infrastructure to sustain canada’s north - arctic parl · infrastructure to sustain canada’s...

TRANSCRIPT

September 9, 2014 11th CPAR - Whitehorse, Yukon 1

Infrastructure to Sustain Canada’s North

11th CPAR, Whitehorse, Yukon

September 9, 2014

Rick Meyers The Mining Association of Canada

AGENDA

MAC & Canada’s Mining Industry Towards Sustainable Mining

Canada’s North – Mining’s Contribution Infrastructure North

Current Status (Access & Energy) Rationale for Infrastructure Investment

to help Sustain the North

About MAC

The national voice of the

mining industry in Canada:

Advocacy - to advance the

business of mining

Towards Sustainable Mining:

About performance, stewardship

and social license

39 Corporate members in iron ore,

gold, diamonds, oil sands, met-

coal, base metals, uranium

50 Associate members in

engineering, environment, finance

Advocacy work supported by

member committees: environment,

science, economics, public affairs,

Aboriginal relations

11th CPAR - Whitehorse, Yukon 2 September 9, 2014

Canada’s Mining Industry Contributions

Domestic Contribution

• 220 mines, 33 smelters and refineries

• 380K employees,

• $20B annual capital investment

• $71B taxes over the past decade

• Largest private sector employer of

Aboriginal Canadians

Global Competitor

• Attracted 18% of world exploration

spending in 2011

• TSX/TSX-V: 1,600 mining companies

listed, 47% projects outside Canada

• Minerals account for 23% of

Canada’s total goods exports

• Primary source of minerals for Clean

Technology

• Top five world producer in uranium,

potash, nickel, platinum, zinc

aluminum, diamonds, met coal 11th CPAR - Whitehorse, Yukon 3 September 9, 2014

Canada’s Mining Industry Coast to Coast to Coast

11th CPAR - Whitehorse, Yukon 4 September 9, 2014

5

Northern Canada’s growth rooted in Resource

Development

• Infrastructure

Contributions to communities and

infrastructure

• Dawson City, Yukon; Yellowknife,

NWT; Rankin Inlet, Nunavut

• Roads, ports, hydro facilities, rail,

microwave communications

• Community health and sports facilities

• Environmental and Social Legacies

Pressure on regulators – pressure on

industry to improve performance

Importance of improving performance

Towards Sustainable Mining: Our Commitment

Established in 2004, TSM is MAC’s

commitment to responsible mining that

every member agrees to implement.

TSM’s primary objective is to enable

mining companies to meet society’s

minerals products needs in the most

socially, environmentally and economically

responsible way.

The program’s core strengths are:

• Accountability – Mandatory for all

members to report at the facility level

• Transparency – Annual reporting against

23 indicators with independent verification

• Credibility – Through ongoing

consultation with our Community of

Interest Advisory panel to improve industry

performance and help shape TSM for

continual advancement

6 11th CPAR - Whitehorse, Yukon September 9, 2014

TSM Program Architecture

TSM Guiding Principles

Policy Frameworks

TSM Performance Protocols

Communities and People Environmental Stewardship Energy Efficiency

Aboriginal and Community Outreach

Crisis Management Planning

Safety and Health

Tailings Management

Biodiversity Conservation Management

Energy Use and GHG Emissions Management

Good Practice Guidance Assessment Protocols Performance Measurement

and Reporting System External Verification

Energy Efficiency

Guidance and Expectations

23 Performance Indicators in 6 protocols

Public Reporting and Verification

11th CPAR - Whitehorse, Yukon 7 September 9, 2014

Governance

Tailings Working Group Energy Task Force

Community of Interest Advisory

Panel

MAC Board of Directors

TSM Governance Team

TSM Initiative Leaders

Public Affairs Committee

Biodiversity Task Force

Other MAC Committees/ Taskforces/Working Groups

Towards Sustainable Mining (TSM)

