investment analysis picking the right projects - nyuadamodar/pdfiles/ovhds/inv.pdf · what is a...

TRANSCRIPT

Asw

ath Dam

odaran55

Picking the R

ight Projects:

Investment A

nalysis

Asw

ath Dam

odaran

Asw

ath Dam

odaran56

First P

rinciples

Invest in projects that yield a return greater than the minim

umacceptable hurdle rate.•

The hurdle rate should be higher for riskier projects and reflect the

financing mix used - ow

ners’ funds (equity) or borrowed m

oney(debt)

•R

eturns on projects should be measured based on cash flow

s generatedand the tim

ing of these cash flows; they should also consider both positive

and negative side effects of these projects.

Choose a financing m

ix that minim

izes the hurdle rate and matches the

assets being financed.

If there are not enough investments that earn the hurdle rate, return the

cash to stockholders.•

The form

of returns - dividends and stock buybacks - will depend upon

the stockholders’ characteristics.

Asw

ath Dam

odaran57

What is a investm

ent or a project?

Any decision that requires the use of resources (financial or otherw

ise)is a project.

Broad strategic decisions•

Entering new

areas of business

•E

ntering new m

arkets

•A

cquiring other companies

Tactical decisions

Managem

ent decisions•

The product m

ix to carry

•T

he level of inventory and credit terms

Decisions on delivering a needed service

•L

ease or buy a distribution system

•C

reating and delivering a managem

ent information system

Asw

ath Dam

odaran58

The notion of a benchm

ark

Since financial resources are finite, there is a hurdle that projects haveto cross before being deem

ed acceptable.

This hurdle w

ill be higher for riskier projects than for safer projects.

A sim

ple representation of the hurdle rate is as follows:

Hurdle rate =

R

iskless Rate +

Risk Prem

ium

The tw

o basic questions that every risk and return model in finance

tries to answer are:

•H

ow do you m

easure risk?

•H

ow do you translate this risk m

easure into a risk premium

?

Asw

ath Dam

odaran59

What is R

isk?

Risk, in traditional term

s, is viewed as a ‘negative’. W

ebster’sdictionary, for instance, defines risk as “exposing to danger or hazard”.T

he Chinese sym

bols for risk, reproduced below, give a m

uch betterdescription of risk

The first sym

bol is the symbol for “danger”, w

hile the second is thesym

bol for “opportunity”, making risk a m

ix of danger andopportunity.

Asw

ath Dam

odaran60

The C

apital Asset P

ricing Model

Uses variance as a m

easure of risk

Specifies that a portion of variance can be diversified away, and that is

only the non-diversifiable portion that is rewarded.

Measures the non-diversifiable risk w

ith beta, which is standardized

around one.

Translates beta into expected return -

Expected R

eturn = R

iskfree rate + B

eta * Risk Prem

ium

Works as w

ell as the next best alternative in most cases.

Asw

ath Dam

odaran61

The M

ean-Variance F

ramew

ork

The variance on any investm

ent measures the disparity betw

een actualand expected returns.

Expected R

eturn

Low

Variance Investm

ent

High V

ariance Investment

Asw

ath Dam

odaran62

The Im

portance of Diversification: R

isk Types

The risk (variance) on any individual investm

ent can be broken down

into two sources. Som

e of the risk is specific to the firm, and is called

firm-specific, w

hereas the rest of the risk is market w

ide and affects allinvestm

ents.

The risk faced by a firm

can be fall into the following categories –

•(1) Project-specific; an individual project m

ay have higher or lower cash

flows than expected.

•(2) C

ompetitive R

isk, which is that the earnings and cash flow

s on aproject can be affected by the actions of com

petitors.

•(3) Industry-specific R

isk, which covers factors that prim

arily impact the

earnings and cash flows of a specific industry.

•(4) International R

isk, arising from having som

e cash flows in currencies

other than the one in which the earnings are m

easured and stock is priced

•(5) M

arket risk, which reflects the effect on earnings and cash flow

s ofm

acro economic factors that essentially affect all com

panies

Asw

ath Dam

odaran63

The E

ffects of Diversification

Firm-specific risk can be reduced, if not elim

inated, by increasing thenum

ber of investments in your portfolio (i.e., by being diversified).

Market-w

ide risk cannot. This can be justified on either econom

ic orstatistical grounds.

On econom

ic grounds, diversifying and holding a larger portfolioelim

inates firm-specific risk for tw

o reasons-•

(a) Each investm

ent is a much sm

aller percentage of the portfolio, muting

the effect (positive or negative) on the overall portfolio.

•(b) Firm

-specific actions can be either positive or negative. In a largeportfolio, it is argued, these effects w

ill average out to zero. (For everyfirm

, where som

ething bad happens, there will be som

e other firm, w

heresom

ething good happens.)

Asw

ath Dam

odaran64

The R

ole of the Marginal Investor

The m

arginal investor in a firm is the investor w

ho is most likely to be

the buyer or seller on the next trade.

Generally speaking, the m

arginal investor in a stock has to own a lot of

stock and also trade a lot.

Since trading is required, the largest investor may not be the m

arginalinvestor, especially if he or she is a founder/m

anager of the firm(M

ichael Dell at D

ell Com

puters or Bill G

ates at Microsoft)

In all risk and return models in finance, w

e assume that the m

arginalinvestor is w

ell diversified.

Asw

ath Dam

odaran65

The M

arket Portfolio

Assum

ing diversification costs nothing (in terms of transactions costs),

and that all assets can be traded, the limit of diversification is to hold a

portfolio of every single asset in the economy (in proportion to m

arketvalue). T

his portfolio is called the market portfolio.

Individual investors will adjust for risk, by adjusting their allocations

to this market portfolio and a riskless asset (such as a T

-Bill)

Preferred risk level

Allocation decision

No risk

100% in T

-Bills

Some risk

50% in T

-Bills; 50%

in Market Portfolio;

A little m

ore risk25%

in T-B

ills; 75% in M

arket Portfolio

Even m

ore risk100%

in Market Portfolio

A risk hog..

Borrow

money; Invest in m

arket portfolio;

Every investor holds som

e combination of the risk free asset and the

market portfolio.

Asw

ath Dam

odaran66

The R

isk of an Individual Asset

The risk of any asset is the risk that it adds to the m

arket portfolio

Statistically, this risk can be measured by how

much an asset m

ovesw

ith the market (called the covariance)

Beta is a standardized m

easure of this covariance

Beta is a m

easure of the non-diversifiable risk for any asset can bem

easured by the covariance of its returns with returns on a m

arketindex, w

hich is defined to be the asset's beta.

The cost of equity w

ill be the required return,

Cost of E

quity = R

f + E

quity Beta * (E

(Rm ) - R

f )w

here,

Rf =

Riskfree rate

E(R

m ) = E

xpected Return on the M

arket Index

Asw

ath Dam

odaran67

Limitations of the C

AP

M

1. The m

odel makes unrealistic assum

ptions

2. The param

eters of the model cannot be estim

ated precisely- D

efinition of a market index

- Firm m

ay have changed during the 'estimation' period'

3. The m

odel does not work w

ell- If the m

odel is right, there should be a linear relationship betw

een returns and betas

the only variable that should explain returns is betas

- The reality is that

the relationship between betas and returns is w

eak

Other variables (size, price/book value) seem

to explain differences in returnsbetter.

Asw

ath Dam

odaran68

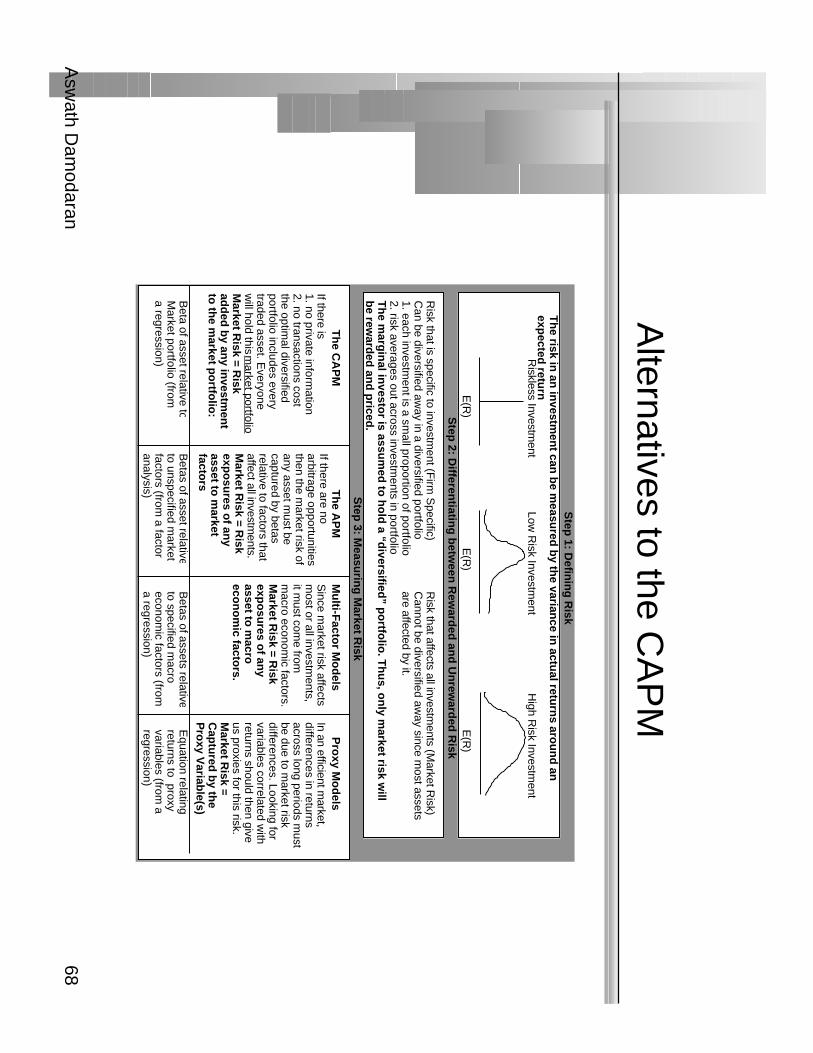

Alternatives to the C

AP

M

Th

e risk in an

investm

ent can

be m

easured

by th

e variance in

actual retu

rns aro

un

d an

exp

ected retu

rnE(R

)

Riskless Investm

entLow

Risk Investm

entH

igh Risk Investm

ent

E(R

)E

(R)

Risk that is specific to investm

ent (Firm

Specific)

Risk that affects all investm

ents (Market R

isk)C

an be diversified away in a diversified portfolio

Cannot be diversified aw

ay since most assets

1. each investment is a sm

all proportion of portfolioare affected by it.

2. risk averages out across investments in portfolio

Th

e marg

inal in

vestor is assu

med

to h

old

a “diversified

” po

rtfolio

. Th

us, o

nly m

arket risk will

be rew

arded

and

priced

.

Th

e CA

PM

Th

e AP

MM

ulti-F

actor M

od

elsP

roxy M

od

elsIf there is 1. no private inform

ation2. no transactions costthe optim

al diversified portfolio includes everytraded asset. E

veryonew

ill hold this market portfolio

Market R

isk = Risk

add

ed b

y any in

vestmen

t to

the m

arket po

rtfolio

:

If there are no arbitrage opportunities then the m

arket risk ofany asset m

ust be captured by betas relative to factors that affect all investm

ents.M

arket Risk = R

isk exp

osu

res of an

y asset to

market

factors

Beta of asset relative t o

Market portfolio (from

a regression)

Betas of asset relative

to unspecified market

factors (from a factor

analysis)

Since m

arket risk affectsm

ost or all investments,

it must com

e from

macro econom

ic factors.M

arket Risk = R

isk exp

osu

res of an

y asset to

macro

eco

no

mic facto

rs.

Betas of assets relativ e

to specified macro

economic factors (from

a regression)

In an efficient market,

differences in returnsacross long periods m

ustbe due to m

arket riskdifferences. Looking forvariables correlated w

ithreturns should then give us proxies for this risk.M

arket Risk =

Cap

tured

by th

e P

roxy V

ariable(s)

Equation relating

returns to proxy variables (from

aregression)

Step

1: Defin

ing

Risk

Step

2: Differen

tiating

betw

een R

eward

ed an

d U

nrew

arded

Risk

Step

3: Measu

ring

Market R

isk

Asw

ath Dam

odaran69

Identifying the Marginal Investor in your firm

…

Percent of Stock held by

Institutions

Percent of Stock held by

Insiders

Marginal Investor

High

Low

Institutional Investora

High

High

Institutional Investor, with

insider influence

Low

High (held by

founder/manager of firm

)

Insider (often undiversified)

Low

High (held by w

ealthy

individual investor)

Wealthy individual

investor, fairly diversified

Low

Low

Sm

all individual investor

with restricted

diversification

Asw

ath Dam

odaran70

Analyzing D

isney’s Stockholders

Percent of stock held by insiders = 1%

Percent of stock held by institutions = 62%

Who is the m

arginal investor in Disney?

Asw

ath Dam

odaran71

Application T

est: Who is the m

arginal investorin your firm

?

You can get inform

ation on insider and institutional holdings in your firmfrom

:

http://finance.yahoo.com/

Enter your com

pany’s symbol and choose profile.

Looking at the breakdow

n of stockholders in your firm, consider

whether the m

arginal investor isA

n institutional investor

An individual investor

An insider

Asw

ath Dam

odaran72

Inputs required to use the CA

PM

-

(a) the current risk-free rate

(b) the expected market risk prem

ium (the prem

ium expected for investing

in risky assets over the riskless asset)

(c) the beta of the asset being analyzed.

Asw

ath Dam

odaran73

The R

iskfree Rate and T

ime H

orizon

On a riskfree asset, the actual return is equal to the expected return.

Therefore, there is no variance around the expected return.

For an investment to be riskfree, i.e., to have an actual return be equal

to the expected return, two conditions have to be m

et –•

There has to be no default risk, w

hich generally implies that the security

has to be issued by the government. N

ote, however, that not all

governments can be view

ed as default free.

•T

here can be no uncertainty about reinvestment rates, w

hich implies that

it is a zero coupon security with the sam

e maturity as the cash flow

beinganalyzed.

Asw

ath Dam

odaran74

Riskfree R

ate in Practice

The riskfree rate is the rate on a zero coupon governm

ent bondm

atching the time horizon of the cash flow

being analyzed.

Theoretically, this translates into using different riskfree rates for each

cash flow - the 1 year zero coupon rate for the cash flow

in year 1, the2-year zero coupon rate for the cash flow

in year 2 ...

Practically speaking, if there is substantial uncertainty about expectedcash flow

s, the present value effect of using time varying riskfree rates

is small enough that it m

ay not be worth it.

Asw

ath Dam

odaran75

The B

ottom Line on R

iskfree Rates

Using a long term

government rate (even on a coupon bond) as the

riskfree rate on all of the cash flows in a long term

analysis will yield a

close approximation of the true value.

