introduction 3 - poweranking.compoweranking.com/kantarretail2013poweranking(r).pdf · executive...

TRANSCRIPT

®

KANTAR RETAIL372 Danbury Road

Suite 100

Wilton, CT 06897

Phone: 203.834.2800

Price: $1000.00 USD

© 2013 Kantar Retail. All rights reserved.

No part of this work may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and/or retrieval system, without permission in writing from the publisher.

INTRODUCTION

EXECUTIVE SUMMARY

KEY FINDINGS

Manufacturer Rankings

Retailer Rankings

3

8

16

32

CONTENTS

®

INTRODUCTION

KANTAR RETAIL SPONSORED THE FIRST ANNUAL POWERANKING® SURVEY IN 1997. The survey originated from our industry benchmarking studies on category management and trade promotion management, which for the past 19 years have provided insight into industry best practices in these areas. The objective of the PoweRanking study is to research and benchmark how retailers and manufacturers view each other in the most important areas of the manufacturer-retailer relationship.

THE POWERANKING STUDY identifies those retailers and manufacturers who set the standard of performance as ranked by their trading partners. This provides benchmarks for retailers and manufacturers across trade channels.

The specific goals of the research were to:

• Identify the best manufacturers and retailers, as evaluated by their trading partners

• Provide insight into what makes them “the best”

• Define the importance of key metrics between trading partners

• Highlight areas for improvement

-3-

®

INTRODUCTION

Customized questionnaires were developed for retailer and wholesaler respondents in food, drug, mass merchandiser, dollar, convenience and club channels and manufacturers in food, household products, general merchandise and health & beauty care. These questionnaires were distributed each spring from 1997 to 2013 to personnel at all levels of management, with the assurance of total confidentiality of respondents.

Over 500 manufacturer and retailer respondents participated in this year's study. The results of the 2013 survey were compared with the results of 2011 and 2012 to determine the causes

behind shifts in the rankings.

Retailers were asked to rank manufacturers on criteria that fall into two broad areas:

Manufacturers were asked to rank retailers on similar criteria:

STRATEGIC

• Clearest company strategy

• Most important consumer brands to retailers

• Best combination of growth and profitability

BUSINESS FUNDAMENTALS

• Best customer/sales teams

• Most innovative marketing approach

• Most helpful consumer/shopper insights; category management

• Best supply chain leadership

• Best shopper marketing programs

STRATEGIC

• Clearest company strategy

• Best job of branding their stores

• Projected to be Power Retailers in the next 15 years

BUSINESS FUNDAMENTALS

• Best retailer with which to do business

• Best category management/buying teams

• Most innovative merchandising approach

• Best supply chain leadership

• Best practice category management

-4-

®

INTRODUCTION

Results were tabulated on a two-year rolling basis, reflecting the percent of respondents ranking the company among the top three. Additionally, follow-up qualitative interviews were conducted among a diverse group of manufacturers and retailers to provide further insight into the data.

The PoweRanking® methodology reflects mergers and acquisitions that have occurred in the past. We have consciously rolled up operations into the parent company, where appropriate for this year and versus year ago. At the same time, where retailers and manufacturers are operating largely as independent companies, they are treated as such in the data. As a dynamic monitor, the PoweRanking will continue to consolidate or separate companies as retailers perceive them. For example, this year in the PoweRanking, Kraft Foods Group and Mondelēz

are treated as new, separate entities.

POWERANKING COMPOSITES

The 2013 PoweRanking survey includes the overall PoweRanking Composite, created by weighting the three strategic rankings equally with the five business fundamental rankings (see previous page) – thus placing greater importance on the strategic rankings. This reflects the

importance of sound strategy as an overall driving force in business performance.

STRATEGIC COMPOSITE

The Strategic Composite combines the three strategic measures into an overall composite to provide better insight into which manufacturers and retailers are most strategically important to

their trading partners.

BUSINESS FUNDAMENTALS COMPOSITE

The Business Fundamentals Composite combines the five fundamental areas of business (see previous page) into a composite, which reflects the retailers’ and manufacturers’ opinions of those trading partners who have the strongest organizations and personnel and provide the best

tools for solid business development.

DIGITAL MARKETING

For the first time in 2011, Kantar Retail added a measure for Digital Marketing. Given its increasing influence on retailers, manufacturers and consumers, digital is now a measure to be monitored. It is not included as part of the PoweRanking Composite.

-5-

®

INTRODUCTION

Over 500 manufacturer and retailer participants provided input. Respondents included all levels of retailer/wholesaler and manufacturer management. Listed below is an alphabetical listing of some of these leading companies.

Army and Air Force Exchange ServiceAhold U.S.A., Inc.Amazon.com, Inc.Associated Wholesale Grocers, Inc.Bashas' Inc.BI-LO Holding, LLCBJ’s Wholesale Club, Inc.Bozzuto’s Inc.BP America Inc.C&S Wholesale Grocers, Inc.CVS Caremark CorporationDollar General CorporationExxon Mobil CorporationFood Lion, LLCGiant Eagle, Inc.Giant Food Stores, LLCH.E. Butt Grocery CompanyHannaford Bros. Co.Harris Teeter Supermarkets, Inc.The Kroger Co.Lowe’s Companies, Inc.

Lowes Foods Inc.Martin’s Super Markets, Inc.Meijer, Inc.Nash-Finch CompanyPilot Oil CoPrice Chopper/The Golub CorporationRite Aid CorporationSafeway Inc.Save-A-Lot, Ltd.Save Mart SupermarketsSears Holdings CorporationWakefern Food CorporationSuperValu Inc.Target CorporationTrue Value CompanyUnified Grocers, Inc.Wakefern Food CorporationWalgreen CompanyWal-Mart Stores, Inc.Wegmans Food Markets, Inc.

RETAILERS

-6-

®

INTRODUCTION

Below is an alphabetical listing of some of the leading manufacturer respondents.

3M

Abbott Laboratories

Anheuser-Busch Companies, LLC

Bayer Healthcare AG

Beiersdorf North America Inc.

Bemis Company, Inc.

Société Bic

Bush Brothers & Company

Campbell Soup Company

Caterpillar Inc.

The Coca-Cola Company

The Clorox Company

Colgate-Palmolive Company

ConAgra Foods, Inc.

Continental Mills Inc

Crayola, LLC

Dawn Foods Limited

Dean Foods Company

Del Monte Corporation

DeMet’s Candy Company

Diageo North America, Inc.

Dr Pepper Snapple Group, Inc.

E. & J. Gallo Winery

Energizer Holdings, Inc.

Frito-Lay, Inc.

General Electric Company

General Mills, Inc.

Georgia-Pacific LLC

Glaxo SmithKline plc

Green Mountain Coffee Roasters, Inc.

H.J. Heinz Company

Hallmark Cards, Inc.

Hamilton Beach Brands, Inc.

Hasbro, Inc.

Henkel of America Inc

The Hershey Company

Hewlett Packard Company

Hormel Foods Corporation

The J.M. Smucker Company

Jarden Corporation

Jasco Products Company LLC

Johnson & Johnson

Kao USA, Inc.

Kellogg Company

Kimberly-Clark Corporation

Kraft Foods Group, Inc.

Land O’Lakes, Inc.

LEGO Systems, Inc.

L’Oreal Usa, Inc.

Mars Incorporated

McCormick & Company, Inc.

McKee Foods Corporation

Menasha Corporation

Merck & Co., Inc.

Mondelēz International, Inc.

Nestle USA, Inc.

Ocean Spray Cranberries, Inc.

Pactiv LLC

Pepperidge Farm, Inc.

PepsiCo, Inc.

Perdue Incorporated

Perrigo Company

Pfizer Inc.

Philips Electronics North America Corporation

The Procter & Gamble Company

Reckitt Benckiser Inc.

Red Bull, North America, Inc.

Reynolds Consumer Products

Rich Products Corporation

Ricos Products Co. Inc.

S.C. Johnson & Son, Inc.

Seneca Foods Corporation

Skyy Spirits, LLC

The Sun Products Corporation

Time Inc.

T-Mobile USA, Inc.

Tom’s of Maine, Inc.

Tree Top, Inc.

Tyson Foods, Inc.

Unilever PLC

The Walt Disney Company

Welch’s Foods Inc.

William Wrigley Jr. Company

World Kitchen, LLC

MANUFACTURERS

-7-

EXECUTIVESUMMARY

MAPPING A CLEAR DESTINATION

The “Storm” Is Really Permanent Climate Change: Volatility = The New Normal The changes in the retail landscape that seemed temporary and in many cases economic

downturn-driven have achieved permanence. Retailers and manufacturers alike are grappling

with a polarized and more demanding shopper base that is increasingly aware of prices and

competitive offers. Diversified, specialized and more capable competition has developed in almost

every trading area and category — all against the backdrop of a slow-growth world. The digital

ecosystem is reshaping not only how and where shoppers buy, but also their Path to Purchase

irrespective of where the sale happens.

This year’s PoweRanking® survey participants broadly acknowledged the uncertain and

rapidly evolving road ahead, noting the shopper and business behavior changes that are afoot.

“The customer base is changing in terms of demographic shifts . MILLENNIALS ARE LESS LOYAL and are willing to travel to multiple outlets. The average shopper now visits 5 channels.” --VP, SALES STRATEGY, MAJOR CPG MANUFACTURER

Five key dynamics emerged as the strongest themes throughout this year’s survey:

1. Providing a beacon (and a map)

2. Innovation: The beacon’s source of light

3. Innovation isn’t just about ideas, but approach

4. Triangulation

5. Measurement

-9-

PROVIDING A BEACON (AND A MAP)1

In choppy waters, sailors look to a beacon to provide direction. Consistent among this year’s responses was the mandate for a two-part approach:

a highly actionable short-term plan accompanied by a longer-term vision for future

growth. A frequent concern voiced by many retailers was manufacturers’ tendencies

to come to the table with only one but not the other.

Trusted beacons have recognized traits. PoweRanking leaders are noted for having

great corporate and category visions for growth. Manufacturers with both talent and

stability in their key account staffing were recognized by the largest retailers as

their most trusted beacons.

Increasingly retailers want that beacon to shine directly on their route forward –

asking for customer-specific plans and strategies. A record number of retailers are

now pushing suppliers beyond traditional regional/channel plans to differentiate

across product, packaging, supply chain, shopper marketing, and more.

“We need a SHORT-TERM component of 12-15 months and a LONGER-BURN view of 2-5 years. We won’t turn around anything in a year.” --VP MERCHANDISING, MAJOR RETAILER

-10-

2

One of the key attributes of this beacon is innovation.

Mainstream grocery, in particular, is asking for a vision on maintaining vital differen-

tiation from both curated specialty grocers and the mainstreaming of value retail.

Manufacturer innovation is needed in the traditional areas of product and packaging,

but increasingly in supply chain and pricing.

Supply chain and inventory management innovations are being led from digital

players like AMAZON, who continue to innovate to own product for as short a time as

possible, changing the economics of slow-turn SKUs. “Assortment-based” retailers

must develop multi-tiered distribution systems for items of varied velocities. If

Amazon needs one in their whole system and a traditional retailer needs 20 per

store plus distribution center safety stock, the traditional retailer loses.

Pricing strategies such as SAFEWAY’S Just 4 U platform will increasingly drive

shopper pricing to be more dynamic, and also more personalized and private.

“AMAZONFRESH is still in its early stages but is gaining traction. They are becoming an indispensable habit for Gen Y and the generations beyond Y. Amazon is investing in the right infrastructure to take advantage of routine consumption.” --SR. DIRECTOR, CPG MANUFACTURER

INNOVATION: THE BEACON’S SOURCE OF LIGHT

-11-

3

A new theme emerging in this year’s PoweRanking is an increasing appetite for more testing and experimentation and a true willingness to pioneer a new path. In a world of increasing eCommerce, bricks and mortar retailers have never been

more open than today in collaborating to build better shopping experiences. Current

tests range from pack and assortment options usually reserved for “other channels“

to meal solution centers to full aisle reinventions.

Based on this year’s survey feedback, the test-and-learn approach should now

migrate from an ad hoc, one-time mindset to one that is more formally built into the

mindset and culture of the organization, complete with integration into core busi-

ness planning. Innovation is not just about a single good idea, but an organizational

philosophy dedicated to continuously testing and learning.

“GENERAL MILLS is willing to take risks with us to test new programs that allow us to learn and re-apply with other suppliers. We had some real tangible wins with them in 2012.” --SR. BUYER, MAJOR RETAILER

INNOVATION ISN’T JUST ABOUT IDEAS, BUT APPROACH

-12-

4Triangulation has been a part of navigation since ancient times.

Most companies today use loyalty card or granular transaction data to understand shop-

pers, but winners synthesize this with macro trends and custom research to provide unique

insights that drive the business.

This triangulation is critical to help retailers escape the “sea of sameness” — where every

outlet sells the same things — either in store or on an endless online shelf. Now, the

highest concern is integrating the key insights that help define the retailer’s true right to

win, beyond simple assortment, through shopper target, shopper marketing, convenience,

service, or other value-adds.

How to triangulate?

1. A VERTICAL category view, analyzing traditional sales and profit metrics for key brands

and categories.

2. A HORIZONTAL shopper view, integrating the shopper’s value to total store, including

share of wallet, leakage to competition, and the broader story of the shopping basket.

3. A HOLISTIC view of the Path to Purchase, integrating omni-channel insights and

retailer-specific research to complete the total picture.

“We expect suppliers to show insights on how the category is shifting and how to take advantage of the shift.”

--SR. BUYER, MAJOR RETAILER

TRIANGULATION: WHICH DIRECTION SHOULD THE BEACON SHINE?

-13-

MEASUREMENT: HOW DO WE KNOW WE ARE WINNING IN A TRIANGULATED WORLD? 5

Great navigation tells you not just where you are going, but how far you have gone.

In a similar spirit, winning manufacturers and retail-

ers were praised this year for transparency in track-

ing and sharing results. To earn trusted status on the

journey, manufacturers need to openly track and

learn from failures as well. Players who never fail

are likely not pushing hard enough.

As manufacturers and retailers track the journey

through today’s stormy environment, three key

enablers have emerged:

• PEOPLE— A higher degree of analytical literacy is

needed to facilitate a tracking and metrics discipline.

• DATA—This year expectations have risen to the point

where results tracking will be more granular and more

contextual – going beyond loyalty and POS and

integrating this base data with a wide variety of sources.

• SYSTEMS—Notable performers were those who

had built disciplined systems to track and report not

just immediate results vs. annual plan, but also the

enduring success of programs, both for the featured

brands and products and the entire category.

This year, retailers highlighted a need for clearer

measurements and metrics related to performance

of shopper marketing programs to accurately assess

the long-term return on investment.

“No one ever gives any sense of the enduring success of a pro-gram. We would love to see what happens to the brand or category AFTER the promotion is over.”

--DMM, MAJOR RETAILER

-14-

ACTION STEPS

PROVIDE A BEACON (AND A MAP): BOTH A SHORT-TERM TACTICAL PLAN AND LONGER-TERM

STRATEGIC VISION

In stormy times, companies need to provide strategic clarity on growth to anchor future plans—

including a six-month tactical plan with clear, measurable outcomes, and a longer range two-three

year plan that maps joint strategic priorities. Make staffing stability a priority over the near horizon,

as there is no substitute for a steady, trusted hand on the wheel during stormy weather.

