international solvency and accounting standards … solvency and accounting standards (e) ......

TRANSCRIPT

International Solvency and Accounting Standards (E) Working Group

Agenda

© 2012 National Association of Insurance Commissioners 1

International Solvency and Accounting Standards (E) Working Group Conference Call

Wednesday, March 28, 2012 10:00 a.m. CT (11:00 a.m. ET, 9:00 a.m. MT, 8:00 a.m. PT)

ROLL CALL

Mel Anderson, Chair Arkansas Jim Nixon Nebraska Richard Ford Alabama Ray Conover New Jersey Christina Urias Arizona Alan Seeley New Mexico Kim Hudson/Louis Quan California Joseph Fritsch New York Philip Barlow District of Columbia Dale Bruggeman/Bill

Harrington Ohio

Carolyn Morgan Florida John Doak Oklahoma Cynthia Donovan Indiana Doug Stolte Virginia Jim Armstrong Iowa Peter Medley Wisconsin Jaki Gardner Minnesota Staff Support: Rob Esson/Anne Obersteadt

AGENDA

1. Discuss comments received on the exposed draft ComFrame Module 3, Element 5b and the proposal for possible metrics under ComFrame Module 3, Element 5b

2. Any other matters

w:\National Meetings\2012\Summer\agenda\Intl Acctg_3_28.doc

Discuss Comments Received on the Exposed Draft ComFrame Module 3,

Element 5b and the Proposal for Possible Metrics Under ComFrame Module 3,

Element 5b

California Comments on Draft Proposed Metrics for ComFrame

3-23-2012

The draft metrics proposed in the March 13 memorandum, while useful for general monitoring purposes, are incomplete for that purpose and do very little to measure required capital. In a sense, they represent a significant step backwards in time and sophistication of approach. It is difficult to see this proposal as making any substantive progress toward narrowing the range of target criteria and time horizons for measuring risks to capital, as stated in the Technical Committee’s strategic direction. We are concerned that the IAIS will not view this proposal as a serious effort to fulfill the charge of the Solvency Subcommittee.

The draft metrics are quite limited, and are less complete than the IRIS Ratios that are a standard part of NAIC financial monitoring. It is easy to see that several basic metrics are missing. The very elementary premiums-to-surplus ratio, the simplest measure of underwriting leverage available to property-casualty companies, is not included. There is also no measure of reserve development to test the accuracy of past estimates of claim liabilities. A simple measure of capital adequacy relative to the relevant jurisdiction’s established capital requirement, such as our RBC ratio, would especially seem to be relevant, yet it is not included in these metrics. These are just a few examples; there are undoubtedly numerous others that would be relevant that could be added to the list.

Mention of RBC should remind us that RBC was developed 20 years ago because it was understood at the time that simple metrics such as the premiums-to-surplus ratio were overly simplistic as a means of assessing capital requirements, and something better was needed. The process of developing the RBC formulas involved identifying the major categories of risk typically faced by all insurance companies, and then devising a means of estimating those risks using publicly available information. In recent years, capital modeling has emerged as a tool to evaluate the risks facing individual insurers in a more sophisticated and more tailored way. While the accuracy of these modeling efforts is certainly open to debate, there should be no denying their potential to improve capital assessment.

It seems that reverting to a few simple metrics as the recommended basis for capital assessment for the very large, complex multinational insurance entities we classify as IAIGs could be seen as a step back in time of more than 20 years, and could also be seen as considerably less than a serious attempt to develop effective capital measurement tools in ComFrame. We believe that this approach is not the preferred one, and suggest rather that the NAIC seriously consider the transition period approach we proposed in our January 23 comments and have resubmitted in our current response to the ComFrame Module 3 Element 5 draft.

ComFrame Module 3 Element 5 Draft: California Comments

We note that the Solvency Subcommittee draft of Module 3, Element 5 essentially leaves the determination of the group capital risk measurement up to the group-wide supervisor (in collaboration with other involved supervisors), based on the capital requirements of the various jurisdictions to which the particular IAIG is subject, without establishing any other limitations, and without yet laying out any parameters.

We understand that the Technical Committee has already rejected this approach, apparently on the premise that the draft is not sufficiently responsive to the Technical Committee’s previously provided strategic direction. When this development was discussed at the NAIC Spring National Meeting, we heard that the Technical Committee had in essence directed the Solvency Subcommittee to revisit Module 3, Element 5 and provide a redraft that conforms to the Technical Committee’s strategic direction.

While the Technical Committee’s reasoning was not explained when this development was discussed at the NAIC Spring National Meeting, we make three observations that might have some relevance to the Technical Committee’s response.

First, in the third bullet point in the Module 3 Element 5 introductory comments, the Technical Committee’s strategic direction requires the SSC to “Further develop an approach regarding a range of similar means to address the risks for IAIGs as set out in the Concept Paper”. The SSC response states that it has developed an approach that outlines the risks to be measured. It does not say anything about means to address the risks, other than measuring them, and says nothing about the measurement.

Second, in the fourth bullet point, the Technical Committee’s direction to the SSC is to “Develop a partly harmonised set of standards and parameters which sets out a narrow range of target criteria and time horizons for measurement of those risks.” The SSC’s response is essentially that it is discussing the subject. Confidence intervals, time horizons, and other specific target criteria are not mentioned anywhere in the Module 3, Element 5 draft. There is an implicit promise that the SSC’s discussions will yield a narrowing of standards and parameters, but no progress in that direction is reported in this draft.

Third, in the fifth bullet point, the second sentence reads “Basic principles of internal models and disclosures to allow comparison between various jurisdictions to be spelt out.” The SSC response to this refers to its draft of M3E5b. The relevant portion of the draft appears to be Parameter M3E5b-2-2 which states that the group supervisor will determine how to combine the different risk measurement methods without spelling out how that is to be done.

We continue to be concerned that the strategy that led to the form this draft has taken is a fairly high-risk strategy. The initial response from the Technical Committee has been strongly negative, and it would seem to be an uphill battle to get this new direction reversed. It would also seem that the direction coming from the FSAP Process is that it is highly desirable that the ComFrame initiative will

eventually succeed. The capital component of ComFrame would appear to be fairly central to ComFrame, so its success would seem to be important to the success of ComFrame as a whole.

We think it would be useful to pursue the strategy outlined in our comments submitted prior to the late January meeting of the Solvency Subcommittee in Basel, and we resubmit those comments as part of this communication.

1

Com Frame Suggestions

California Insurance Department

January 23, 2012

We believe that it is important to take a principled stand in the ComFrame effort in support of the key elements of our solvency system that have stood the test of time. At the same time, we also believe we need to take into consideration any implications coming from the FSAP review. We provide an attachment that summarizes some of the observations and recommendations coming out of this review. In particular, we note that the comments on ICP 17 and ICP 23 seem to be particularly relevant. We offer the following constructive concepts that could be used to bridge the gap between our system and the approaches preferred by other countries in a way that could meet our core concerns as well as theirs. With that, we offer the following concepts as suggestions for consideration.

1. Establish a transitional period of several years in which group capital requirements would be informational only and legal entity capital requirements would be the ones that have legal and practical effect. (Recognize that a learning period is required, that we are not ready to agree to a binding international standard just yet, for a variety of very good reasons.)

2. During this transitional period, require a group ORSA, and study these documents intently to determine the following, much of which we believe should typically be part of any ORSA review:

a. Whether there are any areas of risk requiring immediate or near-term attention of the supervisors of the IAIG: (If so, discuss among the involved supervisors and use existing regulatory authority over the individual legal entities in the individual jurisdictions to take appropriate action)

b. The general level of management competence in the area of capital management (this would of course be confidential opinions that regulators would keep to themselves within the regulatory community)

c. If there is a “consensus” or “best practices” approach common to the better run groups for the management of capital and the determination of required capital:

i. What tools and criteria does management use to manage capital?

ii. How often are internal models used? iii. What is the “state of the art” of capital models- how good are they?

