investor and analyst update - banpu mongolia coal 0.2gw 29.4mt • lower s/rs at indominco,...

TRANSCRIPT

lt 2013 results investor and analyst updateinvestor and analyst update

27th February 2014

DISCLAIMER

The views expressed here contain information derived from publicly available sources that have not been independently verified. No representation or warranty ismade as to the accuracy, completeness or reliability of the information. Any forward looking information in this presentation has been prepared on the basis of anumber of assumptions which may prove to be incorrect. This presentation should not be relied upon as a recommendation or forecast by Banpu Public CompanyLi it d N thi i thi l h ld b t d ith ff t ll li it ti f ff t b ll h i j i di tiLimited. Nothing in this release should be construed as either an offer to sell or a solicitation of an offer to buy or sell shares in any jurisdiction.

2

Coal marketingCoal operationsStrategic review

321

Financial summaryPower business

54

3

2013 s mmar strengthening o r core2013 summary: strengthening our core

Indonesia coal• Record output at • Tsant Uul: good

China, Mongolia coal

0.2GW

• Record output at 29.4Mt• Lower S/Rs at

Indominco, Trubaindoand Bharinto

• Tsant Uul: good outcome from coal to chemical testing• Gaohe: 6Mt (above

target 1Mt); rail spur 6Mt

1.2Mt

Power

• Reduction in total costs by 11%• IPCC trial commenced

in Dec 2013

bridge development• Hebi: steady output

1.8GW

29.4Mt1.4GW

Australia coal

• Annual output records: Myuna, Angus Place, Charbon and Clarence

• BIC: record profit• Hongsa: 78% complete• BLCP: equity income up

13% to $82M

13.8Mt

Charbon and Clarence• Strong domestic sales;

new 24Mt, 8-year contract• New equipment at

Corporate• Group OHs down 10%• Coal marketing, sales

and trading office New equipment at Mandalong, Springvale and Myuna should boost productivity• Logistics and

i f i i d

and trading office established in Singapore• Financial management

focus: debt service, share restructuring and

Mines

Power plant

4

infrastructure optimisedderivatives

Note : Output on 100% basis (except Australia ROM output is stated on an equity basis)

Power project

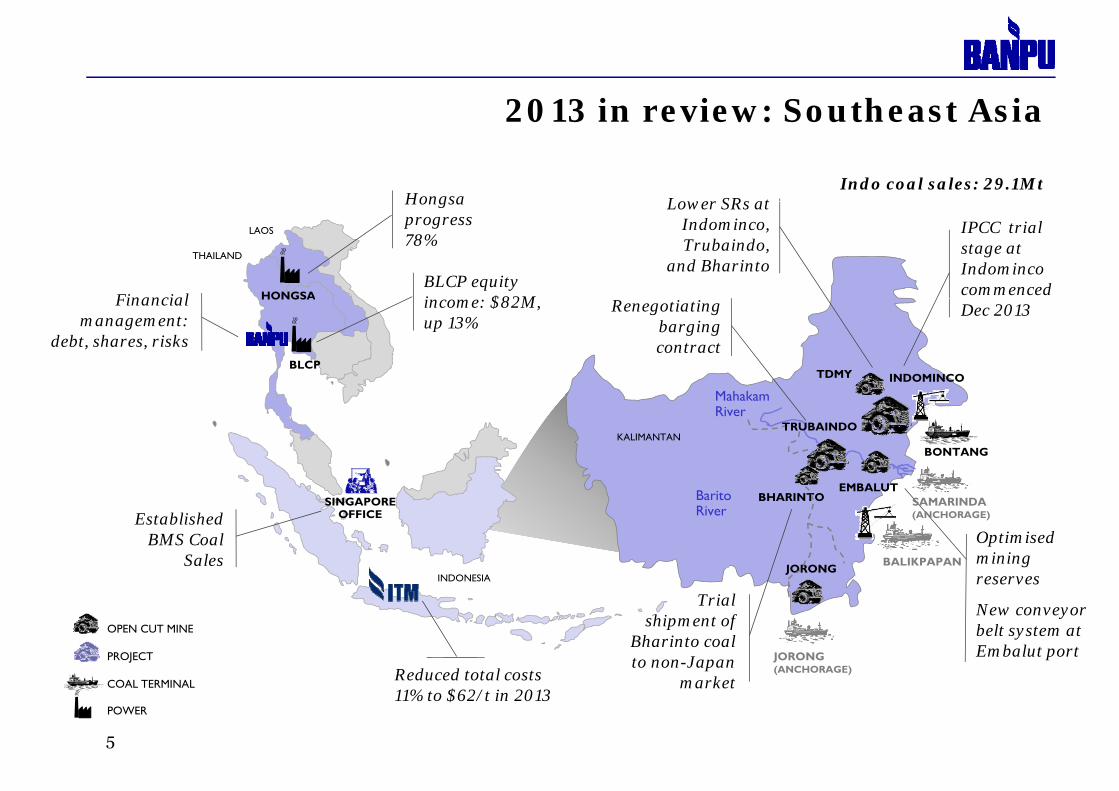

2013 in re ie So theast Asia2013 in review: Southeast Asia

Hongsa Lower SRs at Indo coal sales: 29.1Mt

THAILAND

LAOS

HONGSABLCP equity i $82M Financial

Hongsaprogress 78%

IPCC trial stage at Indominco commenced

Lower SRs at Indominco, Trubaindo,

and Bharinto

Mahakam INDOMINCOTDMY

BLCP

HONGSA income: $82M, up 13%

Financial management:

debt, shares, risks

Dec 2013Renegotiating barging contract

Mahakam River

B itEMBALUT

BONTANG

TRUBAINDOKALIMANTAN

INDONESIA

BaritoRiver

BALIKPAPAN JORONG

BHARINTOSINGAPOREOFFICEEstablished

BMS Coal Sales

Optimisedmining reserves

SAMARINDA(ANCHORAGE)

JORONG(ANCHORAGE) Reduced total costs

OPEN CUT MINE

PROJECT

COAL TERMINAL

Trial shipment of

Bharinto coal to non-Japan

market

New conveyor belt system at Embalut port

5

11% to $62/t in 2013COAL TERMINAL

POWER

market

2013 in re ie A stralia

NORTHERN

2013 in review: AustraliaCost reduction and productivity improvementFour annual production recordsRationalised capex

WESTERN AUSTRALIA

QUEENSLAND

NORTHERNTERRITORY

NSW

SOUTHAUSTRALIA

Rationalised capexSales contract with major power station at long-term export parity

Mandalong -Introduced 3x S d ik MB6

VICTORIA

CHARBONINGLENOOK

NORTHERN OPERATIONSWESTERN

OPERATIONS

Sandvik MB650 CM, with resultant record development

Myuna re equipped Airly re-evaluation

NEWSTANMANDALONG

MYUNA

INGLENOOK

AIRLY

ANGUS PLACE

SPRINGVALE

NEUBECK

IVANHOENewcastle

New state-of-the-t l ll t

Myuna re-equipped, and delivered record production

yof mine plan for re-

opening

Sydney

Wollongong

MANNERINGCLARENCE

OPEN CUT MINE

art longwall at Springvale Improved coordination

between rail, ports and domestic customersRelinquished tonnage

UNDERGROUND MINE

PROJECT

PORT

ROADMannering transfers operating risk through

Relinquished tonnage at PWCS(T4)

6

RAIL

operating risk through 3rd party production sharing arrangement

2013 in re ie China and Mongolia2013 in review: China and Mongolia

MONGOLIA Studying potential

Xinjiang

Heilongjiang

Jilin

Liaoning

Taiwan

Tibet

Sichuan

Yunnan Guangdong

Fujian

Shandong

Hubei

Hunan Jiangxi

Inner Mongolia

NingxiaQinghai

Hebei

Shanxi

Henan

Anhui

Zhejiang

JiangsuShaanxi

Guizhou

MONGOLIA

ALTAI NUURS

Studying potential of CHP in Mongolia

UNST KHUDAGTaiwanYunnan

Guangxi Guangdong

Hainan

TSANT UUL

Tsant Uul: small pilot test with encouraging LUANNANBIC record net

Altai Nuurs :exploration and feasibility study to b l t d i

test with encouraging results on a coal to coal tar, off-gas and semi coke plantHebei

Shanxi

GAOHEZHENGDING

Gaohe: 6 Mt ( b l

profit: $24M contribution

be completed in 2014

Shandong

Shanxi ZHENGDING

ZOUPING

(above plan of 5 Mt)

HenanHEBI

Hebi: 1.2 Mt OPEN CUT MINE

PROJECT

POWER

CHINA

7

CHINA

2014 and be ond Indonesia cost str ct re red ctionCOMMENTS

2014 and beyond: Indonesia cost structure reductionIN-PIT CRUSHING AND CONVEYING (IPCC)

