ifrs 9 - impairments, time to get ready for the new standard

TRANSCRIPT

IFRS 9 -Impairments Time to Get Ready for The New Standard

Eric de WeerdtDirector AuditDeloitte Financial Services

Global Association of Risk ProfessionalsMay 2016

2

The views expressed in the following material are the

author’s and do not necessarily represent the views of

the Global Association of Risk Professionals (GARP),

its Membership or its Management.

IFRS 9: Financial Instruments

The auditor perspective

May 2016

1 © 2015 For information contact Deloitte Touche Tohmatsu Limited.

IFRS 9 from an auditor perspective

• Audit approach and strategy:

First time adoption versus change in accounting policy approach

Team structure (expertise within the team; use of experts (IT/Modelling)

Control reliance?

• Identifying Significant Risks at assertion level

Ability to make use of a robust process applied by client?

Auditing accounting estimates

Identify controls and test of controls (D&I; OE)

Information used in a control (IPE)

Test of details

• Accounting considerations

Sufficiency of disclosures

Transition requirements

• Stakeholder management and communication

Communication with Those Charged with Governance

Communication with regulators and consistency with regulatory reporting

© 2016 Deloitte The Netherlands2

Sixth Global IFRS 9 banking Survey – key findings

© 2016 Deloitte The Netherlands3

Sixth Global IFRS 9 banking Survey – Change programme

© 2016 Deloitte The Netherlands4

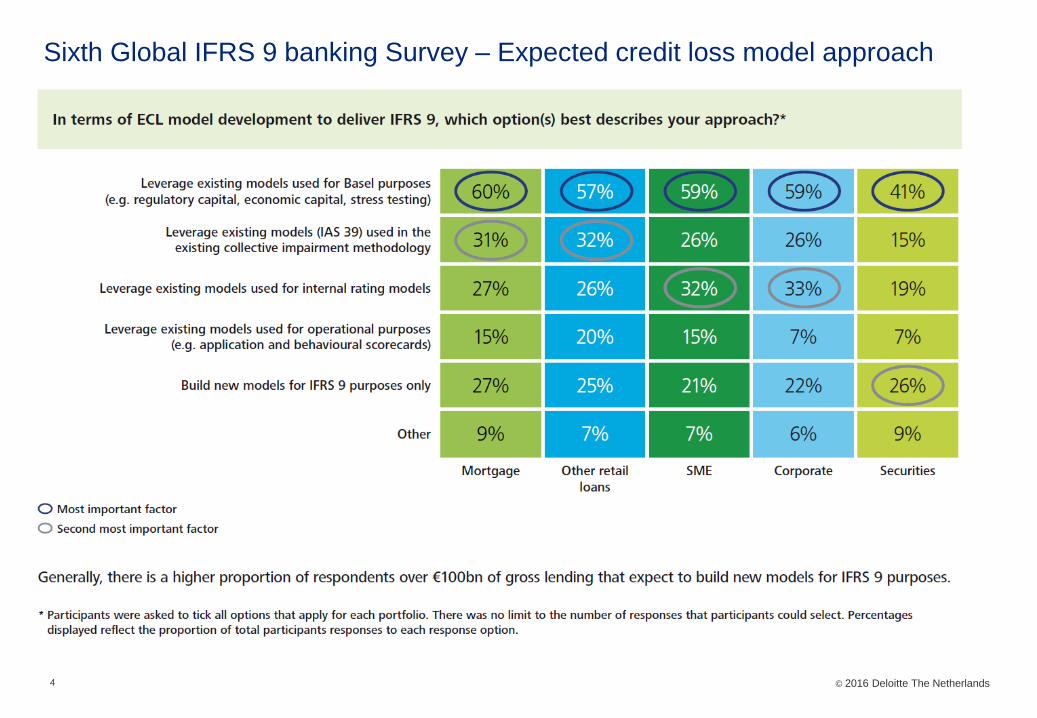

Sixth Global IFRS 9 banking Survey – Expected credit loss model approach

© 2016 Deloitte The Netherlands5

Sixth Global IFRS 9 banking Survey – Expected credit loss model approach

© 2016 Deloitte The Netherlands6

Sixth Global IFRS 9 banking Survey – Expected credit loss model approach

© 2016 Deloitte The Netherlands7

Sixth Global IFRS 9 banking Survey – Forward-looking macroeconomic info

© 2016 Deloitte The Netherlands8

Sixth Global IFRS 9 banking Survey – Significant increase in credit risk

© 2016 Deloitte The Netherlands9

Sixth Global IFRS 9 banking Survey – Definition of default

© 2016 Deloitte The Netherlands10

Sixth Global IFRS 9 banking Survey – Practical expedients/rebuttable presumptions

