investor newsletter - e.l. & c. baillieu limited€¦ · investor newsletter april 2019. 2...

TRANSCRIPT

Investor NewsletterApril 2019

baillieu.com.au2 Baillieu

From the CEO

It has been a volatile six months since our last newsletter, with markets across the globe tumbling in the final quarter of 2018 before rallying in the opening months of the New Year.

Locally, we awaited the outcome of the banking royal commission and with that now completed, we look toward the upcoming federal election. While the recommendations of the royal commission had little impact on equity markets, the result of the election is likely to – if it hasn’t already been priced in – due to the likelihood we will have a Labor government ruling from Canberra in less than two months’ time.

Looking further abroad, concerns surrounding US-China trade tensions and high equity valuations, among other things have dissipated, for now at least, though they have since been replaced by broader concerns about the health of the global economy. Continued uncertainty around Brexit has not helped.

We remain of the view that the Australian economy is likely to lag the rest of the world, with falling house

prices impacting economic activity. For this reason, we continue to recommend clients to look offshore for growth opportunities and in the process diversify their portfolios.

At Baillieu, there has been plenty of activity with the recent reporting season and dozens of company presentations having taken place in our offices. Our staff have also conducted a number of presentations across the country, from Melbourne to Perth and Geelong to the Gold Coast.

We also eagerly await our Melbourne office move to the eastern end of Collins Street, which should take place in the next couple of months.

I hope you enjoy this edition of our newsletter.

Gavin Powell CEO/Managing Director, Baillieu

Please read the disclaimer at the end of this report 3Investor Newsletter 3

Help us to save paper and the planet by electing to receive your copy of the Investor Newsletter by email. Contact your adviser to update your details.

Contents

4 CIO, Malcolm Wood

6 Asset Allocation

8 Financial Planning

10 Baillieu SMSF Solution

12 Fixed Income

13 Banks

14 Energy

16 Resources

18 Consumer Staples

19 Telecoms

20 Stock Focus

21 International

22 Listed Investment Companies

23 Corporate

24 Financial Advisers

27 Disclaimer

baillieu.com.au4 Baillieu

Four global themes for 2019

The global economy surprisingly softened in 2018, impacted by a combination of political and trade uncertainty, central bank tightening, higher oil prices and downturns in select emerging markets, such as Turkey and Argentina.

Looking to the remainder of 2019, we present four global themes that we believe will play out: i) a US soft landing over a hard landing; ii) an inflection point in central bank policy; iii) a decline in political and trade uncertainty; and iv) a valuation extreme.

Theme #1 - US soft landing over hard landing: The usual drivers of a US downturn are absent – tight Federal Reserve policy, financial or asset price excesses, or a commodity shock. Household, business and housing fundamentals appear robust. Most concerning is the yield curve. A “fiscal cliff”, as the fiscal stimulus ends in 2020, or an external shock could hurt the US but would lead to a quick easing of Fed policy.

Theme #2 - Central bank policy inflection point: After lifting rates and moving away from quantitative easing over the past 1-2 years, the major central banks have reversed policy course. The US Fed has indicated it plans to lift rates just once in the next three years and also plans to end Quantitative Tightening in September. The European Central Bank has extended its unchanged policy guidance through year-end and promised to restart targeted longer-term refinancing operations. The Bank of Japan has kept its ultra-accommodative policies and China’s People Bank Of China has continued its gradual pace of easing. Overall, real rates should stay at low levels (Figure 2).

Theme #3 - Trade and political uncertainty to moderate: Deadlines loom on US-China trade negotiations and Brexit. Resolution would reduce uncertainty. The election calendar has no major G5 elections over the next 18 months, with elections in India, Canada, Australia and Indonesia the most important this year.

Theme #4 - Valuation supportive: Whilst equities have rebounded in 1Q19, bond yields and cash rates have remained at very low levels. Equity valuations versus bonds remain attractive.

CIO, Malcolm WoodGlobal and domestic themes for 2019

Fig.1

Source: Datastream, Baillieu

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15 Jan-17 Jan-19

US Employment & Real Wages Growth

US Jobs 3M YoY% US Real AHE 3M YoY% US Agg Hours 3M YoY%

Fig.2

Source: Datastream, Baillieu

-4.00

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

Jan-88 Jan-92 Jan-96 Jan-00 Jan-04 Jan-08 Jan-12 Jan-16

Real Official Cash Rates: US, EUR, JPN, AUS

US Fed Funds JPN Policy Rate ECB Refi Rate RBA Cash Rate

Fig.3

Source: Datastream, Baillieu

-450

-400

-350

-300

-250

-200

-150

-100

-50

0

50

1Q99 1Q02 1Q05 1Q08 1Q11 1Q14 1Q17

US$

bn a

r

US Trade Balances by Major Trading Partner

China Canada Japan Mexico EU-28 OPEC

Please read the disclaimer at the end of this report 5Investor Newsletter

Four Australian themes for 2019

Australia faces deepening challenges in 2019, whether it be the highly risky housing downturn now underway, an intensifying squeeze on households, unusually elevated political risks, or the significant AUD downside risks.

Theme #1 - Early stages of the housing downturn: Whilst home prices and dwelling approvals are down 8.2% YoY and 21.1% YoY respectively (Figure 4), we see substantial further downside for six reasons - oversupply, overvaluation, overleverage, overspeculation, political risk and limited policy flexibility. We see home prices falling 15-20% in total and approvals 50%.

Theme #2 - The household squeeze to intensify: Headwinds are intensifying, reflecting low wages growth, rising interest and debt burdens, tax bracket creep (though this will ease in FY20) and, critically, an inflection point in household savings as the housing downturn deepens (Figure 5).

Theme #3 - Elevated political risk: ALP domination of opinion polls points to a landslide election victory (Figure 6). After the election, political risk will remain high as the ALP’s anti-investor policy agenda is legislated. Australia’s risk premia could rise, particularly hurting bank funding costs. Underweight Australian assets.

Theme #4 - Further Australian dollar downside risks: Despite a decline of 9.7% in 2018, record negative rate spreads, deteriorating relative growth, large foreign debt at 57% of GDP and political risks all point to continuing downside.

From an investment perspective, we are overweight international equities, particularly Japan, but also Europe and emerging markets. Within our Australian portfolios we are overweight Australian ‘global leaders’ such as Macquarie, QBE, ResMed, Sonic Healthcare, Brambles, Woodside Petroleum, BHP, Amcor and James Hardie.

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Q1 2003 Q1 2005 Q1 2007 Q1 2009 Q1 2011 Q1 2013 Q1 2015 Q1 2017 Q1 2019

AUS Major City Home Prices YoY%

AUS SYD MEL BRI PER

Fig.4

Source: Datastream, Baillieu

Fig.5

Source: Datastream, Baillieu

-2.0

0.0

2.0

4.0

6.0

8.0

10.0-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

Dec-91 Dec-03 Dec-15

AUS Home Prices and Saving Rate

AUS Home Price YoY% (Left) AUS H/H Saving Rate (%, Right)

Fig.6

Source: Datastream, Baillieu

40

42

44

46

48

50

52

54

56

58

Sep-13 Jun-14 Dec-14 Aug-15 Mar-16 Oct-16 Jun-17 Feb-18 Aug-18

AUS Two-Party Preferred Newspoll

ALP Coalition

Election 2013

Election 2016

Turnbull PM

Morrison PM

baillieu.com.au6 Baillieu

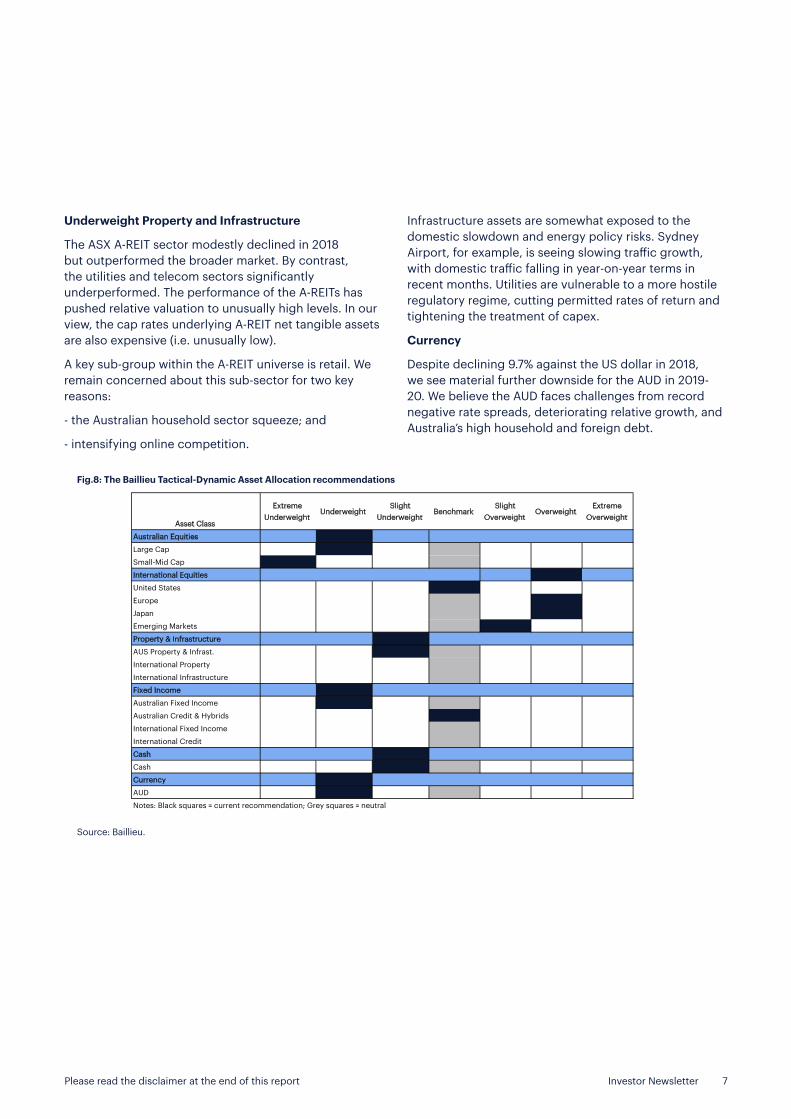

Asset AllocationRemain overweight international equities

Overall, our tactical-dynamic asset allocation recommendations are to remain overweight international equities and underweight Australian equities, property, fixed income, cash and the Australian dollar (Figure 8).

