ifri energy breakfast roundtable brussels, february 27, 2007 1 wec european regional study: the...

Post on 18-Dec-2015

215 views

TRANSCRIPT

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 1

WEC European Regional Study: WEC European Regional Study: The Future Role of Nuclear The Future Role of Nuclear

Power in EuropePower in Europe

Alessandro CLERICI, Chairman of the study, ABB Italy

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 2

INDEX

1. Preamble

2. The launch of WEC Regional Study

3. The WEC Study Report

3.1. Introduction3.2. Chapter I3.3. Chapter II3.4. Chapter III3.5. Chapter IV3.6. Conclusions

4. Next Steps

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 3

1. Preamble

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 4

• Energy is and will remain one of the major global concerns of

the 21st Century and Europe is no exception.

• By 2050, the world population is expected to reach close to 9

billion people. Without a doubt, global energy consumption will

grow strongly and is forecast to double to some 20,000 Mtoe per

year.

• Electricity penetration rate is always increasing and electrical

energy consumption is forecast to triple to some 45,000 TWh per

year.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 5

Nuclear power is again becoming the subject of analyses and discussions. The possible recourse to nuclear power basically depends on

• environmental problems • its economic feasibility compared to other energy sources • load growth and substitution of old plants• public acceptance

The possible security of supply of some primary energy resources and their price volatility is another factor in favour of better analyses on the nuclear option. EC has considered what above in their “green paper”.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 6

Europe is the continent with the largest number of reactors in operation in 2005 (204 over 441 worldwide), the largest nuclear capacity in operation (172 GW over 368 GW worldwide) and the largest production of electricity from nuclear plants (1200 TWh over 2600 TWh) which corresponds to about 28% of the total electricity produced in European countries (4200 TWh).

What about Europe?

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 7

After the nuclear industry restructuring of the nineties, Europe has also the largest manufacturing NPP industry with BNFL (including the previous BNFL, ASEA ATOM and it was including the previous Westinghouse nuclear, now Toshiba), FRAMATOME ANP (AREVA) and the RUSSIANS.

Europe has the major shares of world capacities in conversion of uranium oxide to UF6, in enrichment and final fabrication; European uranium resources are however scarce and Europe will depend more and more in exploration and extraction abroad.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 8

2. The launch of WEC Regional Study

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 9

• In 2005, the European Regional Group decided to launch a study “The Future Role of Nuclear Power in Europe”.

• A study group was created, including 25 active members from 20 European countries.

• The first Study Group Meeting took place in Bucharest, in May 23, 2005 and the fifth and last one in Helsinki on November 1-2, 2006.

• The final report has been launched in London by WEC on January 30, 2007 and it is now on WEC site

http://www.worldenergy.org/wec-geis/news_events/news/pressreleases/pr220107.asp

The launch of WEC Regional Study

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 10

3. The WEC Study Report

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 11

• Energy in general and electricity in particular are always more essential to economic development and to prosperity, health and security of citizens: GDP is strictly related to energy consumption/cost/quality of supply.

• The world population in these last 10 years has seen an increase of more than 12% and now East & South East Asia together with South Asia account for more than 55% of the global world population; Europe has seen an increase in population of 1.4% (EU 25 of 2%) and has now the 13.6% of the 6.4 billion people leaving in the world. (EU 7.2%).

• The world primary energy consumption, now of about 11,000 MTOE, has seen an increase in 10 years of 20% led by E-S&SE Asia availing an increase of around 35% compared to the 7.3% value of Europe and 10.2% of EU 25.

3.1. Introduction

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 12

• The world electricity consumption, now of about 18,000 TWh, is characterized by an increase in the last 10 years of more than 31.5% with E-S&SE Asia having a value above 60% compared to the 16% one of EU 25 and 20.6% of EU 25.

• Electricity consumption is therefore growing faster than primary energy consumption also in Europe and in EU 25 and its penetration rate is always more increasing.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 13

• Considering the dramatic increase of electricity consumption driven by E-S&SE Asia (e.g. China and India) and by a portion of world population of around 1.7 billion people which doesn’t avail now commercial energy sources, there is the expectation of future high and volatile fossil fuel prices, of security of some prime energy resources supply and of environmental problems caused by the explosion of coal plants in E-S&SE Asia and gas CCGT plants in liberalized markets. It is worth mentioning how oil and gas prices have seen a practical doubling in these last 2 years.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 14

Considering:

• EU 25 is always more dependent on external energy supplies (50% now and more than 70% in 2030)

• the key role of Russia and other CSI countries in the European energy arena

• the necessary investments to meet growth in demand and old power plants replacement

• the commitment for CO2 emissions• European competitiveness

in 2005, the WEC European Regional Group decided tolaunch with high priority a study to clarify the conditionsnuclear should meet, to be re-integrated into theEuropean electricity market.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 15

The four main chapters of the final WG report cover four areas:

• Electricity production in Europe (coordinated by A. Gonzales - Spain)

• Overview of existing NPP’s in Europe (coordinated by F. Naredo - Belgium)

• Development of new NPPS’s with existing technologies (2010-2030) (coordinated by D. Beutier /M. Benard -France)

• Nuclear power with new technologies (coordinated by F. Carré - France)

