intermediary leverage cycles and financial stability · · 2012-11-26intermediary leverage cycles...

TRANSCRIPT

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors’ and are not representative of the views of the Federal Reserve Bank of New York or of the Federal Reserve System

Introduction

Outline

Introduction

The Model

Solution

Distortions and AmplificationSolvencyAmplification

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 2 / 38

Introduction

Questions about Financial Stability Policy

Systemic distress of financial intermediaries raises questions aboutfinancial stability policies:

How does capital regulation affect the tradeoff between the pricing ofcredit and the amount of systemic risk?

How does macroprudential policy function in equilibrium?

What are the welfare implications of capital regulation?

We develop a theoretical framework to address these questions

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 3 / 38

Introduction

Our Approach

We use a standard macro model with a financial sector and add onekey assumption:

Funding constraints of financial intermediaries are risk based, sointermediaries have to hold more capital when the riskiness of theirassets increases

This assumption is empirically motivated and it allows us to capturestylized facts about:

Procyclical leverage of intermediary balance sheetsProcyclical share of intermediated creditRelationship between asset risk premia and intermediary leverage

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 4 / 38

The Model

Outline

Introduction

The Model

Solution

Distortions and AmplificationSolvencyAmplification

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 5 / 38

The Model

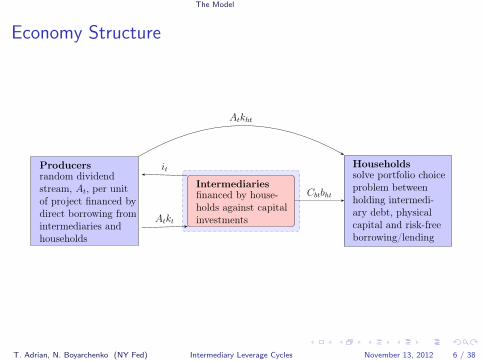

Economy Structure

Producersrandom dividendstream, At, per unitof project financed bydirect borrowing fromintermediaries andhouseholds

Intermediariesfinanced by house-holds against capitalinvestments

Householdssolve portfolio choiceproblem betweenholding intermedi-ary debt, physicalcapital and risk-freeborrowing/lending

Atkht

it

Atkt

Cbtbht

1

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 6 / 38

The Model

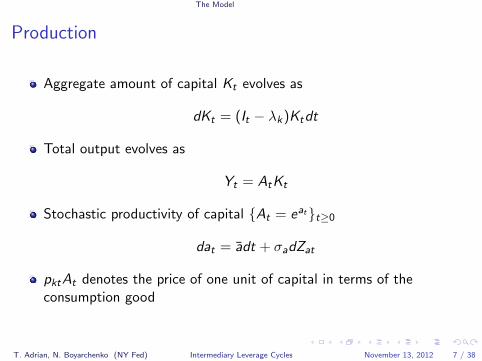

Production

Aggregate amount of capital Kt evolves as

dKt = (It − λk)Ktdt

Total output evolves as

Yt = AtKt

Stochastic productivity of capital {At = eat}t≥0

dat = adt + σadZat

pktAt denotes the price of one unit of capital in terms of theconsumption good

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 7 / 38

The Model

Households

Household preferences are:

E[∫ +∞

0e−(ξt+ρht) log ctdt

]Liquidity preference shocks (as in Allen and Gale (1994) and Diamondand Dybvig (1983)) are exp (−ξt)