For short term analysis, it is entirely appropriate to use a short term

government security rate as the riskfree rate.

If the analysis is being done in real terms (rather than nom

inal terms)

use a real riskfree rate, which can be obtained in one of tw

o ways –

•from

an inflation-indexed government bond, if one exists

•set equal, approxim

ately, to the long term real grow

th rate of the economy

in which the valuation is being done.

Data Source: Y

ou can get riskfree rates for the US in a num

ber ofsites. T

ry http://ww

w.bloom

berg.com/m

arkets.

Asw

ath Dam

odaran76

Measurem

ent of the risk premium

The risk prem

ium is the prem

ium that investors dem

and for investingin an average risk investm

ent, relative to the riskfree rate.

As a general proposition, this prem

ium should be

•greater than zero

•increase w

ith the risk aversion of the investors in that market

•increase w

ith the riskiness of the “average” risk investment

Asw

ath Dam

odaran77

What is your risk prem

ium?

Assum

e that stocks are the only risky assets and that you are offered two

investment options:

•a riskless investm

ent (say a Governm

ent Security), on which you can m

ake 5%

•a m

utual fund of all stocks, on which the returns are uncertain

How

much of an expected return w

ould you demand to shift your m

oney from the

riskless asset to the mutual fund?

Less than 5%

Betw

een 5 - 7%

Betw

een 7 - 9%

Betw

een 9 - 11%

Betw

een 11- 13%

More than 13%

Check your prem

ium against the survey prem

ium on m

y web site.

Asw

ath Dam

odaran78

Risk A

version and Risk P

remium

s

If this were the capital m

arket line, the risk premium

would be a

weighted average of the risk prem

iums dem

anded by each and everyinvestor.

The w

eights will be determ

ined by the magnitude of w

ealth that eachinvestor has. T

hus, Warren B

ufffet’s risk aversion counts more

towards determ

ining the “equilibrium” prem

ium than yours’ and m

ine.

As investors becom

e more risk averse, you w

ould expect the“equilibrium

” premium

to increase.

Asw

ath Dam

odaran79

Risk P

remium

s do change..

Go back to the previous exam

ple. Assum

e now that you are m

aking thesam

e choice but that you are making it in the afterm

ath of a stockm

arket crash (it has dropped 25% in the last m

onth). Would you

change your answer?

I would dem

and a larger premium

I would dem

and a smaller prem

ium

I would dem

and the same prem

ium

Asw

ath Dam

odaran80

Estim

ating Risk P

remium

s in Practice

Survey investors on their desired risk premium

s and use the averageprem

ium from

these surveys.

Assum

e that the actual premium

delivered over long time periods is

equal to the expected premium

- i.e., use historical data

Estim

ate the implied prem

ium in today’s asset prices.

Asw

ath Dam

odaran81

The S

urvey Approach

Surveying all investors in a market place is im

practical.

How

ever, you can survey a few investors (especially the larger

investors) and use these results. In practice, this translates into surveysof m

oney managers’ expectations of expected returns on stocks over

the next year.

The lim

itations of this approach are:•

there are no constraints on reasonability (the survey could producenegative risk prem

iums or risk prem

iums of 50%

)

•they are extrem

ely volatile

•they tend to be short term

; even the longest surveys do not go beyond oneyear

Asw

ath Dam

odaran82

The H

istorical Prem

ium A

pproach

This is the default approach used by m

ost to arrive at the premium

touse in the m

odel

In most cases, this approach does the follow

ing•

it defines a time period for the estim

ation (1926-Present, 1962-Present....)

•it calculates average returns on a stock index during the period

•it calculates average returns on a riskless security over the period

•it calculates the difference betw

een the two

•and uses it as a prem

ium looking forw

ard

The lim

itations of this approach are:•

it assumes that the risk aversion of investors has not changed in a

systematic w

ay across time. (T

he risk aversion may change from

year toyear, but it reverts back to historical averages)

•it assum

es that the riskiness of the “risky” portfolio (stock index) has notchanged in a system

atic way across tim

e.

Asw

ath Dam

odaran83

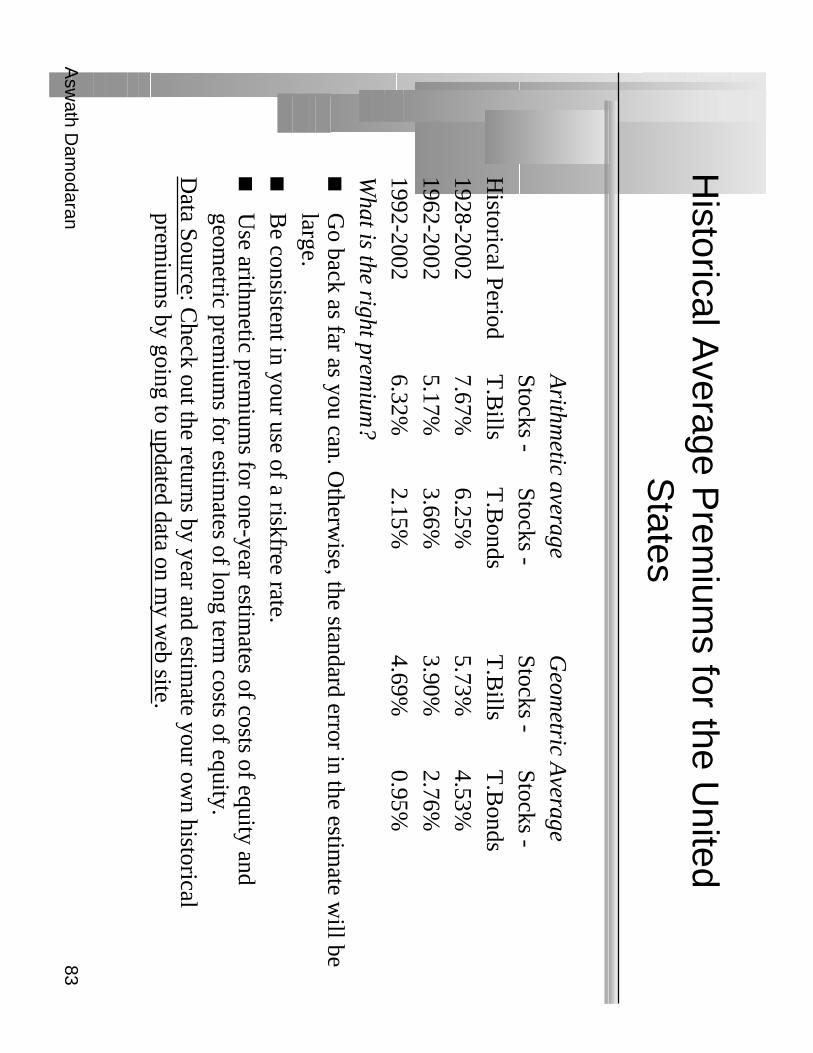

Historical A

verage Prem

iums for the U

nitedS

tates

Arithm

etic averageG

eometric A

verageStocks -

Stocks -Stocks -

Stocks -H

istorical PeriodT

.Bills

T.B

ondsT

.Bills

T.B

onds1928-2002

7.67%6.25%

5.73%4.53%

1962-20025.17%

3.66%3.90%

2.76%1992-2002

6.32%2.15%

4.69%0.95%

What is the right prem

ium?

Go back as far as you can. O

therwise, the standard error in the estim

ate will be

large.B

e consistent in your use of a riskfree rate.U

se arithmetic prem

iums for one-year estim

ates of costs of equity andgeom

etric premium

s for estimates of long term

costs of equity.D

ata Source: Check out the returns by year and estim

ate your own historical

premium

s by going to updated data on my w

eb site.

Asw

ath Dam

odaran84

What about historical prem

iums for other

markets?

Historical data for m

arkets outside the United States tends to be sketch

and unreliable.Ibbotson, for instance, estim

ates the following prem

iums for m

ajorm

arkets from 1970-1996

Country

Stock return B

ond Return

Equity R

isk Prem

iumA

ustralia8.47%

6.99%1.48%

France11.51%

9.17%2.34%

Germ

any11.30%

12.10%-0.80%

Italy5.49%

7.84%-2.35%

Japan15.73%

12.69%3.04%

Mexico

11.88%10.71%

1.17%Singapore

15.48%6.45%

9.03%Spain

8.22%7.91%

0.31%Sw

itzerland13.49%

10.11%3.38%

UK

12.42%7.81%

4.61%

Asw

ath Dam

odaran85

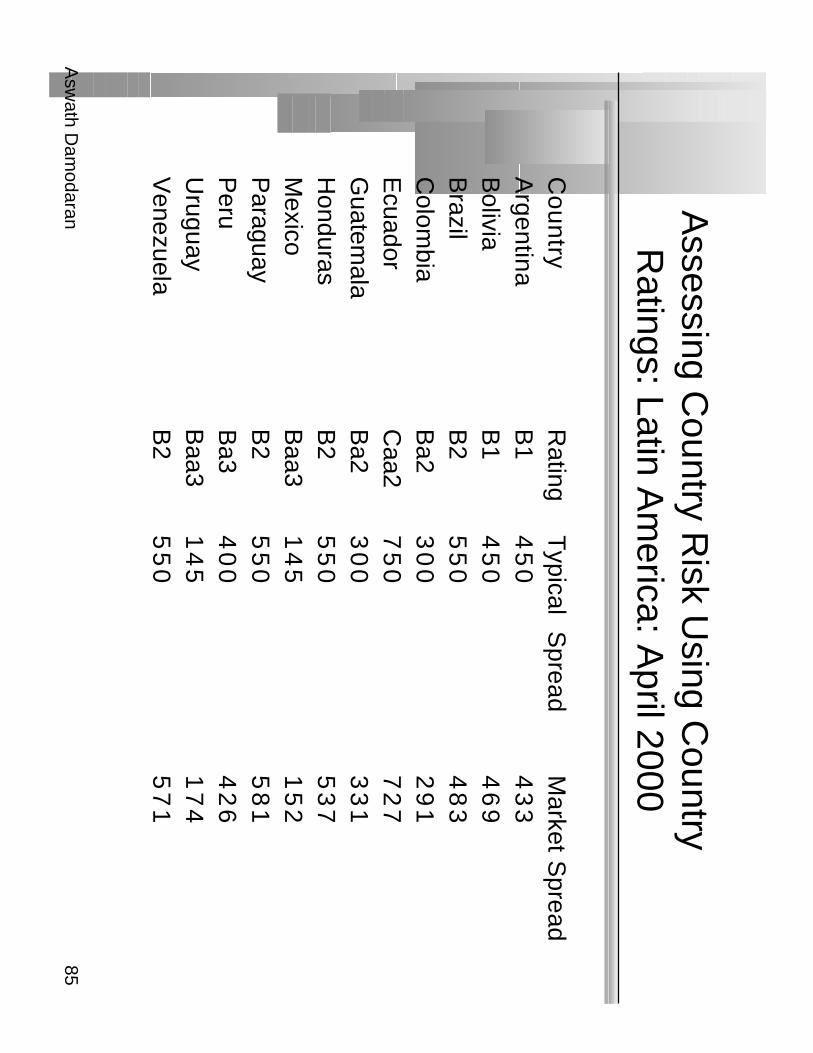

Assessing C

ountry Risk U

sing Country

Ratings: Latin A

merica: A

pril 2000

Co

un

tryR

atingT

ypical Spread

Market S

preadA

rgentina B

1 4

50

43

3B

olivia B

1 4

50

46

9B

razil B

2 5

50

48

3C

olombia

Ba2

30

02

91

Ecuador

Caa2

75

07

27

Guatem

ala B

a2 3

00

33

1H

onduras B

2 5

50

53

7M

exico B

aa3 1

45

15

2P

araguay B

2 5

50

58

1P

eru B

a3 4

00

42

6U

ruguay B

aa3 1

45

17

4V

enezuela B

2 5

50

57

1

Asw

ath Dam

odaran86

Using C

ountry Ratings to E

stimate E

quityS

preads

The sim

plest way of dealing w

ith country risk is to view the default spread as

the country equity risk premium

.C

ountry ratings measure default risk. W

hile default risk premium

s and equityrisk prem

iums are highly correlated, one w

ould expect equity spreads to behigher than debt spreads.

•O

ne way to adjust the country spread upw

ards is to use information from

the US

market. In the U

S, the equity risk premium

has been roughly twice the default

spread on junk bonds.•

Another is to m

ultiply the bond spread by the relative volatility of stock and bondprices in that m

arket. For example,

–Standard D

eviation in Bovespa (E

quity) = 30.64%

–Standard D

eviation in Brazil C

-Bond =

15.28%

–A

djusted Equity Spread =

4.83% (30.64%

/15.28%) =

9.69%

Data Source: C

heck out the latest ratings and country premium

s by going toupdated data on m

y web site.

Asw

ath Dam

odaran87

Implied E

quity Prem

iums

If we use a basic discounted cash flow

model, w

e can estimate the

implied risk prem

ium from

the current level of stock prices.

For instance, if stock prices are determined by the sim

ple Gordon

Grow

th Model:

•V

alue = E

xpected Dividends next year/ (R

equired Returns on Stocks -

Expected G

rowth R

ate)

•Plugging in the current level of the index, the dividends on the index andexpected grow

th rate will yield a “im

plied” expected return on stocks.Subtracting out the riskfree rate w

ill yield the implied prem

ium.

The problem

s with this approach are:

•the discounted cash flow

model used to value the stock index has to be the

right one.