The global economy slowed more than expected in 2018, impacted by a combination of heightened political and trade uncertainty, central bank tightening, higher oil prices and downturns in some emerging markets (EM). This drove an equity market correction and bond market rally in 4Q18. For the year, global equities fell 10.4% in US dollars, or 0.7% in AUD-terms, while bond markets yielded modestly positive returns. Crude oil and major base metal prices fell 17-25% YoY.

Asset allocation for 2019Equities

Equities – overweight International: With neutral-to-attractive valuations, significant improvements in liquidity conditions, a US-led soft landing and a forecast moderation in current high levels of trade and political uncertainty, we see international equities as attractive.

Within international equities we prefer Japan given extreme valuation, positive earnings momentum and ongoing liquidity support. Our positive views on EM and Europe, which lack the earnings positives of the US and Japan, need the catalysts of effective China policy easing – early signs of this are appearing – and reduced trade and political uncertainty. We are positive on the US but see more upside elsewhere.

Underweight Australia: Valuation in absolute terms, and relative to other equity markets, is neutral-to-unattractive (Figure 7). Earnings momentum is likely to continue to deteriorate as the domestic slowdown becomes increasingly apparent. While liquidity conditions remain supportive, the RBA appears reactive – as opposed to pre-emptive – to the housing downturn and consumer slowdown.

Underweight Fixed Income

We continue to recommend an underweight position in Fixed Income. Generally speaking, bonds remain expensive in absolute and relative terms, and in the major economies growth indicators and inflationary pressures are higher than bonds are discounting. That said, central banks are supportive and with the end of quantitative tightening, bond supply is moderating.

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

Jan-88 Jan-92 Jan-96 Jan-00 Jan-04 Jan-08 Jan-12 Jan-16

AUS-US PE Relative

AUS-US 12MF PE Relative

Fig.7

Source: Datastream, Baillieu

Please read the disclaimer at the end of this report 7Investor Newsletter

Underweight Property and Infrastructure

The ASX A-REIT sector modestly declined in 2018 but outperformed the broader market. By contrast, the utilities and telecom sectors significantly underperformed. The performance of the A-REITs has pushed relative valuation to unusually high levels. In our view, the cap rates underlying A-REIT net tangible assets are also expensive (i.e. unusually low).

A key sub-group within the A-REIT universe is retail. We remain concerned about this sub-sector for two key reasons:

- the Australian household sector squeeze; and

- intensifying online competition.

Infrastructure assets are somewhat exposed to the domestic slowdown and energy policy risks. Sydney Airport, for example, is seeing slowing traffic growth, with domestic traffic falling in year-on-year terms in recent months. Utilities are vulnerable to a more hostile regulatory regime, cutting permitted rates of return and tightening the treatment of capex.

Currency

Despite declining 9.7% against the US dollar in 2018, we see material further downside for the AUD in 2019-20. We believe the AUD faces challenges from record negative rate spreads, deteriorating relative growth, and Australia’s high household and foreign debt.

Fig.8: The Baillieu Tactical-Dynamic Asset Allocation recommendations

Source: Baillieu.

Asset Class

Extreme Underweight

UnderweightSlight

UnderweightBenchmark

Slight Overweight

OverweightExtreme

Overweight

Australian Equities

Large Cap

Small-Mid Cap

International Equities

United States

Europe

Japan

Emerging Markets

Property & Infrastructure

AUS Property & Infrast.

International Property

International Infrastructure

Fixed Income

Australian Fixed Income

Australian Credit & Hybrids

International Fixed Income

International Credit

Cash

Cash

Currency

AUD

Notes: Black squares = current recommendation; Grey squares = neutral

baillieu.com.au8 Baillieu

Financial PlanningFranking credits

#1: Franking creditsWe have written a number of pieces on this issue, including in ‘Taking Stock’ (24 October 2018) and the ‘First Quarter FY19 Quarterly Review’. However, with considerable confusion around the potential loss of franking credits, it is an important issue worthy of further discussion.

Franking credits are generated when a company pays tax and are distributed to shareholders through their dividend payments. This helps avoid company profits being taxed twice – firstly, when the company pays tax on profits and secondly, when the shareholder adds the dividend income to their taxable income. In circumstances where a taxpayer’s franking credits received exceed their tax payable, they are entitled to receive a refund of this amount. Not surprisingly, this has led many retirees and investors to target franked dividends to top up their income.

It is the process of receiving a refund of any excess franking credits that the ALP has proposed to change. Below we have summarised the ALP’s proposal:

• removal of the ability to receive a refund for excess franking credits. Franking credits may still be used to reduce taxable income to $0, but any excess will no longer be refundable;

• charities and not-for-profits (NFPs) will be exempt;

• a subsequent adjustment (“Pensioner Guarantee”) to the proposal was announced to exempt full- and part-pensioners (as at 28 March 2018). This exemption extends to SMSFs where one member is currently in receipt of a Centrelink/Department of Veterans’ Affairs (DVA) pension; and

• the policy will apply from 1 July 2019 (according to the proposal and assuming it is legislated).

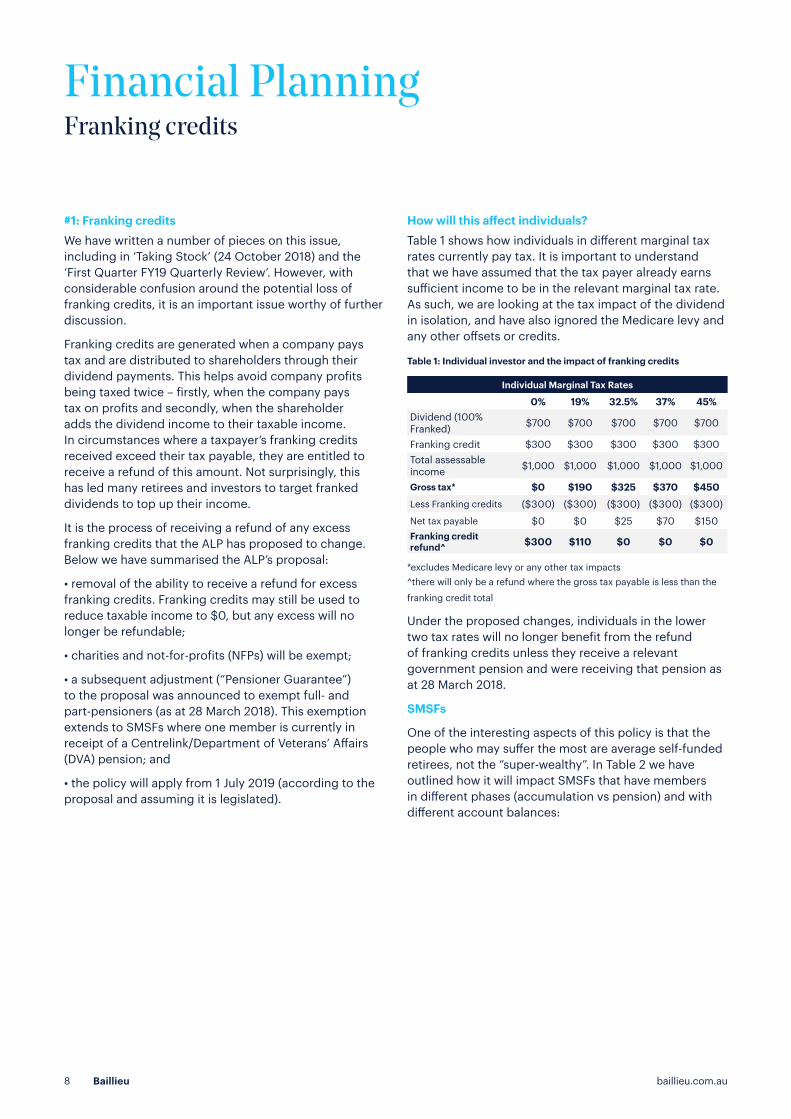

How will this affect individuals?Table 1 shows how individuals in different marginal tax rates currently pay tax. It is important to understand that we have assumed that the tax payer already earns sufficient income to be in the relevant marginal tax rate. As such, we are looking at the tax impact of the dividend in isolation, and have also ignored the Medicare levy and any other offsets or credits.

Table 1: Individual investor and the impact of franking credits

*excludes Medicare levy or any other tax impacts^there will only be a refund where the gross tax payable is less than the

franking credit total

Under the proposed changes, individuals in the lower two tax rates will no longer benefit from the refund of franking credits unless they receive a relevant government pension and were receiving that pension as at 28 March 2018.