NAVIGATE THROUGH INNOVATION: DRIVING CUSTOMIZATION THROUGHOUT THE CUSTOMER BASE

Recognize the broad impact of channel and assortment blurring and leverage innovation to drive

meaningful differentiation at a retailer and brand level. Reapply supply chain innovations and

efficiencies from e-commerce leaders to drive value throughout the range of partnerships.

Leverage emerging technology to deliver innovation in pricing, loyalty, and brand equity.

INNOVATE NOT ONLY WITH IDEAS, BUT APPROACH: INVEST IN THOUGHT LEADERSHIP WITH TESTING

Manufacturers and retailers alike should embrace the new readiness to test and learn—from new

products, to digital shopper marketing to breakthrough aisle leadership work. Ensure your organization

looks at testing as a core discipline—not a hobby project—and staffs and resources accordingly.

TRIANGULATE THROUGH INSIGHTS: THE CATEGORY, THE SHOPPER, THE PATH TO PURCHASE

Leverage and integrate a diverse range of insights for the category, shopper behavior, and

Path to Purchase to provide granularity on performance but also a broader context on the true

value of the shopper. Leverage the power of loyalty portals and emerging omni-channel

data sources to provide a more real-time lens on behaviors.

TRACK THE JOURNEY: CLEARER METRICS FOR REVIEWING IMMEDIATE AND ENDURING RESULTS

Agree on success criteria and goals up front and make transparent sharing of performance the

new normal. Look beyond the short-term sales results of a program or a quarter and tap into

the longer-term category and shopper behavior impact, then course correct and plan a better

future journey.

1

2

3

4

5

-15-

MANUFACTURER RANKINGS

Consumer Brands

Company Strategy

Growth &Profitability

MarketingApproach

Insights/Category Leadership

SupplyChain

ShopperMarketing

Sales Force/Customer Teams

®

“GENERAL MILLS is the most collaborative vendor we deal with, and they offer unique supply chain programs that drive mutual business growth.”

“P&G is known for being best in class in Supply Chain. They always do a great job of sharing theirstrategy and looking to see how they can align their strategy with our own.”

Retailer Comments on Composite

RANK

2013 2012

Procter & Gamble

Unilever

General Mills

Kraft Foods Group

PepsiCo

Nestle

Kellogg

Coca-Cola

ConAgra

Kimberly-Clark

%

1

2

3

4

5

6

7

8

9

10

1

4

3

-

5

6

8

7

9

10

28.2

24.6

24.4

19.0

18.0

13.3

11.4

10.1

6.6

6.3

“Unilever is the most flexible in meeting retailer needs.” RETAILER COMMENT

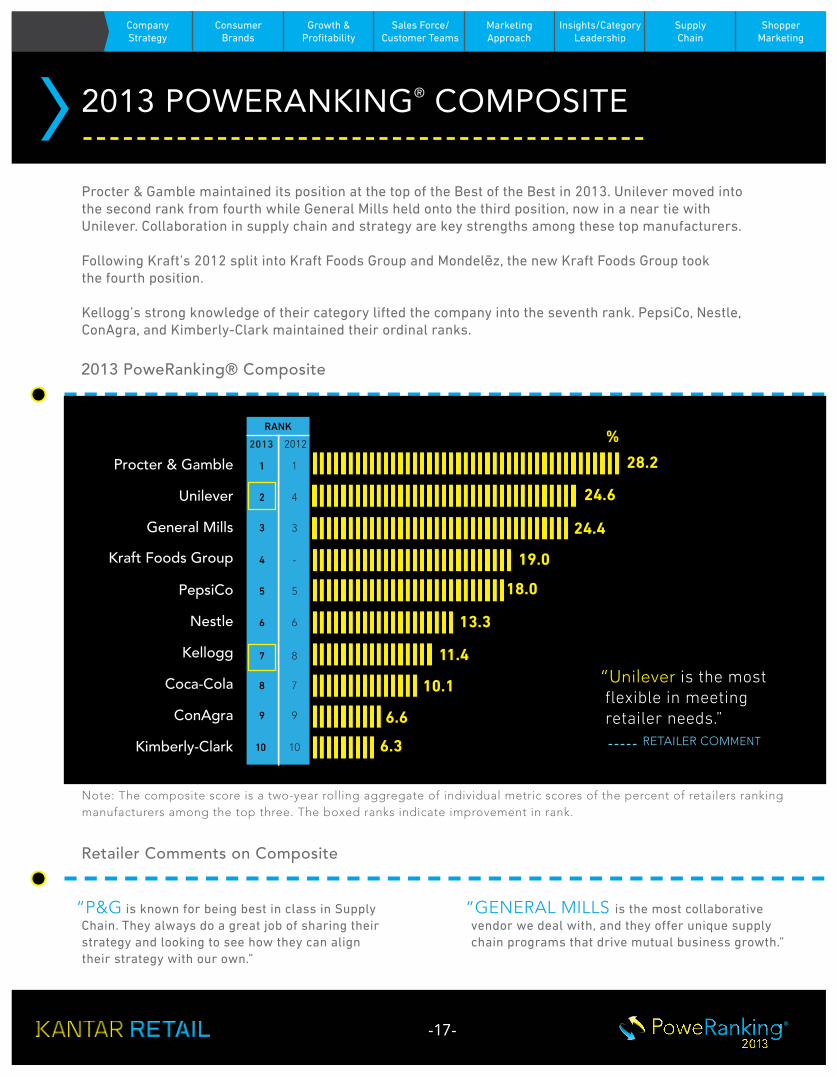

Procter & Gamble maintained its position at the top of the Best of the Best in 2013. Unilever moved into the second rank from fourth while General Mills held onto the third position, now in a near tie with Unilever. Collaboration in supply chain and strategy are key strengths among these top manufacturers.

Following Kraft’s 2012 split into Kraft Foods Group and Mondelēz, the new Kraft Foods Group took the fourth position.

Kellogg’s strong knowledge of their category lifted the company into the seventh rank. PepsiCo, Nestle, ConAgra, and Kimberly-Clark maintained their ordinal ranks.

2013 PoweRanking® Composite

Note: The composite score is a two-year rolling aggregate of individual metric scores of the percent of retailers ranking manufacturers among the top three. The boxed ranks indicate improvement in rank.

2013 POWERANKING® COMPOSITE

-17-

Consumer Brands

Company Strategy

Growth &Profitability

MarketingApproach

Insights/Category Leadership

SupplyChain

ShopperMarketing

Sales Force/Customer Teams

®

Retailer Comments on Composite

2013 PoweRanking® Composite

“KELLOGG has seasoned pros that know the category.”

“KRAFT FOODS GROUP brands cross over all aspects of grocery products. They are the most recognized.”

Note: The composite score is a two-year rolling aggregate of individual metric scores of the percent of retailers ranking manufacturers among the top three.

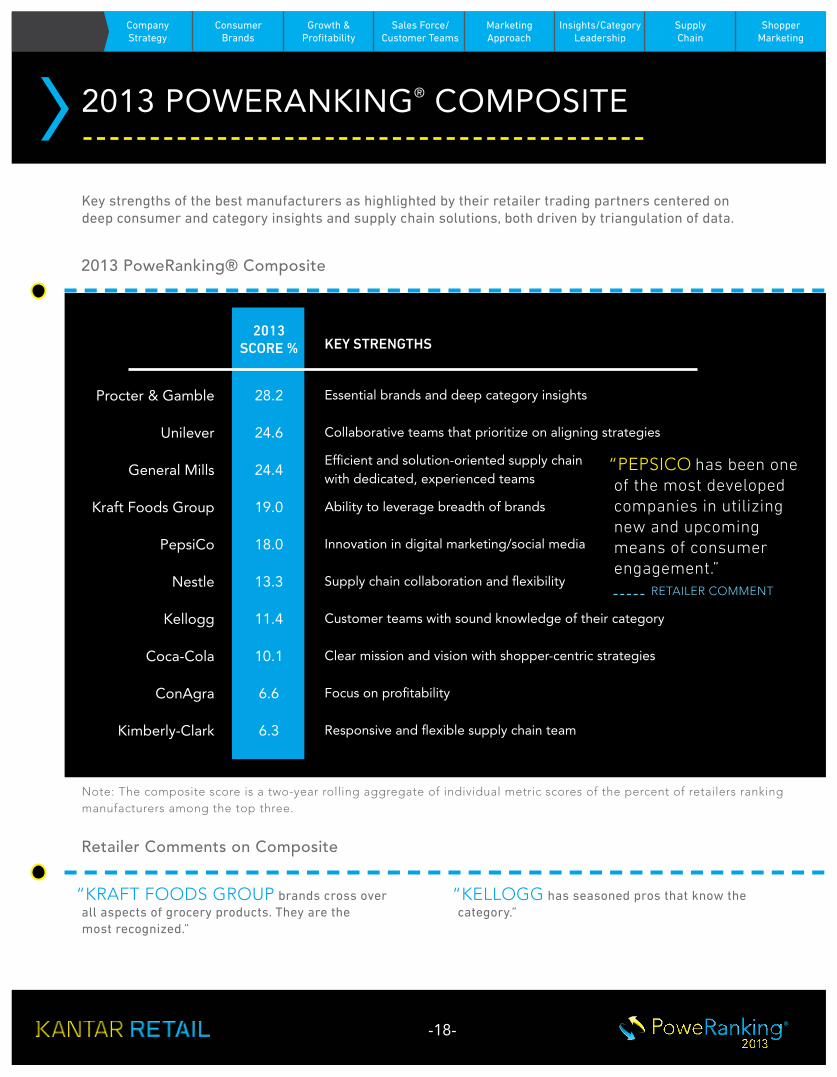

Key strengths of the best manufacturers as highlighted by their retailer trading partners centered on deep consumer and category insights and supply chain solutions, both driven by triangulation of data.

KEY STRENGTHS

Procter & Gamble

Unilever

General Mills

Kraft Foods Group

PepsiCo

Nestle

Kellogg

Coca-Cola

ConAgra

Kimberly-Clark

28.2

24.6

24.4

19.0

18.0

13.3

11.4

10.1

6.6

6.3

Essential brands and deep category insights

Collaborative teams that prioritize on aligning strategies

Efficient and solution-oriented supply chain with dedicated, experienced teams

Ability to leverage breadth of brands

Innovation in digital marketing/social media

Supply chain collaboration and flexibility

Customer teams with sound knowledge of their category

Clear mission and vision with shopper-centric strategies

Focus on profitability

Responsive and flexible supply chain team

2013 SCORE %

2013 POWERANKING® COMPOSITE

“PEPSICO has been one of the most developed companies in utilizing new and upcoming means of consumer engagement.” RETAILER COMMENT

-18-

2013 RANK

2013 RANK

2013 RANK

2012 RANK

2012 RANK

2012 RANK

®

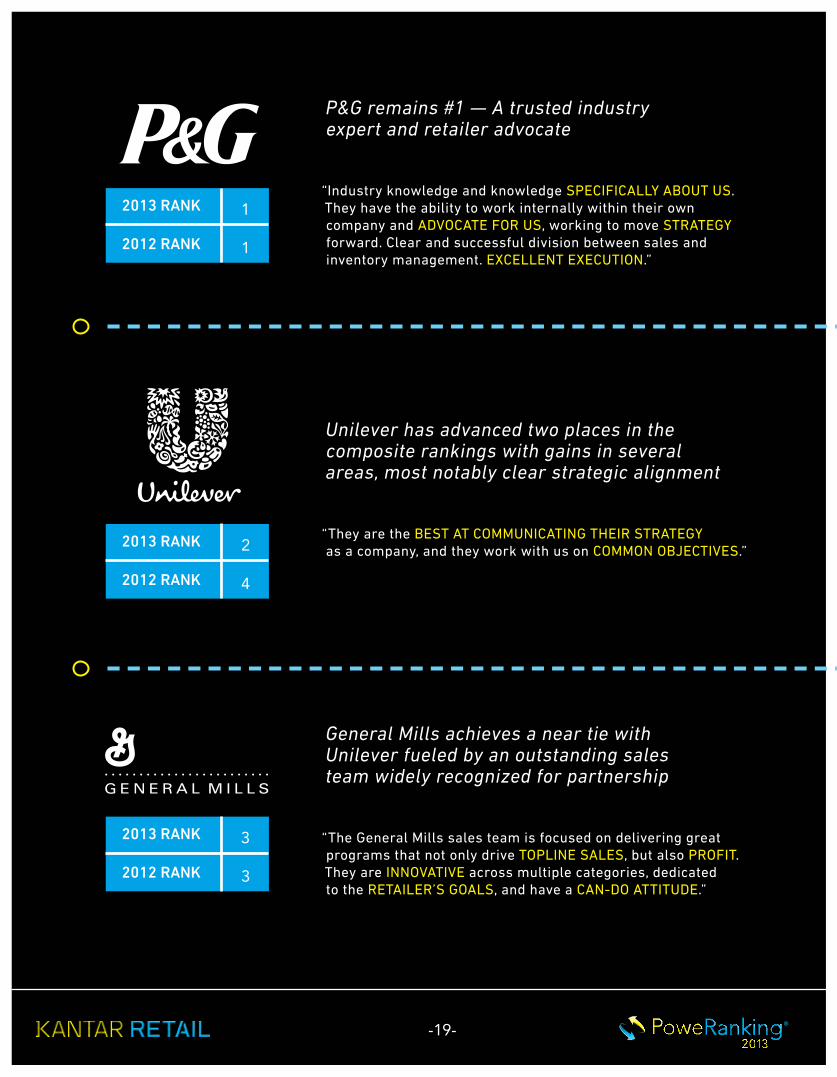

P&G remains #1 — A trusted industry expert and retailer advocate

“Industry knowledge and knowledge SPECIFICALLY ABOUT US. They have the ability to work internally within their own company and ADVOCATE FOR US, working to move STRATEGY forward. Clear and successful division between sales and inventory management. EXCELLENT EXECUTION.”

Unilever has advanced two places in the composite rankings with gains in several areas, most notably clear strategic alignment

“They are the BEST AT COMMUNICATING THEIR STRATEGY as a company, and they work with us on COMMON OBJECTIVES.”

General Mills achieves a near tie with Unilever fueled by an outstanding sales team widely recognized for partnership

“The General Mills sales team is focused on delivering great programs that not only drive TOPLINE SALES, but also PROFIT. They are INNOVATIVE across multiple categories, dedicated to the RETAILER’S GOALS, and have a CAN-DO ATTITUDE.”

1

2

3

1

4

3

-19-

Consumer Brands

Company Strategy

Growth &Profitability

MarketingApproach

Insights/Category Leadership

SupplyChain

ShopperMarketing

Sales Force/Customer Teams

®

Seasoned customer teams

Collaborative work on tailored programs

Willingness to provide information

Willing to try different things

Flexibility and willingness to customize

Driving category growth

Responsive customer team

Supply chain solutions

Social media campaigns

Use of multiple marketing vehicles

Retailer Comments on Composite

“CAMPBELL’S has continued product and flavor rejuvenation. They are willing to work with my team to create new items.”

Note: The composite score is a two-year rolling aggregate of individual metric scores of the percent of retailers ranking manufacturers among the top three.

