insurance & the challenges of economic uncertainty 4 th annual european insurance industry...

TRANSCRIPT

Insurance & the Challenges of Economic Uncertainty

4th Annual European Insurance Industry Conference

London, U.K.

26 November 2002

Robert P. Hartwig, Ph.D., CPCU, Senior Vice President & Chief EconomistInsurance Information Institute 110 William Street New York, NY 10038Tel: (212) 346-5520 Fax: (212) 732-1916 [email protected] www.iii.org

If you would like a copy of this presentation, please give me your business card with e-mail address

Download at http://www.iii.org

Presentation Outline

Challenges of Economic Uncertainty

• Economic Origins & Geopolitical Instability

• Exogenous (External Influences)

• Endogenous (Internal Influences)

• Conclusions

• Q&A

The Impacts & Implications

• IMPACTS:

• Volatile revenue streams

• Volatile underwriting results

• Volatile investment returns

• Inconsistent financial performance

• IMPLICATIONS:

Low Return on Equity

Unattainable Cost of Capital

Mergers and Acquisitions Difficult

ECONOMIC OVERVIEW

Weak/Weakening Growth

Geopolitical Uncertainty

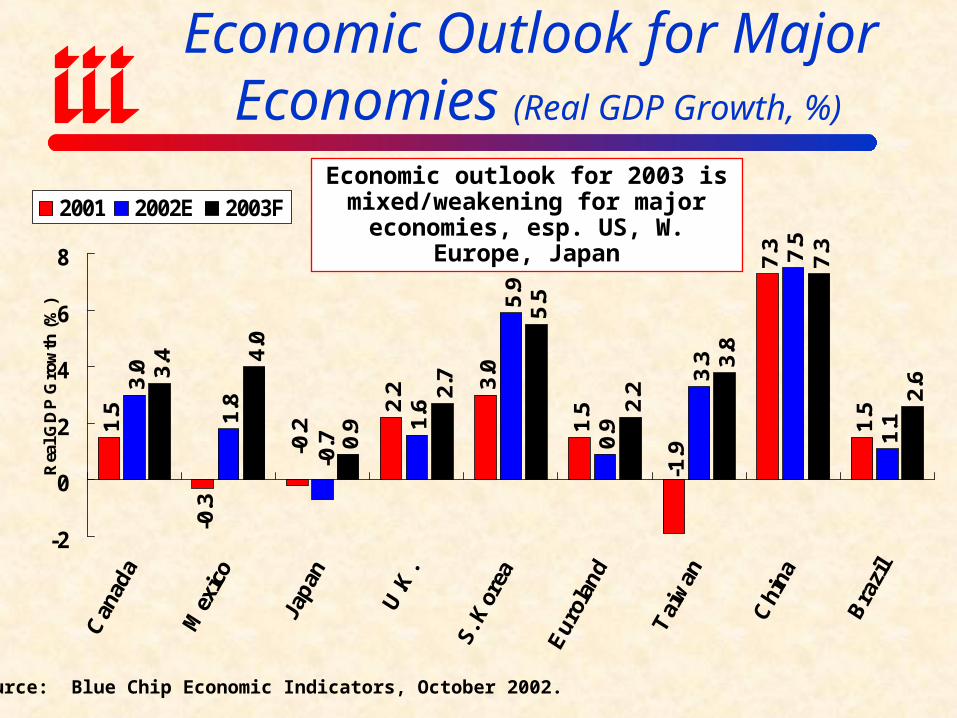

Economic Outlook for Major Economies (Real GDP Growth, %)

1.5

-0.3

2.2 3.

0

1.5

7.3

1.5

3.0

1.8

1.6

5.9

0.9

3.3

7.5

1.1

3.4 4.

0

0.9

2.7

5.5

2.2

3.8

7.3

2.6

-0.2

-1.9-0.7

-2

0

2

4

6

8

Rea

l GD

P G

row

th (

%)

2001 2002E 2003F

Source: Blue Chip Economic Indicators, October 2002.

Economic outlook for 2003 is mixed/weakening for major economies,

esp. US, W. Europe, Japan

4.4%3.5%

2.5%

5.7%

8.3%

4.8%5.6%

2.2%

1.0%

-0.6%

-1.6%

-0.3%

5.0%

1.1%

2.4%3.0%2.7%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

U.S. Real GDP Growth

Source: US Department of Commerce, Blue Economic Indicators 10/02, Insurance Information Institute.

