impact of repo rate and reverse repo rate on bank niftyadalyajournal.com/gallery/84-nov-2330.pdf ·...

TRANSCRIPT

Impact of Repo Rate and Reverse repo rate on Bank Nifty

Dr E.M. Naresh Babu

Associate Professor,

ABBS School of Management

Bengaluru-560091

----------------------------------------------------------------------------------------------------------------

Abstract

Banking sector is considered to be one of the most promising sectors for investment in

India. Bank Nifty is an index comprising 12 leading bank stocks in India. The

announcement of Repo, Reverse Repo rates by RBI will influence the banking sector, when

there is an increase in Repo rate, it becomes burden to the banks as the banks have to pay

higher rate for the funds which they have taken from the RBI. This will impact not only the

banks but also the Bank Nifty, similarly there will be a change in the Bank Nifty whenever

there is a change in the Reverse Repo Rate also. The present study focuses on the impact of

Bank Nifty when there is a change in Repo and Reverse Repo Rate for the period from 2005

to 2019 August. The results found were, Repo Rate increasing is more impacting Bank Nifty

in terms of returns Variance.

Key Words: Bank Nifty, Repo Rate, Reverse Repo Rate, Variance

----------------------------------------------------------------------------------------------------------------

Introduction

India is one of the emerging economies and lot of sectors are contributing to the

economy. The GDP is dominated by the service sector after the LPG. Banking sector is

considered as one of the growing sectors since 1991. Bank Nifty is the index which gives a

brief idea about the major banking stocks in India. Index calculation has been started since

2001 and the base value is taken as value from 2000. The index is influenced by the stocks

movement in the index and which are dependent on the RBIs announcement of policy rates.

Many investors believe that banking stocks will be influenced by Repo and Reverse Repo

rates. The policy rates will influence the money flow in the economy.

Literature review

The Stock market is considered to be the most representative indicator of economy of

any country. For smooth functioning of economy, the central monetary authority plays a vital

role. The central monetary authority uses monetary policy to control the money supply in the

country. There is a insignificant relationship between macro economic variables and Nifty.

The Nifty performance is not affected by the changes in the macro economic policies such as

CRR and Reverse Repo Rate. (Kumari & Nagendra, 2019)

Central bank controls supply of money with the help of monetary policy. The announcement

of CRR, SLR, PLR and Repo rate not only influences the money flow in the country but also

ADALYA JOURNAL

Volome 8, Issue 11, November 2019 932

ISSN NO: 1301-2746

http://adalyajournal.com/

the banking stocks listed in National Stock Exchange. It is found that announcement of

changes in Reverse Repo Rate and Cash Reserve Ratio are impacting the baking stocks.

Reverse Repo Rate has given a positive impact on CAAR(Cumulative Abnormal Average

Returns) where as Cash Reserve Ratio change has given a negative CAAR.. It is also

observed that Reverse Repo Rate is more influential than Repo Rate (Vanitha et al, 2013)

RBIs monetary policy announcements have been identified to be influencing the

Indian Stock Market Efficiency. Nifty values have been observed for a period of 31 days i.e.

15 days prior to the announcement and 15 days after the announcement of monetary policy

decision. Certain variables like Average Return, Average Abnormal Return and Cumulative

Average Abnormal Return were observed with Single Index Model and found to be

impacting Nifty returns. Certain announcement have not shown immediate impact on the day

of announcement as it is been in the discussion in market for some period, but on a whole, the

Monetary policy announcements have got an impact on stock market but not efficient in semi

strong form. (Agarwal, 2007)

Research Methodology

Need for the study

Many of the investors feel that there will be a difference in the Bank Nifty returns

when there is a change in the Repo and Reverse Repo rates change announcement by RBI.

So there is a dire need for identifying whether there will be a huge difference in the Bank

Nifty in the short run and long run when there is a rate change announcement by RBI.

Scope of the study

The present study focuses on the aspects of Repo Rate and Reverse Repo rates

changes and its’ impact on Bank Nifty. The period of data analysis is from Jan 2005 to

August 2019 For the present study the data of Bank Nifty values has been gathered from

National Stock Exchange Official website and Repo and Reverse Repo rates have been

gathered from official website of Reserve Bank of India.

Objectives of the study :

To analyze the effect of announcement of Repo Rate changes on Bank Nifty

To analyze the effect of announcement of Reverse Repo Rate changes on Bank Nifty

To compare the volatility in variance of returns in the Bank Nifty for 3 days, 6 days

and 9 days when there is a change in Repo rate (Pre and Post)

To compare the volatility in variance of returns in the Bank Nifty for 3 days, 6 days

and 9 days when there is a change in Reverse Repo rate (Pre and Post)

Limitations of the study

The study considers Repo rate and Reverse Repo rate announcements of RBI and the

other macro-economic, political, economical social factors are not considered.