The conclusions report the key issues raised by the WG with respect to the possible “renaissance” of a nuclear option in Europe.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 16

3.2. Chapter I: Current Overview of the Electricity

Production in EuropeCoordinator: Mr. Antonio Gonzalez (FORO NUCLEAR - Spain)

1.1. Introduction

1.2. Current Overview of Electricity Production in Europe

. Energy mix - EU and EUROPE, Dec 31st. 2004

31.0% 27.5%

54% 54%

10% 15% 3.6% 5%

0%

20%

40%

60%

80%

100%

EU 25 EUROPE

Other Hydro Thermal Nuclear

Generation mix (TWh per year) Dec 31st. 2004

939 1210

1637

300 659

151 157

2375

0

500

1000

1500

2000

2500

E U 25 EUROPE

Nuclear Thermal Hydro Other

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 17

The Ageing Factor

0

20

40

60

80

100

120

140

0-5 6-10 11-15 16-20 21-25 26-30 31-35 36-40 41-45 46-50 51-120classe di età

GW

coal and lignite nuclear oil natural gas hydro renewables dual fuel unknown

11%

9%

7%

15%14%

13%

12%

8%

4%

3% 3%

80% in 2020 >30 years

30% now > 30 years

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 18

3.3. Chapter II: Overview of Nuclear Power in EuropeCoordinator: Mr. Fernando Naredo

(Westinghouse-Belgium)

• Status of NPPs in Europe• Economics and Performances of Existing NPPs• Life Extension and Power Up-ratings• Status and Strategies on Radioactive Waste

Management and Decommissioning• Public Acceptance• Governmental and Industrial Prospects for Nuclear

Power

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 19

Installed nuclear capacity and number on nuclear units EUROPE 36 December 31st, 2004

1815

23

119

7 6 5 41 1 1 1

31

644

58

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

Fra

nce

Rus

sia

Ger

man

y

Ukr

aine UK

Sw

eden

Spa

in

Bel

gium

Cze

ch R

ep.

Sw

itzer

land

Bul

garia

Fin

land

Slo

vaki

a

Hun

gary

Lith

uani

a

Rom

ania

Slo

veni

a

Net

herla

nds

Inst

alle

d c

apac

ity

GW

e

0

10

20

30

40

50

60

70

Nu

clea

r re

acto

rs

Nuclear Capacity GWe (left)

Number of reactors (right)

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 20

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 21

Economics and Performance of the Existing Plants

• Most of the nuclear plants operating in the EU are fully amortized at this time, and their generation cost is mainly due to O & M + Fuel.

• O&M costs are in the range from 4 to 6 euros/MWh. Fuel cost is increased due to uranium prices but still remains approximately 3.5-4 euros /MWh.

• Total cost is therefore very competitive even with provisions for final waste management, decommissioning and special taxes (when applicable).

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 22

Energy Availability Factor median

50

55

60

65

70

75

80

85

90

95

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

%

North America Western Europe Eastern Europe

Nuclear power plants are the most reliable ones

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 23

Life Extension and Power Up-rating

Reactor age of operating NPPs in Europe is

as follows:

– 30% between 25 and 35 years– 60% between 15 and 25 years– 10% less than 15 years

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 24

• NPP licensed life was planned originally for up to 40 years, to be extended, on the basis of periodic safety reviews, up to 50 to 60 years.

• Without life extension, planned reactor closures would affect more than 80% of all NPPs by 2025.

• Life extensions are programmed or in consideration, among the others, in Bulgaria, France, Netherlands, Czech Republic, Romania, Slovenia, Sweden and Switzerland.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 25

Life extension and power up-ratings are the cheapest

Sources for increasing European electricity generation

and security of supply without impact on emissions

(e.g. Sweden).

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 26

Radioactive Waste Management and Decommissioning

• Low and Intermediate Level Waste Management is a common practice with no impact on the environment and on the public acceptance.

• For High Level Waste, technical solutions exist (deep geological disposal) and there is no urgent time requirement, considering available interim storage facilities.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 27

• It is essential to act quickly at the government level to find and check suitable locations and to approach public opinion.

• In any case, appropriate legislations are necessary to secure the financing for decommissioning and high level waste disposal.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 28

Public Acceptance

• Risk perception is changing with a lower concern for major accidents. NIMBY effect for new plants is still strong but by far less for life extension of existing NPP’s.

• Recent polls in Sweden, Italy, Germany, Poland, etc. have provided key indicators of change.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 29

