presentation: asia's perspectives on rebalancing and orei … · 2011-04-25 · reverse...

TRANSCRIPT

Asia’s Perspectives onAsia’s Perspectives onAsia s Perspectives onAsia s Perspectives onRebalancing & OREI ResearchRebalancing & OREI Research

1.1. Asia’s Issues & ChallengesAsia’s Issues & Challenges2.2. OREI’s Research AgendaOREI’s Research Agenda

IwanIwan J. J. AzisAzisHead, Office of Regional Economic IntegrationHead, Office of Regional Economic Integration

Asian Development Bank forAsian Development Bank forAsian Development Bank, for Asian Development Bank, for ADBADB--PIIE Book launchingPIIE Book launching

Washington DC, 25 April 2011Washington DC, 25 April 2011

Contribution to CPI Inflation

Jan-June 2010 July 2010-latest data

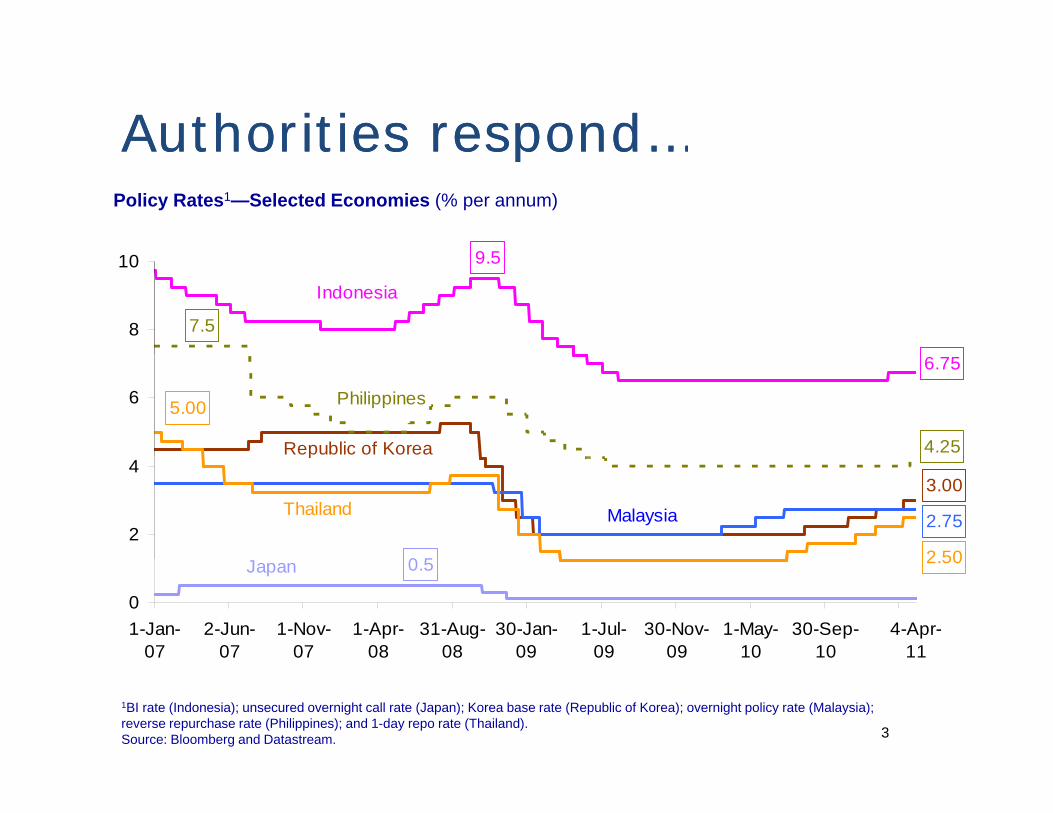

Authorities respond…Authorities respond…Authorities respond…Authorities respond…Policy Rates1—Selected Economies (% per annum)

9 5

7.5

9.5

8

10

Indonesia

4.25

5.00

6.75

6 Philippines

Republic of Korea

3.00

2.75

2 500 5

2

4

Thailand Malaysia

J 2.500.5

01-Jan-

072-Jun-

071-Nov-

071-Apr-

0831-Aug-

0830-Jan-

091-Jul-09 30-Nov-

091-May-

1030-Sep-

101-Mar-

11

Japan

4-Apr-11

1-Jul-09

1BI rate (Indonesia); unsecured overnight call rate (Japan); Korea base rate (Republic of Korea); overnight policy rate (Malaysia); reverse repurchase rate (Philippines); and 1-day repo rate (Thailand).Source: Bloomberg and Datastream. 3

Currency appreciation helpsCurrency appreciation helpsChange in Exchange Rate against US dollar1 (%)