SMSFs

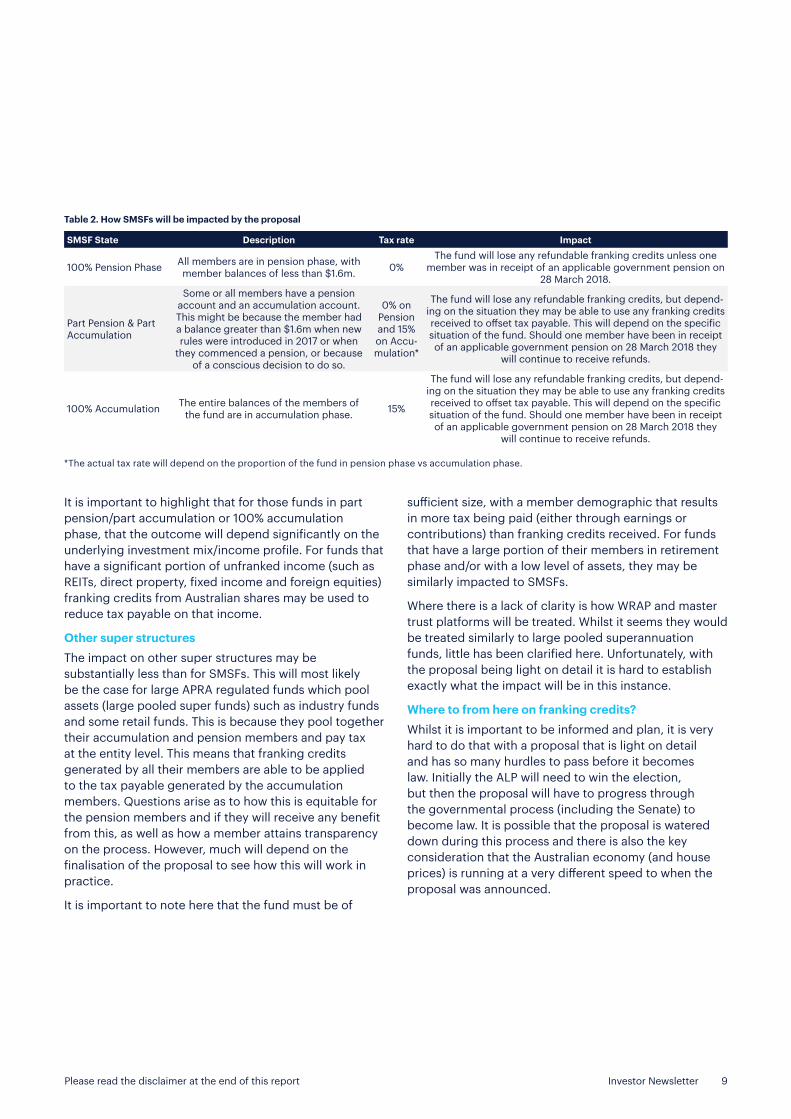

One of the interesting aspects of this policy is that the people who may suffer the most are average self-funded retirees, not the “super-wealthy”. In Table 2 we have outlined how it will impact SMSFs that have members in different phases (accumulation vs pension) and with different account balances:

Individual Marginal Tax Rates

0% 19% 32.5% 37% 45%Dividend (100% Franked) $700 $700 $700 $700 $700

Franking credit $300 $300 $300 $300 $300Total assessable income $1,000 $1,000 $1,000 $1,000 $1,000

Gross tax* $0 $190 $325 $370 $450Less Franking credits ($300) ($300) ($300) ($300) ($300)

Net tax payable $0 $0 $25 $70 $150Franking credit refund^ $300 $110 $0 $0 $0

Please read the disclaimer at the end of this report 9Investor Newsletter

SMSF State Description Tax rate Impact

100% Pension Phase All members are in pension phase, with member balances of less than $1.6m. 0%

The fund will lose any refundable franking credits unless one member was in receipt of an applicable government pension on

28 March 2018.

Part Pension & Part Accumulation

Some or all members have a pension account and an accumulation account. This might be because the member had a balance greater than $1.6m when new rules were introduced in 2017 or when

they commenced a pension, or because of a conscious decision to do so.

0% on Pension and 15% on Accu-mulation*

The fund will lose any refundable franking credits, but depend-ing on the situation they may be able to use any franking credits received to offset tax payable. This will depend on the specific situation of the fund. Should one member have been in receipt of an applicable government pension on 28 March 2018 they

will continue to receive refunds.

100% Accumulation The entire balances of the members of the fund are in accumulation phase. 15%

The fund will lose any refundable franking credits, but depend-ing on the situation they may be able to use any franking credits received to offset tax payable. This will depend on the specific situation of the fund. Should one member have been in receipt of an applicable government pension on 28 March 2018 they

will continue to receive refunds.

It is important to highlight that for those funds in part pension/part accumulation or 100% accumulation phase, that the outcome will depend significantly on the underlying investment mix/income profile. For funds that have a significant portion of unfranked income (such as REITs, direct property, fixed income and foreign equities) franking credits from Australian shares may be used to reduce tax payable on that income.

Other super structuresThe impact on other super structures may be substantially less than for SMSFs. This will most likely be the case for large APRA regulated funds which pool assets (large pooled super funds) such as industry funds and some retail funds. This is because they pool together their accumulation and pension members and pay tax at the entity level. This means that franking credits generated by all their members are able to be applied to the tax payable generated by the accumulation members. Questions arise as to how this is equitable for the pension members and if they will receive any benefit from this, as well as how a member attains transparency on the process. However, much will depend on the finalisation of the proposal to see how this will work in practice.

It is important to note here that the fund must be of

sufficient size, with a member demographic that results in more tax being paid (either through earnings or contributions) than franking credits received. For funds that have a large portion of their members in retirement phase and/or with a low level of assets, they may be similarly impacted to SMSFs.

Where there is a lack of clarity is how WRAP and master trust platforms will be treated. Whilst it seems they would be treated similarly to large pooled superannuation funds, little has been clarified here. Unfortunately, with the proposal being light on detail it is hard to establish exactly what the impact will be in this instance.

Where to from here on franking credits?Whilst it is important to be informed and plan, it is very hard to do that with a proposal that is light on detail and has so many hurdles to pass before it becomes law. Initially the ALP will need to win the election, but then the proposal will have to progress through the governmental process (including the Senate) to become law. It is possible that the proposal is watered down during this process and there is also the key consideration that the Australian economy (and house prices) is running at a very different speed to when the proposal was announced.

Table 2. How SMSFs will be impacted by the proposal

*The actual tax rate will depend on the proportion of the fund in pension phase vs accumulation phase.

baillieu.com.au10 Baillieu

Baillieu SMSF SolutionTake control with a Self-Managed Superannuation Fund

So, you’ve decided to set up a Self-Managed Superannuation Fund (SMSF) and want someone you can trust to assist not only with the initial setup but also the ongoing requirements.

Traditionally, SMSF trustees relied on the suburban accountant to establish the fund and assist with meeting their compliance needs.

With the rapid growth of the SMSF sector, there are now a range of SMSF services on offer from the budget ‘bare bones’ offerings to customised and comprehensive solutions.

So, what type of service is right for you?There is no simple answer to this question. Rather, your choice of SMSF administrator should be driven by your need for administrative and technical support, the type and complexity of your investments, and your fund balance. As with most things in life, the saying ‘you get what you pay for’ is just as relevant for your SMSF as it is with other products and services. To aid you in your evaluation, let’s look at some of the different types of SMSF services out in the market.

Low-cost, online SMSF administrationThe typical low-cost SMSF administration service is ideal for SMSF trustees who are cost conscious, have a minimum level of complexity and require year-end administration only.

Generally, these providers come equipped with a processing system that inputs data into an accounting software and provides a set of accounts at the end of the year without review or oversight. The types of investments may be restricted and there is no opportunity to engage with SMSF professionals for advice or education.

The suburban accountantAnother traditional SMSF administration and compliance approach involves meeting with the suburban accountant to set up the SMSF and provide end-of-year tax returns. This approach generally involves a more personal touch as the family accountant is familiar with the SMSF trustee’s financial situation but does not offer day-to-day administration or portfolio management systems.

Costs and service offerings vary for each accountant and SMSF trustees need to ensure that the services provided are suitable to their own needs. They also need to be mindful that not all accountants are well versed in SMSF and superannuation. Compliance breaches and excess contributions can cause significant problems and costs for those unfamiliar with the rules.

The complete SMSF administratorMany firms now offer the complete SMSF administration package. These offerings provide a comprehensive solution and generally includes management of the initial set up process through to the ongoing annual administration and accounts. What you get with the higher-end SMSF services is a level of oversight and review of your financial accounts, ensuring that everything is as it should be, and an SMSF contact to help with the organisation.

SMSF administrators may also package strategic and investment advice together with the administration, or may offer these services as an added optional cost for the client to use when required.

