investment outlook update for q2 2015

TRANSCRIPT

Macroeconomic Outlook for 2015 - Q2 Update

Samir Rath (CAIA)!MBA (Brown[USA] & IE[Spain]) !+1 312 985 7570 +65 9750 6842 [email protected] !Financial Consultant Global Financial Consultants

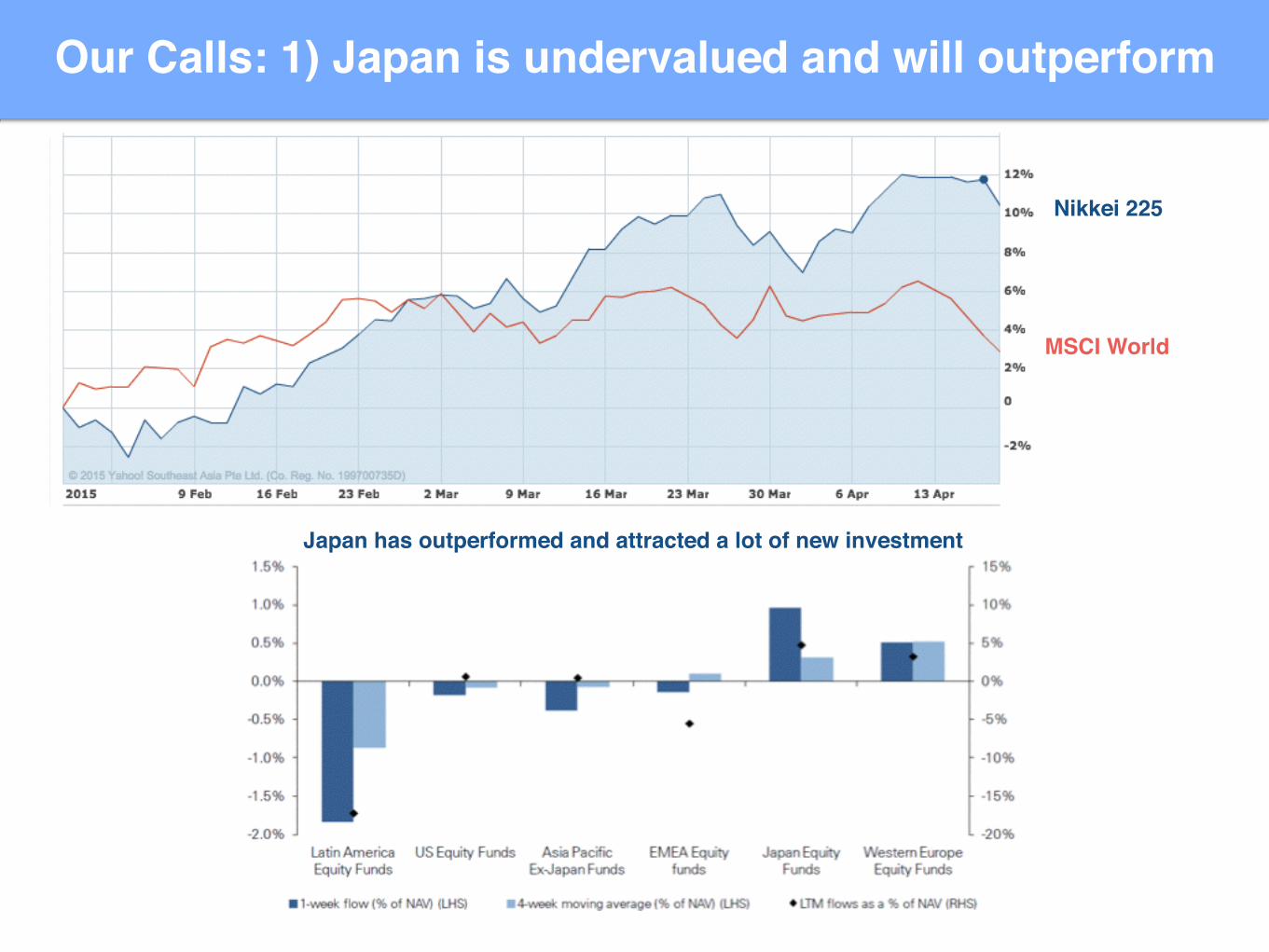

Our Calls: 1) Japan is undervalued and will outperform

Nikkei 225

MSCI World

Japan has outperformed and attracted a lot of new investment

Our Calls: 2) Emerging Market Corporate will outperform while G10 treasuries other than the US will disappoint

Emerging High Yield

Emerging Corporate

US High YieldUS Govt

International Treasuries

Our Calls: 3) Global Investors will prefer equities over bonds

Our Calls: 3) Global Investors will prefer equities over bonds

! Equity is absolutely expensive and overbought, but relatively cheap when compared to fixed income.