● IPCC trial commenced in December 2013 at Indominco East Block

OB l it

Mine depth without IPCCMine depth with IPCC

ILLUSTRATIVE ONLY

SPREADER

IPCC WASTE DUMPNON-IPCC

WASTE DUMP

● OB removal capacity: 14 MBcm per year

● Using power from Indominco coal-fired

PIT BENCHES

IN-PIT CONVEYORS

BACKHOE EXCAVATOR

TRUCKC.120 M

power plant

● Estimated cost savings around 10% of OB costs

C.80 MIN-PIT

CRUSHERDEEPER

TONNAGES

IPCC WASTE

● Facilitates access to deeper coal reserves

● More environmentally friendly: less dust less friendly: less dust, less noise, lower emissions

8

2014 and be ond f rther Indonesia cost plansMID-TERM: ELECTRIFICATION

2014 and beyond: further Indonesia cost plansDIESEL SUBSTITUTION

ILLUSTRATIVE ONLYILLUSTRATIVE ONLY

● Completed study for trucks to partially replace ● Electric overland conveyors being studied to d l t t t t b th I d i

Test unitwith LNG tank

diesel with LNG or other alternative fuels

● Currently at trial stage for coal transport at Indominco-Bontang

P hi i h d i i

reduce coal transport cost at both Indomincoand adjacent operations and Trubaindo-Bharinto

● Would enhance efficiency of coal transport while reducing operating costs

● Partnership with contractor under negotiation

● Possible implementation at Trubaindo-Bharinto

g p g

● Proven technology widely used in Europe, USA and Australia

● Possible medium term implementation

9

2014 and be ond A stralia optimisation programme2014 and beyond: Australia optimisation programme

COST MANAGEMENT REVENUE OPTIMISATION

Improving production volume

Logistics optimisation Sales contract pricing Balance customer diversification

• Lidsdale siding upgrade, completion due May 14

• Optimisation of rail and port capacity

• Target increased production from Springvale, Mandalongand Myuna, following new equipment

• New domestic sales contracts to be priced at long-term export parity price, providing a natural hedge against A$/US$

• Balance coal sales and revenues from domestic and export business

• Reduce customer i i k• Improved coordination

between rail, ports and domestic customers

new equipment installation in 2013

• Reduced longwallchangeover time

• ‘Step Change’

hedge against A$/US$ volatility concentration risk

• Step Change productivity programmecommenced

10

2014 and be ond po er b siness gro thNOTE: COMPARATIVE ECONOMICS

2014 and beyond: power business growthINVESTMENT OPPORTUNITIES IN POWER

Value creationValue creation

CURRENT PROJECTS NEW PROJECTS Capex($/kW)

Non-fuel O&M ($/kW)

Capacity factor

Constructiontime

Nuclear 74,500 1 2 3 85%

BLCP18 year lifetime

??

??

Brownfield?

Greenfield?

Hongsa

Coal supercritical

Gas CCGT 3

5

700

1,500

2 5

6 0

60%

80%

Lifecycle

78% progressWind

Solar 1.5

1.5

3,500

1,600 2 1

na

22%

na

● Fossil fuel like thermal coal and gas remains a primary source for power generation

● Renewable energy growing due to supportive li i d l

● Hongsa project in Laos: 78%-progress; COD in 2H2015 and in 1H2016

● Potential for brownfield growth around existing ? government policies toward cleaner energy

● Japan and China aimed to significantly expand power capacity from wind and solar: short construction time of 1.5 years

power assets ?● Banpu exploring potential for new investment in

coal-fired power and potentially also in renewable power businesses in Asia-Pacific

11 Source: IEA Note : capital costs include interest during construction, engineering, procurement , construction and legal expenses

Long term Asia Pacific po er demand to 2035Long term Asia Pacific power demand to 2035

China 1 193 1,258

Japan9,542

CAGR5% CAGR

Power demand in Asia-Pacific forecast to China 1,174 1,193 , 58

IndiaKorea

616514 5553,437

5,462

6,467

CAGR

2%

8%

CAGR

-3%

0%

2%

forecast to increase 76% by 2035 including 66% increase in coal-fired power

i l 514 555

1,855

1 374

2015 2020 20352015 2020 2035

6%

3%

6%

2%2%

-2%

1%

1%

equivalent to 2.1 billion tonnesincremental coal demand*

Vietnam

Thailand

761

1,102

670220353

187

128 174

410

1,374

2015 2020 2035 201 2020 203

2015 2020 20355%

CAGR

%

CAGR16%2%5%8%

Other Asia Pacific

CAGR0%4%Philippines

Indonesia

6701872015 2020 2035

2015 2020 2035

2015 2020 2035

Coal

Gas

2%6%

2015 2020 2035

4%

1%

10483187 CAGR

6%

2015 2020 2035

Australia221 286

607

311290 353

Unit: TWh

Hydro

Others*

2015 2020 2035CAGR1%6%3%

6%CAGR

6%1%EIA assumption

12 *Note: ‘Others’* include power generation from oil, nuclear, geothermal and non-hydro renewablesSource : Energy outlook for Asia and the Pacific report, October 2013, ADB and APEC

2015 2020 2035

2015 2020 2035 5%2%

1,870 KWh = 1 tonne coal1 TWh = 0.54 million tonnes coal

B i i it t t i h iBanpu examining its strategic horizonsfi

c*ra

ns-

Pac

if

?

Tr

AUSTRALIA ?

ia-P

acif

ic COAL

CHINACHINA COAL

?

As CHINA

POWER

?

BONTANG

INDONESIA COAL

COALHUNNU

C l i i Coal power/oil New energy**

BLCPHONGSAILLUSTRATIVE ONLY

13

Coal-mining

* The Trans-Pacific Partnership (‘TPP’) is currently under negotiation between countries of Asia-Pacific and the America to foster trans-Pacific trade and investment growth

Coal-power/oil New energy**

* New energy technologies: renewable energy, unconventional energy extraction, alternative fuels…

Coal marketingCoal operationsStrategic review

321

Financial summaryPower business

54

14

A stralia Coal operational and financial s mmarAustralia Coal: operational and financial summary2013 OUTPUT (ROM EQUITY BASIS) KEY UPDATES

Production ASP Production● Equity ROM 3.7Mt (up 21%

YoY), with all three LWs* in full production during 4Q13

● Equity ROM of 13.8 Mt (2012 14 6 Mt ) l t

ASP ● 4Q13: A$68/t ● Sales volume down 5% YoY● Domestic: export split

62%:38% (2012: 56%:44%)Newcastle (2012: 14.6 Mt ); placement

of Airly and Mannering into C&M in 4Q12

● Focus on productivity resulted in four annual

d ti d

● Improved domestic margins helping to sustain ASP

● 2013 ASP c. A$70/t

Charbon

Airly

Neubeck Angus Place

Mandalong Myuna

Newstan Extension

PWCS

Newcastle

InglenookNCIG

M i

2013 YoY 4Q13 QoQ

production records*LW: longwall

FINANCIAL SUMMARY

Place

Clarence

SpringvaleNORTHERN OPERATIONS:

7.0 Mt

Mannering

Sales revenue A$966m ▼ 12% A$259m ▲ 10%

EBITDA (pre FX) A$160m ▼53% A$49m 0%

PBT (pre FX) A$(11)m n.a. A$1m n.a.

Unrealised FX3 A$(56)m n a A$(5)m n.a.

Sydney

Open-cut mine

WESTERN OPERATIONS: 6.8 Mt

Unrealised FX A$(56)m n.a. A$(5)m n.a.

NPAT A$(47)m n.a. A$(2)m n.a.