dξt = σξρξ,adZat + σξ

√1− ρ2

ξ,adZξt

Households do not have access to the investment technology

dkht = −λkkhtdt

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 8 / 38

The Model

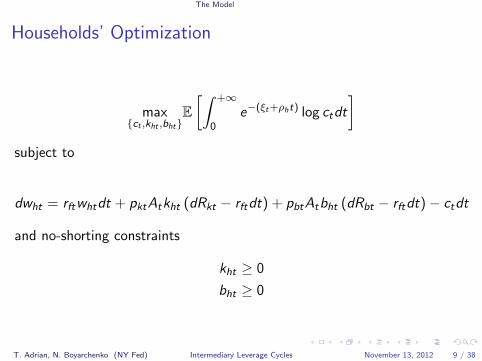

Households’ Optimization

max{ct ,kht ,bht}

E[∫ +∞

0e−(ξt+ρht) log ctdt

]subject to

dwht = rftwhtdt + pktAtkht (dRkt − rftdt) + pbtAtbht (dRbt − rftdt)− ctdt

and no-shorting constraints

kht ≥ 0

bht ≥ 0

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 9 / 38

The Model

Intermediaries

Financial intermediaries create new capital

dkt = (Φ(it)− λk) ktdt

Investment carries quadratic adjustment costs (Brunnermeier andSannikov (2012))

Φ (it) = φ0

(√1 + φ1it − 1

)Intermediaries finance investment projects through inside equity andoutside risky debt giving the budget constraint

pktAtkt = pbtAtbt + wt

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 10 / 38

The Model

Intermediaries’ Risk Based Capital Constraint

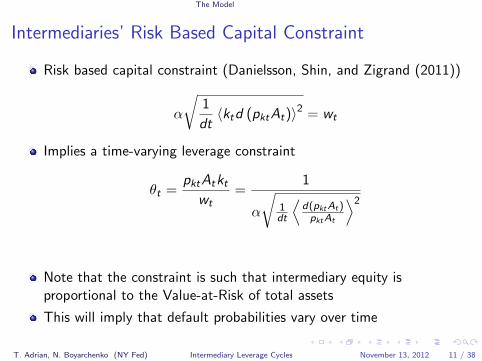

Risk based capital constraint (Danielsson, Shin, and Zigrand (2011))

α

√1

dt〈ktd (pktAt)〉2 = wt

Implies a time-varying leverage constraint

θt =pktAtkt

wt=

1

α

√1dt

⟨d(pktAt)pktAt

⟩2

Note that the constraint is such that intermediary equity isproportional to the Value-at-Risk of total assets

This will imply that default probabilities vary over time

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 11 / 38

The Model

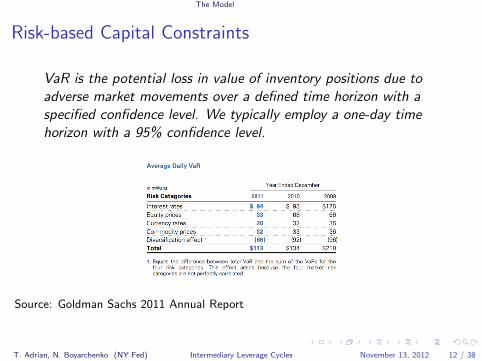

Risk-based Capital Constraints

VaR is the potential loss in value of inventory positions due toadverse market movements over a defined time horizon with aspecified confidence level. We typically employ a one-day timehorizon with a 95% confidence level.

Source: Goldman Sachs 2011 Annual Report

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 12 / 38

The Model

Commercial Bank Lending Standards

Q2−91 Q2−93 Q2−95 Q2−97 Q2−99 Q2−01 Q2−03 Q2−05 Q2−07 Q2−09 Q2−110

20

40

60V

IX

−50

0

50

100

Cre

dit T

ight

enin

g

ρ=0.68013

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 13 / 38

The Model

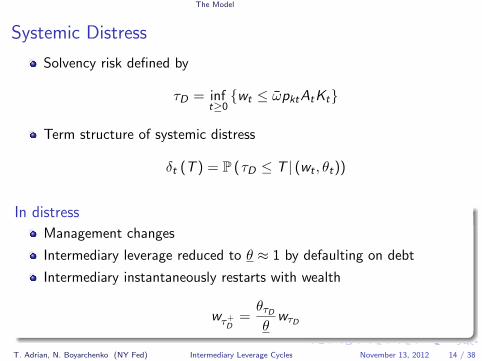

Systemic Distress

Solvency risk defined by

τD = inft≥0{wt ≤ ωpktAtKt}

Term structure of systemic distress

δt (T ) = P (τD ≤ T | (wt , θt))