A strong U.S. economy helps equity, but a rising interest rate environment disproportionally hurts fixed income.

Our Calls: 4) Europe Stays in a Bubble

Current Yields for Spain and Italy stay lower than the US. Not sustainable in the long run

Our Calls: 5) Global Easing Continues

Our Calls: 6) India will moderate while Chinese stock markets will get more connected to the real economy

FTSE China

MSCI World

FTSE India

The Shanghai Stock Market Index is up 20 per cent just this month, 30 per cent for the year and almost 100 per cent over 12 months. On Apr 17, $US250 billion of Chinese stocks changed hands, which represented more than the combined volume in US equity markets.

All this activity has been supported by massive easing moves from the Chinese Government

In 2015, Indian equities are expected to maintain their uptrend, due to lower commodity prices, progress with reforms, a loosening of monetary policy, and ultimately accelerating growth. There may however be some short term corrections on the way as investors may be expecting too much too soon from the government.

China

India

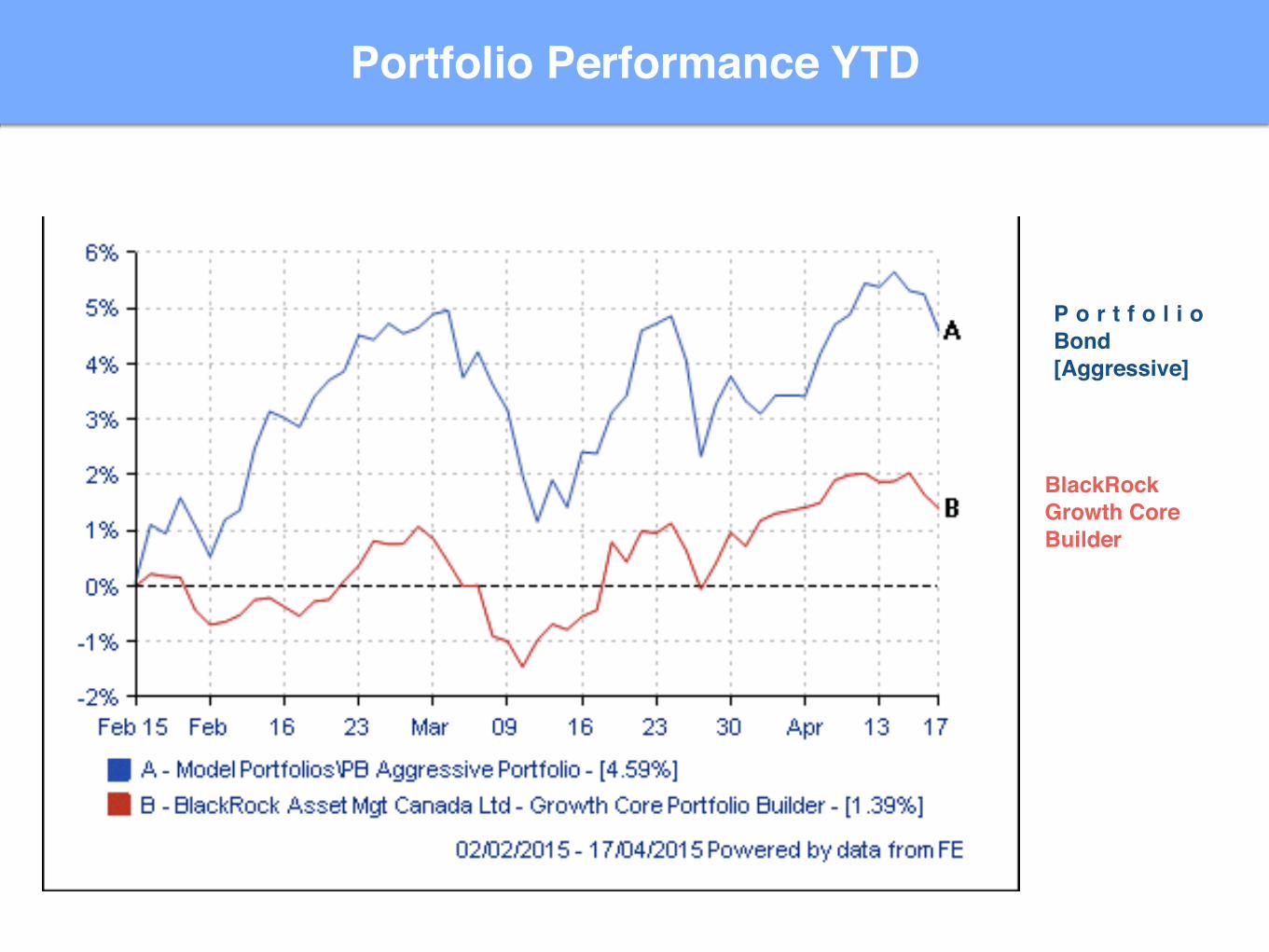

P o r t f o l i o Bond![Aggressive]

