interim report january – june 2015 - hoist...

TRANSCRIPT

April–June, year-on-year Gross cash collections increased 36 per cent to SEK 834m (615)

Total revenue increased 34 per cent to SEK 537m (401)

EBIT totalled SEK 161m (132)

The EBIT margin was 30 per cent (33)

Profit before tax totalled SEK 52m (56)

Portfolio acquisitions totalled SEK 665m (897)

Basic earnings per share totalled SEK 0.53 (0.79) Diluted earnings per share totalled SEK 0.51 (0.66)1)

Financial net amounted to an expense of SEK 109m (expense: 76) and was charged with an expense of SEK 4m (expense: 7) related to currency and interest hedges

30 June, year-on-year The carrying value of acquired loans2) increased 22 per cent to SEK 9,040m (7,386)

Gross 120-month ERC (Estimated Remaining Collections) increased 26 per cent to SEK 15,316m (12,182)

The total capital ratio improved to 15.28 per cent (12.74)

The CET1 ratio was 12.58 per cent (9.24)

Subsequent events Hoist Finance acquired an extensive and diversified loan portfolio on 1 July 2015

for a total investment of SEK 1,256m

SEKmQuarter 2

2015Quarter 2

2014Change

%Jan–Jun

2015Jan–Jun

2014Change

%

Gross cash collections 834 615 36 1,625 1,151 41Net revenue from acquired loan portfolios 477 347 37 912 653 40Total revenue 537 401 34 1,036 759 37EBIT* 161 132 22 276 253 9EBIT margin, % 30 33 –3 pp 27 33 –7 pp Profit before tax 52 56 –6 59 106 –44Net profit 44 44 0 48 82 –41Basic earnings per share, SEK1) 0.53 0.79 N/A 0.58 – N/A Diluted earnings per share, SEK1) 0.51 0.66 N/A 0.57 – N/A Acquisition of loan portfolios 665 897 –24 938 1,330 –29

* The Jan-Jun 2015 period includes IPO costs of SEK 46m that have a negative impact on EBIT.

30 Jun 2015

30 Jun 2014

Change%

31 Dec 2014

Carrying value of acquired loans, SEKm2) 9,040 7,386 22 8,921Gross 120-month ERC, SEKm3) 15,316 12,182 26 15,576Return on equity, % 11 16 –5 pp 16Total capital ratio, % 15.28 12.74 3 pp 12.17CET1 ratio, % 12.58 9.24 3 pp 9.35Liquidity ratio, % 59 41 18 pp 50Number of employees (FTEs) 1,174 792 48 1,077

Hoist Finance AB (publ) (the “Company” or the “Parent”) is the parent company of the Hoist Finance group of companies (“Hoist Finance”). The Company’s wholly owned subsidiary, Hoist Kredit AB (publ) (“Hoist Kredit”) is a regulated credit market company. Hence, Hoist Finance produces financial statements in accordance with the guidance and format set forth in the Swedish Annual Accounts Act for Credit Institutions and Securities Companies. In order to assess the operational performance of the debt purchasing and collection operations and to facilitate comparison with our competitors, Hoist Finance supplements its statutory financial statements with an operating income statement. The operating income statement is prepared based on the accounting and valuation principles used in the statutory financial statements, with no amendments or adjustments thereto.

The information in this interim report has been published pursuant to the Swedish Securities Market Act and/or Swedish Financial Instruments Trading Act. This information was submitted for publication on 31 July 2015 at 8.00 A.M. (CET).

Interim report January – June 2015

Gross cash collections

SEK 834m

Acquisition of loan portfolios

SEK 665m

EBIT margin

30%CET1 ratio

12.58%

1) Includes effect of 983,913 outstanding warrants.

2) Including run-off consumer loan portfolio and portfolios held in joint venture.

3) Excluding run-off consumer loan portfolio and portfolios held in joint venture.

Second quarter

Hoist Finance AB (publ) • Interim report January – June 2015 2

Statement by the CEO

Continued stable earnings trend and high market activity

Hoist Finance continued its stable growth with a good earnings trend

during the second quarter of 2015. Gross as well as net revenue from

acquired loan portfolios was the highest ever, as was total revenue.

EBIT was up 22 per cent year-on-year.

The EBIT margin was impacted by the rise in legal collections during

the quarter, particularly in the UK. This has increased costs in the short

term according to plan.

High market activity and the single largest acquisition to dateThe second quarter was primarily distinguished by high market activity

with negotiations and acquisitions in multiple markets, including the

acquisitions of loan portfolios in Poland, Italy and Germany. Major

efforts were also focused on preparing for the significant Compello

acquisition in the UK. All of these portfolios will generate revenue as of

the third quarter.

We are very pleased to have completed its single largest transaction

to date on July 1st with the acquisition of debt management company

Compello Holdings. The acquisition includes a diversified banking port-

folio, comprised of over one million overdue loans from 19 financial

institutions and an established collection platform with 178 employ-

ees. At 30 June 2015 the portfolio had estimated collections (ERC) of

approximately SEK 2,823m over 120 months.

This acquisition is highly consistent with our strategy to develop

and strengthen our position in key markets. It also enables us to

increase our operational capacity and thereby consolidate our market

position among core banking customers in the UK.

The acquisition will not give rise to any acquisition goodwill, as the

entire purchase price is related to the debt portfolios. The total invest-

ment is SEK 1,256 million.

Overall, Hoist Finance has thus far this year acquired portfolios

valued at SEK 2.5 billion, including Compello, which is well in line with

our target for 2015.

A growing marketThe supply of non-performing consumer loans is expected to remain

strong due to the growing need of many European banks to divest loan

portfolios. Although the market remains competitive, we have not seen

any discernible changes in pricing during the year. We have, however,

seen greater pricing harmonisation between countries.

Strategy for continued profitable growthIn line with our successful strategy, we will continue to ensure long-

term profitable growth. Our strategy is based on wide geographical

presence, a focused acquisition model based on well-structured pro-

cesses, and long-term instalment plans founded on fair and amicable

settlements.

As always, we focus on deepening our relationships with partners

in existing markets and following them into new markets, while also

working to strengthen our position as a permanent work-out unit

for the largest international banks. We also actively evaluate various

opportunities to enter new European markets.

Another important component of Hoist Finance’s strategy is to have

well-diversified financing through deposits from the public as well as

the bond market. Hoist Finance’s capital adequacy was considerably

strengthened through the new share issues conducted in 2014 and in

conjunction with the IPO in 2015.

As a credit market company Hoist Finance is well versed in what it

means to operate in a regulated environment with internal governance,

risk management and control, and is thus able to meet its partners’

high standards.

OutlookWith a strong financial position and over 20 years’ experience, and as

leading partner to many international banks, Hoist Finance is well po-

sitioned to capitalise on the growing market. We also see good acqui-

sition opportunities during the remainder of the year. Accordingly, our

assessment is that we will achieve or exceed our indicated acquisition

volumes for 2015 – ie, volumes in line with or higher than recent years.

Jörgen Olsson

CEO

Hoist Finance AB (publ)

Hoist Finance AB (publ) • Interim report January – June 2015 3

Second quarter 2015

Second quarter 2015

RevenueGross cash collections increased to SEK 834m (615), chiefly due to the

large portfolio acquisitions made in 2014. Revenue growth remains

stable due to the high level of acquisition activity. Portfolio acquisitions

totalled SEK 665m (897) during the quarter, mainly attributable to

Poland, Italy and Germany, and will start to generate revenue as of the

third quarter.

Portfolio amortisation increased 29 per cent to SEK 360m (278).

The increase is chiefly attributable to the increased volume of acquired

loan portfolios and an normalised collection rate, from the portfolio

acquired in Poland during Q2 2013.

In line with loan amortisation, interest income from the run-off

consumer loan portfolio decreased during the period to SEK 3m (10).

Net revenue from acquired loan portfolios consequently increased

37 per cent to SEK 477m (347).

Fee and commission income increased 8 per cent to SEK 42m (39).

The greater part of this increase is attributable to the UK operations

and to the business in Poland, which has revenues from third-party

cash collection.

Profit from participation in the joint venture in Poland increased

13 per cent to SEK 15m (13).

Total year-on-year revenue increased to SEK 537m (401).

Operating expensesPersonnel expenses increased 39 per cent to SEK 153m (110), due

primarily to greater Group business volumes and to Hoist Finance’s

in-house collection platforms in Italy and Poland following company

acquisitions in those regions.

The Group had 1,174 FTEs (792) as at 30 June 2015. Most of this

increase is attributable to the above-referenced company acquisitions

in Poland and Italy.

Other operating expenses increased 39 per cent during Q2 2015 to

SEK 212m (152). The increase is mainly attributable to the added legal

collection expenses incurred by the UK operations. The remaining

increase is a result of acquisitions and greater business volumes.

Depreciation and amortisation of tangible and intangible fixed

assets totalled SEK 11m (7). The increase is attributable to production

systems acquired in TRC in Italy and to continued investments in Group

IT systems.

Financial itemsFinancial items as per the Company’s segment reporting totalled

SEK –109m (–76). Interest income (excluding run-off consumer loan

portfolio) decreased to SEK –12m (12). This also includes changes in the

market value of interest-bearing securities (Treasury bills, bonds and

other interest-bearing securities) of SEK –13m.

Interest expense totalled SEK 93m (82) and is mainly comprised

of the SEK 49m (51) interest expense related to the deposits offered

by HoistSpar. Due to the adjustment of loan terms to the prevailing

market situation, the rise in deposits from the public has not resulted

in higher interest expense. Also included is an interest expense of

SEK 27m (18) related to the senior unsecured debts, attributable to the

bond issued during Q4 2014. Fees for the deposit guarantee scheme

and stability levy of SEK 8m (8) are also included in interest expense.

Net income from financial transactions totalled SEK –4m (–7), gen-

erated primarily from the hedging of currencies and interest rates via

derivatives (mostly valuation effects from interest derivatives). Hoist

Finance hedges interest rate risk on a continuous basis, currently in the

short and medium term. Some old corporate loans were settled in line

with operational streamlining, giving rise to a loan loss of SEK 5m and

leaving SEK 31m in corporate loans outstanding.

Unless otherwise specified, all market, financial and operational comparisons refer to the second quarter of 2014.The analysis below follows the operating income statement.

0

20

40

60

80

100

120

140

160

180

Q22015

Q22014

Q22013

Gross cash collections

SEKm SEKm SEKm

EBIT and EBIT marginPortfolio acquisitions

SEKm

Profit before tax

0

200

400

600

800

1 000

Kv22015

Kv22014

Kv22013

0

100

200

300

400

500

600

700

800

900

Kv22015

Kv22014

Kv22013

0

20

40

60

80

100

120

140

160

180

Kv22015

Kv22014

Kv22013

0

5

10

15

20

25

30

35

40

45

0

10

20

30

40

50

60

Kv22015

Kv22014

Kv22013

0

200

400

600

800

1,000

Q22015

Q22014

Q22013

0

100

200

300

400

500

600

700

800

900

Q22015

Q22014

Q22013

0

10

20

30

40

50

60

Q22015

Q22014

Q22013

Portföljförvärv

MSEK MSEK MSEK % MSEK

EBIT och EBIT-marginalInkasserade belopp på förvärvade fordringsportföljer Resultat före skatt

EBIT

0

5

10

15

20

25

30

35

40

45%

EBIT margin

EBIT

EBIT-marginal

Hoist Finance AB (publ) • Interim report January – June 2015 4

Second quarter 2015

Cash flow

SEKmQuarter 2

2015Quarter 2

2014Jan–Jun

2015Jan–Jun

2014

Cash flow from operating activities 284 –1,009 1 428 –1,793Cash flow from investing activities –661 –360 –1 447 –162Cash flow from financing activities –11 300 739 374Cash flow for the period –387 –1,069 720 –1,581

Cash flow from operating activities improved to SEK 284m (–1,009)

due to higher deposit volumes in HoistSpar and improved cash flow

of payments from acquired loan portfolios. HoistSpar is a competitive

product on the deposit market and Hoist Finance sees stable growth in

increased volumes as well as new customers. The SEK 412m increase in

deposit volumes during the second quarter was entirely attributable

to deposits on fixed terms of 12, 24 and 36 months. The cash flow of

payments from acquired loan portfolios increased to SEK 834m (615)

and portfolio acquisitions totalled SEK 604m (1,093).