Governmental Attitude

Considering:

the increasing importance of energy in competitiveness in all countries

the high oil and gas prices and their security of supply the environmental concerns (CO2 emission charges)

many governments are more and more oriented to

consider a possible nuclear option

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 30

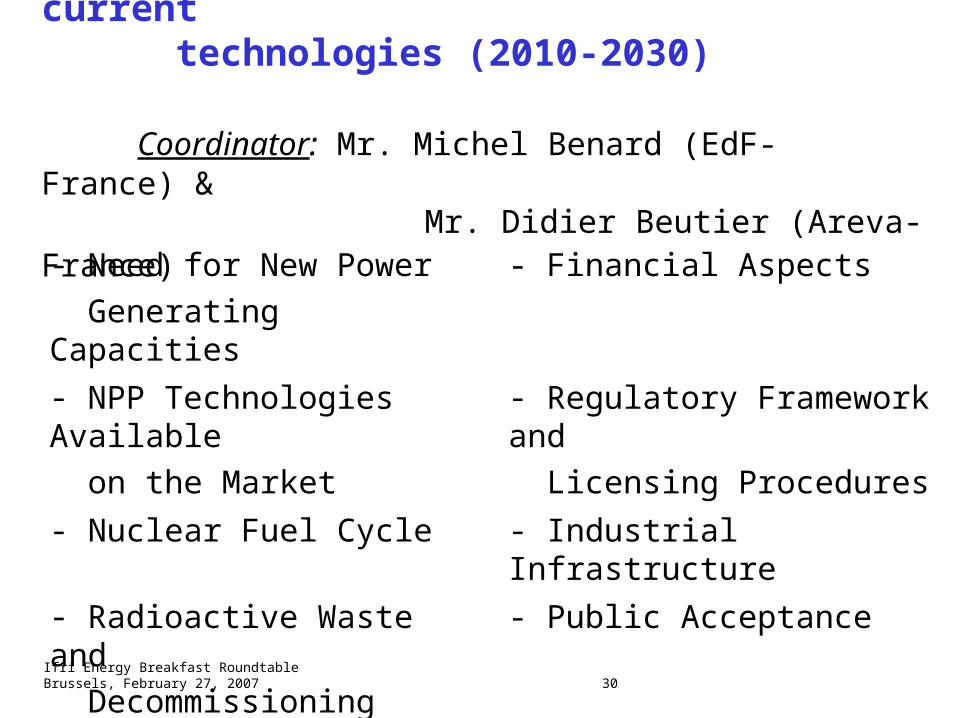

3.4. Chapter III: Nuclear power with current technologies (2010-2030)

Coordinator: Mr. Michel Benard (EdF- France) &

Mr. Didier Beutier (Areva-France)

- Need for New Power

Generating Capacities

- Financial Aspects

- NPP Technologies Available

on the Market

- Regulatory Framework and

Licensing Procedures

- Nuclear Fuel Cycle - Industrial Infrastructure

- Radioactive Waste and

Decommissioning

- Public Acceptance

- Economics of New NPPs - Energy Policy Framework

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 31

Need for New Power Capacity

• Many power plants operating in base load are approaching their end of life (mainly coal fired and nuclear) and will have to be replaced.

• Electricity demand is expected to grow at a rate of

1.5 to 2.0% per year. • IEA (WEO 2004) estimates that more than 1,000 GW

have to be installed in overall Europe between 2000 and 2030 (replacements+increased demand).

• As concerns nuclear energy, available technologies

are known: they are called 3rd generation reactors.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 32

NPP Technologies Available on the Market

The performances with respect to safety and economics are set at a very high level:

- design lifetime: 60 years- availability: better than 90%- fuel cycles: 18 months to two years- very low core damage probability and large off-sites

releases - very low occupational radiation exposure

European Utilities have joined efforts to establish clear general acceptance criteria for new plants.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 33

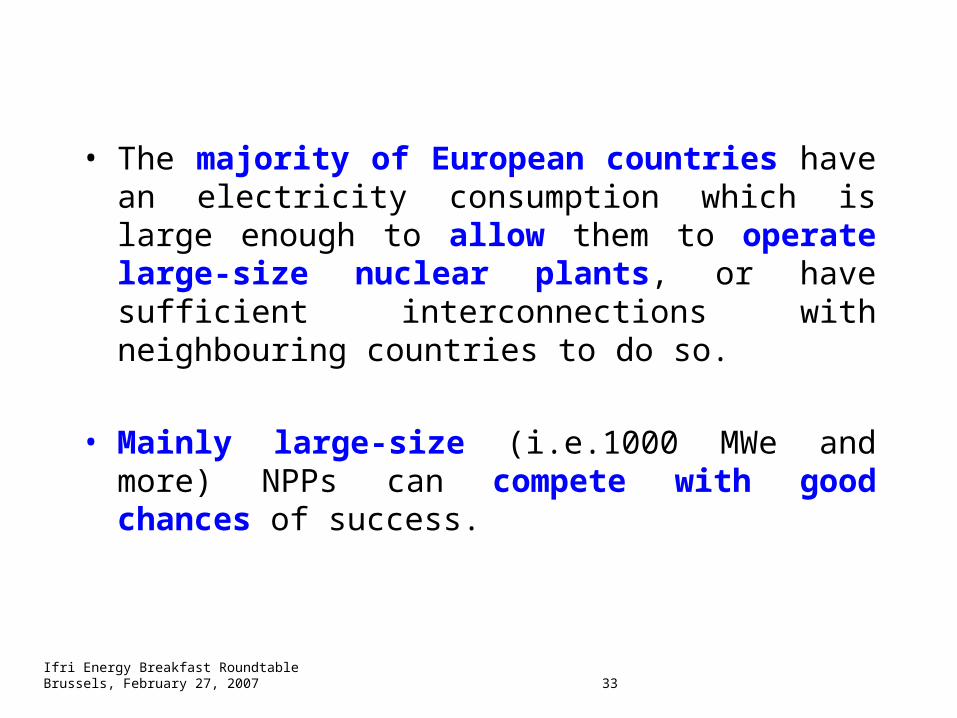

• The majority of European countries have an electricity consumption which is large enough to allow them to operate large-size nuclear plants, or have sufficient interconnections with neighbouring countries to do so.

