innovation in brazil: challenges, opportunies and barriers · innovation in brazil: challenges,...

TRANSCRIPT

Alex da Silva Alves College of Agriculture “Luiz de Queiroz” - Esalq

University of São Paulo

Innovation in Brazil: challenges, opportunies

and barriers

Presentation structure

• The context for innovation in Brazil

– Economic growth perspectives

– R&D spending

– Profile of entrepreneurs

– Innovation and entrepreneurship financing

– Barriers to innovation and entrepreneurship

• Islands of Excellence in Brazil

• Some final words

The context for innovation in Brazil

Economic growth perspectives

International Monetary Fund. World Economic Outlook. Washington, DC, April 2013.

Economic growth perspectives

• Real GDP growth in the LAC region declined to 3 percent in 2012, from 4½ percent in 2011, reflecting a slowdown in external demand and, in some cases, the impact of domestic factors.

• The deceleration was particularly pronounced in Brazil, the region’s largest economy, where large policy stimulus failed to spur private investment.

• The slowdown in Brazil spilled over to its regional trading partners, especially Argentina, Paraguay, and Uruguay.

International Monetary Fund. World Economic Outlook. Washington, DC, April 2013.

Economic growth perspectives

International Monetary Fund. World Economic Outlook. Washington, DC, April 2013.

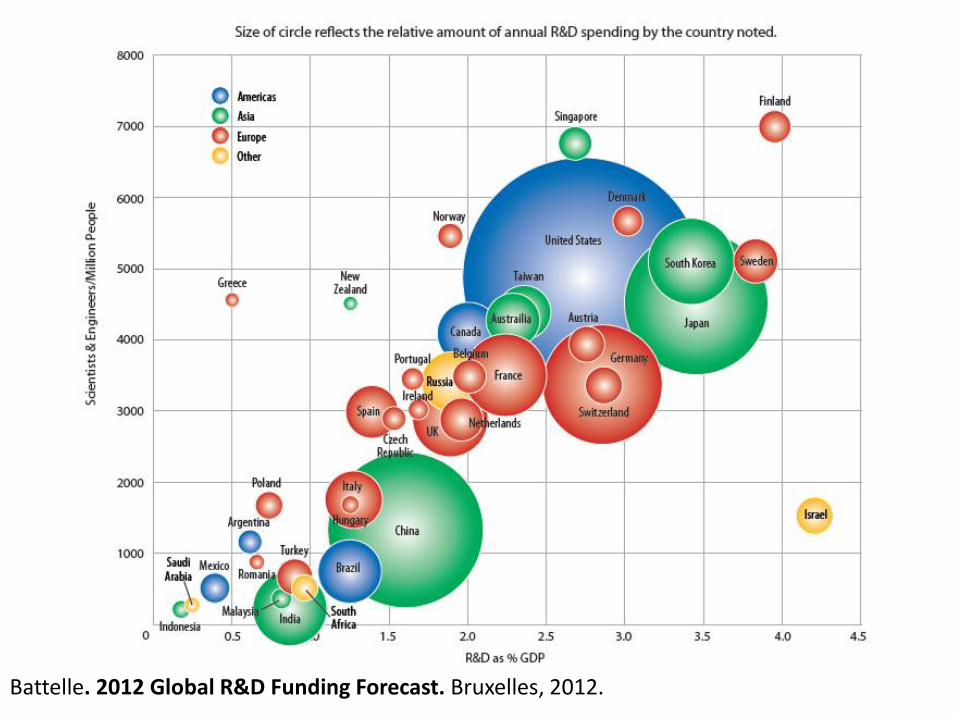

R&D spending

World Ranking

Company Industry R&D-

2011 €m

R&D 1-year growth

R&D CAGR-3y Sales-

2011 €m

Sales 1-year growth

92 Vale Mining 1190,0 96,6% 4,2% 45590,8 46,0

96 Petroleo Brasiliero

Oil & gas producers 1149,6 67,9% 8,0% 101524,2 22,6

748 CPFL Energia Gas, water & multiutilities 88,6 10,2% 35,7% 5307,1 -1,7

763 EMBRAER Aerospace & defence 85,9 72,8% -23,4% 4098,8 10,8

998 Totvs Software & computer services

60,5 -3,0% 27,9% 531,9 13,3

1068 Weg Industrial engineering 56,0 33,7% 14,9% 2157,7 18,2

1347 Braskem Chemicals 41,2 25,8% 13794,1 30,1

The most R&D-intensive Brazilian firms

Battelle. 2012 Global R&D Funding Forecast. Bruxelles, 2012.