Economy is experiencing sluggish growth following the

recession of 2001

(first recession since 1990/91)

14.4%

16.2%15.0%

13.0%

10.2%9.0%

11.9%

13.4%14.6%

13.9%

14.1%

14.0%13.7%15.2%

10.4%

10.0%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

All US Industries

Return in Equity: Fortune 5001987–2002E

Source: Insurance Information Institute; Fortune

Profitability among the Fortune 500 has fallen during the difficult economic

period of the past 2-3 years.

Impact of Recession on US Non-Life Premiums and Profitability (1970-2001)

7.5%

5.7%

-1.8%

-0.4%

4.3% 4.6% 4.2%4.1%

8.6%

4.6%

6.8%

9.0%9.6%

11.4%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

Inflation (CPI) NWP Growth(unadj.)

Real NWPGrowth

ROE--P/CInsurers*

ROE--AllIndustries*

ROE--Banks* ROE--DiversifiedFinancial*

Recession Years (1970; 74-75; 80-82; 90-91;2001)

Non-Recession Years (all other years, 1970-2001)

*GAAP return on equity, adjusted for inflation; Bank data 1952-2001; Div. Fin. 1987-2001Source: Insurance Information Institute

Geopolitical Instability Remains High

War on Terrorism

Terrorists & Terrorism

Expansion of War Is Iraq Next?

MANIFESTATIONS OF ECONOMIC UNCERTAINTY ON

GLOBAL INSURANCE INDUSTRY:

Profitability

Underwriting Performance

Ratings/Downgrades

Management Shifts

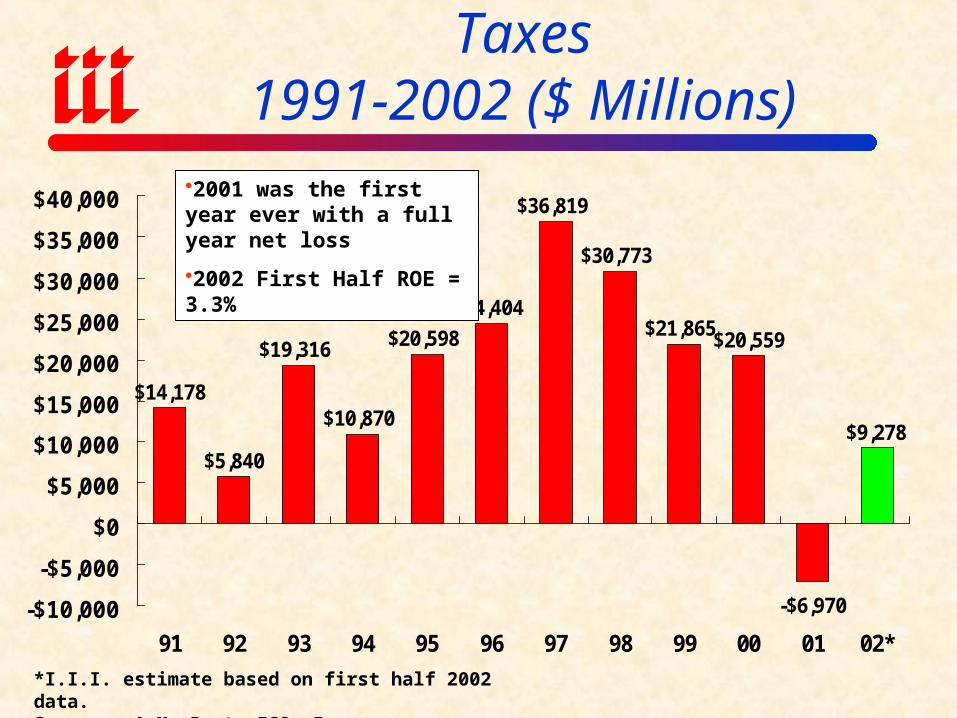

US Non-Life Net Income After Taxes1991-2002 ($ Millions)

$14,178

$5,840

$19,316

$10,870

$20,598

$24,404

$36,819

$30,773

$21,865$20,559

-$6,970

$9,278

-$10,000

-$5,000

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

91 92 93 94 95 96 97 98 99 00 01 02*

*I.I.I. estimate based on first half 2002 data.Sources: A.M. Best, ISO, Insurance Information Institute.