11th CPAR - Whitehorse, Yukon 8

COI Advisory Panel Composition

Aboriginal peoples

Environmental NGO

Economic/community development

Social NGO including faith based groups

Finance/investment

International development

Labour/workplace

Media/communications

MAC Board of Directors

Junior Mining Company Representative

September 9, 2014

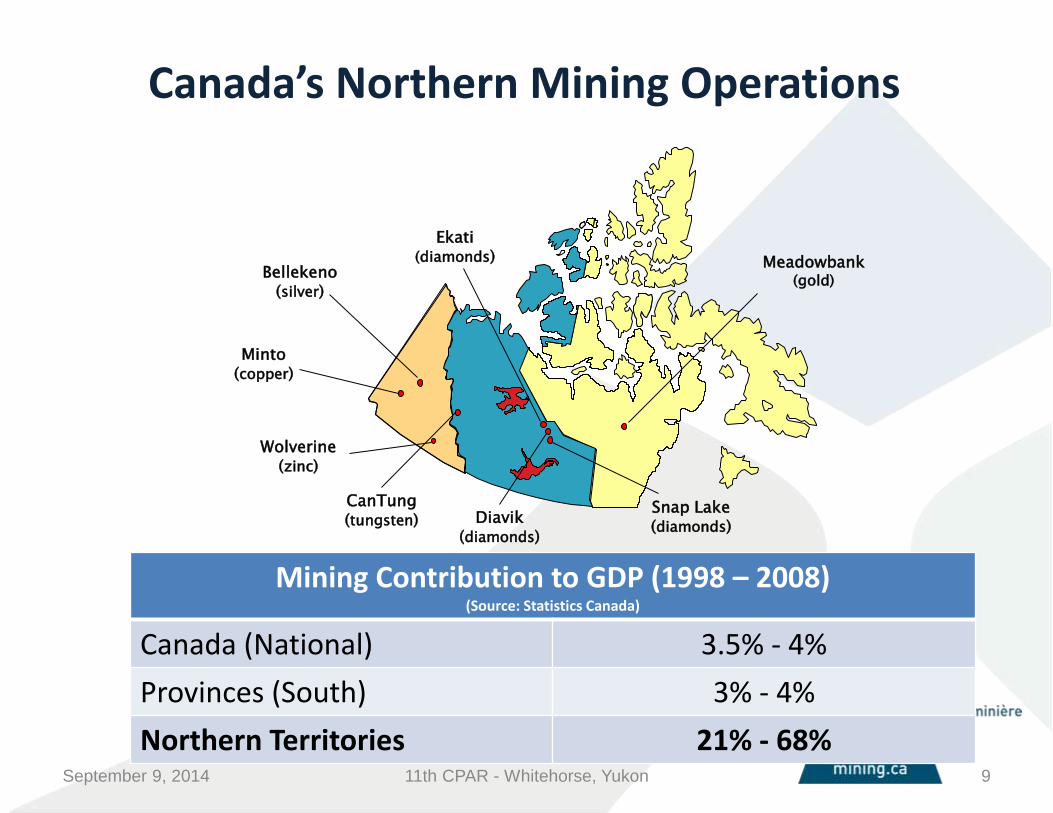

Minto (copper)

Bellekeno (silver)

Ekati (diamonds) Meadowbank

(gold)

CanTung (tungsten) Diavik

(diamonds)

Snap Lake (diamonds)

Wolverine (zinc)

Canada’s Northern Mining Operations

11th CPAR - Whitehorse, Yukon 9

Mining Contribution to GDP (1998 – 2008) (Source: Statistics Canada)

Canada (National) 3.5% - 4%

Provinces (South) 3% - 4%

Northern Territories 21% - 68% September 9, 2014

Contribution to Northern Economies

11th CPAR - Whitehorse, Yukon 10

Employment

35,000+ person-years

Production

>$30 Billion over 3 decades in

diamonds, copper, gold, silver,

lead, zinc, tungsten

Investment/Spending >$15 B+ in capital and

operating expenditures

Taxes ~$4 Billion to 2013

~$6 Billion by 2020

September 9, 2014

Business and Social Development

Local Business Development

• >$9 B Northern, $4 B Aboriginal

contracts

• More than 50 new Aboriginal

Businesses in the NWT alone

Workforce & Social development

• Extensive programming in Aboriginal

skills training and education

• >$100 million social and community

contributions

• Support for health care, education

and sports facilities

11th CPAR - Whitehorse, Yukon 11 September 9, 2014

Northern Realities (Canada vs. Europe!)

Facts

• >1/3 of Canada’s landmass

• Arctic conditions

• ~100,000 residents

• Most heavily subsidized region of

Canada

• Communities dependent on

Government - or resource

development for employment

Challenges

• High cost of living

• Little or no infrastructure (“BYO”)

• Employment opportunities are limited

• Resource development is the primary

economic advantage

Area of Canada’s North = Norway, Sweden, Finland, Denmark, France, Germany, Poland, Spain, Portugal, Italy combined.