Company Beta

coefficient

Ibovespa 1,00

Vale 0,92

Petrobras 1,05

Totvs 0,84

CPFL 0,05

Braskem 0,66

Embraer 0,51

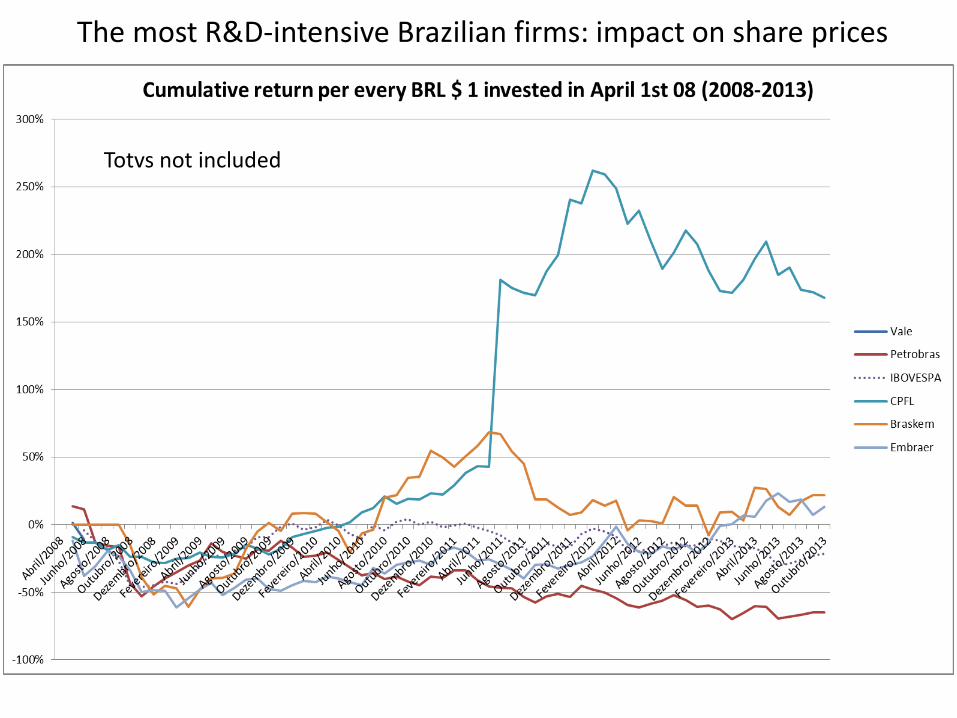

The most R&D-intensive Brazilian firms: impact on share prices

Totvs not included

The most R&D-intensive Brazilian firms: impact on share prices

Totvs and CPFL not included

The most R&D-intensive Brazilian firms: impact on share prices

The context: R&D investments

Battelle. 2012 Global R&D Funding Forecast. Bruxelles, 2012.

Profile of Brazilian entrepreneurs

• Since its first edition a decade ago, the Global Entrepreneurship Monitor (GEM, 2012) continues to claim entrepreneurship in Brazil as mostly driven by need than by the exploitation of a market opportunity.

• According to GEM, there are 27 million people in Brazil directly involved with some kind of entrepreneurial activity. – This is ¼ of the population aged 18-64.

Profile of Brazilian entrepreneurs

• Responsible for over 60 per cent of jobs in the country, SMEs generate 20 per cent of GDP and account for 99 per cent of the 6 million companies working in Brazil (GEM, 2012).