• Mainly large-size (i.e.1000 MWe and more) NPPs can compete with good chances of success.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 34

The list of reactors under consideration is the following:

• ABWR, ESBWR, both developed by GE, and SWR 1000, developed by Framatome ANP (AREVA). These three models belong to the BWR family, and are large-size reactors as defined above.

• EPR, developed by Framatome ANP (AREVA), AP-1000, developed by Westinghouse, and VVER91, developed by Hidropress. These reactors belong to the PWR family and are also large-size reactors.

• Candu-6, ACR 700 (developed by AECL) which are reactors using heavy water. These two models have a size close to 700 MWe

Beyond 2020, one could also include more innovative and small size reactor types.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 35

Nuclear Fuel Cycle

• The weak step is uranium mining, since domestic uranium resources are scarce. Europe will remain strongly dependent on external sources of uranium, consuming more than 28,000 tons per year, producing less than 5,000 tons per year (Russia, Czech Rep).

• All other operations are mastered on the continent: conversion to fluorides, enrichment, uranium fuel and MOX fuel fabrication, reprocessing.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 36

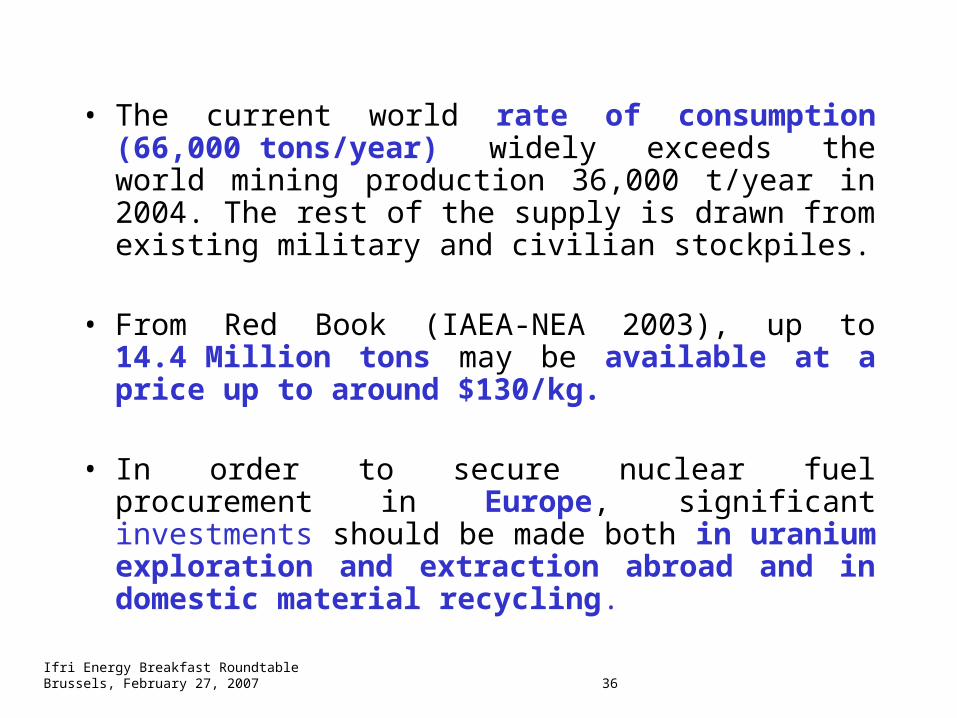

• The current world rate of consumption (66,000 tons/year) widely exceeds the world mining production 36,000 t/year in 2004. The rest of the supply is drawn from existing military and civilian stockpiles.

• From Red Book (IAEA‑NEA 2003), up to 14.4 Million

tons may be available at a price up to around $130/kg.

• In order to secure nuclear fuel procurement in Europe, significant investments should be made both in uranium exploration and extraction abroad and in domestic material recycling.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 37

Radioactive Waste and Decommissioning • Each country is responsible for taking care of its own

waste. • As soon as possible in all involved countries, operational

repositories for the final disposal of short-lived low and intermediate level waste should become standard practice.

• Regulatory framework should be set up. • For high level waste or spent fuel as such, national

programmes should be launched to develop safe technologies.

• Success requires public and political confidence, and real benefits to the local communities hosting repositories.

• For funding of such long term expenses as plant dismantling and high level waste disposal, sufficient amount of money should be put aside each year.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 38

Economics of New Nuclear Power Plants

Main items affecting the total cost of kWh from new NPP’s, compared to alternative energy productions are:

1. Licensing and permits2. Local conditions, taxes and inflation rate3. Investment cost for the specific NPP (overnight cost - OVN)4. Insurance from major accidents5. Operation and Maintenance (O&M)6. Fuel prior to electricity production7. Spent fuel and waste management excluding final disposal8. Decommissioning9. Final waste disposal10. GHG emission penalties / advantages

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 39

• Approaches and values for each cost item are different in different countries.