Gearing(Net debt to net debt + book value of equity)

36% 36%

Wollongong

PKCT

Open cut mine

ProjectUnderground mine

PortPower station

RoadRail

CAPEX4 A$174 ▼58% A$48 ▼5%

15Note 1: Airly and Mannering mines placed on “Care & Maintenance” November 2012.Note 2: NCIG = Newcastle Coal Infrastructure Group; PWCS = Port Waratah Coal Services; PKCT = Port Kembla Coal Terminal.Note 3: Pre tax impact of A$ translation of US$ denominated net debt. A$ depreciated 14% in 2013.Note 4: Plant & Equipment

A stralia Coal Northern Operations q arterl o tp tNEWSTAN EXTENSIONMANDALONG OTHER OPERATIONS

Australia Coal: Northern Operations quarterly output

COAL OUTPUT (Mt)*

CV: 6,700 kcal/kg**

COAL OUTPUT (Mt)*

CV: 6,700 kcal/kg**

COAL OUTPUT (Mt)*

CV: 6,700 kcal/kg**

1.1 0.8

1.9

0.7

1.5 1.4

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14e

0.6 0.5 0.6 0.5 0.5 0.7

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14e 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14e

Completion date extended

LW MOVE SCHEDULE

Mth 16

k

● Mandalong Annual production down 10% YoY:

d d h

LW MOVE SCHEDULE

Mth 1

COMMENT

3Mth 1

Mth 2

Mth 3 4 wks

wks two extended changeovers, LW outperformance; installation road failure 3x new development units achieving

record performance

Mth 2

Mth 3

7 wks

3wks

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14e 2Q14e

● Myuna: 2013 annual production record of 1.6 Mt, 10% up on 2012

● Newstan: continues as CM mine while expansion opportunities assessed ventilation shaft completed

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14e

16

ventilation shaft completed

Note: *ROM output on an equity basis**CV figures are air-dried basis

A stralia Coal Western Operations q arterl o tp tOTHER OPERATIONSANGUS PLACE SPRINGVALE

Australia Coal: Western Operations quarterly output

0 9 1 0 1 0 8

COAL OUTPUT (Mt)*

CV: 6,700 kcal/kg**

COAL OUTPUT (Mt)*

CV: 6,700 kcal/kg**

COAL OUTPUT (Mt)*

CV: 6,700 kcal/kg**

0.9 0.7 1.0 1.0 0.7 0.8

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14e

0.4 0.3 0.2 0.4 0.5 0.50.2 0.5 0.5 0.5 0.5 0.4

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14e4Q12 1Q13 2Q13 3Q13 4Q13 1Q14e

COMMENT

● Angus Place: above plan performance: record c.4.0 Mt (100%)

● Charbon and Clarence: Strong performances resulted in record

LW MOVE SCHEDULELW MOVE SCHEDULE

2 pannual output of 1.5 Mt and 2.4 Mt respectively (100%)

● Springvale: challenging mining conditions and ageing equipment for much of 2013; new LW commissioned

Mth 1

Mth 2

Mth 3

Mth 1

Mth 2

Mth 3

6 wks

2 wks

1 4 much of 2013; new LW commissioned during 4Q13, now full production

● Bushfires 4Q: Lost 5-days output at Clarence and Springvale; rail network affected for two weeks

Mth 3

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14e 2Q14e

Mth 3

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14e 2Q14e

1 wk

4wks

17 Note: *ROM output on an equity basis: Angus Place and Springvale 50%, Clarence 85% & Charbon 95% **CV figures are air-dried basis

A stralia Coal operating costsCOMMENTS

Australia Coal: operating costsINDICATIVE AVERAGE PRODUCTION COSTS*

60

● Strong 4Q13 performance delivered lowest quarterly cost for year

● Focus on cost control and d ti it d li d i d $52

$59A$/t$58

$52$55

$53

Planned cost reduction 2012 achieved

$ $

40

50productivity delivered improved costs YoY

● A$100m removed from 2013 cost base compared to 2012 (including Coal handling & preparation

Open-cut contractor cost

Depreciation

$52 $5

$47

$51 $51 $50

30

p ( gone-off redundancy costs in 4Q13)

● Group productivity improved c.9%, leading to four annual production records

General expenses

g p p

Repairs & maintenance

Cash overhead

10

20records

● One-off costs due to bushfires and further restructuring impacted 4Q13 by c. $1/tonne

Stores & supplies

Labour

0

● Continuing focus on improving operating costs and productivity: FY14 costs expected to improve further

Labour

1Q 2Q 3Q 4Q2012

Full year2012

1Q Full year20132013

2Q 3Q 4Q

18

further* These figures do not include selling, distribution and royalty costs** Based on ‘sold’ production

2012 32013

A t li C l f th ti i tiLOGISTICS

Australia Coal: further optimisationPRODUCTIVITY

● Lidsdale Siding: Western load point upgrade to ● Springvale: new generation high productivity g p pg8 Mt will complete May 2014

● Rail efficiency improving, with longer trains driving lower costs

p g g g p yLW in full production

● Mandalong: 3x New generation LW Development CMs delivering + 20% improvement in development rates ● Improved coordination between rail, ports and

domestic customers

improvement in development rates

● Myuna: completely re-equipped

● “Step Change” productivity programmecommenced across all mines

19

commenced across all mines

I d i l ti l d fi i l KEY UPDATES

Indonesia coal: operational and financial summaryOUTPUT 2014 (100% BASIS, SALEABLE COAL)

2014 target: 29 5 Mt Production ASP

East Kalimantan

Indominco

KitadinTandung Mayang1.8 Mt

2014 target: 29.5 Mt Production

• 2013: record output of 29.4mt (slightly lower than plan), up 7% YoY

Q d %

ASP

• 2013: $74.9/t (down 17% YoY)

• 4Q13: $71.0/t (down 2% Q Q)

Bunyut Port

15.2 Mt

Trubanindo7 3 Mt

Bontang Coal Terminal

Captive coal-fired power

project

• 4Q13: 7.4mt, down 7% YoY

• 2013 production slightly lower than target due to weather condition

QoQ)

• Weak coal market throughout 2013 impacted ASP

FINANCIAL SUMMARY

2013 YoY 4Q13 QoQ

BalikpapanCentral Kalimantan

Kitadin -Embalut

1.0 Mt

7.3 Mt

Bharinto3.0 Mt

Samarinda weather condition

2013 YoY 4Q13 QoQ

Sales revenue $2,179m ▼ 11% $546m ▲ 1%

EBITDA $401m ▼ 35% $102m ▼ 11%

Palangkaraya

Banjarmasin

South Kalimantan

NPAT $230m ▼ 47% $46m ▼25%

Gearing(Net debt to Net debt + book value of equity)

n.a. n.a.

CAPEX $44m $4m

Jorong1.2 Mt

Jorong Port

OperationProject

OperationProject

POWER

COAL

20

CAPEX $44m $4m

Indonesia coal q arterl o tp tEMBALUT AND JORONGINDOMINCO - BONTANG TRUBAINDO - BHARINTO

Indonesia coal: quarterly output

COAL OUTPUT (Mt)* COAL OUTPUT (Mt)* COAL OUTPUT (Mt)*

0.3 0.2 0.3 0.20.4 0.30.4

80.6 0.7

0 5

4.9

4.3 4.14.6 4.7

4.3

COAL OUTPUT (Mt)*

CV: 6050 - 6500 kcal/kg**

MY

COAL OUTPUT (Mt)*

CV: 6250 - 7200 kcal/kg**

TO

COAL OUTPUT (Mt)*CV: 5750 kcal/kg**

EM

BA

LUT

NG

0.50.2 0.5

3.4

2.01.1 1.1

1.3 1.0 0.40.8 0.5 0.5

TDM

WB

LOCK

ND

OB

HA

RIN

T

2.4 2.3

CV: 5300 kcal/kg**

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14e2.6 2.52.2

0.32.1

0.3 0.3 0.3 0.3 0.3 0.3JOR

ON

2.1 2.0 2.0 2.0 1.9 1.72.5 2.4 2.5 2.7 3.0 3.4

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14e

E B

LOC

K

TRU

BA

IN

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14e 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14e

15.1 15.1 15.1 15.1 15.117.9

STRIP RATIOS (bcm/t)

TDM

Y

STRIP RATIOS (bcm/t)

BH

AR

INTO

6.9 6.9

STRIP RATIOS (bcm/t)

10.611.5

MB

ALU

T

6

11.510.9 10.6

7.5

9.2

7.57.8

7.2

16.9

IND

OM

INC

O

13.919.1

9.3

16.8

7.2

TRU

BA

IND

O

10.312.2 10.9 10.9 11.18.6 6.0JO

RO

NG

EM

8.6

6.0

8.6 8.6

10.9

8.6

10.6

9.0 9.311.2

EA

STW

EST 19.1 17.1

8.3

21 Note: *Output figures are 100% basis**CV figures are air-dried basis

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14e 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14e 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14e

Indonesia Coal total costsCOMMENTS

Indonesia Coal: total costs4Q13 AND FY13 AVERAGE TOTAL COSTS

● Achieved lower total costs of $61/tonne in 4Q13 down from $67/tonne in 4Q12

ITM ti t d 70

80$74

$72$68

$65

$/t

$67$70

$64 ● ITM continue to reduce average strip ratios in 2013 to cope with lower coal price trend50

60

$65

SG&A expenses

Royalty

$62$64

$59 $61

● Continue to focus on cost reductions including implementation of cost reduction program such as 30

40 Other production costs*

Dep. & Amortisation

p gIPCC, renegotiate barging contract, fuel substitute, etc.