2

1. How well do they model the insurer group’s risks, and what risks are poorly modeled or not modeled at all?

2. How good are the assumptions that management makes as inputs to the models? Are they well thought out, do they appear valid, or are they inadequately determined or biased?

3. How good is the data quality, and how complete is it? iv. What is the consensus of what level of capital is optimal- i.e. the balance point

at which protection is sufficient but the amount of capital is not so great as to cause an undue cost of capital to be borne by policyholders in the form of excessive rates (It is not clear that the 99.5% confidence interval choice is based on any such considerations; we should consider this concept essential) (Optimal, or “economic” capital should not be the level of capital we regulate, but knowing this level establishes an absolute ceiling well above where the uppermost regulatory intervention level should be; it is an essential “yardstick” that should aid the determination of the regulatory intervention levels)

d. What levels of capital (relative to regulatory minimum capital and specified confidence levels) are held in practice by IAIGs

e. Compare the total of individual entity capital requirements to group capital requirements. Observe how often the group capital requirement is greater than the sum of the individual requirements, then determine why, and summarize the learning experiences- are there significant risks at the group level that regularly outweigh the diversification benefits inherent in group size and structure, or not? If there are, what are they?

3. Also during the transition, consider the following items, which could be useful for developing a “partially harmonized” approach to assessing Group Capital that may be mutually agreeable within the ComFrame effort:

a. Determine the track record of each major regulatory regime in terms of both frequency of insolvency broken down by groupings based on stated capital strength, and also in terms of policyholder claims left unsatisfied due to insolvency;

b. Compare the regulatory approaches used by the various major jurisdictions and compare the strengths and areas for improvement of each;

c. Determine which elements of the US system are important enough that they should be

included in the joint international regulatory approach to IAIGs- and do the same for other key jurisdictions’ approaches

3

(This both satisfies one of our key concerns and addresses the basic principle that a “harmonized” approach, in order to win acceptance of all involved, should adopt the best elements of each major jurisdiction involved.)

d. Make a serious effort to calibrate US RBC to the equivalent of a confidence level/time

horizon measurement. Do the same for any similar regulatory capital formula. (This will be important for the ability to compare different formulas, and we think this information could be useful.)

e. Consider the unique aspects of IAIGs that require them to maintain capital above the

level implied by US RBC Company Action Level, such as the reputational damage caused by failure to maintain a specified rating agency rating; (a practical example is that most significant commercial firms require their insurance be placed with “A” rated insurers, so loss of an “A” rating means loss of business and a negative spiral; IAIGs presumably suffer reputational damage earlier than this (i.e. at a higher rating))

f. Consider evaluating a possible modification to RBC for IAIGs only to establish another “intervention level” above Company Action level that would conceptually involve softer actions- perhaps just call it a “watch” level and require mandatory conferences between the IAIG management and regulators- with the upper boundary of this “action level” set at a level at which US regulators agree that reputational damage is likely to occur if capital is not increased. (This concept is necessarily loose but might provide a “bridge” necessary to merge US capital requirement concepts with those of the EU and other jurisdictions who are content with the 99.5% confidence interval over a one-year time horizon.)

4. Near the conclusion of the transition period, a group capital formula and approach could be developed based on the learning experiences gained during the transition period, and taking into proper consideration the principles outlined above.

FSAP Findings/Recommendations Principle Recommended Action ICP 1 – Conditions for effective insurance supervision The authorities should (i) increase information-sharing and coordination between state regulators and federal authorities, including representation of state regulators in national bodies with responsibilities for system wide oversight and financial stability; (ii) agree policies and procedures for the regulation of systemically important institutions, markets and instruments, where assessed to exist in the insurance sector; and (iii) make new arrangements to increase the authority of federal authorities in relation to the implementation of international agreements. ICP 2 – Supervisory Objectives Insurance departments, the NAIC and state legislatures should develop a clear, joint statement of the objectives of insurance regulation, taking into account good practice internationally, and align the objectives of individual state departments with these objectives. This work should address whether there are potential conflicts between existing objectives and how to manage them and the need to balance the objectives of achieving financial safety and soundness and consumer protection with the desirability of fostering market efficiency and competitiveness. ICP 3 – Supervisory authority The NAIC and state legislatures should make reforms including (i) providing for fixed terms to be standard for commissioner appointments, with dismissal mid-term to be possible only for prescribed causes and with publication of reasons; (ii) making departments fully self-funding, subject to continued accountability to and oversight by state legislatures, while allowing them greater flexibility to hire staff with specialist skills and reduce reliance on external experts; and (iii) extending the rule-making powers of departments to a wider range of technical issues (for example valuation and risk-based capital), and subject to appropriate consultation and requirements for due process. State laws should be changed, where this has not already been done, to extend the protection of information received from other government agencies to foreign agencies, which is essential to support the widest scope of informationsharing internationally. The NAIC and state legislatures should consider extending the protection of confidentiality, to the extent consistent with the wider legal environment, to all relevant information which is received by departments, rather than limiting protection according to the source of the information, as at present. ICP 4 – Supervisory process To further improve the transparency of its work, the NAIC should: (i) make publicly available some information that is currently available only on payment of a fee or by subscription (for example the NAIC model laws and material on how states have adopted them); (ii) publish summary information on their assessment of states’ compliance with accreditation standards (even if scores

remain private); and (iii) commit to publication on a regular basis (maybe every two years) of their self-assessment of compliance with IAIS Insurance Core Principles. These measures would help to foster improved understanding of state regulation and the role of the NAIC. In addition, the NAIC could also consider developing its approach to regulatory impact analysis and making such work a routine part of its analysis of proposed new or changed requirements. ICP 5 – Supervisory cooperation and information sharing The states and NAIC should continue to develop the network of MoUs. As mentioned in connection with ICP3, all state insurance departments should ensure that laws are updated to enable them to protect information received from foreign regulators. This will ensure that overseas regulators are not deterred from sharing information freely. ICP 7 – Suitability of persons Specific requirements in relation to individuals’ fitness and propriety should be adopted. Gaps in the requirements of departments should be filled—companies should have to notify the department of concerns about the fitness and propriety of key individuals and departments should be able to disallow functionaries from holding two positions that could result in material conflict. ICP 9 – Corporate Governance As examiners gain experience, the NAIC and/or departments should consider issuing more guidance on good and bad practices in corporate governance for insurers. This would help examiners and firms to develop a clearer expectation of what constitutes effective governance for insurance business, including for groups. ICP 10 – Internal controls As examiners gain experience, the NAIC and/or departments should consider the scope for issuing guidance on good and bad practices in internal control. They should also make it a formal requirement for insurers to have an internal audit function. Such a function is now widely considered as an important part of a good control framework—similarly to audit committees, where there are now extensive requirements of all but the smaller insurers. ICP 11 – Market analysis Regulators should collect more complete group-wide consolidated data for insurance groups and broader financial conglomerates. They should develop further their analysis of developments outside the U.S. markets. ICP 12 – Reporting to supervisors and off-site monitoring Collection of group-wide consolidated data for insurance groups and broader financial conglomerate groups should be introduced.