ADALYA JOURNAL

Volome 8, Issue 11, November 2019 933

ISSN NO: 1301-2746

http://adalyajournal.com/

Analysis and Discussion

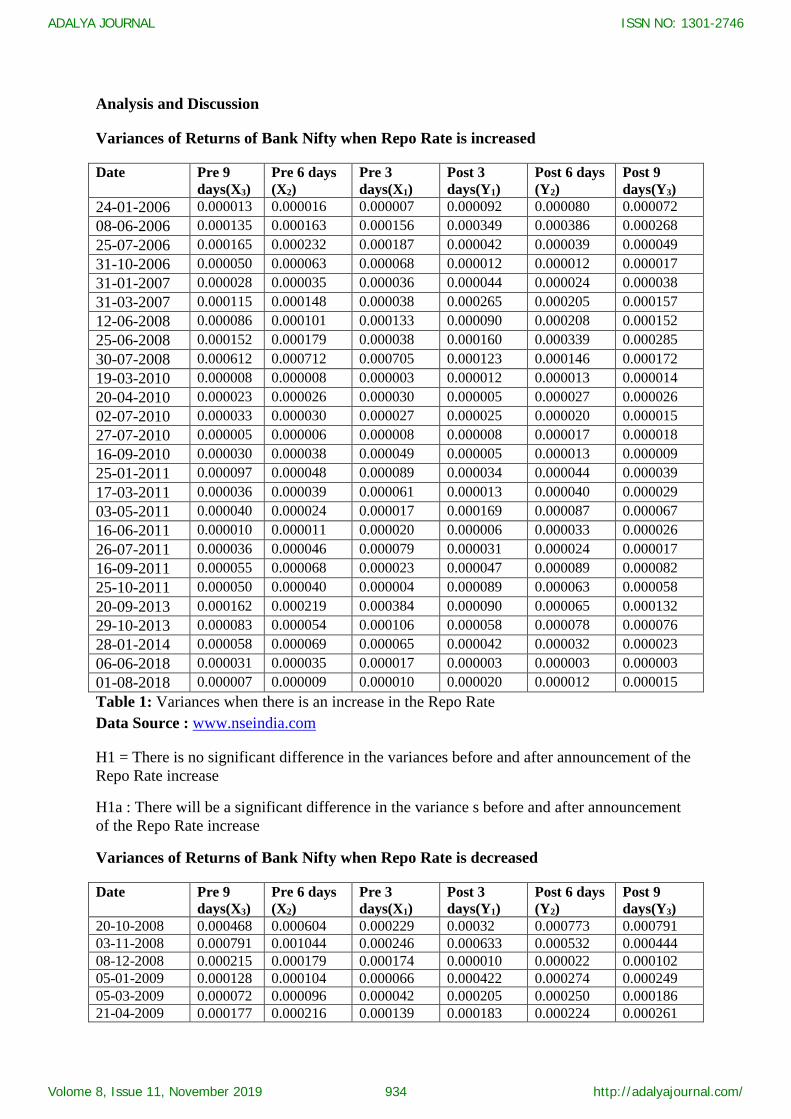

Variances of Returns of Bank Nifty when Repo Rate is increased

Date Pre 9

days(X3)

Pre 6 days

(X2)

Pre 3

days(X1)

Post 3

days(Y1)

Post 6 days

(Y2)

Post 9

days(Y3)

24-01-2006 0.000013 0.000016 0.000007 0.000092 0.000080 0.000072

08-06-2006 0.000135 0.000163 0.000156 0.000349 0.000386 0.000268

25-07-2006 0.000165 0.000232 0.000187 0.000042 0.000039 0.000049

31-10-2006 0.000050 0.000063 0.000068 0.000012 0.000012 0.000017

31-01-2007 0.000028 0.000035 0.000036 0.000044 0.000024 0.000038

31-03-2007 0.000115 0.000148 0.000038 0.000265 0.000205 0.000157

12-06-2008 0.000086 0.000101 0.000133 0.000090 0.000208 0.000152

25-06-2008 0.000152 0.000179 0.000038 0.000160 0.000339 0.000285

30-07-2008 0.000612 0.000712 0.000705 0.000123 0.000146 0.000172

19-03-2010 0.000008 0.000008 0.000003 0.000012 0.000013 0.000014

20-04-2010 0.000023 0.000026 0.000030 0.000005 0.000027 0.000026

02-07-2010 0.000033 0.000030 0.000027 0.000025 0.000020 0.000015

27-07-2010 0.000005 0.000006 0.000008 0.000008 0.000017 0.000018

16-09-2010 0.000030 0.000038 0.000049 0.000005 0.000013 0.000009

25-01-2011 0.000097 0.000048 0.000089 0.000034 0.000044 0.000039

17-03-2011 0.000036 0.000039 0.000061 0.000013 0.000040 0.000029

03-05-2011 0.000040 0.000024 0.000017 0.000169 0.000087 0.000067

16-06-2011 0.000010 0.000011 0.000020 0.000006 0.000033 0.000026

26-07-2011 0.000036 0.000046 0.000079 0.000031 0.000024 0.000017

16-09-2011 0.000055 0.000068 0.000023 0.000047 0.000089 0.000082

25-10-2011 0.000050 0.000040 0.000004 0.000089 0.000063 0.000058

20-09-2013 0.000162 0.000219 0.000384 0.000090 0.000065 0.000132

29-10-2013 0.000083 0.000054 0.000106 0.000058 0.000078 0.000076

28-01-2014 0.000058 0.000069 0.000065 0.000042 0.000032 0.000023

06-06-2018 0.000031 0.000035 0.000017 0.000003 0.000003 0.000003

01-08-2018 0.000007 0.000009 0.000010 0.000020 0.000012 0.000015

Table 1: Variances when there is an increase in the Repo Rate

Data Source : www.nseindia.com

H1 = There is no significant difference in the variances before and after announcement of the

Repo Rate increase

H1a : There will be a significant difference in the variance s before and after announcement

of the Repo Rate increase

Variances of Returns of Bank Nifty when Repo Rate is decreased

Date Pre 9

days(X3)

Pre 6 days

(X2)

Pre 3

days(X1)

Post 3

days(Y1)

Post 6 days

(Y2)

Post 9

days(Y3)

20-10-2008 0.000468 0.000604 0.000229 0.00032 0.000773 0.000791 03-11-2008 0.000791 0.001044 0.000246 0.000633 0.000532 0.000444 08-12-2008 0.000215 0.000179 0.000174 0.000010 0.000022 0.000102 05-01-2009 0.000128 0.000104 0.000066 0.000422 0.000274 0.000249 05-03-2009 0.000072 0.000096 0.000042 0.000205 0.000250 0.000186 21-04-2009 0.000177 0.000216 0.000139 0.000183 0.000224 0.000261

ADALYA JOURNAL

Volome 8, Issue 11, November 2019 934

ISSN NO: 1301-2746

http://adalyajournal.com/

17-04-2012 0.000027 0.000033 0.000026 0.000013 0.000018 0.000014 29-01-2013 0.000012 0.000009 0.000013 0.000005 0.000003 0.000003 19-03-2013 0.000060 0.000044 0.000058 0.000070 0.000046 0.000035 03-05-2013 0.000049 0.000039 0.000050 0.000062 0.000036 0.000060 15-01-2015 0.000062 0.000047 0.000062 0.000039 0.000025 0.000026 04-03-2015 0.000054 0.000072 0.000083 0.000046 0.000035 0.000035 02-06-2015 0.000036 0.000049 0.000079 0.000041 0.000043 0.000042 29-09-2015 0.000050 0.000059 0.000017 0.000049 0.000033 0.000023 05-04-2016 0.000052 0.000068 0.000049 0.000041 0.000060 0.000046 04-10-2016 0.000031 0.000037 0.000055 0.000006 0.000016 0.000024 02-08-2017 0.000005 0.000007 0.000010 0.000017 0.000012 0.000017 07-02-2019 0.000017 0.000012 0.000001 0.000002 0.000001 0.000005 04-04-2019 0.000019 0.000021 0.000003 0.000014 0.000011 0.000014 06-06-2019 0.000035 0.000023 0.000034 0.000039 0.000023 0.000018 07-08-2019 0.000027 0.000029 0.000038 0.000068 0.000039 0.000040