Indonesian rupiah 2010

Malaysian ringgit

Singapore dollar

Indonesian rupiah 2010

2011 YTD

PRC renminbi

Philippine peso

Japanese yen

2

Thai baht

Hong Kong dollar

Korean won

-8 -4 0 4 8 12 16

Vietnamese dong

Thai baht

1Year-to-date (YTD) figures based on 21 Mar 2011 closing. Negative values indicate depreciation.2PRC = People's Republic of China.Source: OREI staff calculations based on Reuters data. 4

Keeping food costs downKeeping food costs downAdministrative Measures (as of 16 February 2011)

Control

EconomiesReduce

taxesIncrease supply

Restrict exports

Control prices /

subsidize consumers

Cash transfers

Food for work Food aid

Feeding programs

Stimulate production

China, People's Rep. ofCambodiaIndonesiaL PDRLao PDRPhilippinesThailandViet Nam

Source: Asian Development Bank 2011, April 2011.

5

Declining Correlation of Output Gap and Commodity PricesGap and Commodity Prices

3 06%2000CY=1

2 0

2.5

3.0

4

6

Global Output Gap(RHS)

S&P GSCI

1.5

2.0

2

Linear approximation of S&P GSCI

0.5

1.0

-2

0

-0.5

0.0

-41998 99 2000 01 02 03 04 05 06 07 08 09 10 11

Linear approximation of Global Output Gap

6

(Note) S&P GSCI is shown as relative price to the global headline CPI.(Source) IMF, Bloomberg

998 99 000 0 0 03 0 05 06 0 08 09 0

Upward Level Shift in Correlation: Structural Changes?Structural Changes?

3.0 2000=1

2.5 1998-2002

1.5

2.0 2003-2005

2006-2010

Linear approximation of 1998-2002PG

SC

I

1.0 Linear approximation of 2006-2010S

&P

0.5 -4 -2 0 2 4 (%)

Global Output Gap

7

(Note) S&P GSCI is shown as relative price to the global headline CPI.(Source) IMF, Bloomberg

Global Output Gap

Stalled Oil Supply vs Increased Inventories Inventories

4,500 90 Million barrelsMillion barrels/day

4,300

4,400

85

World Oil Supply

World Petroleum Stocks (RHS)

4 000

4,100

4,200

80

3,800

3,900

4,000

75

3,600

3,700 70

8

3,500 65 1994 1996 1998 2000 2002 2004 2006 2008 2010

(Source) U.S. Department of Energy

One‐year rolling correlation between daily return of global

Interest rate gap = short‐term real interest rate minus potential GDP growth (minus means easy monetary conditions). S&P GSCI is shown as

equity index (MSCI AC‐World) and that of commodity index (S&P GSCI) . (Source) Bloomberg

relative price to the global headline CPI. (Source) IMF, Bloomberg

Global Investors’ Portfolio R b l i “Fi i li ti ”?

• Institutional investors aiming to

Rebalancing: “Financialisation”?

• Institutional investors aiming to gain the benefits of asset diversification and inflation diversification and inflation hedging and higher returns.

• Improvements in market infrastructure

• Development of commodity indices and Improvement in indices and Improvement in trading-related platform.

Destabilizing capital flowsDestabilizing capital flowsg pg pNet Financial Flows—Selected Economies1

(% of GDP)

5.7

5.820

30Gross Inflows

-0.4

4.3

3.8

0

10

-5.9

-6.1-20

-10

-40

-30

2007Q1 2007Q4 2008Q3 2009Q2 2010Q1 2010Q4

Direct Investment Portfolio Investment Other Investment Net Financial Flows

Gross Outflows

GDP = gross domestic product.1Includes Hong Kong, China; Indonesia; Republic of Korea; Philippines; Singapore; Thailand; and Viet Nam. Does not include Malaysia from 2010Q2 to 2010Q4 as data on inflow-outflow breakdown for portfolio and other investment unavailable. Does not include Viet Nam in 2010Q4 as data unavailable. "Other investment" includes financial derivatives. Source: OREI staff calculations based on data from International Financial Statistics, International Monetary Fund; and national sources.

Policy IssuesPolicy Issues• Managing inflationary pressureg g y p

• Monetary-fiscal & other policies • Currency appreciation • Regional cooperation & other policies?

• Managing capital flows effectively (well t t d & t d i )targeted & temporary, and conversion)• Limit foreign currency borrowing• Foreign currency reserve requirement• Foreign currency reserve requirement• Holding period• Withholding tax on foreign investmentWithholding tax on foreign investment• Tax on foreign capital• Regional coordination & intraregional trade

• Excess saving and cross-border financial flows

DevelopmentTrade & Finance

em

DevelopmentTrade & Finance

mployym

ent & povverty

Real sectorsFinancial sectors

PRODTY

LBR PRODTY