Cash flow from investing activities, including translation differences,

totals SEK –661m (–360). The change is due to increased investments

in bonds and other securities as a result of improved cash flow from

operating activities.

Cash flow from financing activities totals SEK –11m (300) and is

comprised of a warrant buy-back and interest paid on convertible debt

instruments.

Total cash flow for the quarter totals SEK –387m (–1,069).

Balance SheetTotal assets increased 50 per cent to SEK 17,403m (11,615). The increase

is primarily attributable to an SEK 1,868m (128%) increase in bonds

and other securities, an SEK 1,724m (25%) increase in loan portfolio

carrying value, and an SEK 465m (37%) increase in Treasury bills and

Treasury bonds.

Total liabilities amount to SEK 15,255m (10,410). The increase is

mainly due to an SEK 3,855m (43%) increase in deposit volumes and an

additional bond issue of SEK 718m (97%).

Funding and capital structure

SEKm30 Jun

201530 Jun

2014Change

%31 Dec

2014

Deposits from the public 12,768 8,913 43 10,987Subordinated liabilities 335 331 1 333Senior unsecured debt 1,459 740 97 1,493

Total interest-bearing liabilities 14,562 9,984 46 12,813

Other liabilities 693 426 61 852Shareholders' equity 2,148 1,205 79 1,397Total liabilities and shareholders' equity 17,403 11,615 50 15,062

Cash and interest- bearing securities 7,654 3,803 101 5,560Other assets 9,749 7,812 25 9,501Total assets 17,403 11,615 50 15,062

Liquidity ratio, % 59 41 18 pp 50

CET1 ratio, % 12.58 9.24 3 pp 9.35Total capital ratio, % 15.28 12.74 2 pp 12.17

Acquired loansPortfolio acquisitions 938 1,330 –29 3,227Carrying value of acquired loans1 9,040 7,386 22 8,921Gross 120-month ERC2) 15,316 12,186 26 15,576

1) Including run-off consumer loan portfolio and portfolios held in joint venture.2) Excluding run-off consumer loan portfolio and portfolios held in joint venture.

Hoist Finance funds its operations through deposits from the public

and through the bond market. Deposits from the public total SEK

12,768m (8,913). Of this amount, SEK 5,334m is attributable to fixed

term deposits of 12-, 24- and 36-month durations. In line with its

funding structure diversification strategy, Hoist Finance issued a bond

denominated in EUR in 2014. As at 30 June 2015, outstanding bond

debt totalled SEK 1,459m.

Group equity totals SEK 2,148m (1,205). The capital base was

strengthened substantially through the new share issues in 2014 and

the new share issue in connection with the listing.

The total capital ratio improved to 15.28 (12.74) per cent and the

CET1 (Common Equity Tier 1) ratio to 12.58 (9.24) per cent. The Com-

pany is thus well capitalised for further expansion in the acquisition of

non-performing consumer loans.

Cash and interest-bearing securities total SEK 7,654m (3,809). The

liquidity ratio is 59 (41) per cent of deposits from the public.

Basic earnings per share total SEK 0.53 (0.79). Interest on the subor-

dinated liabilities is included in the calculation.

Hoist Finance AB (publ) • Interim report January – June 2015 5

Second quarter 2015

Risk developmentHoist Finance had a year-on-year volume increase in loan portfolios of

approximately SEK 1,724m at the close of Q2 2015, attributable mainly

to portfolio acquisitions in Poland, Italy and Germany.

Loan portfolio credit risk is deemed to have increased during Q2

2015 proportionally with the volume of acquired loans. Portfolio credit

quality is still deemed good.

Operational risks increased (although at a lower rate than growth)

as a result of acquisitions and greater business volumes. The main

reasons for the increase are deemed to stem from increased risks (in

the form of systems integrations and differences in corporate cultures)

associated with the integration of acquired companies, and legal and

tax risks associated with the Group operating in several European

countries. Hoist Finance has limited these risks through increased fo-

cus on the quality of internal processes and will continue working this

year on quality improvements in various areas.

Hoist Finance’s capital position in terms of the CET1 and total cap-

ital ratios increased significantly year-on-year, due in part to business

growth during Q2 2015. Also, due to the reallocation of liquid assets re-

sulting from the Compello Holdings Ltd acquisition, the Company holds

capital as of the close of June to cover around half of its acquisition

volume. The capital ratio improved significantly year-on-year, mainly

due to new share issues conducted in 2014 and at listing in March 2015

and the fact that the company decided to reinvest the profits generated

by the business.

The liquidity ratio increased from 41 per cent to 59 per cent year-

on-year, due primarily to the issuance of a EUR bond, higher deposit

volumes, and the new share issue conducted in connection with listing

during the spring of 2015.

Other informationEmployeesThe Group had 1,174 (792) FTEs during Q2 2015. The year-on-year

increase of 382 FTEs is mainly attributable to the acquisitions in Poland

(182) and Italy (146).

Parent CompanyThe Parent Company reported a small pre-tax loss of SEK –2m (–2).

The share and shareholdersHoist Finance was listed on the NASDAQ Stockholm Mid Cap List on 25

March 2015. The price per share was set at SEK 58, corresponding to a

market capitalisation of SEK 4,555m. As at 30 June 2015 the share price

closed at SEK 62.50.

Ownership structure

Name Capital and votes, %

Swedbank Robur fonder AB 9.1Toscafund Asset Management LLP 9.1Carve Capital AB 9.0Olympus Investment S,àr,l, 7.5Beagle Investments S,A, 7.0Deciso AB 6.1Thoupos Costas 4.2Norges Bank Investment Management 4.1Zenit funds 3.8SHB funds 3.1Carnegie funds 2.5The Confederation of Swedish Enterprise 1.9Echiquier funds 1.9Per Josefsson Invest AB 1.7Skandia Liv 1.3Other shareholders 27.7Total 100.0

Source: SIS Ownership Service, 30 June 2015

Subsequent eventsAfter the close of the period Hoist Finance acquired an extensive and

diversified loan portfolio in the UK through the shares in Compello

Holdings Limited. The acquisition includes a diversified portfolio of

claims on banks, comprised of over one million overdue loans from 19

financial institutions and an established call centre with 178 employees.

At 30 June 2015 the portfolio has estimated collections of approxi-

mately SEK 2,823m over 120 months (ERC). The total investment is SEK

1,256m. Following the acquisition the CET1 capital adequacy ratio for

the second quarter changed from 12.58 to 11.67 pro forma.

ReviewThis interim report has not been reviewed by the Company’s auditor.

Hoist Finance AB (publ) • Interim report January – June 2015 6

Quarterly overview

Quarterly overview

Segment reporting

SEK thousandQuarter 2

2015Quarter 1

2015Quarter 4

2014Quarter 3

2014Quarter 2

2014

Gross cash collections 834,098 790,735 750,218 640,091 615,479Portfolio amortisation and revaluation –360,477 –358,925 –339,425 –284,861 –278,348Interest income from run-off consumer loan portfolio 2,994 3,118 5,641 11,907 9,566

Net revenue from acquired loan portfolios 476,615 434,928 416,434 367,137 346,697Fee and commission income 41,747 47,616 39,467 36,881 39,111Earnings from participations in joint ventures 14,946 15,350 17,918 15,671 13,203Other income 3,439 1,546 5,904 2,226 2,205

Total revenue 536,747 499,440 479,723 421,915 401,216 Personnel expenses –153,016 –145,666 –132,299 –122,225 –110,255Other operating expenses –211,764 –227,741 –188,040 –166,043 –151,843Depreciation and amortisation of tangible and intangible assets –10,859 –10,753 –9,623 –6,880 –7,267

Total operating expenses –375,639 –384,160 –329,962 –295,148 –269,365 EBIT 161,108 115,280 149,761 126,767 131,851 Interest income excl. run-off consumer loan portfolio –12,111 4,745 7,525 21,462 12,284Interest expense –92,876 –92,621 –93,437 –85,498 –81,653Net income from financial transactions –3,779 –20,259 –16,321 2,507 –6,518

Total financial items –108,766 –108,135 –102,233 –61,529 –75,887 Profit before tax 52,342 7,145 47,528 65,238 55,964

Key ratios, segment reporting

SEKmQuarter 2

2015Quarter 1

2015Quarter 4

2014Quarter 3

2014Quarter 2

2014

EBIT margin, % 30 23 31 30 33Portfolio acquisitions 665 273 1 544 353 897Carrying value of acquired loans 9,040 8,827 8,921 7,504 7,386CET1 ratio, % 12.58 14.33 9.35 8.99 9.24Gross 120-month ERC1) 15,316 15,238 15,576 12,657 12,182

1) Excluding run-off consumer loan portfolio and portfolios held in joint venture.

Hoist Finance AB (publ) • Interim report January – June 2015 7

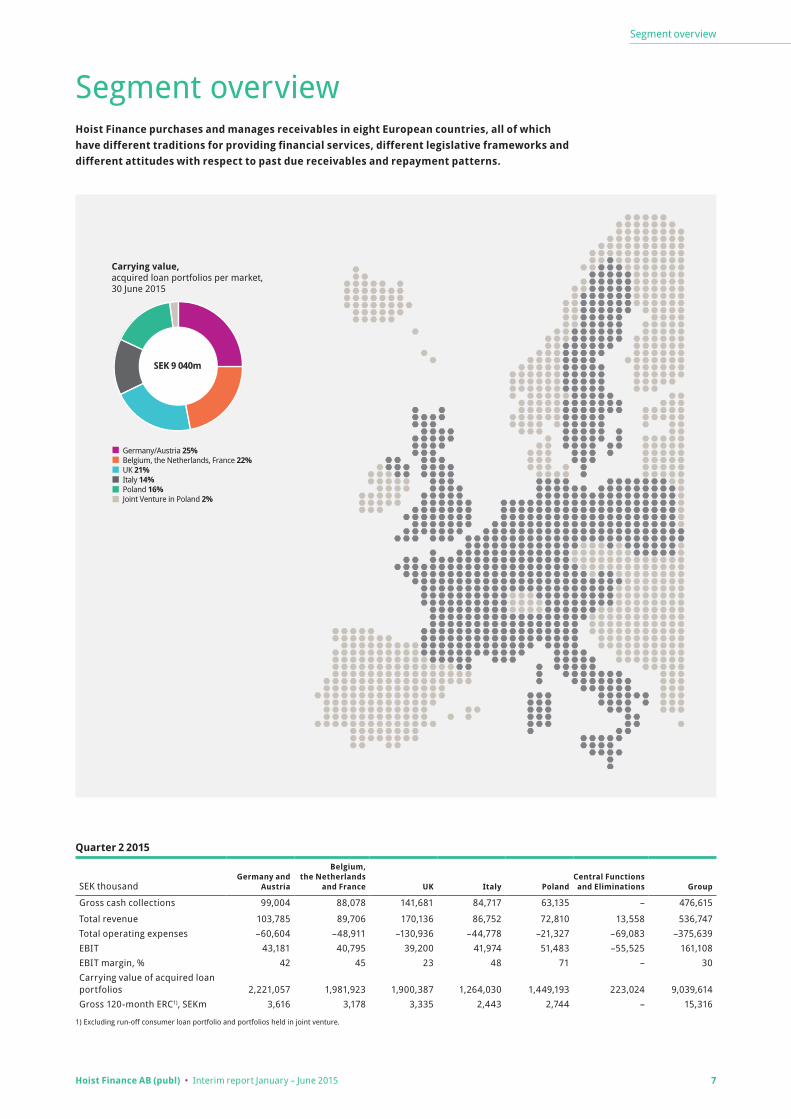

Segment overview

Segment overviewHoist Finance purchases and manages receivables in eight European countries, all of which have different traditions for providing financial services, different legislative frameworks and different attitudes with respect to past due receivables and repayment patterns.

Quarter 2 2015

SEK thousandGermany and

Austria

Belgium, the Netherlands

and France UK Italy PolandCentral Functions and Eliminations Group

Gross cash collections 99,004 88,078 141,681 84,717 63,135 – 476,615

Total revenue 103,785 89,706 170,136 86,752 72,810 13,558 536,747Total operating expenses –60,604 –48,911 –130,936 –44,778 –21,327 –69,083 –375,639EBIT 43,181 40,795 39,200 41,974 51,483 –55,525 161,108EBIT margin, % 42 45 23 48 71 – 30Carrying value of acquired loan portfolios 2,221,057 1,981,923 1,900,387 1,264,030 1,449,193 223,024 9,039,614Gross 120-month ERC1), SEKm 3,616 3,178 3,335 2,443 2,744 – 15,316

1) Excluding run-off consumer loan portfolio and portfolios held in joint venture.