In distress

Management changes

Intermediary leverage reduced to θ ≈ 1 by defaulting on debt

Intermediary instantaneously restarts with wealth

wτ+D

=θτDθ

wτD

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 14 / 38

The Model

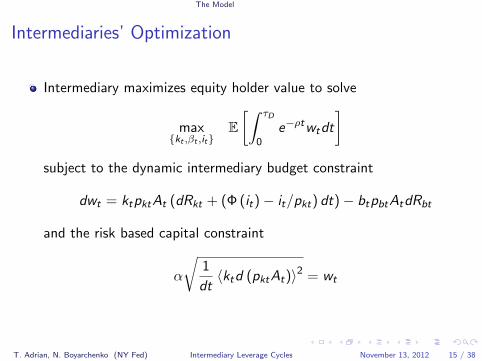

Intermediaries’ Optimization

Intermediary maximizes equity holder value to solve

max{kt ,βt ,it}

E[∫ τD

0e−ρtwtdt

]subject to the dynamic intermediary budget constraint

dwt = ktpktAt (dRkt + (Φ (it)− it/pkt) dt)− btpbtAtdRbt

and the risk based capital constraint

α

√1

dt〈ktd (pktAt)〉2 = wt

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 15 / 38

The Model

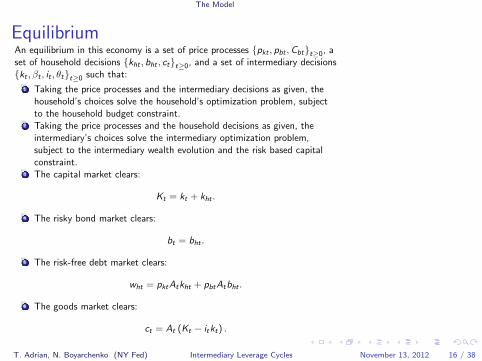

EquilibriumAn equilibrium in this economy is a set of price processes {pkt , pbt ,Cbt}t≥0, aset of household decisions {kht , bht , ct}t≥0, and a set of intermediary decisions{kt , βt , it , θt}t≥0 such that:

1 Taking the price processes and the intermediary decisions as given, thehousehold’s choices solve the household’s optimization problem, subjectto the household budget constraint.

2 Taking the price processes and the household decisions as given, theintermediary’s choices solve the intermediary optimization problem,subject to the intermediary wealth evolution and the risk based capitalconstraint.

3 The capital market clears:

Kt = kt + kht .

4 The risky bond market clears:

bt = bht .

5 The risk-free debt market clears:

wht = pktAtkht + pbtAtbht .

6 The goods market clears:

ct = At (Kt − itkt) .

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 16 / 38

The Model

Related Literature

Leverage Cycles: Geanakoplos (2003), Fostel and Geanakoplos(2008), Brunnermeier and Pedersen (2009)

Amplification in Macroeconomy: Bernanke and Gertler (1989),Kiyotaki and Moore (1997)

Financial Intermediaries and the Macroeconomy: Gertler andKiyotaki (2012), Gertler, Kiyotaki, and Queralto (2011), He andKrishnamurthy (2012a,b), Brunnermeier and Sannikov (2011, 2012)

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 17 / 38

Solution

Outline

Introduction

The Model

Solution

Distortions and AmplificationSolvencyAmplification

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 18 / 38

Solution

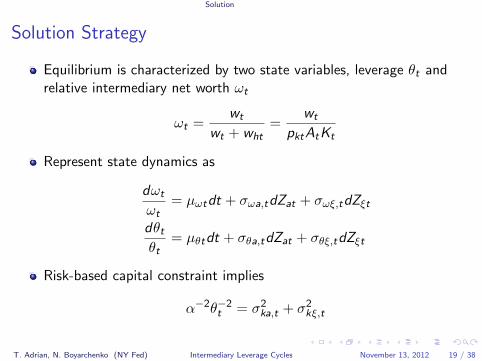

Solution Strategy

Equilibrium is characterized by two state variables, leverage θt andrelative intermediary net worth ωt