BlackRock!Growth Core!Builder

Portfolio Performance YTD

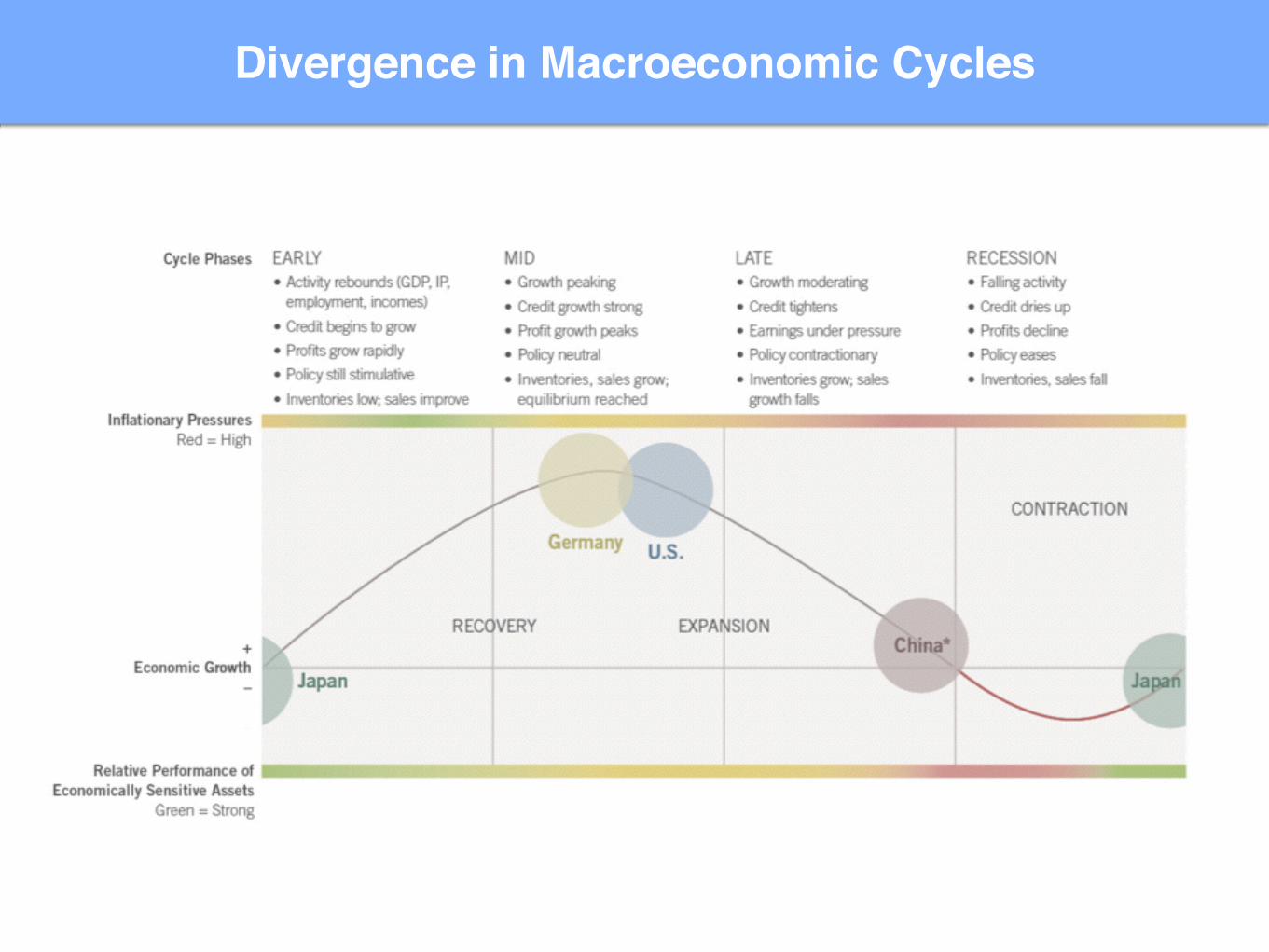

Divergence in Macroeconomic Cycles

Emerging Markets face challenges from increased Leverage and lower Growth

This is compounded by weak commodities and slowing Chinese Growth