Kellogg proved to be the mightiest of manufacturers with sales under $10B by claiming the seventh rank in the Total Composite while improving its overall score.

Hershey’s advance planning to align on strategy moved it into the thirteenth rank. Campbell’s cooperative planning with their customers to drive innovation earned the company a higher score.

J.M. Smucker, Red Bull, Chobani, and Hillshire each improved their ranks in 2013.

Kellogg

Hershey

Campbell Soup Co.

Clorox

J.M. Smucker

Red Bull

Hormel Foods

Del Monte Foods

Agro Farma/Chobani

Hillshire Brands

7

13

15

17

18

20

21

22

25

27

8

18

15

12

20

23

19

21

31

NR

2013 RANK

2012 RANK

2013 PoweRanking® Composite Under $10B

“HERSHEY understands their customers and works well in advance (in some cases 18 months) to deter-mine a strategy that works well for both companies.”

POWERANKING® COMPOSITE UNDER $10B

KEY STRENGTHS

-20-

Consumer Brands

Company Strategy

Growth &Profitability

2013 PoweRanking® Strategic Composite

MarketingApproach

Insights/Category Leadership

SupplyChain

ShopperMarketing

Sales Force/Customer Teams

®

Retailer Comments on Strategic Metrics

“MARS is the most collaborative supplier in my business. They work hard on win-win solutions that drive growth and profitability in both cost and supply chain efficiency.”

“GENERAL MILLS is willing to take risks with us and develop new programs that allow us to learn and re-apply with other suppliers. We had some real tangible wins with General Mills in 2012.”

RANK

2013 2012

Procter & Gamble

Unilever

General Mills

Kraft Foods Group

PepsiCo

Nestle

Kellogg

Coca-Cola

ConAgra

Mars

%

1

2

3

4

5

6

7

8

9

10

1

4

3

-

5

6

8

7

9

14

27.6

22.9

22.8

18.7

17.8

13.5

10.7

9.5

7.4

6.5

“It is evident that UNILEVER has a road map for innovation along with a strategy to grow.” RETAILER COMMENT

The Manufacturers’ Strategic Composite comprises the Clearest Company Strategy, Consumer Brands, and Growth & Profitability metrics.

Procter & Gamble maintained its top rank, while Unilever moved up two spots. General Mills held its third place ordinal rank. These top three manufacturers set themselves apart by working hand-in-hand with retailers to achieve shared objectives.

Kellogg jumped ahead of Coca-Cola into the seventh position. Mars moved into the Top 10 from the fourteenth rank in 2012, reflecting its tangible wins with retailers in supply chain.

STRATEGIC COMPOSITE

-21-

Company Strategy

Growth &Profitability

SupplyChain

ShopperMarketingCompany Strategy Sales Force/

Customer Teams

®

Insights/Category Leadership

MarketingApproach

Consumer Brands

“COCA-COLA has a clear mission and vision for total Coca-Cola and an extremely clear view of how that mission and vision translates to their business at our stores. Their strategies are guest-centric.”

RANK

2013 2012

Procter & Gamble

Unilever

General Mills

PepsiCo

Kraft Foods Group

Coca-Cola

Kellogg

Nestle

ConAgra

Hershey

Mars

%

1

2

3

4

5

6

7

8

9

10

10

1

4

2

5

-

7

8

6

18

12

21

27.1

23.5

21.8

19.3

16.3

14.6

12.6

12.1

6.5

7.3

6.5

“UNILEVER is very clear on their strategy and how we fit into the strategy, as well as understanding our strategy, what is important to us and how Unilever fits in.” RETAILER COMMENT

Retailer Comments on Clearest Company Strategy

”MARS is always on top of goals, new trends, and long term vision.”

Which Manufacturers Have the Clearest Company Strategy?(Percent of Retailers Ranking Among Top 3 Manufacturers)

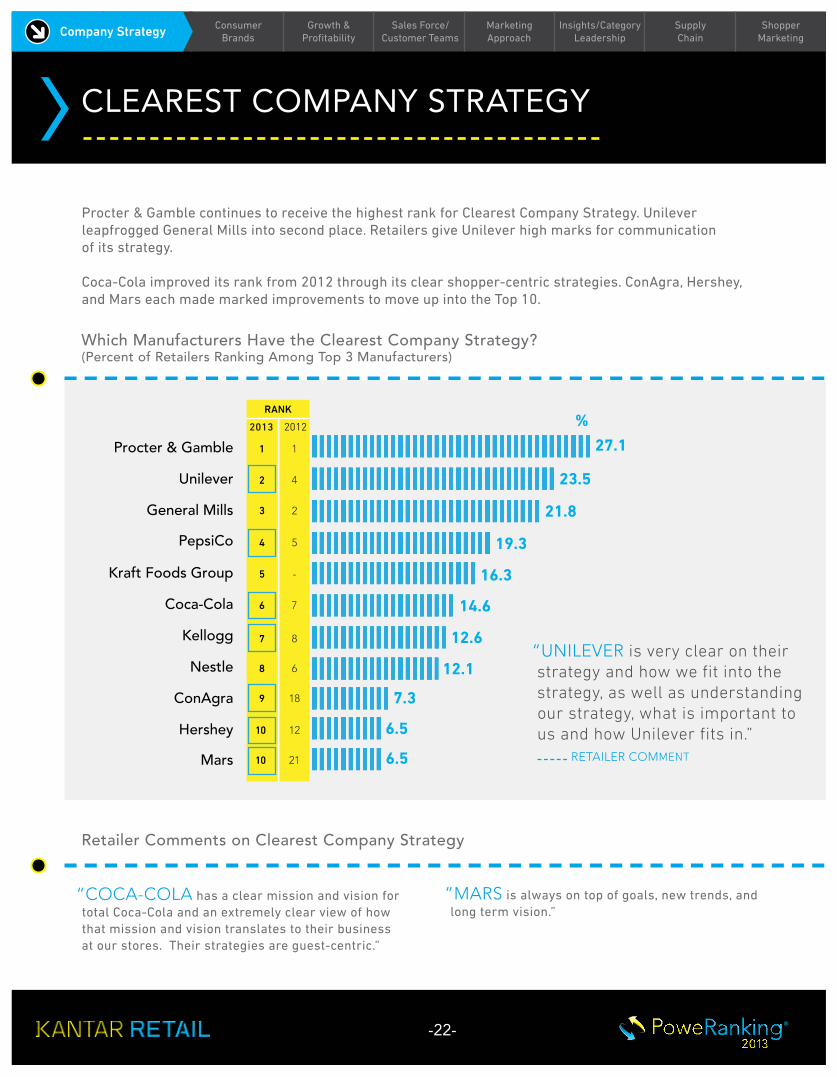

Procter & Gamble continues to receive the highest rank for Clearest Company Strategy. Unilever leapfrogged General Mills into second place. Retailers give Unilever high marks for communication of its strategy.

Coca-Cola improved its rank from 2012 through its clear shopper-centric strategies. ConAgra, Hershey, and Mars each made marked improvements to move up into the Top 10.

CLEAREST COMPANY STRATEGY

-22-

Company Strategy

SupplyChain

ShopperMarketing

Sales Force/Customer Teams

®

Insights/Category Leadership

MarketingApproach

Growth &ProfitabilityConsumer Brands

RANK

2013 2012

Procter & Gamble

General Mills

Unilever

Kraft Foods Group

PepsiCo

Nestle

Coca-Cola

Kellogg

Mars

Johnson & Johnson

%

1

2

3

4

5

6

7

8

9

10

1

3

5

-

4

6

7

9

11

8

43.2

26.9

22.7

21.7

21.2

16.9

9.9

9.3

8.3

8.2

“The power of the carbonated beverages category continues to be a force that drives customers to the

retail store. With COCA-COLA having the largest two brands available (Coke and Diet Coke), they are the driver when it comes to appealing to consumers.”

“P&G still has the power brands that create the most significant impact on basket size when part of the advertising plan.” RETAILER COMMENT

Retailer Comments on Most Important Consumer Brands to Retailers

“GENERAL MILLS has the strongest brands in dry grocery (e.g., Cheerios).”

“UNILEVER has the top brands in the categories they play in.”

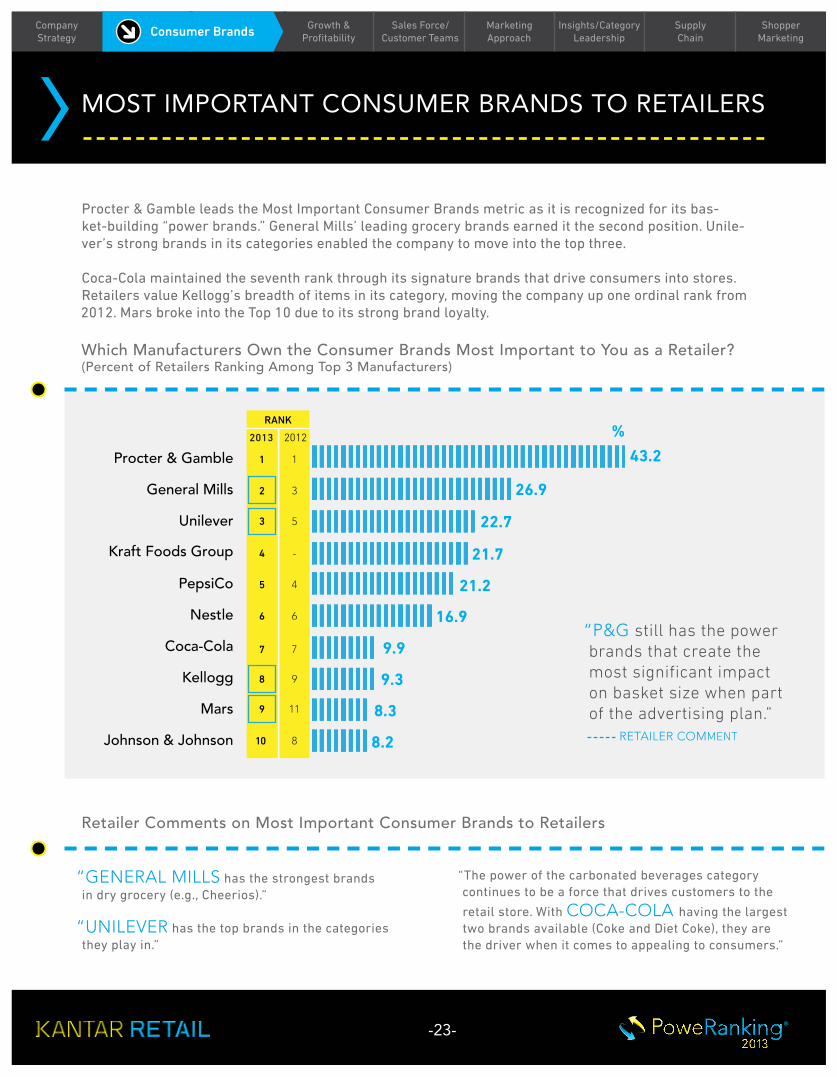

Which Manufacturers Own the Consumer Brands Most Important to You as a Retailer?(Percent of Retailers Ranking Among Top 3 Manufacturers)

Procter & Gamble leads the Most Important Consumer Brands metric as it is recognized for its bas-ket-building “power brands.” General Mills’ leading grocery brands earned it the second position. Unile-ver’s strong brands in its categories enabled the company to move into the top three.

Coca-Cola maintained the seventh rank through its signature brands that drive consumers into stores. Retailers value Kellogg’s breadth of items in its category, moving the company up one ordinal rank from 2012. Mars broke into the Top 10 due to its strong brand loyalty.

MOST IMPORTANT CONSUMER BRANDS TO RETAILERS

Company Strategy

-23-

Consumer Brands

Growth &Profitability

SupplyChain

ShopperMarketing

Sales Force/Customer Teams

®

Insights/Category Leadership

MarketingApproach

Consumer Brands

“THIS A TOUGH ONE. I think a lot of these manufacturers have some tough issues and challeng-es ahead. They’ve boxed themselves into a corner with clubs and special deals by retailer. This isn’t sustainable and will cause waste in their supply chains, which will end up having to be addressed.”

“GENERAL MILLS has worked with our teams to drive top line sales through effective marketing and merchandising programs while reducing costs in the supply chain.”

“PEPSICO has strong growth in core brands and significant growth in more profitable segments that enable us to be differentiated.”

RANK

2013 2012

Unilever

General Mills

Kraft Foods Group

PepsiCo

Procter & Gamble

Conagra

Nestle

Kellogg

Mondelēz

Hershey

%

1

2

3

4

5

6

7

8

9

10

3

2

-

6

5

7

4

8

-

20

22.5

19.8

18.2

12.9

12.5

12.1

11.5

10.0

6.5

5.4

“UNILEVER consistently grows top line sales while at the same time, growing profits ahead of sales.” RETAILER COMMENT

Retailer Comments on Best Combination of Growth & Profitability

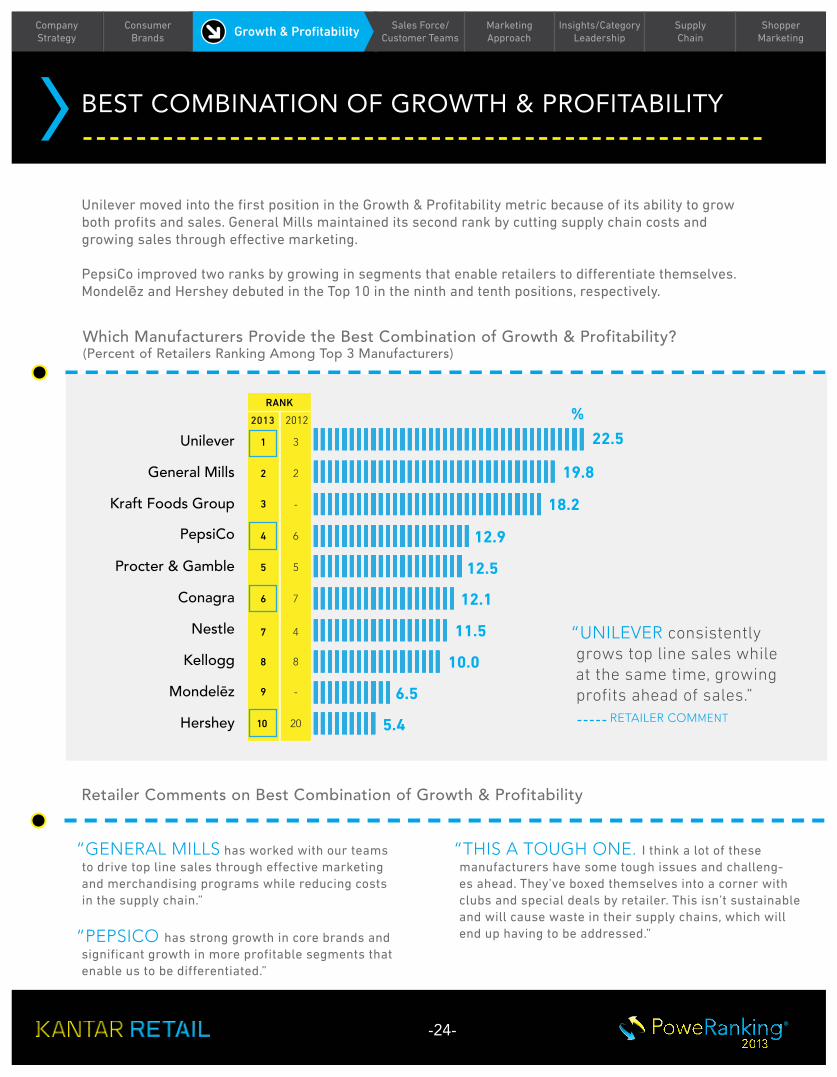

Which Manufacturers Provide the Best Combination of Growth & Profitability?(Percent of Retailers Ranking Among Top 3 Manufacturers)

Unilever moved into the first position in the Growth & Profitability metric because of its ability to grow both profits and sales. General Mills maintained its second rank by cutting supply chain costs and growing sales through effective marketing.