• The major portion of the cost of the produced kWh is that connected to the investment and it is strongly influenced by:

• plant size and number of units per site• standardization and number of plants ordered• local safety rules and local taxes/costs/conditions• required Return On Investment (IRR)

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 40

• The overnight cost (OVN) of future Generation 3 projects should be lower than the costs recently announced for the two first EPR (FOAK-First Of A Kind Unit). According to vendors’ knowledge, it is likely to stand in the 1200-2000 €/kW range (in Euros 2005), lower values being reached when full benefit can be drawn from series and site effects (for comparison, the OVN cost of 1360 €/kW indicated by France in OECD report was related to a program series of 10 EPR and based on a 2002-2003 study).

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 41

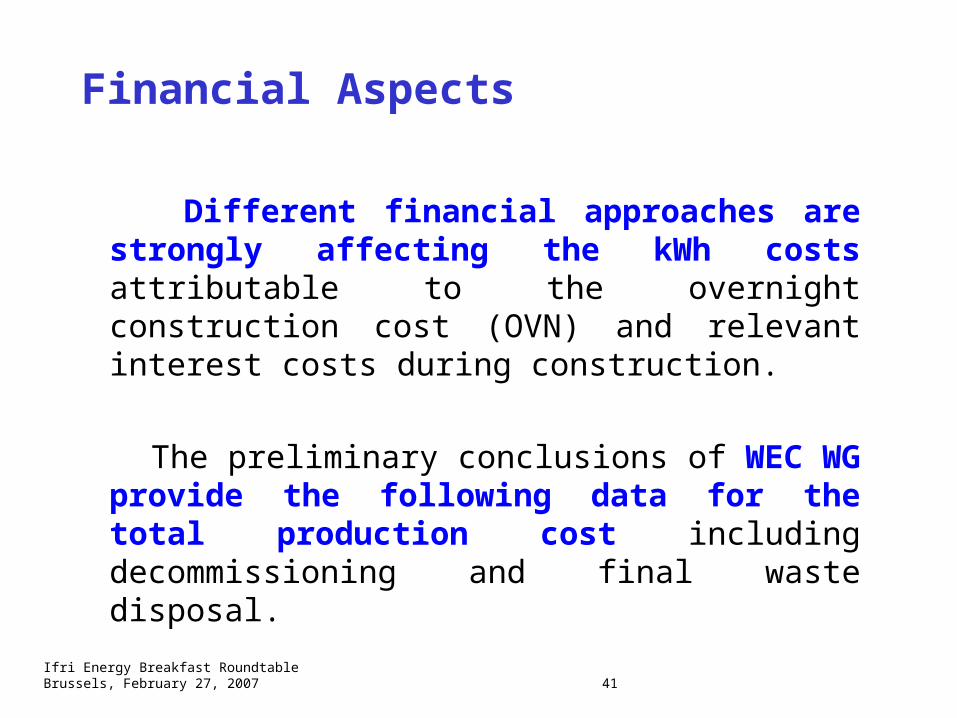

Financial Aspects

Different financial approaches are strongly affecting the kWh costs attributable to the overnight construction cost (OVN) and relevant interest costs during construction.

The preliminary conclusions of WEC WG provide the following data for the total production cost including decommissioning and final waste disposal.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 42

O&M+ fuel+decommissionning Costs

• O&M costs are in the range 6-9 €/MWh (excluding special case local taxes)

• Fuel prior to electricity production is evaluated for the next years at 3.5 - 4.5 €/MWh for Light Water Reactors

• Fuel Cycle back end (Temporary waste management + reprocessing+ final disposal) is considered by new investors 1-4 €/MWh

• For decommissioning, they have deferred costs that do not contribute substantially to the total kWh cost, even if the actual values may be high (e.g. 250-1000$/kW);the range of cost is 0.5-1 € / MWh