• The relative importance of these segments has grown consistently and the growth of its turnover exceeds the average of the Brazilian economy.

Innovation and entrepreneurship financing

• Credit market in Brazil is more targeted to the consumer than to the producer, to short than to long term, and reaches more high than low income borrowers.

• A market for private R&D investment is mainly available through public finding sources:

– Brazil’s innovation agency - FINEP www.finep.gov.br

– Brazil’s Development Bank - BNDES www.bndes.gov.br

– The Brazilian Research Council – www.cnpq.br

Innovation and entrepreneurship financing

R&D and proof of concept financing Entreprise financing

Brazil’s Innovation Agency (FINEP) provides funding on a sunk-cost or reimbursable basis up to R$ 1 million.

Public funding from the Brazilian Development Bank (BNDES) and other sources through the CRIATEC seed fund - up to R$ 3 million.

Brazil’s Ministry of Science and Technology (MCT), the National Research Council (CNPq) and States’ Research Support Agencies provide financial resources for business plan development, proof of concept and R&D on a sunk cost basis.

Private funding from seed funds (scarse but growing with the entry of FINEP and BNDES as general or limited partners). Private funding from business angels (still scarse and limited to larger and richer regions, but growing in importance) – up to R$ 1 million. Private VC funding –available but more scarse for firms after the 2008 turmoil.

On May 2013 FINEP and BNDES annouced a R$ 1 billion joint financing scheme with a mix of credit and sunk cost funding to projects that boost the Brazilian agro-industry value chain (Inova-Agro) – up to R$ 30 million per project.

Main funding sources for entrepreneurship and innovation

Innovation and entrepreneurship financing

2011 2012 Venture Capital

Mezzanine Private Investments

In Public Equity - PIPE

Others

Modes of Private Equity Investments in Brazil

ABVCAP – Brazilian Venture Capital Association. Available at http://www.abvcap.com.br/Download/Estudos/2325.pdf

Brazilian R$ (billions)

Innovation and entrepreneurship financing

ABVCAP – Brazilian Venture Capital Association. Available at http://www.abvcap.com.br/Download/Estudos/2325.pdf

Percentage (%) of Private Equity Investments in Brazil – by Sector

Innovation and entrepreneurship financing

ABVCAP – Brazilian Venture Capital Association. Available at http://www.abvcap.com.br/Download/Estudos/2325.pdf