PepsiCo improved two ranks by growing in segments that enable retailers to differentiate themselves. Mondelēz and Hershey debuted in the Top 10 in the ninth and tenth positions, respectively.

BEST COMBINATION OF GROWTH & PROFITABILITY

Growth & ProfitabilityCompany Strategy

-24-

®

Consumer Brands

Company Strategy

Growth &Profitability

MarketingApproach

Insights/Category Leadership

SupplyChain

ShopperMarketing

Sales Force/Customer Teams

Retailer Comments on Business Fundamentals Metrics

2013 PoweRanking® Business Fundamentals Composite

“UNILEVER continues to work with our category teams to develop and implement consumer market-ing programming that increases consumer traffic in the store and basket size.”

“GENERAL MILLS has provided active engagement in improving the overall supply chain and providing strong fill rates.”

RANK

2013 2012

Procter & Gamble

Unilever

General Mills

Kraft Foods Group

PepsiCo

Nestle

Kellogg

Coca-Cola

Mondelēz

Kimberly-Clark

%

1

2

3

4

5

6

7

8

9

10

1

4

3

-

5

6

8

7

-

10

28.9

26.2

26.0

19.2

18.2

13.2

12.2

10.6

7.8

7.6

“P&G has the depth and breadth of category knowledge and the resources to gather and analyze data/research and develop key insights.” RETAILER COMMENT

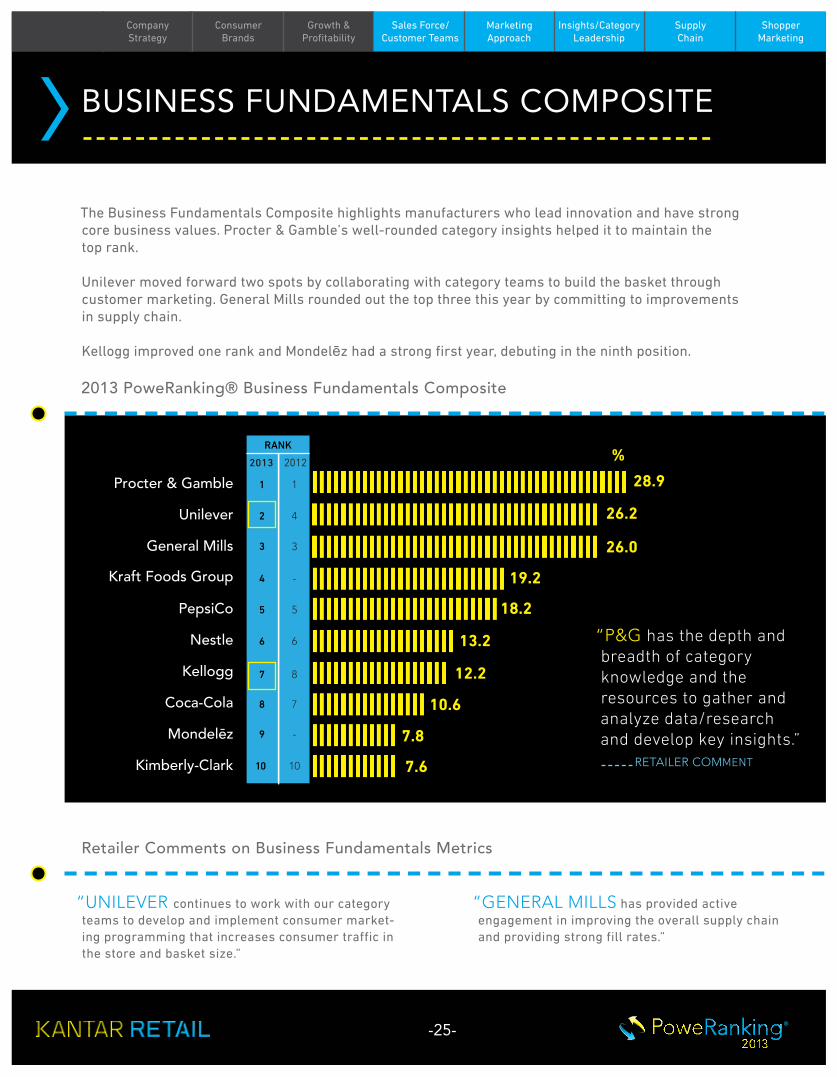

The Business Fundamentals Composite highlights manufacturers who lead innovation and have strong core business values. Procter & Gamble’s well-rounded category insights helped it to maintain the top rank. Unilever moved forward two spots by collaborating with category teams to build the basket through customer marketing. General Mills rounded out the top three this year by committing to improvements in supply chain.

Kellogg improved one rank and Mondelēz had a strong first year, debuting in the ninth position.

BUSINESS FUNDAMENTALS COMPOSITE

-25-

Growth &Profitability

SupplyChain

ShopperMarketing

Sales Force/Customer Teams

®

Insights/Category Leadership

MarketingApproach

“The HERSHEY team is able to work collaboratively to provide programs tailored to our business model and follows through with execution.”

RANK

2013 2012

General Mills

Procter & Gamble

Unilever

Kellogg

Kraft Foods Group

PepsiCo

Coca-Cola

Nestle

Mondelēz

Hershey

%

1

2

3

4

5

6

7

8

9

10

3

1

4

6

-

5

8

7

-

18

25.6

25.3

24.7

19.6

18.3

17.8

11.8

11.8

8.5

7.2

“GENERAL MILLS’ sales teams are experienced, know the job and the customer as well as the overall strategy of their company.” RETAILER COMMENT

Retailer Comments on Best Sales Force/Customer Teams

“KELLOGG knows their business and categories they play in very well and how to apply that knowledge to retail initiatives.”

Which Manufacturers Have the Best Sales Force/Customer Teams?(Percent of Retailers Ranking Among Top 3 Manufacturers)

General Mills rose two positions in the Customer Teams metric to take over the first position due to its seasoned sales teams. Unilever rounded out the top three after improving one rank. Kellogg jumped two ranks because of its customer teams’ sound knowledge of the category.

Retailers recognized Hershey’s collaboration to create tailored programs, earning the company a spot in the Top 10 for the first time.

BEST SALES FORCE/CUSTOMER TEAMS

Sales Force/ Customer Teams

Company Strategy

Consumer Brands

Growth &Profitability

-26-

MarketingPrograms

SupplyChain

ShopperMarketing

®

Insights/Category Leadership

Sales Force/Customer Teams

“UNILEVER balances the need to customize with retailers with national cause and benefit marketing to create holistic and effective programs.”

RANK

2013 2012

Procter & Gamble

Unilever

General Mills

Kraft Foods Group

PepsiCo

Kellogg

Coca-Cola

Nestle

Kimberly-Clark

Mars

%

1

2

3

4

5

6

7

8

9

10

1

4

3

-

5

8

7

6

10

11

30.3

27.5

20.6

19.0

17.7

11.6

11.0

9.7

8.5

6.7

“P&G truly understands what makes their consumer tick, and taps into that on a regular basis. I believe the work they’re doing in digital marketing, in particular, is way ahead of their peers.” RETAILER COMMENT

Retailer Comments on Most Innovative Marketing Approach

“KIMBERLY-CLARK is the most focused on category growth versus brand switching.”

Which Manufacturers Have the Most Innovative Overall Marketing Approach?(Percent of Retailers Ranking Among Top 3 Manufacturers)

Procter & Gamble held its position as the most innovative marketer by having the best understanding of its consumers. Unilever surpassed General Mills to move into the second rank as it was recognized for customized marketing programs that were successful at retail.

Kellogg improved two ordinal ranks. For the second year in a row, Kimberly-Clark saw its rank improve by focusing its attention on category growth.

MOST INNOVATIVE MARKETING APPROACH

Company Strategy

Consumer Brands

Growth &Profitability Marketing Approach

-27-

ConsumerInsights

SupplyChain

ShopperMarketing

®

MarketingApproach

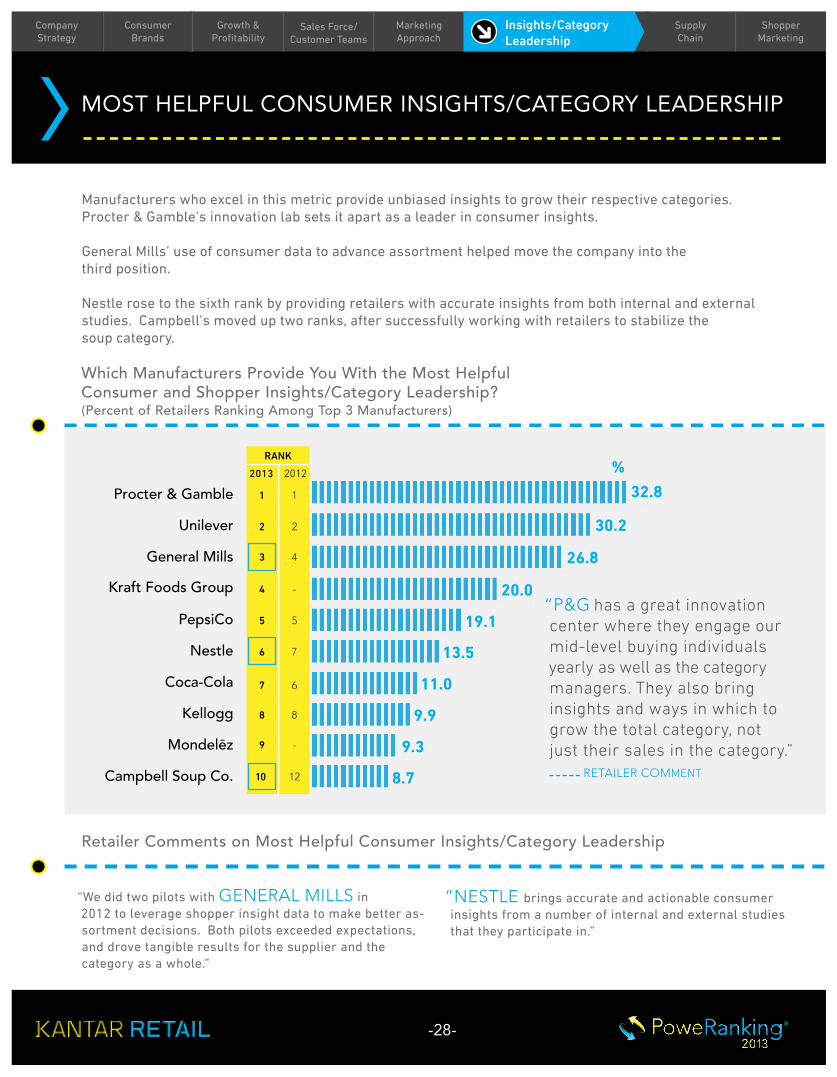

Manufacturers who excel in this metric provide unbiased insights to grow their respective categories. Procter & Gamble’s innovation lab sets it apart as a leader in consumer insights.

General Mills’ use of consumer data to advance assortment helped move the company into the third position.

Nestle rose to the sixth rank by providing retailers with accurate insights from both internal and external studies. Campbell’s moved up two ranks, after successfully working with retailers to stabilize the soup category.

“We did two pilots with GENERAL MILLS in 2012 to leverage shopper insight data to make better as-sortment decisions. Both pilots exceeded expectations, and drove tangible results for the supplier and the category as a whole.”

RANK

2013 2012

Procter & Gamble

Unilever

General Mills

Kraft Foods Group

PepsiCo

Nestle

Coca-Cola

Kellogg

Mondelēz

Campbell Soup Co.

%

1

2

3

4

5

6

7

8

9

10

1

2

4

-

5

7

6

8

-

12

32.8

30.2

26.8

20.0

19.1

13.5

11.0

9.9

9.3

8.7

“P&G has a great innovation center where they engage our mid-level buying individuals yearly as well as the category managers. They also bring insights and ways in which to grow the total category, not just their sales in the category.” RETAILER COMMENT

Retailer Comments on Most Helpful Consumer Insights/Category Leadership

Which Manufacturers Provide You With the Most Helpful Consumer and Shopper Insights/Category Leadership?(Percent of Retailers Ranking Among Top 3 Manufacturers)

MOST HELPFUL CONSUMER INSIGHTS/CATEGORY LEADERSHIP

Insights/Category Leadership

Sales Force/Customer Teams

Company Strategy

Consumer Brands

Growth &Profitability

“NESTLE brings accurate and actionable consumer insights from a number of internal and external studies that they participate in.”

-28-

ConsumerInsights

SupplyChain

ShopperMarketing

®

General Mills improved one ordinal rank to lead the Supply Chain Management metric. Retailers value General Mills’ commitment to improving service while cutting costs.

Procter & Gamble’s access to supply chain expertise and its solutions-oriented approach allows it to capi-talize on opportunities.

Nestle and Kimberly-Clark both improved their ranks as each was recognized for their flexibility.

“P&G is a great thought partner in supply chain, and are top of mind to help solve supply chain issues. When presented with a problem or opportunity to solve, they quickly reach out to subject matter experts within their organization to address our areas of opportunity. They are structured well to respond and respond quickly.”

RANK

2013 2012

General Mills

Procter & Gamble

Nestle

Kraft Foods Group

Unilever

PepsiCo

Kellogg

Kimberly-Clark

Heinz

Campbell Soup Co.

%

1

2

3

4

5

6

7

8

9

10

2

1

4

-

5

6

9

9

8

13

30.5

26.0

22.2

17.1

15.8

11.2

9.2

9.2

8.0

7.4

“GENERAL MILLS allocates resources and works with our team to identify opportunities for improving service, while removing cost from the supply chain.” RETAILER COMMENT

Retailer Comments on Best Supply Chain Management

“NESTLE is willing to partner with us to find creative and flexible ways to get product through the supply chain in less time and for less money.”

“KIMBERLY-CLARK is flexible, forward thinking and willing to listen.”