Carrying value, acquired loan portfolios per market, 30 June 2015

Germany/Austria 25%Belgium, the Netherlands, France 22%UK 21%

Poland 16%Joint Venture in Poland 2%

Italy 14%

SEK 9 040m

Hoist Finance AB (publ) • Interim report January – June 2015 8

Segment overview

Germany and Austria

SEK thousandQuarter 2

2015Quarter 2

2014Change

%Jan–Jun

2015Jan–Jun

2014Change

%Full year

2014

Gross cash collections 210,312 155,454 35 461,906 309,572 49 724,044Portfolio amortisation and revaluation –114,302 –84,250 36 –264,923 –154,423 72 –348,873Interest income from run-off consumer loan portfolio 2,994 9,566 –69 6,112 20,633 –70 38,180

Net revenue from acquired loan portfolios 99,004 80,770 23 203,095 175,782 16 413,351Fee and commission income 1,416 4,469 –68 4,095 9,061 –55 17,889Other income 3,365 2,979 13 4,527 4,143 9 14,294

Total revenue 103,785 88,218 18 211,717 188,986 12 445,534

Personnel expenses –35,781 –32,687 9 –71,676 –64,492 11 –133,245Other operating expenses –23,954 –20,040 20 –46,151 –35,357 31 –85,272Depreciation and amortisation of tangible and intangible assets –869 –708 23 –1,744 –1,416 23 –2,940

Total operating expenses –60,604 –53,435 13 –119,571 –101,265 18 –221,457

EBIT 43,181 34,783 24 92,146 87,721 5 224,077

EBIT margin, % 42 39 3 pe 44 46 –2 pe 50Expenses/Gross cash collections, % 26 28 –2 pe 24 27 –3 pe 25Carrying value of acquired loan portfolios1) 2,221,057 2,010,265 10 N/A N/A – 2,350,392Gross 120-month ERC, SEKm2) 3,616 3,235 12 N/A N/A – 3,817

1) Including run-off consumer loan portfolio. 2) Excluding run-off consumer loan portfolio.

Operating incomeGross cash collections increased 35 per cent during the second quarter

to SEK 210m (155). This increase is largely attributable to two large

acquisitions. Portfolio amortisation totalled SEK 114m (84) during the

quarter, with the increase due to a higher collection rate. Revenues

from the run-off consumer loan portfolio decreased to SEK 3m (10)

in pace with gradual amortisation of the portfolio. Fee and commis-

sion income was lower year-on-year, due primarily to Hoist Finance’s

acquisition of a significant portfolio it had previously serviced for a

third party.

Operating expensesSecond quarter operating expenses increased to SEK 61m (53). Most

of the increase is attributable to collection expenses, including fees

payable to partners and initiation of legal proceedings. Some internal

functions located in Germany were reclassified as Group functions

during Q2 2015 and, as a result, costs associated with these functions

are now included in the Central Functions operating segment. The

carrying costs for the current and previous years have been reclassi-

fied accordingly.

EBITThe segment’s EBIT totalled SEK 43m (35) for the quarter with a cor-

responding EBIT margin of 42 per cent (39). The profitability improve-

ment is attributable to increased collections, with operating expenses

increasing to a lesser extent.

AcquisitionsSecond quarter acquisition activity was higher year-on-year. The carry-

ing value of acquired loan portfolios was SEK 2,221m (2,010) at 30 June

2015. Gross ERC for the same period totalled SEK 3,616m (3,235).

OtherAlthough Austria currently represents a small portion of the segment,

Hoist Finance continues to consider it an attractive market. Due to the

acquisitions made during the second half of 2014, revenue contribution

was higher than last year despite the fact that no acquisitions were

made during the second quarter.

The earnings trend for each operating segment, excluding Central Functions and Eliminations, is set forth below.

Hoist Finance AB (publ) • Interim report January – June 2015 9

Segment overview

Belgium, the Netherlands and France

SEK thousandQuarter 2

2015Quarter 2

2014Change

%Jan–Jun

2015Jan–Jun

2014Change

%Full year

2014

Gross cash collections 234,349 192,280 22 412,037 350,168 18 733,474Portfolio amortisation and revaluation –146,271 –115,263 27 –251,499 –220,230 14 –484,991

Net revenue from acquired loan portfolios 88,078 77,017 14 160,538 129,938 24 248,483Fee and commission income 1,636 1,755 –7 3,451 3,373 2 6,989Other income –8 0 N/A –8 0 N/A 218

Total revenue 89,706 78,772 14 163,981 133,311 23 255,690

Personnel expenses –21,389 –21,530 –1 –45,831 –40,382 13 –86,886Other operating expenses –27,011 –23,264 16 –50,931 –44,158 15 –102,656Depreciation and amortisation of tangible and intangible assets –511 –998 –49 –1,320 –1,866 –29 –4,679

Total operating expenses –48,911 –45,792 7 –98,082 –86,406 14 –194,221

EBIT 40,795 32,980 24 65,899 46,905 40 61,469

EBIT margin, % 45 42 3 pe 40 35 5 pe 24Expenses/Gross cash collections, % 20 23 –3 pe 23 24 –1 pe 251)

Carrying value of acquired loan portfolios 1,981,923 2,084,060 –5 N/A N/A – 2,194,000

Gross 120-month ERC, SEKm 3,178 3,423 –7 N/A N/A – 3,512

1) Excluding non-recurring expenses.

Operating incomeSecond quarter gross cash collections increased 22 per cent to SEK

234m (192) and portfolio amortisation increased to SEK 146m (115).

Belgium is responsible for a large part of the increase in both gross

cash collections and portfolio amortisation, with unusually large VAT

recoveries contributing to high collection levels. The Netherlands also

had good second quarter revenues, buoyed somewhat by seasonal

fluctuations. Fee and commission income originated from third-party

services offered via the French operations.

Operating expensesOperating expenses for the second quarter total SEK 49m (46). The

increase is primarily attributable to the Netherlands, which saw an

increase in both the number of employees and the collection activity

level. Restructuring efforts have continued in France, and support

functions were migrated from the Guyancourt office to the Lille office

established by Hoist Finance in 2014. As of the close of Q2 Hoist

Finance has no employees in Guyancourt and has closed its office

there, which is seen in the lower personnel expenses in France.

EBITThe segment’s EBIT totalled SEK 41m (33) for the quarter with a corre-

sponding EBIT margin of 45 per cent (42).

AcquisitionsThe segment’s acquisitions during Q2 2015 were conducted predomi-

nantly in the Netherlands, with only an insignificant portion conducted

in France and Belgium. Overall, the segment’s acquired volumes are

lower year-on-year. This does not apply to the French market, however,

where acquired volumes (including acquisitions concluded during early

Q3) already exceed full-year 2014. The carrying value of acquired loan

portfolios totalled SEK 1,982m (2,084) at 30 June 2015. Gross ERC for

the same period decreased to SEK 3,178M (3,423).

Hoist Finance AB (publ) • Interim report January – June 2015 10

Segment overview

Great Britain

SEK thousandQuarter 2

2015Quarter 2

2014Change

%Jan–Jun

2015Jan–Jun

2014Change

%Full year

2014

Gross cash collections 162,516 125,220 30 314,144 257,898 22 527,346Portfolio amortisation and revaluation –20,835 –52,380 –60 –59,253 –106,867 –45 –200,802

Net revenue from acquired loan portfolios 141,681 72,840 95 254,891 151,031 69 326,544Fee and commission income 27,379 32,887 –17 60,548 64,440 –6 128,344Other income 1,076 141 663 1,082 558 94 2,686

Total revenue 170,136 105,868 61 316,521 216,029 47 457,574

Personnel expenses –41,383 –30,490 36 –78,649 –63,392 24 –134,502Other operating expenses –88,682 –33,288 166 –150,911 –71,244 112 –137,601Depreciation and amortisation of tangible and intangible assets –871 –1,750 –50 –1,726 –3,081 –44 –4,588

Total operating expenses –130,936 –65,528 100 –231,286 –137,717 68 –276,691

EBIT 39,200 40,340 –3 85,235 78,312 9 180,883

EBIT margin, % 23 38 –15 pe 27 36 –9 pe 40Expenses/Gross cash collections, % 63 26 37 pe 54 28 26 pe 281)

Carrying value of acquired loan portfolios 1,900,387 1,438,361 32 N/A N/A – 1,797,520Gross 120-month ERC, SEKm 3,335 2,496 34 N/A N/A – 3,391

1) ) Excluding non-recurring expenses.

Operating incomeGross cash collections during the second quarter totalled SEK 163m

(125). The change is chiefly attributable to loan portfolios acquired dur-

ing the second half of 2014 and to a favourable currency trend. Port-

folio amortisation totalled SEK 21m (52). Due to an initially high cost

burden for a large portfolio acquired during Q4 2014, the amortisation

rate remained relatively low during the quarter. The portfolio also has

an impact on Other operating expenses. Fee and commission income,

derived from services offered to third parties, has declined as the UK

operations have been adapted to Hoist Finance’s strategy focused on

loan portfolio acquisitions.

Operating expensesOperating expenses increased 100 per cent on a quarterly basis to

SEK 131m (66). Increased personnel expenses are a consequence of

Hoist Finance adjusting its workforce to acquired business volumes.

The increase in Other operating expenses is mostly attributable to a

rise in legal collection expenses and the negative (from a cost perspec-

tive) currency trend.

EBITThe segment’s EBIT totalled SEK 39m (40) for the quarter with a corre-

sponding EBIT margin of 23 per cent (38).

AcquisitionsExtensive work was carried out during the second quarter in prepara-

tion for the acquisition of Compello Holdings, completed during the

first days of Q3. The year-on-year acquisition level was lower but, in

terms of future collections, the strong start to Q3 will more than com-

pensate for this. The carrying value of acquired loan portfolios totalled

SEK 1,900m (1,438) at 30 June 2015. Gross ERC for the same period

increased to SEK 3,335m (2,496).

OtherThe acquired debt purchase company, Compello Holdings Limited,

adds a diversified portfolio of claims on banks, comprised of over one

million overdue loans from 19 financial institutions and an established

call centre with 178 employees. At 30 June 2015 the portfolio has esti-

mated collections (ERC) of approximately SEK 2,823m over 120 months.

Hoist Finance AB (publ) • Interim report January – June 2015 11

Segment overview

Italy

SEK thousandQuarter 2

2015Quarter 2

2014Change

%Jan–Jun

2015Jan–Jun

2014Change

%Full year

2014

Gross cash collections 127,465 60,769 110 250,952 110,920 126 260,828Portfolio amortisation and revaluation –42,748 –22,522 90 –87,726 –46,438 89 –91,324

Net revenue from acquired loan portfolios 84,717 38,247 121 163,226 64,482 153 169,504Fee and commission income 1,705 – N/A 2,912 – N/A 0Other income 330 – N/A 675 – N/A 311

Total revenue 86,752 38,247 127 166,813 64,482 159 169,815

Personnel expenses –14,642 – N/A –27,339 – N/A –17,854Other operating expenses –28,526 –14,249 100 –54,061 –23,468 130 –86,028Depreciation and amortisation of tangible and intangible assets –1,610 – N/A –3,184 – N/A –2,340

Total operating expenses –44,778 –14,249 214 –84,584 –23,468 260 –106,222

EBIT 41,974 23,998 75 82,229 41,014 100 63,593

EBIT margin, % 48 63 –15 pe 49 64 –15 pe 37Expenses/Gross cash collections, % 34 23 11 pe 32 21 11 pe 41Carrying value of acquired loan portfolios 1,264,030 518,847 144 N/A N/A – 1,181,210Gross 120-month ERC, SEKm 2,443 839 191 N/A N/A – 2,407

Operating incomeGross cash collections in the second quarter increased 110 per cent to

SEK 127m (61). The increase is attributable to the acquisition from TRC

in April 2014 and the large acquisition made in December 2014. Port-

folio amortisation during Q2 totalled SEK 43m (23), with the increase

chiefly due to the above-named December 2014 acquisition. Fees and

commission income and Other income, totalling SEK 2m, relate to

services rendered by the business integrated during Q3 2014.