Table 2: Variances when there is a decrease in the Repo Rate

Data Source : www.nseindia.com

H2 = There is no significant difference in the variances before and after announcement of the

Repo Rate decrease

H2a : There will be a significant difference in the variance s before and after announcement

of the Repo Rate decrease

Variances of Returns of Bank Nifty when Reverse Repo Rate is increased

Date Pre 9

days(X3)

Pre 6 days

(X2)

Pre 3

days(X1)

Post 3

days(Y1)

Post 6 days

(Y2)

Post 9

days(Y3)

24-01-2006 0.000013 0.000016 0.000007 0.000092 0.000080 0.000072 08-06-2006 0.000135 0.000163 0.000156 0.000349 0.000386 0.000268 25-07-2006 0.000165 0.000232 0.000187 0.000042 0.000039 0.000049 19-03-2010 0.000008 0.000008 0.000003 0.000012 0.000013 0.000014 20-04-2010 0.000023 0.000026 0.000030 0.000005 0.000027 0.000026 02-07-2010 0.000033 0.000030 0.000027 0.000025 0.000020 0.000015 27-07-2010 0.000005 0.000006 0.000008 0.000008 0.000017 0.000018 16-09-2010 0.000030 0.000038 0.000049 0.000005 0.000013 0.000009 25-01-2011 0.000097 0.000048 0.000089 0.000034 0.000044 0.000039 17-03-2011 0.000036 0.000039 0.000061 0.000013 0.000040 0.000029 03-05-2011 0.000040 0.000024 0.000017 0.000169 0.000087 0.000067 16-06-2011 0.000010 0.000011 0.000020 0.000006 0.000033 0.000026 26-07-2011 0.000036 0.000046 0.000079 0.000031 0.000024 0.000017 16-09-2011 0.000055 0.000068 0.000023 0.000047 0.000089 0.000082 25-10-2011 0.000050 0.000040 0.000004 0.000089 0.000063 0.000058 20-09-2013 0.000162 0.000219 0.000384 0.000090 0.000065 0.000132 29-10-2013 0.000083 0.000054 0.000106 0.000058 0.000078 0.000076 28-01-2014 0.000058 0.000069 0.000065 0.000042 0.000032 0.000023 05-04-2016 0.000052 0.000068 0.000049 0.000041 0.000060 0.000046 06-04-2017 0.000007 0.000008 0.000007 0.000012 0.000007 0.000005 06-06-2018 0.000031 0.000035 0.000017 0.000003 0.000003 0.000003 01-08-2018 0.000007 0.000009 0.000010 0.000020 0.000012 0.000015

Table 3: Variances when there is an increase in the Reverse Repo Rate

Data Source : www.nseindia.com

ADALYA JOURNAL

Volome 8, Issue 11, November 2019 935

ISSN NO: 1301-2746

http://adalyajournal.com/

H3 = There is no significant difference in the variances before and after announcement of the

Reverse Repo Rate increase

H3a : There will be a significant difference in the variance s before and after announcement

of the Reverse Repo Rate increase

Variances of Returns of Bank Nifty when Reverse Repo Rate is decreased

Date Pre 9

days(X3)

Pre 6 days

(X2)

Pre 3

days(X1)

Post 3

days(Y1)

Post 6 days

(Y2)

Post 9

days(Y3)

29-10-2005 0.000046 0.000048 0.000054 0.000203 0.000108 0.000076

08-12-2008 0.000215 0.000179 0.000174 0.000010 0.000022 0.000102

05-01-2009 0.000128 0.000104 0.000066 0.000422 0.000274 0.000249

05-03-2009 0.000072 0.000096 0.000042 0.000205 0.000250 0.000186

21-04-2009 0.000177 0.000216 0.000139 0.000183 0.000224 0.000261

17-04-2012 0.000027 0.000033 0.000026 0.000013 0.000018 0.000014

29-01-2013 0.000012 0.000009 0.000013 0.000005 0.000003 0.000003

19-03-2013 0.000060 0.000044 0.000058 0.000070 0.000046 0.000035

03-05-2013 0.000049 0.000039 0.000050 0.000062 0.000036 0.000060

15-01-2015 0.000062 0.000047 0.000062 0.000039 0.000025 0.000026

04-03-2015 0.000054 0.000072 0.000083 0.000046 0.000035 0.000035

02-06-2015 0.000036 0.000049 0.000079 0.000041 0.000043 0.000042

29-09-2015 0.000050 0.000059 0.000017 0.000049 0.000033 0.000023

04-10-2016 0.000031 0.000037 0.000055 0.000006 0.000016 0.000024

02-08-2017 0.000005 0.000007 0.000010 0.000017 0.000012 0.000017

07-02-2019 0.000017 0.000012 0.000001 0.000002 0.000001 0.000005

04-04-2019 0.000019 0.000021 0.000003 0.000014 0.000011 0.000014

06-06-2019 0.000035 0.000023 0.000034 0.000039 0.000023 0.000018

07-08-2019 0.000027 0.000029 0.000038 0.000068 0.000039 0.000040

Table 4: Variances when there is a decrease in Reverse Repo Rate

Data Source : www.nseindia.com

H4 = There is no significant difference in the variances before and after announcement of the

Reverse Repo Rate decrease

H4a : There will be a significant difference in the variance s before and after announcement