11th CPAR - Whitehorse, Yukon 12 September 9, 2014

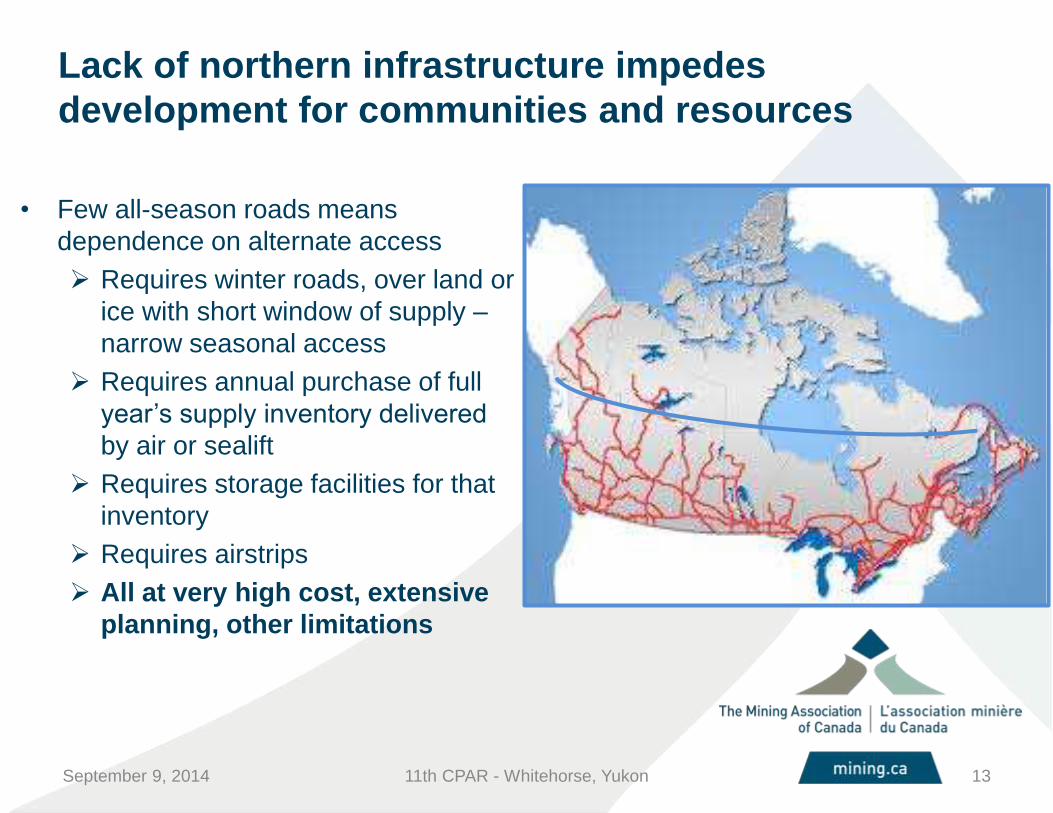

Lack of northern infrastructure impedes

development for communities and resources

• Few all-season roads means

dependence on alternate access

Requires winter roads, over land or

ice with short window of supply –

narrow seasonal access

Requires annual purchase of full

year’s supply inventory delivered

by air or sealift

Requires storage facilities for that

inventory

Requires airstrips

All at very high cost, extensive

planning, other limitations

11th CPAR - Whitehorse, Yukon 13 September 9, 2014

Northern Energy Supply

14

Very limited hydro electric grids with no

connectivity to outside producers; no opportunity

to import power

• Off-grid power primarily diesel generation

• (Contributing to GHG production)