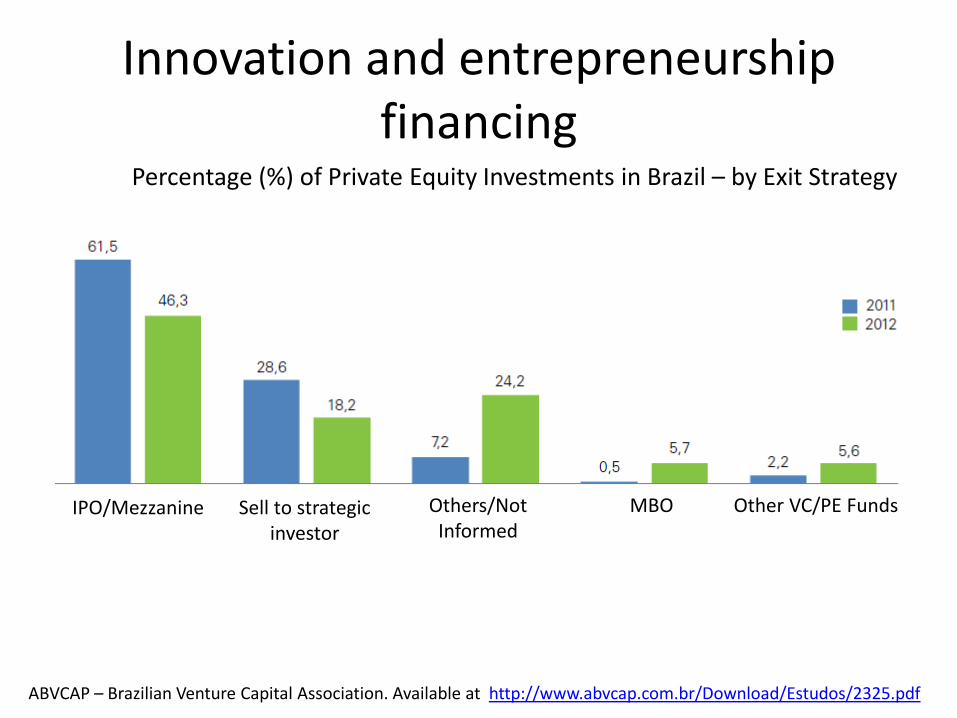

Percentage (%) of Private Equity Investments in Brazil – by Exit Strategy

IPO/Mezzanine Sell to strategic investor

Others/Not Informed

MBO Other VC/PE Funds

Private Equity Fund

Periodo of time

Cumulative return since IPO

Performance of Private Equity-backed Companies in Brazil

Innovation and entrepreneurship financing

Barriers to innovation and entrepreneurship

Entrepreneurship Barometer 2013 & Valor Econômico (Oct, 7th 2013).

2600

347

0

1000

2000

3000

Brazil G20

Time spent with tax issues - hours (2010/2012)

Taxes and regulation Brazil G20 Time frame

Number or procedures to start a new business (number) 12,0 7,6 2010/2012

Time to start a new business (days) 119,0 22,0 2010/2012

Costs to start a new business (% of per capita income) 5,8 9,4 2010/2012

Minimim capital required to start a business (% of per capita income) - 17,9 2010/2012

Cost of firing employees (weeks and salaries paid) 46,0 50,0 2007/2009

Tax and labour contributions (% of profits) 40,8 24,0 2012

Total tax rates (%) 69,3 49,7 2012

Total sales taxes (%) 19,0 14,2 2012

Barriers to innovation and entrepreneurship

OECD. Brazil STI Outlook. Bruxelles, 2012. Available at: http://www.oecd.org/brazil/sti-outlook-2012-brazil.pdf .

Barriers to innovation and entrepreneurship

• Before joining the WTO in 1995, the Brazilian patent office, INPI, could cap royalty payments and demand that local partners gain rights to imported know-how.

• The discovery of oil in ultra-deep waters offshore has helped to change attitudes. Firms drilling in the new fields must spend 1% of gross revenues locally on research and development.

The economist. Brazil: Getting serious about patents. November, 2012. Available at: http://www.economist.com/news/americas/21565606-getting-serious-about-patents-owning-ideas.

Barriers to innovation and entrepreneurship

• During the 1970s state investment made Brazil a world leader in sugar-cane ethanol. But that wave of innovation petered out.

• Mr Ávila of INPI hopes that more effective, and swifter, patent protection and a 2004 law granting universities greater rights to exploit spin-offs from publicly funded research will mean that innovation will now bear more fruit.

The economist. Brazil: Getting serious about patents. November, 2012. Available at: http://www.economist.com/news/americas/21565606-getting-serious-about-patents-owning-ideas.

Barriers to innovation and entrepreneurship

World Intellectual Property Organization (WIPO). 2012 World Intellectual Property Indicators. available at http://www.wipo.int/export/sites/www/freepublications/en/intproperty/941/wipo_pub_941_2012.pdf.

Based on WIPO data.

0

10000

20000

30000

40000

50000

60000

0

2000

4000

6000

8000

10000

12000

14000

16000

1998 2000 2002 2004 2006 2008 2010 2012 2014

Onl

y Ja

pan

All

cou

ntr

ies

-ex

cep

t Ja

pan

Number of Patents Granted as Distributed by Year of Patent Grant

GERMANY

TAIWAN

UNITED KINGDOM

FRANCE

KOREA, SOUTH

ITALY

ISRAEL

CHINA, PEOPLE'S REPUBLIC OF

FINLAND

INDIA

SPAIN

RUSSIAN FEDERATION

BRAZIL

TURKEY

JAPAN

Barriers to innovation and entrepreneurship

0

2000

4000

6000

8000

10000

12000

14000

1998 2000 2002 2004 2006 2008 2010 2012 2014

All

cou

ntr

ies

-ex

cep

t Ja

pan

Number of Patents Granted as Distributed by Year of Patent Grant

TAIWAN

CHINA, PEOPLE'S REPUBLIC OF

INDIA

RUSSIAN FEDERATION

BRAZIL

TURKEY

Based on WIPO data.