Which Manufacturers Practice the Best Supply Chain Management?(Percent of Retailers Ranking Among Top 3 Manufacturers)

BEST SUPPLY CHAIN MANAGEMENT

Supply ChainMarketingApproach

Insights/Category Leadership

Sales Force/Customer Teams

Company Strategy

Consumer Brands

Growth &Profitability

-29-

SupplyChain

ShopperMarketing

®

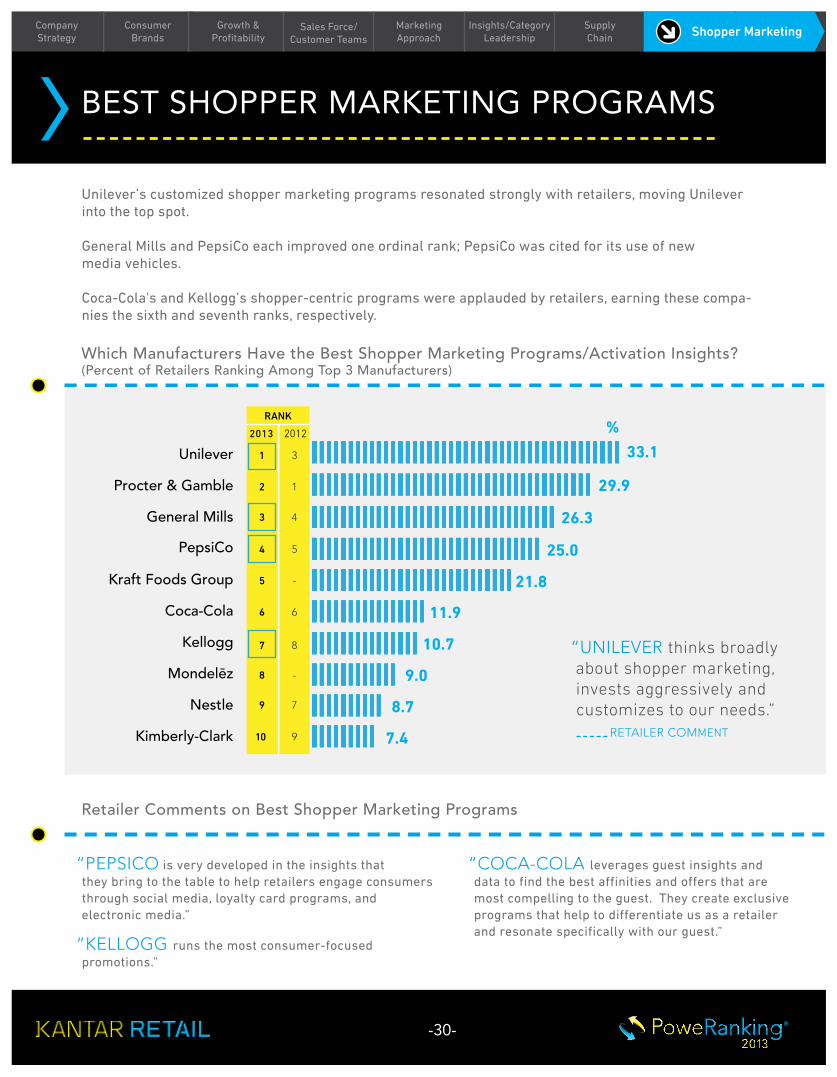

Unilever’s customized shopper marketing programs resonated strongly with retailers, moving Unilever into the top spot.

General Mills and PepsiCo each improved one ordinal rank; PepsiCo was cited for its use of new media vehicles.

Coca-Cola's and Kellogg’s shopper-centric programs were applauded by retailers, earning these compa-nies the sixth and seventh ranks, respectively.

“COCA-COLA leverages guest insights and data to find the best affinities and offers that are most compelling to the guest. They create exclusive programs that help to differentiate us as a retailer and resonate specifically with our guest.”

RANK

2013 2012

Unilever

Procter & Gamble

General Mills

PepsiCo

Kraft Foods Group

Coca-Cola

Kellogg

Mondelēz

Nestle

Kimberly-Clark

%

1

2

3

4

5

6

7

8

9

10

3

1

4

5

-

6

8

-

7

9

33.1

29.9

26.3

25.0

21.8

11.9

10.7

9.0

8.7

7.4

“UNILEVER thinks broadly about shopper marketing, invests aggressively and customizes to our needs.” RETAILER COMMENT

Retailer Comments on Best Shopper Marketing Programs

“PEPSICO is very developed in the insights that they bring to the table to help retailers engage consumers through social media, loyalty card programs, and electronic media.”

“KELLOGG runs the most consumer-focused promotions.”

Which Manufacturers Have the Best Shopper Marketing Programs/Activation Insights?(Percent of Retailers Ranking Among Top 3 Manufacturers)

BEST SHOPPER MARKETING PROGRAMS

Shopper MarketingMarketingApproach

Insights/Category Leadership

Supply Chain

Sales Force/Customer Teams

Company Strategy

Consumer Brands

Growth &Profitability

-30-

®

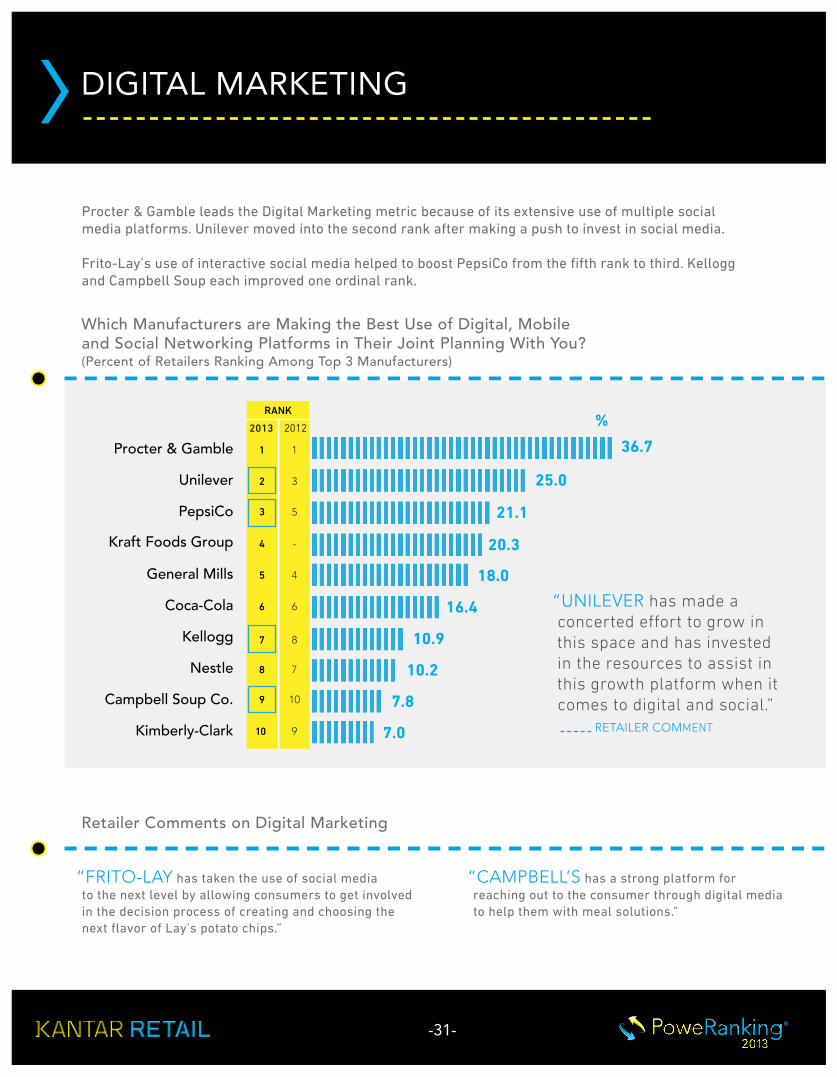

Procter & Gamble leads the Digital Marketing metric because of its extensive use of multiple social media platforms. Unilever moved into the second rank after making a push to invest in social media.

Frito-Lay’s use of interactive social media helped to boost PepsiCo from the fifth rank to third. Kellogg and Campbell Soup each improved one ordinal rank.

“FRITO-LAY has taken the use of social media to the next level by allowing consumers to get involved in the decision process of creating and choosing the next flavor of Lay’s potato chips.”

RANK

2013 2012

Procter & Gamble

Unilever

PepsiCo

Kraft Foods Group

General Mills

Coca-Cola

Kellogg

Nestle

Campbell Soup Co.

Kimberly-Clark

%

1

2

3

4

5

6

7

8

9

10

1

3

5

-

4

6

8

7

10

9

36.7

25.0

21.1

20.3

18.0

16.4

10.9

10.2

7.8

7.0

“UNILEVER has made a concerted effort to grow in this space and has invested in the resources to assist in this growth platform when it comes to digital and social.” RETAILER COMMENT

Retailer Comments on Digital Marketing

“CAMPBELL’S has a strong platform for reaching out to the consumer through digital media to help them with meal solutions.”

Which Manufacturers are Making the Best Use of Digital, Mobile and Social Networking Platforms in Their Joint Planning With You?(Percent of Retailers Ranking Among Top 3 Manufacturers)

DIGITAL MARKETING

-31-

RETAILER RANKINGS

Store Branding

Company Strategy

Projected Power Retailers

Cat-Man / Buying Teams

SupplyChain

Category Leadership

Best to do Business With

®

Innovative Merchandising

2013 POWERANKING® COMPOSITE

Manufacturer Comments on Composite

2013 PoweRanking® Composite

“The ‘alternate channels’ continue to be the growth engines in the grocery retailing space, and

COSTCO is the leader of the pack with pricing that cannot be beat in the current environment, along with great merchandising, quality and fun.”

“WALMART, being by far the largest retailer, will continue to evolve and adjust to consumer/shopper needs. They are open to building strategic partner-ships with manufacturers and they capitalize on the available information to build their plans.”

Note: The composite score is a two-year rolling aggregate of individual metric scores of the percent of manufacturers ranking retailers among the top three.

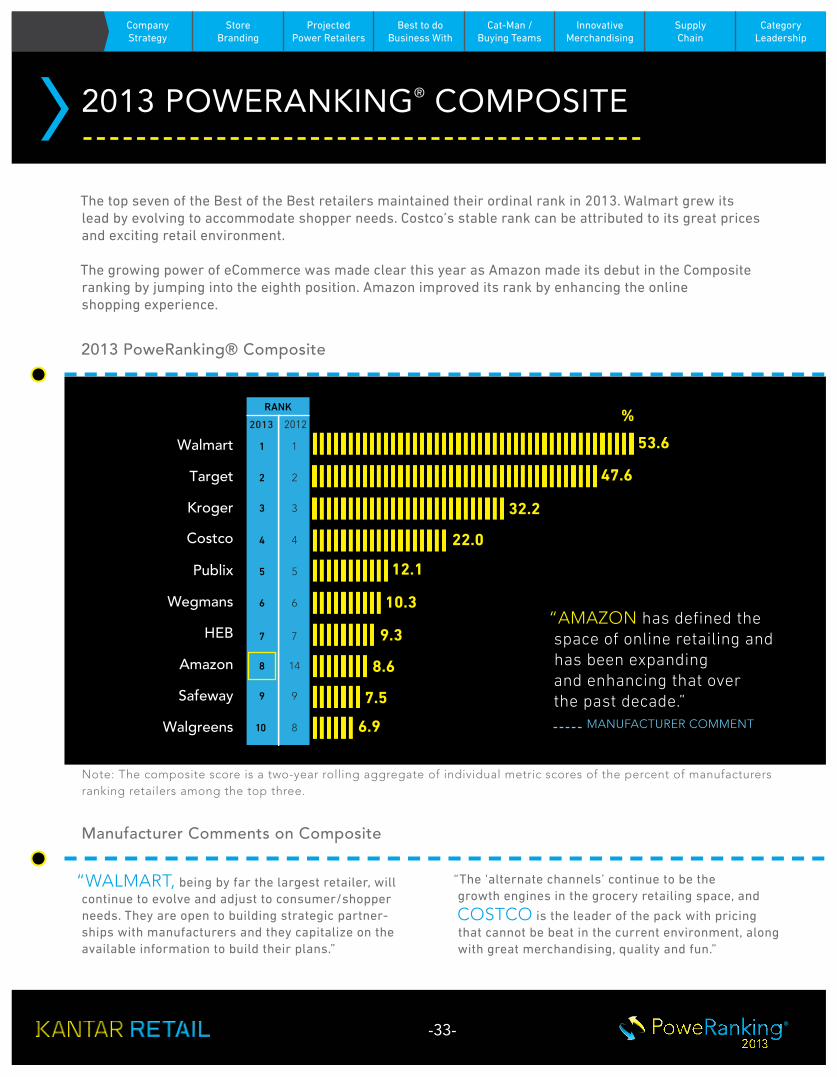

RANK

2013 2012

Walmart

Target

Kroger

Costco

Publix

Wegmans

HEB

Amazon

Safeway

Walgreens

1

2

3

4

5

6

7

8

9

10

1

2

3

4

5

6

7

14

9

8

53.6

47.6

32.2

22.0

12.1

10.3

9.3

8.6

7.5

6.9

%

The top seven of the Best of the Best retailers maintained their ordinal rank in 2013. Walmart grew its lead by evolving to accommodate shopper needs. Costco’s stable rank can be attributed to its great prices and exciting retail environment.

The growing power of eCommerce was made clear this year as Amazon made its debut in the Composite ranking by jumping into the eighth position. Amazon improved its rank by enhancing the online shopping experience.

“AMAZON has defined the space of online retailing and has been expanding and enhancing that over the past decade.” MANUFACTURER COMMENT

-33-

Store Branding

Company Strategy

Projected Power Retailers

Cat-Man / Buying Teams

SupplyChain

Category Leadership

Best to do Business With

®

Innovative Merchandising

Manufacturer Comments on Composite

2013 PoweRanking® Composite

“HEB will evaluate each category at its highest level, including Hispanic and Ethnic items and adapting each store’s product mix to the local influences. They are also very much open to testing and experiencing, with collaborative work that we do not see in many accounts.”

“TARGET puts the wants/needs of their guests first in everything. They have created such a positive shopping experience for their guests that guests often give them credit for carrying more brands and sizes than they actually do.”

Note: The composite score is a two-year rolling aggregate of individual metric scores of the percent of manufacturers ranking retailers among the top three.