• Wind used in few locations

• Limited LNG use; lacks long-term storage

technology

All major cost considerations for

communities and potential developers

15

Yukon Roads

• 3 – Wolverine – Zinc

• 1 – Minto –Copper

• 2 – Bellekeno - Silver

Yukon - Long history of mining

• 1890s Klondike Gold Rush

• Currently 3 Mines brought into

production

• $500 million investment

• Generates over 1,000 direct

jobs and innovative First

Nations partnerships

• Expanding the road network

would enhance exploration

opportunities

Yukon roads infrastructure

is the most advanced of the

three territories

Minto

Bellekeno

Wolverine

Yukon

16

Yukon

Future Development

Eagle Gold

Howard’s Pass

Mactung Carmacks Copper

Casino

• New projects will represent another

$3.5 - $5 billion in investment in the

next 10 years

• Potential for 2,000 new mining jobs,

plus equivalent in service sector

• Secure energy supply

• access to grid power

• Yukon as a northern gateway, with

good transportation links to Asia

17

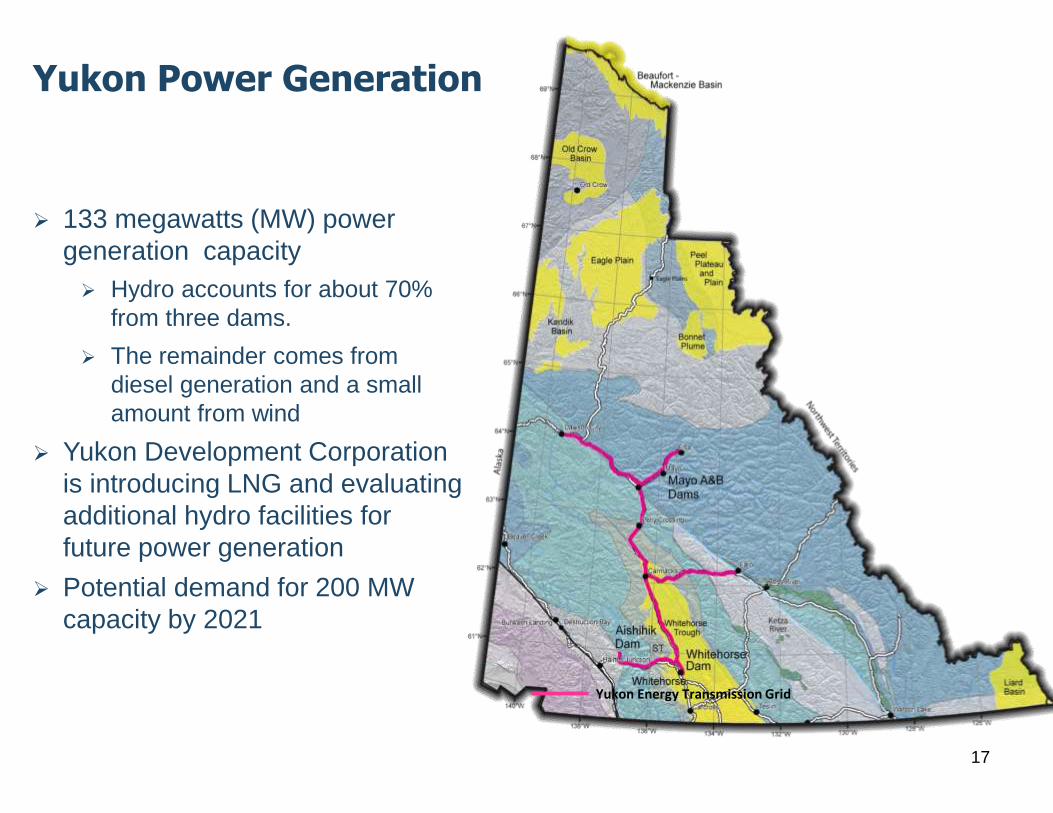

133 megawatts (MW) power

generation capacity

Hydro accounts for about 70%

from three dams.

The remainder comes from

diesel generation and a small

amount from wind

Yukon Development Corporation

is introducing LNG and evaluating

additional hydro facilities for

future power generation

Potential demand for 200 MW

capacity by 2021

Yukon Power Generation

Yukon Energy Transmission Grid

Northwest Territories Roads

NWT

NUNAVUT

.