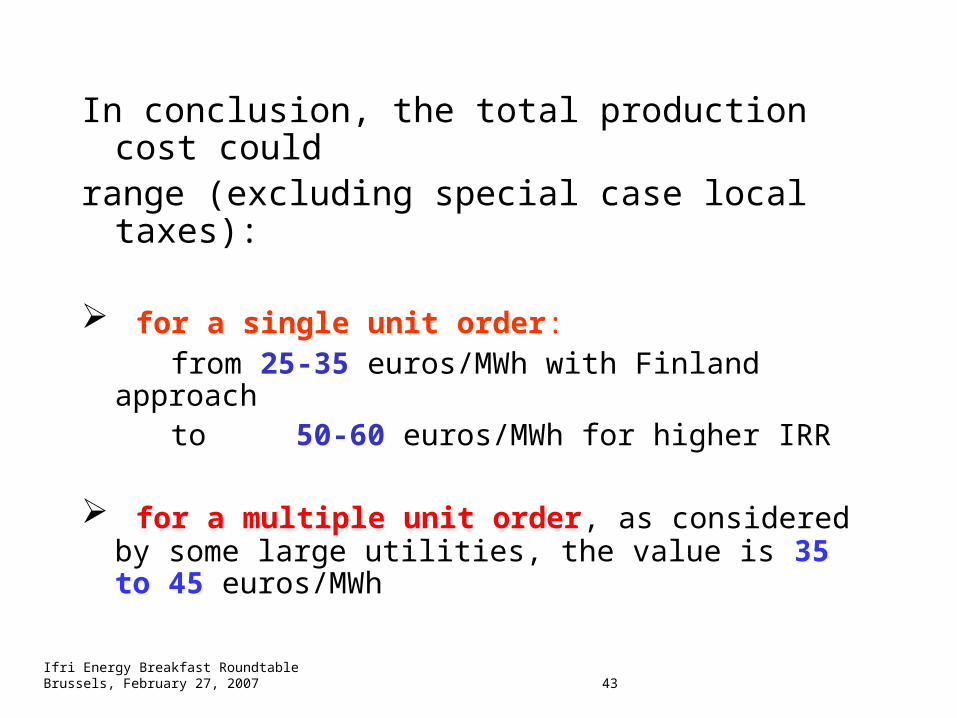

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 43

In conclusion, the total production cost could range (excluding special case local taxes):

for a single unit order: from 25-35 euros/MWh with Finland approach to 50-60 euros/MWh for higher IRR

for a multiple unit order, as considered by some large utilities, the value is 35 to 45 euros/MWh

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 44

With emission trading at 20 €/ton of CO2, the following"advantages" have to be considered for NPP’s withrespect to:

Gas CCGT plant : 6-8 €/MWh

Coal plant : 15-18 €/MWh

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 45

For comparison purposes, the present kWh price offered by an IPP in Italy with a CCGT plant and with a gas cost close to 0.3 euro/m3 is around 70 euro/MWh, not considering the CO2 emission charge of ~ 7 euro/MWh; 80% of the 70 euro are gas cost!

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 46

Apart from the time for licensing, site definition/preparation

and final authorizations, for a new generation 3 plant

from the first concrete poured to commissioning on

the grid (excluding FOAK) total construction time is in the

range of 3.5 to 5 years.

Construction time length

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 47

Public Acceptance Nuclear energy will only develop within the limits of

public acceptance. Since it has been a subject of controversy for a long time, members of nuclear bodies in research, industry and administration are aware they have to respond to social demands, such as:

assurance of no serious accident consequence, protection of facilities against external aggression, transparency and full reporting from operators, established independence of safety authority, coherence with explicit national policy priorities, established waste management policy, public involvement,

in a nutshell, being trustworthy

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 48

3.5. Chapter IV: Nuclear Power with a New Generation Technology (2030-2050)

Coordinator: Mr. Frank Carré (CEA-France)

• Potential for New technologies (Generation IV; fast breeder reactors, etc.)

• R&D for New Technologies of Nuclear Power and Financing: Generation IV International Forum, Contribution of Europe etc.

• Nuclear Fuel Cycle and Non Proliferation Requirements: Utilization of Uranium Resources and Waste Management, etc.

• Means to Implement the Recommended R&D Programme: Competences, Facilities, Budget.

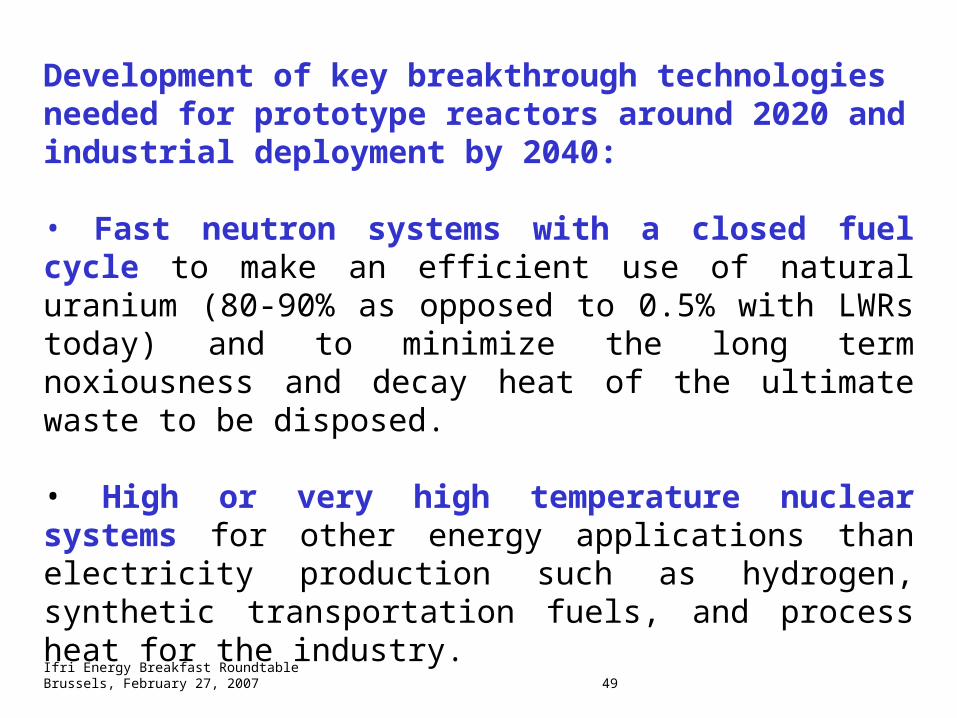

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 49

Development of key breakthrough technologies needed for prototype reactors around 2020 and industrial deployment by 2040:

• Fast neutron systems with a closed fuel cycle to make an efficient use of natural uranium (80-90% as opposed to 0.5% with LWRs today) and to minimize the long term noxiousness and decay heat of the ultimate waste to be disposed.