ωt =wt

wt + wht=

wt

pktAtKt

Represent state dynamics as

dωt

ωt= µωtdt + σωa,tdZat + σωξ,tdZξt

dθtθt

= µθtdt + σθa,tdZat + σθξ,tdZξt

Risk-based capital constraint implies

α−2θ−2t = σ2

ka,t + σ2kξ,t

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 19 / 38

Solution

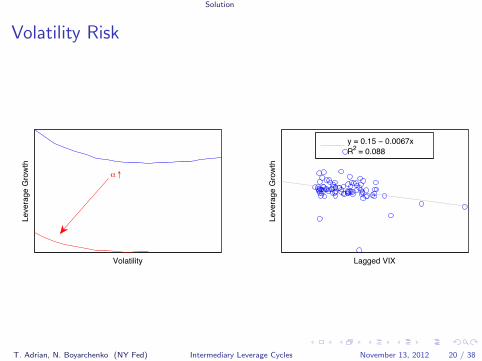

Volatility Risk

Volatility

Leve

rage

Gro

wth

Lagged VIXLe

vera

ge G

row

th

y = 0.15 − 0.0067xR2 = 0.088

α ↑

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 20 / 38

Solution

Intermediary Balance Sheets

Equity Growth

Leve

rage

Gro

wth

Equity Growth

Leve

rage

Gro

wth

Asset Growth

Leve

rage

Gro

wth

Asset Growth

Leve

rage

Gro

wth

Total Credit GrowthInte

rmed

iate

d C

redi

t Gro

wth

Total Credit GrowthInte

rmed

iate

d C

redi

t Gro

wth

y = −0.071 + 0.76xR2 = 0.46

α ↑

α ↑

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 21 / 38

Solution

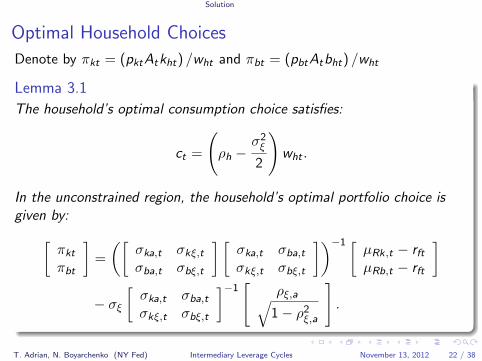

Optimal Household Choices

Denote by πkt = (pktAtkht) /wht and πbt = (pbtAtbht) /wht

Lemma 3.1

The household’s optimal consumption choice satisfies:

ct =

(ρh −

σ2ξ

2

)wht .

In the unconstrained region, the household’s optimal portfolio choice isgiven by:[

πktπbt

]=

([σka,t σkξ,tσba,t σbξ,t

] [σka,t σba,tσkξ,t σbξ,t

])−1 [µRk,t − rftµRb,t − rft

]− σξ

[σka,t σba,tσkξ,t σbξ,t

]−1[

ρξ,a√1− ρ2

ξ,a

].

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 22 / 38

Solution

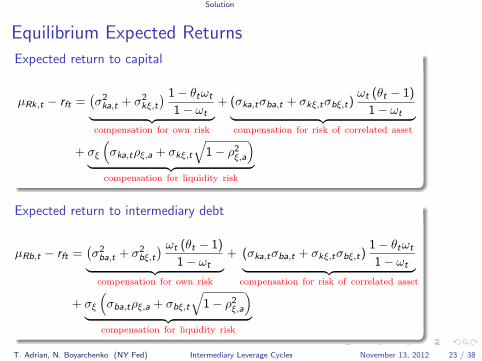

Equilibrium Expected Returns

Expected return to capital

µRk,t − rft =(σ2ka,t + σ2

kξ,t

) 1− θtωt

1− ωt︸ ︷︷ ︸compensation for own risk

+ (σka,tσba,t + σkξ,tσbξ,t)ωt (θt − 1)

1− ωt︸ ︷︷ ︸compensation for risk of correlated asset

+ σξ

(σka,tρξ,a + σkξ,t

√1− ρ2

ξ,a

)︸ ︷︷ ︸

compensation for liquidity risk

Expected return to intermediary debt

µRb,t − rft =(σ2ba,t + σ2

bξ,t

) ωt (θt − 1)