Operating expensesThe substantial change in operating expenses, which increased 214 per

cent to SEK 45m (14), reflects the fact that Hoist Finance now operates

its own collection platform in Italy, with 146 employees. Integration

of the business and associated IT systems acquired in 2014 resulted in

Hoist Finance’s depreciation of tangible and intangible assets in Italy.

Additionally, Hoist Finance is now implementing extensive collection

activities, both in-house and via external partners, for the substantial

loan portfolios acquired in 2014.

EBITThe segment’s EBIT totalled SEK 42m (24) for the quarter with a corre-

sponding EBIT margin of 48 per cent (63).

AcquisitionsYear-on-year acquisition activity was somewhat lower during the quar-

ter. The carrying value of acquired loan portfolios totalled SEK 1,264m

(519) at 30 June 2015. Gross ERC for the same period increased to SEK

2,443m (839).

Hoist Finance AB (publ) • Interim report January – June 2015 12

Segment overview

Poland

SEK thousandQuarter 2

2015Quarter 2

2014Change

%Jan–Jun

2015Jan–Jun

2014Change

%Full year

2014

Gross cash collections 99,456 81,756 22 185,794 122,444 52 295,619Portfolio amortisation and revaluation –36,321 –3,933 823 –56,001 9,224 N/A –17,030

Net revenue from acquired loan portfolios 63,135 77,823 –19 129,793 131,668 –1 278,589Fee and commission income 9,611 – N/A 18,357 – N/A –Other income 64 – N/A 97 0 N/A 0

Total revenue 72,810 77,823 –6 148,247 131,668 13 278,589

Personnel expenses –5,208 –475 996 –10,404 –878 N/A –2,035Other operating expenses –15,155 –16,750 –10 –29,570 –28,139 5 –74,812Depreciation and amortisation of tangible and intangible assets –964 –27 N/A –1,745 –27 N/A 0

Total operating expenses –21,327 –17,252 24 –41,719 –29,044 44 –76,847

EBIT 51,483 60,571 –15 106,528 102,624 4 201,742

EBIT margin, % 71 78 –7 pe 72 78 –6 pe 72Expenses/Gross cash collections, % 12 21 –9 pe 13 24 –11 pe 26Carrying value of acquired loan portfolios 1,449,193 1,114,723 30 N/A N/A – 1,182,459Gross 120-month ERC, SEKm 2,744 2,189 25 N/A N/A – –2,449

Operating incomeSecond quarter gross cash collections increased 22 per cent to SEK 99m

(82). The rate of increase in portfolio amortisation (considerably higher

than the increase in gross cash collections) is chiefly attributable to a

large portfolio acquired during Q2 2013. The amortisation rate has nor-

malised with the increase in this portfolio’s cash flow. The increase in

fee and commission income is due entirely to services offered to third

parties by Navi Lex, acquired by Hoist Finance during Q4 2014.

Operating expensesFor the past year Hoist Finance has managed the Polish operations in

accordance with a business model that involves many more in-house

activities. In contrast to Q2 2014 when the workforce was comprised of

a small Warsaw sales office, Hoist Finance employed 186 FTEs in Poland

as at 30 June 2015. Because there were 152 FTEs at the beginning of the

quarter, personnel expenses for the quarter do not fully correspond to

the cost of 186 FTEs.

Employees in Poland also perform services for third parties, al-

though the emphasis has shifted as the management of Hoist Finance’s

portfolios has been gathered in the internal platform. Accordingly,

expenses that were previously Other external operating expenses

are shifting to Internal personnel expenses. Total operating expenses

increased 24 per cent to SEK 21m (17).

EBITThe segment’s EBIT totalled SEK 51m (61) for the quarter with a corre-

sponding EBIT margin of 71 per cent (78). The relatively low operating

expenses as compared with gross cash collections reflect a profitable

market in which we have historically acquired portfolios with relatively

good returns.

AcquisitionsAcquisition activity picked up significantly during the second quarter

following a cautious start to the year. The total acquisition volume for

the first half of 2015 exceeds the corresponding period for 2014. The

carrying value of acquired loan portfolios totalled SEK 1,449m (1,115).

Gross ERC for the same period increased to SEK 2,744m (2,189).

OtherThe activity plan for an additional portfolio was reviewed and expense

and gross cash collection forecasts were updated during the second

quarter as part of the continued integration of Navi Lex. One effect of

this is an increase of SEK 6m in the portfolio’s amortisation. This reval-

uation is included in the second quarter figures for Portfolio amortisa-

tion and revaluation.

Hoist Finance AB (publ) • Interim report January – June 2015 13

Financial statements

Consolidated income statement

SEK thousand NoteQuarter 2

2015Quarter 2

2014Jan–Jun

2015Jan–Jun

2014Full year

2014

Net revenues from acquired loan portfolios 1 473,621 337,131 905,431 632,268 1,398,291

Interest income –9,117 21,850 –1,254 43,196 89,731

Interest expense –92,876 –81,653 –185,497 –166,034 –344,969

Net interest income 371,628 277,328 718,680 509,430 1,143,053

Fee and commission income 41,747 39,111 89,363 76,874 153,222

Net income from financial transactions 1,519 –6,518 –18,740 –3,905 –17,719

Other income 3,439 2,205 4,985 4,089 12,219

Total operating income 418,333 312,126 794,288 586,488 1,290,775

General administrative expenses

Personnel expenses –153,016 –110,255 –298,682 –218,676 –473,200

Other operating expenses –211,764 –151,843 –439,505 –273,383 –627,467

Depreciation and amortisation of tangible and intangible assets –10,859 –7,267 –21,612 –13,778 –30,281

Total operating expenses –375,639 –269,365 –759,799 –505,837 –1,130,948

Profit before credit losses 42,694 42,761 34,489 80,651 159,827Net credit losses –5,298 – –5,298 – –

Earnings from participations in joint ventures 14,946 13,203 30,296 25,073 58,662

Profit before tax 52,342 55,964 59,487 105,724 218,489

Income tax expense –8,178 –12,266 –11,683 –23,522 –38,386

Profit for the period 44,164 43,698 47,804 82,202 180,103

Profit attributable to:Owners of Hoist Finance AB (publ) 44,164 43,698 47,804 82,202 180,103

Basic earnings per share1) 0.53 0.79 0.58 – 9.21

Diluted earnings per share1) 2) 0.51 0.66 0.57 – 8.16

1) A 1:3 split was conducted in February 2015.2) Includes effect of 983,913 outstanding warrants.

Financial statements

Hoist Finance AB (publ) • Interim report January – June 2015 14

Financial statements

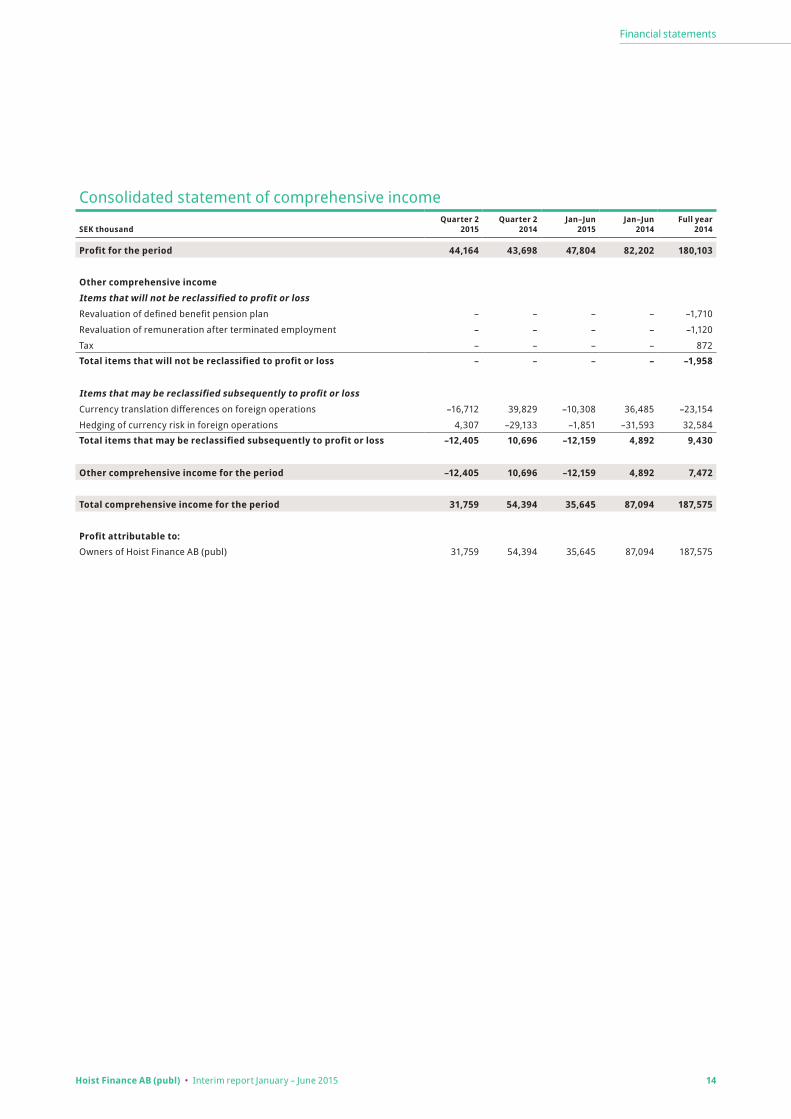

Consolidated statement of comprehensive income

SEK thousandQuarter 2

2015Quarter 2

2014Jan–Jun

2015Jan–Jun

2014Full year

2014

Profit for the period 44,164 43,698 47,804 82,202 180,103

Other comprehensive incomeItems that will not be reclassified to profit or lossRevaluation of defined benefit pension plan – – – – –1,710

Revaluation of remuneration after terminated employment – – – – –1,120

Tax – – – – 872

Total items that will not be reclassified to profit or loss – – – – –1,958

Items that may be reclassified subsequently to profit or lossCurrency translation differences on foreign operations –16,712 39,829 –10,308 36,485 –23,154

Hedging of currency risk in foreign operations 4,307 –29,133 –1,851 –31,593 32,584

Total items that may be reclassified subsequently to profit or loss –12,405 10,696 –12,159 4,892 9,430

Other comprehensive income for the period –12,405 10,696 –12,159 4,892 7,472

Total comprehensive income for the period 31,759 54,394 35,645 87,094 187,575

Profit attributable to:Owners of Hoist Finance AB (publ) 31,759 54,394 35,645 87,094 187,575