•the inputs on dividends and expected grow

th have to be correct

•it im

plicitly assumes that the m

arket is currently correctly valued

Asw

ath Dam

odaran88

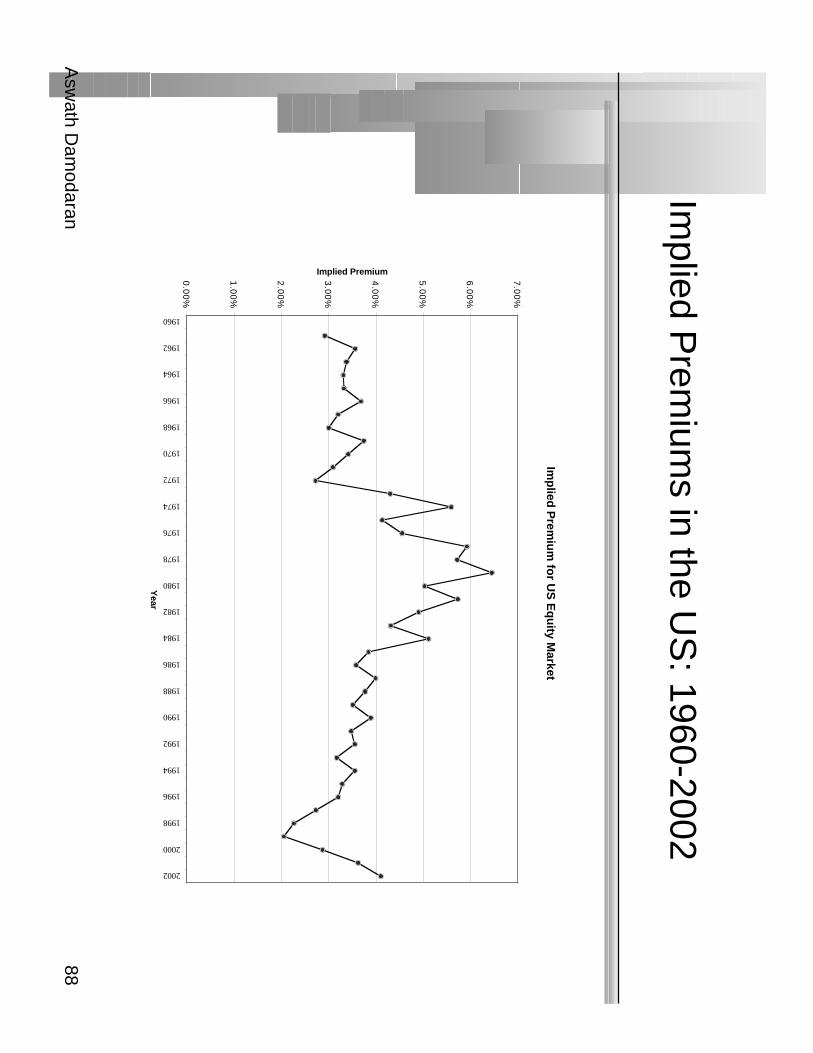

Implied P

remium

s in the US

: 1960-2002

Imp

lied P

remiu

m fo

r US

Eq

uity M

arket

0.0

0%

1.0

0%

2.0

0%

3.0

0%

4.0

0%

5.0

0%

6.0

0%

7.0

0%

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

Year

Implied Premium

Asw

ath Dam

odaran89

A

pplication Test: A

Market R

isk Prem

ium

Based upon our discussion of historical risk prem

iums so far, the risk

premium

looking forward should be:

About 7.5%

, which is w

hat the arithmetic average prem

ium has been

since 1981, for stocks over T.B

ills

About 4.5%

, which is the geom

etric average premium

since 1928, forstocks over T

.Bonds

About 4%

, which is the im

plied premium

in the stock market today

Asw

ath Dam

odaran90

Estim

ating Beta

The standard procedure for estim

ating betas is to regress stock returns(R

j ) against market returns (R

m ) -

Rj =

a + b R

m

•w

here a is the intercept and b is the slope of the regression.

The slope of the regression corresponds to the beta of the stock, and

measures the riskiness of the stock.

Asw

ath Dam

odaran91

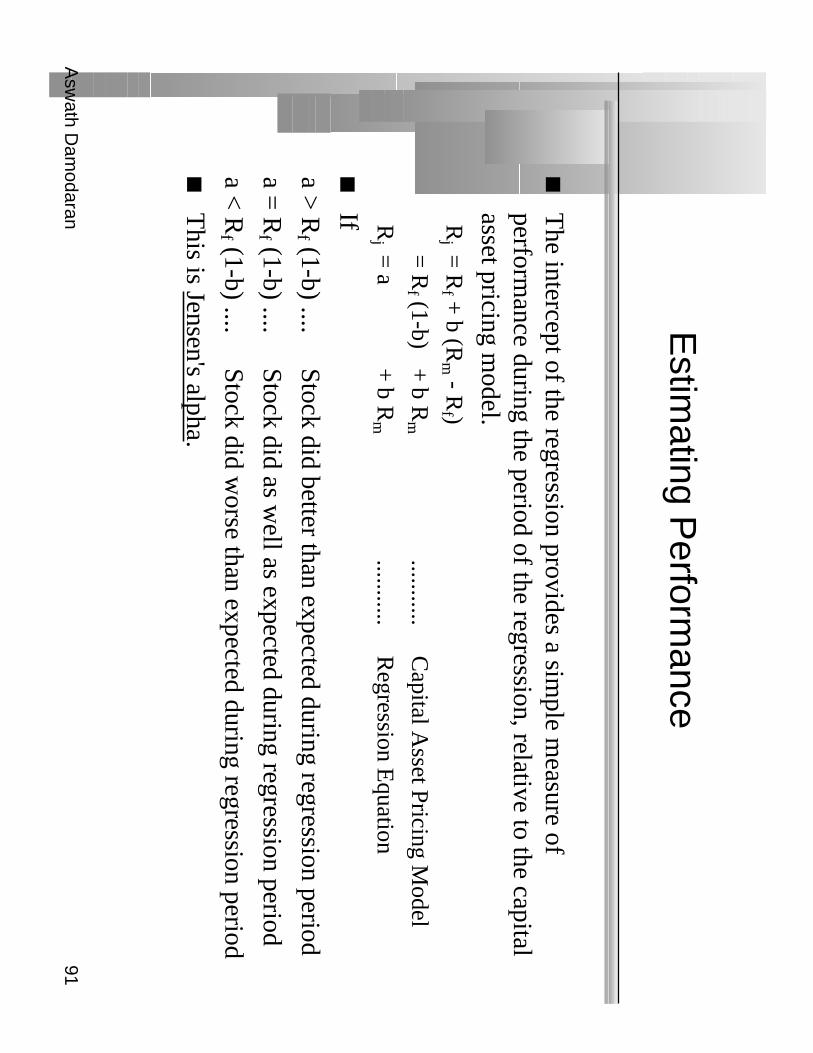

Estim

ating Perform

ance

The intercept of the regression provides a sim

ple measure of

performance during the period of the regression, relative to the capital

asset pricing model.

Rj =

Rf +

b (Rm - R

f )

= R

f (1-b) + b R

m...........

Capital A

sset Pricing Model

Rj =

a + b R

m...........

Regression E

quation

If

a > R

f (1-b) ....Stock did better than expected during regression period

a = R

f (1-b) ....Stock did as w

ell as expected during regression period

a < R

f (1-b) ....Stock did w

orse than expected during regression period

This is Jensen's alpha.

Asw

ath Dam

odaran92

Firm

Specific and M

arket Risk

The R

squared (R2) of the regression provides an estim

ate of theproportion of the risk (variance) of a firm

that can be attributed tom

arket risk;

The balance (1 - R

2) can be attributed to firm specific risk.

Asw

ath Dam

odaran93

Setting up for the E

stimation

Decide on an estim

ation period•

Services use periods ranging from 2 to 5 years for the regression

•L

onger estimation period provides m

ore data, but firms change.

•Shorter periods can be affected m

ore easily by significant firm-specific

event that occurred during the period (Exam

ple: ITT

for 1995-1997)

Decide on a return interval - daily, w

eekly, monthly

•Shorter intervals yield m

ore observations, but suffer from m

ore noise.

•N

oise is created by stocks not trading and biases all betas towards one.

Estim

ate returns (including dividends) on stock•

Return =

(PriceE

nd - PriceB

eginning + D

ividendsPeriod )/ Price

Beginning

•Included dividends only in ex-dividend m

onth

Choose a m

arket index, and estimate returns (inclusive of dividends)

on the index for each interval for the period.

Asw

ath Dam

odaran94

Choosing the P

arameters: D

isney

Period used: 5 years

Return Interval =

Monthly

Market Index: S&

P 500 Index.

For instance, to calculate returns on Disney in A

pril 1992,•

Price for Disney at end of M

arch = $ 37.87

•Price for D

isney at end of April =

$ 36.42

•D

ividends during month =

$0.05 (It was an ex-dividend m

onth)

•R

eturn =($36.42 - $ 37.87 +

$ 0.05)/$ 37.87=-3.69%

To estim

ate returns on the index in the same m

onth•

Index level (including dividends) at end of March =

404.35

•Index level (including dividends) at end of A

pril = 415.53

•R

eturn =(415.53 - 404.35)/ 404.35 =

2.76%

Asw

ath Dam

odaran95

Disney’s H

istorical Beta

Disn

ey versus S

&P

500: 1992-1996

-6.0

0%

-4.0

0%

-2.0

0%

0.0

0%

2.0

0%

4.0

0%

6.0

0%

8.0

0%

-15

.00

%-1

0.0

0%

-5.0

0%

0.0

0%

5.0

0%

10

.00

%1

5.0

0%

20

.00

%

Asw

ath Dam

odaran96

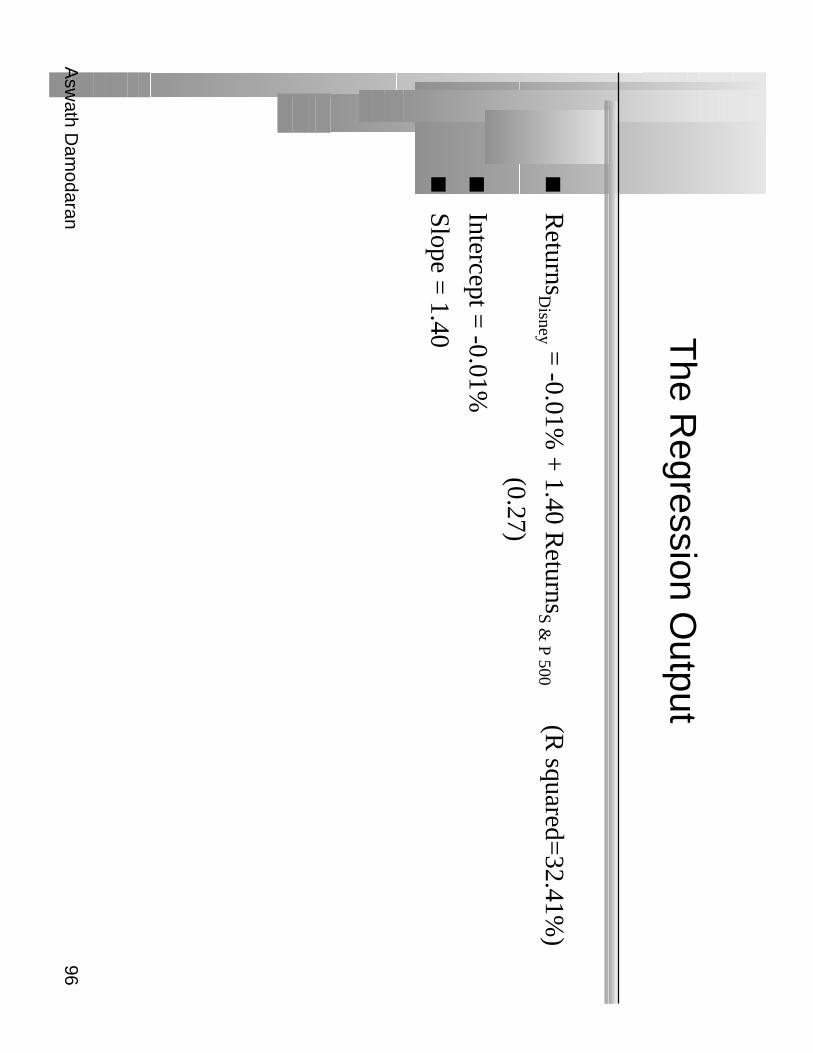

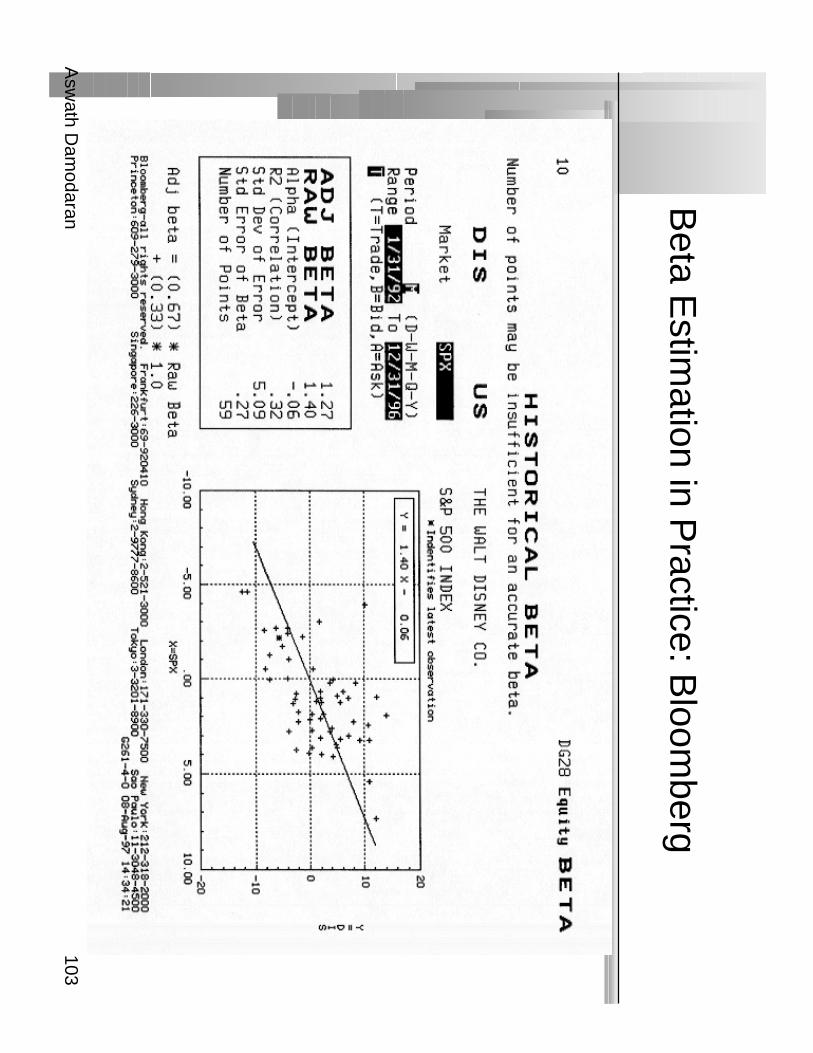

The R

egression Output

Returns

Disney =

-0.01% +

1.40 Returns

S & P 500 (R

squared=32.41%

)

(0.27)

Intercept = -0.01%

Slope = 1.40

Asw

ath Dam

odaran97

Analyzing D

isney’s Perform

ance

Intercept = -0.01%

•T

his is an intercept based on monthly returns. T

hus, it has to be compared

to a monthly riskfree rate.

•B

etween 1992 and 1996,

–M

onthly Riskfree R

ate = 0.4%

(Annual T

.Bill rate divided by 12)

–R

iskfree Rate (1-B

eta) = 0.4%

(1-1.40) = -.16%

The C

omparison is then betw

eenIntercept

versusR

iskfree Rate (1 - B

eta)-0.01%

versus0.4%

(1-1.40)=-0.16%

•Jensen’s A

lpha = -0.01%

-(-0.16%) =

0.15%

Disney did 0.15%

better than expected, per month, betw

een 1992 and1996.•

Annualized, D

isney’s annual excess return = (1.0015) 12-1=

1.81%

Asw

ath Dam

odaran98

More on Jensen’s A

lpha

If you did this analysis on every stock listed on an exchange, what w

ouldthe average Jensen’s alpha be across all stocks?