of the Reverse Repo Rate decrease

F test results of comparing variances when Repo Rate is increased

F Value F Critical P value

X1 and Y1 1.624902 1.955447 0.115891

Y2 and Y1 0.791541 0.511392 0.281642

Y2 and Y3 1.06714 1.955447 0.436116

Y3 and Y1 1.34818 1.955447 0.230226

X3 and Y1 0.934045 0.511392 0.432952

X3 and Y2 0.739335 0.511392 0.227803

X3 and Y3 0.692819 0.511392 0.182512

Table 5 : F test results of comparison of variances when Repo rate is increased

ADALYA JOURNAL

Volome 8, Issue 11, November 2019 936

ISSN NO: 1301-2746

http://adalyajournal.com/

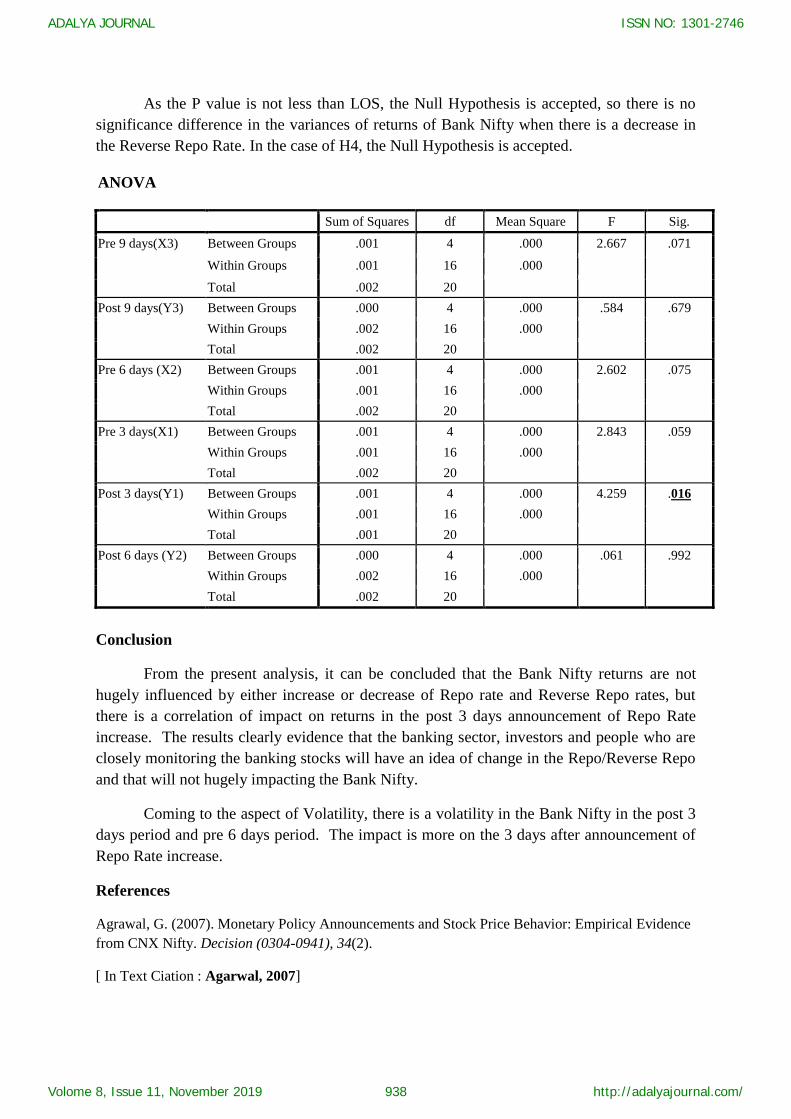

As the P value is not less than LOS, the Null Hypothesis is accepted, so there is no

significance difference in the variances of returns of Bank Nifty when there is a decrease in

the Reverse Repo Rate. In the case of H1, the Null Hypothesis is accepted.

F test results of comparing variances when Repo Rate is decreased

F Value F Critical P value

X1 and Y1 1.426819 2.124155 0.21684

Y2 and Y1 1.523929 2.124155 0.176969

Y2 and Y3 0.933567 0.470775 0.439677

Y3 and Y1 0.612606 0.470775 0.140769

X3 and Y1 0.788792 0.470775 0.300375

X3 and Y2 1.202063 2.124155 0.342323

X3 and Y3 1.287601 2.124155 0.288598

Table 6 : F test results of comparison of variances when Repo rate is decreased

As the P value is not less than LOS, the Null Hypothesis is accepted, so there is no

significance difference in the variances of returns of Bank Nifty when there is a decrease in

the Repo Rate. In the case of H2, the Null Hypothesis is accepted

F test results of comparing variances when Reverse Repo Rate is increased

F Value F Critical P value

X1 and Y1 1.478497 2.084189 0.188728

Y2 and Y1 0.835193 0.479803 0.341824

Y2 and Y3 0.955595 0.479803 0.459046

Y3 and Y1 1.144161 2.084189 0.380256

X3 and Y1 0.908376 0.479803 0.413894

X3 and Y2 0.758669 0.479803 0.266194

X3 and Y3 0.793924 0.479803 0.300859

Table 7 : F test results of comparison of variances when Reverse Repo rate is increased

As the P value is not less than LOS, the Null Hypothesis is accepted, so there is no

significance difference in the variances of returns of Bank Nifty when there is an increase in

the Reverse Repo Rate. In the case of H3, the Null Hypothesis is accepted

F test results of comparing variances when Reverse Repo Rate is decreased

F Value F Critical P value

X1 and Y1 1.248508 2.217197 0.321372

Y2 and Y1 0.664172 0.45102 0.196777

Y2 and Y3 0.880052 0.45102 0.394649

Y3 and Y1 1.325037 2.217197 0.27832

X3 and Y1 0.758313 0.45102 0.28167

X3 and Y2 0.50365 0.45102 0.077601

X3 and Y3 0.572296 0.45102 0.122974

Table 8 : F test results of comparison of variances when Reverse Repo rate is decreased

ADALYA JOURNAL

Volome 8, Issue 11, November 2019 937

ISSN NO: 1301-2746

http://adalyajournal.com/

As the P value is not less than LOS, the Null Hypothesis is accepted, so there is no

significance difference in the variances of returns of Bank Nifty when there is a decrease in

the Reverse Repo Rate. In the case of H4, the Null Hypothesis is accepted.

ANOVA

Sum of Squares df Mean Square F Sig.

Pre 9 days(X3) Between Groups .001 4 .000 2.667 .071

Within Groups .001 16 .000

Total .002 20

Post 9 days(Y3) Between Groups .000 4 .000 .584 .679

Within Groups .002 16 .000

Total .002 20

Pre 6 days (X2) Between Groups .001 4 .000 2.602 .075

Within Groups .001 16 .000

Total .002 20

Pre 3 days(X1) Between Groups .001 4 .000 2.843 .059

Within Groups .001 16 .000

Total .002 20

Post 3 days(Y1) Between Groups .001 4 .000 4.259 .016

Within Groups .001 16 .000

Total .001 20

Post 6 days (Y2) Between Groups .000 4 .000 .061 .992

Within Groups .002 16 .000

Total .002 20

Conclusion

From the present analysis, it can be concluded that the Bank Nifty returns are not

hugely influenced by either increase or decrease of Repo rate and Reverse Repo rates, but

there is a correlation of impact on returns in the post 3 days announcement of Repo Rate

increase. The results clearly evidence that the banking sector, investors and people who are

closely monitoring the banking stocks will have an idea of change in the Repo/Reverse Repo

and that will not hugely impacting the Bank Nifty.