2001 was the first year ever with a full year net loss

2002 First Half ROE = 3.3%

-5%

0%

5%

10%

15%

20%

ROE Cost of Capital

ROE vs. Cost of Capital: US Non-Life 1991 – 2002

Source: The Geneva Association, Ins. Information Inst.

There is an enormous gap between the industry’s cost of capital and its rate of return

14.6

pts

7.9.

pts

US P/C insurers have missed their cost of capital by an

average 6.7 points since 1991

Gap Between Required and Actual UW Result Needed to Achieve Target ROE

As a % of Premium

-16

-14

-12

-10

-8

-6

-4

-2

0

U.S. Canada U.K. France Germany

(%)

Note: US, Canada are 2000 data, 1999 for all othersSource: Swiss Re, sigma 5/01.

Most major insurer markets missing target ROEs by wide margins

even before 11 September

0%

5%

10%

15%

20%

25%

30%

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

UK Switzerland France Germany

Cost of Capital: Non-Life Insurers:1978 – 1998

*

Source: Kielholz, Walter, “The Cost of Capital for Insurance Companies,” The Geneva Papers on Economic Activity, v 25, no. 1, January 2000.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

Non-Life US Non-Life Canada

Return on EquityUS vs. Canada: 1975 – 2000

*

Source: Insurance Information Institute; Insurance Bureau of Canada.

95

100

105

110

115

120

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00

02**

P/C Industry Combined Ratio

2001 = 115.7

2002E = 105.0*

Combined Ratios

1970s: 100.3

1980s: 109.2

1990s: 107.7

2000s: 110.4

*Based on first half 2002 results

Sources: A.M. Best; III

Growth in Premium Volume:Life vs. Non-Life*

2000 vs. 1999

7.610.2

29.4

3.8

20.0

0.6

-5

0

5

10

15

20

25

30

US Canada U.K. Germany France Japan

(% Growth)

Non-Life Life

*Growth rates based on premium volume in local currencies.Source: Swiss Re, sigma 6/01.

Life insurance growth led the way in the 1990s

through 2000. Non-Life growth will lead the way for some time to come.

0%

5%

10%

15%

20%

25%

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

*Estimate based on first half 2002 results.Source: A.M. Best, Insurance Information Institute

Growth in Net Premiums Written (All US Non-Life Lines)

2000: 5.1%

2001: 8.1%

2002: 12.0(est.)

The underwriting cycle went AWOL in the 1990s.

It’s Back!

Ratings Downgrades: Swarms of Downgrades Stinging Insurers

Reasons for Recent Downgrades

of Insurers Worldwide

• Asbestos

• Reserve Deficiencies

• Management Issues (e.g., transitions)

• Reinsurance Uncollectibles

• Investment Write-Downs

• Adverse Development

• Missed/Shifting Earnings Targets

Large Number of Senior Management Changes: Symptomatic of Underlying Difficulties

Senior Management Changes at Many Companies

• American Re AMP Ltd. Annuity & Life Re

• Assicur. Generali AXA Corp Solutions Caliber One

• CA State FundChubb Cigna

• C N A Credit Suisse Employers Re

• General Star Gerling MLP

• Mutual Risk Mgmt OneBeacon Royal & SunAlliance

• Royal America Safeco St. Paul

• Scor Swiss Life Trenwick

• Zurich

Source: Morgan Stanley as of Nov. 8, 2002.