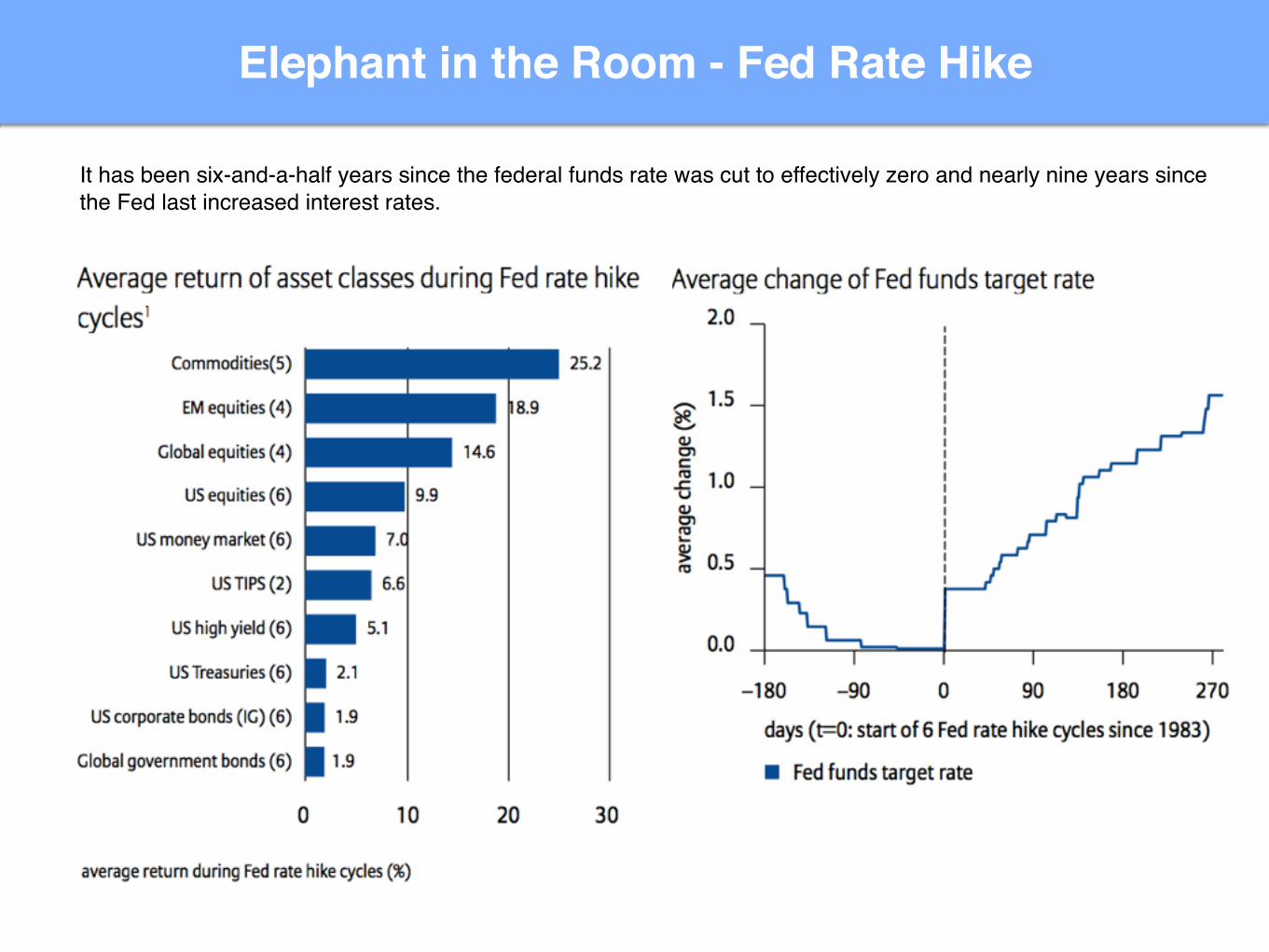

Elephant in the Room - Fed Rate Hike

It has been six-and-a-half years since the federal funds rate was cut to effectively zero and nearly nine years since the Fed last increased interest rates.

