

Our EPS estimates are shown below:

1 Qtr. 2 Qtr. 3 Qtr. 4 Qtr. Yearly

2013 Current -- -- -- -- ($0.10A)

2014 Current -- -- -- -- ($0.13A)

2015 Current -- -- -- -- ($0.09E)

2016 Current -- -- -- -- ($0.07E)

Our CFPS estimates are shown below:

1 Qtr. 2 Qtr. 3 Qtr. 4 Qtr. Yearly

2013 Current -- -- -- -- ($0.06A)

2014 Current -- -- -- -- ($0.10A)

2015 Current -- -- -- -- ($0.09E)

2016 Current -- -- -- -- ($0.05E)

Initiation: Timing Is Everything - August 13, 2015

34

IMPORTANT DISCLOSURES:

Analyst Certification: Each CIBC World Markets research analyst named on the front page of this research report, or

at the beginning of any subsection hereof, hereby certifies that (i) the recommendations and opinions expressed herein

accurately reflect such research analyst's personal views about the company and securities that are the subject of this

report and all other companies and securities mentioned in this report that are covered by such research analyst and (ii)

no part of the research analyst's compensation was, is, or will be, directly or indirectly, related to the specific

recommendations or views expressed by such research analyst in this report.

Potential Conflicts of Interest: Equity research analysts employed by CIBC World Markets are compensated from

revenues generated by various CIBC World Markets businesses, including the CIBC World Markets Investment Banking

Department. Research analysts do not receive compensation based upon revenues from specific investment banking

transactions. CIBC World Markets generally prohibits any research analyst and any member of his or her household from

executing trades in the securities of a company that such research analyst covers. Additionally, CIBC World Markets

generally prohibits any research analyst from serving as an officer, director or advisory board member of a company that

such analyst covers.

In addition to 1% ownership positions in covered companies that are required to be specifically disclosed in this report,

CIBC World Markets may have a long position of less than 1% or a short position or deal as principal in the securities

discussed herein, related securities or in options, futures or other derivative instruments based thereon.

Recipients of this report are advised that any or all of the foregoing arrangements, as well as more specific disclosures

set forth below, may at times give rise to potential conflicts of interest.

Important Disclosure Footnotes for Euromax Resources (EOX)

CIBC World Markets Inc. expects to receive or intends to seek compensation for investment banking

services from Euromax Resources in the next 3 months.

Important Disclosure Footnotes for Companies Mentioned in this Report that Are Covered

by CIBC World Markets Inc.:

Stock Prices as of 08/13/2015:

Dundee Precious Metals Incorporated (2g) (DPM-TSX, C$2.18, Sector Performer)

Eldorado Gold Corporation (2g, 7) (EGO-NYSE, $3.81, Sector Outperformer)

Reservoir Minerals Inc. (2g) (RMC-V, C$4.18, Sector Performer)

Royal Gold, Inc. (2g) (RGLD-NASDAQ, $53.00, Sector Outperformer)

Companies Mentioned in this Report that Are Not Covered by CIBC World Markets Inc.:

Stock Prices as of 08/13/2015:

Caterpillar (CAT-NYSE, $77.76, Not Rated)

Important disclosure footnotes that correspond to the footnotes in this table may be found in the "Key to

Important Disclosure Footnotes" section of this report.

Initiation: Timing Is Everything - August 13, 2015

35

Key to Important Disclosure Footnotes:

1 CIBC World Markets Corp. makes a market in the securities of this company.

1a CIBC WM Corp. makes a market in the securities of this company

1b CIBC WM Corp. makes a market in the securities of this company

1c CIBC WM Corp. makes a market in the securities of this company

2a This company is a client for which a CIBC World Markets company has performed investment banking services

in the past 12 months.

2b CIBC World Markets Corp. has managed or co-managed a public offering of securities for this company in the

past 12 months.

2c CIBC World Markets Inc. has managed or co-managed a public offering of securities for this company in the

past 12 months.

2d CIBC World Markets Corp. has received compensation for investment banking services from this company in

the past 12 months.

2e CIBC World Markets Inc. has received compensation for investment banking services from this company in the

past 12 months.

2f CIBC World Markets Corp. expects to receive or intends to seek compensation for investment banking services

from this company in the next 3 months.

2g CIBC World Markets Inc. expects to receive or intends to seek compensation for investment banking services

from this company in the next 3 months.

3a This company is a client for which a CIBC World Markets company has performed non-investment banking,

securities-related services in the past 12 months.

3b CIBC World Markets Corp. has received compensation for non-investment banking, securities-related services

from this company in the past 12 months.

3c CIBC World Markets Inc. has received compensation for non-investment banking, securities-related services

from this company in the past 12 months.

4a This company is a client for which a CIBC World Markets company has performed non-investment banking,

non-securities-related services in the past 12 months.

4b CIBC World Markets Corp. has received compensation for non-investment banking, non-securities-related

services from this company in the past 12 months.

4c CIBC World Markets Inc. has received compensation for non-investment banking, non-securities-related

services from this company in the past 12 months.

5a The CIBC World Markets Corp. analyst(s) who covers this company also has a long position in its common

equity securities.

5b A member of the household of a CIBC World Markets Corp. research analyst who covers this company has a

long position in the common equity securities of this company.

6a The CIBC World Markets Inc. fundamental analyst(s) who covers this company also has a long position in its

common equity securities.

6b A member of the household of a CIBC World Markets Inc. fundamental research analyst who covers this

company has a long position in the common equity securities of this company.

7 CIBC World Markets Corp., CIBC World Markets Inc., and their affiliates, in the aggregate, beneficially own 1%

or more of a class of equity securities issued by this company.

8 An executive of CIBC World Markets Inc. or any analyst involved in the preparation of this research report has

provided services to this company for remuneration in the past 12 months.

9 An executive committee member or director of Canadian Imperial Bank of Commerce (“CIBC”), the parent

company to CIBC World Markets Inc. and CIBC World Markets Corp., or a member of his/her household is an

officer, director or advisory board member of this company or one of its subsidiaries.

10 Canadian Imperial Bank of Commerce ("CIBC"), the parent company to CIBC World Markets Inc. and CIBC

World Markets Corp., has a significant credit relationship with this company.

11 The equity securities of this company are restricted voting shares.

12 The equity securities of this company are subordinate voting shares.

13 The equity securities of this company are non-voting shares.

14 The equity securities of this company are limited voting shares.

Initiation: Timing Is Everything - August 13, 2015

36

CIBC World Markets Inc. Stock Rating System

Abbreviation Rating Description

Stock Ratings

SO Sector Outperformer Stock is expected to outperform the sector during the next 12-18 months.

SP Sector Performer Stock is expected to perform in line with the sector during the next 12-18 months.

SU Sector Underperformer Stock is expected to underperform the sector during the next 12-18 months.

NR Not Rated CIBC World Markets does not maintain an investment recommendation on the stock.

R Restricted CIBC World Markets is restricted (due to potential conflict of interest) from rating the stock.