SOURCES OF VOLATILITY & UNCERTAINTY

Exogenous & Endogenous Factors

EXOGENOUS INFLUENCES

Catastrophic LossInvestment Volatility

Crisis in Corporate GovernanceExcessive Litigiousness

Health Care Cost InflationTerrorism

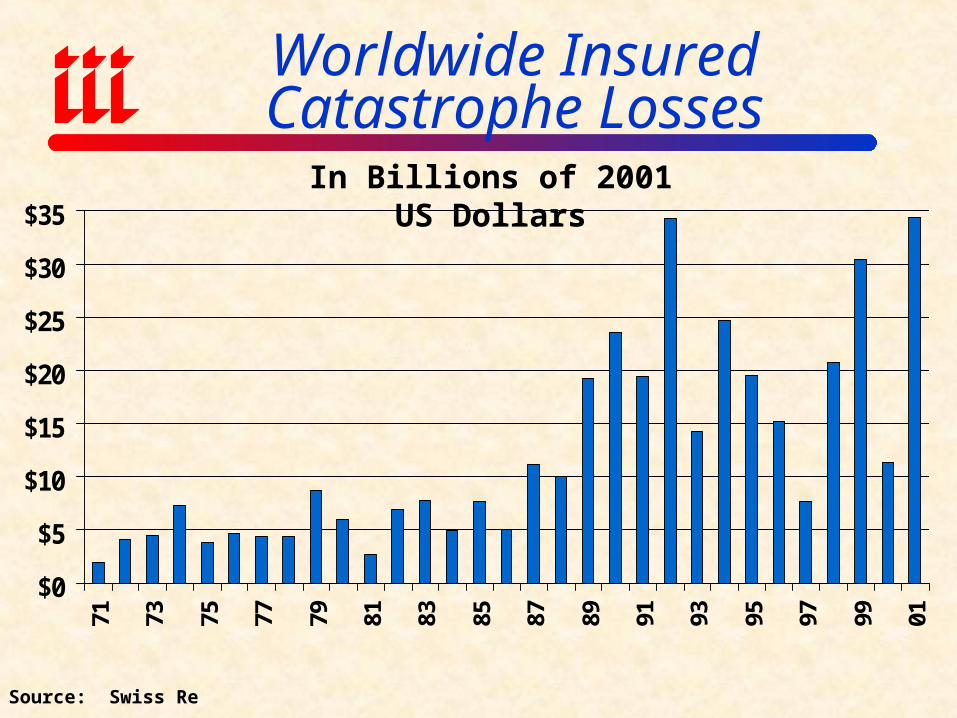

Worldwide InsuredCatastrophe Losses

$0

$5

$10

$15

$20

$25

$30

$35

71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 01

Source: Swiss Re

In Billions of 2001 US Dollars

U.S. InsuredCatastrophe Losses

$7.5

$2.7$4.7

$22.9

$5.5

$16.9

$8.3 $7.3

$2.6

$10.1$8.3

$4.3

$28.1

$4.1

0

5

10

15

20

25

30

89 90 91 92 93 94 95 96 97 98 99 00 01 02*

*Estimate through October 2002.Note: 2001 figure includes $20.3B for 9/11 losses reported through 12/31/01. Includes only business and personal property claims, business interruption and auto claims.Source: Property Claims Service, Insurance Information Institute

$ BillionsCAT Losses for 2001 Set a Record

•20 events (lowest since 1969)•1.5 million claims

•9/11: $20.3B = 51,000 claims

International Stock Markets:YTD Performance (%)

As of 12 November 2002

-40

-30

-20

-10

0

U.S. Canada U.K. France Germany Italy Japan

(% YTD Return)

Source: Dow Jones

The slide in equity markets has been felt more acutely by European and life

companies because of the higher proportion of equities held.

-30%

-20%

-10%

0%

10%

20%

30%

40%

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

*

*As of November 1, 2002.Source: Ibbotson Associates, Insurance Information Institute

US: Total Returns for Large Company Stocks: 1970-2002*

Headed for 3rd consecutive year of decline for stocks

Last happened 1939-1941

Stocks account for just 21% of p/c insurer investments

P/C Industry Investments,by Type (as of Dec. 31, 2001)

Other5%

Bonds66%

Real Est. & Mortgages

1%

Common Stock21%

Cash & ST Secs.6%

Preferred Stock1%

Bond Holdings, by Type

Industrial & Misc. 32.5%

Special Revenue 30.5%

Governments 18.0%

States/Terr/Other 15.4%

Public Utilities 3.1%

Parents/Subs/Affiliates 0.5%

Source: A.M. Best, Insurance Information Institute

Common stock accounts for about 1/5 of invested

assets

$0

$9

$18

$27

$36

$45

75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02

U.S. Net Investment Income

Facts

1997 Peak = $41.5B

2000= $40.7B

2001 = $37.7B

2002E = $35.8B

Source: A.M. Best, Insurance Information Institute

Bil

lion

s

(US

$)