Hikes are not so favorable when markets are caught by surprise - Hike of 1994

First Fed Hike not a ShowStopper in the US

It has been six-and-a-half years since the federal funds rate was cut to effectively zero and nearly nine years since the Fed last increased interest rates.

Business and Fed Cycles effect on Equity Performance

Business and Fed Cycles effect on Equity Performance

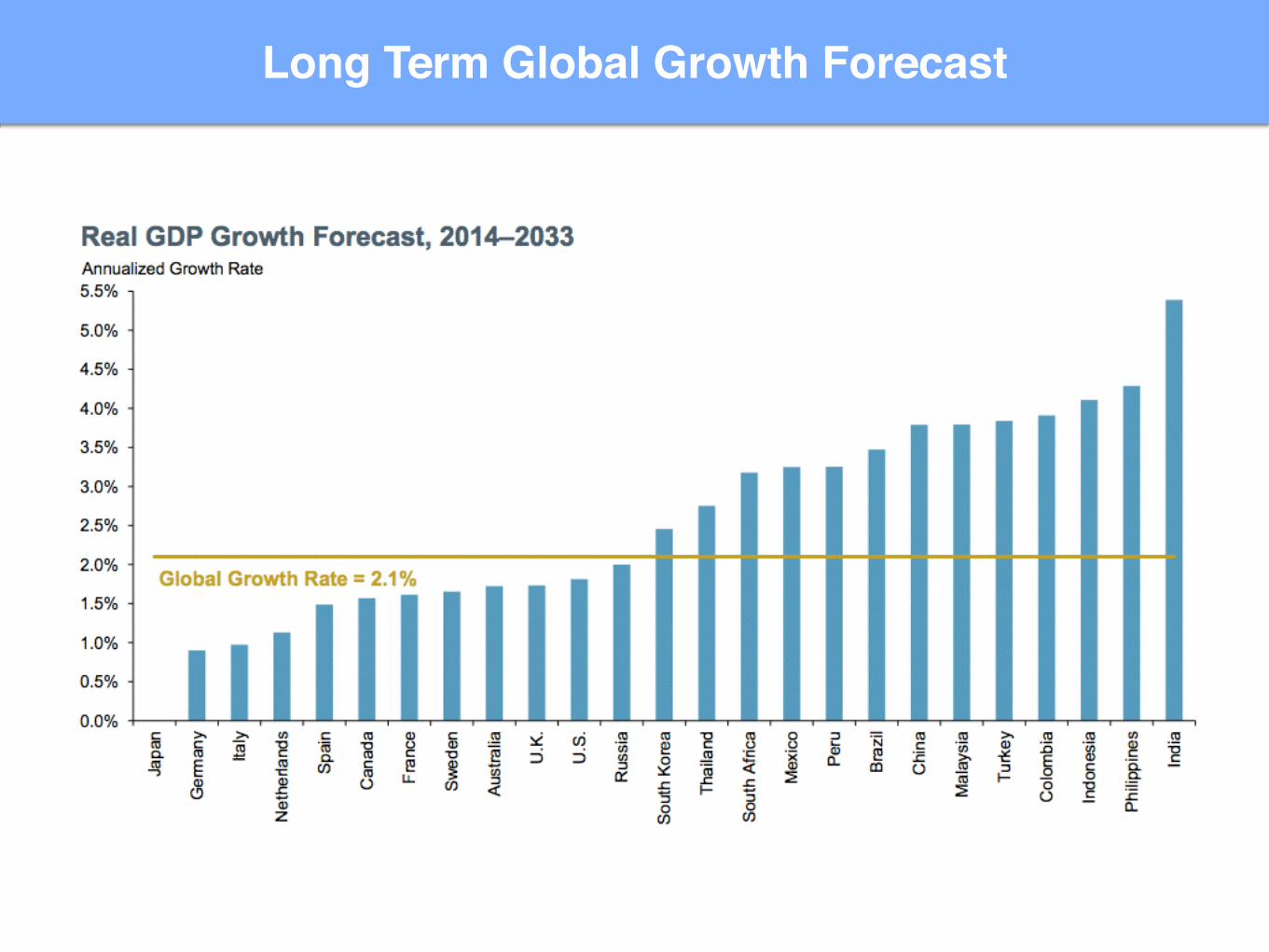

Long Term Global Growth Forecast

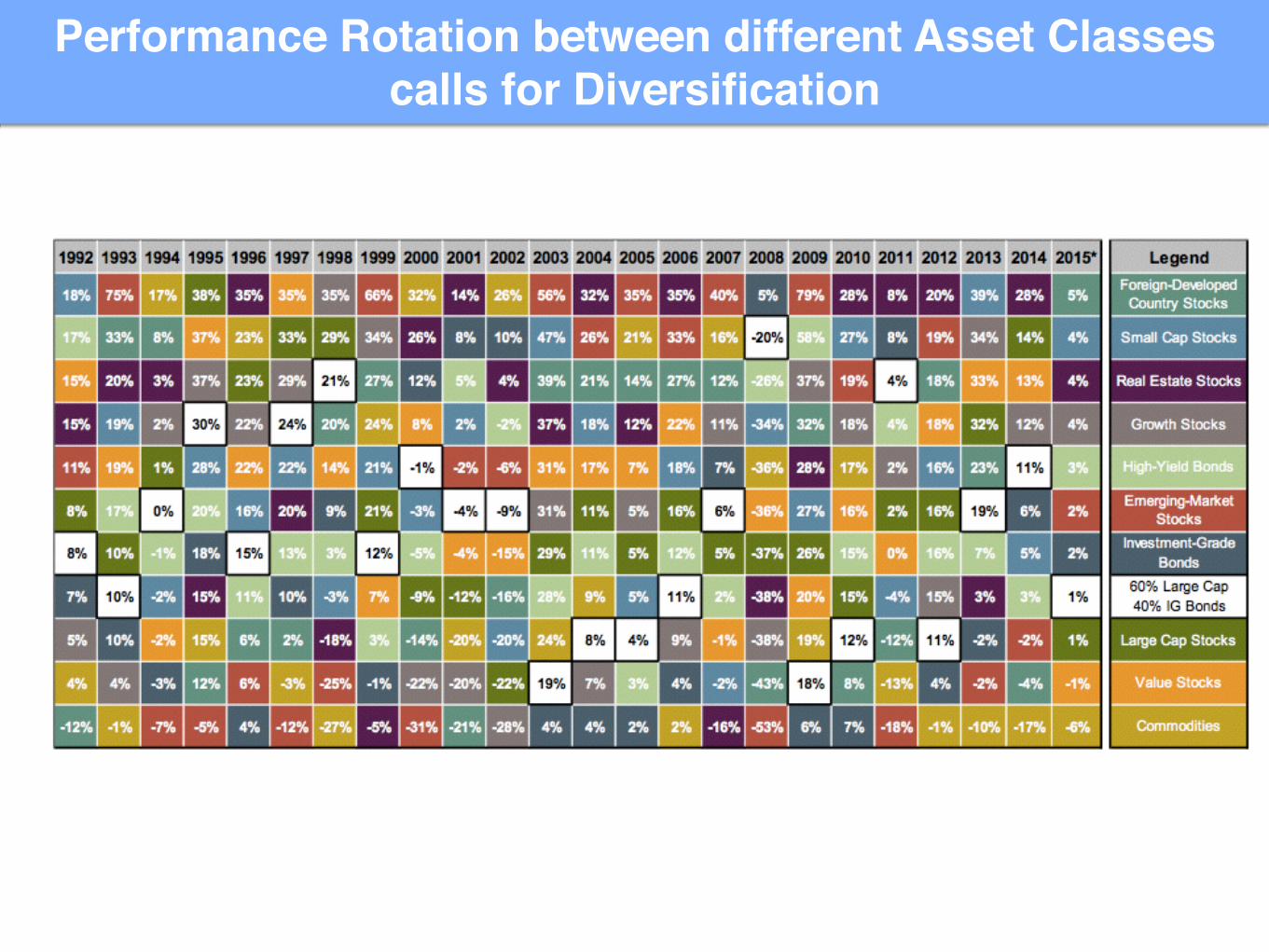

Performance Rotation between different Asset Classes calls for Diversification