Hoist Finance AB (publ) • Interim report January – June 2015 15

Financial statements

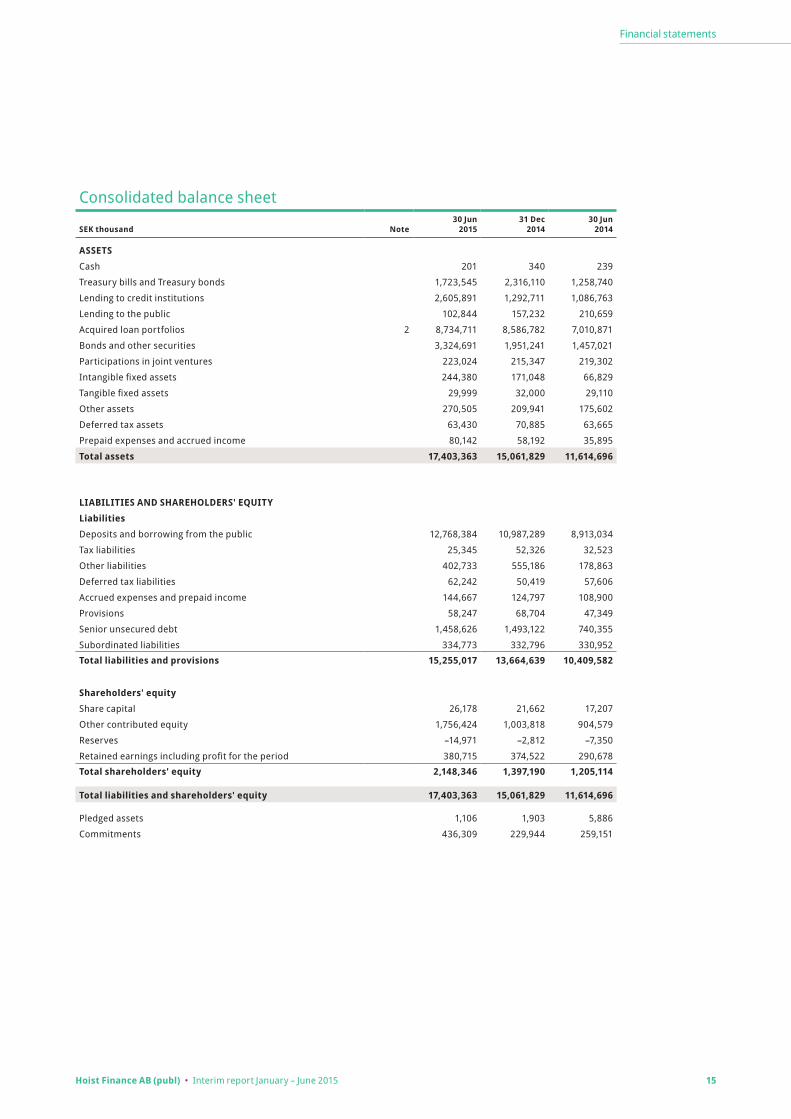

Consolidated balance sheet

SEK thousand Note30 Jun

201531 Dec

201430 Jun

2014

ASSETSCash 201 340 239

Treasury bills and Treasury bonds 1,723,545 2,316,110 1,258,740

Lending to credit institutions 2,605,891 1,292,711 1,086,763

Lending to the public 102,844 157,232 210,659

Acquired loan portfolios 2 8,734,711 8,586,782 7,010,871

Bonds and other securities 3,324,691 1,951,241 1,457,021

Participations in joint ventures 223,024 215,347 219,302

Intangible fixed assets 244,380 171,048 66,829

Tangible fixed assets 29,999 32,000 29,110

Other assets 270,505 209,941 175,602

Deferred tax assets 63,430 70,885 63,665

Prepaid expenses and accrued income 80,142 58,192 35,895

Total assets 17,403,363 15,061,829 11,614,696

LIABILITIES AND SHAREHOLDERS' EQUITYLiabilitiesDeposits and borrowing from the public 12,768,384 10,987,289 8,913,034

Tax liabilities 25,345 52,326 32,523

Other liabilities 402,733 555,186 178,863

Deferred tax liabilities 62,242 50,419 57,606

Accrued expenses and prepaid income 144,667 124,797 108,900

Provisions 58,247 68,704 47,349

Senior unsecured debt 1,458,626 1,493,122 740,355

Subordinated liabilities 334,773 332,796 330,952

Total liabilities and provisions 15,255,017 13,664,639 10,409,582

Shareholders' equityShare capital 26,178 21,662 17,207

Other contributed equity 1,756,424 1,003,818 904,579

Reserves –14,971 –2,812 –7,350

Retained earnings including profit for the period 380,715 374,522 290,678

Total shareholders' equity 2,148,346 1,397,190 1,205,114

Total liabilities and shareholders' equity 17,403,363 15,061,829 11,614,696

Pledged assets 1,106 1,903 5,886

Commitments 436,309 229,944 259,151

Hoist Finance AB (publ) • Interim report January – June 2015 16

Financial statements

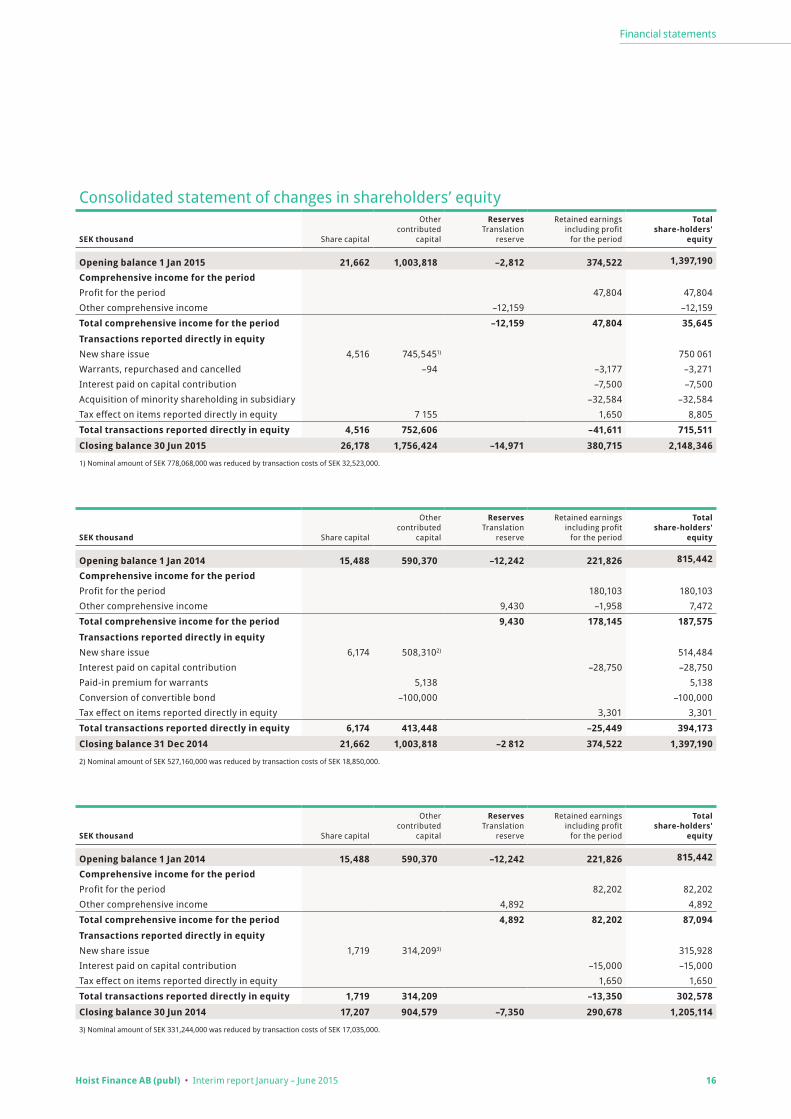

Consolidated statement of changes in shareholders’ equity

SEK thousand Share capital

Other contributed

capital

Reserves Translation

reserve

Retained earnings including profit

for the period

Total share-holders'

equity

Opening balance 1 Jan 2015 21,662 1,003,818 –2,812 374,522 1,397,190

Comprehensive income for the period Profit for the period 47,804 47,804Other comprehensive income –12,159 –12,159

Total comprehensive income for the period –12,159 47,804 35,645Transactions reported directly in equity New share issue 4,516 745,5451) 750 061Warrants, repurchased and cancelled –94 –3,177 –3,271Interest paid on capital contribution –7,500 –7,500Acquisition of minority shareholding in subsidiary –32,584 –32,584Tax effect on items reported directly in equity 7 155 1,650 8,805

Total transactions reported directly in equity 4,516 752,606 –41,611 715,511Closing balance 30 Jun 2015 26,178 1,756,424 –14,971 380,715 2,148,346

1) Nominal amount of SEK 778,068,000 was reduced by transaction costs of SEK 32,523,000.

SEK thousand Share capital

Other contributed

capital

Reserves Translation

reserve

Retained earnings including profit

for the period

Total share-holders'

equity

Opening balance 1 Jan 2014 15,488 590,370 –12,242 221,826 815,442

Comprehensive income for the period Profit for the period 180,103 180,103Other comprehensive income 9,430 –1,958 7,472

Total comprehensive income for the period 9,430 178,145 187,575Transactions reported directly in equity New share issue 6,174 508,3102) 514,484Interest paid on capital contribution –28,750 –28,750Paid-in premium for warrants 5,138 5,138Conversion of convertible bond –100,000 –100,000Tax effect on items reported directly in equity 3,301 3,301

Total transactions reported directly in equity 6,174 413,448 –25,449 394,173Closing balance 31 Dec 2014 21,662 1,003,818 –2 812 374,522 1,397,190

2) Nominal amount of SEK 527,160,000 was reduced by transaction costs of SEK 18,850,000.

SEK thousand Share capital

Other contributed

capital

Reserves Translation

reserve

Retained earnings including profit

for the period

Total share-holders'

equity

Opening balance 1 Jan 2014 15,488 590,370 –12,242 221,826 815,442

Comprehensive income for the period Profit for the period 82,202 82,202Other comprehensive income 4,892 4,892

Total comprehensive income for the period 4,892 82,202 87,094Transactions reported directly in equity New share issue 1,719 314,2093) 315,928Interest paid on capital contribution –15,000 –15,000Tax effect on items reported directly in equity 1,650 1,650

Total transactions reported directly in equity 1,719 314,209 –13,350 302,578Closing balance 30 Jun 2014 17,207 904,579 –7,350 290,678 1,205,114

3) Nominal amount of SEK 331,244,000 was reduced by transaction costs of SEK 17,035,000.

Hoist Finance AB (publ) • Interim report January – June 2015 17

Financial statements

Consolidated cash flow statement

SEK thousandQuarter 2

2015Quarter 2

2014Jan–Jun

2015Jan–Jun

2014Full year

2014

OPERATING ACTIVITIESGross cash collections 834,098 615,480 1,624,833 1,151,002 2,541,310

Paid-in interest –9,117 14,778 –1,254 31,883 89,731

Provisions received 41,747 39,111 89,363 76,874 153,222

Other operating income 3,439 2,206 4,985 4,089 12,220

Interest paid –53,916 –32,096 –117,760 –74,318 –274,982

Operating expenses –385,516 –293,199 –740,775 –499,558 –1,093,078

Net cash flow from financial transactions 1,518 –6,518 –18,741 –3,905 –17,719

Capital gain on redemption of joint venture certificates 15,673 2,464 15,673 2,464 27,941

Income tax paid –10,188 –10,867 –19,862 –40,443 –52,292

Total 437,738 331,359 836,462 648,088 1,386,353

Increase/decrease in acquired loans incl. translation differences –603,520 –1,092,526 –867,331 –1,531,670 –3,731,866

Increase/decrease in joint venture certificates 5,691 1,329 5,691 1,329 13,544

Increase/decrease in lending to the public 28,620 86,476 49,090 118,292 171,719

Increase/decrease in deposits and borrowing from the public 412,170 –226,411 1,713,358 –859,184 1,215,800

Increase/decrease in other assets –83,785 –87,414 –51,283 –67,208 –94,502

Increase/decrease in other liabilities 99,274 –8,628 –243,419 –53,774 307,124

Increase/decrease in provisions –5,753 –17,780 –10,457 –47,288 –25,933

Change in other balance sheet items –6,440 4,262 –3,893 –1,925 –310

Total –153,743 –1,340,692 591,756 –2,441,428 –2,144,424

Net Cash from operating activities 283,995 –1,009,333 1,428,218 –1,793,340 –758,071

INVESTING ACTIVITIESInvestments in intangible fixed assets –6,780 –7,972 –18,713 –10,552 –64,286

Investments in tangible fixed assets –2,815 – –4,300 –3,268 –14,247

Acquisition of business(es) – – –50,569 – –49,434

Investments in bonds and other securities –650,978 –351,702 –1,373,450 –148,031 –653,564

Net Cash from investing activities –660,573 –359,674 –1,447,032 –161,851 –781,531

FINANCING ACTIVITIESNew share issue – 315,050 750,061 315,050 414,484

Paid-in premium for warrants – – – – 5,139

Warrants, repurchased and cancelled –3,217 – –3,271 – –

Issued bonds – – – 74,000 831,007

Interest paid on capital contribution –7,500 –15,000 –7,500 –15,000 –28,750

Net Cash from financing activities –10,717 300,050 739,290 374,050 1,221,880

Net Cash flow for the period –387,295 –1,068,957 720,476 –1,581,141 –317,722

Cash and cash equivalents at the beginning of the period 4,716,932 3,414,699 3,609,161 3,926,883 3,926,883

Cash and cash equivalents at the end of the period1) 4,329,637 2,345,742 4,329,637 2,345,742 3,609,1611) Consists of cash, Treasury bills/bonds and lending to credit institutions.