Investment income in 2002 is expected to fall 5% due primarily to historically low interest rates

0%

2%

4%

6%

8%

10%

12%

14%

16%

3-Month T-Bill 1-Yr. T-Bill 10-Year T-Note

U.S. Interest Rates: Lower Than They’ve Been in Decades

*Average for week ending November 1, 2002.Source: Board of Governors, Federal Reserve System; Insurance Information Institute

1. Historically low interest rates are the primary driver behind lower investment yields. Nevertheless, overall insurer investment performance outpaces all major market indices and almost every major category of mutual fund.

2. 66% of the industry’s invested assets are in bonds

Falling Interest Rates Mean Lower Bond Yields for Years to Come

3-Month Yields

3.06%

4.44%

3.65% 3.65% 3.65%

0.10%0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

Canada Japan U.K. Germany France Euroland

Most Recent 2002Year Ago

Source: Blue Chip Economic Indicators, October 2002.

Interest rates are down globally. More room to fall in Europe than

in US or Japan

Accounting Problems are Getting Many Companies into Trouble

•Enron was tip of an iceberg

•Major implications for insurers (p/c and life)

Corporate Governance: Expensive and Hard-Learned Lessons

• Crisis of Confidence—skepticism is on the rise Ratings agencies Analysts Regulators

Investors/Creditors Employees Lawmakers

• Regulatory/Legislative Fallout Unclear SEC is “rudderless”

Enormous number of investigations under way

SEC, State Attorneys General, IRS, DoJ, etc.

Most new SEC cases are against large companies

Many competing reforms from Congress, SEC, A.G.’s., NYSE, NASDAQ, etc.

Collectively are likely to help, at least somewhat

• SEC, Administration & Congressional proposals vary

• Surge in shareholder suits well underway

Financial Restatements Filed

116

160

215233

270

0

50

100

150

200

250

300

1997 1998* 1999* 2000 2001

*ApproximateSources: Huron Consulting Group

The number of financial restatements is rising

even thought the number of publicly traded

companies is falling.

Serious Implications for Insurers

• Insurers exposed to a wide variety of risks:

Investment risk (as institutional investors)

Insurance risk (surety, D&O, E&O, etc.)

Litigation risk (as both plaintiff & defendant)

Accounting Risk

Regulatory risk

Enron-Related Losses for Insurers

Source: Loss estimates from Morgan Stanley as Feb. 8, 2002; Insurance Information Institute.

Surety26%

Multiple7%

D&O1%

Fin. Guarantee

2%Investment

64%

Total Exposure (Life & Non-Life): $3.796 BillionEnron is the biggest bankruptcy in US history ($31B+)

Equity/debt widely-held as S&P 500 company

Biggest impact in institutional investors/creditors

11 Congressional investigations

56 suits against officers & directors

Will spark similar suits

Average U.S. Jury Awards1994 vs. 2000

419759

187 333

1,140 1,185

1,744

1,168

1,727

269698

3,482 3,566

6,817

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

Overall BusinessNegligence

VehicularLiability*

PremisesLiability

MedicalMalpractice

WrongfulDeath

ProductsLiability

($00

0)

1994 2000

Source: Jury Verdict Research; Insurance Information Institute.

Cost of U.S. Tort System($ Billions)

Source: Tillinghast-Towers Perrin; Insurance Information Institute estimates for 2001/2002 assume tort costs equal to 2% of GDP. 2005 forecasts from Tillinghast.

$129 $130$141 $144 $148

$159 $156 $156$167 $169 $179

$198 $204

$298

$0

$50

$100

$150

$200

$250

$300

$350

90 91 92 93 94 95 96 97 98 99 00 01* 02E* 05F

Tort costs consumed 2.0% of GDP annually on average since 1990, expected to rise to 2.4% of GDP by 2005!

Tort costs equaled $636 per person in 2000!

Expected to rise to $1,000 by 2005

Who Will Pay for the US Asbestos Mess?