Diamond

Mines Ice Road

Road network mainly

limited to the south

Supplemented by winter

ice roads

11th CPAR - Whitehorse, Yukon 18 September 9, 2014

Challenges

Seasonal Ice Road Access

Diavik

11th CPAR - Whitehorse, Yukon 19

• Companies joint venture of three Diamond Mines

• 400 km to operations - 75% over lake ice

• Sophisticated engineering support

• 2 month window to complete all haulage

• Annual number of loads ranges from 5,500 to 11,000

• Major demand on trucking

• Impacts of Climate Change

Source: NWT Economic Outlook 2014-2015

September 9, 2014

NWT Energy Options: Grid Power

All NWT hydro power was developed

by mining operations • Built to support mines and

neighbouring communities • Bluefish – Con mine

• Snare – Giant mine

• Taltson – Pine Point mine

All remain in operation today

and continue to supply

power to communities

11th CPAR - Whitehorse, Yukon 20

NWT

September 9, 2014

Energy Alternatives - NWT Hydro Expansion Project

• Project proposed to link existing isolated hydro facilities

• Cheaper power for communities and operating mines

• Displace millions of litres/year of diesel consumption annually

• Several hundred

construction jobs

• Lower cost of

living

Courtesy: NWT Energy Corp

11th CPAR - Whitehorse, Yukon 21 September 9, 2014

22

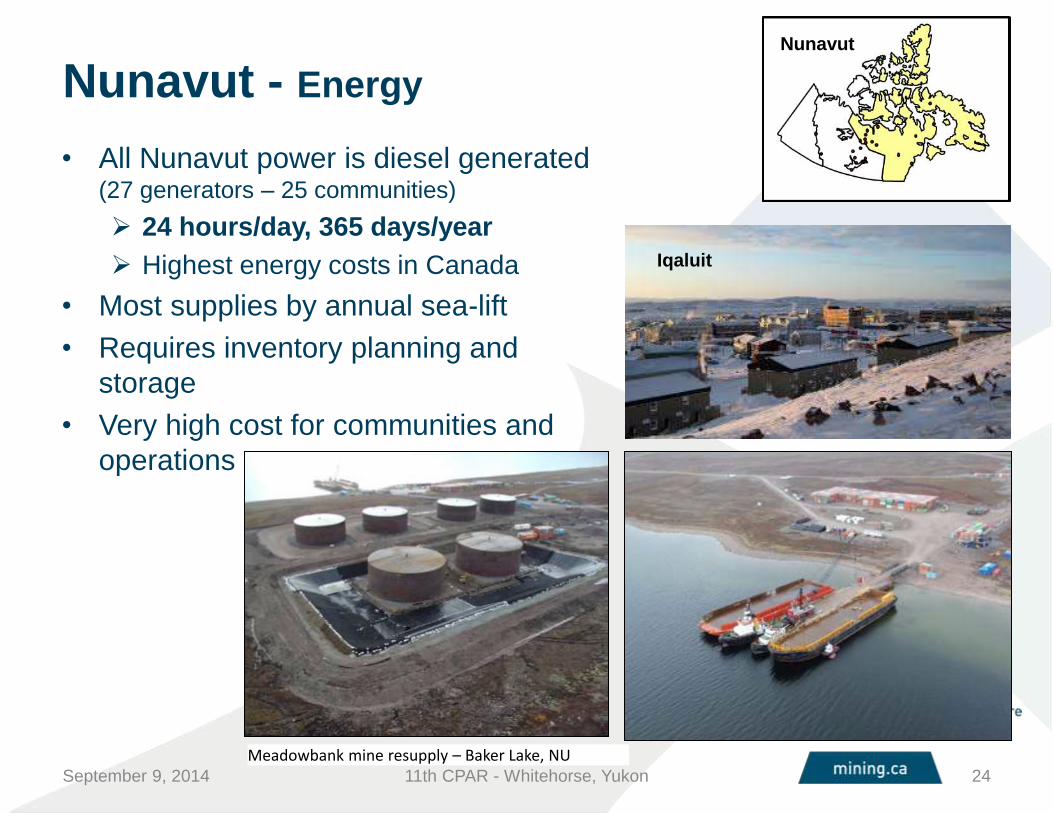

Nunavut

Nunavut – Infrastructure is scarce But high mineral potential (Au, Fe, Zn, Diamonds, U)

11th CPAR - Whitehorse, Yukon 23

Nunavut needs road access

Meadowbank Access

Nunavut Nunavut:

• Largest northern territory; isolated communities

• No public road network

• Three company-operated private access roads

• No long-distance power transmission grid

• One mine produces ~23% of Territorial GDP

• Total dependence on air or sea for access & supply

September 9, 2014

Nunavut - Energy

• All Nunavut power is diesel generated (27 generators – 25 communities)