Developing countries

Barriers to innovation and entrepreneurship

Country

CAGR

1999-

2012

Total Patents

granted

(1999-2012)

CHINA, PEOPLE'S REPUBLIC OF 36% 21.922

INDIA 23% 8.932

TURKEY 22% 426

SINGAPORE 14% 7.129

KOREA, SOUTH 11% 112.247

ISRAEL 10% 25.326

SPAIN 8% 8.489

BRAZIL 8% 3.087

TAIWAN 8% 125.749

AUSTRALIA 6% 29.236

AUSTRIA 5% 16.652

RUSSIAN FEDERATION 5% 3.593

CHINA, HONG KONG S.A.R. 5% 11.972

CANADA 4% 101.448

DENMARK 4% 13.866

FINLAND 4% 18.799

JAPAN 4% 904.801

NETHERLANDS 4% 42.143

GERMANY 3% 313.675

UNITED KINGDOM 3% 119.359

ITALY 3% 53.095

SWEDEN 3% 41.735

SWITZERLAND 3% 49.227

FRANCE 3% 119.182

Compounded Average Growth Rate for Selected Countries – Patents Granted 1999-2012

Based on WIPO data.

Barriers to innovation and entrepreneurship

Barriers to innovation and entrepreneurship

The Economist Intelligence Unit.

Islands of excellence in Brazil

Context

• Despite the aspects discussed so far, there are “islands of excellence” in Brazil.

• These are sectors and areas that gained scale by exploiting positive economic externalities derived by past state investments in agriculture, oil & gas, and infrastructure provision to universities.

Context

• The comprehension of innovation as a lever of competitiveness has increased in Brazil and contributed to the creation of a more receptive environment to entrepreneurship.

• Unprecedented levels of R&D investments (public + private):

– 2000: R$ 12 billion (€ 6,5 billion – money of the day)

– 2011: R$ 50 billion (€ 20,5 billion – money of the day)

Support institutions

The National Research Council (CNPq) is a federal support agency created in 1951. CNPq provides research grants to universities, researchers and firms cooperating with universities in science, technology and innovation projects. Funds provided are on a sunk cost basis. More at www.cnpq.br

Support institutions

The São Paulo Research Foundation – FAPESP – is an independent state foundation with the mission to foster research and the scientific and technological development of the State of São Paulo. FAPESP is the most important state research foundation in the country. It provides funds to researchers, firms and universities on a sunk cost basis. More at www.fapesp.br

Support institutions

.

“The Brazilian Development Bank (BNDES) is the main financing agent for development in Brazil. Since its foundation, in 1952, the BNDES has played a fundamental role in stimulating the expansion of industry and infrastructure in the country”. More at www.bndes.gov.br

Support institutions

The Brazilian Innovation Agency – FINEP – provides universities and firms with financial resources on a sunk cost and reimbursable basis. The aim of the Agency is to advance the country’s technological and entrepreneurial development through the financing of collaborative or individual projects. More at www.finep.gov.br

Research facilities

The Centro de Pesquisas Leopoldo Américo Miguez de Mello - Cenpes - is the Petrobras’ research unit responsible for R&D and engineering in simulation and production for energy-related areas. Created in 1963 in a area of 300000 m2, Cenpes is one the world’s most important applied research facilities. More at http://www.petrobras.com.br/