Depend upon w

hether the market w

ent up or down during the period

Should be zero

Should be greater than zero, because stocks tend to go up more often

than down

Asw

ath Dam

odaran99

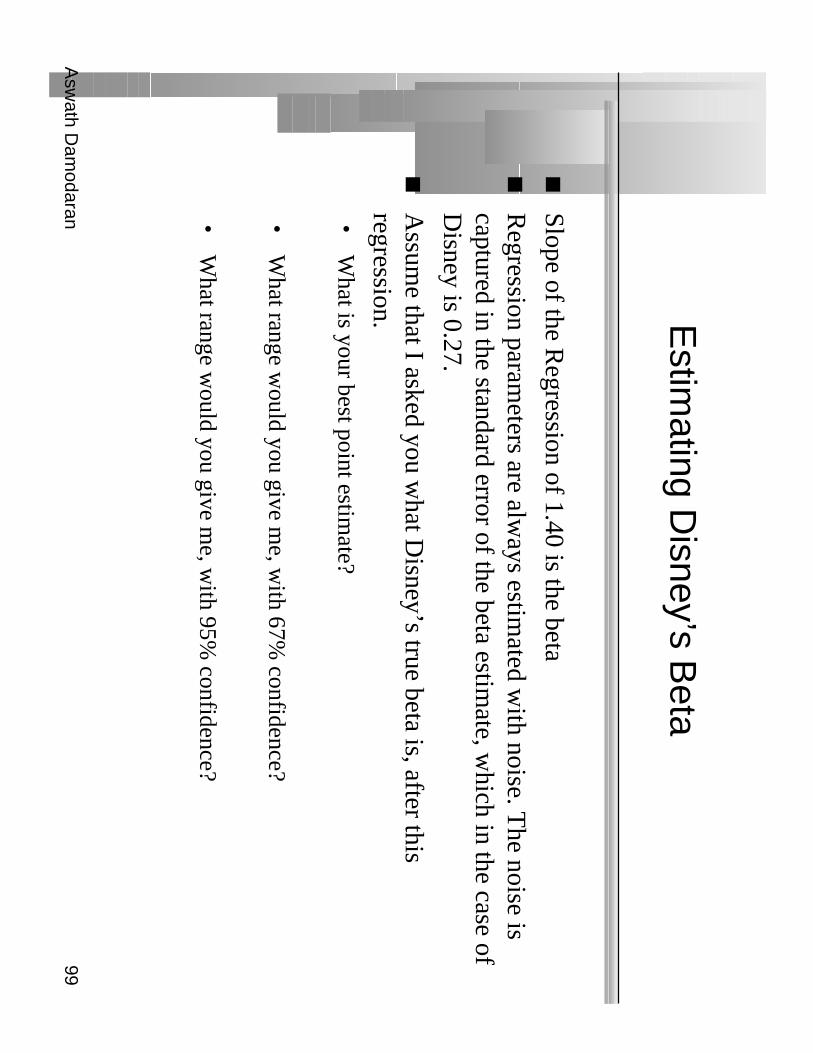

Estim

ating Disney’s B

eta

Slope of the Regression of 1.40 is the beta

Regression param

eters are always estim

ated with noise. T

he noise iscaptured in the standard error of the beta estim

ate, which in the case of

Disney is 0.27.

Assum

e that I asked you what D

isney’s true beta is, after thisregression.•

What is your best point estim

ate?

•W

hat range would you give m

e, with 67%

confidence?

•W

hat range would you give m

e, with 95%

confidence?

Asw

ath Dam

odaran100

The D

irty Secret of “S

tandard Error”

Distrib

utio

n o

f Stan

dard

Erro

rs: Beta E

stimates fo

r U.S

. stocks

0

20

0

40

0

60

0

80

0

10

00

12

00

14

00

16

00

<.1

0.10 - .20

.20 - .30.30 - .40

.40 -.50.50 - .75

> .75

Stan

dard

Erro

r in B

eta Estim

ate

Number of Firms

Asw

ath Dam

odaran101

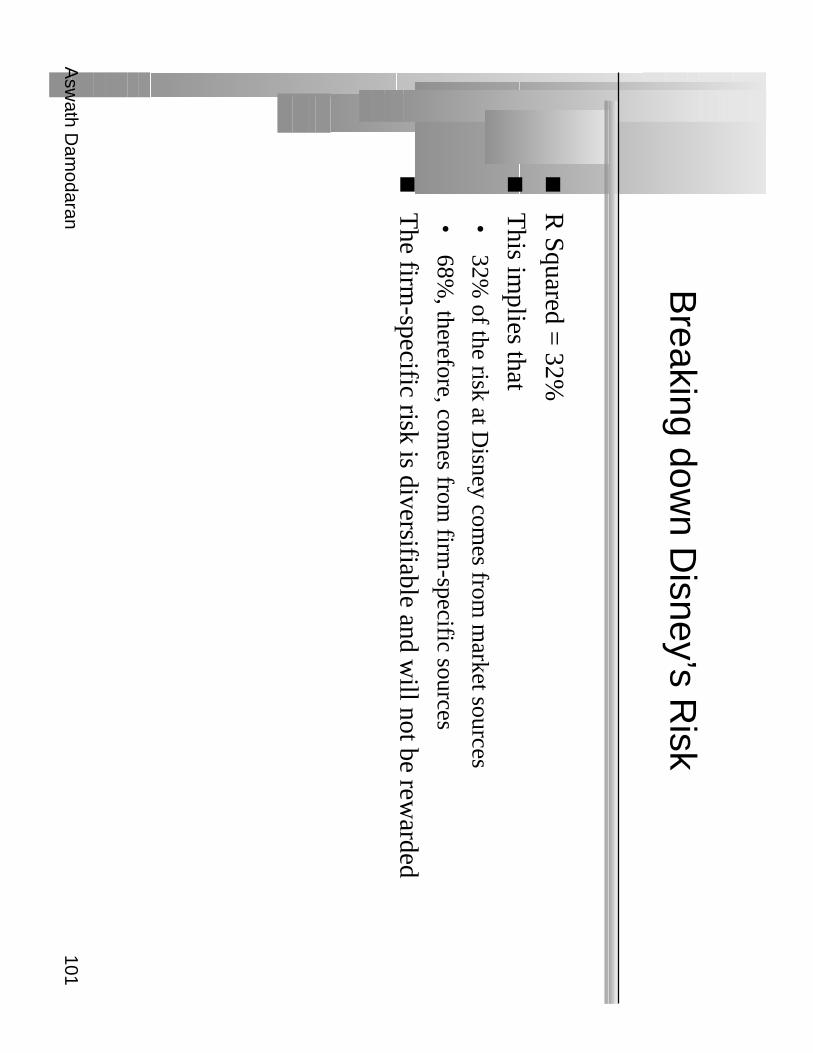

Breaking dow

n Disney’s R

isk

R Squared =

32%

This im

plies that•

32% of the risk at D

isney comes from

market sources

•68%

, therefore, comes from

firm-specific sources

The firm

-specific risk is diversifiable and will not be rew

arded

Asw

ath Dam

odaran102

The R

elevance of R S

quared

You are a diversified investor trying to decide w

hether you should investin D

isney or Am

gen. They both have betas of 140, but D

isney has anR

Squared of 32% w

hile Am

gen’s R squared of only 15%

. Which one

would you invest in?

Am

gen, because it has the lower R

squared

Disney, because it has the higher R

squared

You w

ould be indifferent

Would your answ

er be different if you were an undiversified investor?

Asw

ath Dam

odaran103

Beta E

stimation in P

ractice: Bloom

berg

Asw

ath Dam

odaran104

Estim

ating Expected R

eturns: Septem

ber 30,1997

Inputs to the expected return calculation•

Disney’s B

eta = 1.40

•R

iskfree Rate =

7.00% (L

ong term G

overnment B

ond rate)

•R

isk Premium

= 5.50%

(Approxim

ate historical premium

)

Expected R

eturn = R

iskfree Rate +

Beta (R

isk Premium

)

= 7.00%

+ 1.40 (5.50%

) = 14.70%

Asw

ath Dam

odaran105

Use to a P

otential Investor in Disney

As a potential investor in D

isney, what does this expected return of

14.70% tell you?

This is the return that I can expect to m

ake in the long term on D

isney,if the stock is correctly priced and the C

APM

is the right model for

risk,

This is the return that I need to m

ake on Disney in the long term

tobreak even on m

y investment in the stock

Both

Assum

e now that you are an active investor and that your research

suggests that an investment in D

isney will yield 25%

a year for thenext 5 years. B

ased upon the expected return of 14.70%, you w

ould

Buy the stock

Sell the stock

Asw

ath Dam

odaran106

How

managers use this expected return

Managers at D

isney•

need to make at least 14.70%

as a return for their equity investors to breakeven.

•this is the hurdle rate for projects, w

hen the investment is analyzed from

an equity standpoint

In other words, D

isney’s cost of equity is 14.70%.

What is the cost of not delivering this cost of equity?

Asw

ath Dam

odaran107

A

pplication Test: A

nalyzing the Risk

Regression

Using your B

loomberg risk and return print out, answ

er the following

questions:•

How

well or badly did your stock do, relative to the m

arket, during theperiod of the regression? (Y

ou can assume an annualized riskfree rate of

4.8% during the regression period)

Intercept - 0.4% (1- B

eta) = Jensen’s A

lpha

•W

hat proportion of the risk in your stock is attributable to the market?

What proportion is firm

-specific?

•W

hat is the historical estimate of beta for your stock? W

hat is the rangeon this estim

ate with 67%

probability? With 95%

probability?

•B

ased upon this beta, what is your estim

ate of the required return on thisstock?

Riskless R

ate + B

eta * Risk Prem

ium

Asw

ath Dam

odaran108

A Q

uick Test

You are advising a very risky softw

are firm on the right cost of equity to

use in project analysis. You estim

ate a beta of 2.0 for the firm and

come up w

ith a cost of equity of 18%. T

he CFO

of the firm is

concerned about the high cost of equity and wants to know

whether

there is anything he can do to lower his beta.

How

do you bring your beta down?

Should you focus your attention on bringing your beta down?

Yes

No

Asw

ath Dam

odaran109

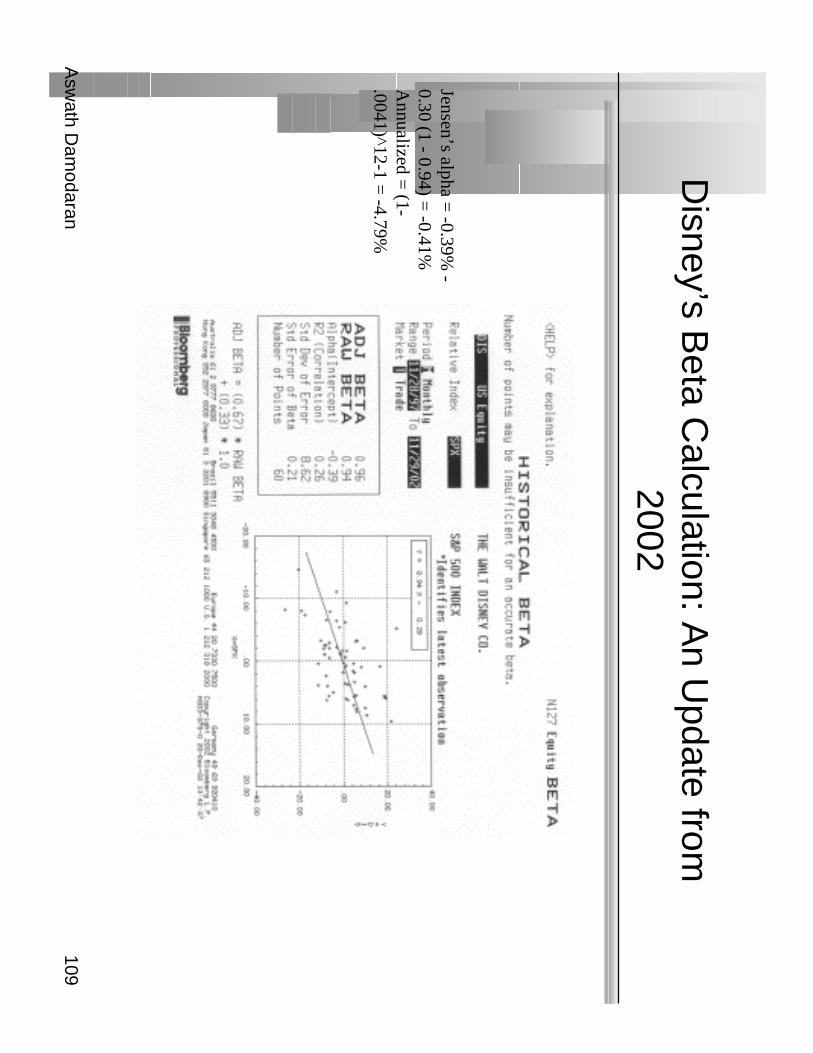

Disney’s B

eta Calculation: A

n Update from

2002

Jensen’s alpha = -0.39%

-0.30 (1 - 0.94) =

-0.41%A

nnualized = (1-

.0041)^12-1 = -4.79%

Asw

ath Dam

odaran110

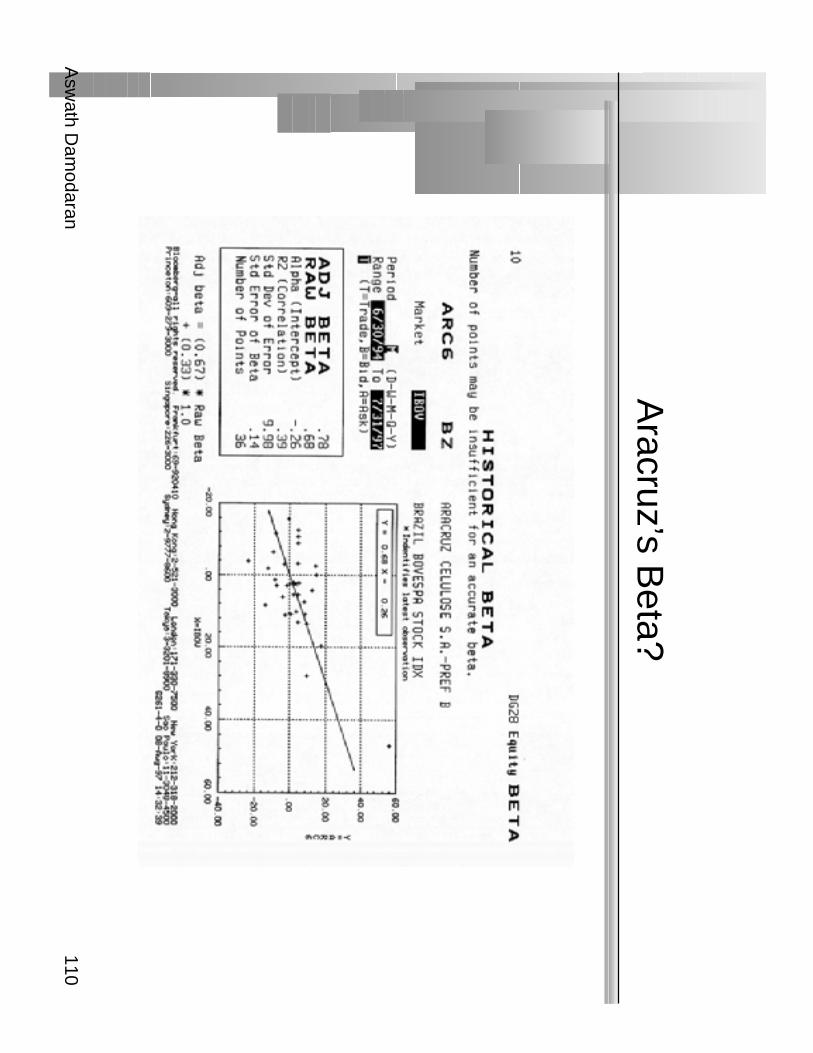

Aracruz’s B

eta?