● IPCC will lower usage of diesel truck and shovel and use more 10

20

3

Mining and contractor cost

truck and shovel and use more electricity from owned power plant0

10

1Q 2Q 3Q 4Q Full year 1Q Full year2012 2012 2013 2013

2Q 3Q 4Q

22

* Coal transportations, repair and maintenance, salaries and allowance, etc.

China Coal gro ing coal o tp tCHINA COAL 2013 PRODUCTION TARGETS*

China Coal: growing coal outputOPERATIONAL UPDATES

Gaohe (45%),

GAOHE

● 2013 production 6Mt (above target 5Mt)

● Mining bolter was installed underground in Dec’13

BEIJING

Hebi

(45%),Shanxi 6.0 Mt

Summary 3Q13 4Q13 2012 2013Sales (Mt) 1.2 1.8 4.0 5.5ASP (RMB/t) 505 527 616 561Revenue (US$ M) 101 157 388 341COGS (RMB/t) 357 297 458 417Hebi

(40%),Henan1.2 Mt

OperationProjectOperationProject

POWERCOAL

HEBI

V il i h f i id i D b d

COGS (RMB/t) 357 297 458 417EBITDA (US$ M) 13 32 145 181

1.2 1.4 1.3 1.22.1 1.6

4Q12 – 4Q13 COAL OUTPUT (Mt ROM)● Ventilation shaft incident in December caused stoppage

to one LW unit; shaft was repaired; LW back to fullproduction since Jan’14

● Improvements to mine safety and planning withcontinued introduction of hazard mapping and geologic

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14e

GaoheCV 6 8 K l/k **

HebiCV 68 K l/k **

0.3 0.3 0.3 0.3 0.3 0.3

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14e

continued introduction of hazard mapping and geologicmodeling

● Degas improvement trials showed promising results forwater flushing and under-seam protection mining (UPM)

23

CV: 6500-8000 Kcal/kg** CV: 5300-6800 Kcal/kg**

Note: *Output figures are ROM output (100% basis)

**CV figures are air-dried basis

Mongolia Coal project de elopmentALTAI NUURS AND UNST KHUDAG PROJECTS

Mongolia Coal: project developmentTSANT UUL PROJECT

● Altai Nuurs Project:

Completed drilling test and plan to complete the PEA (Preliminary Economic Analysis) and PFS (Preliminary Feasibility Study) in 2014

COAL TAR

DIESELREFINER

COAL TO SEMI-COKE AND COAL TAR PILOT STUDY

(Preliminary Feasibility Study) in 2014OVENCOAL SEMI-

COKE

OFF GAS

COKING/ STEEL MAKING PLANT

CAPTIVE POWER PLANT

STEELOVEN

● Completed mine development

POWER PLANT

GRID?

● Completed mine development

● Completed small pilot tests with encouraging results on a potential coal to coal tar, off-gas and semi-coke plant

● Focus on larger scale test plants and product testing, i i d l M l h i l • Unst Khudag Project

Completed the updated Geological and Mining Models

aiming to develop c.0.5 Mtpa coal-to-chemicals commercial scale plant by 2015

● Currently testing the market in China; some trial lots have been sent to customers

24

Coal marketingCoal operationsStrategic review

321

Financial summaryPower business

54

25

N i th l t d f 2014

E i l USA i i

New emerging thermal trends for 2014SUPPLY TRENDS DEMAND TRENDS

Europe Continue power plant retirement, strong clean-dark spreads keep coal burn high

China Slower demand growth,

USA Continue retracting to domestic and HS bigger share of export

Colombia Drummond export ban in Q1,

-3 Mt +1-5 Mt

gpolitical / environmental issues, low quality coal import ban (?), high competition from domestic suppliers.

I di Hi h l i i d d

p Qpolitical, social/environmental issues continue

South Africa

Higher rail efficiencyContinuing political social

+5 Mt

+2 Mt

+1-5 Mt

India High electricity demand growth, insufficient domestic coal supply, focus LCV

Other Continue nuclear stoppage in

Africa Continuing political, social issues. Expand or not debatable

Indonesia Debating policies: export level, price levels tax levels DMO

+2 Mt

+15 Mt

+12 Mt

Other NorthAsia

Continue nuclear stoppage in Japan, coal still competitive in all north Asian countries

price levels, tax levels, DMO, losing market share for LCV, offshore loading, trading oversightConsiderable expansion (more

/ l )

+1-5 Mt

Others Other Asian and South Americas drive demand growth

LCV / less HCV)

Australia Encouraged by exchange rate Discouraged by prices and challenges for higher ash

d bl

+10 Mt +10 Mt

Considerable expansion

26

B ASP th l l b h k iBanpu ASPs vs thermal coal benchmark pricesBANPU ASP VS BENCHMARK PRICES COMMENTS

• Declines in ITM ASP are combination of continued market easing and product mixes

Unit: $/t

160

180

200

Monthly NEX

Quarterly ITM ASP

Q l C i l ASP • Tonnages remain high for shipment, protecting total revenues

• Centennial concluded sales of 3.7 Mt in 100

120

140

160 Quarterly Centennial ASP

4Q13 at ASP of A$71/t, down 4% QoQ in line with easing export prices and more domestic deliveries

40

60

80

100

• Reduced demurrage cost of Indonesia coal from $0.9/t in 2012 to $0.7/t in 2013, down 35%

ITM ASP US$ /

0

20

40

n-07

r-07

ul-07

ct-07

n-08

r-08

ul-08

ct-08

n-09

r-09

ul-09

ct-09

n-10

r-10

ul-10

ct-10

n-11

r-11

ul-11

ct-11

n-12

r-12

ul-12

ct-12

n-13

r-13

ul-13

ct-13

n-14

• ITM ASP 2013 US$75/t

• CEY ASP 2013 A$70/tITM ASP 4Q13 $71.0 (-2% QoQ)

CEY ASP 4Q13 A$70.6 (-3% QoQ)

Jan

Ap Ju Oc

Jan

Ap Ju Oc

Jan

Ap Ju Oc

Jan

Ap Ju Oc

Jan

Ap Ju Oc

Jan

Ap Ju Oc

Jan

Ap Ju Oc

Jan

27 * The Newcastle Export Index (previously known as the Barlow Jonker Index – BJI)

NEX* February 20, 2014 $77.0

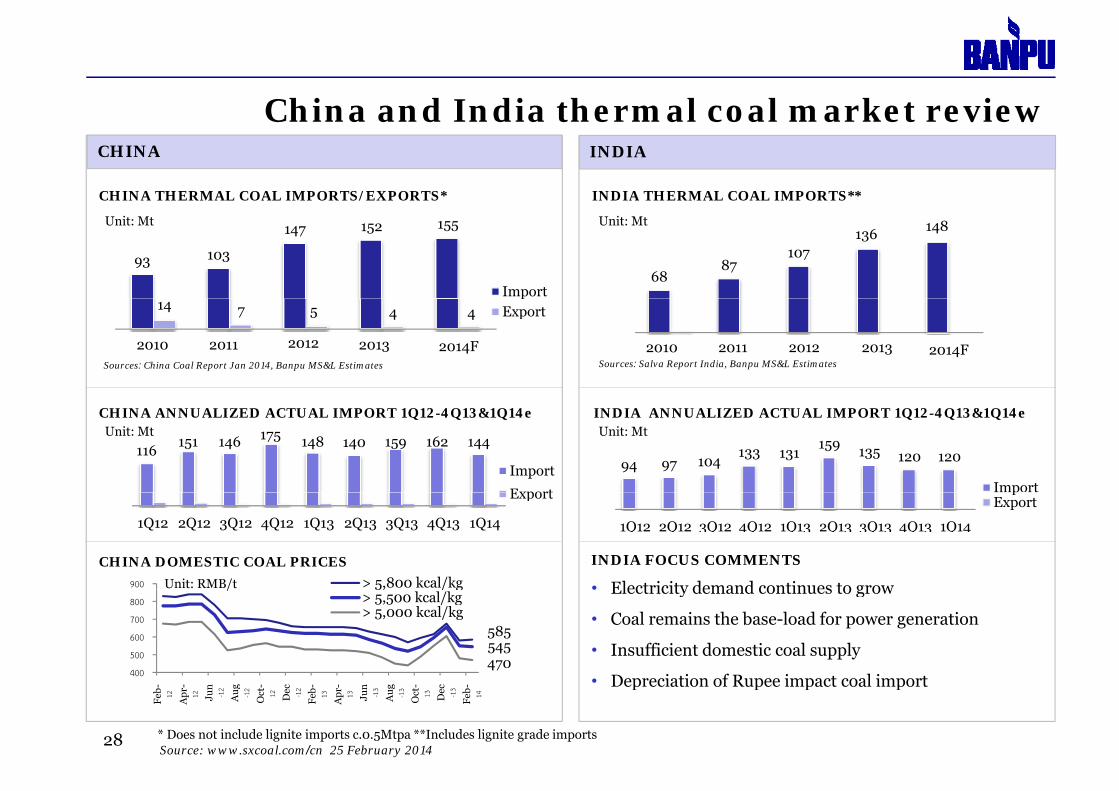

China and India thermal coal market re ieChina and India thermal coal market review