1− ωt︸ ︷︷ ︸compensation for own risk

+ (σka,tσba,t + σkξ,tσbξ,t)1− θtωt

1− ωt︸ ︷︷ ︸compensation for risk of correlated asset

+ σξ

(σba,tρξ,a + σbξ,t

√1− ρ2

ξ,a

)︸ ︷︷ ︸

compensation for liquidity risk

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 23 / 38

Solution

Excess Returns

Leverage Growth

Equi

ty R

etur

n

Lagged Leverage Growth

Fina

ncia

l Sec

tor E

quity

Ret

urn

y = 0.12 − 0.31xR2 = 0.17

Leverage Growth

Bond

Ret

urn

Lagged Leverage Growth

Fina

ncia

l Sec

tor B

ond

Ret

urn

y = 0.011 − 0.049xR2 = 0.063

α ↑

α ↑

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 24 / 38

Solution

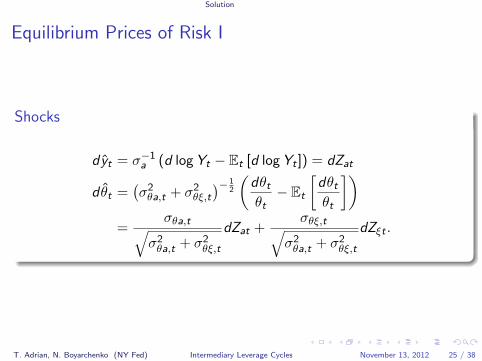

Equilibrium Prices of Risk I

Shocks

dyt = σ−1a (d log Yt − Et [d log Yt ]) = dZat

d θt =(σ2θa,t + σ2

θξ,t

)− 12

(dθtθt− Et

[dθtθt

])=

σθa,t√σ2θa,t + σ2

θξ,t

dZat +σθξ,t√

σ2θa,t + σ2

θξ,t

dZξt .

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 25 / 38

Solution

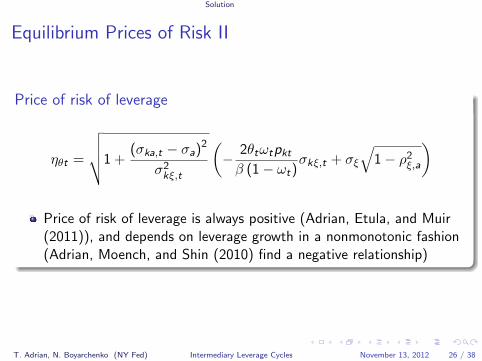

Equilibrium Prices of Risk II

Price of risk of leverage

ηθt =

√√√√1 +(σka,t − σa)2

σ2kξ,t

(− 2θtωtpkt

β (1− ωt)σkξ,t + σξ

√1− ρ2

ξ,a

)

Price of risk of leverage is always positive (Adrian, Etula, and Muir(2011)), and depends on leverage growth in a nonmonotonic fashion(Adrian, Moench, and Shin (2010) find a negative relationship)

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 26 / 38

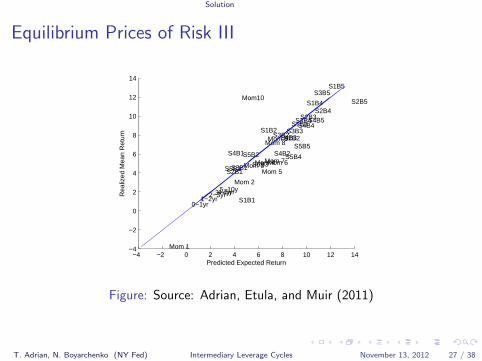

Solution

Equilibrium Prices of Risk III

−4 −2 0 2 4 6 8 10 12 14−4

−2

0

2

4

6

8

10

12

14

S1B1

S1B2 S1B3

S1B4

S1B5

S2B1

S2B2

S2B3 S2B4

S2B5

S3B1

S3B2 S3B3

S3B4

S3B5

S4B1 S4B2

S4B3

S4B4 S4B5

S5B1

S5B2 S5B3

S5B4

S5B5

Mom 1

Mom 2

Mom 3Mom 4Mom 5

Mom 6Mom 7

Mom 8Mom 9

Mom10

0−1yr

5−10y1−2yr

2−3yr3−4yr4−5yr

Predicted Expected Return

Rea

lized

Mea

n R

etur

n

Figure: Source: Adrian, Etula, and Muir (2011)