ICP 15 – Enforcement or Sanctions The insurance laws should be changed to provide the supervisory authority with powers to fine individual directors and senior managers of insurers, and to bar them from acting in responsible capacities in the future. ICP 17 – Group-wide Supervision U.S. supervisors should (i) include fuller assessment of the financial condition of the whole group of which a licensed insurance company is a member; this may involve quantitative techniques and practices in use internationally; (ii) extend the risk-focused approach to examinations of solo insurance companies to groups, again starting with U.S. groups—in effect extending the lead regulator and college of regulators arrangements already in widespread use for such groups within the framework developed by the NAIC; (iii) ensure that colleges of supervisors for the U.S. groups with major international operations are established and functioning effectively—and led by U.S. regulators with appropriate insurance expertise. It may also be desirable for insurance regulators to be given additional powers, such as clear authority to license insurance holding companies, apply insurance capital requirements to the consolidated insurance group and direct the insurance holding company to make changes at the group level to rectify any shortcomings. ICP 18 – Risk assessment and Management The relevant laws, regulations or standards should be changed to include a requirement that an insurer have in place comprehensive risk management policies and systems capable of promptly identifying, measuring, assessing, reporting and controlling their risks. ICP 19 – Insurance activity The relevant laws or regulation should explicitly provide that an insurer must have in place strategic underwriting and pricing policies approved and reviewed regularly by the Board. ICP 23 – Capital adequacy and Solvency For general transparency and for comparison, it is recommended that consideration be given to specifying a target safety level for reserving and an associated target safety level for capital. This should assist not only with peer comparisons of reserving and capital across insurers, but also comparisons against other insurance regimes internationally. Requirements to address inflation of capital through multiple gearing (i.e., holding company debt raisings injected as equity into insurance subsidiaries) should be included in the law, regulation or rules. Further development of stress testing could be considered, using the experience gained from exercises undertaken during the financial crisis. ICP 24 – Intermediaries Some strengthening of the approach to producer regulation is recommended: (i) to extend broker trust fund arrangements across states (where not already in

place) to ensure that client funds are fully protected; (ii) to develop a uniform approach to the regulation of major brokers which reflects the important role which large brokers play in the commercial lines market; and (iii) to complete the current work on a consistent approach to the regulation of commission disclosure. In addition, producers should be required to make disclosures to customers of the status under which they are doing business, including which insurance companies have appointed them. ICP 28 - Anti-money laundering, combating the financing of terrorism It is recommended that a timetable is set for the agreement and implementation of new arrangements between state insurance departments and federal authorities that will deliver greater resourcing of supervisory activities as well as necessary information exchange

March 23, 2012

Mr. Ramon Calderon

National Association of Insurance Commissioners

1100 Walnut St, Suite 1500

Kansas City, MO 64106-2197

Re: IAIS Module 3 Element 5 & Possible Metrics for Use Under ComFrame

Dear Mr. Calderon:

NAMIC is a trade association comprising approximately 1,300 mutual property/casualty

member insurers domiciled in the United States and another 100 in Canada. The 1,300

members domiciled in the United States write approximately 37 percent of the annual

property/casualty premium in this country. NAMIC appreciates the opportunity to

provide comments to the National Association of Insurance Commissioners regarding the

latest draft of the International Association of Insurance Supervisors (IAIS) Common

Framework (ComFrame) document for Module 3, Element 5b, as well as proposed

metrics for use under ComFrame.

The IAIS has described the goals of the ComFrame to include 1) Developing methods of

operating group-wide supervision of Internationally Active Insurance Groups (IAIGs) in

order to make group-wide supervision more effective and more reflective of actual

business practices; 2) Establishing a comprehensive framework for supervisors to address

group-wide activities and risks and also set grounds for better supervisory cooperation in

order to allow for a more integrated and international approach; 3) Fostering global

convergence of regulatory and supervisory measures and approaches.

NAMIC believes that while improvements could be made to the regulation of insurance

groups, the key to such improvements has already been identified in the formation of

supervisory colleges. Consequently, NAMIC agrees with the comments made by

members and representatives of the NAIC that ComFrame is not practical and far too

prescriptive. Additionally, NAMIC has concerns that ComFrame as drafted conflicts with

the current approach taken toward insurance regulation in the United States.

Consequently, the result of such an approach can only lead to a redundant layer of

regulation.

As previously stated, the IAIS has already established the most important aspect of group

regulation in the form of supervisory colleges. Such forums have been used for years in

the United States, but what U.S. regulators may be able to attest to is that the success of

such forums can only be obtained by regulators after a period of working together.

2

NAMIC believes that the history of working together allows regulators to share different

perspectives on different issues and this is far more important than a specific way of

measuring a very specific risk. However, if the primary goal of ComFrame is improving

group supervision, frankly, the result of any supervisory college, or ComFrame, should

be discussions between management and the supervisors regarding those risks that either

the supervisors or management believe are noteworthy. NAMIC believes that the vast

majority of a supervisory college should revolve around management describing how the

insurance group is managed, including presenting various information that it uses to do

so. NAMIC believes U.S. regulators already recognize the importance of such

information since the U.S. risk-focused surveillance system and U.S. ORSA are revolved

around this concept.

NAMIC supports and is appreciative of the many comments made by members and

representatives of the NAIC who seem to already recognize these views. NAMIC

specifically supports the view taken within the NAIC ORSA that focuses on group-wide

capital assessment as opposed to a specific quantified group-wide capital requirement

established with a regulatory specified risk measure at a regulatory specified time

horizon. NAMIC also supports the concept of what the NAIC has recently proposed with

respect to possible metrics for use under ComFrame. We support the concept because we

agree that in order to truly understand the group one must look at so many other facts

than simply a group capital calculation. Additionally, what is most important is the

amount of capital available within the insurance legal entity to pay future possible claims,

and we think the current U.S. system appropriately recognizes this importance and

therefore appropriately views the group capital as additional information that is helpful to

understand the risks of the group and potential sources of capital for individual entities

within the group, but it shouldn’t be the driving force in the regulation of insurance.

However, we do not believe the use of these specific metrics will necessarily improve

group supervision. While we are not opposed to supervisors calculating them using the

financial statements of the insurer, we believe it would be more beneficial to look at the

metrics used by management. In addition to our main point that what is most important is

that the supervisor understands the risks of the company from the perspective of

management, we believe great caution should be used with such metrics as they may be

misleading when calculated on a group basis where different types of businesses are

combined. We have concerns that such metrics would vary significantly between

different types of insurers. Specifically, the business model of a property/casualty insurer

is much different from a life insurer, and consequently useful metrics should differ as

well.

The use of the same approach for insurers with different business models leads us to

another concern of the exposure draft: the area of accounting. We note that the

International Accounting Standards Board (IASB) believes that the same accounting

model should be used by property/casualty insurers that is used by life insurers (the one

model method). Fortunately, the Financial Accounting Standards Board (FASB)

3

recognizes that two models are more appropriate (the two model method), and the FASB

is currently favoring an approach that is much closer to statutory accounting than the

IASB views.

It is unclear where the IASB will end up with its insurance contract project, and it is also

unclear what presentation requirements will be prescribed under the building block

measurement model. It is possible a margin format will be required for income statement

reporting thereby reducing the availability of underwriting components upon which some

of the desired metrics can be based. NAMIC is strongly opposed to the use of IFRS

within ComFrame. Again, NAMIC believes the information used by supervisory colleges

should be that information that is used by the group to manage itself. This includes but is

not limited to financial statements. The use of U.S. GAAP, or even statutory in the case

of insurers that do not prepare U.S GAAP statements (such as mutual insurance

companies), should be allowed. NAMIC believes that requiring a company that does not

otherwise prepare IFRS statements is an unnecessary cost that should be avoided.

NAMIC also believes that just as it would be inappropriate for ComFrame to require the

use of U.S. GAAP for non-U.S. companies that write only 10 percent of their business in

the United States, so, too, is it inappropriate for ComFrame to require the use of IFRS for

U.S. companies that only write 10 percent of their business outside of the U.S.