Asw

ath Dam

odaran111

Telebras: H

igh R S

quared?

Asw

ath Dam

odaran112

A F

ew Q

uestions

The R

squared for Telebras is very high (70%

), at least relative to U.S.

firms. W

hy is that?

The beta for T

elebras is 1.11.•

Is this an appropriate measure of risk?

•If not, w

hy not?

The beta for every other stock in the index is also m

isestimated. Is

there a way to get a better estim

ate?

Asw

ath Dam

odaran113

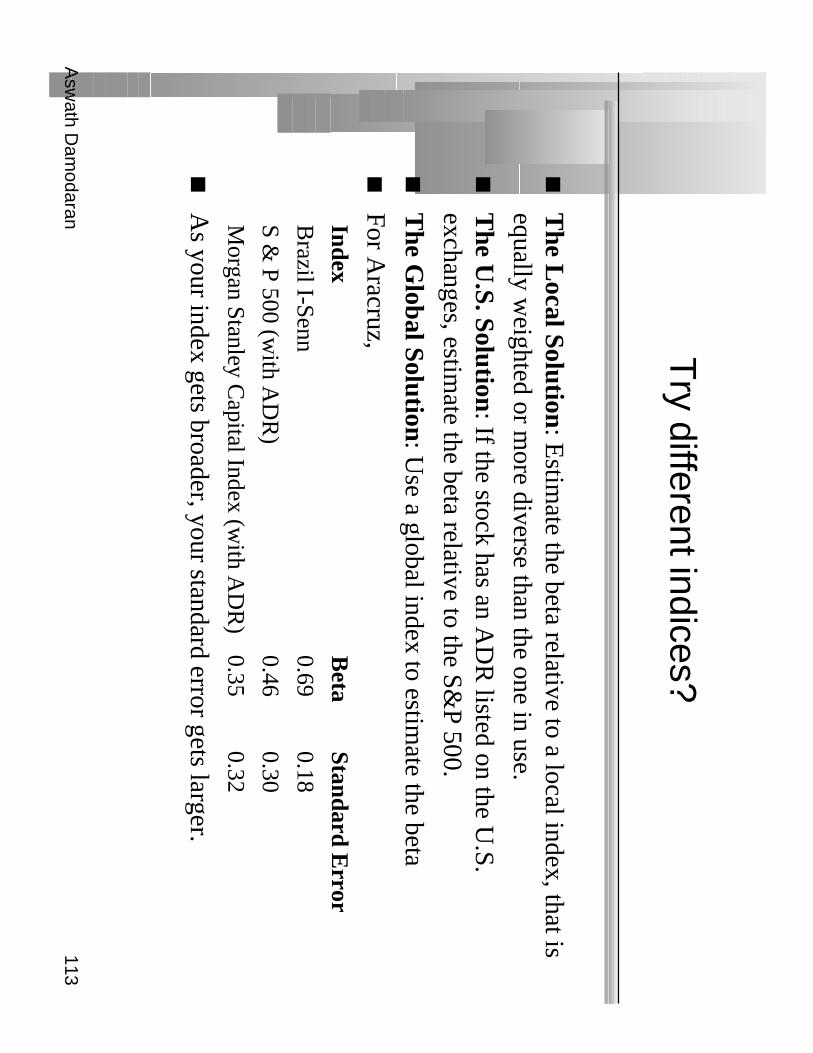

Try different indices?

The L

ocal Solution: E

stimate the beta relative to a local index, that is

equally weighted or m

ore diverse than the one in use.

The U

.S. Solution: If the stock has an A

DR

listed on the U.S.

exchanges, estimate the beta relative to the S&

P 500.

The G

lobal Solution: Use a global index to estim

ate the beta

For Aracruz,

IndexB

etaStandard E

rrorB

razil I-Senn0.69

0.18

S & P 500 (w

ith AD

R)

0.460.30

Morgan Stanley C

apital Index (with A

DR

)0.35

0.32

As your index gets broader, your standard error gets larger.

Asw

ath Dam

odaran114

Beta: E

xploring Fundam

entals

Beta =

1

Beta >

1

Beta =

0

Beta <

1

Real N

etworks: 3.2 4

Qw

est Com

munications: 2.60

General E

lectric: 1.10

Microsoft: 1..2 5

Philip M

orris: 0.65

Exxon M

obil: 0.40

Barrick (G

old Mines): - 0.10

Enron: 0.95

Asw

ath Dam

odaran115

Determ

inant 1: Product T

ype

Industry Effects: T

he beta value for a firm depends upon the

sensitivity of the demand for its products and services and of its costs

to macroeconom

ic factors that affect the overall market.

•C

yclical companies have higher betas than non-cyclical firm

s

•Firm

s which sell m

ore discretionary products will have higher betas than

firms that sell less discretionary products

Asw

ath Dam

odaran116

A S

imple T

est

Consider an investm

ent in Tiffany’s. W

hat kind of beta do you think thisinvestm

ent will have?

Much higher than one

Close to one

Much low

er than one

Asw

ath Dam

odaran117

Determ

inant 2: Operating Leverage E

ffects

Operating leverage refers to the proportion of the total costs of the firm

that are fixed.

Other things rem

aining equal, higher operating leverage results ingreater earnings variability w

hich in turn results in higher betas.

Asw

ath Dam

odaran118

Measures of O

perating Leverage

Fixed Costs M

easure = Fixed C

osts / Variable C

osts

This m

easures the relationship between fixed and variable costs. T

hehigher the proportion, the higher the operating leverage.

EB

IT V

ariability Measure =

% C

hange in EB

IT / %

Change in R

evenues

This m

easures how quickly the earnings before interest and taxes

changes as revenue changes. The higher this num

ber, the greater theoperating leverage.

Asw

ath Dam

odaran119

A Look at D

isney’s Operating Leverage

Year

Net Sales

% C

hange

in Sales

EB

IT%

Change

in EB

IT

19872877

756

19883438

19.50%848

12.17%

19894594

33.62%1177

38.80%

19905844

27.21%1368

16.23%

19916182

5.78%1124

-17.84%

19927504

21.38%1429

27.14%

19938529

13.66%1232

-13.79%

199410055

17.89%1933

56.90%

199512112

20.46%2295

18.73%

199618739

54.71%2540

10.68%

Average

23.80%16.56%

Asw

ath Dam

odaran120

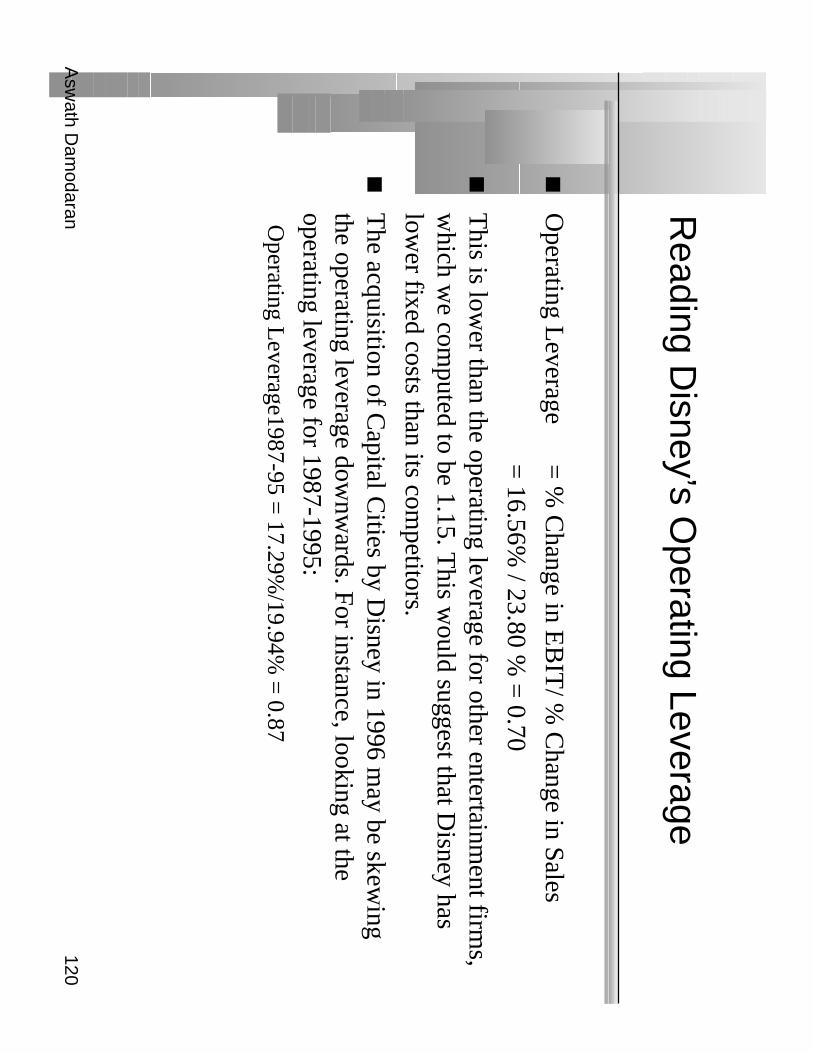

Reading D

isney’s Operating Leverage

Operating L

everage =

% C

hange in EB

IT/ %

Change in Sales

= 16.56%

/ 23.80 % =

0.70

This is low

er than the operating leverage for other entertainment firm

s,w

hich we com

puted to be 1.15. This w

ould suggest that Disney has

lower fixed costs than its com

petitors.

The acquisition of C

apital Cities by D

isney in 1996 may be skew

ingthe operating leverage dow

nwards. For instance, looking at the

operating leverage for 1987-1995:O

perating Leverage1987-95 =

17.29%/19.94%

= 0.87

Asw

ath Dam

odaran121

A T

est

Assum

e that you are comparing a E

uropean automobile m

anufacturingfirm

with a U

.S. automobile firm

. European firm

s are generally much

more constrained in term

s of laying off employees, if they get into

financial trouble. What im

plications does this have for betas, if theyare estim

ated relative to a comm

on index?

European firm

s will have m

uch higher betas than U.S. firm

s

European firm

s will have sim

ilar betas to U.S. firm

s

European firm

s will have m

uch lower betas than U

.S. firms

Asw

ath Dam

odaran122

Determ

inant 3: Financial Leverage

As firm

s borrow, they create fixed costs (interest paym

ents) that make

their earnings to equity investors more volatile.

This increased earnings volatility w

hich increases the equity beta

Asw

ath Dam

odaran123

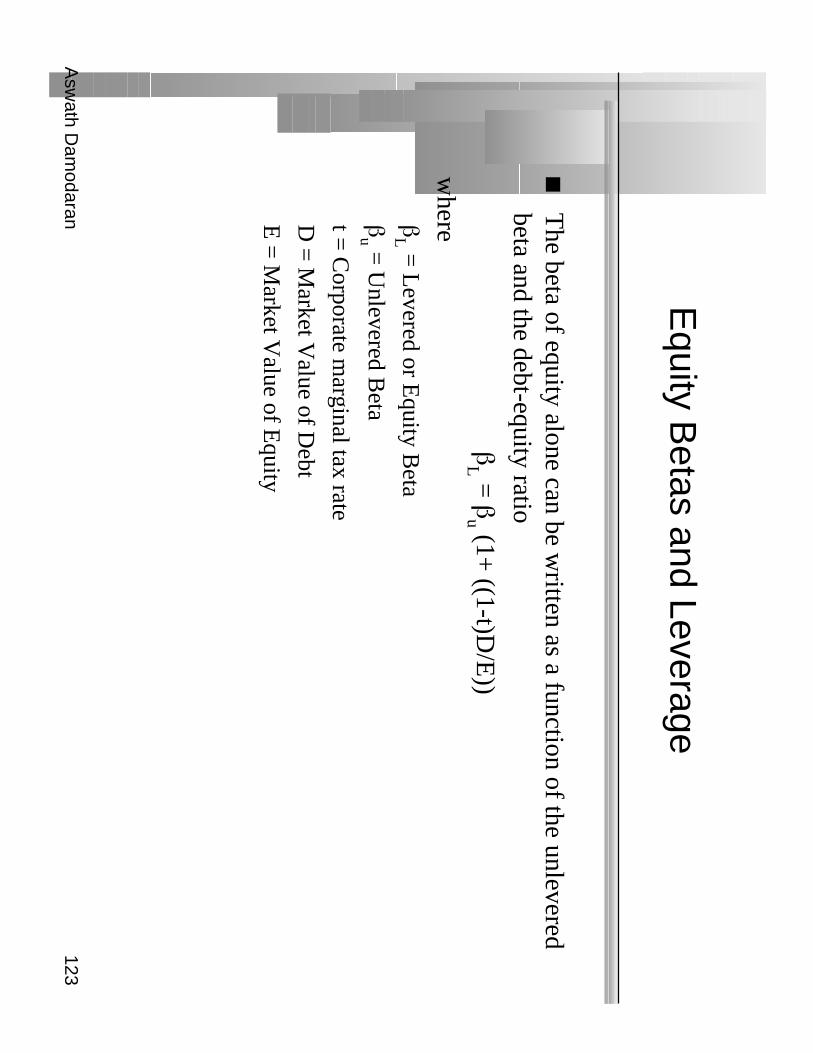

Equity B

etas and Leverage

The beta of equity alone can be w

ritten as a function of the unleveredbeta and the debt-equity ratio

βL =

βu (1+

((1-t)D/E

))

whereβ

L = L

evered or Equity B

eta

βu =

Unlevered B

eta

t = C

orporate marginal tax rate

D =

Market V

alue of Debt

E =

Market V

alue of Equity

Asw

ath Dam

odaran124

Effects of leverage on betas: D

isney

The regression beta for D

isney is 1.40. This beta is a levered beta

(because it is based on stock prices, which reflect leverage) and the

leverage implicit in the beta estim

ate is the average market debt equity

ratio during the period of the regression (1992 to 1996)

The average debt equity ratio during this period w

as 14%.