CHINA THERMAL COAL IMPORTS/EXPORTS* INDIA THERMAL COAL IMPORTS**

CHINA INDIA

/

93 103

147 155

Import

Unit: Mt 152 155

6887

107

148 136 148Unit: Mt

14 7 5 4 4

2010 2011 2012 2013 2014F

pExport

Sources: China Coal Report Jan 2014, Banpu MS&L Estimates

2010 2011 2012 2013 2010 2011 2012 2013 2014FSources: Salva Report India, Banpu MS&L Estimates

2010 2011 2012 2013

CHINA ANNUALIZED ACTUAL IMPORT 1Q12-4Q13&1Q14e INDIA ANNUALIZED ACTUAL IMPORT 1Q12-4Q13&1Q14e

116 151 146 148 140 159 162 144

Import

Export

94 97 104133 131

159 135 120 120

Import

Unit: Mt Unit: Mt175

CHINA DOMESTIC COAL PRICES

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14

Export

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14

pExport

900 > 5,800 kcal/kgUnit: RMB/t

INDIA FOCUS COMMENTS

• Electricity demand continues to grow

400

500

600

700

800

- - n g - c - - n g - c -

5, / g> 5,500 kcal/kg> 5,000 kcal/kg

/

585545470

• Electricity demand continues to grow

• Coal remains the base-load for power generation

• Insufficient domestic coal supply

• Depreciation of Rupee impact coal import

28

Feb- 12

Apr

-12 Ju

n-12

Au g -12

Oct

-12 De c -12

Feb - 13

Apr

-13 Ju

n-13

Au g -13

Oct

-13 De c -13

Feb - 14

Source: www.sxcoal.com/cn 25 February 2014

Depreciation of Rupee impact coal import

* Does not include lignite imports c.0.5Mtpa **Includes lignite grade imports

Banp gro p coal sales 2013 and 2014eBanpu group coal sales 2013 and 2014eCOAL SALES(1) 2013 : 45.7 Mt(2) COAL SALES(1) 2014e : 48.2 Mt(2)

2.90.1USA0.6 Mt

24%

6%

1%

Indonesia Coal

Australia Coal

China Coal

% of total sales 3.20.1

USA0.7 Mt

%

21%1%

JAPAN

S KOREA2.9 Mt

CHINA11.1 Mt

ITALY0.8 Mt

1.8

4.6

8.1 0.72.2

14%

8%

6%2%

JAPAN

S KOREA3.2 Mt

CHINA10.1 Mt

ITALY0.7 Mt

1.8

5.2

6.8 1.12.1

5%

7% 15%1%

6.4 Mt

THAILAND1.9 Mt

INDIA2.5 Mt

OTHERS0.8 Mt

HK0.3 Mt

TAIWAN3.7 Mt

2.01.7

0.30.5

5%

5%

5%1%

1%

7.0 Mt

THAILAND2.3 Mt

INDIA3.0 Mt

OTHERS1.9 Mt

HK0.4 Mt

TAIWAN2.6 Mt

1.80.8

1.50.4

6%5%

1%

5

4%

4%

PHILIPPINES2.2 Mt

INDONESIA3.2 Mt

9

MALAYSIA0.8 Mt

19%7%2% PHILIPPINES1.8 Mt

INDONESIA3.7 Mt

3

MALAYSIA0.7 Mt

1% 8% 21%

AUSTRALIA8.5 Mt

Total: 45.7 Mt (Sales from Indonesia are included on 100% basis,

l f A t li d Chi i l d d it b i )

AUSTRALIA10.1 Mt

Total: 48.2 Mt (Sales from Indonesia are included on 100% basis,

29(1) Excluding Mongolia coal

(2) Sales from Indonesia are included on 100% basis, sales from Australia and China are included on equity basis

sales from Australia and China are included on equity basis ) sales from Australia and China are included on equity basis )

Indicati e 2014 Banp coal sales pricing stat sIndicative 2014 Banpu coal sales pricing statusINDONESIA COALAUSTRALIA COAL

7% 9%

UnsoldIndexed

11%Domestic:

LegacyUnpriced1

Unsold 21%

Fixed 47%Unpriced

Fixed

53%

13%

7%

Fixed ExportDomestic: long-term

export parity Indexed20%

12%

TARGET SALES 2014 (equity basis): c.15.3 Mt b

TARGET SALES 2014: c. 30.7 MtA t F b As at 25 Feb 2014

Note:1JPU contracts comprise 10% of 11% of unpriced sales.

As at 25 Feb 2014

30

Coal marketingCoal operationsStrategic review

321

Financial summaryPower business

54

31

Thailand Po er BLCP in 2013Thailand Power: BLCP in 2013USD million

Q-Q : -40.4%Y Y %

Q-Q : -52.2 %Y Y 10 7%

Q-Q: -68.3%Y-Y : -13.1%Y-Y : -10.7%

Y-Y: +12.6%

7536

263 235

95

605 526

160

Availability Payment (AP)

Q-Q : -87.6%Y-Y : -15.8%

Total revenue

Q-Q : -31.8%Y-Y : -14.9%

73FX gain

823Q13 4Q13 2012 20132012 2013

310

3Q13 4Q13 2012 20132012 20137

Y Y : 15.8%

27

78 53

3Q13 4Q13

3264

7

3Q13 4Q13 2012 2013

176148

56

1

7581

9684

96 93

Energy Payment (EP)

Q-Q : -67.2 %Y-Y : -7.3%

EBIT8

FX

FX gain

3Q13 4Q13 2012 20132012 2013 3Q13 4Q13 2012 20132012 2013

26

3

1

5

884

3Q13 4Q13 2012 2013 Equity income

FX Loss

2012 2013

2012 20133Q13 4Q1324

3Q13 4Q13 2012 20132012 2013

244227

73

-8

3Q13 4Q13 2012 2013

32

Dispatch (%) EBITDA Based on Banpu’s 50% interest Equity income3 3Q13 4Q13 0 0 32012 2013

Th il d P H j t i LPROGRESS UPDATES 4Q13

Thailand Power: Hongsa project in LaosPROGRESS UPDATES 4Q12PROGRESS UPDATES 4Q12

115 COOLING TOWER 1ST115 COOLING TOWER 1S

UNIT 115 KV TRANSMISSION LINE

33Note: *Banpu’s equity injection US$340M from 2014-2016

Overall progress approx. 78% completeOverall progress approx. 40% complete

Hongsa project constr ction progressHongsa project: construction progress

COAL STOCKYARD BELT CONVEYOR COAL MINE

SUB-STATION PHASE SHIFT TRANSFORMER TRANSMISSION LINE

34

China Po er BIC* in 2013 (100% basis)Sales**

(USD m)

EBITDA

(USD m)

Utilization

(hours)

Power tariff

(RMB/kwh)

Coal price***

(RMB/t)BIC*

China Power: BIC* in 2013 (100% basis)

LuannanHebei Province

Power 100MW;

( ) ( ) ( ) ( / ) ( / )

0.44 0.43

511 498

1,54110.112.3

4.6

47.8

9.5

15.55,879 5,911

0.44 0.44

676515

48.7

Power 100MW;

Steam 128tph

(Banpu 100% )

Zhengding

1,2513.3 4.6

16.87 752

7,948630

3Q13 4Q13 2012 2013 3Q13 4Q13 2012 2013 3Q13 4Q13 2012 2013 3Q13 4Q13 2012 2013 3Q13 4Q13 2012 2013

ZhengdingHebei Province

Power 48MW;

Steam 180tph 1,748

2,311 0.41 0.408.3 13.8

2.45.5

484 465

45.7 13.7 7,752

0.40 0.40

630504

45.7

(100%)

Zouping

4

655 630

97.9

18.6

25.07,245

7,761 833

65293.7

3Q13 4Q13 2012 2013 3Q13 4Q13 2012 2013 3Q13 4Q13 2012 2013 3Q13 4Q13 2012 2013 3Q13 4Q13 2012 2013

p gShandong Province

Power 100MW;

Steam 430tph

(70%)