Respectfully,

Dan Daveline

Financial Regulation Manager

From: Dana Hunt Sent: Friday, March 23, 2012 2:20 PM To: '[email protected].' Cc: '[email protected]' Subject: ComFrame: IAIG Capital - Comments to NAIC

Ramon, thanks for the opportunity to provide input. Here are comments from some experienced U.S. actuaries.

Sincerely, Dana

Dana Hunt VP, SOLVENCY II & FUTURE DEVELOPMENT Aviva USA 7700 Mills Civic Pkwy, West Des Moines, IA 50266-3862 Tel: 515-342-3747 E-mail: [email protected]

Review of ComFrame Modules 3-5 and 3-5b by experienced actuaries

Item

Comment

M3E5b-2-1 Concern that subsidiary legal entities in countries not domiciled in country of Group-wide supervisor may be penalized by having to hold ‘higher of’ two capital requirements. How will supervisors, in practice, work out the differing jurisdictional capital requirements, so as not to negatively affect global commercial interests?

3-5, fourth bullet: “Develop a partly harmonized set of standards and parameters…”

Could the SSC expand on what is meant by “harmonized”? It’s meaning isn’t obvious. What components are being harmonized? In addition, for “partly harmonized”, what elements would be in- or exclude?

3-5b, Specification M3E5b-2-3-1: towards the end of the first paragraph “… if so, allowance for the risk reduction may be made…

It seems that after consideration of counterparty risk, allowance for the risk reduction should (rather than may) be made.

3-5b, Specification M3E5b-3-1-1: non-insurance risks

Should “non-insurance risks” be included on the list in the first column (Parameters)?

A1(2w

MS D M MN1K Ru TMeaPafr Gerc Cdj Itars Ij

American Council 101 Constitution A202) 624-2313 t

www.acli.com

Michael MonahaSenior Director,

DELIVERED V

March 27, 201

Mr. Ramon CaNational Asso1100 Walnut Kansas City, M

Re: ComFramunder ComFra

The AmericanModule 3, Eleexposed for calso appreciatPolicy Staff readdressed in Cfraternal benerepresent ove

General Commeffective grouresource‐intecapital and va

ComFrame, atdesigned to purisdictions.

nsurance matherefore be facceptance anreporting systsufficient for C

n our view thurisdictions r

of Life Insurers Avenue, NW, Was (866) 953-4083

an Accounting Pol

VIA E-MAIL

12

alderon ociation of InsSt, Suite 1500MO 64106‐219

me Module 3, ameDear Mr.

n Council of Liement 5 introomment by tte the opportecently exposeComFrame Mefit society mer 90 percent

ments: ACLI sup‐wide supernsive and cosaluation.

t its core, shorevent or min

rkets around flexible enougnd legitimacytems and othComFrame pu

he group supeegulating an

shington, DC 2003 f robertneill@ac

licy

surance Comm0 97

Element 5 an Calderon:

ife Insurers (“ductory commhe Internatiotunity to comed relating to

Module 3, Elemmember compof the assets

supports the rvision. Howestly new requ

ould be flexibnimize the ne

the world cogh to accommy. Where apprer regulatoryurposes.

ervisor shouldInternational

001-2133 cli.com

missioners

nd March 13,

“ACLI”) apprements and thonal Solvency ment on the o possible mement 5b. Wepanies operatis and premium

overarching aever, we encoirements for

le enough to eed to establis

onsist of variemodate for thropriate capity tools current

d respect the lly Active Insu

2012 NAIC m

ciates the ope draft of Comand AccountMarch 13, 20trics for use u represent ming in the Unims of the U.S

aim of ComFrourage the NAmany of our

permit evolush new statut

d jurisdictionhese specific jtal adequacy tly exist, Com

valuation andurance Group

memorandum

pportunity to mFrame Modting Working 012, memoraunder the Gro

more than 300ited States. OS. life insuranc

rame to ultimAIC to resist tmember com

utionary changtory powers w

nal regulatoryurisdictional standards, in

mFrame shoul

d solvency stap’s (IAIG’s) res

m on possible

comment ondule 3, ElemeGroup (Workndum that NAoup Capital A0 legal reserveOur member ce and annuit

mately create the creation ompanies, in th

ge in superviswithin the rel

y frameworksattributes to

nternal controld defer to th

andards of suspective legal

metrics for us

the ComFrament 5b which wking Group). WAIC InternatioAssessment e life insurer acompanies ty industry.

a forum for of extremely his case conce

sion and alsolevant

and must achieve globol requiremene same as

upervisors in l entities.

se

me were We onal

and

erning

be

bal nts,

other

-2- There is also an over‐arching question that we think should be clarified within ComFrame and for the purposes of the proposed Group Capital Assessment metrics ‐ what constitutes a group that is to be subject to ComFrame itself? As you know, some insurance groups, especially U.S. insurance groups, reside within conglomerate organizations of which they are a part, sometimes a major part and sometimes less so. It is thus difficult to assess how the metrics could, or would, be applied in such circumstances. We have reviewed the exposed documents and offer the following comments. NAIC Memorandum on Possible Metrics for Use Under ComFrame On a conceptual level identifying commonly accepted reliable metrics and encouraging their use by the IAIG supervisors is reasonable, provided that the supervisors for the specific IAIG determine which metrics are most appropriate in their circumstance and jurisdictions. The available metrics should not be constrained or prematurely prescribed by the ComFrame and should be sufficiently vetted by IAIS members and observers to ensure that there is appropriate flexibility going forward and that examples can be tailored to meet parameters of varied jurisdictions. We would point out that the formulae/metrics provided to explain the high‐level indicators in the draft memorandum will not , in our opinion, provide regulators with the kind of information they would need to make appropriate group capital assessments and could yield inaccurate results. For this reason, we would appreciate the opportunity to offer more specific comments if identifying commonly accepted reliable metrics becomes the direction of the IAIS Solvency Subcommittee. We believe it is critically important that supervisors continue to consult with industry at every possible stage as we continue to further develop and offer our analysis on these metrics and on existing supervisory tools. Liquidity: We suggest that the metric on liquidity is the inverse of what is usually considered liquidity. The proposed ratio defines liquidity as Liability/Liquid assets. We also observe that the NAIC has already developed a template to give regulators information about matters relating to “liquidity risk,” or the likelihood that the insurer might have to come up with cash quickly. Stress Tests: We suggest that significant thought and discussion is needed before offering specific stress test scenarios and recommend that internal models and company liquidity stress tests would be a better measure of liquidity risk. Market Risk: All of the market risks mentioned can be addressed by effective hedging strategies. Module 3 Element 5 Introductory Comments Bullet point 2 – IFRS (“or reconciliation to IFRS”) remains the “working assumption” in this document. It states that the “SSC [IAIS Solvency Subcommittee] recognizes the need to use the IFRS balance sheet (or conversion to IFRS balance sheet through appropriate means) as a starting point for all considerations of the capital component”. ACLI members recognize that IFRS may be one useful element for supervising IAIGs. However, requiring that it be the “starting point for all considerations” could lead to unwelcome consequences. For example, creating an IFRS balance sheet for an entity within an IAIG which does not have one, but is well capitalized and financially strong based on reliable local solvency metrics, seems unnecessary and costly. In our view, therefore, the document should be changed to allow the aggregation of local supervisory valuation and solvency rules to be used at a group level. This would, of course, require regulators to be

fHda BrctPdft Norca WW S

MS

fluent in the mHowever it wodisrupting localong with co

Bullet point 4regulators thrcapital for IAIGthat the metrPrinciples (ICPdecide that cefamiliarity witthe local regu