Please read the disclaimer at the end of this report 11Investor Newsletter

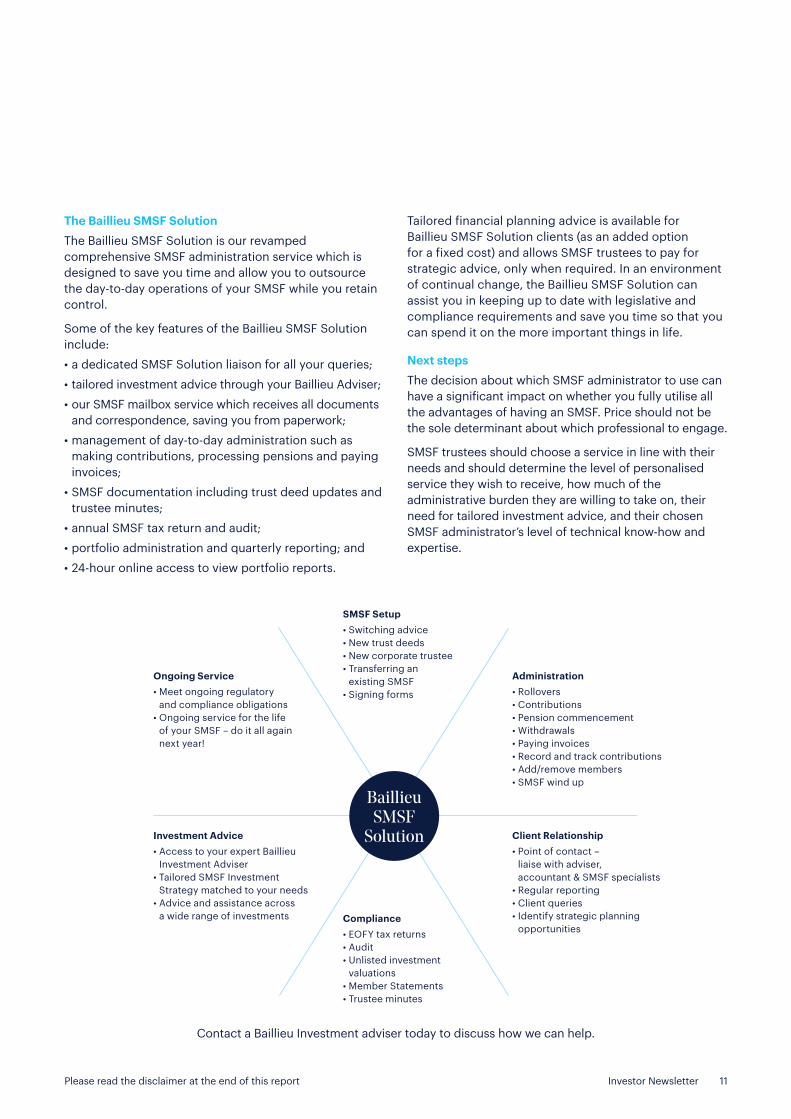

The Baillieu SMSF SolutionThe Baillieu SMSF Solution is our revamped comprehensive SMSF administration service which is designed to save you time and allow you to outsource the day-to-day operations of your SMSF while you retain control.

Some of the key features of the Baillieu SMSF Solution include:• a dedicated SMSF Solution liaison for all your queries;• tailored investment advice through your Baillieu Adviser;• our SMSF mailbox service which receives all documents

and correspondence, saving you from paperwork;• management of day-to-day administration such as

making contributions, processing pensions and paying invoices;

• SMSF documentation including trust deed updates and trustee minutes;

• annual SMSF tax return and audit;• portfolio administration and quarterly reporting; and• 24-hour online access to view portfolio reports.

Tailored financial planning advice is available for Baillieu SMSF Solution clients (as an added option for a fixed cost) and allows SMSF trustees to pay for strategic advice, only when required. In an environment of continual change, the Baillieu SMSF Solution can assist you in keeping up to date with legislative and compliance requirements and save you time so that you can spend it on the more important things in life.

Next stepsThe decision about which SMSF administrator to use can have a significant impact on whether you fully utilise all the advantages of having an SMSF. Price should not be the sole determinant about which professional to engage.

SMSF trustees should choose a service in line with their needs and should determine the level of personalised service they wish to receive, how much of the administrative burden they are willing to take on, their need for tailored investment advice, and their chosen SMSF administrator’s level of technical know-how and expertise.

Contact a Baillieu Investment adviser today to discuss how we can help.

SMSF Setup• Switching advice• New trust deeds• New corporate trustee• Transferring an

existing SMSF• Signing forms

Ongoing Service• Meet ongoing regulatory

and compliance obligations• Ongoing service for the life

of your SMSF – do it all again next year!

Administration• Rollovers• Contributions• Pension commencement• Withdrawals• Paying invoices• Record and track contributions• Add/remove members• SMSF wind up

Compliance• EOFY tax returns• Audit• Unlisted investment

valuations• Member Statements• Trustee minutes

Client Relationship• Point of contact –

liaise with adviser, accountant & SMSF specialists

• Regular reporting• Client queries• Identify strategic planning

opportunities

Investment Advice• Access to your expert Baillieu

Investment Adviser• Tailored SMSF Investment

Strategy matched to your needs• Advice and assistance across

a wide range of investments

Baillieu SMSF

Solution

baillieu.com.au12 Baillieu

Fixed IncomeRisks remain high

Earlier, in our asset allocation piece, we mentioned our underweight recommendation towards Fixed Income.

Looking ahead, we see five sources of upside risk in bond yields, therefore providing reasons for the likely underperformance of bonds in the year ahead.

Expensive absolute valuations: Real bond yields are well below average, ranging from -0.5 to 0.4%. The US real yield of 0.4% compares to the long-term average of 2.1%, Europe at -0.1% (2.2% long-term average), Japan at -0.5% (1.5% long-term average) and Australia at 0.1% (3.0% long-term average).

Unattractive relative valuations: Bonds are back at extreme valuations relative to equities (Figure 9). European equities are back around Eurozone debt crisis spreads, while Japan is at a record extreme and even US and Australian equities are at spreads rarely seen outside the GFC and its aftermath.

Depressed growth expectations: Weaker PMIs have reduced growth expectations. Even so, PMIs are still at above average levels in Japan and the US, and China may have troughed. The typical pre-conditions of downturns – tight policy, financial excess and/or commodity shocks – do not generally appear to be present. We expect the extended policy pause, reduced uncertainty and the tailwind from more moderate oil prices to support

growth expectations in 2019, a negative for bond yields.

Inflation outlook: Whilst lower oil prices will moderate inflation in the near-term, labour markets in the major economies are now the tightest since at least pre-GFC, consistent with gradually rising labour costs and inflation. In the US, unemployment is around 50-year lows at 3.8%, which has driven a gradual recovery in wages growth to ~3.3% YoY, in line with the long-term average (Figure 10). In Japan, unemployment at ~2.3% and wages at ~1.5% YoY are both at their best levels in 25 years. Even in Europe, unemployment is at a decade low 7.8% and wages have recovered to an average 2.3% YoY.

Elevated bond supply in the US: With the foreshadowed end to quantitative tightening, US net bond supply should moderate from extreme levels, though issuance to fund the widening budget deficit should remain high.

In our view, this combination of headwinds should see bond yields rise and bonds underperform in the year ahead. With the central bank policy inflection point behind us, a trough in growth and inflation expectations should push yields higher. We see US bond yields ending the year back above 3%. Outside the US, with more supportive policy and growth lagging behind the US, bond yields are likely to rise, but more slowly.

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

Jan-88 Jan-92 Jan-96 Jan-00 Jan-04 Jan-08 Jan-12 Jan-16

Bond Yield-Earnings Yield Gap

US AUS JPN EUR

Fig.9

Source: Datastream, Baillieu

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Q1 1990 Q1 1994 Q1 1998 Q1 2002 Q1 2006 Q1 2010 Q1 2014 Q1 2018

US Wages vs Unemployment

US ECI All Wages YoY% US ECI Real Wages YoY% US Unemployment (Right)

Fig.10

Source: Datastream, Baillieu

Please read the disclaimer at the end of this report 13Investor Newsletter

BanksBanks escape relatively unscathed

After being the subject of great uncertainty for the last 15 months, the Australian banking sector finally had its day of reckoning at the beginning of February.

As is frequently the case in financial markets, the final banking royal commission (RC) report contained little in the way of surprise versus expectations and was perhaps more positive than expected – certainly less negative anyway.

From a shareholder perspective, tail risk recommendations around responsible lending and mis-selling were largely absent. Importantly, the commission recommended that the National Consumer Credit Protection Act should not be changed.

While there were some questions regarding the use of HEM (Household Expense Measure) as a way to measure household expenditure, it was not recommended to be outlawed.

So overall, the lack of no major new negative recommendations from the final report meant the banks escaped relatively unscathed.

In terms of relative winners and losers, we think Commonwealth Bank (CBA) and Westpac (WBC) benefit the most given the mortgage broker remuneration recommendations and the lack of structural separation. National Australia Bank (NAB), on the other hand, is, relatively speaking, the loser given commentary around the lack of confidence that issues have yet to be fully addressed – although the management and board changes announced in the aftermath of the report’s release should address some of this.

With the RC risk largely behind us, the market has turned its attention to the recently completed reporting season. CBA was the only major bank to report results. Its first half result was in line with our forecasts with ongoing cash earnings of $4,676m. The group’s capital position of 10.8% was about 50 basis points ahead of our expectations, and taking into account planned divestments should rise to about 12%. A targeted cost-to-income ratio of 40% was also positive.

However, soft non-interest income was impacted by storms in NSW and Victoria, while other negatives included the loss of fees, lower trading income and continued funding pressures.

Importantly, with a forecast capital ratio of >12% likely in FY19, subject to the completion of announced divestments, we now explicitly factor in capital management removing discontinued operational earnings in FY20/21.

CBA has a number of capital management options. For our forecasts, we include a $5bn vanilla on-market buyback but acknowledge that given a franking account balance of ~A$1.7bn, a combination of a structured off-market buyback and a special dividend is possible and achieves a balance among different shareholders’ preferences.

The market seems to be factoring in some capital management initiatives which, given the uncertainty over franking credits, will attract a lot of attention.

Overall, the CBA result and the other major banks’ trading updates highlighted the difficulties the sector faces, with continued slowing balance sheet growth and re-pricing not enough to maintain margins, let alone see any improvement.

With the RC risk largely behind us and CBA’s result not revealing any rapid deterioration in underlying fundamentals outside of lacklustre loan growth, the market is likely to focus on the weakening macro environment for signs the slowing housing market is beginning to impact the banks further.