The unlevered beta for D

isney can then be estimated:(using a m

arginaltax rate of 36%

)=

Current B

eta / (1 + (1 - tax rate) (A

verage Debt/E

quity))

= 1.40 / ( 1 +

(1 - 0.36) (0.14)) = 1.28

Asw

ath Dam

odaran125

Disney : B

eta and Leverage

Debt to C

apitalD

ebt/Equity R

atioB

etaE

ffect of Leverage

0.00%0.00%

1.280.00

10.00%11.11%

1.380.09

20.00%25.00%

1.490.21

30.00%42.86%

1.640.35

40.00%66.67%

1.830.55

50.00%100.00%

2.110.82

60.00%150.00%

2.521.23

70.00%233.33%

3.201.92

80.00%400.00%

4.573.29

90.00%900.00%

8.697.40

Asw

ath Dam

odaran126

Betas are w

eighted Averages

The beta of a portfolio is alw

ays the market-value w

eighted average ofthe betas of the individual investm

ents in that portfolio.

Thus,•

the beta of a mutual fund is the w

eighted average of the betas of the stocksand other investm

ent in that portfolio

•the beta of a firm

after a merger is the m

arket-value weighted average of

the betas of the companies involved in the m

erger.

Asw

ath Dam

odaran127

The D

isney/Cap C

ities Merger: P

re-Merger

Disney:

Beta =

1.15

Debt =

$ 3,186 million

Equity =

$ 31,100 million

Firm =

$34,286

D/E

= 0.10

AB

C:Beta =

0.95

Debt =

$ 615 million

Equity =

$ 18,500 million

Firm=

$ 19,115

D/E

= 0.03

Asw

ath Dam

odaran128

Disney C

ap Cities B

eta Estim

ation: Step 1

Calculate the unlevered betas for both firm

s•

Disney’s unlevered beta =

1.15/(1+0.64*0.10) =

1.08

•C

ap Cities unlevered beta =

0.95/(1+0.64*0.03) =

0.93

Calculate the unlevered beta for the com

bined firm•

Unlevered B

eta for combined firm

= 1.08 (34286/53401) +

0.93 (19115/53401)

= 1.026

[Rem

ember to calculate the w

eights using the firm values of the tw

o firms]

Asw

ath Dam

odaran129

Disney C

ap Cities B

eta Estim

ation: Step 2

If Disney had used all equity to buy C

ap Cities

•D

ebt = $ 615 +

$ 3,186 = $ 3,801 m

illion

•E

quity = $ 18,500 +

$ 31,100 = $ 49,600

•D

/E R

atio = 3,801/49600 =

7.66%

•N

ew B

eta = 1.026 (1 +

0.64 (.0766)) = 1.08

Since Disney borrow

ed $ 10 billion to buy Cap C

ities/AB

C•

Debt =

$ 615 + $ 3,186 +

$ 10,000 = $ 13,801 m

illion

•E

quity = $ 39,600

•D

/E R

atio = 13,801/39600 =

34.82%

•N

ew B

eta = 1.026 (1 +

0.64 (.3482)) = 1.25

Asw

ath Dam

odaran130

Firm

Betas versus divisional B

etas

Firm B

etas as weighted averages: T

he beta of a firm is the w

eightedaverage of the betas of its individual projects.

At a broader level of aggregation, the beta of a firm

is the weighted

average of the betas of its individual division.

Asw

ath Dam

odaran131

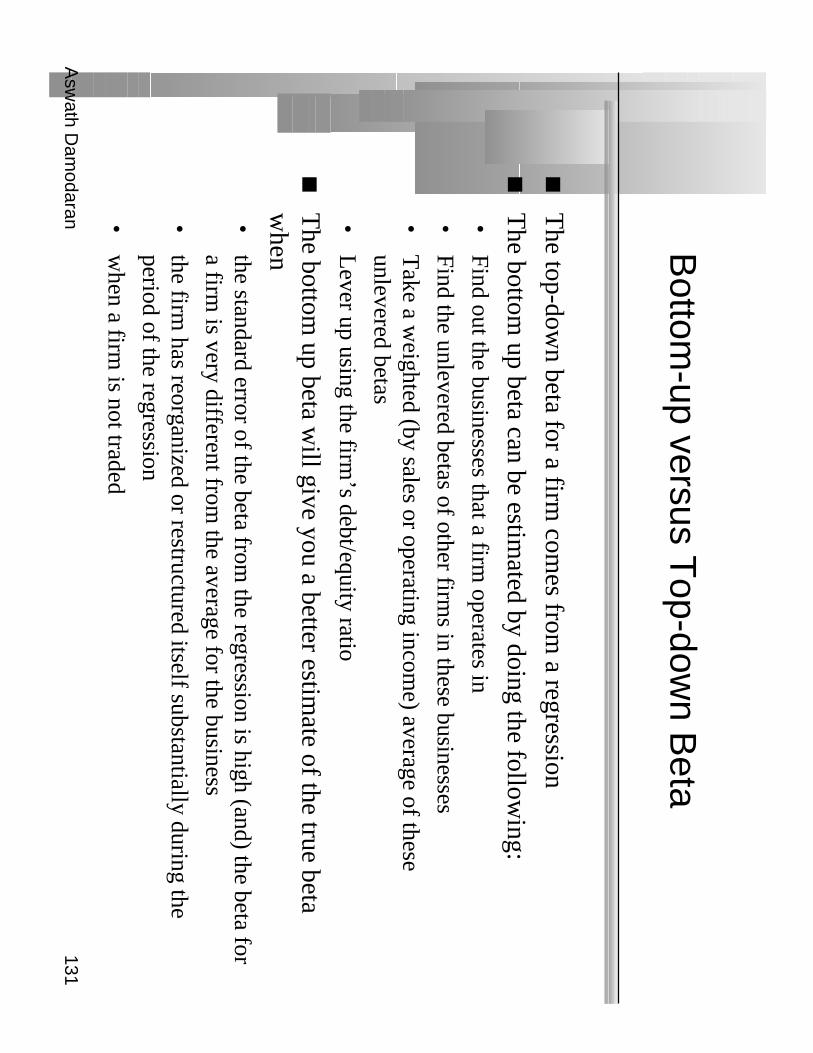

Bottom

-up versus Top-dow

n Beta

The top-dow

n beta for a firm com

es from a regression

The bottom

up beta can be estimated by doing the follow

ing:•

Find out the businesses that a firm operates in

•Find the unlevered betas of other firm

s in these businesses

•T

ake a weighted (by sales or operating incom

e) average of theseunlevered betas

•L

ever up using the firm’s debt/equity ratio

The bottom

up beta will give you a better estim

ate of the true betaw

hen•

the standard error of the beta from the regression is high (and) the beta for

a firm is very different from

the average for the business

•the firm

has reorganized or restructured itself substantially during theperiod of the regression

•w

hen a firm is not traded

Asw

ath Dam

odaran132

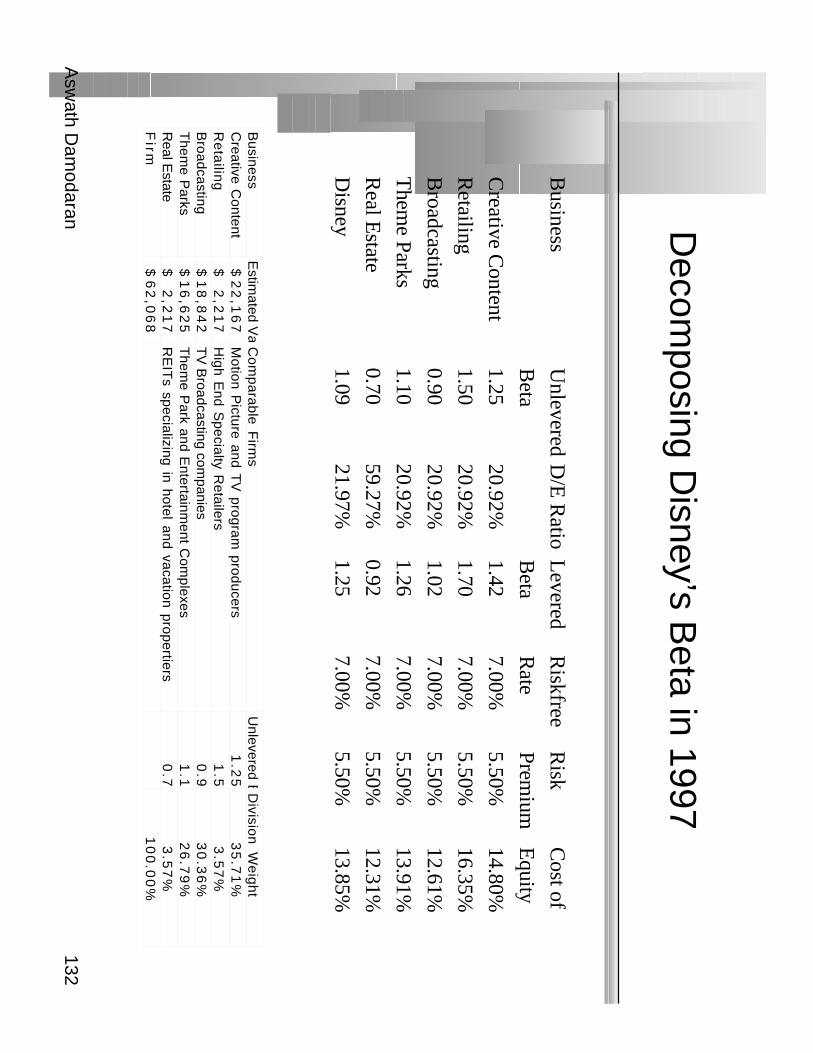

Decom

posing Disney’s B

eta in 1997

Business

Unlevered

D/E

Ratio

Levered

Riskfree

Risk

Cost of

Beta

Beta

Rate

Premium

Equity

Creative C

ontent1.25

20.92%1.42

7.00%5.50%

14.80%

Retailing

1.5020.92%

1.707.00%

5.50%16.35%

Broadcasting

0.9020.92%

1.027.00%

5.50%12.61%

Them

e Parks1.10

20.92%1.26

7.00%5.50%

13.91%

Real E

state0.70

59.27%0.92

7.00%5.50%

12.31%

Disney

1.0921.97%

1.257.00%

5.50%13.85%

Business

Estim

ated Va

Co

mp

ara

ble

Firm

sU

nlevered BD

ivision

We

igh

tC

reative Content

22

,16

7$

Motion P

icture and TV

program producers

1.2

53

5.7

1%

Re

tailin

g2

,21

7$

High E

nd Specialty R

etailers1

.53

.57

%B

roadcasting1

8,8

42

$ T

V B

roadcasting companies

0.9

30

.36

%T

heme P

arks1

6,6

25

$ T

heme P

ark and Entertainm

ent Com

plexes1

.12

6.7

9%

Real E

state2

,21

7$

RE

ITs specializing in hotel and vacation propertiers

0.7

3.5

7%

Firm

62

,06

8$

10

0.0

0%

Asw

ath Dam

odaran133

Discussion Issue

If you were the chief financial officer of D

isney, what cost of equity

would you use in capital budgeting in the different divisions?

The cost of equity for D

isney as a company

The cost of equity for each of D

isney’s divisions?

Asw

ath Dam

odaran134

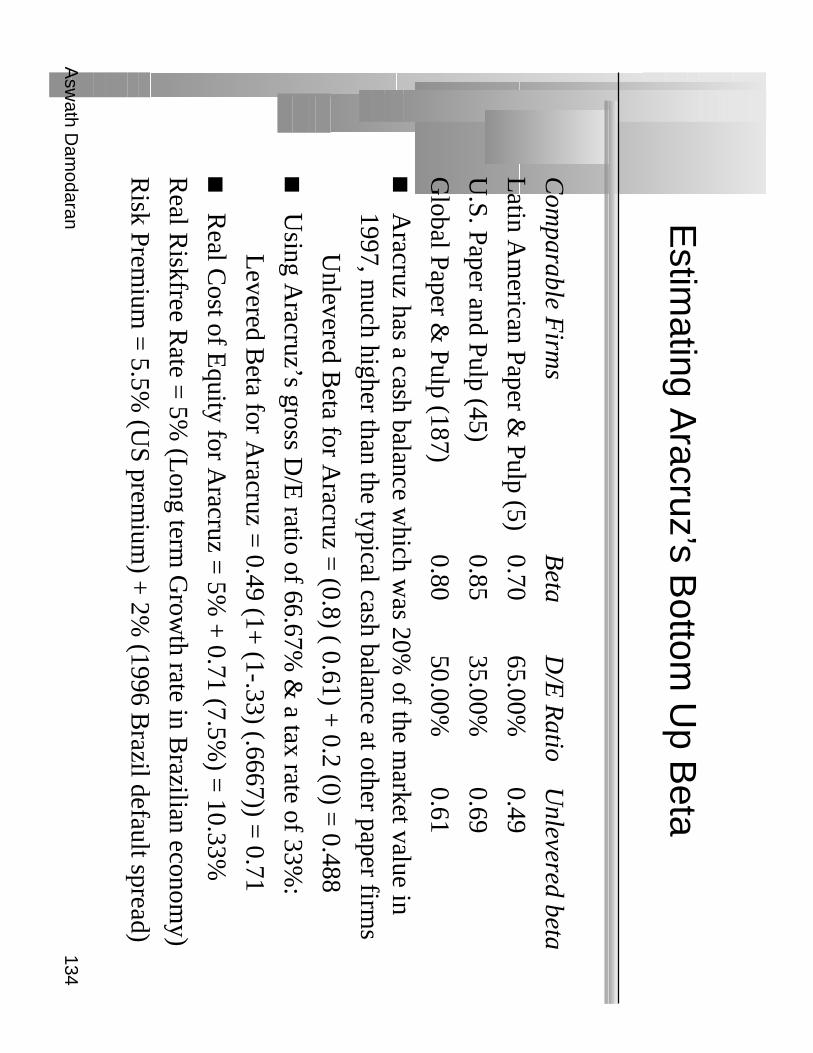

Estim

ating Aracruz’s B

ottom U

p Beta

Com

parable Firm

sB

eta D

/E R

atioU

nlevered beta

Latin A

merican Paper &

Pulp (5)0.70

65.00%0.49

U.S. Paper and Pulp (45)

0.8535.00%

0.69

Global Paper &

Pulp (187)0.80

50.00%0.61

Aracruz has a cash balance w

hich was 20%

of the market value in

1997, much higher than the typical cash balance at other paper firm

s

Unlevered B

eta for Aracruz =

(0.8) ( 0.61) + 0.2 (0) =

0.488

Using A

racruz’s gross D/E

ratio of 66.67% &

a tax rate of 33%:

Levered B

eta for Aracruz =

0.49 (1+ (1-.33) (.6667)) =

0.71

Real C

ost of Equity for A

racruz = 5%

+ 0.71 (7.5%

) = 10.33%

Real R

iskfree Rate =

5% (L

ong term G

rowth rate in B

razilian economy)

Risk Prem

ium =

5.5% (U

S premium

) + 2%

(1996 Brazil default spread)

Asw

ath Dam

odaran135

Estim

ating Bottom

-up Beta: D

eutsche Bank

Deutsche B

ank is in two different segm

ents of business - comm

ercialbanking and investm

ent banking.