Narrowing theoverly prescrireflect that thconsistent witapproaches, i

We appreciatWorking Grou

Sincerely,

Michael MonaSenior Directo

more commoould avoid imal insurance rresponding c

‐ The emphasrough a “narrGs that is narics available tPs). We realizertain capital th the IAIG anlators.

e metrics avaptive and unnhe IAIG regulath the categonternal mode

e the opportuup.

ahan or, Accountin

nly used valumposing a potmarkets—by capital requir

sis in this poinow range of trrower than cto the IAIG ree that in ordemetrics may nd associated

ilable to IAIGnecessary. Wators should dories reflectedels, combinat

unity to provi

g Policy

ation bases, centially signifrequiring IAIGrements.

nt appears totarget criteriacurrently allowegulators miger to supervisbe more usef risks. Any re

G regulators bWe believe thedetermine thed in Parameteions of those

ide our comm

-3-

capital frameficant burdenGs to adopt w

o be on narrowa and time howed for undeht be fewer tse a particulaful than othegulatory actio

efore they dee language in e appropriateer M3E5b‐2‐2 listed).

ments and loo

eworks, and ren on IAIGs—awhat could be

wing the capiorizons” or ther the ICPs.” Tthan those avr IAIG that thers. That concon would occ

etermine the this bullet poe measureme2 (factor based

ok forward to

eporting reqund thus potene a new accou

ital metrics avrough an “asThis languagevailable in thee involved suclusion wouldcur under the

appropriate oint should bents for capitad methods, st

discussing th

uirements. ntially even unting framew

vailable to IAsessment of e indicates to e Insurance Coupervisors ma be based on laws availab

approach seee changed toal assessmenttandard

hem with the

work,

IG

us ore ay their le to

ems o t

From: Robert Kasinow [[email protected]] Sent: Friday, March 23, 2012 10:39 AM To: Calderon, Ramon Subject: Exposed for Comment: A Proposal on a Way Forward to Group Capital Assessment Addressed in ComFrame Module 3, Element 5b

Ramon, Below are a few thoughts from a perspective as a regulator and now supporting regulators after following the ComFrame closely at the IAIS and NAIC The memorandum suggests the use of high level ratios as indicators. Financial ratios as key indicators without a common and consistent basis of financial reporting would yield differences such a ratios under IFRS and ratios under U.S. Statutory. If a comparison was done on volatility, I believe ratios would be more volatile under IFRS than even US GAAP. Leverage and Liquidity ratios definitely would be affected by FV accounting practices leaving the question, are they comparable. If the result is a suggestion to use ratios perhaps added to that should be a required reconciliation, do I dare say to IFRS, so at the very least, the ratios can be view collectively with knowledge of the surplus effects of different accounting methods. On the stress testing, in addition to the equity shock being tested of 30%, perhaps a test tied to the S&P number, similar to the equity shock but still different in that in should test for markets seizing up with limited access to credit. Best regards, Bob Robert B. Kasinow CFE, ARe | Director Examination Resources, LLC 2150 Highway 35, Brook 35 Plaza, Suite 250 | Sea Girt, NJ 08750 email: [email protected] O: 732-359-0201 | F: 732-359-0206 | C: 908-433-9409 website: www.examresources.net

Stephen W. Broadie Vice President, Financial Policy

March 26, 2012 Mr. Ramon Calderon Chair, IAIS Solvency and Actuarial Issues Subcommittee National Association of Insurance Commissioners 1100 Walnut St., Suite 1600 Kansas City, MO 64106 Dear Mr. Calderon: The Property Casualty Insurers Association of America (PCI) appreciates the opportunity to comment on the draft ComFrame Module 3 capital assessment language and Possible Metrics under ComFrame document exposed by the NAIC’s International Solvency and Accounting Standards (E) Working Group. We also appreciate the extra time granted us to respond to these documents. PCI strongly supports the NAIC’s position that the International Association of Insurance Supervisors’ (IAIS) ComFrame (Common Framework for the Supervision of Internationally-Active Insurance Groups) project should facilitate supervisors’ capital assessment of IAIGs, rather than attempting to promulgate a uniform international capital standard, and that a one-size-fits-all approach will not work. We appreciate your work with other concerned international supervisors to develop language intended to implement the capital assessment concept. This is a very complex issue, however, and we believe that much more discussion is necessary before we arrive at final language. The Working Group’s conference call on March 28 is a very good start, and we look forward to discussing these issues with you. We also appreciate the efforts of staff who drafted the “Possible Metrics” memo, and we look forward to discussing it with staff and regulators. We note, however, that there are many reasons why financial ratio results may differ between (and within) insurance groups – differences in types of business (life vs. P/C), lines of business (property vs. casualty), geographical exposure and the extent to which insurance activities are predominant within a group can produce significant differences in the financial ratios of healthy groups. We are skeptical that one set of financial ratios and stress tests can be designed that will apply to all groups. We would also like to mention some textual issues in the draft Module 3 language:

Specification M3E5b-3-4-1 (p. 98) -- o Probably should read "Attention will have to be paid to (or given to) consequences arising

from changes in the group structure . . .". o The second paragraph should apply only if the IAIG has been determined to be a G-SII

(global systemically important insurer).

Specification M3E5c-1-1-1 (p. 101) -- As part of the definition of "available capital resources", the paragraph reads "Defined technical provisions and other liabilities in accounting terms, such as perpetual subordinated debt, asset valuation reserve, and dividend liability may be treated as available capital resources instead of liabilities in the valuation for solvency purposes." If the point is that some items that may generally be considered to be accounting liabilities (such as surplus notes in the US) may also be considered to be part of available capital resources, the sentence should be rewritten to make this point more narrowly. As written, this language implies that loss and LAE reserves ("technical provisions") could be considered to be available capital resources.

2

Module 3, Element 5d (p. 107) clearly imposes a minimum capital requirement at the group level. It appears that the requirement and the ladder of regulatory intervention would differ on a group-by-group level. The consequences of this concept require much thought. One issue is due process -- will requirements (and the consequences of breach) be required to be made clear to the groups, based on the jurisdictional law of the group-wide supervisor?

o Parameter M3E5d-1-1 also implies that, even if the group PCR (Prescribed Capital Requirement) is "a consistent and interdependent set of PCRs for legal entities that are members of the group" rather than a single group-wide PCR, this "should have no bearing on the way that individual regulated entities of the group have their capital adequacy assessment set within their own jurisdictions." Does that mean then that the individual legal entities will in effect have two different PCRs, one that triggers action against the company and another to be used to compute the level at which actions are taken against the group?

o Specification M3E5d-1-1-2 suggests that group-wide supervisors of large IAIGs may have recovery and resolution plans ('living wills") in place, and that "they will form the basis for the different levels of intervention that the supervisor imposes". We question strongly whether this is appropriate for insurance groups. Unlike the banking industry for which the concept of "living wills" is designed, insurance regulation the world over features strong provisions for orderly resolution. The living will process also involves guessing the reason why the insurer may fail, which makes it much more likely that if the insurer fails it will be for an unforeseen cause.

These comments are meant as initial thoughts on very important concepts, and we hope the Working Group’s March 28 call continues a process of increased dialogue between the NAIC and the industry on this and other ComFrame issues. We look forward to the discussion during tomorrow’s call.