Company ASX Code Rating Last Price P/E FY19 Yield FY19 Franking

ANZ ANZ Hold $25.65 10.9x 6.4% 100

Commonwealth Bank CBA Buy $70.25 13.9x 6.1% 100

National Australia Bank NAB Buy $24.59 10.8x 8.1% 100

Westpac WBC Hold $25.84 12.1x 7.3% 100Data as of 09/04/2019

baillieu.com.au14 Baillieu

EnergyOil prices continue to recover

Crude oil prices have been highly volatile over the last six months. After touching highs of above US$75/bbl in early October, West Texas Intermediate crude oil plunged to lows of about US$42/bbl in late-December.

This was primarily driven by the US granting waivers on its Iran sanctions and a sharp unwind of speculative positioning, as well as higher-than-expected US production.

Nonetheless, we continue to believe that oil prices can rebound. This is based on the following reasons: 1) resilient global demand growth of ~1.4% pa; 2) very little OPEC spare capacity as the Iran sanctions tighten; 3) significant budgetary pressure on OPEC, with Saudi Arabia’s fiscal breakeven at US$83/bbl; 4) little growth outside the US and OPEC, with US activity likely to have moderated at WTI oil prices around US$50/bbl; and 5) inventory is close to normal levels, with OPEC+ (OPEC plus 10 non-OPEC nations) production cuts of 1.3 million barrels per day still to impact.

Please read the disclaimer at the end of this report 15Investor Newsletter

Australian energy stocks offer growth and leverage to oil prices. Woodside Petroleum (WPL) offers growth through four projects – Scarborough, Browse, Senegal and Myanmar; Oil Search (OSH) a doubling of capacity through its PNG and Elk-Antelope LNG projects and Alaska prospect; and Origin Energy (ORG), by contrast, offers cost-cutting and deleveraging.

Woodside recently reported another fine operational result, with revenue up 32% YoY to US$5.24bn and NPAT up 28% YoY to US$1.36bn on the back of production growth, higher prices and sustained cost metrics. This was in line with our forecasts and contained no major surprises, except for the higher dividend which was up 47% YoY to US$1.44/sh, representing a ~99% payout ratio for 2H18.

Oil price movements aside, we expect price support for WPL over the coming year to be driven by progress on Scarborough, possible Wheatstone outperformance, start-up of Greater Enfield and Senegal Final Investment Decision, as well as potential life extension announcements at North West Shelf and possible associated M&A activity.

Key risks relate to commodity price assumptions, which are particularly relevant given current volatility, and delivery issues associated with growth projects and timing and capex.

Oil Search recently reported an FY18 NPAT of US$420mn, which was about ~6% lower than market consensus. Revenue was up 6% YoY to US$1,536m. The slightly weaker-than-expected result was mostly due to costs, although some margin of error in cost estimates was inevitable given the earthquake in Papua New Guinea.

With higher prices offsetting the earthquake disruption, we believe the overall result was good despite slightly missing the market’s optimistic expectations. The dividend of US10.5cps presents a payout of 47%, at the upper end of Board’s dividend policy to return 35-50% of NPAT. Oil Search has guided to 2019 production guidance of 28.0-31.5 million barrels of oil equivalent.

We believe there are some near-term positive catalysts for OSH, including a possible Alaska reserves upgrade and option selldown. However, they could potentially be offset by the risk of delay to PNG LNG expansion FEED entry and lower spot LNG prices.

Origin Energy reported a 1H19 NPAT of $592mn, approximately 4% ahead of our forecasts, and announced they would recommence the payment of dividends (10cps fully franked interim dividend declared).

The company delivered a strong gas result in the Energy Markets division. Going forward, we expect a 12% higher FY19 gas gross margin than the prior corresponding period (pcp), with a 10% 1H19 increase in external sales and a A$0.40/GJ increase in margins. The company expects such a gas contribution to be sustainable going forward.

The electricity gross margin declined 7% vs the pcp, while the second half will be impacted by retail competition and concessions. This is the foundation of lower FY20 earnings, along with lower renewable energy certificate prices.

In terms of LNG, we have increased our FY19 APLNG revenue 6% due to higher realised prices and a lower AUD/USD.

Company ASX Code Rating Last Price P/E FY19 Yield FY19 Franking

Origin Energy ORG Hold $7.31 11.8x 3.0% 100

Oil Search OSH Hold $8.15 18.7x 2.3% -

Woodside Petroleum WPL Buy $35.50 17.0x 4.7% 100

Data as of 09/04/2019

baillieu.com.au16 Baillieu

ResourcesSupply concerns and capital management drive stocks

Iron ore was further boosted by supply disruptions following the Vale disaster in Brazil, which will likely persist for some time.

Commodity prices, relatively stable cost bases and reasonable, but far from perfect, operating performances are providing a boon for shareholders. Miners are in a free cash flow sweet spot, confirmed by the recent reporting season that delivered cash returns that were at worst in line with market expectations. More often than not, they were well above.

We cannot recall a time where company balance sheets were so under geared right across the sector. We believe EPS upgrades for the bulk miners are likely and there is

It has been a positive six months for the big miners. Commodity prices have been resilient, as global demand remained strong against expectations that the global economy was headed for a recession. Further, this commodity price strength has bucked the trend of weak Chinese economic data.

Please read the disclaimer at the end of this report 17Investor Newsletter

Company ASX Code Rating Last Price P/E FY19 Yield FY19 Franking

BHP Billiton BHP Hold $40.03 14.4x 5.1% 100

Rio Tinto RIO Hold $101.58 11.5x 5.4% 100

Data as of 09/04/2019

the real potential for further capital management at FY19 results.

At a company specific level, BHP Group (BHP) reported slightly softer 1H19 earnings. Underlying NPAT of US$4bn was just shy of our forecasts and market consensus. An interim dividend of 55cps was declared, representing a 75% payout ratio (1H18 payout 72%).

Commodity prices are clearly driving near-term sentiment. While our near-term iron ore price assumptions have been revised up materially to account for the Brazilian supply shock, our cautious view on Chinese steel demand, coupled with modest supply growth, leads the market back to significant surplus by Q4 of this year.

Our valuation is somewhat stretched, but with further capital returns likely forthcoming and spot commodity prices holding firm, there’s enough to keep existing shareholders happy, in our view.

Rio Tinto (RIO) also reported, delivering full year earnings of US$8.8bn, ahead of our forecasts for US$8.4bn. A final and special dividend of A$2.51ps & A$3.39ps respectively were declared.

RIO remains a high quality, well-managed company, which should continue to generate and return significant amounts of capital to shareholders. Management’s strategy of prudent capital discipline has been highly effective in creating value and providing material returns to shareholders. That said, everything has its price,

and even with revised iron ore prices we can’t get our numbers to stack up for RIO.

Given our cautious view on Chinese steel demand over the next 12 months, we maintain our HOLD.

Despite both stocks being HOLD rated, we currently have a preference for BHP over RIO. With less of an exposure relatively to iron ore (~47% of 2019E EBITDA vs RIO at ~70%) and more obvious pathways to improved valuation through organic growth options, we prefer BHP.BHP’s balance sheet is where it wants it to be, and with a de-risked capex profile and a more favourable commodity mix (we like the supply/demand fundamentals of petroleum compared to bulks), we think BHP is still well placed to perform at least in line with the market through 2019.

baillieu.com.au18 Baillieu

Consumer StaplesSector facing macro headwinds

From a macro perspective, we are cautious towards stocks exposed to the Australian consumer. We believe we are in the early stages of a housing downturn which, combined with a number of other factors, is squeezing Australian households.

These factors include low wages growth, rising interest and debt burdens, tax bracket creep (until 2H19) and, critically, an inflection point in household savings as the housing downturn deepens.

On a stock specific level, Coles (COL) recently reported its first standalone result following the demerger from Wesfarmers in November 2018. The 1H19 result was a little lacklustre, however, with operating earnings down 5.8% to $733m compared to the previous corresponding period (pcp).

COL’s core Coles Supermarket business reported a sales increase of 3.6% to $16.2bn, while EBIT only increased marginally, up 0.4% to $602m. The company also noted slightly lower margins. Given this, further weakness in sales in 2H19 seems likely as more emphasis is given to everyday pricing over promotions.

Liquor sales increased 0.6% to $1.7bn in 1H19, while comparative store sales growth was 0.7% for 2Q19, with trading adversely impacted by unfavourable weather.

Looking ahead, Coles outlined a number of near- and medium-term challenges, but proposed few immediate solutions to soft revenue growth and significant cost headwinds. This does not appear to be supportive of a significant rebound in profit growth momentum in 2H19.

With earnings growth likely to remain weak and COL not cheap in an absolute sense, we are happy to remain on the sidelines for now and continue to assess the likely impact of significant investment in stores and supply chain.

Following the Coles demerger and sale of a number of assets, Wesfarmers (WES) reported a complex result. Cutting through the noise, divisional EBIT of $1.6bn was up 3.5% on a continuing business basis on the pcp. Bunnings was the standout performer, reporting a 7.9% increase in EBIT. Kmart and WES’ Industrials operations reported earnings declines of 3.8% and 2.6% respectively.

Officeworks reported an 11.8% increase in EBIT, but remains a relatively small contributor.

We believe WES emerged from this result in a strong capital position and with most businesses performing solidly. Management noted it was a good time to have a strong balance sheet as it allowed them to invest in core businesses and growth initiatives.

One potential growth initiative was the surprise takeover bid for Lynas Corp, a rare earths producer. While the bid was turned down by Lynas’ board, WES obviously believe in the battery thematic underpinning rare earth demand.