Coming to the aspect of Volatility, there is a volatility in the Bank Nifty in the post 3

days period and pre 6 days period. The impact is more on the 3 days after announcement of

Repo Rate increase.

References

Agrawal, G. (2007). Monetary Policy Announcements and Stock Price Behavior: Empirical Evidence

from CNX Nifty. Decision (0304-0941), 34(2).

[ In Text Ciation : Agarwal, 2007]

ADALYA JOURNAL

Volome 8, Issue 11, November 2019 938

ISSN NO: 1301-2746

http://adalyajournal.com/

Kumari, Lakshmi., Kumar Nagendra. (2019). The Effect of Cash Reserve Ratio and Reverse Repo

rate on Stock Market Performance – Empirical Evidence from India. IOSR Journal of Economics and

Finance , Volume 10, Issue 1, Ser II(Jan, - Feb.2019), PP 47-51

[In Text Citation : Kumari & Nagendra, 2019]

Vanitha, S., Nageswari, P., & Srinivasan, P. (2013). Impact of reverse repo rate and cash

reserve ratio in National Stock Exchange (NSE) CNX bank index. International Journal of

Management and Business Studies, 3(1), 72-81.

[In Text Citation : Vanita et al, 2013]

Websites

www.rbi.org.in

www.nseindia.com

www.investopedia.com

ADALYA JOURNAL

Volome 8, Issue 11, November 2019 939

ISSN NO: 1301-2746

http://adalyajournal.com/

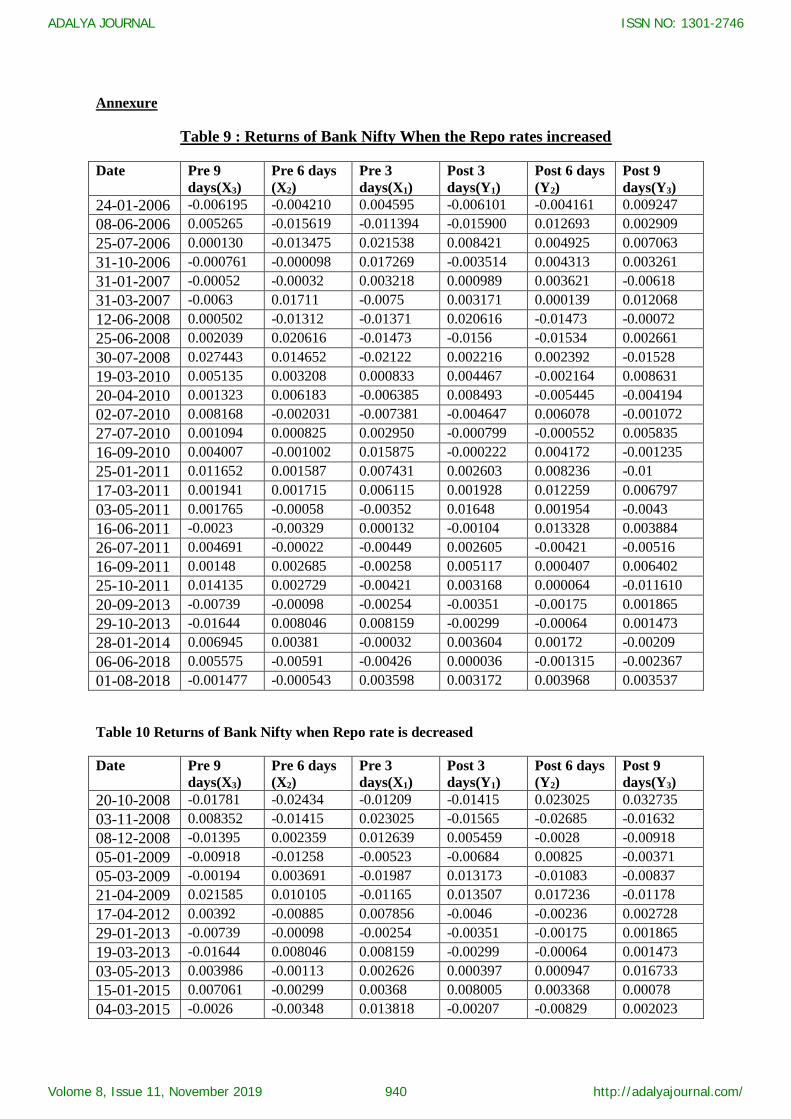

Annexure

Table 9 : Returns of Bank Nifty When the Repo rates increased

Date Pre 9

days(X3)

Pre 6 days

(X2)

Pre 3

days(X1)

Post 3

days(Y1)

Post 6 days

(Y2)

Post 9

days(Y3)

24-01-2006 -0.006195 -0.004210 0.004595 -0.006101 -0.004161 0.009247

08-06-2006 0.005265 -0.015619 -0.011394 -0.015900 0.012693 0.002909

25-07-2006 0.000130 -0.013475 0.021538 0.008421 0.004925 0.007063

31-10-2006 -0.000761 -0.000098 0.017269 -0.003514 0.004313 0.003261

31-01-2007 -0.00052 -0.00032 0.003218 0.000989 0.003621 -0.00618

31-03-2007 -0.0063 0.01711 -0.0075 0.003171 0.000139 0.012068

12-06-2008 0.000502 -0.01312 -0.01371 0.020616 -0.01473 -0.00072

25-06-2008 0.002039 0.020616 -0.01473 -0.0156 -0.01534 0.002661

30-07-2008 0.027443 0.014652 -0.02122 0.002216 0.002392 -0.01528

19-03-2010 0.005135 0.003208 0.000833 0.004467 -0.002164 0.008631

20-04-2010 0.001323 0.006183 -0.006385 0.008493 -0.005445 -0.004194

02-07-2010 0.008168 -0.002031 -0.007381 -0.004647 0.006078 -0.001072

27-07-2010 0.001094 0.000825 0.002950 -0.000799 -0.000552 0.005835

16-09-2010 0.004007 -0.001002 0.015875 -0.000222 0.004172 -0.001235

25-01-2011 0.011652 0.001587 0.007431 0.002603 0.008236 -0.01

17-03-2011 0.001941 0.001715 0.006115 0.001928 0.012259 0.006797

03-05-2011 0.001765 -0.00058 -0.00352 0.01648 0.001954 -0.0043

16-06-2011 -0.0023 -0.00329 0.000132 -0.00104 0.013328 0.003884

26-07-2011 0.004691 -0.00022 -0.00449 0.002605 -0.00421 -0.00516

16-09-2011 0.00148 0.002685 -0.00258 0.005117 0.000407 0.006402

25-10-2011 0.014135 0.002729 -0.00421 0.003168 0.000064 -0.011610

20-09-2013 -0.00739 -0.00098 -0.00254 -0.00351 -0.00175 0.001865

29-10-2013 -0.01644 0.008046 0.008159 -0.00299 -0.00064 0.001473

28-01-2014 0.006945 0.00381 -0.00032 0.003604 0.00172 -0.00209

06-06-2018 0.005575 -0.00591 -0.00426 0.000036 -0.001315 -0.002367

01-08-2018 -0.001477 -0.000543 0.003598 0.003172 0.003968 0.003537

Table 10 Returns of Bank Nifty when Repo rate is decreased

Date Pre 9

days(X3)