To estim

ate its comm

ercial banking beta, we w

ill use the average betaof com

mercial banks in G

ermany.

To estim

ate the investment banking beta, w

e will use the average bet

of investment banks in the U

.S and U.K

.

Com

parable Firm

sA

verage Beta

Weight

Com

mercial B

anks in Germ

any0.90

90%

U.K

. and U.S. investm

ent banks1.30

10%

Beta for D

eutsche Bank =

0.9 (.90) + 0.1 (1.30)=

0.94

Cost of E

quity for Deutsche B

ank (in DM

) = 7.5%

+ 0.94 (5.5%

)

= 12.67%

Asw

ath Dam

odaran136

Estim

ating Betas for N

on-Traded A

ssets

The conventional approaches of estim

ating betas from regressions do

not work for assets that are not traded.

There are tw

o ways in w

hich betas can be estimated for non-traded

assets•

using comparable firm

s

•using accounting earnings

Asw

ath Dam

odaran137

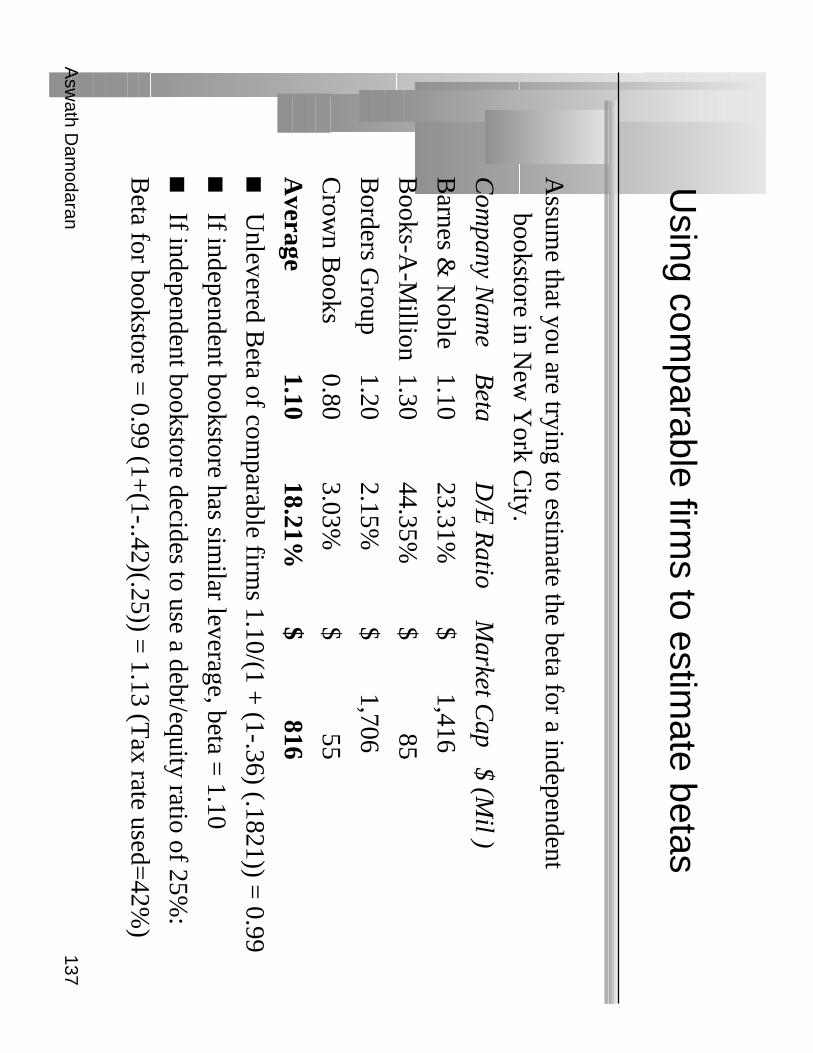

Using com

parable firms to estim

ate betas

Assum

e that you are trying to estimate the beta for a independent

bookstore in New

York C

ity.

Com

pany Nam

eB

etaD

/E R

atioM

arket Cap $ (M

il )

Barnes &

Noble

1.1023.31%

$ 1,416

Books-A

-Million

1.3044.35%

$ 85

Borders G

roup1.20

2.15% $ 1,706

Crow

n Books

0.803.03%

$ 55

Average

1.1018.21%

$ 816

Unlevered B

eta of comparable firm

s 1.10/(1 + (1-.36) (.1821)) =

0.99

If independent bookstore has similar leverage, beta =

1.10

If independent bookstore decides to use a debt/equity ratio of 25%:

Beta for bookstore =

0.99 (1+(1-..42)(.25)) =

1.13 (Tax rate used=

42%)

Asw

ath Dam

odaran138

Using A

ccounting Earnings to E

stimate B

eta

Year

S&P

500B

ookscapeY

earS&

P 500

Bookscape

1980-2.10%

3.55%1989

2.60%3.50%

1981-6.70%

4.05%1990

-18.00%-10.50%

1982-45.50%

-14.33%1991

-47.40%-32.00%

198337.00%

47.55%1992

64.50%55.00%

198441.80%

65.00%1993

20.00%31.00%

1985-11.80%

5.05%1994

25.30%21.06%

19867.00%

8.50%1995

15.50%11.55%

198741.50%

37.00%1996

24.00%19.88%

198841.80%

45.17%

Asw

ath Dam

odaran139

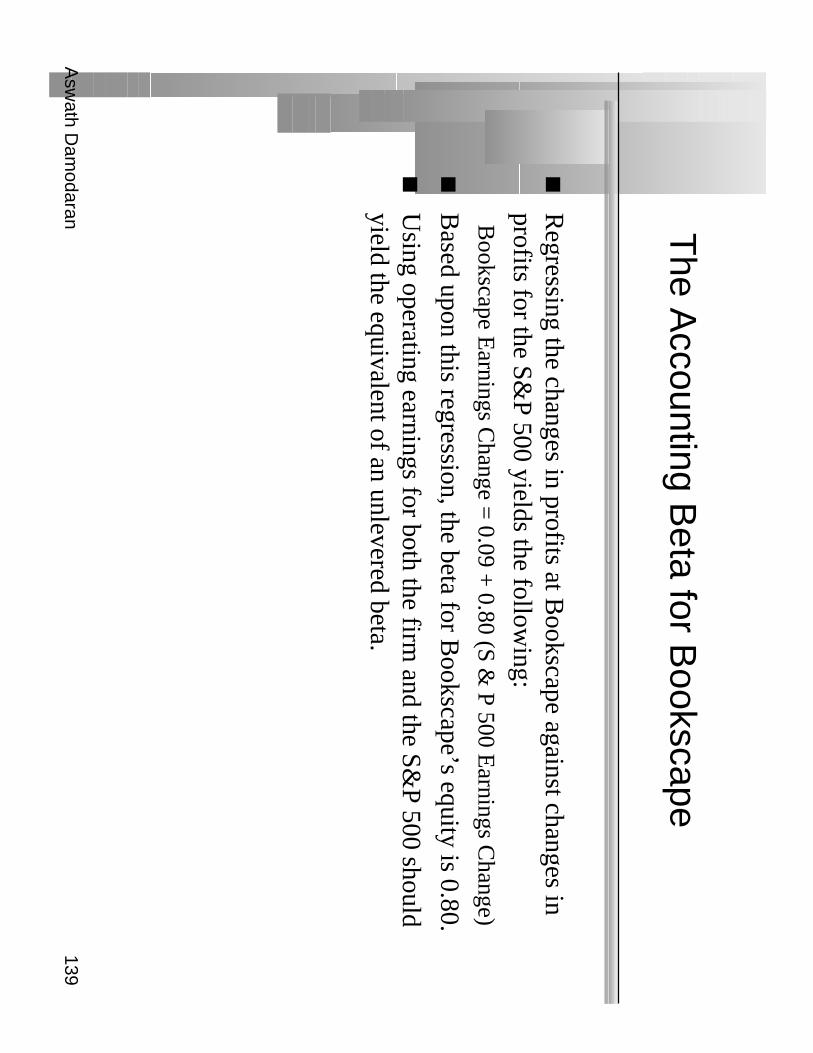

The A

ccounting Beta for B

ookscape

Regressing the changes in profits at B

ookscape against changes inprofits for the S&

P 500 yields the following:

Bookscape E

arnings Change =

0.09 + 0.80 (S &

P 500 Earnings C

hange)

Based upon this regression, the beta for B

ookscape’s equity is 0.80.

Using operating earnings for both the firm

and the S&P 500 should

yield the equivalent of an unlevered beta.

Asw

ath Dam

odaran140

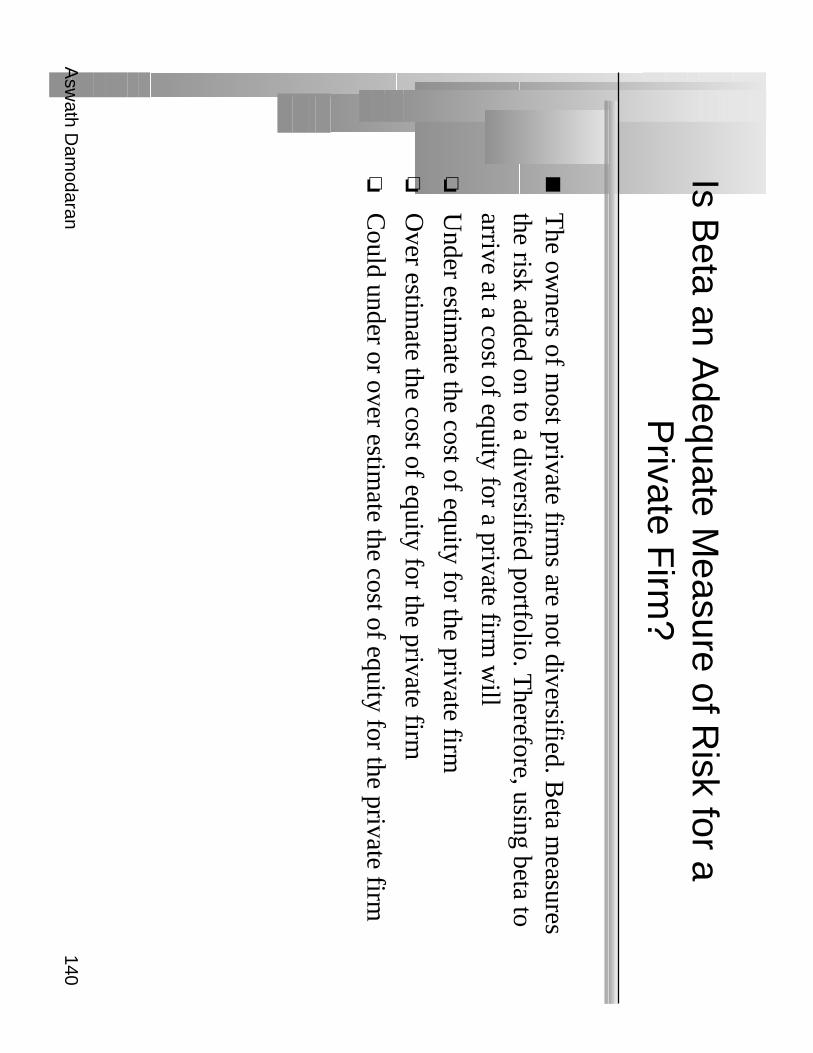

Is Beta an A

dequate Measure of R

isk for aP

rivate Firm

?

The ow

ners of most private firm

s are not diversified. Beta m

easuresthe risk added on to a diversified portfolio. T

herefore, using beta toarrive at a cost of equity for a private firm

will

Under estim

ate the cost of equity for the private firm

Over estim

ate the cost of equity for the private firm

Could under or over estim

ate the cost of equity for the private firm

Asw

ath Dam

odaran141

Total R

isk versus Market R

isk

Adjust the beta to reflect total risk rather than m

arket risk. This

adjustment is a relatively sim

ple one, since the R squared of the

regression measures the proportion of the risk that is m

arket risk. T

otal Beta =

Market B

eta / √R squared

In the Bookscapes exam

ple, where the m

arket beta is 1.10 and theaverage correlation of the com

parable publicly traded firms is 33%

,•

Total B

eta = 1.10/0.33 =

3.30

•T

otal Cost of E

quity = 7%

+ 3.30 (5.5%

)= 25.05%

Asw

ath Dam

odaran142

A

pplication Test: E

stimating a B

ottom-up

Beta

Based upon the business or businesses that your firm

is in right now,

and its current financial leverage, estimate the bottom

-up unleveredbeta for your firm

.

Data Source: Y

ou can get a listing of unlevered betas by industry onm

y web site by going to updated data.

Asw

ath Dam

odaran143

From

Cost of E

quity to Cost of C

apital

The cost of capital is a com

posite cost to the firm of raising financing

to fund its projects.

In addition to equity, firms can raise capital from

debt

Asw

ath Dam

odaran144

What is debt?

General R

ule: Debt generally has the follow

ing characteristics:•

Com

mitm

ent to make fixed paym

ents in the future

•T

he fixed payments are tax deductible

•Failure to m

ake the payments can lead to either default or loss of control

of the firm to the party to w

hom paym

ents are due.

As a consequence, debt should include

•A

ny interest-bearing liability, whether short term

or long term.

•A

ny lease obligation, whether operating or capital.

Asw

ath Dam

odaran145

Estim

ating the Cost of D

ebt

If the firm has bonds outstanding, and the bonds are traded, the yield

to maturity on a long-term

, straight (no special features) bond can beused as the interest rate.

If the firm is rated, use the rating and a typical default spread on bonds

with that rating to estim

ate the cost of debt.

If the firm is not rated,

•and it has recently borrow

ed long term from

a bank, use the interest rateon the borrow

ing or

•estim

ate a synthetic rating for the company, and use the synthetic rating to

arrive at a default spread and a cost of debt

The cost of debt has to be estim

ated in the same currency as the cost of

equity and the cash flows in the valuation.