22.526.3 4.8 6.6

1,7872,162

0.43 0.42

18.6

0.44 0.43

Note: *BIC = Banpu Investment China (formerly BPIC),** Unaudited figures, *** Including transportation

(70%)

3Q13 4Q13 2012 201335

3Q13 4Q13 2012 2013 3Q13 4Q13 2012 2013 3Q13 4Q13 2012 2013 3Q13 4Q13 2012 2013 3Q13 4Q13 2012 2013

Coal marketingCoal operationsStrategic review

321

Financial summaryPower business

54

36

Ke e ternal and corporate e entsKey external and corporate eventsTony Abbot won the election to be new Australian prime minister

Moody’s and Fitch

Anti-government protest in Thailand

VE

NT

S

IND

IRE

CT U.S.

government shutdown

ADB lower

World Bank announced limits

lending for coal-fired

Syria chemical weapon threat

FED not to reduce QE

ywarned a potential credit downgrade if political unrest prolongs

THB falls

SET fell by 68 points and Baht

China’s dimmed GDP forecast (7.4%), reforms may slow growth to the lowest

XT

ER

NA

L

EV

T

Thailand’s 2013 economic growth to 3.8% from 4.9%

lending for coal fired power plants

• Positive economic Thermal coal dipped to 4-year

THB falls to 32/USD

and Baht weakened

Japanese power utilities agree to buy coal at $89/t

BHP cut 230 jobs at

Australian coal mine

the lowest since 1990

EX

DIR

EC

T

China increases export taxes on coking coal to 10%

Bushfire in Australia

impacts coal rail network

Positive economic data from China •Moody’s upgrade

US coal sector to STABLE

India to defer coal import

from Indonesia as Rupee falls

dipped to 4-year lows at $77/t

coal at $89/t (lowest since 2009)

coal mine

Indonesia to cap coal

output to 400 mt in 2014

EV

EN

TS

3Q13 Result announcement

2Q13 Result announcement

3Q13 4Q13 1Q14

4Q13 Result announcement

OR

PO

RA

TE

E announcement

3Q13 Analyst

meeting

3Q13 SET Opportunity Day

Bt5/share interim dividend paymentEnd of share

buy-back program of 5% ( illi

Share split announced EGM to

approve the share split

2Q13 Analyst

meeting

2Q13 SET Opportunity Day Banpu

Filing to the SEC; write-off of 135.6m shares between Mar 15-Sep 14, 2013

4Q13 Analyst meeting

Decrease in

announcement

Announced Bt0.70/share 2H dividend

4Q13 SET Opportunity Day

37

CO Change in par value

from Bt 10 to Bt 1(13.6million shares)

Announced Bt5/share interim

dividend

roadshow in Singapore

Decrease in Paid-up Capital

announced

Banp gro p Q Q re en e anal sis coal operationsBanpu group Q-Q revenue analysis: coal operationsIndonesia Coal (ITM)

SALES (Mt)Domestic 100% basis

China Coal

SALES (Mt) Equity basisDomestic

Australia Coal (Centennial)

SALES (Mt) Equity basisDomestic

7.6 6.5 6.1 6.7 6.8

6.6 7.1 6.9 7.5 7.6

Q Q Q Q Q

Export

0.7 0.7 0.7 0.7 0.9

Q Q Q Q Q

Export

1.7 1.6 2.5 1.8 2.5

3.3 2.9 3.8 3.2 3.7

Q Q Q Q Q

Export

4Q12 1Q13 2Q13 3Q13 4Q13

AVERAGE SELLING PRICE (US$/t)

NE

X*

86 93 86 78 84

AVERAGE SELLING PRICE (US$/t) excl. VAT

4Q12 1Q13 2Q13 3Q13 4Q13

NE

X*

86 93 86 78 84

4Q12 1Q13 2Q13 3Q13 4Q13

AVERAGE SELLING PRICE (A$/t)

NE

X*

86 93 86 78 84

REVENUE ($M)

ASP 81 80 77 73 71

4Q12 1Q13 2Q13 3Q13 4Q13

REVENUE ($M)

ASP 101 106 90 81 88

4Q12 1Q13 2Q13 3Q13 4Q13

78

REVENUE (A$M)

ASP 74 65 70 73 70

4Q12 1Q13 2Q13 3Q13 4Q13

78

REVENUE ($M)

653 563 527 543 545

100% basis REVENUE ($M)

154 161 133 126 186

100% basisREVENUE (A$M)

244 202 271 234 259

Equity basis

Note: ITM and Centennial revenues are consolidated in Banpu income statement.Australia Coal – Third party coal sales included.

4Q12 1Q13 2Q13 3Q13 4Q13

Note: ‘$’ in this presentation denotes US dollar only, otherwise stated

*NEX = Newcastle Export Index (formerly Barlow Jonker Index or BJI)

Note: Hebi and Gaohe revenues are not consolidated in Banpu income statement.

4Q12 1Q13 2Q13 3Q13 4Q134Q12 1Q13 2Q13 3Q13 4Q13

38

NEX Newcastle Export Index (formerly Barlow Jonker Index or BJI) It is relevant but not linked to China Coal’s ASP

Banp consolidated sales re en esBanpu consolidated sales revenuesUSD million

3,775

USD million

Power+5% Y Y

-11% Y –Y 3,351-13% Y –Y

+5% Q – Q 183

191 +5% Y - Y

Coal Australia-15% Y - Y

1,079

913

984Power+29% Q - Q+4% Y Y

Coal Indonesia

984809

Power

C l A t li

854

-11 % Y - YCoal Australia+12% Q - Q-4% Y - Y

+4% Y - Y2,513

2,247248

214 239

51 41 53

Coal Australia

Coal IndonesiaCoal Indonesia+1% Q- Q-18 % Y - Y

685 554 562

2012 2013

39 Note: Revenue from other is included in Coal.

4Q12 3Q13 4Q13 2012 20132012 2013

Banp consolidated coal gross margin 2013 32%Coal gross margin (weighted average) 4Q13: 32% Coal gross margin (weighted average) 2013: 32%

Banpu consolidated coal gross margin 2013 : 32%

USD million USD million

Indonesia gross margin: 35%Indonesia Coal

672

Australia gross margin: 25%Australia Coal

Indonesia gross margin: 36%Indonesia Coal

Australia gross margin: 23%Australia Coal

7

5455402,476

2,182

38%38%

248 239214

43%

1,079913

4Q12 3Q13 4Q13

35%38%

4Q12 3Q13 4Q13

25%29%27%

2012 2013

36%43%

2012 2013

23%30%

2012 2013 2012 2013

40 Coal sales Gross margin

4Q 3Q 3 4Q 3 4Q 3Q 3 4Q 3 2012 2013 2012 20132012 2013 2012 2013

Banp consolidated EBITDABanpu consolidated EBITDAUSD million USD million

68

974-16% Q –Q -20% Y –Y

-28% Y –Y

29

226

103

Power

Coal Australia

697+52% Y-Y

27

146 Coal China

Power -7% Y-Y+26% Q-Q

-35% Y-Y

651

42011 49

43 54

11 35 9

Coal Indonesia -35% Y-Y213

203Coal - Australia

Coal - China 171

+200% Q-Q

+26% Q-Q +10% Y-Y

Q Q+10% Y-Y

142 122 99

11 3 9 43 54

Q * Q Q *

Coal - Indonesia

-30% Y-Y

-18% Y-Y

-19% Q-Q

+200% Q Q

2012* 20134Q12* 3Q13 4Q13 2012* 2013

41 Power Coal Australia Coal China Coal Indonesia * Reflects new TFRS accounting policies

2012 2013

Banp consolidated NPATBanpu consolidated NPATUSD million

272USD million

8

26

42272

-32% Q –Q -71% Y –Y

103

-62% Y –Y

28

21

66FX• FX gains (Banpu)

+U$30M

Power

Coal China

103

+57% Y-Y

25% Y Y

81

202

110

7

3

21

2323

+U$30M• FX losses (CEY)

-U$7M

Coal Indonesia -46% Y-Y

7130

Coal Indonesia

Coal China

+0% Y-Y20 +133% Q-Q

-25% Y-Y

3967

-6 -18 -13

-67 -9

-2-2 -16

23

-27 Coal Australia

Coal Indonesia

Power

-93% Y-YCoal Australia +43% Q-Q

-85% Q-Q

+117% Y-Y n.m.