© 2016 Deloitte The Netherlands11

Sixth Global IFRS 9 banking Survey – Data quality

© 2016 Deloitte The Netherlands

IFRS 9 implementation timeline, stakeholders and hot topics

Auditor focus on stakeholders influence, management estimates, consistency

(internal and industry) and reliability of source info used

12

IFRS 9 International stakeholders Hot topics

Forward-looking economic information

(estimates)

Experienced credit judgement process (controls)

Definition of default (accounting policy)

Behavioural vs contractual life (judgment)

Comparatives, transition requirements

(accounting)

Disclosures (accounting)

Significant increase in credit risk and stage

allocation (judgment)

ECL modelling approach (use of experts)

IASB, ITG and

IFRIC

Large audit

firms

National

competent

authorities

(NCAs)

Enhanced

Disclosures

Task Force

(EDTF)

IFRS 9

European

Banking

Authority (EBA)

and European

Central Bank

(ECB)

Financial

Accounting

Standards

Board

(FASB)

Basel

Committee on

Banking

Supervision

(BCBS)

2014 2015 2016 2017 2018

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Study Design Build Parallel Run Live Run

Availability of data and reliability thereof (IT

audit)

13 © 2015 For information contact Deloitte Touche Tohmatsu Limited.

Auditing of management estimates is arranged in ISA 540: AUDITING ACCOUNTING ESTIMATES, INCLUDING FAIR VALUE

ACCOUNTING ESTIMATES, AND RELATED DISCLOSURES and for example includes a critical approach on management

bias, assess potential alternative outcomes and analyse whether the significant assumptions used by management are

reasonable.

Common pitfalls in auditing loans loss provisions in general:

• External factors (economic, industry or regulatory) are inconsistently applied

• Failure to adequately test subjective assumptions or factors used by management

• Failure to perform a retrospective review to assess if management has demonstrated proficiency in determining the

estimate for loan losses

• Failure to adequately test internal controls that mitigate the identified risks

• Failure to document enough information about the procedures performed and professional judgments made to enable an

experienced auditor, having no previous experience with the engagement, to understand the nature, timing and extent of the

procedures performed, the evidence obtained and the conclusions reached

Framework for Auditing Accounting Estimates

Identify Accounting Estimates

Understand How Management Makes

the Accounting Estimate

Identify and Assess Risks of Material

Misstatement for the Accounting Estimate

Respond to Risks of Material Misstatement

- Perform Tests of Controls

Respond to Risks of Material Misstatement - Perform Substantive

Procedures

Evaluate Audit Evidence Obtained for the Accounting

Estimate

Auditor testing of management estimates remains a major source of inspection findings, primarily

from failing to evaluate management’s assumptions or challenge management’s explanations for

reasonableness and failing to test underlying data used in developing estimates

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their

related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide

services to clients. Please see www.deloitte.nl/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, consulting, financial advisory, risk management, tax and related services to public and private clients spanning multiple industries. With a

globally connected network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients,

delivering the insights they need to address their most complex business challenges. Deloitte’s more than 210,000 professiona ls are committed to becoming the

standard of excellence.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the

“Deloitte network”) is, by means of this communication, rendering professional advice or services. No entity in the Deloitte network shall be responsible for any loss

whatsoever sustained by any person who relies on this communication.

14© 2015 Deloitte

C r e a t i n g a c u l t u r e o fr i s k a w a r e n e s s ®

Global Association ofRisk Professionals

111 Town Square Place14th FloorJersey City, New Jersey 07310U.S.A.+ 1 201.719.7210

2nd FloorBengal Wing9A Devonshire SquareLondon, EC2M 4YNU.K.+ 44 (0) 20 7397 9630

www.garp.org

About GARP | The Global Association of Risk Professionals (GARP) is a not-for-profit global membership organization dedicated to preparing professionals and organizations to make better informed risk decisions. Membership represents over 150,000 risk management practitioners and researchers from banks, investment management firms, government agencies, academic institutions, and corporations from more than 195 countries and territories. GARP administers the Financial Risk Manager (FRM®) and the Energy Risk Professional (ERP®) Exams; certifications recognized by risk professionals worldwide. GARP also helps advance the role of risk management via comprehensive professional education and training for professionals of all levels. www.garp.org.

4 | © 2014 Global Association of Risk Professionals. All rights reserved.