The positive surprise in the result was the dividend announcement. WES declared and has now paid a $1.00 dividend and a $1.00 special dividend, utilising its large franking credit balance before a possible change in the franking credit refund legislation. In terms of outlook, the company expects moderated trading conditions to continue, particularly for Bunnings and Kmart.

Turning our attention to Woolworths (WOW), and its 1H19 result was below market expectations. With the exception of its Supermarket division, earnings declined across the board or, in Big W’s case, remained loss-making.

Supermarkets experienced improved sales momentum in 2Q19, but also stated demand remained relatively subdued. Liquor earnings declined in a tough trading environment, with a 6.4% decline in EBIT to $290m. The company expects the FY19 Liquor result to be below that of FY18.

BIG W reported a loss of $8m, which was a modest improvement on the $10m loss reported in 1H18. Also, as part of a review into Big W WOW announced it would be shutting 30 stores.

On the capital management front, WOW announced a $1.7bn off-market buyback following the completion of the sale of its petrol business.

In terms of outlook, trading across the group in the first seven weeks of 2H19 had improved, however the company said to expect “a more subdued consumer environment to continue for the foreseeable future”. It also expects cost pressures to increase in 2H19.

Company ASX Code Rating Last Price P/E FY19 Yield FY19 Franking

Coles COL Hold $12.24 18.6x 2.5% 100Wesfarmers WES Hold $34.14 19.5x 5.0% 100

Woolworths WOW Hold $30.17 23.2x 3.3% 100

Data as of 09/04/2019

Please read the disclaimer at the end of this report 19Investor Newsletter

TelecomsThree players better than four

Over the last few years, the Australian telecommunications sector has been driven by an increasingly competitive landscape, however, as announced several months ago, the yet-to-be approved merger between TPG Telecom (TPM) and Vodafone Hutchison Australia has the potential to change the landscape for the better.

With the final ACCC decision scheduled for May, we note that TPG’s decision in early February to cease its planned network rollout in Australia indicates the merger with Vodafone is likely to be approved.

From a broader perspective, the approval would be neutral to positive for the Australian telecommunications sector, as the shift from an expected four players back down to three should lower the risk profile of industry returns. The proposed merger largely eliminates the price war that was expected to come from TPG entering as the country’s fourth mobile network operator.

While a combined Vodafone-TPG will be a formidable entity, the status quo of three mobile operators is still better for the competitive dynamics than having an aggressive, price-led challenger such as TPG invading the market with its own network.

Turning our attention to Telstra’s (TLS) recent result, and 1H19 earnings were broadly in line with our estimates, with earnings before interest, tax depreciation and amortisation (EBITDA) of $4.26bn vs our forecast of $4.19bn.

NPAT came in slightly stronger than our forecast of $1.13bn at $1.23bn. Underlying EBITDA was circa 3% ahead of our estimates, driven by better-than-expected performance in the Mobile division, where there were

strong net post-paid handheld additions of 239,000 users.

Despite the better-than-expected Mobile numbers, management has indicated that the mobile market remains highly competitive, expecting (1) a net fixed and mobile market decline at the upper end of the previously guided 2-3% range and (2) for postpaid handheld average revenue per user (ARPU) in 2H to decline at a faster rate than 1H19. This is also consistent with Optus’ recent earnings release.

The full-year dividend was effectively lowered. TLS gave no specific dividend guidance for FY19, but 1H DPS was lower than our forecasts (8.5cps) at 8.0cps and management noted that post the NBN rollout, EBITDA needs to be in the $7-8bn range for a 16.0cps dividend to be paid out. Given this, we lowered our FY19 DPS to 16.0cps (was 17.0cps) and expect this to be sustainable until FY21, which is the last year of NBN one-off receipts.

We increased our price target to $3.15 after the result.

Elsewhere in the sector, TPG Telecom (TPM) reported 1H19 earnings ahead of our estimates despite lower revenues.

While the result was well ahead of our numbers, it was supported by: 1) lack of negative impact from Singapore Mobile (which has been delayed until FY20); 2) lower D&A; and 3) lower finance costs, with the company capitalising a significant portion of interest related to the acquisition of spectrum and the build out of the Australian mobile network.

Despite the solid 1H result, FY19 guidance for EBITDA of A$800-820m was maintained, implying a decline of ~3% at the mid-point, which is largely due to an expected increase in NBN access costs in 2H.

The proposed merger with Vodafone remains key to the performance of TPG. However, we believe that any upside is more than factored in at current trading levels. Hence, we have a SELL rating and $5.60 target price.

Company ASX Code Rating Last Price P/E FY19 Yield FY19 Franking

Telstra TLS Hold $3.30 15.7x 4.8% 100

TPG Telecom TPM Sell $6.88 17.7x 0.6% 100

Data as of 09/04/2019

baillieu.com.au20 Baillieu

Stock FocusIdeas towards the smaller end of town

MNF GroupMNF Group (MNF) provides software platforms and applications which enable the providers of communications products to service their clients. MNF also provides some of these products in their own right.

MNF recently delivered a 1H19 result that missed our forecasts, though this could be put down to one-offs – essentially a rebasing of earnings in its Global Wholesale business and the acquisition costs of TelcoInABox (TIAB). There was also an increase in depreciation from Singapore and NZ assets coming on line.

The company declared an interim dividend of 2.1cps fully franked.

MNF has multiple organic growth drivers, including: 1) winning new customers; 2) expanding its software capabilities with existing customers; 3) benefiting from the growth of its wholesale clients; and 4) expanding into Asia on the back of demand from large, global unified communications service providers (eg. Microsoft, Google).

The growth engine is its Domestic Wholesale business, which continued its strong growth in 1H19 with gross profit up 42% to $12.2m. This was driven by 24% organic growth and three weeks of TIAB contribution. A key indicator of future growth was that phone numbers ported in to MNF grew by 25% on the pcp.

With TIAB now completed, steady growth will continue in the Domestic and Global Wholesale divisions. We believe there is significant medium-term upside potential from TIAB revenue and cost synergies, the continued ramp-up of PennyTel and the offshore expansion into Asia.

On a valuation basis, the stock is trading at historically low levels and, as such, we believe it is good value.

Village RoadshowVillage Roadshow (VRL) is an international entertainment company which operates businesses such as Theme Parks, Film Distribution, Cinema Exhibition and Film Production. The company’s businesses include Village Cinemas, Roadshow Films and Village Roadshow Theme Parks, where it operates Warner Bros. Movie World, Sea World, Wet’n’Wild, Paradise Country, Australian Outback Spectacular and Sea World Resort & Water Park.

After a sustained period of underperformance, VRL’s 1H19 result showed evidence of what can happen when better execution is combined with favourable trading conditions. The EBITDA of $65.0m (+31% pcp) was a significant turnaround and came despite a $4m negative impact from revenue recognition accounting standard changes.

Other positives from the result included a turnaround in Theme Parks, a good Cinema Exhibition result, a significant reduction in net debt and the cost reduction program which was cited as on target. The company also said dividends are likely to be reinstated from 2H19.

VRL expects stronger results from both Theme Parks and Cinema Exhibition in the second half than the first half. However, film distribution is expected to deliver a weaker result in FY19 versus FY18 and corporate costs are likely to be slightly higher in 2H19 than 1H19.

We returned to a positive view on VRL following the result. This was largely driven by upgrades to our Theme Park earnings forecasts, a strong outlook for Cinema Exhibition, much improved cash flow generation, debt levels that are now moderate and seemingly under control, and the likely resumption of dividends.

Company ASX Code Rating Last Price P/E FY19 Yield FY19 Franking

MNF Group MNF Buy 4.07 21.0x 2.0% 100

Village Roadshow VRL Buy 3.22 20.4x 1.1% 100

Data as of 09/04/2019

Please read the disclaimer at the end of this report 21Investor Newsletter

InternationalRebound in global equity markets has lifted valuations

As outlined in our asset allocation section, we currently recommend an overweight position in international equities. At a geographic level, we recommend overweights to Japan and Europe, a slight overweight to emerging markets (EM) and a benchmark weighting to the US.

The rebound in global equity markets has lifted equity valuations. The US is moderately above its long-term average of 16x, while Europe, Japan and EM are at below-to-far below-average levels (Figure 11). Versus rates, short- or long-term, equities are far more attractive than average across all markets, but particularly in Japan and Europe (Figure 12). Dividend yields are attractive in absolute terms.

In relative terms, the US is expensive versus Europe and Japan. Overall, composite valuation metrics range from slightly unattractive in the US to attractive in Europe and EM, and extremely attractive in Japan.

In terms of liquidity conditions, the inflection in central bank policy has driven a significant improvement. The rate rises and quantitative tightening seen over the past 12-24 months has given way to an extended pause in the US and moves toward easier policy in Europe. The Bank of Japan has continued its ultra-accommodative policies and the Peoples Bank Of China is gradually easing.

The earnings outlook is somewhat mixed across the regions, as earnings growth expectations have deteriorated in line with softening purchasing manager and business sentiment surveys (Figure 13 & 14). Japan and the US appear positive as a US soft landing, supported by robust underlying fundamentals in its consumer and business sectors, should support earnings, while a robust Tankan should support an ongoing positive earnings outlook in Japan. China stimulus may have driven an earnings inflection point. Resolution of the US-China trade tensions should help China, broader EM and Europe.