-27

4Q12* 3Q13 4Q13 2012* 2013

Power n.m. FX

• FX gains (Banpu) +U$25M• FX losses (CEY) -U$52M

2012* 20134Q 3Q 3 4Q 3 3

42 Power Coal Australia Coal China Coal Indonesia * Reflects new TFRS accounting policiesFX and derivative

3

Banp gearing and foreign e change str ct reGEARING RATIOS

Banpu gearing and foreign exchange structureDEBT FX STRUCTURE

Net debt / Equity1 (x)

THB Float2%

0.74 0.791.07

Net debt / Equity (x)

AUD Fixed

4%

2% THB Fixed14%

Net market gearing2 (%)

USD Float53%

USD Fixed27%

42% 45%52%

27%

Net debt / EBITDA (x)

3.99

TOTAL DEBT: $3.24 billionAs at 31 January 2014

2.052.52

3.99

2011 2012 20132011 2012 2013

43 Note: 1 Net debt to book value of shareholders' equity2 Net debt to enterprise value (enterprise value = net debt + market capitalization as at 31 December 2013)

2011 2012 20132011 2012 2013

Cape o tlook 2012 2015Capex outlook : 2012-20151,273340(1)USD million

1 00

200779

1 97

427 10037

1 23

269230

Capex FY12 13

Capex FY14-15494

Australia Total capexLaosIndonesia

146

MongoliaChina

Capex FY12-13

IPCC, BoCTexpansion, BunyutExpansion, etc

Newstan and Angus Place extension

China Power (BIC)

Tsant Uuldevelopment and Altai Nuurs

l ti

Capex from Hongsaproject in 2014-2016

44 * Capex figures exclude maintenance capex Disclaimer: all capex figures are indicative only and are subject to change(1) Includes 2016 Hongsa equity injection

exploration

Change in acco nting standard Indonesia coalCOMMENTS

Change in accounting standard: Indonesia coal

1 Cash basis

4. IFRIC 20/ISAK29IFRIC 20 : MINING COSTCURRENT PRACTICESBased on LOM S/R, production and reservesS/R ILLUSTRATIVE ONLY

● IFRIC 20 – Stripping costs in the production phase of a surface mining

● Stripping costs, which

1. Cash basis*New practice to be applied for all ITM mines

8.0 8.4 8.2 8.7 4.2 S/R7.0

11.8

3.5

8.09.0

Avg. 8.0

Stripping costs, which provides an improved access benefit to ore/ coal is recognized as an asset

● Effective date: January 1

2. Life of mineBased on LOM S/R

Avg. 8.0

121 2.5 3.5ROM

8.0 8.0 8.0 8.0 8.0S/R

● Effective date: January 1, 2014

● Compulsory for all mining companies with surface

i

Amort.(year 1)

Amort.(year 2)

• Jorong

Avg. 8.0

S/R

mines● Change in accounting

policy (retroactive and require restatement)• Capitalized O/B if there is future benefit

2.01.0 2.5 1.03.53. Betterment

ROM

Based on S/R attributable to coal inventory

8.9 7.5 7.9 4.011.6S/R

• Td.Mayang

ROM

● First result will be shown in 1Q14 statements

Capitalized O/B if there is future benefit (e.g. access to coal)

• O/B above LOM avg. is capitalized• Capitalized O/B is amortized according to

production and remaining reserves by pit• Indominco

• Trubaindo

• Embalut

coal inventory

45 Note: charts not drawn to scale. IFRIC stands for International Financial Reporting Accounting Interpretation Committee, ISAK stands for Interpretation of Financial Accounting Standard

• Bharinto ROM

Change in acco nting standard BLCPCOMMENTS

Change in accounting standard: BLCPTFRIC4 ADJUSTMENTS FOR BLCP INCOME

● TFRIC 4 – Determining whether an arrangement contains a lease

● Effective date: January 1 2014APR1: Availability Payment for investment cost

Adjustment :

APR

EXISTING REVENUE

TARIFF BASED INCOME

TFRIC 4

LEASE BASED INCOME

● Effective date: January 1,2014

● PPA is considered as a lease

● Treats capacity utilization as a ‘lease rental’

1

- APR1

+ Interest income

+ Depreciation

+/ Gain(loss) on FX lease rental

● Potential impact:

o Smooths revenue and net income curve over long

APR2: Availability Payment for power plant maintenance2 No adjustment

+/- Gain(loss) on FX

term

o No change to cash flows and tax treatment

EP :

Energy payment for fuel cost3 No adjustment

VOM :

Variable operating and maintenance

4 No adjustment

46

A diAppendices

47

Banp gro p indicati e fi e ear plan o tp t targetsINDONESIA COAL: SALEABLE COAL 100% BASIS

Banpu group indicative five-year plan output targetsAUSTRALIA COAL: SALEABLE EQUITY BASIS

25

30

35

Bharinto JorongEmbalut

* **

Mt

25

30

35Mt

10

15

20 Trubaindo

Others - WestSpringvale (50%)Angus Place (50%)Others - North

10

15

20

0

5

2012 2013 2014 2015 2016

Indominco

* Tandung Mayang

Others - NorthNewstan Ext (100%)Mandalong (100%)

0

5

2012 2013 2014 2015 20162012 2013 2014 2015 2016 2012 2013 2014 2015 2016

MONGOLIA COAL: SALEABLE 100%BASISCHINA COAL: SALEABLE COAL EQUITY BASIS

Tandung Mayang

10 10

MtMt

0

5

2012 2013 2014 2015 2016

Gaohe (45%)Hebi (40%)

0

5

2012 2013 2014 2015 20162012 2013 2014 2015 20162012 2013 2014 2015 2016

48 Disclaimer: These output targets are indicative only and are subject to change.

2012 2013 2014 2015 20162012 2013 2014 2015 20162012 2013 2014 2015 2016

Indonesia Coal gross margin 4Q13 35%Indonesia Coal gross margin 4Q13 : 35%USD million

672

545333

672

540

259258

228

38%

179160

35%38%

38%

40%37%

37%

34%

36%

31%

53%

29% 25%19 14 16 52% 20

54% 32% 34%

28 1717

52

47%

48%52%

53

37%40%

51%38 39

25

34%

4Q12 3Q13 4Q13

Indonesia Coal

4Q12 3Q13 4Q13

Indominco

4Q12 3Q13 4Q13

34 31%

Trubaindo

4Q12 3Q13 4Q13

Jorong

29% 30% 25%

4Q12 3Q13 4Q13

3 34

Kitadin

4Q12 3Q13 4Q13

Bharinto

48%

4Q12 3Q13 4Q13

TandungMayang

34%

49

g Mayang

B EBITDA b kdBanpu group EBITDA breakdown

& holding companies

Unit: $M 148 175 203 171

-3 -3 -3 -399 88 114 102

Power & New energy

companies

65%AACI OVERHEAD

100%

1162 43 43 -2 -2 -3 -2

Unit: AUD Mil

1Q13 2Q13 3Q13 4Q13

46 43 34 5851 46 21 65

58 72 7324

50%

45%

Gaohe

BLCP

IndomincoAll figures are 100% basis except for Centennial

1Q13 2Q13 3Q13 4Q13 1Q13 2Q13 3Q13 4Q13 1Q13 2Q13 3Q13 4Q13 1Q13 2Q13 3Q13 4Q13

1Q13 2Q13 3Q13 4Q13

1Q13 2Q13 3Q13 4Q13

18 19 12 16 -4 -2 -1 -4

2 0

-2

1

40%

40%

Hebi

HONGSATrubaindo

which is equity basis

Bharinto

Q 3 Q 3 3Q 3 4Q 31Q13 2Q13 3Q13 4Q13

1Q13 2Q13 3Q13 4Q13

1Q13 2Q13 3Q13 4Q131Q13 2Q13 3Q13 4Q13

9 10 12 0

70%

BIC*

Kitadin

17 13 10 14

Bharinto

1Q13 2Q13 3Q13 4Q13

1Q13 2Q13 3Q13 4Q13

2

1

1 1

19 16 13 20

Jorong

N ll hi % l h i h

Zouping

7 6 5 7

Zhengding

6 3 2 6

Luannan

4 3 3 5

1Q13 2Q13 3Q13 4Q13

1Q13 2Q13 3Q13 4Q13 1Q13 2Q13 3Q13 4Q13 1Q13 2Q13 3Q13 4Q13

50

-1 Note: all ownership 100% unless otherwise shown.*BIC = Banpu Investment China (formerly BPIC) Consolidated NOT consolidated