24 hours/day, 365 days/year

Highest energy costs in Canada

• Most supplies by annual sea-lift

• Requires inventory planning and

storage

• Very high cost for communities and

operations

Meadowbank mine resupply – Baker Lake, NU 11th CPAR - Whitehorse, Yukon 24

Nunavut

Iqaluit

September 9, 2014

Nunavut supply means major shipping costs

• Supplies shipped from

southern Canada

• Mine production shipped to

southern or international

markets

• Require deep water ports

11th CPAR - Whitehorse, Yukon 25 September 9, 2014

11th CPAR - Whitehorse, Yukon 26

Supply and Logistics

• 52,000 tonnes of sealift supplies every 10-12 weeks from Quebec

• 54M litres of fuel annually

• 400 passengers per week (air)

• 60,000 lbs of cargo per week

• Baker – Meadowbank road year-round transportation for fuel, passengers, cargo

Meadowbank Mine (Nunavut’s only mine)

Nunavut

September 9, 2014

27

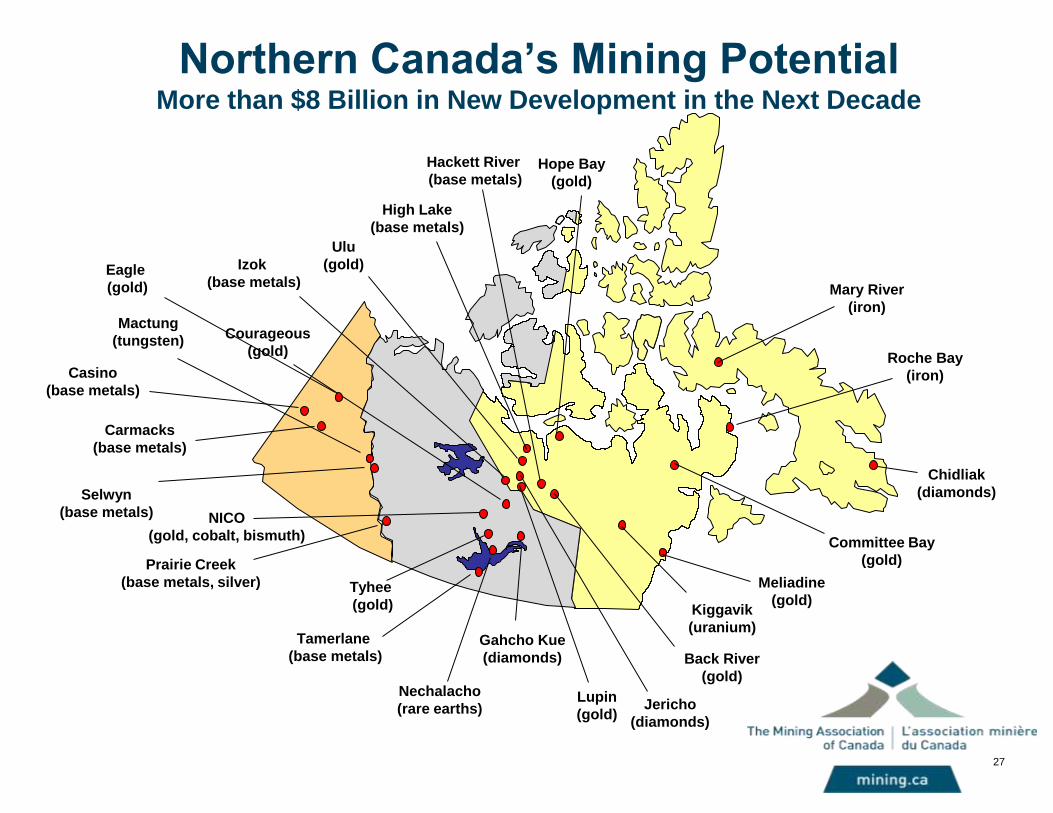

Northern Canada’s Mining Potential More than $8 Billion in New Development in the Next Decade

Mary River

(iron)

Hope Bay

(gold)

High Lake

(base metals)

Meliadine

(gold)

Roche Bay

(iron)

Hackett River

(base metals)

Kiggavik

(uranium)

Ulu

(gold)

Selwyn

(base metals)

Prairie Creek

(base metals, silver)

Gahcho Kue

(diamonds)

Nechalacho

(rare earths)

Tyhee

(gold)

NICO

(gold, cobalt, bismuth)

Tamerlane

(base metals)

Courageous

(gold)

Back River

(gold)

Izok

(base metals)

Lupin

(gold) Jericho

(diamonds)

Committee Bay

(gold)

Chidliak

(diamonds)

Carmacks

(base metals)

Eagle

(gold)

Casino

(base metals)