Source: Tillinghast-Towers Perrin; Insurance Information Institute

US Insurers30%Asbestos

Defendants39%

Foreign Insurers

31%

Estimated Total US Settlements & Expenses = $200 billion

$78 billion $60 billion

$62 billion

Non-Malignant Asbestos Claimants File Most Claims, Get Most $$$

DISTRIBUTION OF CLAIMS

1991-2000

ALLOCATION OF COMPENSATION

1991-2000Lung & Other

Cancers7%

Non-malignant

90%

Meso-thelioma

3%

Source: RAND, Tillinghast-Towers Perrin

Lung & Other

Cancers18%

Non-malignant

65%

Meso-thelioma

17%

THE CHALLENGE OF TERRORISM

Sept. 11 Industry Loss Estimates($ Billions)

Life$2.7 (7% )

Aviation Liability

$3.5 (9% )

Other Liability$10.0 (25% )

Biz Interruption$11.0 (27% )

Property -WTC 1 & 2$3.5 (9% )

Property - Other

$6.0 (15% )

Aviation Hull$0.5 (1% )

Event Cancellation$1.0 (2% )

Workers Comp$2.0 (5% )

Consensus Insured Losses Estimate: $40.2BSource: Insurance Information Institute

Insured Loss Estimates (updated through September 13, 2002)

0

500

1000

1500

2000

2500

3000

3500

$ M

illi

ons

Source: Morgan Stanley, Insurance Information Institute as of September 13, 2002.

Top 20 Groups (pre-tax, net of reinsurance, $ millions)

NOTES:

*Includes $474 mil for American Re

**Includes $289 mil for Converium

***Insurer is bankrupt

Industry Losses Under Proposed Federal Backstop Using 9/11 Scenario

(as proposed/interpreted as of 10/18/02)

$8.75$12.50

$18.75$1.125

$10.

575

$15.

75

$18.

00

$0

$5

$10

$15

$20

$25

$30

Year 1 Year 2 Year 3

($ B

illi

ons)

Industry Retention Surcharge Layer Co-Reinsurance Layer

Source: Insurance Information Institute.

$1.75B Industry Co-Share

Assumes $30B Commercial Prop & WC Loss, $125B “At Risk” Commercial DPW

$2.0B Industry Co-Share

$0.925B Industry Co-Share

$0.125B Industry Co-Share

Total Ind. Loss: $10.875B $14.25B $19.675B

Top 5 Costliest Terrorist Attacks (by insured property loss*)

*Includes business interruption and aviation hull losses.Source: Swiss Re; Insurance Information Institute.

$20,300

$907 $744 $725 $671$0

$5,000

$10,000

$15,000

$20,000

9/11 TerroristAttacks

Bomb NearNatWestTower inLondon

IRA Car BombNear

ManchesterMall

Bomb in WTCGarage

Bomb inLondon

FinancialDistrict

$ Millions, Adjusted to 2001 Price Level

9/11/01

3,056 Killed

4,000 Injured

4/24/93

1 Killed

54 Injured

6/15/96

0 Killed

228 Injured

2/26/93

6 Killed

725 Injured

4/10/92

3 Killed

91 Injured

Oklahoma City bombing in 1995 cost insurers $145 million, killed 166, 467 injured

489487498

565

635612

666

605

375

437

565

363

431

322

440

296304274

395

426

348

250

300

350

400

450

500

550

600

650

700

81 83 85 87 89 91 93 95 97 99 01

Total International Terrorist Attacks(1981-2001)

The number of terrorist attacks in 2001 actual declined!

Source: US Department of State

11 11

24

84

45

0

121

11

21

42

128

37

13

52

21

49

14

111

31

0

4853

35

122

26

2

85

55

98

31

192

20

0

3033

68

3

194

29

4

17

72

0

25

50

75

100

125

150

175

200

96 97 98 99 00 01

International Terrorist Attacks by Region, 1996-2001

Source: US Department of State

ENDOGENOUS INFLUENCES

CyclicalityCapacity/Capital

Reserve DeficienciesPricing

Mergers & Acquisitions

Length of Underwriting Cycle, Selected Countries*

12.03

12.01

10.19

7.39

7.07

5.79

5.73

5.18

4.84

0 3 6 9 12 15

Netherlands

Malaysia

France

U.S.