Fig.11

Source: Datastream, Baillieu

10

15

20

25

30

35

40

45

50

55

60

6

8

10

12

14

16

18

20

22

24

26

Jan-88 Jan-92 Jan-96 Jan-00 Jan-04 Jan-08 Jan-12 Jan-16

Forward PE (12MF): US, EUR & JPN

US (Left) EUR (Left) JPN (Right)

Fig.12

Source: Datastream, Baillieu

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

Jan-88 Jan-92 Jan-96 Jan-00 Jan-04 Jan-08 Jan-12 Jan-16

Bond Yield-Earnings Yield Gap

US AUS JPN EUR

Fig.13

Source: Datastream, Baillieu

-4.00

-3.00

-2.00

-1.00

0.00

1.00

2.00

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

Jan-90 Jan-94 Jan-98 Jan-02 Jan-06 Jan-10 Jan-14 Jan-18

US S&P500 EPS vs ISM Manufacturing & Services

US S&P500 fwd EPS YoY% (Left) US ISM Mfg & S's z score (Right)

Fig.14

Source: Datastream, Baillieu

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

Jan-91 Jan-94 Jan-97 Jan-00 Jan-03 Jan-06 Jan-09 Jan-12 Jan-15 Jan-18

EUR MSCI EPS vs Business Sentiment

EUR 12MF EPS YoY% (Left) EUR Business Sentiment z score (Right)

baillieu.com.au22 Baillieu

Listed Investment CompaniesTop Picks

Traditional LICs: Traditional LICs significantly underperformed (TSR) a strong All Ordinaries Accumulation Index (XAOAI: +6.1%) in February, which we believe was primarily driven by: 1) a majority trading ex-dividend during the month; and 2) elevated trading levels (higher than historical averages) in January 2019. We commonly refer to these factors as the “dividend run-up period”. Following special dividend announcements by AFIC and BKI, Milton (MLT) recently announced a 2.5cps special. BKI also announced an FY19 final special, and we believe risk remains to the upside for traditional LIC TSR outperformance in FY19. Trading at estimated 8.8% and 6.1% discounts to NTA respectively, Diversified United (DUI) and MLT are our current top picks.

Large capitalisation: WAM Leaders (WLE) and Ophir High Conviction Fund (OPH) are our current top picks. The discount of WLE has drifted to an estimated 6.3% discount, which we believe is excessive given the quality of management. Elsewhere, since listing (Dec-18), OPH has been a top performer in our coverage universe, holding a high conviction portfolio of securities such as A2M, APT, and CWY. Top pick OPH is currently trading at a 2% discount to NTA.

Small capitalisation: Acorn Capital (ACQ) and WAM Microcap (WMI) are our current top picks within the small cap space. Trading at an estimated 13.6% discount to NTA, we believe ACQ provides investors exposure to asset class (Private Equity/VC) that is often difficult to

access and illiquid (unlisted securities accounts for 33% of ACQ’s underlying portfolio). We recently added WMI to our coverage list and into our small cap top picks. We believe WMI is currently trading at an estimated discount to its historical trading levels. The manager, Wilson Asset Management International (WAMI), has a strong track record of performance within the microcap space, and we believe a 0.5% discount to NTA provides an attractive entry point.

International: Our top picks MFF, PGF and TGG (on an NTA basis) performed broadly in-line with the strong MSCI in February. That said, TSR’s of PGF and TGG lagged NTA growth and as a result, respective discounts are estimated to be 13.7% and 14.2%. Although a top performer across our LIC universe, MFF is trading at an estimated 3.4% discount to NTA.

Specialist: Hearts and Minds (HM1) is our top pick. HM1 holds a concentrated portfolio of the highest conviction picks from some of Australia’s leading fund managers (many of whom have closed investment strategies to new capital). HM1 has outperformed the XAOAI since listing in Nov-18 and we believe the 0.4% premium to NTA remains an attractive entry point.

Our top picks refer to preferred exposures within each sector based on

numerous quantitative and qualitative factors. However, they should not

be treated as official stock recommendations but merely as a guide to

where we would apportion funds at this particular point in time.

Company Code Share Price

Market Cap. ($)

Dividend (cents)

Dividend Yield

Grossed Up Yield

Current Est. NTA

Current Estimated Disc/Prem

Feb NTA Feb Disc/Prem

1 Yr Ave Disc/Prem

3 Yr Ave Disc/Prem MER

Diversified United DUI 4.11 867.1 15.5 3.8% 5.4% 4.51 -8.8% 4.45 -9.4% -5.7% -6.0% 0.13%

Milton Corporation MLT 4.41 2950.1 19.2 4.4% 6.2% 4.69 -6.1% 4.71 -5.5% -2.2% -1.2% 0.12%

Ophir High Conviction OPH 2.49 498.0 0.0 na na 2.54 -2.0% 2.47 3.6% 2.9% na 1.23%

WAM Leaders Limited WLE 1.14 888.4 5.0 4.4% 6.3% 1.21 -6.3% 1.19 -5.4% -2.5% -1.9% 1.00%

Acorn Cap Inv Fund ACQ 1.10 57.9 6.2 5.7% 6.7% 1.27 -13.6% 1.23 -12.9% -10.3% -12.8% 0.95%

WAM Microcap Ltd WMI 1.24 173.6 6.0 4.9% 6.9% n.a n.a 1.26 -0.5% 7.4% 7.6% 1.00%

MFF Capital Invest. MFF 3.00 1624.7 3.0 1.0% 1.4% 3.11 -3.4% 2.98 -4.3% -6.4% -9.4% 1.25%

Pm Capital Fund PGF 1.16 407.3 3.6 3.1% 4.4% 1.34 -13.7% 1.32 -13.5% -6.0% -8.4% 1.00%

Templeton Global TGG 1.27 275.7 10.0 7.9% 11.3% 1.48 -14.2% 1.46 -11.5% -8.9% -9.8% 1.20%

Hearts and Minds HM1 2.86 572.0 0.0 n.a n.a 2.85 0.4% 2.86 -3.1% 1.0% na 0.00%

Source: Company releases, Bloomberg, Baillieu estimatesData as of 09/04/2019

Please read the disclaimer at the end of this report 23Investor Newsletter

Corporate

Despite experiencing relatively low equity capital market volumes over the last quarter, Baillieu Corporate is pleased to provide an update on the successful completion of several primary and secondary capital raisings.

In October 2018, Mainstream Group Holdings announced the successful completion of its $9.5 million placement and $0.8 million share purchase plan (SPP), in which Baillieu Corporate acted as Lead Manager. Baillieu Corporate was also involved in Data Exchange Networks’ $2.0 million placement and Bass Metals’ $3.3 million placement, both in December 2018, as Lead Manager and Joint Lead Manager respectively. More recently, in February 2019, Baillieu Corporate successfully acted as Lead Manager to Genex Power’s $2.1 million placement.

Baillieu Corporate was pleased to have acted as Co-Manager to Australia’s largest ever coal initial public offering on the ASX, Coronado Global Resources, which raised $3.6 billion in October 2018. Further, we were also involved in Syrah Resources’ $103.0 million placement and SPP in September 2018, and the Webjet $121.0 million placement and SPP in November 2018, acting as broker in both capital raisings.

Baillieu Corporate was also involved in several hybrid issuances for some of Australia’s leading financial institutions. This includes Commonwealth Bank of Australia’s $1.6 billion notes issuance in December 2018, Macquarie Group’s $500 million notes issuance in February 2019, and more recently, National Australia Bank’s $1.9bn notes issuance in March 2019.

In addition to assisting ASX-listed companies Baillieu Corporate was also active in the unlisted space, raising $4.5 million via a converting note issue and $2.1 million via a private equity placement for unlisted companies Agersens and hitIQ respectively. Agersens is an Australian-based agri-tech company that has commercialised the world’s first automated fencing system for livestock, whilst hitIQ has developed a head impact surveillance system that measures and reports serious head impacts during contact sport via a custom mould mouthguard.

The support received from Baillieu Corporate’s transactions indicate that investors are continuing to seek quality investment opportunities, which are typically underpinned by a solid track record, professional senior management team and a well-defined growth strategy. We are currently working on a strong pipeline of corporate mandates and potential opportunities which we hope to announce in due course.

baillieu.com.au24 Baillieu

Financial Advisers

Jonathan Andrews BCom(Ec) BA GDipAppFin ADA2 (03) 9282 8145Nick Bird Associate Financial Adviser (03) 9602 9218Roger Bryan BCom MSI Dip (03) 9602 9258Chris Christidis BCom MeSAFAA ADA2 (03) 9602 9222Florin Clopovschi BAppSc(IT) MAppFin ProfDipStockbroking ADA2 (03) 9602 9223Stewart Collingwood AdDipFP AdDipMktg (03) 9282 8106David Comben MSAFAA(1) (03) 9602 9226Bryan Cooper BCom MeSAFAA (03) 9602 9230Trevor Davidson BA BCom GDipAppFin SA Fin MeSAFAA(1) (03) 9282 8117John Edwards Financial Adviser (03) 9282 8153Ben Ellwood BCom ADA2 (03) 9602 9273James Fletcher BCom(Eco&Fin) GDipArts(History) (03) 9602 9345Stephen Fulton BEng(Civil)(1) (03) 9282 8164Chris Girgis BCom BA ADA1 (03) 9602 9239Alexandar Hay BBus MeSAFAA Director(1) (03) 9602 9341Paul Haysey BA LLB MeSAFAA (03) 9282 8110Charlie Heerey BEc(hons.) GDip AppFin GCertBus (Philanthropy) ADA2 (03) 9602 9219Andrew Hellier Master Stockbroker SMSF SpecialistAdviserTM Diploma in Stockbroking MFinPlan Deakin(1) (03) 9602 9342Charlie Holst GDipAppFin(1) (03) 9602 9317David Holst BEc(1) (03) 9282 8105Craig Hutchinson BEc ProfDipStockbroking (03) 9282 8198