Mactung

(tungsten)

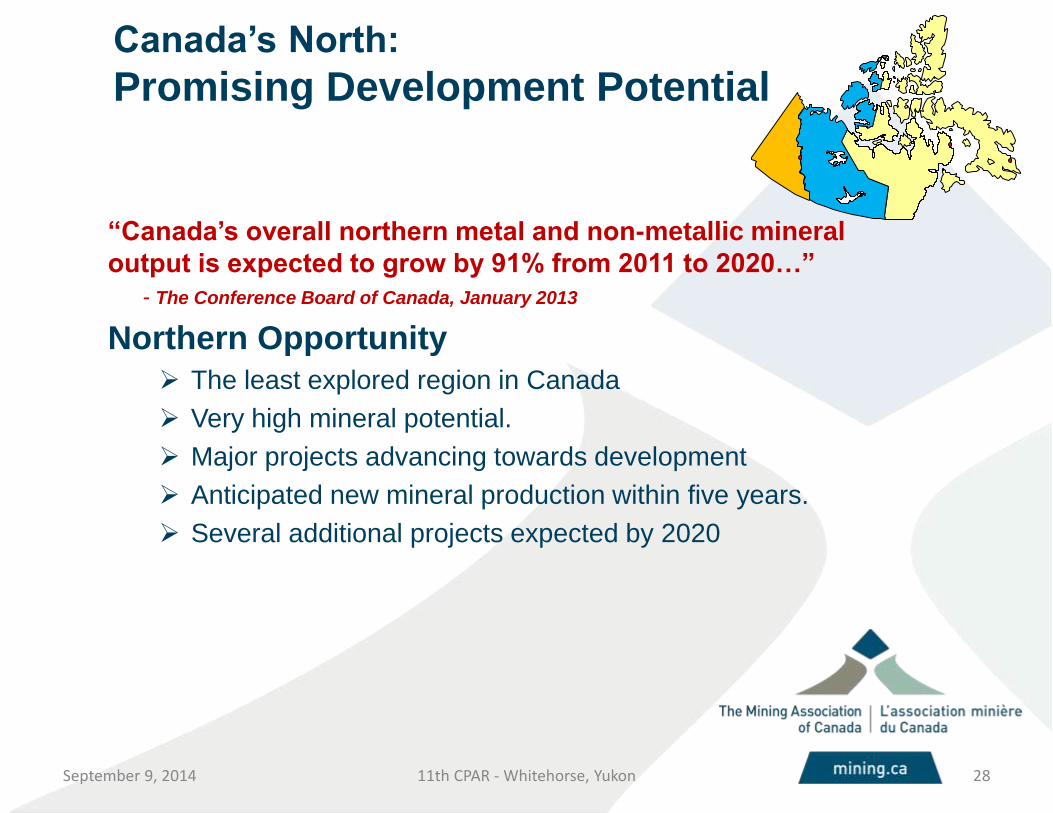

Canada’s North:

Promising Development Potential

“Canada’s overall northern metal and non-metallic mineral

output is expected to grow by 91% from 2011 to 2020…”

- The Conference Board of Canada, January 2013

Northern Opportunity

The least explored region in Canada

Very high mineral potential.

Major projects advancing towards development

Anticipated new mineral production within five years.

Several additional projects expected by 2020

11th CPAR - Whitehorse, Yukon 28 September 9, 2014

29

Business Case:

Infrastructure development can help Sustain

the North

11th CPAR - Whitehorse, Yukon

Resource Development:

• North’s primary economic advantage

• Employment and community benefits

• Capital investment – business development

• Taxes & Royalties to Governments to further support healthy communities

Infrastructure:

• Critical for regional development

• Critical for mineral development

Providing infrastructure to support development also supports communities

Improves the Quality of Life

Reduces the need for Government subsidies and helps communities become more self-sufficient

Federal and Territorial Governments

Devolution to Territorial Governments Initiatives to facilitate northern development

Working towards improving regulatory processes

Funding for public geoscience

Education and workforce training initiatives

Negotiating to settle land claims

Territorial initiatives to improve access and energy supply

11th CPAR - Whitehorse, Yukon 30 September 9, 2014

31 22

FOR MORE INFORMATION

PLEASE CONTACT:

Rick Meyers

Vice President, Technical and

Northern Affairs

613-233-9392

Follow us on Twitter:

@theminingstory

Thank You

Merci