Pre 6 days

(X2)

Pre 3

days(X1)

Post 3

days(Y1)

Post 6 days

(Y2)

Post 9

days(Y3)

20-10-2008 -0.01781 -0.02434 -0.01209 -0.01415 0.023025 0.032735

03-11-2008 0.008352 -0.01415 0.023025 -0.01565 -0.02685 -0.01632

08-12-2008 -0.01395 0.002359 0.012639 0.005459 -0.0028 -0.00918

05-01-2009 -0.00918 -0.01258 -0.00523 -0.00684 0.00825 -0.00371

05-03-2009 -0.00194 0.003691 -0.01987 0.013173 -0.01083 -0.00837

21-04-2009 0.021585 0.010105 -0.01165 0.013507 0.017236 -0.01178

17-04-2012 0.00392 -0.00885 0.007856 -0.0046 -0.00236 0.002728

29-01-2013 -0.00739 -0.00098 -0.00254 -0.00351 -0.00175 0.001865

19-03-2013 -0.01644 0.008046 0.008159 -0.00299 -0.00064 0.001473

03-05-2013 0.003986 -0.00113 0.002626 0.000397 0.000947 0.016733

15-01-2015 0.007061 -0.00299 0.00368 0.008005 0.003368 0.00078

04-03-2015 -0.0026 -0.00348 0.013818 -0.00207 -0.00829 0.002023

ADALYA JOURNAL

Volome 8, Issue 11, November 2019 940

ISSN NO: 1301-2746

http://adalyajournal.com/

02-06-2015 0.00411 -0.00256 -0.00211 -0.00419 0.005364 -0.00161

29-09-2015 0.007752 0.011228 0.005679 0.013067 -0.00353 -0.0007

05-04-2016 0.007461 -0.0078 0.000183 0.00105 0.01076 0.007569

04-10-2016 -0.00052 -0.00682 -0.01051 0.000113 0.001507 -0.00185

02-08-2017 0.00109 0.001772 -0.00194 0.001378 -0.00281 0.00576

07-02-2019 -0.002413 0.004101 0.001611 -0.003476 -0.002275 0.001558

04-04-2019 0.000938 0.008823 -0.001345 0.003890 0.002217 -0.004403

06-06-2019 -0.001678 -0.000683 -0.002232 0.003227 -0.005102 0.000159

07-08-2019 0.001360 -0.007541 -0.002492 -0.010870 -0.000476 -0.010865

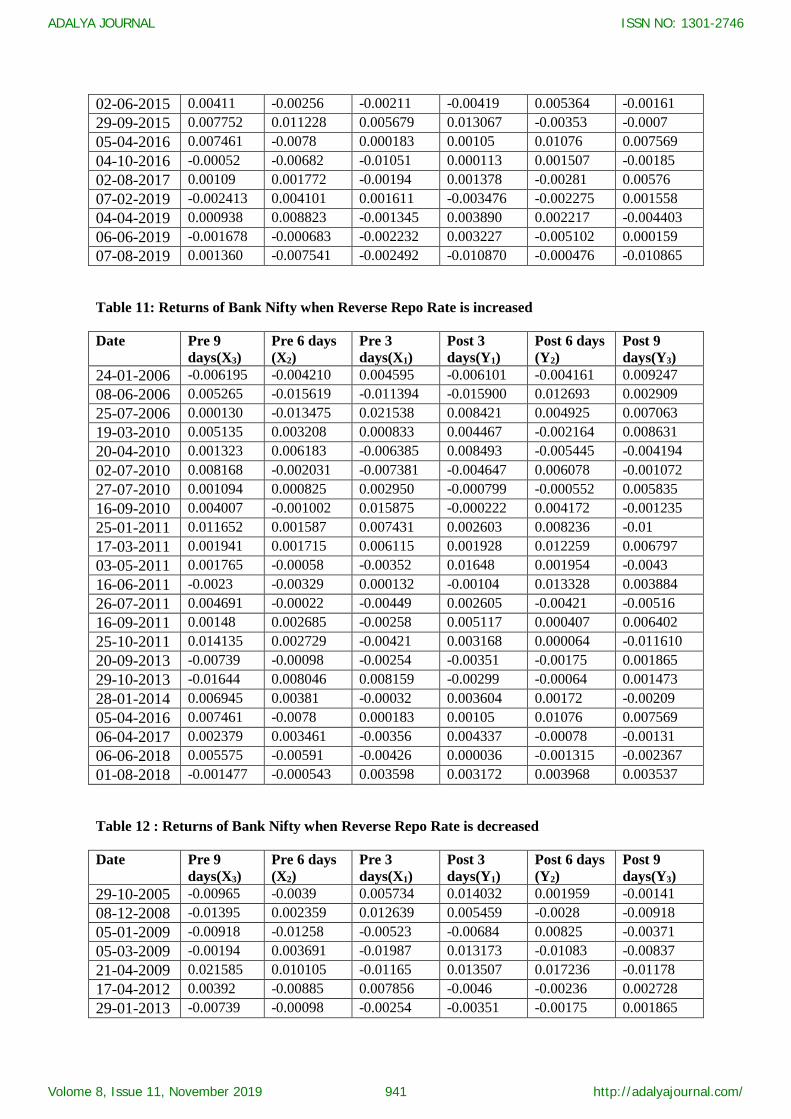

Table 11: Returns of Bank Nifty when Reverse Repo Rate is increased

Date Pre 9

days(X3)

Pre 6 days

(X2)

Pre 3

days(X1)

Post 3

days(Y1)

Post 6 days

(Y2)

Post 9

days(Y3)