Hoist Finance AB (publ) • Interim report January – June 2015 18

Financial statements

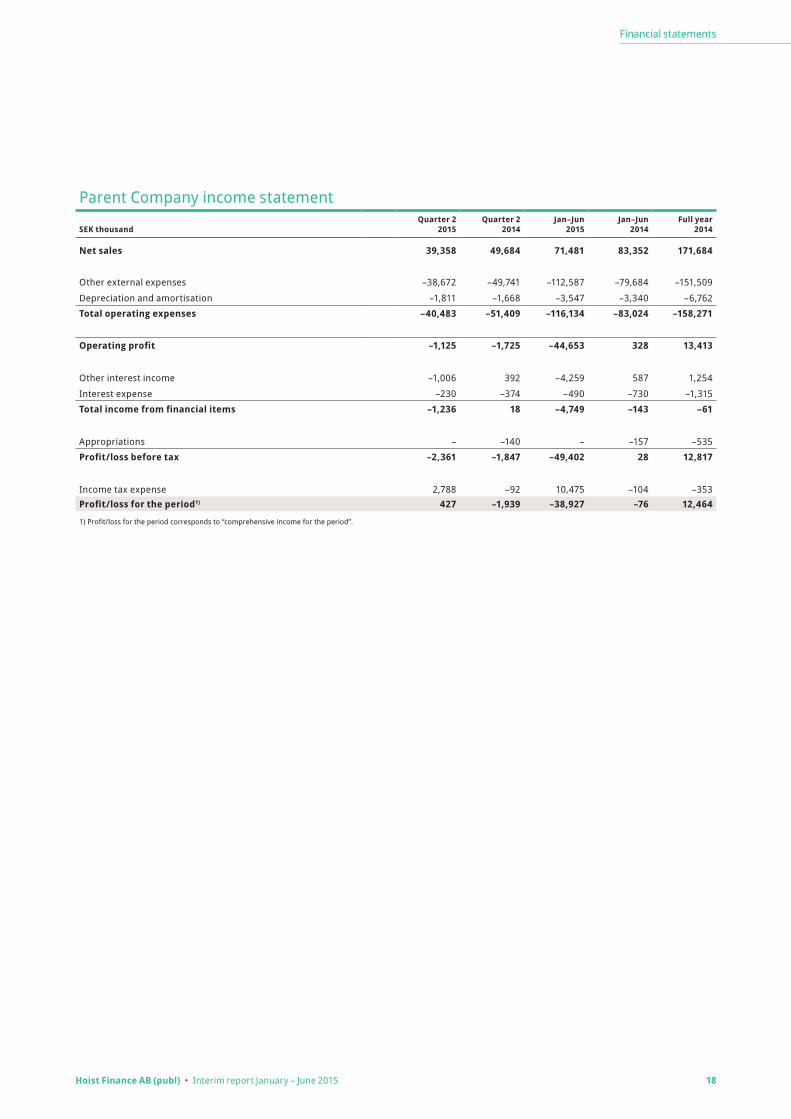

Parent Company income statement

SEK thousandQuarter 2

2015Quarter 2

2014Jan–Jun

2015Jan–Jun

2014Full year

2014

Net sales 39,358 49,684 71,481 83,352 171,684

Other external expenses –38,672 –49,741 –112,587 –79,684 –151,509

Depreciation and amortisation –1,811 –1,668 –3,547 –3,340 –6,762

Total operating expenses –40,483 –51,409 –116,134 –83,024 –158,271

Operating profit –1,125 –1,725 –44,653 328 13,413

Other interest income –1,006 392 –4,259 587 1,254

Interest expense –230 –374 –490 –730 –1,315

Total income from financial items –1,236 18 –4,749 –143 –61

Appropriations – –140 – –157 –535

Profit/loss before tax –2,361 –1,847 –49,402 28 12,817

Income tax expense 2,788 –92 10,475 –104 –353Profit/loss for the period1) 427 –1,939 –38,927 –76 12,464

1) Profit/loss for the period corresponds to “comprehensive income for the period”.

Hoist Finance AB (publ) • Interim report January – June 2015 19

Financial statements

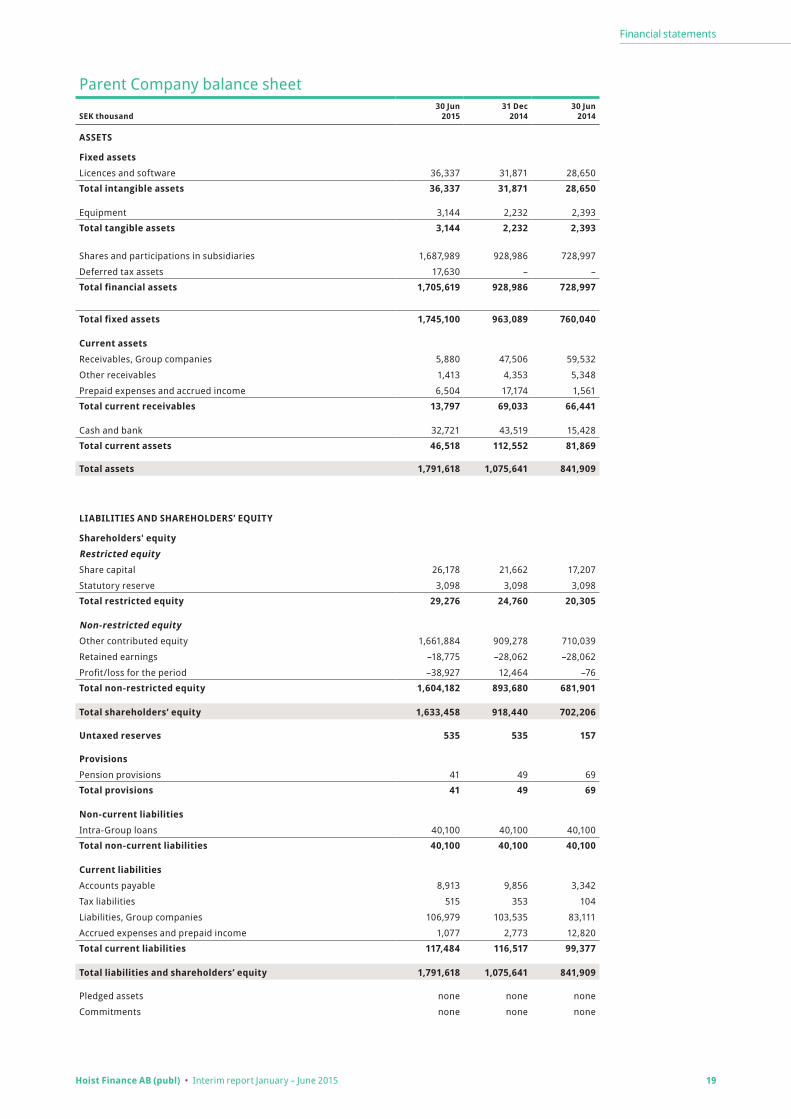

Parent Company balance sheet

SEK thousand30 Jun

201531 Dec

201430 Jun

2014

ASSETS

Fixed assetsLicences and software 36,337 31,871 28,650

Total intangible assets 36,337 31,871 28,650

Equipment 3,144 2,232 2,393

Total tangible assets 3,144 2,232 2,393

Shares and participations in subsidiaries 1,687,989 928,986 728,997

Deferred tax assets 17,630 – –

Total financial assets 1,705,619 928,986 728,997

Total fixed assets 1,745,100 963,089 760,040

Current assetsReceivables, Group companies 5,880 47,506 59,532

Other receivables 1,413 4,353 5,348

Prepaid expenses and accrued income 6,504 17,174 1,561

Total current receivables 13,797 69,033 66,441

Cash and bank 32,721 43,519 15,428

Total current assets 46,518 112,552 81,869

Total assets 1,791,618 1,075,641 841,909

LIABILITIES AND SHAREHOLDERS’ EQUITY

Shareholders' equityRestricted equityShare capital 26,178 21,662 17,207

Statutory reserve 3,098 3,098 3,098

Total restricted equity 29,276 24,760 20,305

Non-restricted equityOther contributed equity 1,661,884 909,278 710,039

Retained earnings –18,775 –28,062 –28,062

Profit/loss for the period –38,927 12,464 –76

Total non-restricted equity 1,604,182 893,680 681,901 Total shareholders’ equity 1,633,458 918,440 702,206

Untaxed reserves 535 535 157

ProvisionsPension provisions 41 49 69

Total provisions 41 49 69

Non-current liabilitiesIntra-Group loans 40,100 40,100 40,100

Total non-current liabilities 40,100 40,100 40,100

Current liabilitiesAccounts payable 8,913 9,856 3,342

Tax liabilities 515 353 104

Liabilities, Group companies 106,979 103,535 83,111

Accrued expenses and prepaid income 1,077 2,773 12,820

Total current liabilities 117,484 116,517 99,377

Total liabilities and shareholders’ equity 1,791,618 1,075,641 841,909

Pledged assets none none none

Commitments none none none

Hoist Finance AB (publ) • Interim report January – June 2015 20

Financial statements

Parent Company statement of changes in shareholders’ equityRestricted equity Non-restricted equity

SEK thousand Share capitalStatutory

reserve

Other contributed

equityRetained earnings

Profit for the period

Total shareholders'

equity

Opening balance 1 Jan 2015 21,662 3,098 909,278 –28,062 12,464 918,440

Transfer of previous year's net profit/loss 12,464 –12,464 0 Comprehensive income for the period

Profit for the period –38,927 –38,927

Total comprehensive income for the period –38,927 –38,927

Transactions reported directly in equity

New share issue 4,516 745,5451) 750,061

Warrants, repurchased and cancelled –94 –3,177 –3,271

Tax effect on items reported directly in equity 7,155 7,155

Total transactions reported directly in equity 4,516 752,606 –3,177 753,945

Closing balance 30 Jun 2015 26,178 3,098 1,661,884 –18,775 –38,927 1,633,458

1) Nominal amount of SEK 778,068,000 was reduced by transaction costs of SEK 32,523,000.

Restricted equity Non-restricted equity

SEK thousand Share capitalStatutory

reserve

Other contributed

equityRetained earnings

Profit for the period

Total shareholders'

equity

Opening balance 1 Jan 2014 15,488 3,098 395,830 –23,111 –4,951 386,354

Transfer of previous year's net profit/loss –4,951 4,951 0 Comprehensive income for the period

Profit for the period 12,464 12,464

Total comprehensive income for the period 12,464 12,464

Transactions reported directly in equity

New share issue 6,174 508,3102) 514,484

Paid-in premium for warrants 5,138 5,138

Total transactions reported directly in equity 6,174 513,448 519,622

Closing balance 31 Dec 2014 21,662 3,098 909,278 –28,062 12,464 918,440

2) Nominal amount of SEK 527,160,000 was reduced by transaction costs of SEK 18,850,000.

Restricted equity Non-restricted equity

SEK thousand Share capitalStatutory

reserve

Other contributed

equityRetained earnings

Profit for the period

Total shareholders'

equity

Opening balance 1 Jan 2014 15,488 3,098 395,830 –23,111 –4,951 386,354

Transfer of previous year's net profit/loss –4,951 4,951 0

Comprehensive income for the period

Profit for the period –76 –76

Total comprehensive income for the period –76 –76

Transactions reported directly in equity

New share issue 1,719 314,2093) 315,928

Total transactions reported directly in equity 1,719 314,209 315,928

Closing balance 30 Jun 2014 17,207 3,098 710,039 –28,062 –76 702,206

3) Nominal amount of SEK 331,244,000 was reduced by transaction costs of SEK 17,035,000.