Japan

Canada

Spain

Australia

Italy

Cycle Length (Years)

Sources: J. Lamm-Tenant and M. Weiss, “International Insurance Cycles” Rational Expectations/Institutional Intervention, Journal of Risk and Insurance, September 1997; R. Chen, K. Wong and H. Lee, “Underwriting Cycles in Asia,”, ibid, March 1999.

*Study found no cycles evident in Austria, Denmark, S. Korea or Taiwan.

RESTORE & REBUILD

DESTROYEDCAPACITY

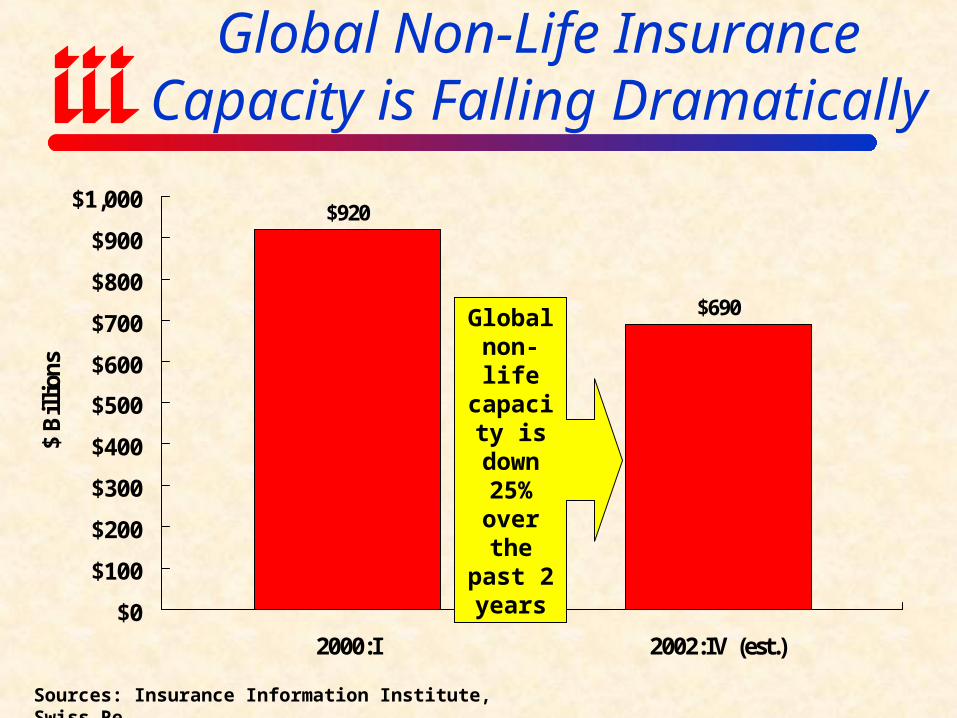

Global Non-Life Insurance Capacity is Falling Dramatically

$920

$690

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

2000:I 2002:IV (est.)

$ B

illi

ons

Sources: Insurance Information Institute, Swiss Re

Global non-life capacity is down

25% over the past 2 years

50%

75%

100%

125%

150%

175%

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

US Canada Germany France

Capital Funds as a Percentage of Net Premium

*

Source: Swiss Re.

Global capital ratios are shrinking

$0

$50

$100

$150

$200

$250

$300

$350

75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02

Policyholder Surplus: 1975-2002*

*As of June 30, 2002Source: A.M. Best, Insurance Information Institute

Bil

lion

s

(US

$)

Surplus (capacity) peaked at $336.3 Billion in mid-1999 and has fallen by 15.9% ($53.4 billion) to $282.9 billion since then.

•Surplus fell 2.3% in the 1st half of 2002

•Surplus is now lower than at year-end 1997.

“Surplus” is a measure of underwriting capacity. It is analogous to “Owners Equity” or “Net Worth” in non-insurance organizations

Capital Raising by Non-Life InsurersWorldwide Since Sept.11, 2001*

$20,492

$11,442

$16,437

$4,872

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

2001 2002*

($ M

illi

on

s)

Completed Pending

$25.4 Billion$27.9 Billion

*As of September 13, 2002.

Source: Morgan Stanley, Insurance Information Institute.