1Q13 2Q13 3Q13 4Q13

Banp gro p net debt breakdo nBanpu group net debt breakdown

2,484 2,469 2,482 2,500 Unit: $M

& holding companies

1Q13 2Q13 3Q13 4Q13

AUSTRALIA COAL INDONESIA COAL CHINA COAL MONGOLIA COAL100% 65% 45% 40% 100%

318 224 192 155

4Q131Q13 2Q13 3Q13

Gaohe Hebi

548 631 687 667-496 -400 -418 -289

-40 -24 -18 -19 -5 -5 -7 -5Unit: AUD Mil

4Q131Q13 2Q13 3Q13 4Q131Q13 2Q13 3Q13 4Q131Q13 2Q13 3Q13 4Q131Q13 2Q13 3Q134Q131Q13 2Q13 3Q13

THAILAND POWER LAOS POWER CHINA POWER

HONGSABLCP BIC*

50% 40% 100%

4Q131Q13 2Q13 3Q13 4Q131Q13 2Q13 3Q13 4Q131Q13 2Q13 3Q13 4Q131Q13 2Q13 3Q13

1201 1286 1472 1686

HONGSABLCP BIC*Consolidated

NOT consolidatedNet debt

Net cash

574 557 506 490 -4

1 3

-15

4Q131Q13 2Q13 3Q13 4Q131Q13 2Q13 3Q13 4Q131Q13 2Q13 3Q13

51 Note: all ownership 100% unless otherwise shown.*BIC = Banpu Investment China (formerly BPIC)

Net cash

B lid t d ti fitBanpu consolidated : operating profit

Units: USD million YoY%

-11%Total sales revenues*

2013

3,351

2012

3,775

Sales revenues – Power (BIC)

Cost of sales

Sales revenues – Coal -12%

5%191

(2,276)

3,128

183

(2,332)

3,555

Gross profit* -25%

Gross profit - Coal -27%

Gross profit – Power (BIC) 67%

1,075

1,008

52

1,443

1,387

31

GPM

p ( )

GPM P (BIC)

GPM - Coal

7

32%

5

%

32%

38%

3

%

39%

GPM – Power (BIC) 27% 17%

52 Note: * Including other business

B lid t d ti fitBanpu consolidated: operating profit

Units: USD million

Gross profit -25%GPM

YoY%

1,07532%

2013

1,44338%

2012

GPM

SG&ARoyalty

Income from associates

32%

(402)(325)

95

38%

(448)(383)

86Other income

EBIT 36%

Income from associates

Other expenses - Operations57

471

95

(30)

63

740

86

(21)EBIT -36%

EBITDA 28%

EBIT - Coal -45%EBIT - Power 72%

471

697

38091

740

974

68753

EBITDA -28%

EBITDA - Coal -34%EBITDA - Power 51%

697

594103

974

90668

53

B lid t d t fitBanpu consolidated : net profit

Units: USD million

EBIT -36%

YoY%

471

2013

740

2012

Interest expensesFinancial expenses

Mi itiIncome tax (core business)

(116)(11)

( )(104)

(112)(11)

( )(183)

Minorities

Non-recurring items*

I ( b i )

Net profit before extra items(85)

(39)

155 -45%(152)

0

283

Income tax (non - core business) (21)

Net profit before FX -57%130

Deferred tax income (expenses) 35(14)

298

30

FX translations

Net Profit -62%

(27)

103

EPS (USD/share) 0.04

(27)

272

1.00

54 Note: * Income from non-core assets and other non-operating expenses

( / ) 4

B lid t d ti fitBanpu consolidated : operating profit

Units: USD million

Total sales revenues*

YoY%

-13%

3Q13

809

4Q12

983

QoQ%

5%

4Q13

854

Sales revenues – Power (BIC)

Cost of sales

Sales revenues – Coal -14%

4%41

(526)

760

51

(648)

920 4%

29%53

(580)

793

Gross profit*

Gross profit - Coal

Gross profit – Power (BIC)

-18%

-21%

69%

284

271

9

336

321

9

-4%

-6%

71%

274

255

15

GPM

p ( )

GPM P (BIC)

GPM - Coal

9

35%

9

%

36%

34%

9

8%

35%

7

32%

5

%

32%

GPM – Power (BIC) 22% 18%29%

55 Note: * Including other business

B lid t d ti fitBanpu consolidated: operating profit

Units: USD million

Gross profitGPM

-18%

YoY%

28435%

3Q13

33634%

4Q12

27432%

4Q13

-4%

QoQ%

GPM

SG&ARoyaltyIncome from associates

35%

(93)(81)

29

34%

(122)(105)

17

32%

(97)(82)

7 Other income

EBIT

Income from associates

26%

Other expenses - Operations13

144

29

(7)28

143

17

(10)

11

105

7

(7)

27%EBIT

EBITDA

EBIT - CoalEBIT - Power

-26%

20%

-27%-17%

144

203

11727

143

213

1376

105

171

1005

-27%

16%

-15%-81%

EBITDA

EBITDA - CoalEBITDA - Power

-20%

-20%-18%

203

16835

213

20211

171

1629

-16%

-4%-74%

56

B lid t d t fitBanpu consolidated : net profit

Units: USD million

EBIT -26%

YoY%

144

3Q13

143

4Q12

105

4Q13

-27%

QoQ%

Interest expensesFinancial expenses

Mi itiIncome tax (core business)

(30)(3)

( )(29)

(29)(2)

( )(33)

(30)(3)

( )(24)

Minorities

Non-recurring items*

I ( b i )

Net profit before extra items -46%(22)

(20)

60(23)

(17)

57

(17)

(31)

31 -48%

Income tax (non - core business)

Net profit before FX -104%

Deferred tax income (expenses)

-

40

0

-

73

32

(8)

(3)

(6)

-108%

FX translations

Net Profit

EPS (USD/share)

-71%

(10)

30

0 012

(2)

71

0 26

23

20

0 008

-32%

57 Note: * Income from non-core assets and other non-operating expenses

EPS (USD/share) 0.012 0.260.008

C t i l I St t tUnits: USD million 2013 YoY%

S l l ( )

2012

Centennial : Income Statement

Cost of sales

-5%

Sales revenue

Sales volume (Mt)

-15%(751.25)

14.30

1,079.03(699.42)

13.59

913.38

Gross profit -35%GPM SG&A -17%

327.7830%

( )(186.44)

213.9723%

( )(155.56)

Royalty -21%

%EBIT

Other income 30%

(75.01)

68 8

22.98(58.96)

( 8 )

29.84Other expenses (20.46)(30.16) 47%

-101%EBIT

Interest expensesFinancial expenses

68.85

(25.56)

(5.80)

(0.87)

(26.33)

(5.76)Gain (loss) on exchange rate 5 34(52 40)Gain (loss) on exchange rate 5.34(52.40)

Corporate income tax 0.55-Gain (loss) on derivative 57.9518.38

Deferred tax -17.69 Net profit -149%101.33(49.30)

58

7 69

C t i l I St t tUnits: USD million

S l l ( )

4Q12

Centennial : Income StatementYoY%QoQ%4Q13 3Q13

Cost of sales

G fi

Sales revenue

Sales volume (Mt)

(179.87)

3.297

248.05

11%

-4%

14%

12%(180.50)

3.659

239.29(153.21)

3.214

214.37

Gross profit GPM

R ltSG&A

68.1827%

(17 03)(48.06)

-14%

-26%10%

-4%

-6%%

58.7825%

(15 33)(35.56)

61.1529%

(14 37)(37.75)

Royalty

EBIT

Other income(17.03)

2 05

Other expenses

-10%

464%

19%

-29%

9.19

(10.23)

7%

70%

131%

4%

(15.33)

11 56

10.91

(7.24)

(14.37)

6 81

4.73

(6.96)EBIT

Interest expensesFinancial expenses

G i (l ) h t

2.05

(6.50)

(2.13)

(1 43)

464%70%11.56

(6.57)

(1.62)

(6 58)

6.81

(6.40)

(1.34)

0 99Gain (loss) on exchange rate

fi

Gain (loss) on derivative

(1.43)

18.23

Deferred tax income -

(6.58)

0.33

0.45

0.99

0.29

-

Net profit 10.24

59

n.m.n.m.(2.44) 0.36

A stralia Coal q arterl eq it ROM o tp t Australia Coal: quarterly equity ROM output

Total equity ROM (Mt)ACTUAL PLANNED (INDICATIVE ONLY)

8

4.2

3.13.7 3.6

3.3

4.4

3.63.54.04.55.0

ACTUAL PLANNED (INDICATIVE ONLY)

ER

N

1 9 1 6

1.3

2.51.2 2.0 2.1 1.7

2.71.9

2.83

1 01.52.02.53.03 5

TER

NN

OR

THE

R

1.5 1.7 1.9 1.7 1.5 1.6 1.7 1.7

0.00.51.0

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14

WE

ST

6 wks

7 wks 3

2013 2014

6 ks

3

Normal production Bolt-up/commissioning LW relocation

6 wks

5 wks

60 Note: Bar width is indicative of the equity production contributions to CentennialNote 2: Production generally responds to the timing of longwall changeovers (i.e. lower production results during a longwall changeover period)