Hoist Finance AB (publ) • Interim report January – June 2015 21

Financial statements

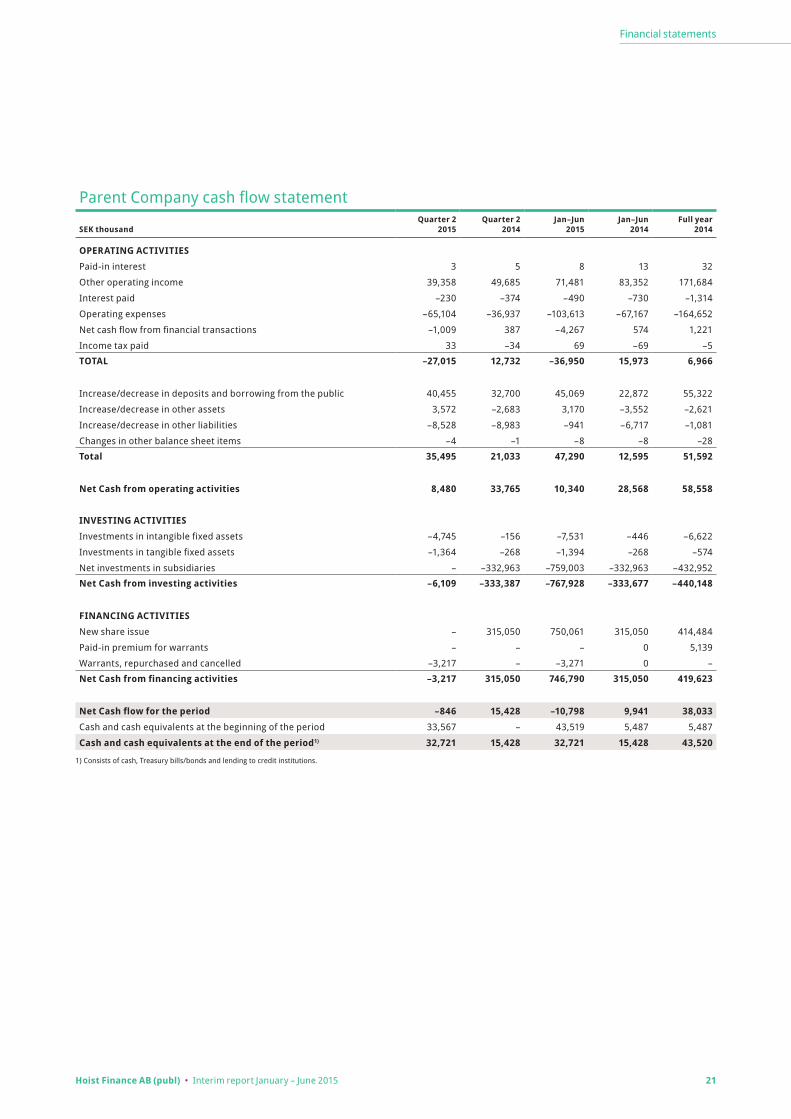

Parent Company cash flow statement

SEK thousandQuarter 2

2015Quarter 2

2014Jan–Jun

2015Jan–Jun

2014Full year

2014

OPERATING ACTIVITIESPaid-in interest 3 5 8 13 32

Other operating income 39,358 49,685 71,481 83,352 171,684

Interest paid –230 –374 –490 –730 –1,314

Operating expenses –65,104 –36,937 –103,613 –67,167 –164,652

Net cash flow from financial transactions –1,009 387 –4,267 574 1,221

Income tax paid 33 –34 69 –69 –5

TOTAL –27,015 12,732 –36,950 15,973 6,966

Increase/decrease in deposits and borrowing from the public 40,455 32,700 45,069 22,872 55,322

Increase/decrease in other assets 3,572 –2,683 3,170 –3,552 –2,621

Increase/decrease in other liabilities –8,528 –8,983 –941 –6,717 –1,081

Changes in other balance sheet items –4 –1 –8 –8 –28

Total 35,495 21,033 47,290 12,595 51,592

Net Cash from operating activities 8,480 33,765 10,340 28,568 58,558

INVESTING ACTIVITIESInvestments in intangible fixed assets –4,745 –156 –7,531 –446 –6,622

Investments in tangible fixed assets –1,364 –268 –1,394 –268 –574

Net investments in subsidiaries – –332,963 –759,003 –332,963 –432,952

Net Cash from investing activities –6,109 –333,387 –767,928 –333,677 –440,148

FINANCING ACTIVITIESNew share issue – 315,050 750,061 315,050 414,484

Paid-in premium for warrants – – – 0 5,139

Warrants, repurchased and cancelled –3,217 – –3,271 0 –

Net Cash from financing activities –3,217 315,050 746,790 315,050 419,623

Net Cash flow for the period –846 15,428 –10,798 9,941 38,033Cash and cash equivalents at the beginning of the period 33,567 – 43,519 5,487 5,487

Cash and cash equivalents at the end of the period1) 32,721 15,428 32,721 15,428 43,520

1) Consists of cash, Treasury bills/bonds and lending to credit institutions.

Hoist Finance AB (publ) • Interim report January – June 2015 22

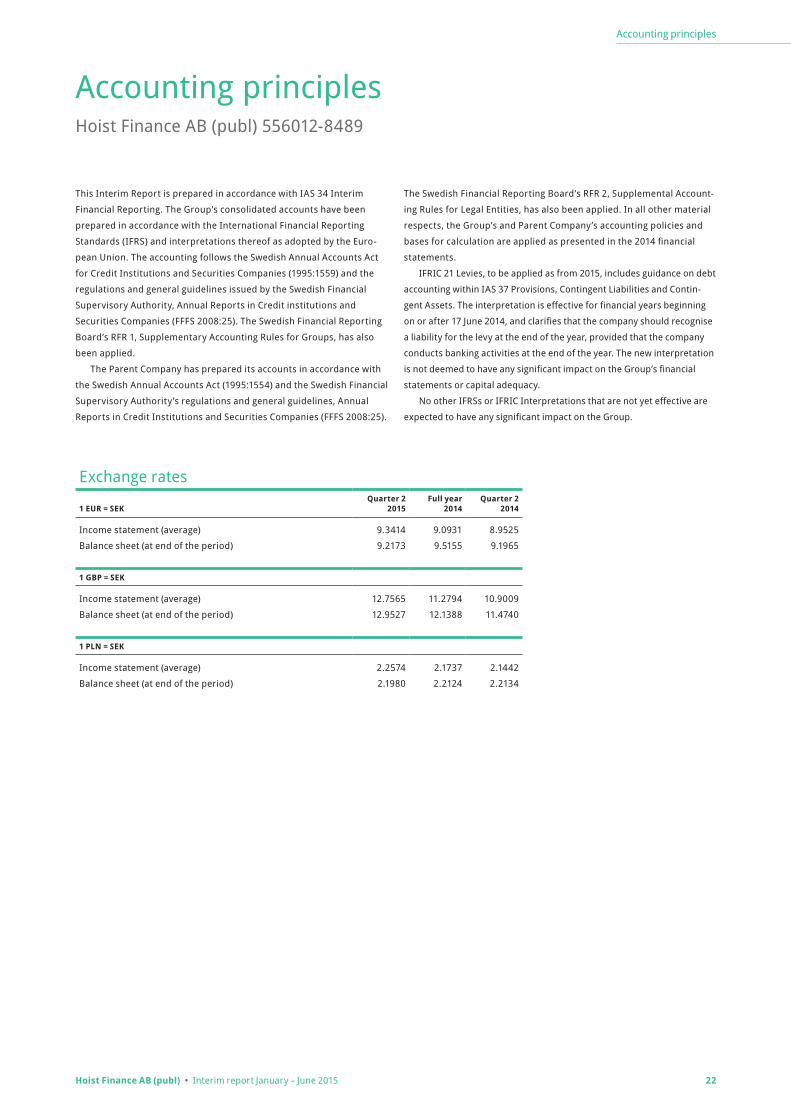

Accounting principles

Accounting principlesHoist Finance AB (publ) 556012-8489

This Interim Report is prepared in accordance with IAS 34 Interim

Financial Reporting. The Group’s consolidated accounts have been

prepared in accordance with the International Financial Reporting

Standards (IFRS) and interpretations thereof as adopted by the Euro-

pean Union. The accounting follows the Swedish Annual Accounts Act

for Credit Institutions and Securities Companies (1995:1559) and the

regulations and general guidelines issued by the Swedish Financial

Supervisory Authority, Annual Reports in Credit institutions and

Securities Companies (FFFS 2008:25). The Swedish Financial Reporting

Board’s RFR 1, Supplementary Accounting Rules for Groups, has also

been applied.

The Parent Company has prepared its accounts in accordance with

the Swedish Annual Accounts Act (1995:1554) and the Swedish Financial

Supervisory Authority’s regulations and general guidelines, Annual

Reports in Credit Institutions and Securities Companies (FFFS 2008:25).

Exchange rates

1 EUR = SEKQuarter 2

2015Full year

2014Quarter 2

2014

Income statement (average) 9.3414 9.0931 8.9525

Balance sheet (at end of the period) 9.2173 9.5155 9.1965

1 GBP = SEK

Income statement (average) 12.7565 11.2794 10.9009

Balance sheet (at end of the period) 12.9527 12.1388 11.4740

1 PLN = SEK

Income statement (average) 2.2574 2.1737 2.1442

Balance sheet (at end of the period) 2.1980 2.2124 2.2134

The Swedish Financial Reporting Board’s RFR 2, Supplemental Account-

ing Rules for Legal Entities, has also been applied. In all other material

respects, the Group’s and Parent Company’s accounting policies and

bases for calculation are applied as presented in the 2014 financial

statements.

IFRIC 21 Levies, to be applied as from 2015, includes guidance on debt

accounting within IAS 37 Provisions, Contingent Liabilities and Contin-

gent Assets. The interpretation is effective for financial years beginning

on or after 17 June 2014, and clarifies that the company should recognise

a liability for the levy at the end of the year, provided that the company

conducts banking activities at the end of the year. The new interpretation

is not deemed to have any significant impact on the Group’s financial

statements or capital adequacy.

No other IFRSs or IFRIC Interpretations that are not yet effective are

expected to have any significant impact on the Group.

Hoist Finance AB (publ) • Interim report January – June 2015 23

Notes

NotesNote 1 Segment reporting

Consolidated income statement

SEK thousand Quarter 2 2015 Quarter 2 2014 Jan–Jun 2015 Jan–Jun 2014 Full year 2014

Revenue from acquired loan portfolios 473,621 337,131 905,431 632,268 1,398,291 Of which, gross cash collections 834,098 615,479 1,624,833 1,151,002 2,541,311 Of which, portfolio amortisation and revaluation –360,477 –278,348 –719,402 –518,734 –1,143,020Interest income –9,117 21,850 –1,254 43,196 89,731 Of which, interest income from run-off portfolio of consumer loans 2,994 9,566 6,112 20,633 38,180 Of which, interest income excl. run-off loan portfolio –12,111 12,284 –7,366 22,563 51,551Interest expense –92,876 –81,653 –185,497 –166,034 –344,969

Net interest income 371,628 277,328 718,680 509,430 1,143,053 Fee and commission income 41,747 39,111 89,363 76,874 153,222Net income from financial transactions 1,519 –6,518 –18,740 –3,905 –17,719Other income 3,439 2,205 4,985 4,089 12,219

Total operating income 418,333 312,126 794,288 586,488 1,290,775 General administrative expensesPersonnel expenses –153,016 –110,255 –298,682 –218,676 –473,200Other operating expenses –211,764 –151,843 –439,505 –273,383 –627,467Depreciation and amortisation of tangible and intangible assets –10,859 –7,267 –21,612 –13,778 –30,281

Total operating expenses –375,639 –269,365 –759,799 –505,837 –1,130,948 Profit before loan losses 42,694 42,761 34,489 80,650 159,827

Net loan losses –5,298 – –5,298 – –Profit from shares and participations in joint ventures 14,946 13,203 30,296 25,073 58,662

Profit before tax 52,342 55,964 59,487 105,724 218,489

Operating income statement based on segment reporting

SEK thousand Quarter 2 2015 Quarter 2 2014 Jan–Jun 2015 Jan–Jun 2014 Full year 2014

Gross cash collections 834,098 615,479 1,624,833 1,151,002 2,541,311Portfolio amortisation and revaluation –360,477 –278,348 –719,402 –518,734 –1,143,020Interest income from run-off consumer loan portfolio 2,994 9,566 6,112 20,633 38,180

Net revenue from acquired loan portfolios 476,615 346,697 911,543 652,901 1,436,471Fee and commission income 41,747 39,111 89,363 76,874 153,222Profit from shares and participations in joint ventures 14,946 13,203 30,296 25,073 58,662Other income 3,439 2,205 4,985 4,089 12,219

Total revenue 536,747 401,216 1,036,187 758,937 1,660,574

Personnel expenses –153,016 –110,255 –298,682 –218,676 –473,200Other operating expenses –211,764 –151,843 –439,505 –273,383 –627,467Depreciation and amortisation of tangible and intangible assets –10,859 –7,267 –21,612 –13,778 –30,281

Total operating expenses –375,639 –269,365 –759,799 –505,837 –1,130,948 EBIT 161,108 131,851 276,388 253,100 529,626

Interest income excl. run-off portfolio of consumer loans –12,111 12,284 –7,366 22,563 51,551Interest expense –92,876 –81,653 –185,497 –166,034 –344,969Net income from financial transactions incl. financing expenses –3,779 –6,518 –24,038 –3,905 –17,719

Total financial items –108,766 –75,887 –216,901 –147,376 –311,137

Profit before tax 52,342 55,964 59,487 105,724 218,489

Segment reporting has been prepared based on the manner in which executive management monitors operations. This differs from statutory account preparation; the material differences are as follows:• Revenueincludesincomefrom − acquired loan portfolios − run-off portfolios of consumer loans

− fee and commission income from third parties – profit from shares and participations in joint ventures − certain other income• Totalfinancialitemsincludeinterestincomefromsourcesother

than acquired loan portfolios, interest expense and net income from financial transactions.