Asw

ath Dam

odaran146

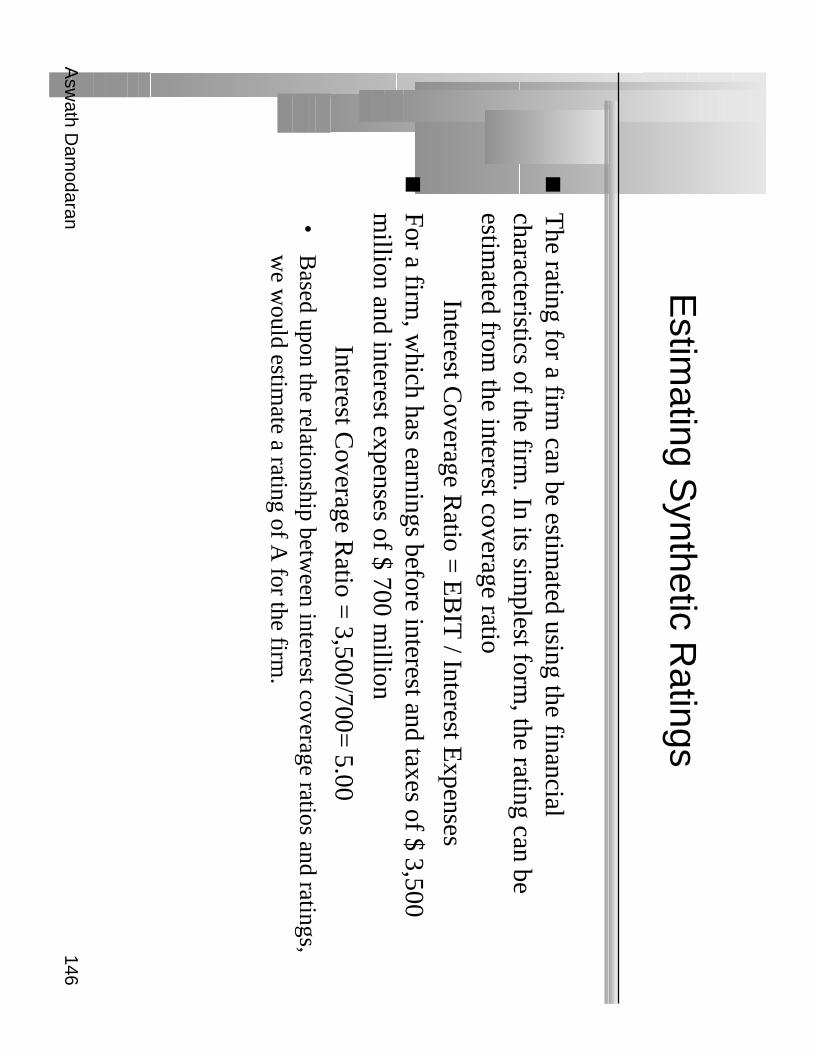

Estim

ating Synthetic R

atings

The rating for a firm

can be estimated using the financial

characteristics of the firm. In its sim

plest form, the rating can be

estimated from

the interest coverage ratio

Interest Coverage R

atio = E

BIT

/ Interest Expenses

For a firm, w

hich has earnings before interest and taxes of $ 3,500m

illion and interest expenses of $ 700 million

Interest Coverage R

atio = 3,500/700=

5.00•

Based upon the relationship betw

een interest coverage ratios and ratings,w

e would estim

ate a rating of A for the firm

.

Asw

ath Dam

odaran147

Interest Coverage R

atios, Ratings and D

efaultS

preads

If Interest Coverage R

atio isE

stimated B

ond Rating

Default Spread

> 8.50A

AA

0.75%6.50 - 8.50

AA

1.00%5.50 - 6.50

A+

1.50%4.25 - 5.50

A1.80%

3.00 - 4.25A

–2.00%

2.50 - 3.00B

BB

2.25%2.00 - 2.50

BB

3.50%1.75 - 2.00

B+

4.75%1.50 - 1.75

B6.50%

1.25 - 1.50B

–8.00%

0.80 - 1.25C

CC

10.00%0.65 - 0.80

CC

11.50%0.20 - 0.65

C12.70%

< 0.20D

14.00%

Asw

ath Dam

odaran148

A

pplication Test: E

stimating a C

ost of Debt

Based upon your firm

’s current earnings before interest and taxes, itsinterest expenses, estim

ate•

An interest coverage ratio for your firm

•A

synthetic rating for your firm (use the table from

previous page)

•A

pre-tax cost of debt for your firm

•A

n after-tax cost of debt for your firm

Asw

ath Dam

odaran149

Estim

ating Market V

alue Weights

Market V

alue of Equity should include the follow

ing•

Market V

alue of Shares outstanding•

Market V

alue of Warrants outstanding

•M

arket Value of C

onversion Option in C

onvertible Bonds

Market V

alue of Debt is m

ore difficult to estimate because few

firms

have only publicly traded debt. There are tw

o solutions:•

Assum

e book value of debt is equal to market value

•E

stimate the m

arket value of debt from the book value

•For D

isney, with book value of $12.342 m

illion, interest expenses of $479m

illion, a current cost of borrowing of 7.5%

and an weighted average

maturity of 3 years.

Estim

ated MV

of Disney D

ebt =479

11

1075

07512

3421

07511

1803

3

((

.)

.,

(.

)$

,−

+=

Asw

ath Dam

odaran150

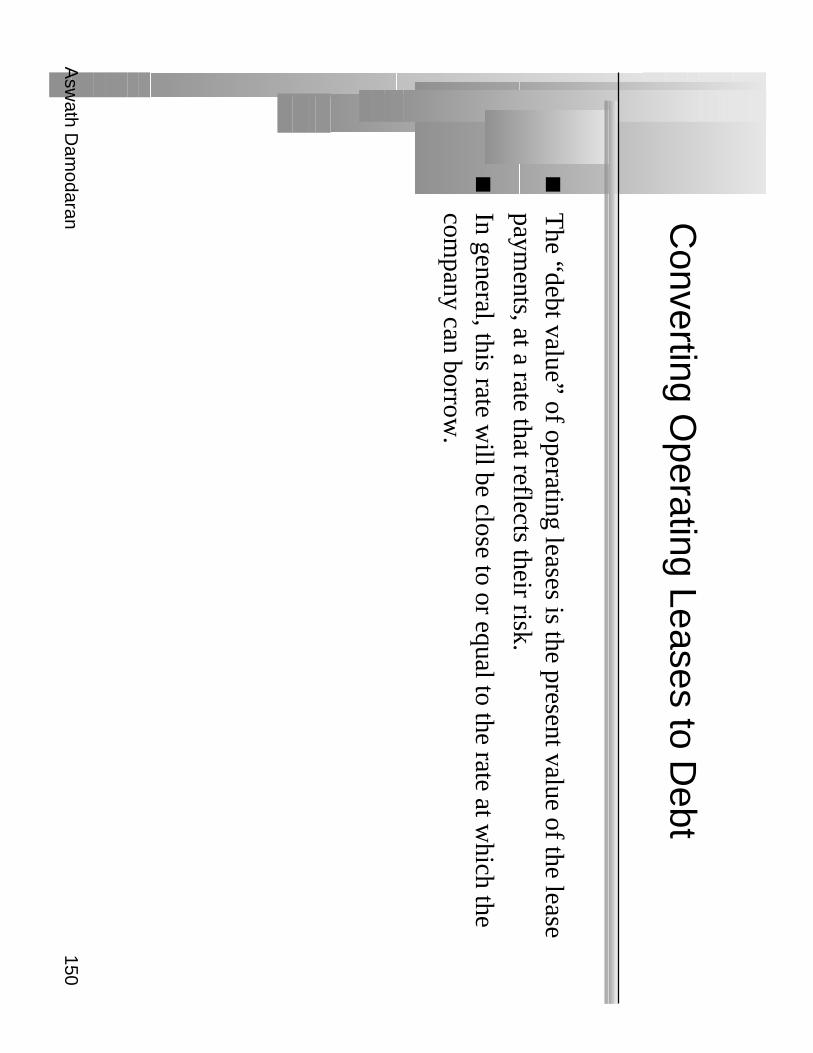

Converting O

perating Leases to Debt

The “debt value” of operating leases is the present value of the lease

payments, at a rate that reflects their risk.

In general, this rate will be close to or equal to the rate at w

hich thecom

pany can borrow.

Asw

ath Dam

odaran151

Operating Leases at T

he Hom

e Depot

The pre-tax cost of debt at the H

ome D

epot is 6.25%Y

rO

perating Lease Expense

Present V

alue 1

$ 294 $ 277

2$ 291

$ 258 3

$ 264 $ 220

4$ 245

$ 192 5

$ 236 $ 174

6-15 $ 270

$ 1,450 (PV

of 10-yr annuity) P

resent Value of O

perating Leases =$ 2,571

Debt outstanding at the H

ome D

epot = $1,205 +

$2,571 = $3,776 m

il(T

he Hom

e Depot has other debt outstanding of $1,205 m

illion)

Asw

ath Dam

odaran152

A

pplication Test: E

stimating M

arket Value

Estim

ate the•

Market value of equity at your firm

and Book V

alue of equity

•M

arket value of debt and book value of debt (If you cannot find theaverage m

aturity of your debt, use 3 years): Rem

ember to capitalize the

value of operating leases and add them on to both the book value and the

market value of debt.

Estim

ate the•

Weights for equity and debt based upon m

arket value

•W

eights for equity and debt based upon book value

Asw

ath Dam

odaran153

Current C

ost of Capital: D

isney

Equity•

Cost of E

quity = R

iskfree rate + B

eta * Risk Prem

ium=

7% +

1.25 (5.5%) =

13.85%

•M

arket Value of E

quity =

$50.88 Billion

•E

quity/(Debt+

Equity ) =

82%

Debt

•A

fter-tax Cost of debt =

(Riskfree rate +

Default Spread) (1-t)

= (7%

+0.50) (1-.36) =

4.80%

•M

arket Value of D

ebt =$ 11.18 B

illion

•D

ebt/(Debt +

Equity) =

18%

Cost of C

apital = 13.85%

(.82)+4.80%

(.18) = 12.22%

50.88/(50.88+

11.18)

Asw

ath Dam

odaran154

Disney’s D

ivisional Costs of C

apital

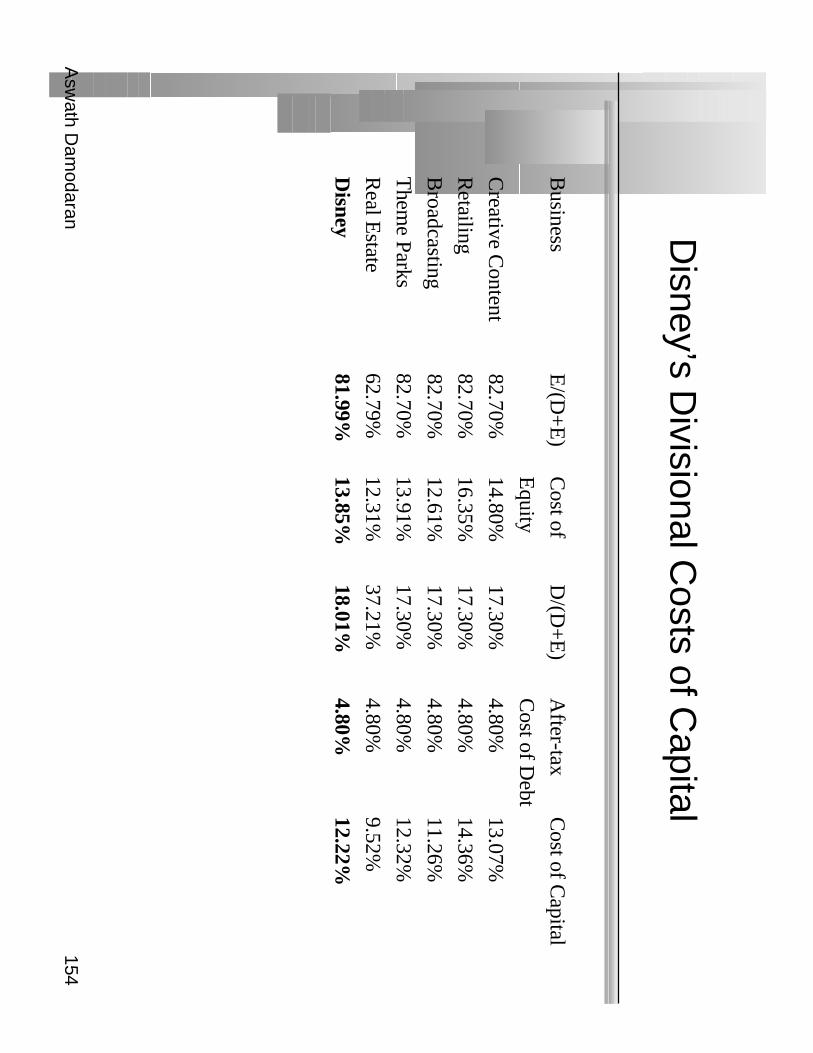

Business

E/(D

+E

)C

ost of D

/(D+

E)

After-tax

Cost of C

apital

Equity

Cost of D

ebt

Creative C

ontent82.70%

14.80%17.30%

4.80%13.07%

Retailing

82.70%16.35%

17.30%4.80%

14.36%

Broadcasting

82.70%12.61%

17.30%4.80%

11.26%

Them

e Parks82.70%

13.91%17.30%

4.80%12.32%

Real E

state62.79%

12.31%37.21%

4.80%9.52%

Disney

81.99%13.85%

18.01%4.80%

12.22%

Asw

ath Dam

odaran155

A

pplication Test: E

stimating C

ost of Capital

Using the bottom

-up unlevered beta that you computed for your firm

,and the values of debt and equity you have estim

ated for your firm,

estimate a bottom

-up levered beta and cost of equity for your firm.

Based upon the costs of equity and debt that you have estim

ated, andthe w

eights for each, estimate the cost of capital for your firm

.

How

different would your cost of capital have been, if you used book

value weights?

Asw

ath Dam

odaran156

Choosing a H

urdle Rate

Either the cost of equity or the cost of capital can be used as a hurdle

rate, depending upon whether the returns m

easured are to equityinvestors or to all claim

holders on the firm (capital)

If returns are measured to equity investors, the appropriate hurdle rate

is the cost of equity.

If returns are measured to capital (or the firm

), the appropriate hurdlerate is the cost of capital.

Asw

ath Dam

odaran157

Back to F

irst Principles

Invest in projects that yield a return greater than the minim

umacceptable hurdle rate.•

The hurdle rate should be higher for riskier projects and reflect the

financing mix used - ow

ners’ funds (equity) or borrowed m

oney(debt)

•R

eturns on projects should be measured based on cash flow

s generatedand the tim

ing of these cash flows; they should also consider both positive

and negative side effects of these projects.

Choose a financing m

ix that minim

izes the hurdle rate and matches the

assets being financed.

If there are not enough investments that earn the hurdle rate, return the

cash to stockholders.•

The form

of returns - dividends and stock buybacks - will depend upon

the stockholders’ characteristics.