Sincerely,

Stephen W. Broadie

March 27, 2012 Mel Anderson Chair, NAIC International Solvency and Accounting Working Group Comments on ComFrame Module 3, Element 5 Draft and Possible Metrics Dear Chairman Anderson: The Group of North American Insurance Enterprises (GNAIE) appreciates the opportunity to comment on the working draft of ComFrame Module 3, Element 5 and the possible metrics for use under ComFrame. ComFrame Module 3, Element 5 GNAIE supports the broader use of Enterprise Risk Management by companies and in supervisory assessments as described in Module 3. We believe ERM should be at the heart of ComFrame. GNAIE has said in its earlier comments on the ComFrame draft that we agree with the NAIC that a group capital assessment, which includes a review of all risks to which a company is exposed, is a more productive approach than a group capital requirement. We have numerous concerns regarding the practical application of a group solvency requirement as included in the recent working papers on ComFrame, including the following:

• If there were a group capital requirement, where would the capital be held? • How would offset for capital already held at the legal entity level be applied? • How would a group capital requirement be implemented in the US? • What would be the objective of a group capital requirement? Who would such a

requirement protect? • How would such a requirement reconcile with the ICPs, which are being implemented in

each jurisdiction? We continue to oppose a ComFrame valuation based on IFRS (or reconciliation to IFRS) as a working assumption with filters as needed. It is premature to introduce this requirement since the IFRS Insurance Contracts Standard has not been completed. Although the concept of an international standard is enticing, at the moment, we have not seen consistent implementation of the IFRS standards that do exist and are concerned that the new standards will also vary by jurisdiction. As we have said before, we also do not think that ICP 14 will serve as a common measurement basis and that additional work needs to be done on this standard.

Possible Metrics for Use under ComFrame GNAIE’s initial response to the metrics proposed in Rob Esson’s memo of March 13 raise an approach to ComFrame which we would suggest be explored further. If such common metrics can be developed, these will help to address the comparability objectives of the supervisors outside the US without placing too much reliance on a single number such as a confidence level. Our initial reaction is that separate calculations will need to be made for these metrics by lines of insurance if they are to be meaningful and that different measures may be appropriate for differing lines of insurance. These issues should be explored. We understand that these ratios are similar to the FAST ratios. Obviously, one issue in the use of these ratios outside of the US is whether they will work if the inputs are based on differing valuation methods. We would support further exploration and testing of the ratios in that regard. We are somewhat more concerned about the value of common stress tests, since groups already use stress tests that are appropriate to their own business and risks. Much more work would need to be done to determine whether there is value in applying common stresses. Thank you again for the opportunity to comment. Sincerely, William Sergeant Chair, GNAIE Solvency Committee cc: Rob Esson, Ramon Calderon

M E M O R A N D U M

DATE: March 13, 2012

TO: [Ultimately SSC – for the present internal draft] CC: Elise Liebers

FROM: Rob Esson

RE: Possible metrics for use under ComFrame

This memorandum articulates some US supervisory views with regard to developing ComFrame specifications for the assessment of group capital. Thus far, we recognize the difficulty in developing criteria that results in a common methodology for assessing group capital across jurisdictions due to a variety of reasons, including differences in accounting frameworks, differences in product designs, differences in legal frameworks, and differences in supervisory and solvency frameworks.

We believe that ComFrame specifications can be developed that would promote commonality in approach and would narrow the approaches to assessing group capital adequacy. These specifications would be built on common metrics that most jurisdictions currently use. These common metrics can take the form of financial ratios (or other leverage ratios) and can be used by supervisors around the world to prompt further action if the financial ratios are out of range (to be defined later).

The purpose of this memorandum therefore is to investigate such a narrowing of assessments: these might be regarded as ideas with which we can walk before we try to run. The ideas are all based on ratios and stress testing, and consequently do not result in any one specific monetary capital requirement, which may be difficult to achieve in the short term. Nonetheless they may well constitute a common basis for further discussion and development.

We have tried to find a small set of 5 high level indicators that seem to be relatively universal between regulators, rating agencies, and analysts. We have grouped these indicators under various headings although these are merely indicative. As the results are ratios, they may be a little less sensitive to differences in accounting standards, and the trend of the ratios may be more illuminating than a single ratio on its own. One would expect that one could derive current and prior year ratios from the public financial statements of IAIGs.

While individually none of these metrics will provide a perfect answer, collectively the ratios provide a picture or assessment of the IAIG as a whole. The appropriate ranges for the ratios would be subject to negotiation, but we have tried to indicate some thoughts about relative size and their meanings.

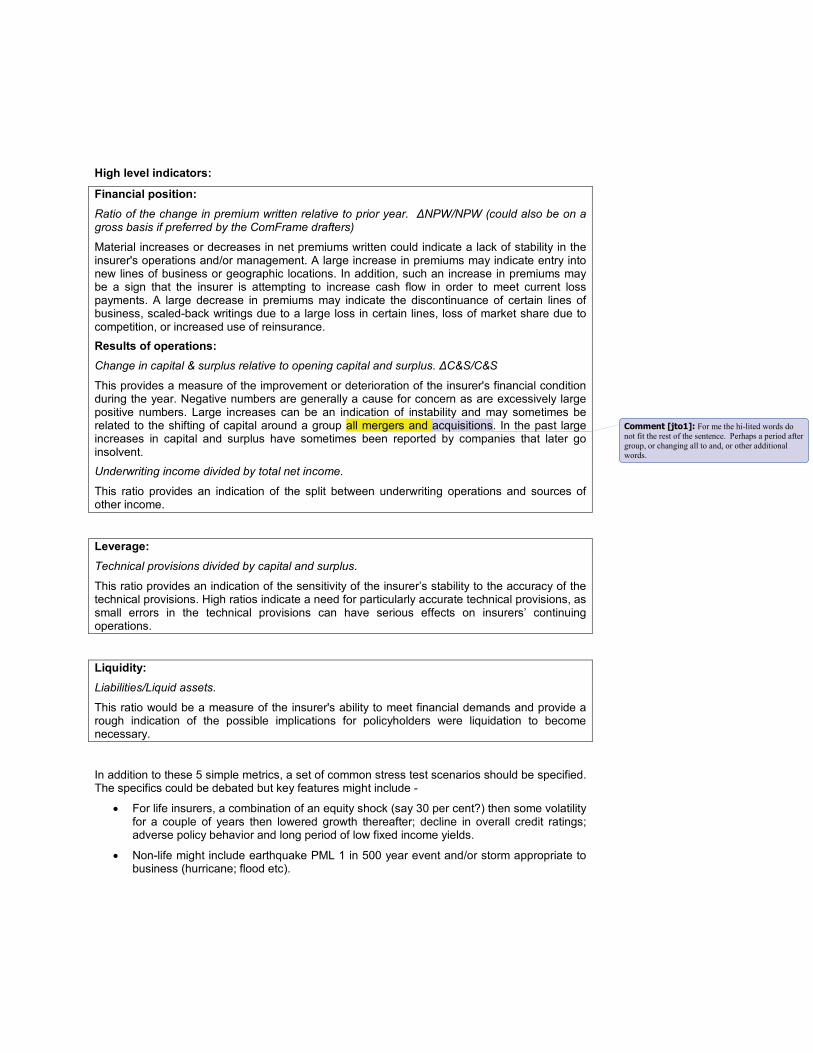

High level indicators:

Financial position: Ratio of the change in premium written relative to prior year. ΔNPW/NPW (could also be on a gross basis if preferred by the ComFrame drafters)

Material increases or decreases in net premiums written could indicate a lack of stability in the insurer's operations and/or management. A large increase in premiums may indicate entry into new lines of business or geographic locations. In addition, such an increase in premiums may be a sign that the insurer is attempting to increase cash flow in order to meet current loss payments. A large decrease in premiums may indicate the discontinuance of certain lines of business, scaled-back writings due to a large loss in certain lines, loss of market share due to competition, or increased use of reinsurance. Results of operations: Change in capital & surplus relative to opening capital and surplus. ΔC&S/C&S

This provides a measure of the improvement or deterioration of the insurer's financial condition during the year. Negative numbers are generally a cause for concern as are excessively large positive numbers. Large increases can be an indication of instability and may sometimes be related to the shifting of capital around a group all mergers and acquisitions. In the past large increases in capital and surplus have sometimes been reported by companies that later go insolvent. Underwriting income divided by total net income.