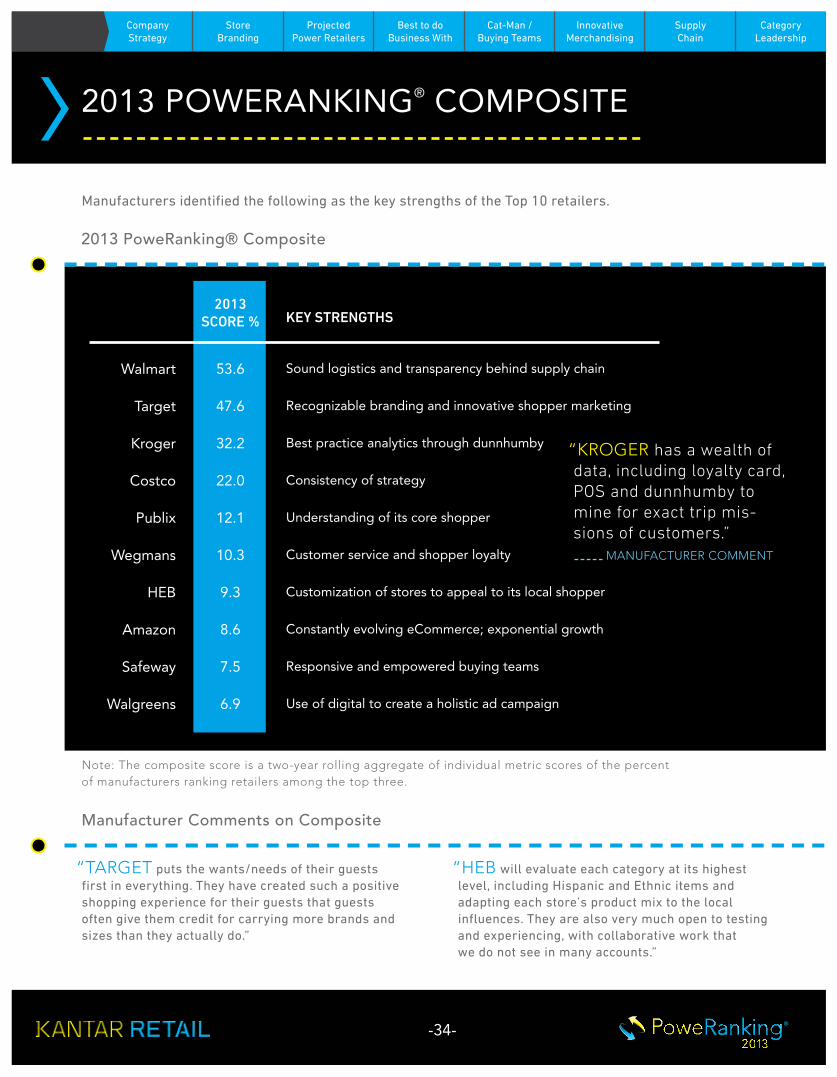

Manufacturers identified the following as the key strengths of the Top 10 retailers.

“KROGER has a wealth of data, including loyalty card, POS and dunnhumby to mine for exact trip mis-sions of customers.” MANUFACTURER COMMENT

KEY STRENGTHS

Walmart

Target

Kroger

Costco

Publix

Wegmans

HEB

Amazon

Safeway

Walgreens

53.6

47.6

32.2

22.0

12.1

10.3

9.3

8.6

7.5

6.9

Sound logistics and transparency behind supply chain

Recognizable branding and innovative shopper marketing Best practice analytics through dunnhumby

Consistency of strategy

Understanding of its core shopper

Customer service and shopper loyalty

Customization of stores to appeal to its local shopper

Constantly evolving eCommerce; exponential growth

Responsive and empowered buying teams

Use of digital to create a holistic ad campaign

2013 SCORE %

2013 POWERANKING® COMPOSITE

-34-

Store Branding

Company Strategy

Projected Power Retailers

Cat-Man / Buying Teams

SupplyChain

Category Leadership

Best to do Business With

®

Customer service and shopper loyalty

Branding of stores, products and employees Aggressive testing of merchandising

Generating and maintaining shopper loyalty

More mainstream shopper attraction

Collaborative, flexible and teamwork centric

Omni-shopper relationship

Easy to do business

Innovative Merchandising

Manufacturer Comments on Composite

Wegmans

Trader Joe’s

Giant Eagle

Harris Teeter

Family Dollar

Hy-Vee

Wawa

Demoulas Market Basket

6

16

17

20

21

23

29

30

6

17

16

19

23

28

32

35

2013 RANK

2012 RANK

POWERANKING® COMPOSITE UNDER $10B

Manufacturer Comments on Composite

2013 PoweRanking® Composite Under $10B

“Everything from product assortment to store environ-ment at TRADER JOE’S speaks to their company strategy: Wholesome, Natural and Specialty.”

“WEGMANS knows their customer and sternly aligns their strategy to meet and exceed their shoppers’ expectations.”

Manufacturers identified PoweRanking leaders under $10B. These retailers are recognized for being collaborative and innovative in merchandising, and having clearly branded themselves.

“HY-VEE is constantly testing and challenging the retail norms. They are willing to test, try and change.” MANUFACTURER COMMENT

KEY STRENGTHS

-35-

STRATEGIC COMPOSITE

Store Branding

Projected Power Retailers

Cat-Man / Buying Teams

SupplyChain

Category Leadership

Best to do Business With

Company Strategy

®

Innovative Merchandising

Manufacturer Comments on Strategic Metrics

2013 PoweRanking® Strategic Composite

“AMAZON is the clear leader in the eCommerce space with-out any obvious retail alternative. The Prime member model presents a compelling consumer value between price and convenience — and offers a very attractive, loyalty-building opportunity and threat for all CPG manufacturers.”

“WALMART is returning to their roots but in a more modern way. They know who they are and they are not going to apologize for it.”

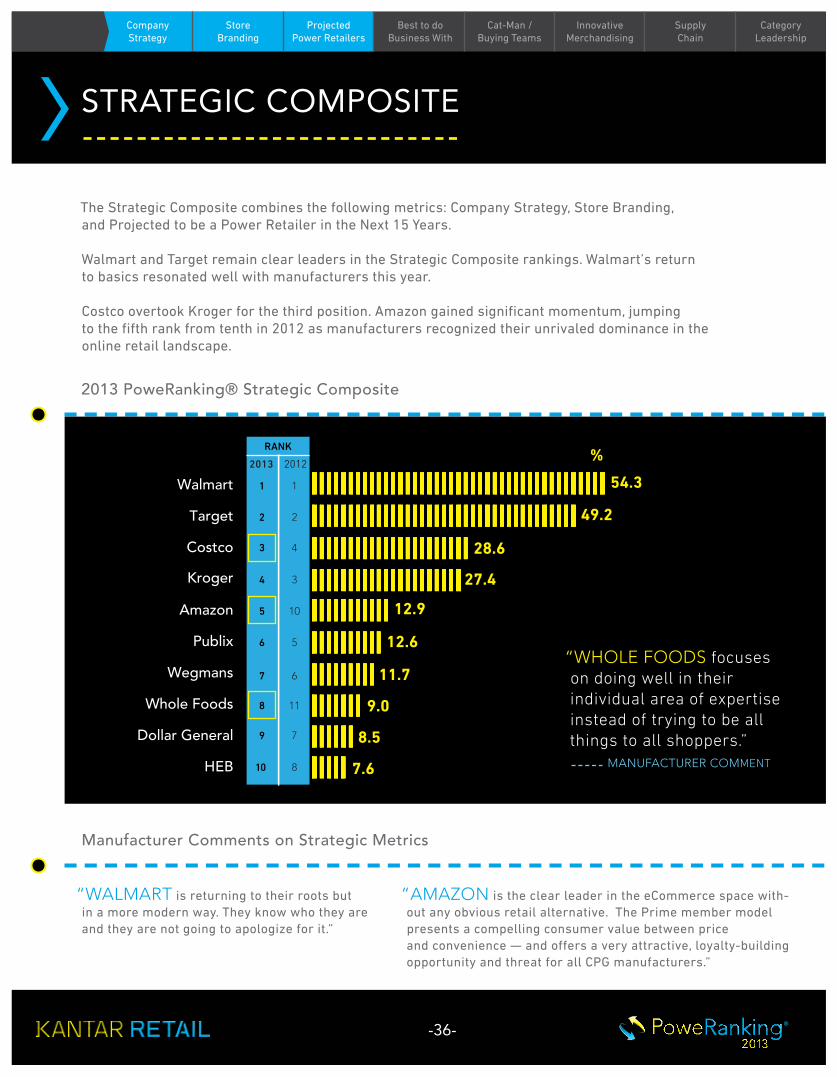

The Strategic Composite combines the following metrics: Company Strategy, Store Branding, and Projected to be a Power Retailer in the Next 15 Years.

Walmart and Target remain clear leaders in the Strategic Composite rankings. Walmart’s return to basics resonated well with manufacturers this year.

Costco overtook Kroger for the third position. Amazon gained significant momentum, jumping to the fifth rank from tenth in 2012 as manufacturers recognized their unrivaled dominance in the online retail landscape.

RANK

2013 2012

Walmart

Target

Costco

Kroger

Amazon

Publix

Wegmans

Whole Foods

Dollar General

HEB

1

2

3

4

5

6

7

8

9

10

1

2

4

3

10

5

6

11

7

8

54.3

49.2

28.6

27.4

12.9

12.6

11.7

9.0

8.5

7.6

%

“WHOLE FOODS focuses on doing well in their individual area of expertise instead of trying to be all things to all shoppers.” MANUFACTURER COMMENT

-36-

Store Branding

Company Strategy

Projected Power Retailers

Cat-Man / Buying Teams

Innovative Marketing/ Merch

SupplyChain

Category LeadershipCompany Strategy Best to do

Business With

®

Manufacturer Comments on Clearest Company Strategy

Which Retailers Have the Clearest Company Strategy? (Percent of Manufacturers Ranking Among Top 3 Retailers)

“COSTCO’S strategy is clear and clean. They know their customer. They have a powerful yet simple assortment, and it resonates well with consumers.”

“WALMART’S strategy is clearly articulated, it’s a part of their execution, and it hasn’t changed for years.”

“WEGMANS has stayed true to their EDLP strategy with a great perimeter and the best customer service.”

RANK

2013 2012

Walmart

Target

Kroger

Costco

Publix

Wegmans

HEB

Dollar General

Walgreens

Whole Foods

1

2

3

4

5

6

7

8

9

10

1

2

3

4

5

6

8

7

9

13

55.7

45.1

30.2

28.8

12.1

10.6

8.6

8.5

7.4

6.2

%

The top six retailers maintained their ordinal rank in the Clearest Company Strategy metric. Walmart expanded its lead by sticking to its tried-and-true strategy.

HEB improved in rank and Whole Foods broke into the Top 10 for the first time. Retailers receiving high marks on this metric closely tie their strategy to their shoppers’ expectations.

“TARGET has a strong understanding of their shopper experience, and that self-awareness drives all they do.” MANUFACTURER COMMENT

CLEAREST COMPANY STRATEGY

Store Branding

Company Strategy

Projected Power Retailers

Cat-Man / Buying Teams

Innovative Merchandising

SupplyChain

Category LeadershipCompany Strategy Best to do

Business With

-37-

Store Branding

Company Strategy

Cat-Man / Buying Teams

SupplyChain

Category Leadership

Best to do Business With

®

Innovative Merchandising

Projected Power Retailers

Manufacturer Comments on Store Branding

“Through Premium and 365, WHOLE FOODS delivers at high end and value, all wrapped in Whole Foods branding, and very consistent from store to store.”

“WEGMANS stores are an experience from their prepared foods sections to their private label presence, making it exciting to shop.”

RANK

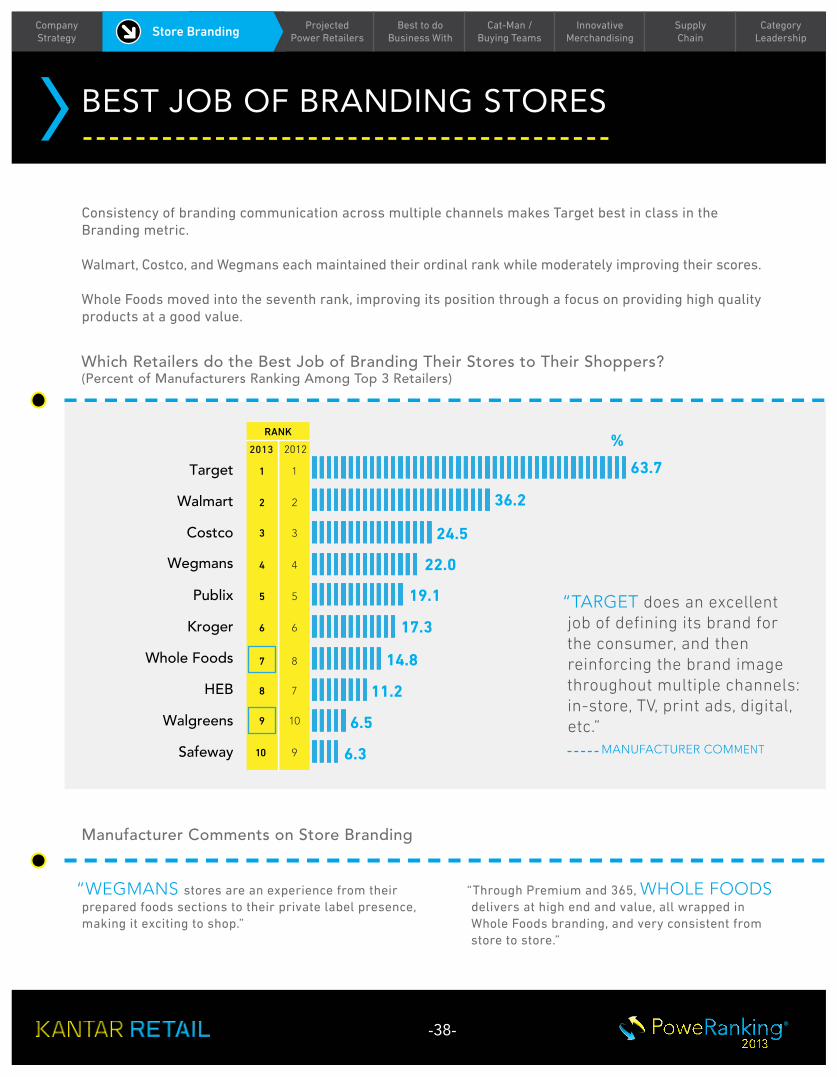

2013 2012

Target

Walmart

Costco

Wegmans

Publix

Kroger

Whole Foods

HEB

Walgreens

Safeway

1

2

3

4

5

6

7

8

9

10

1

2

3

4

5

6

8

7

10

9

63.7

36.2

24.5

22.0

19.1

17.3

14.8

11.2

6.5

6.3

%

“TARGET does an excellent job of defining its brand for the consumer, and then reinforcing the brand image throughout multiple channels: in-store, TV, print ads, digital, etc.” MANUFACTURER COMMENT

Which Retailers do the Best Job of Branding Their Stores to Their Shoppers? (Percent of Manufacturers Ranking Among Top 3 Retailers)

Consistency of branding communication across multiple channels makes Target best in class in the Branding metric.

Walmart, Costco, and Wegmans each maintained their ordinal rank while moderately improving their scores.

Whole Foods moved into the seventh rank, improving its position through a focus on providing high quality products at a good value.

Company Strategy

BEST JOB OF BRANDING STORES

Store Branding

-38-

Store Branding

Projected Power Retailers

Cat-Man / Buying Teams

SupplyChain

Category Leadership

Best to do Business With

®

Innovative Merchandising

Store Branding

Manufacturer Comments on Projected to be Power Retailers

“TARGET is getting more aggressive with expanding their food sections and they offer a better shopping experience.”

“As online shopping continues to grow, AMAZON is set up perfectly to continue capturing share of the market. They have an incredible equity and trust with shoppers, what appears to be a solid business model, and strong leadership in place.”

RANK

2013 2012

Walmart

Target

Kroger

Costco

Amazon

Dollar General

Walgreens

Publix

Whole Foods

CVS

1

2

3

4

5

6

7

8

9

10

1

2

3

4

5

6

7

8

12

9

70.9

38.6

34.6

32.5

30.0

13.4

6.9

6.5

5.8

5.1

%

“I can’t imagine a day where winning the pricing game will not be important. WALMART has a laser focus on consumers’ need for quality values everyday.” MANUFACTURER COMMENT

Amazon saw huge growth this year in the Power Retailer metric, reflecting its ever-growing strength in eCommerce.