Hoist Finance AB (publ) • Interim report January – June 2015 24

Notes

Note 1 Segment reporting, cont.

Income statement Quarter 2, 2015

SEK thousandGerman

and Austria1)

Belgium, the Netherlands

and France2) UK Italy Poland

Central Functions/

Eliminations Group

Gross cash collections 210,312 234,349 162,516 127,465 99,456 – 834,098Portfolio amortisation and revaluation –114,302 –146,271 –20,835 –42,748 –36,321 – –360,477Interest income from run-off consumer loan portfolio 2,994 – – – – – 2,994

Net revenue from acquired loan portfolios 99,004 88,078 141,681 84,717 63,135 – 476,615Fee and commission income 1,416 1,636 27,379 1,705 9,611 – 41,747Profit from shares and participations in joint ventures – – – – – 14,946 14,946Other income 3,365 –8 1,076 330 64 –1,388 3,439

Total revenue 103,785 89,706 170,136 86,752 72,810 13,558 536,747

Personnel expenses –35,781 –21,389 –41,383 –14,642 –5,208 –34,613 –153,016Other operating expenses –23,954 –27,011 –88,682 –28,526 –15,155 –28,436 –211,764Depreciation and amortisation of tangible and intangible assets –869 –511 –871 –1,610 –964 –6,034 –10,859

Total operating expenses –60,604 –48,911 –130,936 –44,778 –21,327 –69,083 –375,639

EBIT 43,181 40,795 39,200 41,974 51,483 –55,525 161,108

Interest income excl. run-off portfolio of consumer loans 116 0 – 0 894 –13,121 –12,111Interest expense – –18 0 0 –102 –92,756 –92,876Net income from financial transactions incl. financing expenses –28,305 –25,652 –23,791 –14,381 –16,005 104,355 –3,779

Total financial items –28,189 –25,670 –23,791 –14,381 –15,213 –1,522 –108,766

Profit before tax 14,992 15,125 15,409 27,593 36,270 –57,047 52,342

1) Total revenue for Germany of SEK 100,368,000 is included in the revenue for Germany and Austria.2) Total revenue for the Netherlands of SEK 62,844,000 is included in the revenue for Belgium, the Netherlands and France.

Income statement Quarter 2, 2014

SEK thousandGerman

and Austria1)

Belgium, the Netherlands

and France2) UK Italy Poland

Central Functions/

Eliminations Group

Gross cash collections 155,454 192,280 125,220 60,769 81,756 – 615,479Portfolio amortisation and revaluation –84,250 –115,263 –52,380 –22,522 –3,933 – –278,348Interest income from run-off consumer loan portfolio 9,566 – – – – – 9,566

Net revenue from acquired loan portfolios 80,770 77,017 72,840 38,247 77,823 – 346,697Fee and commission income 4,469 1,755 32,887 – – – 39,111Profit from shares and participations in joint ventures – – – – – 13,203 13,203Other income 2,979 – 141 – – –915 2,205

Total revenue 88,218 78,772 105,868 38,247 77,823 12,288 401,216

Personnel expenses –32,687 –21,530 –30,490 – –475 –25,073 –110,255Other operating expenses –20,040 –23,264 –33,288 –14,249 –16,750 –44,252 –151,843Depreciation and amortisation of tangible and intangible assets –708 –998 –1,750 – –27 –3,784 –7,267

Total operating expenses –53,435 –45,792 –65,528 –14,249 –17,252 –73,109 –269,365

EBIT 34,783 32,980 40,340 23,998 60,571 –60,821 131,851

Interest income excl. run-off portfolio of consumer loans 6 20 5 – – 12,253 12,284Interest expense 46 –20 –1 – – –81,678 –81,653Net income from financial transactions incl. financing expenses –24,972 –25,460 –16,896 –6,371 –11,461 78,642 –6,518

Total financial items –24,920 –25,460 –16,892 –6,371 –11,461 9,217 –75,887

Profit before tax 9,863 7,520 23,448 17,627 49,110 –51,604 55,964

1) Total revenue for Germany of SEK 87,772,000 is included in the revenue for Germany and Austria.2) Total revenue for the Netherlands of SEK 48,292,000 is included in the revenue for Belgium, the Netherlands and France.

Group costs for central and supporting functions are not allocated to the operating segments but are reported as Central Functions and Eliminations.

A financing cost is allocated to the operating segments based on the acquired loan portfolio assets. The difference between the actual fi-nancing cost and the standardised cost is included in Central Functions and Eliminations. Certain internal functions located in Germany were

reclassified as Group functions during Q2 2015; accordingly, costs asso-ciated with these functions are now included in the Central Functions operating segment.

With respect to the balance sheet, only acquired loan portfolios are monitored. Other assets and liabilities are not monitored on a segment-by-segment basis.

Hoist Finance AB (publ) • Interim report January – June 2015 25

Notes

Income statement Jan–Jun 2015

SEK thousandGerman

and Austria1)

Belgium, the Netherlands

and France2) UK Italy Poland

Central Functions/

Eliminations Group

Gross cash collections 461,906 412,037 314,144 250,952 185,794 – 1,624,833Portfolio amortisation and revaluation –264,923 –251,499 –59,253 –87,726 –56,001 – –719,402Interest income from run-off consumer loan portfolio 6,112 – – – – – 6,112

Net revenue from acquired loan portfolios 203,095 160,538 254,891 163,226 129,793 – 911,543Fee and commission income 4,095 3,451 60,548 2,912 18,357 – 89,363Profit from shares and participations in joint ventures – – – – – 30,296 30,296Other income 4,527 –8 1,082 675 97 –1,388 4,985

Total revenue 211,717 163,981 316,521 166,813 148,247 28,908 1,036,187

Personnel expenses –71,676 –45,831 –78,649 –27,339 –10,404 –64,783 –298,682Other operating expenses –46,151 –50,931 –150,911 –54,061 –29,570 –107,881 –439,505Depreciation and amortisation of tangible and intangible assets –1,744 –1,320 –1,726 –3,184 –1,745 –11,893 –21,612

Total operating expenses –119,571 –98,082 –231,286 –84,584 –41,719 –184,557 –759,799

EBIT 92,146 65,899 85,235 82,229 106,528 –155,649 276,388

Interest income excl. run-off portfolio of consumer loans 337 28 – 0 906 –8,637 –7,366Interest expense – –34 0 –8 –109 –185,346 –185,497Net income from financial transactions incl. financing expenses –56,630 –52,516 –47,145 –28,586 –30,776 191,615 –24,038

Total financial items –56,293 –52,522 –47,145 –28,594 –29,979 –2,368 –216,901

Profit before tax 35,853 13,377 38,090 53,635 76,549 –158,017 59,487

1) Total revenue for Germany of SEK 205,139,000 is included in the revenue for Germany and Austria.2) Total revenue for the Netherlands of SEK 91,879,000 is included in the revenue for Belgium, the Netherlands and France.

Income statement Jan–Jun 2014

SEK thousandGerman

and Austria1)

Belgium, the Netherlands

and France2) UK Italy Poland

Central Functions/

Eliminations Group

Gross cash collections 309,572 350,168 257,898 110,920 122,444 – 1,151,002Portfolio amortisation and revaluation –154,423 –220,230 –106,867 –46,438 9,224 – –518,734Interest income from run-off consumer loan portfolio 20,633 – – – – – 20,633

Net revenue from acquired loan portfolios 175,782 129,938 151,031 64,482 131,668 – 652,901Fee and commission income 9,061 3,373 64,440 – – – 76,874Profit from shares and participations in joint ventures – – – – – 25,073 25,073Other income 4,143 0 558 0 0 –612 4,089

Total revenue 188,986 133,311 216,029 64,482 131,668 24,461 758,937

Personnel expenses –64,492 –40,382 –63,392 – –878 –49,532 –218,676Other operating expenses –35,357 –44,158 –71,244 –23,468 –28,139 –71,017 –273,383Depreciation and amortisation of tangible and intangible assets –1,416 –1,866 –3,081 – –27 –7,388 –13,778

Total operating expenses –101,265 –86,406 –137,717 –23,468 –29,044 –127,937 –505,837

EBIT 87,721 46,905 78,312 41,014 102,624 –103,476 253,100

Interest income excl. run-off portfolio of consumer loans 18 42 233 0 0 22,270 22,563Interest expense 46 –54 –91 – 0 –165,935 –166,034Net income from financial transactions incl. financing expenses –49,778 –47,388 –33,374 –10,064 –22,117 158,816 –3,905

Total financial items –49,714 –47,400 –33,232 –10,064 –22,117 15,151 –147,376

Profit before tax 38,007 –495 45,080 30,950 80,507 –88,325 105,724

1) Total revenue for Germany of SEK 184,925,000 is included in the revenue for Germany and Austria.2) Total revenue for the Netherlands of SEK 81,537,000 is included in the revenue for Belgium, the Netherlands and France.

Note 1 Segment reporting, cont.

Hoist Finance AB (publ) • Interim report January – June 2015 26

Notes

Income statement Full year 2014

SEK thousandGerman

and Austria1)

Belgium, the Netherlands

and France2) UK Italy Poland

Central Functions/

Eliminations Group

Gross cash collections 724,044 733,474 527,346 260,828 295,619 – 2,541,311Portfolio amortisation and revaluation –348,873 –484,991 –200,802 –91,324 –17,030 – –1,143,020Interest income from run-off consumer loan portfolio 38,180 – – – – – 38,180

Net revenue from acquired loan portfolios 413,351 248,483 326,544 169,504 278,589 – 1,436,471Fee and commission income 17,889 6,989 128,344 – – – 153,222Profit from shares and participations in joint ventures – – – – – 58,662 58,662Other income 14,294 218 2,686 311 0 –5,290 12,219

Total revenue 445,534 255,690 457,574 169,815 278,589 53,372 1,660,574

Personnel expenses –133,245 –86,886 –134,502 –17,854 –2,035 –98,678 –473,200Other operating expenses –85,272 –102,656 –137,601 –86,028 –74,812 –141,098 –627,467Depreciation and amortisation of tangible and intangible assets –2,940 –4,679 –4,588 –2,340 – –15,734 –30,281

Total operating expenses –221,457 –194,221 –276,691 –106,222 –76,847 –255,510 –1,130,948

EBIT 224,077 61,469 180,883 63,593 201,742 –202,138 529,626

Interest income excl. run-off portfolio of consumer loans 96 170 241 0 0 51,044 51,551Interest expense –678 –90 –179 –2 0 –344,020 –344,969Net income from financial transactions incl. financing expenses –105,135 –100,481 –72,627 –25,292 –52,232 338,048 –17,719

Total financial items –105,717 –100,401 –72,565 –25,294 –52,232 45,072 –311,137

Profit before tax 118,360 –38,932 108,318 38,299 149,510 –157,066 218,489

1) Total revenue for Germany of SEK 437,105,000 is included in the revenue for Germany and Austria.2) Total revenue for the Netherlands of SEK 119,747,000 is included in the revenue for Belgium, the Netherlands and France.

Acquired loans at 30 Jun 2015

SEK thousandGerman

and Austria

Belgium, the Netherlands

and France UK Italy Poland

Central Functions/

Eliminations Group

Run-off portfolio of consumer loans 81,879 81,879Acquired loan portfolios 2,139,178 1,981,923 1,900,387 1,264,030 1,449,193 8,734,711Shares and participations in joint ventures 223,024 223,024Acquired loans 2,221,057 1,981,923 1,900,387 1,264,030 1,449,193 223,024 9,039,614

Acquired loans at 31 Dec 2014

SEK thousandGerman

and Austria

Belgium, the Netherlands

and France UK Italy Poland

Central Functions/

Eliminations Group

Run-off portfolio of consumer loans 118,799 118,799Acquired loan portfolios 2,231,593 2,194,000 1,797,520 1,181,210 1,182,459 8,586,782Shares and participations in joint ventures 215,347 215,347Acquired loans 2,350,392 2,194,000 1,797,520 1,181,210 1,182,459 215,347 8,920,928

Acquired loans at 30 Jun 2014

SEK thousandGerman

and Austria