This ratio provides an indication of the split between underwriting operations and sources of other income.

Leverage: Technical provisions divided by capital and surplus.

This ratio provides an indication of the sensitivity of the insurer’s stability to the accuracy of the technical provisions. High ratios indicate a need for particularly accurate technical provisions, as small errors in the technical provisions can have serious effects on insurers’ continuing operations.

Liquidity: Liabilities/Liquid assets.

This ratio would be a measure of the insurer's ability to meet financial demands and provide a rough indication of the possible implications for policyholders were liquidation to become necessary.

In addition to these 5 simple metrics, a set of common stress test scenarios should be specified. The specifics could be debated but key features might include -

• For life insurers, a combination of an equity shock (say 30 per cent?) then some volatility for a couple of years then lowered growth thereafter; decline in overall credit ratings; adverse policy behavior and long period of low fixed income yields.

• Non-life might include earthquake PML 1 in 500 year event and/or storm appropriate to business (hurricane; flood etc).

Comment [jto1]: For me the hi-lited words do not fit the rest of the sentence. Perhaps a period after group, or changing all to and, or other additional words.

Such a combination of simple metrics and a common stress test may provide a way forward in the initial years of ComFrame. Rather than being separated by areas of current disagreement, by concentrating on things that we may all be able to agree on, we can build towards even narrower sets of parameters in the future. The common metrics would be analogous to the confidence building measures that are adopted in international arms negotiations that then lead to bigger and better things in the future.

An additional benefit of the metrics is that they can be described in terms that are better understood by our colleagues in other financial sectors.

If this concept is agreed, there are 5 lower level indicators that would be useful. These reflect additional information in the areas of underwriting, market and credit risk as follows:

Additional underwriting indicator

Reinsurance risk: Reinsurance recoverables/Capital & Surplus

This provides additional information on the degree of reliance on reinsurance

Credit risk: Non-investment grade investments/total invested assets

This provides an indicator on the level of exposure to non-investment grade assets

Market risk: Interest income/Capital & Surplus

This is a relatively crude indicator that can be used to assess interest rate risk

Equity investments/Capital & Surplus

This gives an indication of equity risk

Non-base currency investments/Capital & Surplus

This is a simple measure of currency exposure

MEMBERS AND OBSERVERS

Please refer to the confidentiality notice detailed on page 1 of this document.

ComFrame- Work in Progress (version February 6, 2012) Working Party Chairs/Technical Committee, 23-24 February, Basel

Page 94 of 160

Module 3, Element 5b Group Capital Risk Measurement ComFrame Standard M3E5b-1 *reference ICP 17, standard 17.2 The group-wide supervisor, in cooperation with other involved supervisors, establishes the group capital risk measurement of the IAIG, taking into consideration the nature and extent of solvency regulation within the various jurisdictions in which the IAIG operates. Parameter M3E5b-1-1 The nature and extent of solvency regulation within a jurisdiction shall include:

Laws and regulations that specifically limit risk taking opportunities by a legal entity or group

Frequency and level of detail of regulatory reporting requirements for a legal entity or group

Frequency and level of detail of financial analysis and examinations of a legal entity or group

Nature and types of regulatory tools used in the supervision of the legal entity or group

Strength of the corporate governance requirements of a legal entity or group

Adequacy of supervisory resources Nature and scope of supervisory powers.

ComFrame Standard M3E5b-2 The group capital risk measurements should be:

MEMBERS AND OBSERVERS

Please refer to the confidentiality notice detailed on page 1 of this document.

ComFrame- Work in Progress (version February 6, 2012) Working Party Chairs/Technical Committee, 23-24 February, Basel

Page 95 of 160

set at a sufficient level so that, in adversity, an IAIG’s insurance legal entity obligations to policyholders will continue to be met as they fall due

based on an agreed approach that lays out appropriate risk measurement criteria and address all relevant and material categories of risk.

Parameter M3E5b-2-1 Group-wide supervisor, in cooperation with other involved supervisors, will need to set criteria for the IAIG, based on the capital requirements of the various jurisdictions to which the IAIG is subject.

Specification M3E5b-2-1-1 The SSC is currently discussing criteria for risk measurement.

Parameter M3E5b-2-2 The group-wide supervisor, in cooperation with other involved supervisors, may agree to use any or all of the following methods of risk measurement to set the capital assessment:

Factor based methods Standard approaches Internal models Combinations of the above

The group-wide supervisor, in cooperation with other involved supervisors will determine how to combine the different risk measurement methods, and any adjustments needed so that an appropriate group capital assessment can be made.

Specification M3E5b-2-2-1 The group wide supervisor is to document the rationale for selecting the particular risk measurement method(s) , adopted with the other involved supervisors. The documentation is to include:

Description of the method(s) adopted Justification for the method(s) adopted Description of how the different method(s) (if more than one

used) work together Where a group consists of entities doing business across different jurisdictional solvency regimes and/or has members of the group engaged in different financial sectors, it is very likely that group capital assessment will be based on combinations of the methods of risk measurement permitted.

MEMBERS AND OBSERVERS

Please refer to the confidentiality notice detailed on page 1 of this document.

ComFrame- Work in Progress (version February 6, 2012) Working Party Chairs/Technical Committee, 23-24 February, Basel

Page 96 of 160

Specification M3E5b-2-2-2 The group-wide supervisor, in cooperation with other involved supervisors, will need to address risks arising from differences in valuation and between accounting and prudential treatment of assets and liabilities.

Parameter M3E5b-2-3 *reference ICP 17, guidance 17.7.3 The group capital assessment must take into account risk mitigation actions of the group such as the use of reinsurance and hedging programs provided that such programs actually reduce the risks posed to the group.

Specification M3E5b-2-3-1 An external reinsurance program after consideration of counterparty risk may lower the risk to the overall group and, if so, allowance for the risk reduction may be made in the determination of the group capital assessment. A distinction must be made between internal providers of reinsurance (e.g. a group captive) and external providers and different weightings applied accordingly. (See also M3E5d-3 below.)

Specification M3E5b-2-3-2 The same process should be allowed for external hedging programs.

ComFrame Standard M3E5b-3 *reference ICP 17, Standard 17.7 The group-wide supervisor, in cooperation with other involved supervisors, addresses all relevant and material categories of risk (including risk concentrations) in applying a total balance sheet approach, particularly:

Insurance risk Market risk Credit risk Group risk

MEMBERS AND OBSERVERS

Please refer to the confidentiality notice detailed on page 1 of this document.

ComFrame- Work in Progress (version February 6, 2012) Working Party Chairs/Technical Committee, 23-24 February, Basel

Page 97 of 160

Operational risk Parameter M3E5b-3-1 The group capital assessment must take into account risks inherent in different business models that may be used in:

Non-life insurance Life insurance Health insurance Reinsurance (non-life, life, health) Other insurance (such as financial guarantee, mortgage

guarantee)

Specification M3E5b-3-1-1 Specific attention should be paid to the split between traditional and non-traditional risks, and any non-insurance risks undertaken by the IAIG.