24-01-2006 -0.006195 -0.004210 0.004595 -0.006101 -0.004161 0.009247

08-06-2006 0.005265 -0.015619 -0.011394 -0.015900 0.012693 0.002909

25-07-2006 0.000130 -0.013475 0.021538 0.008421 0.004925 0.007063

19-03-2010 0.005135 0.003208 0.000833 0.004467 -0.002164 0.008631

20-04-2010 0.001323 0.006183 -0.006385 0.008493 -0.005445 -0.004194

02-07-2010 0.008168 -0.002031 -0.007381 -0.004647 0.006078 -0.001072

27-07-2010 0.001094 0.000825 0.002950 -0.000799 -0.000552 0.005835

16-09-2010 0.004007 -0.001002 0.015875 -0.000222 0.004172 -0.001235

25-01-2011 0.011652 0.001587 0.007431 0.002603 0.008236 -0.01

17-03-2011 0.001941 0.001715 0.006115 0.001928 0.012259 0.006797

03-05-2011 0.001765 -0.00058 -0.00352 0.01648 0.001954 -0.0043

16-06-2011 -0.0023 -0.00329 0.000132 -0.00104 0.013328 0.003884

26-07-2011 0.004691 -0.00022 -0.00449 0.002605 -0.00421 -0.00516

16-09-2011 0.00148 0.002685 -0.00258 0.005117 0.000407 0.006402

25-10-2011 0.014135 0.002729 -0.00421 0.003168 0.000064 -0.011610

20-09-2013 -0.00739 -0.00098 -0.00254 -0.00351 -0.00175 0.001865

29-10-2013 -0.01644 0.008046 0.008159 -0.00299 -0.00064 0.001473

28-01-2014 0.006945 0.00381 -0.00032 0.003604 0.00172 -0.00209

05-04-2016 0.007461 -0.0078 0.000183 0.00105 0.01076 0.007569

06-04-2017 0.002379 0.003461 -0.00356 0.004337 -0.00078 -0.00131

06-06-2018 0.005575 -0.00591 -0.00426 0.000036 -0.001315 -0.002367

01-08-2018 -0.001477 -0.000543 0.003598 0.003172 0.003968 0.003537

Table 12 : Returns of Bank Nifty when Reverse Repo Rate is decreased

Date Pre 9

days(X3)

Pre 6 days

(X2)

Pre 3

days(X1)

Post 3

days(Y1)

Post 6 days

(Y2)

Post 9

days(Y3)