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 27 / 38

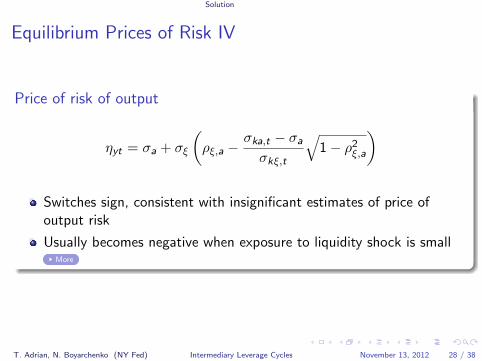

Solution

Equilibrium Prices of Risk IV

Price of risk of output

ηyt = σa + σξ

(ρξ,a −

σka,t − σaσkξ,t

√1− ρ2

ξ,a

)

Switches sign, consistent with insignificant estimates of price ofoutput risk

Usually becomes negative when exposure to liquidity shock is smallMore

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 28 / 38

Distortions and Amplification

Outline

Introduction

The Model

Solution

Distortions and AmplificationSolvencyAmplification

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 29 / 38

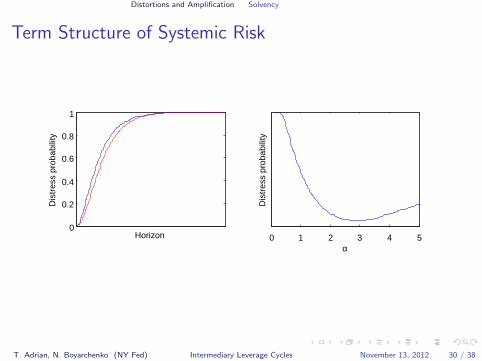

Distortions and Amplification Solvency

Term Structure of Systemic Risk

0

0.2

0.4

0.6

0.8

1

Horizon

Dis

tres

s pr

obab

ility

0 1 2 3 4 5α

Dis

tres

s pr

obab

ility

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 30 / 38

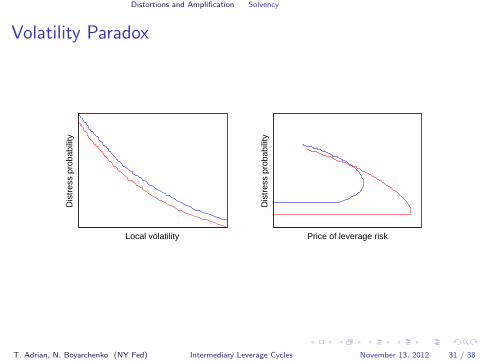

Distortions and Amplification Solvency

Volatility Paradox

Local volatility

Dis

tres

s pr

obab

ility

Price of leverage risk

Dis

tres

s pr

obab

ility

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 31 / 38

Distortions and Amplification Amplification

Constant Leverage Benchmark

Constant expected output and consumption growth

But lower level of output and consumption growth

Constant investment and price of capital

Liquidity shocks have no impact on real activity

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 32 / 38

Distortions and Amplification Amplification

A Sample Path of the Economy

t

Out

put

Con

sum

ptio

n

0

0.5

1

t

Wea

lth

5101520

t

Leve

rage

t

Ret

urn

on d

ebt

BenignFinancial

Crisis

FinancialCrisis

TriggersRecession

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 33 / 38

Distortions and Amplification Amplification

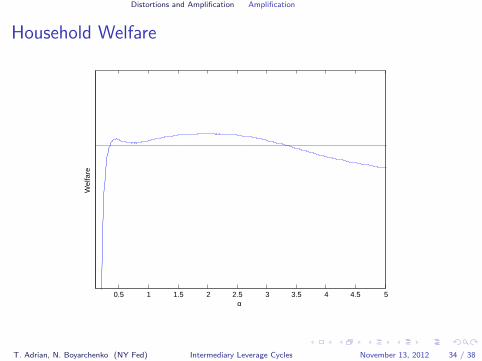

Household Welfare

0.5 1 1.5 2 2.5 3 3.5 4 4.5 5α

Wel

fare

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 34 / 38

Distortions and Amplification Amplification

Conclusion

Dynamic, general equilibrium theory of financial intermediaries’leverage cycle with endogenous amplification and endogenoussystemic risk

Conceptual basis for policies towards financial stability

Systemic risk return tradeoff: tighter intermediary capitalrequirements tend to shift the term structure of systemic downward,at the cost of increased prices of risk today

Model captures important stylized facts:1 Procyclical intermediary leverage2 Procyclicality of intermediated credit3 Financial sector equity return and intermediary leverage growth4 Exposure to intermediary leverage shocks as pricing factor