Anthony Ives BEc GDipFin FFin (03) 9602 9392

Ian Johnston BBus DipFS(1) (03) 9602 9386James Journeaux Financial Adviser (03) 9282 8108David Julian BA/BSc MeSAFAA(1) (03) 9602 9236Michael Kent MAgrSc FFin(1) (03) 9602 9215Daphne Lee DipBusMgmt DipFP CTP MasterArts (03) 9282 8125Kim Lee BCom MBA CA Ffin(1) (03) 9282 8114Kent Mackieson CFA(1) (03) 9602 9372Hamish Macneil BBus GdipAppFin(1) (03) 9602 9360Justin Marshall BBus ADA2 (03) 9602 9266Philip Mitchell BEc FFin MeSAFAA ADA2(1) (03) 9602 9251Peter Mitchell BBus ADA1 DipFin(FinPlan) (03) 9602 9208William Morrison FFin GDipAppFin Director(1) (03) 9602 9252Richard Morrow MSAFAA FellowAusIMM ADA2(1) (03) 9602 9243James Nicolaou ProfDipStockbroking SAA (03) 9602 9248Hege Nolan BBusEco/Fin,GDippAppFin ADA2 (03) 9602 9204

Vince Novelli CFP CPA FPS SSA CTA CGMA GCertTax GDipFP GDipAppFin BBusPDS ACSI ANZIIF FIML FTIA FFin FAICD MSAFAA SMSF Specialist AdviserTM (03) 9602 9374

Simon Power BA GDip AppFin FFin MSAFAA GAICD Director(1) (03) 9282 8113Benjamin Prisk CFP® MSAFAA GDipAppFin DipFP (1) (03) 9282 8188Bruce Pulbrook BEc LLB GDipAppFin&Inv MeSAFAA FFin ProfDipStockbroking(1) (03) 9282 8116Adam Routledge Institutional Equities Adviser (03) 9282 8120Andrew Smith BBus MSAFAA CFP® (1) (03) 9282 8180Adam Spicer BBus(Acc) BBus(Bkg&Fin) DipFS(FinPlan) (03) 9602 9288Tim Stewart BBus FFin (03) 9602 9347Ben Taylor BBus GAICD Director(1) (03) 9602 9387Chesley Taylor BCom FFin MeSAFAA(1) (03) 9602 9340Campbell Thompson BSc MeSAFAA ADA1(1) (03) 9602 9245Ian Warner BEc DipFP CFP MeSAFAA(1) (03) 9602 9229Craig Webb MeSAFAA (03) 9602 9249Ross Williams Associate Financial Adviser (03) 9282 8182Warren Williams BEc(Hons) MAppFin ADA2 (03) 9602 9362Laura Willis Associate Financial Adviser (03) 9602 9398Geoff Worrell DipFS Bbus(Acc) MBA (CPA)(1) (03) 9602 9225

Melbourne

Please read the disclaimer at the end of this report 25Investor Newsletter

Adelaide

Perth

Sydney

Bendigo

Geelong

Gold Coast

Newcastle

Travis Adams CFA BEc GDAFI AFP SMSF Specialist AdviserTM (08) 7074 8402Courtney Biggs BAppFin AdvDipFS(FP) ASA (08) 7074 8400Alex Butler BEc CFP® (08) 7074 8406Helen Dundon BAcc CPA(FPS) CFP® SMSF SPECIALIST Adviser SSATM (1) (08) 7074 8407Alan Hutchinson BEc&Bus(Hons) MeSAFAA AFP GradDipFP (08) 7074 8403Mike James BA(Hons) CFP® (1) (08) 7074 8405Matthew Loveder BEc GradDipAppFin DipFP AFP (1) (08) 7074 8404Benjamin Prisk CFP® MSAFAA GDipAppFin DipFP (03) 9282 8188

Owen Clare BCom CA (08) 6141 9452John Day Financial Adviser (08) 6141 9458Ross Fawell Financial Adviser (08) 6141 9457Scott Green BEng DipFP AFP (08) 6141 9463Travis Hansen Financial Adviser (08) 6141 9453Karl Laufmann Financial Adviser, WA Manager (1) (08) 6141 9451Cameron Pratt BBus GDip(AppFin) DIP(FinPlan) (08) 6141 9461Donald Smith Financial Adviser (08) 6141 9455George Smith BA(Hons) (08) 6141 9462Danny Stent BSc MBA DFP (1) (08) 6141 9454Zachary Stent BCom(Fin&Econ) (08) 6141 9460

Peter Cameron Financial Adviser (02) 9250 8907Glenn Crichton BE(Mining) GDipFP AICD SAFin MeSAFAA AusIMM ADA1 (02) 9250 8918Stephanie Johansen MESAA DipFinMarkets(FINSIA) ADA2(1) (02) 9250 8929Gregory Kelly MESAA ADA2 (02) 9250 8914Adrian Leppinus BCom(1) (02) 9250 8935Simon Martin BBus GDipAppFin ADA2 (02) 9250 8925Gwen Parsons BCom MESAA (02) 9250 8912James Rosenberg MESAA ADA1 (1) (02) 9250 8909Harry Rumble Assosciate Financial Adviser (02) 9250 8969

Mark Haydon BSc DipFinAdvising(ASIA) ADA2 (02) 4037 3503Brodie Hussain BEc BFin DFS(Fin Plan) ADA1(1) (02) 4037 3502Steven Perry BMANGT(Farm Bus)SYD GDipFinPlanning(Finsia) Newcastle Manager(1) (02) 4037 3501

Tony Langford Financial Adviser ADA2 (1) (03) 4433 3400

Charles Mackinnon Financial Adviser ADA2 (1) (03) 4210 0200

Peter Hickey BBus FCA CFP® GradDipFin(Finsia) (1) (07) 5628 2670

baillieu.com.au26 Baillieu

Are you using our website?

Beware of Scammers

We receive regular updates from the ACCC / Scamwatch about investment scams that can result in a loss of money. Examples include:• investors being scammed by an unlicensed company,

resulting in the loss of a significant sum of money;• scammers impersonating well-known businesses;• scammers gaining access to computers to steal bank

account information or money;• investment scams off ering “get-rich-quick” schemes.

There is little we can do once a scam has occurred, and we kindly remind clients of the need to be vigilant. You cannot be too careful.

If you are ever contacted out of the blue for investment matters, or if something simply sounds too good to be true, please first speak to your investment advisor before proceeding.

There are also a number of websites you can check yourself for known scams.

Website features:• A consolidated view of your accounts• Overnight and intra-day market summaries of key

indices and currencies• Improved charting of stocks and indices• Detailed client contract note history• Maintain watchlists of stocks and view ASX company

announcements

• Portfolio valuations and transaction statements• Detailed reporting for clients• Enhanced search functionality for all Baillieu

research reports• Export your financial data to Excel

Please contact your adviser to register.

www.scamwatch.gov.au/

www.moneysmart.gov.au/scams/companiesyou-should-not-deal-with

Please read the disclaimer at the end of this report 27Investor Newsletter

Disclosure of Potential Interest and Disclaimer

This document has been prepared and issued by:Baillieu Limited

ABN 74 006 519 393. AFS Licence No. 245421. Participant of ASX Group. Participant of Chi-X Australia. Participant of NSX. Baillieu Limited (Baillieu) and/or its associates may receive commissions, calculated at normal client rates, from transactions involving securities of the companies mentioned herein and may hold interests in securities of the companies mentioned herein from time to time. Your adviser will earn a commission of up to 55% of any brokerage resulting from any transactions you may undertake as a result of this advice. This advice is issued on the basis that:

1. in preparing the advice, Baillieu did not consider whether the advice is appropriate in light of the particular investment needs, objectives and financial situation of the investor(s) or prospective investor(s); and

2. before making an investment decision on the basis of the advice contained herein, the investor(s) or prospective investor(s) need to consider whether the advice is appropriate in light of their particular investment needs, objectives and financial circumstances.

When we provide advice to you, it is based on the information you have provided to us about your personal circumstances, financial objectives and needs. If you wish to rely on our advice, it is important that you inform us of any changes to your personal investment needs, objectives and financial circumstances.

If you do not provide us with the relevant information (including updated information) regarding your investment needs, objectives and financial

circumstances, our advice may be based on inaccurate information, and you will need to consider whether the advice is suitable to you given your personal investment needs, objectives and financial circumstances. Please do not hesitate to contact our off ices if you need to update your information held with us. Please be assured that we keep your information strictly confidential.

No representation, warranty or undertaking is given or made in relation to the accuracy of information contained in this advice, such advice being based solely on public information which has not been verified by Baillieu Limited.

Save for any statutory liability that cannot be excluded, Baillieu Limited and its employees and agents shall not be liable (whether in negligence or otherwise) for any error or inaccuracy in, or omission from, this advice or any resulting loss suff ered by the recipient or any other person.

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a judgement at its original date of publication and are subject to change without notice. The price, value of and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of securities and financial instruments is subject to exchange rate fluctuation that may have a positive or adverse eff ect on the price or income of such securities or financial instruments. Baillieu Limited assumes no obligation to update this advice or correct any inaccuracy which may become apparent after it is given.

Authors of company comments may hold shares in companies mentioned.

baillieu.com.au

Baillieu Limited ABN 74 006 519 393 AFSL No. 245421 Participant of ASX Group Participant of Chi-X Australia Participant of NSX Ltd

Adelaide +61 8 7074 8400Bendigo +61 3 4433 3400Geelong +61 3 5229 4637Gold Coast +61 7 5628 2670Melbourne +61 3 9602 9222Newcastle +61 2 4037 3500Perth +61 8 6141 9450Sydney +61 2 9250 8900

To discuss any of the services available, please contact your adviser or Baillieu on 1800 339 521