Manufacturers expect that price will continue to be top of mind for shoppers, which is a battle that Walmart is projected to continue to win. Target and Kroger held their ranks to round out the top three; manufactur-ers see customer loyalty as the biggest strength of these retailers.

Whole Foods improved on this metric, breaking into the Top 10, up from the twelfth rank in 2012.

Company Strategy

PROJECTED TO BE POWER RETAILERS IN THE NEXT 15 YEARS

Power Retailers

Which Retailers do You Project to be the “Power Retailers” in 15 Years? (Percent of Manufacturers Ranking Among Top 3 Retailers)

-39-

®

Manufacturer Comments in Business Fundamentals Metrics

“MEIJER is a true partner willing to invest and support category growth that rewards their customers and supports their overall business strategy. Meijer meets with us every quarter to evaluate results and looks to improve despite excellent results.”

“TARGET often leads the trends in CPG in-store presentation, assortment, and meeting the basic fundamentals of reliability.”

2013 PoweRanking® Business Fundamentals Composite

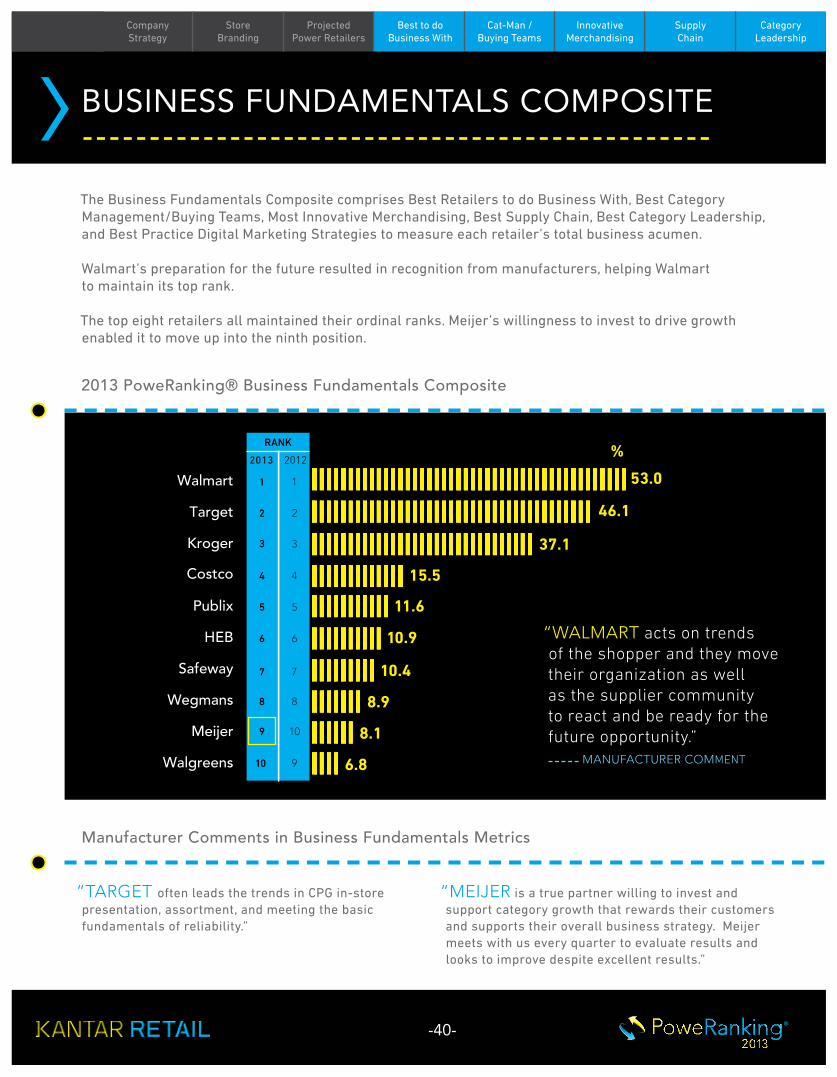

The Business Fundamentals Composite comprises Best Retailers to do Business With, Best Category Management/Buying Teams, Most Innovative Merchandising, Best Supply Chain, Best Category Leadership, and Best Practice Digital Marketing Strategies to measure each retailer’s total business acumen.

Walmart’s preparation for the future resulted in recognition from manufacturers, helping Walmart to maintain its top rank.

The top eight retailers all maintained their ordinal ranks. Meijer’s willingness to invest to drive growth enabled it to move up into the ninth position.

RANK

2013 2012

Walmart

Target

Kroger

Costco

Publix

HEB

Safeway

Wegmans

Meijer

Walgreens

1

2

3

4

5

6

7

8

9

10

1

2

3

4

5

6

7

8

10

9

53.0

46.1

37.1

15.5

11.6

10.9

10.4

8.9

8.1

6.8

%

“WALMART acts on trends of the shopper and they move their organization as well as the supplier community to react and be ready for the future opportunity.” MANUFACTURER COMMENT

BUSINESS FUNDAMENTALS COMPOSITE

Store Branding

Projected Power Retailers

Cat-Man / Buying Teams

Innovative Merchandising

SupplyChain

Category Leadership

Best to do Business With

Company Strategy

-40-

Store Branding

Company Strategy

Projected Power Retailers

Cat-Man / Buying Teams

SupplyChain

Category Leadership

Best to do Business With

®

Innovative Merchandising

Sales Force/Customer Teams

Manufacturer Comments on Best to Do Business With

“KROGER is collaborative, respectful, and has goals that mutually benefit both themselves and their vendor partners.”

“TARGET provides clear expectations, offers tremendous vendor community support for training, is ethical and has integrity in their business approach.”

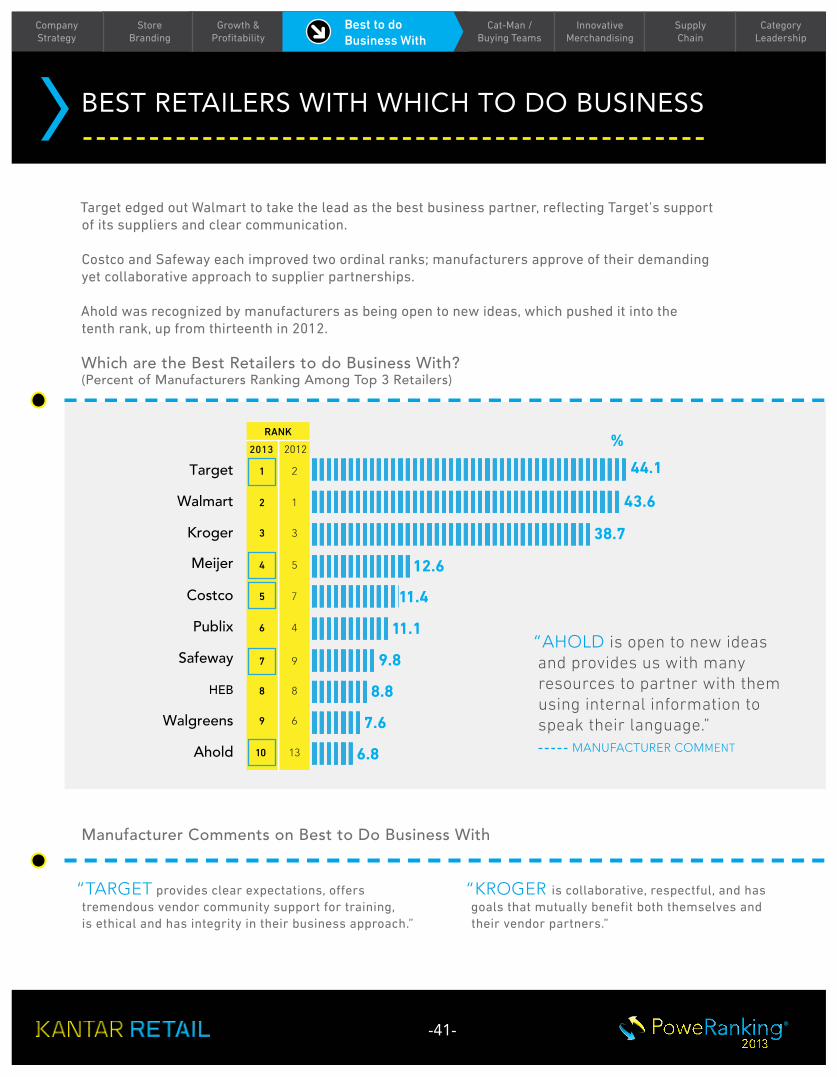

RANK

2013 2012

Target

Walmart

Kroger

Meijer

Costco

Publix

Safeway

HEB

Walgreens

Ahold

1

2

3

4

5

6

7

8

9

10

2

1

3

5

7

4

9

8

6

13

44.1

43.6

38.7

12.6

11.4

11.1

9.8

8.8

7.6

6.8

%

“AHOLD is open to new ideas and provides us with many resources to partner with them using internal information to speak their language.” MANUFACTURER COMMENT

Which are the Best Retailers to do Business With? (Percent of Manufacturers Ranking Among Top 3 Retailers)

Target edged out Walmart to take the lead as the best business partner, reflecting Target’s support of its suppliers and clear communication.

Costco and Safeway each improved two ordinal ranks; manufacturers approve of their demanding yet collaborative approach to supplier partnerships.

Ahold was recognized by manufacturers as being open to new ideas, which pushed it into the tenth rank, up from thirteenth in 2012.

Company Strategy

BEST RETAILERS WITH WHICH TO DO BUSINESS

Growth &Profitability

Store Branding

Best to do Business With

-41-

Store Branding

Company Strategy

Projected Power Retailers

SupplyChain

Category Leadership

Best to do Business With

®

Innovative Merchandising

Sales Force/Customer Teams

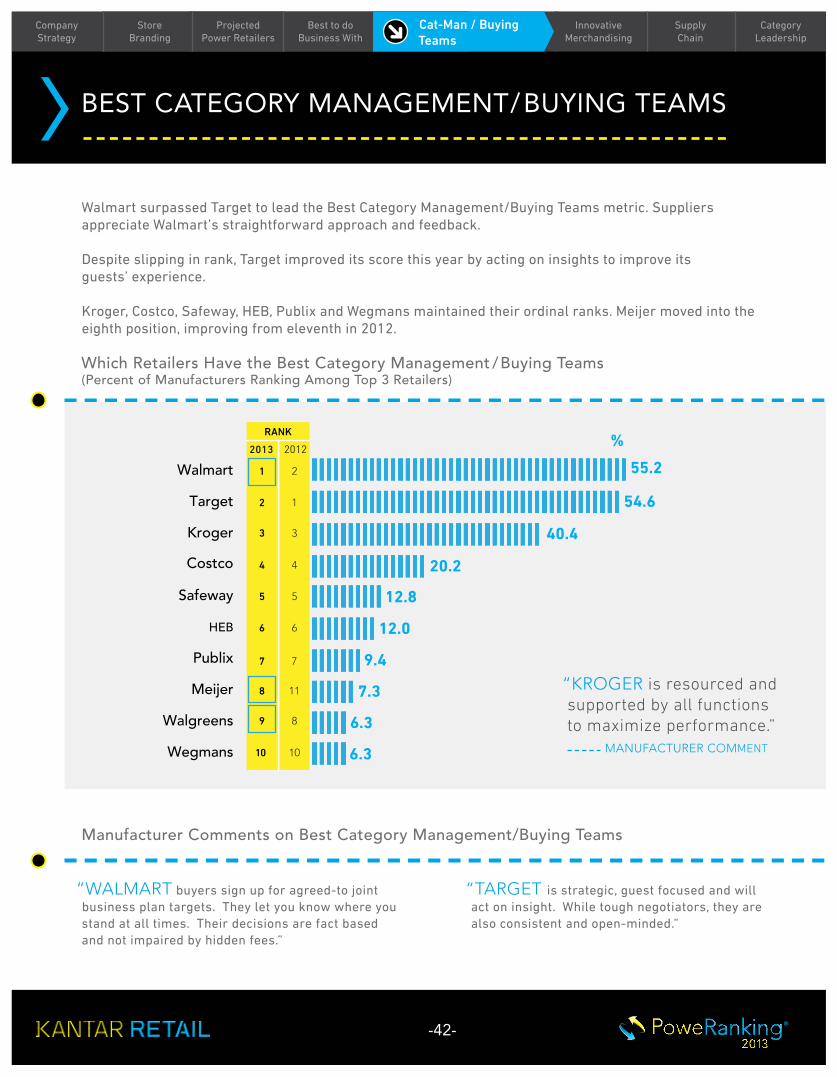

Manufacturer Comments on Best Category Management/Buying Teams

“TARGET is strategic, guest focused and will act on insight. While tough negotiators, they are also consistent and open-minded.”

“WALMART buyers sign up for agreed-to joint business plan targets. They let you know where you stand at all times. Their decisions are fact based and not impaired by hidden fees.”

RANK

2013 2012

Walmart

Target

Kroger

Costco

Safeway

HEB

Publix

Meijer

Walgreens

Wegmans

1

2

3

4

5

6

7

8

9

10

2

1

3

4

5

6

7

11

8

10

55.2

54.6

40.4

20.2

12.8

12.0

9.4

7.3

6.3

6.3

%

“KROGER is resourced and supported by all functions to maximize performance.”

MANUFACTURER COMMENT

Walmart surpassed Target to lead the Best Category Management/Buying Teams metric. Suppliers appreciate Walmart’s straightforward approach and feedback.

Despite slipping in rank, Target improved its score this year by acting on insights to improve its guests’ experience.

Kroger, Costco, Safeway, HEB, Publix and Wegmans maintained their ordinal ranks. Meijer moved into the eighth position, improving from eleventh in 2012.

Company Strategy

BEST CATEGORY MANAGEMENT/BUYING TEAMS

Store Branding

Cat-Man / Buying Teams

Best to do Business With

Projected Power Retailers

Which Retailers Have the Best Category Management /Buying Teams (Percent of Manufacturers Ranking Among Top 3 Retailers)

-42-

SupplyChain

Category Leadership

®

Cat-Man / Buying Teams

Best to do Business With

Projected Power Retailers

Store Branding

Manufacturer Comments on Most Innovative Merchandising Approach

“WALMART’S use of exclusive packs and offer in media and grocery is innovative thinking to draw the consumer to their stores versus their competitors who may have better service departments, etc.”

“WEGMANS is doing more to push the boundaries of a ‘grocery’ store than anyone else out there, turning grocery shopping into a destination event for their shopper.”

“WALGREENS is leveraging every available inch within their stores and is getting creative with how they bring their categories to life through their merchandising efforts.”