Research facilities

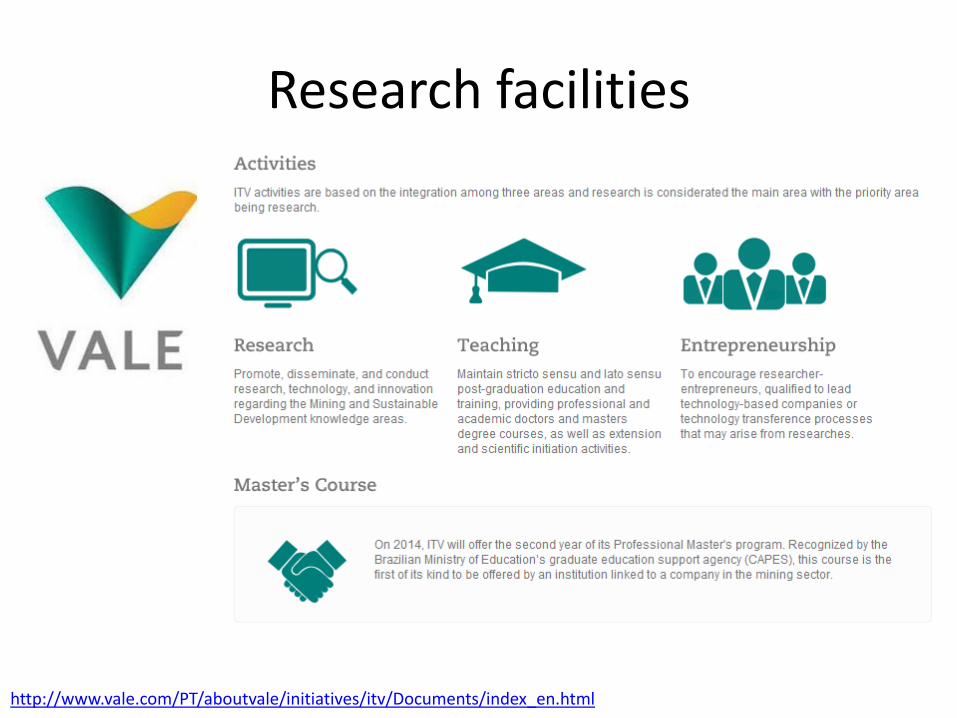

http://www.vale.com/PT/aboutvale/initiatives/itv/Documents/index_en.html

Research facilities

http://www.vale.com/PT/aboutvale/initiatives/itv/Documents/index_en.html

Research facilities

The Sugarcane Technology Center - CTC - is the largest research center for sugarcane in the world. CTC operates in the entire production chain of the sugarcane industry: from cultivation to final production of sugar, ethanol and energy. In one of its core areas, CTC performs the mapping of areas with low productivity and develops sugarcane varieties for these regions within eight years at most. In the past this period of time ranged from 12 to 14 years.

http://revistapesquisa.fapesp.br/en/2013/07/22/from-bagasse-to-innovation/

Agriculture

Develops Plene Cana that, according to the company, eliminates the need for nursery areas and reduces the use of heavy machinery harvesting, thereby preserving the soil. The company also claims that its product resists to some typical sugarcane pests.

http://revistapesquisa.fapesp.br/en/2013/07/22/from-bagasse-to-innovation/

Agriculture

http://revistapesquisa.fapesp.br/en/2013/07/22/from-bagasse-to-innovation/

Agriculture

http://revistapesquisa.fapesp.br/en/2013/07/22/from-bagasse-to-innovation/

Agriculture

http://revistapesquisa.fapesp.br/en/2013/07/22/from-bagasse-to-innovation/

Some final words

Some final words

• The short availability of private money is still a concern for innovation take-up in Brazil. Macroeconomic aspects also contribute.

• (Private) investors complain about the scarcity of good projects.

• Although significant gains emerge, here and there, the participation of universities in the creation of internationally competitive startups is still very modest.

Some final words

• Government participation is fundamental. But the size and scale of some agencies end up inhibiting the willingness of the private sector to taken on more risks.

• The geographical mobility – a prerequisite for the attractiveness of bright professionals from inland and abroad – is reduced due to several factors (disadvantageous law, social aspects, urban disorder, poor infrastructure, education…).

Thanks!