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 35 / 38

Distortions and Amplification Amplification

Tobias Adrian, Emanuel Moench, and Hyun Song Shin. Financial Intermediation,Asset Prices, and Macroeconomic Dynamics. Federal Reserve Bank of NewYork Staff Reports No. 442, 2010.

Tobias Adrian, Erkko Etula, and Tyler Muir. Financial Intermediaries and theCross-Section of Asset Returns. Federal Reserve Bank of New York StaffReports No. 464, 2011.

Franklin Allen and Douglas Gale. Limited market participation and volatility ofasset prices. American Economic Review, 84:933–955, 1994.

Ben Bernanke and Mark Gertler. Agency Costs, Net Worth, and BusinessFluctuations. American Economic Review, 79(1):14–31, 1989.

Markus K. Brunnermeier and Lasse Heje Pedersen. Market Liquidity and FundingLiquidity. Review of Financial Studies, 22(6):2201–2238, 2009.

Markus K. Brunnermeier and Yuliy Sannikov. The I Theory of Money.Unpublished working paper, Princeton University, 2011.

Markus K. Brunnermeier and Yuliy Sannikov. A Macroeconomic Model with aFinancial Sector. Unpublished working paper, Princeton University, 2012.

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 36 / 38

Distortions and Amplification Amplification

Jon Danielsson, Hyun Song Shin, and Jean-Pierre Zigrand. Balance sheetcapacity and endogenous risk. Working Paper, 2011.

Douglas W. Diamond and Philip H. Dybvig. Bank runs, deposit insurance andliquidity. Journal of Political Economy, 93(1):401–419, 1983.

Ana Fostel and John Geanakoplos. Leverage Cycles and the Anxious Economy.American Economic Review, 98(4):1211–1244, 2008.

John Geanakoplos. Liquidity, Default, and Crashes: Endogenous Contracts inGeneral Equilibrium. In M. Dewatripont, L.P. Hansen, and S.J. Turnovsky,editors, Advances in Economics and Econometrics II, pages 107–205.Econometric Society, 2003.

Mark Gertler and Nobuhiro Kiyotaki. Banking, Liquidity, and Bank Runs in anInfinite Horizon Economy. Unpublished working papers, Princeton University,2012.

Mark Gertler, Nobuhiro Kiyotaki, and Albert Queralto. Financial Crises, BankRisk Exposure, and Government Financial Policy. Unpublished working papers,Princeton University, 2011.

Zhiguo He and Arvind Krishnamurthy. A model of capital and crises. Review ofEconomic Studies, 79(2):735–777, 2012a.

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 37 / 38

Distortions and Amplification Amplification

Zhiguo He and Arvind Krishnamurthy. Intermediary asset pricing. AmericanEconomic Review, 2012b.

Nobuhiro Kiyotaki and John Moore. Credit Cycles. Journal of Political Economy,105(2):211–248, 1997.

T. Adrian, N. Boyarchenko (NY Fed) Intermediary Leverage Cycles November 13, 2012 38 / 38