• High or very high temperature nuclear systems for other energy applications than electricity production such as hydrogen, synthetic transportation fuels, and process heat for the industry.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 50

R&D work on 4th generation systems needs to be complemented by continuing R&D to further optimize 3rd generation reactors that are anticipated to last throughout the 21st century.

R&D on improving the conversion ratio of LWRs is of special interest to provide flexibility while facing rising costs of natural uranium in the 2nd half of the 21st century

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 51

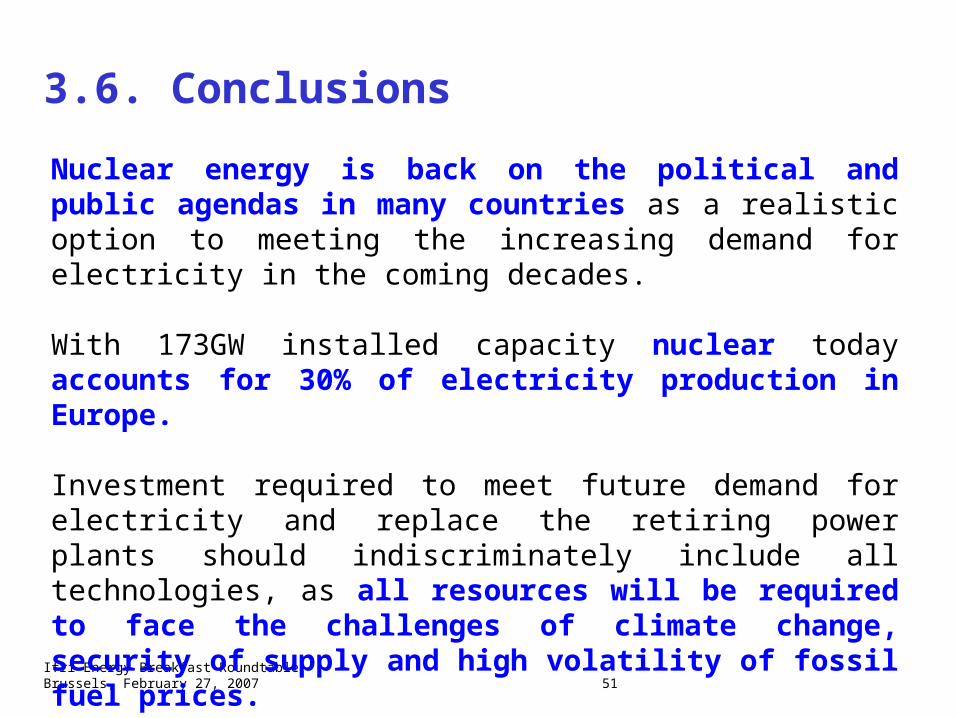

3.6. Conclusions

Nuclear energy is back on the political and public agendas in many countries as a realistic option to meeting the increasing demand for electricity in the coming decades.

With 173GW installed capacity nuclear today accounts for 30% of electricity production in Europe.

Investment required to meet future demand for electricity and replace the retiring power plants should indiscriminately include all technologies, as all resources will be required to face the challenges of climate change, security of supply and high volatility of fossil fuel prices.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 52

The Chernobyl accident (caused by specific design of one particular type of reactor and inadequate operational practices) strongly dented the safety record of nuclear power generation and led to a nuclear slowdown in Europe for 20 years.

Since then the European operators together with the nuclear safety authorities have enhanced the safety standards and all European plants demonstrate excellent performance.

The prevailing public concerns, where nuclear waste management has overtaken safety, are adequately addressed in the legislation. At the same time, public information campaigns, transparency of the institutions and debate on nuclear issues have led to the majority of public opinion supporting nuclear energy in some countries.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 53