29-10-2005 -0.00965 -0.0039 0.005734 0.014032 0.001959 -0.00141

08-12-2008 -0.01395 0.002359 0.012639 0.005459 -0.0028 -0.00918

05-01-2009 -0.00918 -0.01258 -0.00523 -0.00684 0.00825 -0.00371

05-03-2009 -0.00194 0.003691 -0.01987 0.013173 -0.01083 -0.00837

21-04-2009 0.021585 0.010105 -0.01165 0.013507 0.017236 -0.01178

17-04-2012 0.00392 -0.00885 0.007856 -0.0046 -0.00236 0.002728

29-01-2013 -0.00739 -0.00098 -0.00254 -0.00351 -0.00175 0.001865

ADALYA JOURNAL

Volome 8, Issue 11, November 2019 941

ISSN NO: 1301-2746

http://adalyajournal.com/

19-03-2013 -0.01644 0.008046 0.008159 -0.00299 -0.00064 0.001473

03-05-2013 0.003986 -0.00113 0.002626 0.000397 0.000947 0.016733

15-01-2015 0.007061 -0.00299 0.00368 0.008005 0.003368 0.00078

04-03-2015 -0.0026 -0.00348 0.013818 -0.00207 -0.00829 0.002023

02-06-2015 0.00411 -0.00256 -0.00211 -0.00419 0.005364 -0.00161

29-09-2015 0.007752 0.011228 0.005679 0.013067 -0.00353 -0.0007

04-10-2016 -0.00052 -0.00682 -0.01051 0.000113 0.001507 -0.00185

02-08-2017 0.00109 0.001772 -0.00194 0.001378 -0.00281 0.00576

07-02-2019 -0.002413 0.004101 0.001611 -0.003476 -0.002275 0.001558

04-04-2019 0.000938 0.008823 -0.001345 0.003890 0.002217 -0.004403

06-06-2019 -0.001678 -0.000683 -0.002232 0.003227 -0.005102 0.000159

07-08-2019 0.001360 -0.007541 -0.002492 -0.010870 -0.000476 -0.010865

ADALYA JOURNAL

Volome 8, Issue 11, November 2019 942

ISSN NO: 1301-2746

http://adalyajournal.com/

F test Results – Repo Rate increase

X1 and Y1

F-Test Two-Sample for Variances

Variable 1 Variable 2

Mean -0.000482 0.001260

Variance 0.000098 0.000060

Observations 26 26

Df 25 25

F 1.624902

P(F<=f) one-tail 0.115891

F Critical one-tail 1.955447

X2 and Y1

F-Test Two-Sample for Variances

Variable 1 Variable 2

Mean 0.001152 0.001260

Variance 0.000048 0.000060

Observations 26 26

df 25 25

F 0.791541

P(F<=f) one-tail 0.281642

F Critical one-tail 0.511392

Y2 and Y3

F-Test Two-Sample for Variances

Variable 1 Variable 2

Mean 0.001152 0.000439

Variance 0.000048 0.000045

Observations 26 26

df 25 25

F 1.067140

P(F<=f) one-tail 0.436116

F Critical one-tail 1.955447

Y3 and Y1

F-Test Two-Sample for Variances

Variable 1 Variable 2

Mean 0.001260 0.000439

Variance 0.000060 0.000045

Observations 26 26

df 25 25

F 1.348180

P(F<=f) one-tail 0.230226

F Critical one-tail 1.955447

X3 and Y1

F-Test Two-Sample for Variances

Variable 1 Variable 2

Mean 0.001260 0.002381

Variance 0.000060 0.000064

Observations 26 26

df 25 25

F 0.934045

P(F<=f) one-tail 0.432952

F Critical one-tail 0.511392

X3 and Y2

F-Test Two-Sample for Variances

Variable 1 Variable 2

Mean 0.001152 0.002381

Variance 0.000048 0.000064

Observations 26 26

df 25 25

F 0.739335

P(F<=f) one-tail 0.227803

F Critical one-tail 0.511392

X3 and Y3

F-Test Two-Sample for Variances

Variable 1 Variable 2

Mean 0.000439 0.002381

Variance 0.000045 0.000064

Observations 26 26

df 25 25

F 0.692819

P(F<=f) one-tail 0.182512

F Critical one-tail 0.511392

ADALYA JOURNAL

Volome 8, Issue 11, November 2019 943

ISSN NO: 1301-2746

http://adalyajournal.com/

F test Results Repo Decreased

X1 and Y1

F-Test Two-Sample for Variances

Var1 Var2

Mean 0.0003 -0.0002

Variance 0.0001 0.0001

Observations 21 21

df 20 20

F 1.4268

P(F<=f) one-tail 0.2168

F Critical one-

tail 2.1242

Y2 and Y1

F-Test Two-Sample for Variances

Var1 Var2

Mean 0.0002 -0.0002

Variance 0.0001 0.0001

Observations 21 21

df 20 20

F 1.5239

P(F<=f) one-tail 0.1770

F Critical one-

tail 2.1242

Y2 and Y3

F-Test Two-Sample for Variances

Var1 Var2

Mean 0.0002 0.0002

Variance 0.0001 0.0001

Observations 21 21

df 20 20

F 0.9336

P(F<=f) one-tail 0.4397

F Critical one-

tail 0.4708

Y3 and Y1

F-Test Two-Sample for Variances

Var1 Var2

Mean -0.0002 0.0002

Variance 0.0001 0.0001

Observations 21 21

df 20 20

F 0.6126

P(F<=f) one-tail 0.1408

F Critical one-

tail 0.4708

X3 and Y1

F-Test Two-Sample for Variances

Var1 Var2

Mean -0.0002 -0.0003

Variance 0.0001 0.0001

Observations 21 21

df 20 20

F 0.7888

P(F<=f) one-tail 0.3004

F Critical one-

tail 0.4708

X3 and Y2

F-Test Two-Sample for Variances

Var1 Var2

Mean 0.0002 -0.0003

Variance 0.0001 0.0001

Observations 21 21

df 20 20

F 1.2021

P(F<=f) one-tail 0.3423

F Critical one-

tail 2.1242

X3 and Y3

F-Test Two-Sample for Variances

Var1 Var2

Mean 0.0002 -0.0003

Variance 0.0001 0.0001

Observations 21 21

df 20 20

F 1.2876

P(F<=f) one-tail 0.2886

F Critical one-

tail 2.1242

ADALYA JOURNAL

Volome 8, Issue 11, November 2019 944

ISSN NO: 1301-2746

http://adalyajournal.com/

F test Results When Reverse Repo Rate is increased

X 1 and Y1

F-Test Two-Sample for Variances

Var1 Var2

Mean 0.000944 0.001376

Variance 0.000058 0.000039

Observations 22 22

df 21 21

F 1.478497 P(F<=f) one-tail 0.188728 F Critical one-

tail 2.084189

Y2 and Y1

F-Test Two-Sample for Variances

Var1 Var2

Mean 0.002707 0.001376

Variance 0.000033 0.000039

Observations 22 22

df 21 21

F 0.835193 P(F<=f) one-tail 0.341824 F Critical one-

tail 0.479803

Y2 and Y3

F-Test Two-Sample for Variances

Var1 Var2

Mean 0.002707 0.000994

Variance 0.000033 0.000034

Observations 22 22

df 21 21

F 0.955595

P(F<=f) one-tail 0.459046

F Critical one-tail 0.479803

Y3 and Y1

F-Test Two-Sample for Variances

Var1 Var2

Mean 0.001376 0.000994

Variance 0.000039 0.000034

Observations 22 22

df 21 21

F 1.144161

P(F<=f) one-tail 0.380256

F Critical one-tail 2.084189

X3 and Y1

F-Test Two-Sample for Variances

Var1 Var2

Mean 0.001376 0.002243

Variance 0.000039 0.000043

Observations 22 22

df 21 21

F 0.908376

P(F<=f) one-tail 0.413894

F Critical one-

tail 0.479803

X3 and Y2

F-Test Two-Sample for Variances

Var1 Var2

Mean 0.002707 0.002243

Variance 0.000033 0.000043

Observations 22 22

df 21 21

F 0.758669

P(F<=f) one-tail 0.266194

F Critical one-

tail 0.479803

X3 and Y3

F-Test Two-Sample for Variances

Var1 Var2

Mean 0.000994 0.002243

Variance 0.000034 0.000043

Observations 22 22

df 21 21

F 0.793924 P(F<=f) one-tail 0.300859 F Critical one-

tail 0.479803

ADALYA JOURNAL

Volome 8, Issue 11, November 2019 945

ISSN NO: 1301-2746

http://adalyajournal.com/

F test Results – Reverse Repo Rate Decreased

X1 and Y1

F-Test Two-Sample for Variances

Variable 1 Variable 2

Mean 0.000099 0.001984

Variance 0.000070 0.000056

Observations 19 19

df 18 18

F 1.248508 P(F<=f) one-tail 0.321372 F Critical one-

tail 2.217197

Y2 and Y1

F-Test Two-Sample for Variances

Variable 1 Variable 2

Mean -0.000001 0.001984

Variance 0.000037 0.000056

Observations 19 19

df 18 18

F 0.664172 P(F<=f) one-tail 0.196777 F Critical one-

tail 0.451020

Y2 and Y3

F-Test Two-Sample for Variances

Variable 1 Variable 2

Mean -0.000001 -0.001095

Variance 0.000037 0.000042

Observations 19 19

df 18 18

F 0.880052

P(F<=f) one-tail 0.394649

F Critical one-tail 0.451020

Y3 and Y1

F-Test Two-Sample for Variances

Variable 1 Variable 2

Mean 0.001984 -0.001095

Variance 0.000056 0.000042

Observations 19 19

df 18 18

F 1.325037

P(F<=f) one-tail 0.278320

F Critical one-tail 2.217197

X3 and Y1

F-Test Two-Sample for Variances

Variable 1 Variable 2

Mean 0.001984 -0.000735

Variance 0.000056 0.000074

Observations 19 19

df 18 18

F 0.758313

P(F<=f) one-tail 0.281670

F Critical one-

tail 0.451020

X3 and Y2

F-Test Two-Sample for Variances

Variable 1 Variable 2

Mean -0.000001 -0.000735

Variance 0.000037 0.000074

Observations 19 19

df 18 18

F 0.503650

P(F<=f) one-tail 0.077601

F Critical one-

tail 0.451020

X3 and Y3

F-Test Two-Sample for Variances

Variable 1 Variable 2

Mean -0.001095 -0.000735

Variance 0.000042 0.000074

Observations 19 19

df 18 18

F 0.572296

P(F<=f) one-tail 0.122974

F Critical one-tail 0.451020

ADALYA JOURNAL

Volome 8, Issue 11, November 2019 946

ISSN NO: 1301-2746

http://adalyajournal.com/