14 Pending 38 Pending

40 Completed 33 Completed

Capital Raising by P/C Insurers Since 9/11 Totals $53.2B

Capital Myth: US P/C Insurers Have $300 Billion to Pay Terrorism Claims

"Target" Commercial*$100 billion

33%

Other Commercial$50 billion

17%

Personal$150 billion

50%

Total PHS = $298.2 B as of 6/30/01

= $282.9 B as of 6/30/02

*”Target” Commercial includes: Comm property, liability and workers comp; Surplus must also back-up on non-terrorist related property/liability and WC claimsSource: Insurance Information Institute

Only 33% of industry surplus backs up “target” lines

U.S. Reserve Deficiency, by Line(AY 1992-2001, as of 12/01)

-$0.8-$1.8

-$4.1

-$6.2

-$9.1

-$3.8

-$0.8

-$17.8 -$18.0

-$1.9

-$20

-$18

-$16

-$14

-$12

-$10

-$8

-$6

-$4

-$2

$0HO PPA Liab CA Liab WC CMP Med Mal*

SpecialLiab

OtherLiab*

XS LiabReins

ProdLiab*

*Occurrence and claims madeSource: Morgan Stanley

Estimated Deficiency

Total Excluding A&E: $64 Billion

A&E Deficiency: $55 Billion

Total Including A&E: $120 Billion

US: Commercial Rate SurveyThird Quarter 2002

Rate Increases By Line of BusinessRate Increases By Line of Business NoNo

Change Up 1-10% 10-20% 20-30% 30-50% 50%-100% >100%Change Up 1-10% 10-20% 20-30% 30-50% 50%-100% >100%

Comm. Auto 6% 18% 37% 24% 12% 0% 0%

Workers Comp 9% 16% 27% 23% 13% 2% 0%

General Liability 8% 13% 38% 28% 9% 1% 0%

Comm. Umbrella 4% 9% 12% 27% 27% 11% 5%

D&O 4% 9% 21% 16% 18% 16% 3%

Comm. Property 8% 9% 30% 23% 21% 5% 0%

Business Interr. 13% 17% 31% 20% 6% 2% 0%

Surety Bonds 16% 13% 17% 20% 2% 0% 1%

Med Mal 5% 3% 5% 6% 17% 11% 19%

Source: Council of Insurance Agents and Brokers

US: Average Price Change of Commercial Insurance Renewals

(Pre-9/11)

9.5%

13.5%

8.8%

10.0%

12.0%

11.0%

8.9%

6.1%

9.5%

8.0%

8.3%

7.9%

9.0%

-1.6%

-1.2%

-0.4%

-7.0%

-6.0%

-11.0%

-6.0%

-10.0%

-7.0%

-3.0%

1.4%

0.8%

3.5%

3.2%

3.2%

2.8%

4.1%

-2.1%

-2.8%

-1.8%

0.2%

-5.0%

-4.4%

-3.5%

-4.3%

-6.6%

-4.1%

-2.0%

-13%

-11%

-9%

-7%

-5%

-3%

-1%

1% 3% 5% 7% 9% 11%

13%

E&S

Umbrella

Workers' Comp

Commercial Property

CMP

General Liability

Commercial Auto

Spring 2001 Fall 2000 Spring 2000 Fall 99 Spring 99 Fall 98

Source: Conning

100110

120130140

150160

170180190

200210220

230240

250260

89 90 91 92 93 94 95 96 97 98 99 00 01 02*

Rate On Line Index(1989=100)

Source: Guy Carpenter * III Estimate

Prices rising, limits falling: ROL up significantly

Insurance Mergers and Acquisitions

7.1 6.9 8.6 5.0 8.5 12.527.0

40.856.2

41.755.7

6.6

41.5

243 246

171 188149

221

349382

433

109

300

295

468

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

89 90 91 92 93 94 95 96 97 98 99 00 01 02*

Val

ue

of M

& A

s ($

Bill

ion

s)

0

100

200

300

400

500

600

Nu

mb

er o

f M

& A

s

Value of Deals Number of Deals

Source: Compiled from Conning & Company reports.

1998: 565 deals valued at $165.4 B

Number of M&As was down 39.4% during the first half of 2002 vs. first half 2001.

Value of deals was down 80.8%.

None of the top deals were in the P/C sector

Insurance Information Institute On-Line

Download or view this presentation at: http://www.iii.org