RANK

2013 2012

Target

Kroger

Wegmans

Walmart

HEB

Costco

Publix

Whole Foods

Walgreens

Safeway

1

2

3

4

5

6

7

8

9

10

1

2

3

6

4

7

5

8

12

9

51.3

27.7

21.3

19.3

16.2

12.5

11.3

11.2

10.1

9.1

%

“TARGET is very innovative when thinking about fashion/design. Target appeals to both men and women, and their departments have the feel of a specialty retailer.” MANUFACTURER COMMENT

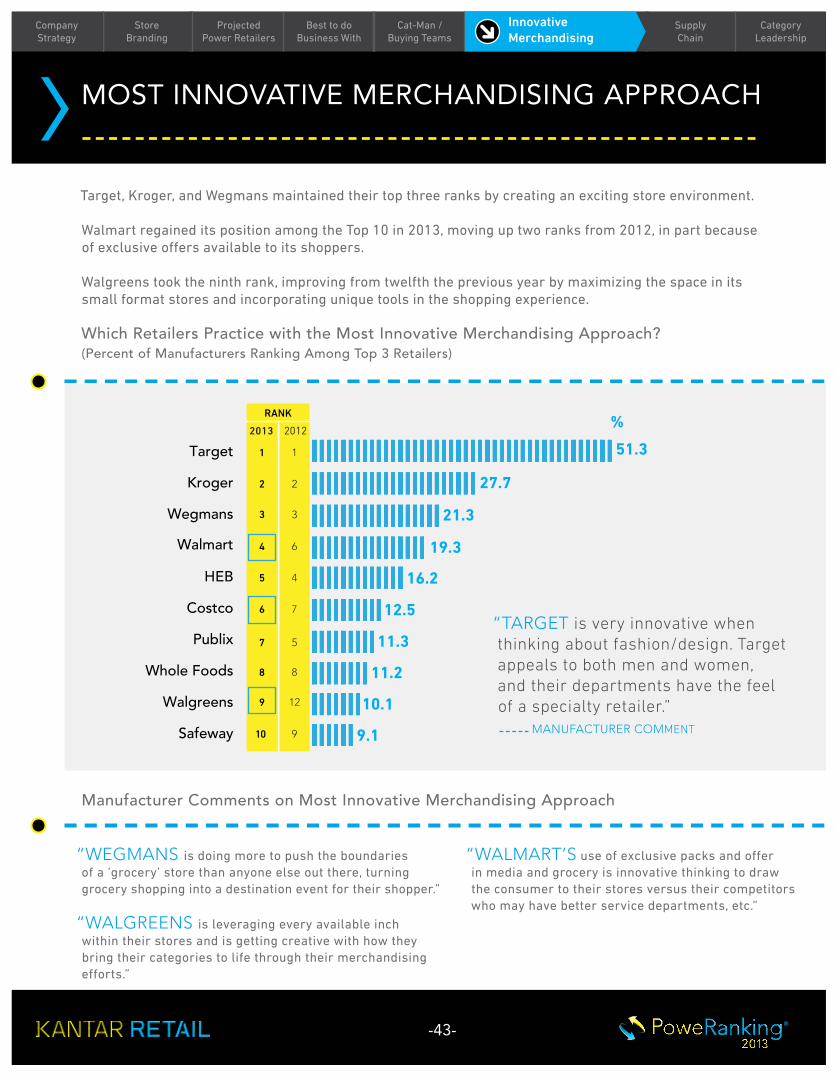

Which Retailers Practice with the Most Innovative Merchandising Approach? (Percent of Manufacturers Ranking Among Top 3 Retailers)

Target, Kroger, and Wegmans maintained their top three ranks by creating an exciting store environment.

Walmart regained its position among the Top 10 in 2013, moving up two ranks from 2012, in part because of exclusive offers available to its shoppers.

Walgreens took the ninth rank, improving from twelfth the previous year by maximizing the space in its small format stores and incorporating unique tools in the shopping experience.

Company Strategy

MOST INNOVATIVE MERCHANDISING APPROACH

Innovative Merchandising

-43-

Innovative Marketing/ Merch

SupplyChain

Category Leadership

®

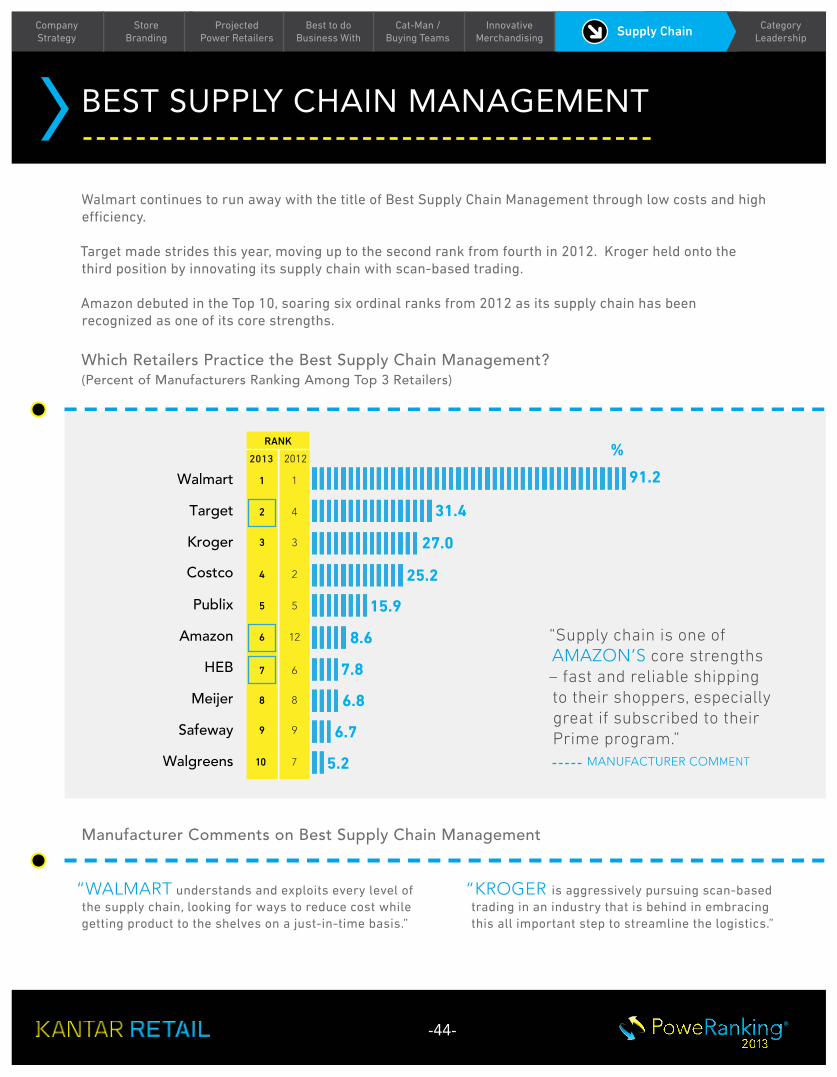

Manufacturer Comments on Best Supply Chain Management

“KROGER is aggressively pursuing scan-based trading in an industry that is behind in embracing this all important step to streamline the logistics.”

“WALMART understands and exploits every level of the supply chain, looking for ways to reduce cost while getting product to the shelves on a just-in-time basis.”

RANK

2013 2012

Walmart

Target

Kroger

Costco

Publix

Amazon

HEB

Meijer

Safeway

Walgreens

1

2

3

4

5

6

7

8

9

10

1

4

3

2

5

12

6

8

9

7

91.2

31.4

27.0

25.2

15.9

8.6

7.8

6.8

6.7

5.2

%

“Supply chain is one of AMAZON’S core strengths – fast and reliable shipping to their shoppers, especially great if subscribed to their Prime program.”

MANUFACTURER COMMENT

Which Retailers Practice the Best Supply Chain Management? (Percent of Manufacturers Ranking Among Top 3 Retailers)

Walmart continues to run away with the title of Best Supply Chain Management through low costs and high efficiency.

Target made strides this year, moving up to the second rank from fourth in 2012. Kroger held onto the third position by innovating its supply chain with scan-based trading.

Amazon debuted in the Top 10, soaring six ordinal ranks from 2012 as its supply chain has been recognized as one of its core strengths.

Company Strategy Supply Chain

BEST SUPPLY CHAIN MANAGEMENT

Store Branding

Projected Power Retailers

Cat-Man / Buying Teams

Innovative Merchandising

Best to do Business With

-44-

SupplyChain

Category Leadership

®

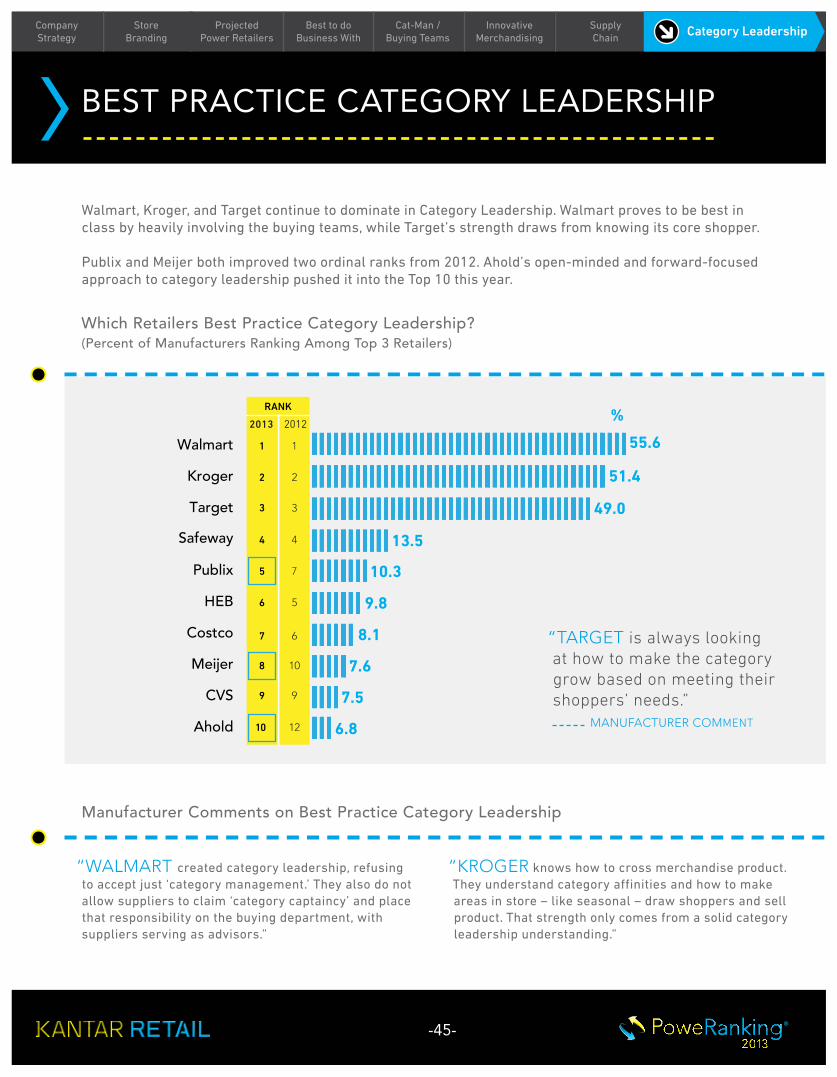

Manufacturer Comments on Best Practice Category Leadership

“KROGER knows how to cross merchandise product. They understand category affinities and how to make areas in store – like seasonal – draw shoppers and sell product. That strength only comes from a solid category leadership understanding.”

“WALMART created category leadership, refusing to accept just ‘category management.’ They also do not allow suppliers to claim ‘category captaincy’ and place that responsibility on the buying department, with suppliers serving as advisors.”

RANK

2013 2012

Walmart

Kroger

Target

Safeway

Publix

HEB

Costco

Meijer

CVS

Ahold

1

2

3

4

5

6

7

8

9

10

1

2

3

4

7

5

6

10

9

12

55.6

51.4

49.0

13.5

10.3

9.8

8.1

7.6

7.5

6.8

%

“TARGET is always looking at how to make the category grow based on meeting their shoppers’ needs.”

MANUFACTURER COMMENT

Which Retailers Best Practice Category Leadership? (Percent of Manufacturers Ranking Among Top 3 Retailers)

Walmart, Kroger, and Target continue to dominate in Category Leadership. Walmart proves to be best in class by heavily involving the buying teams, while Target’s strength draws from knowing its core shopper.

Publix and Meijer both improved two ordinal ranks from 2012. Ahold’s open-minded and forward-focused approach to category leadership pushed it into the Top 10 this year.

Company Strategy Category Leadership

BEST PRACTICE CATEGORY LEADERSHIP

Store Branding

Projected Power Retailers

Cat-Man / Buying Teams

Innovative Merchandising

Supply Chain

Best to do Business With

-45-

Store Branding

Company Strategy

Projected Power Retailers

Cat-Man / Buying Teams

Innovative Marketing/ Merch

SupplyChain

Category LeadershipCompany Strategy Best to do

Business With

®

Manufacturer Comments on Digital Marketing

“SAFEWAY’S ‘just for U’ platform is the most leading effort in this space for a brick and mortar retailer. They have the best connection between ad and in-store messaging and merchandising. They are fully behind the program at all levels.”

“TARGET is using digital, social, and mobile networking platforms to gather data on their shoppers that enable them to begin sending them communication or offers on items they are going to be shopping for before the shopper begins buying.”

RANK

2013 2012

Target

Walmart

Kroger

Safeway

Amazon

Walgreens

Ahold

CVS

Meijer

Publix

1

2

3

4

5

6

7

8

9

10

1

2

3

4

5

6

8

7

9

11

47.0

%

41.4

34.8

24.4

22.7

9.8

8.4

6.9

6.4

4.4

“Digital marketing is AMAZON’S DNA – consistently innovating in the space in terms of how shoppers interact with the site, their selected products and each other.”

MANUFACTURER COMMENT

Which Retailers are Making the Best Use of Digital, Mobile, and Social Networking Platforms in Their Joint Planning with You? (Percent of Manufacturers Ranking Among Top 3 Retailers)

The top six retailers maintained their ordinal ranks in 2013 for Digital Marketing. Safeway improved its score through seamless messaging in the ‘just for U’ platform.

Amazon was recognized by retailers for its continued innovation across multiple facets of its website.

Ahold and Publix each improved one ordinal rank, and Publix reappeared in the Top 10 for the Digital Marketing metric.

DIGITAL MARKETING

Note: This measure is not included in the Composite score.

-46-

®

ABOUT KANTAR RETAIL

THE BENEFITS TO OUR CLIENTS

Our mission at Kantar Retail is to drive tangible transformation in our clients’ businesses — significant, positive achievements that can be seen and measured. We integrate and align multiple marketing objectives, extend global practices and drive business growth. At this challenging time, these insights and actions are needed more than ever.

At Kantar Retail Our Approach to Business Drives Results:

Results range from creating the growth, vision and strategies for a company to (as specific as) testing a shelf redesign or training a single person.

KANTAR RETAIL CONDUCTS BENCHMARKING STUDIES ON THE FOLLOWING SUBJECTS

• PoweRanking® of Manufacturers and Retailers

• Category Leadership

• Trade Promotion Spending and Merchandising

• FoodservicElite® Ranking of Manufacturers and Operators

• Industry Shopper Study Across Retailers

CONSUMERINSIGHTS

CUSTOMERMANAGEMENT

RETAILMARKETING

BRANDBUILDING

SHOPPERINSIGHTS

OUR INSIGHT transforms perspectives.

OUR STRATEGIES transform propositions and organizations.

OUR EXECUTION transforms experiences and results.

Kantar Retail is WPP’s retail insights and consulting business. We offer a broad range of information and insights, capabilities and expertise, with a truly global reach.

WHO IS KANTAR RETAIL?

-1-

-47-