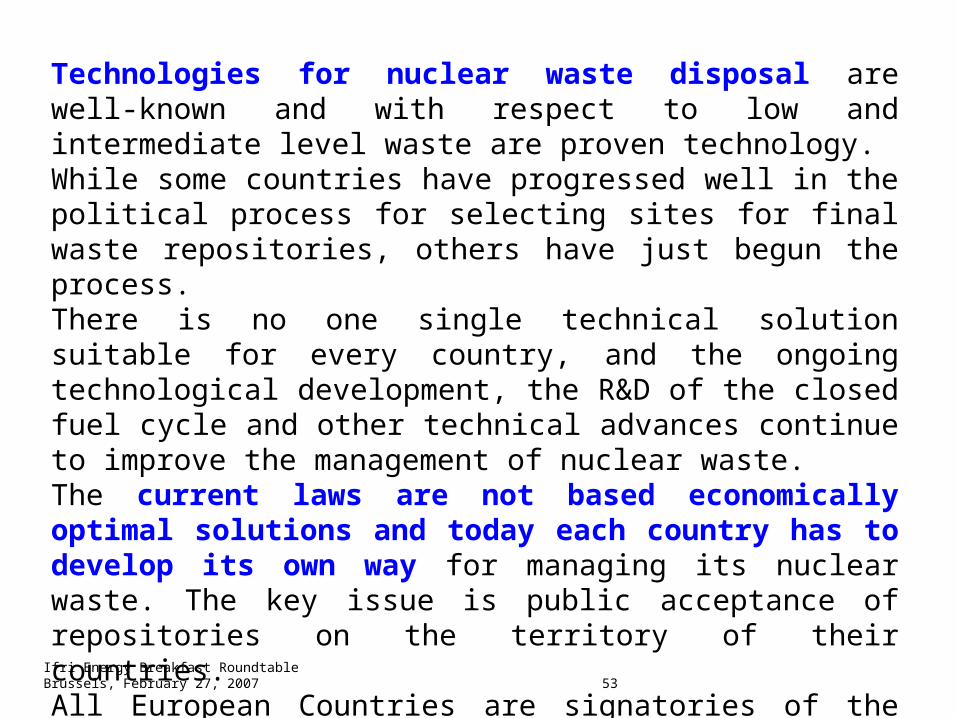

Technologies for nuclear waste disposal are well-known and with respect to low and intermediate level waste are proven technology. While some countries have progressed well in the political process for selecting sites for final waste repositories, others have just begun the process. There is no one single technical solution suitable for every country, and the ongoing technological development, the R&D of the closed fuel cycle and other technical advances continue to improve the management of nuclear waste. The current laws are not based economically optimal solutions and today each country has to develop its own way for managing its nuclear waste. The key issue is public acceptance of repositories on the territory of their countries.All European Countries are signatories of the NPT and additional protocols under IAEA in Vienna.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 54

Already now decommissioning is included in the full operational cycle and has an impact on waste management which depends on the size and the number of reactors.

The average cost of decommissioning is around 300 euros/kWe, except for gas-cooled reactors.

Almost all nuclear operators in Europe have allocated sufficient funds to cover future decommissioning costs, and for the remainder national authorities are taking care of decommissioning costs.

The decommissioning costs for new plants which will operate 60 years or more is between 0.5 - 1.0 euro/MWh.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 55

For the existing fleet the total cost is below 20 euros/MWh, given that almost all plants have already been fully depreciated. The good record of economic and technical performance allows both the service life extension and capacity increases of existing plants.

For the Europe 25 only, continuing the operation of the existing fleet beyond the initially defined service life, could help avoid 700 million tons of CO2 emissions or around 15-20% of the total annual emissions in EU. This offers the end customer a stable and easily predictable impact on the kWh price.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 56

The technology for new NPPs is already available, and is being implemented in the projects under construction in Finland, France, Japan, Romania, Taiwan, etc.

The reactors on today’s market have an overnight cost in the range of 1300-1800 euros/kW depending inter alia on the size and number of units per plant and the economies of serial production.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 57

The final costs of kWh depend on local legislation and taxes, which impact the discount rate, given that NPPs are highly capital intensive. Assuming a stable political environment, clear regulatory frameworks governing the site location, decommissioning regulations and other aspects, these costs can reach 40 euros/MWh. However, under specific circumstances they can be considerably lower (around 30 euros/MWh) or higher (up to 55 euros/MWh). These estimates also include future expenses associated with decommissioning and waste disposal. The uncertainty about these figures will not have a significant affect on the total kWh cost). Even without a CO2 penalty for fossil fuels, nuclear energy is an economically attractive option.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 58

Today nuclear is an integral part of the European energy scene. Tomorrow success will be defined by the following key conditions:

• Stability, consistency and predictability of market rules to ensure investor friendly environment

• Independence and transparency of safety regulations

• Agreement on a common technically feasible, economically efficient and publicly acceptable framework for waste disposal

• Simple and rapid process for granting construction and operational licences

• Standardisation and scale effects for reactor manufacturers

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 59

• Support for nuclear R&D, and in particular for Generation 4 technologies, which are expected to become available on the market around 2030-2040 and bring about a dramatic increase of uranium utilisation by nearly 80 times; this to secure sustainable generation of electricity in a possible context of rising uranium prices and also to co-generate by-products such as hydrogen, synthetic hydrocarbon fuels and high temperature process heat for other industrial applications

• Active involvement of all stakeholders in the consultation and implementation processes

• Equitable distribution of risks and rewards between all involved.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 60

European countries, and the European Union member states in particular, must seriously consider including nuclear option in their energy policies. This also includes improving public awareness about the energy issues, providing factual information and conducting comprehensive and efficient communication campaigns.

The European members of the World Energy Council (WEC) are ready and willing to work together with all stakeholders to ensure a facts-based, balanced and unbiased approach to assessment of nuclear option as a part of WEC’s strategy of keeping all energy sources open.

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 61

4. Next Steps

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 62

Next steps

• Presentation of the study report to EU and to other institutions

• Series of events in the various countries to be organized by the local National WEC Committees

Ifri Energy Breakfast RoundtableBrussels, February 27, 2007 63

Thanks for your attention