Specification M3E5b-3-1-2 Differences in business models may be driven by:

Nature of the insured event (loss of life, longevity and retirement, loss of good health due to accident or sickness, loss or damage of property, loss of employment because of accident or sickness related to employment)

Contract provisions (length, renewability, termination, re-underwriting and re-pricing, benefit guarantee, guarantee durations)

Risk funding mechanism (pay as you go, prepayment of risk) Business line diversification

Parameter M3E5b-3-2 The group-wide supervisor, in cooperation with other involved supervisors, must take into account all risks embedded in any assets, or any liabilities, owned by the group, addressing market risks including

Specification M3E5b-3-2-1 Specific attention should be paid to risks arising from the mis-match of asset and liability cash flows of the group.

MEMBERS AND OBSERVERS

Please refer to the confidentiality notice detailed on page 1 of this document.

ComFrame- Work in Progress (version February 6, 2012) Working Party Chairs/Technical Committee, 23-24 February, Basel

Page 98 of 160

risks arising from: Interest rate risk Equity market risk Currency (FX) risk Other market risks

Attention should also be paid to off-balance sheet risks such as pension obligations.

Parameter M3E5b-3-3 The group-wide supervisor, in cooperation with other involved supervisors, addresses credit risks arising from investments and reinsurance.

Parameter M3E5b-3-4 The group-wide supervisor, in cooperation with other involved supervisors, addresses group specific risks arising from:

diversification of risk across group entities intra-group transactions non-insurance group entities cross jurisdictional entities partial ownership and minority interests non-regulated group entities

Specification M3E5b-3-4-1 Attention will have to be made of consequences arising from changes in the group structure, (e.g. the sale of a particular entity) that may cause a mis-match in original diversification calculations. The SSC will consider if anything should be added with reference to systemic risk (dependent on work being conducted by other committees.)

Parameter M3E5b-3-5 The group-wide supervisor, in cooperation with other involved supervisors, addresses operational risks arising from all of the operations of the IAIG.

Specification M3E5b-3-5-1 Due attention should also be paid to the reputational risk that may arise from operational failure in a particular entity of the group, and from political or catastrophic events occurring in a particular related jurisdiction.

MEMBERS AND OBSERVERS

Please refer to the confidentiality notice detailed on page 1 of this document.

ComFrame- Work in Progress (version February 6, 2012) Working Party Chairs/Technical Committee, 23-24 February, Basel

Page 99 of 160

Specification M3E5b-3-5-2 *reference ICP 17 Particular note .should be paid to the risks arising from an individual entity’s use of models (whether internal of factor based) and arising from any assumptions made in establishing those models, pension obligations.

Parameter M3E5b-3-6 *reference ICP 17 The group-wide supervisor, in cooperation with other involved supervisors, addresses dependencies and inter-relationships between the risks.

Parameter M3E5b-3-7 *reference ICP 17 The group-wide supervisor, in cooperation with other involved supervisors, should apply stress and scenario testing (see M3E5d below) to address risks that are less readily quantifiable.

ComFrame Standard M3E5b-4 *reference ICP 17, standard 17.9 The group-wide supervisor, in cooperation with other involved supervisors , may make adjustments to the group capital assessment of the IAIG in limited circumstances provided the decision is made in a transparent framework, is fully documented and is appropriate to the nature, scale and complexity of the IAIG. Parameter M3E5b-4-1 A legal entity or entities may be excluded or simplified adjustments may

Specification M3E5b-4-1-1 There may be situations where a legal entity is part of a group but is

MEMBERS AND OBSERVERS

Please refer to the confidentiality notice detailed on page 1 of this document.

ComFrame- Work in Progress (version February 6, 2012) Working Party Chairs/Technical Committee, 23-24 February, Basel

Page 100 of 160

be used in the risk measurement of the group capital assessment whether that assessment is conducted using an aggregate or consolidated approach.

no longer actively writing business and has a closed book of business that is an insignificant part of the total group risks. In such a case ignoring the legal entity altogether or using a simplified adjustment factor is appropriate in determining the group capital assessment.

Module 3 Element 5b ComFrame Commentary General Comments

The SSC is developing principles for the application of prudential filters. Technical Comments

To be developed, if any.

MEMBERS AND OBSERVERS

Please refer to the confidentiality notice detailed on page 1 of this document.

ComFrame- Work in Progress (version February 6, 2012) Working Party Chairs/Technical Committee, 23-24 February, Basel

Page 90 of 160

Module 3, Element 5 Capital Adequacy Module 3 Element 5 Introductory Comments As the development of the capital component of solvency assessment for ComFrame is guided strongly by the Technical Committee’s strategic direction, the introductory comments for M3E5 are based on the interpretation of the strategic direction, which follows. The dot points in the following commentary are the strategic directions on the various sub-components of M3E5, as provided by the Technical Committee in November 2011.

ERM and Total Balance Sheet approach as the common foundation The SSC is fully agreed on this approach which is covered in M3E5a. The capital component of solvency assessment is a part of the overall risk management assessment of the enterprise. The total balance sheet approach ensures a consistent valuation approach for all material items on and off the balance sheet.

Valuation based on IFRS (or reconciliation to IFRS) as a working assumption with filters and complements to be built where needed as

IFRS develops The SSC recognises the need to use the IFRS balance sheet (or conversion to IFRS balance sheet through appropriate means) as a starting point for all considerations of the capital component. It is recognised that IFRS standards will continue to evolve and that adjustments may need to be made accordingly.

Further develop an approach regarding a range of similar means to address the risks for IAIGs as set out in the Concept Paper. The SSC has developed an approach that outlines the risks to be measured to establish the capital assessment of an IAIG (M3E5b).

Develop a partly harmonised set of standards and parameters which sets out a narrow range of target criteria and time horizons for

measurement of those risks. Implicit criteria would be allowed providing that the underlying rationale is evidenced. The SSC is currently discussing the criteria for risk measurement in order to provide a set of standards and parameters for the assessment of capital for IAIGs that is narrower than currently allowed for under the ICPs.

Build a system which allows for various standardised approaches (factor or stochastic) with internal models accepted. Basic principles

of internal models and disclosures to allow comparison between various jurisdictions to be spelt out.

MEMBERS AND OBSERVERS

Please refer to the confidentiality notice detailed on page 1 of this document.

ComFrame- Work in Progress (version February 6, 2012) Working Party Chairs/Technical Committee, 23-24 February, Basel

Page 91 of 160

The “system” is already implicit within an overall ERM approach. The SSC has described a range of appropriate operations within both factor-based and internal model approaches in M3E5b.

Basic requirements and common terminology for capital resources along with mapping of capital resources requirements in key

jurisdictions (members of SSC) – June 2012. Common definition of capital resources to be established by 2013 The SSC has developed an approach to describe the basic elements of different capital resources and has agreed to undertake a mapping exercise which will define basic requirements and common terminology used in different jurisdictions. (A template for the exercise is currently being designed.) The common definition for the second stage will emerge from an understanding of the “best practice” emerging from the first stage.

Further elaborate on stress testing in ERM processes and on stress testing by the group-wide supervisor. Stress and scenario testing is a tool that the SSC drafting groups have included in various elements (M3E2 (ERM), M3E5b (capital risk measurement) and M3E5d (maintaining capital resources).

Module 3, Element 5a Total Balance Sheet Approach ComFrame Standard M3E5a-1 *reference ICP 17, standard 17.1 In order to assess capital adequacy of an IAIG, the group-wide supervisor, in cooperation with other involved supervisors, applies a total balance sheet approach to assess all the risks to which the IAIG is exposed. Parameter M3E5a-1-1 ERM requires all material risks to be identified and quantified, where appropriate, whether off or on balance sheet. This forms the basis of the total balance sheet approach which in turn provides a consistent valuation.

Specification M3E5a-1-1-1 The group-wide supervisor is to document and disclose the total balance sheet approach adopted with other involved supervisors and the IAIG. The documentation is to include:

a description of the approach adopted; a justification of the approach adopted ;

Any Other Matters