investor presentation q4 2015 - pkc group...investor presentation q4 2015 strategic projects...

TRANSCRIPT

Investor Presentation Q4 2015Strategic projects advanced, EBITDA continued to improve

PKC Investor Presentation Q4 2015 February 11, 2016 Matti Hyytiäinen, President & CEO

• New truck order activity has slowed and build rates declined in North America

• Truck demand in Europe continued to recover while Brazilian market is in recession

Q4 2015 Highlights

PKC Investor Presentation Q4 2015

Business Environment

PKC’s Operations

PKC’s Financial Performance

• European manufacturing footprint improvement continues

• Curitiba, Brazil factory successfully closed

• Wiring Systems’ comparable EBITDA continued to improve

• Record quarterly cash flow

• Dividend proposal is EUR 0.70 per share

North America Market

PKC Investor Presentation Q4 2015

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2011 2012 2013 2014 2015 2016 2017 2018

Heavy Duty Trucks Medium Duty TrucksSource: LMC Automotive forecasting Q4/2014

Production units

-23%

-10%

+14%

-3%

EPA 2014 1st stage

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

Q1/13Q2/13Q3/13Q4/13Q1/14Q2/14Q3/14Q4/14Q1/15Q2/15Q3/15Q4/15

Heavy Duty Trucks Medium Duty Trucks

+10%

+6%

Source: LMC Automotive forecasting Q4/2015, ACT Build History January 2016, PKC Group

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

2011 2012 2013 2014 2015 2016 2017 2018

Light Vehicle (Pick-up and SUV)

+2%+7%

58%

42%34%

66%

Heavy Duty Trucks Medium Duty Trucks

Market Share 1-12/2015

Production units

Production units

-9%

+3%

EPA 2014 2st stage EPA 2014 1st stage

EU27 + EFTA Market

PKC Investor Presentation Q4 2015

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

2011 2012 2013 2014 2015 2016 2017 2018

Heavy Duty Trucks Medium Duty TrucksSource: LMC Automotive forecasting Q4/2014

Production units

-1%

+4%

+14%

-3%

EURO 6

0

20,000

40,000

60,000

80,000

100,000

120,000

Q1/13Q2/13Q3/13Q4/13Q1/14Q2/14Q3/14Q4/14Q1/15Q2/15Q3/15Q4/15

Heavy Duty Trucks Medium Duty Trucks

EURO 6

+16%

+4%

Source: LMC Automotive forecasting Q4/2015, PKC Group

44%

56%

22%

78%

Heavy Duty Trucks Medium Duty Trucks

Market Share 1-12/2015

Production units

+9%

+10%

Brazil Market

PKC Investor Presentation Q4 2015

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2011 2012 2013 2014 2015 2016 2017 2018

Heavy Duty Trucks Medium Duty TrucksSource: LMC Automotive forecasting Q4/2014

Production units

+12%

-6%

+14%

-3%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Q1/13Q2/13Q3/13Q4/13Q1/14Q2/14Q3/14Q4/14Q1/15Q2/15Q3/15Q4/15

Heavy Duty Trucks Medium Duty Trucks

-44%

-32%

Source: LMC Automotive forecasting Q4/2015, PKC Group

31%

69%

2%

98%

Heavy Duty Trucks Medium Duty Trucks

Market Share 1-12/2015

Production units

+51%

+2%

PKC estimates production volume to continue to decrease

China Market

PKC Investor Presentation Q4 2015

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

2011 2012 2013 2014 2015 2016 2017 2018

Heavy Duty Trucks Medium Duty TrucksSource: LMC Automotive forecasting Q4/2014

Production units

+5%

+4%

+14%

-3%

0

50,000

100,000

150,000

200,000

250,000

Q1/13Q2/13Q3/13Q4/13Q1/14Q2/14Q3/14Q4/14Q1/15Q2/15Q3/15Q4/15

Heavy Duty Trucks Medium Duty Trucks

-29%

-25%

Source: LMC Automotive forecasting Q4/2015, PKC Group

10%

90%

0%

100%

Heavy Duty Trucks Medium Duty Trucks

Market Share 1-12/2015

Production units

+21%

+23%

EURO 4 EURO 4

China market share since September 2015,

joint venture started operations

Revenue

PKC Investor Presentation Q4 2015

17 17 20 13 12 9 9 60

50

100

150

200

250

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15

South America

189 191 195 197 206 209 212 220

15 15 15 1321 15 14 12

0

50

100

150

200

250

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15

Total GroupEUR million EUR million

55 52 46 53 54 58 64 77

10 10 10 8 8 8 88

0

50

100

150

200

250

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15

EuropeEUR million

115 121 129 129 138 142 136 123

0

50

100

150

200

250

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15

North AmericaEUR million

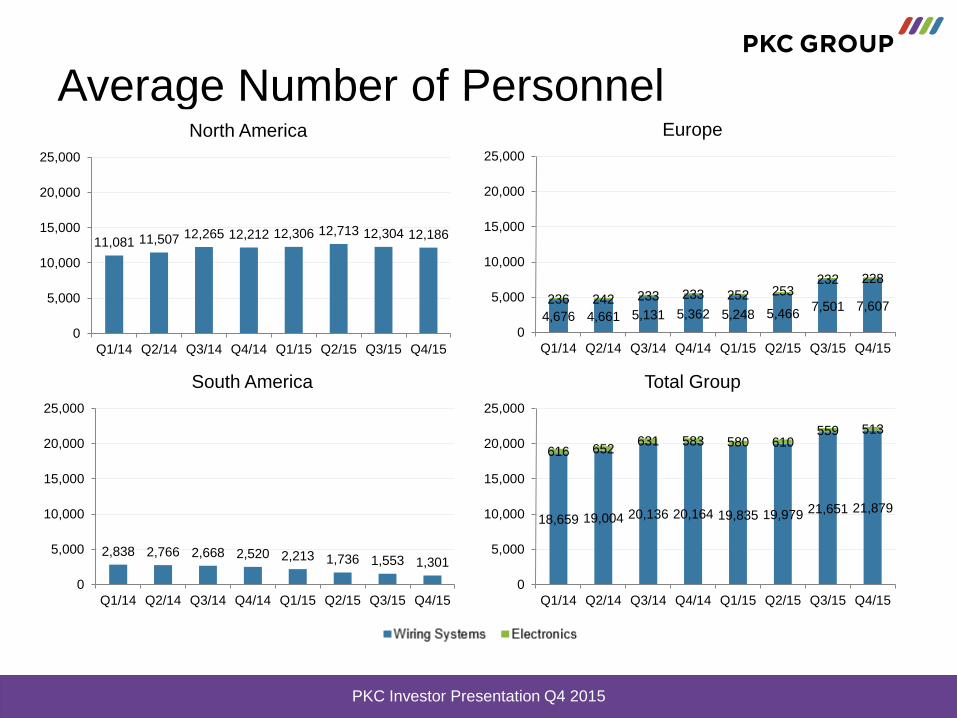

Average Number of Personnel

PKC Investor Presentation Q4 2015

11,081 11,507 12,265 12,212 12,306 12,713 12,304 12,186

0

5,000

10,000

15,000

20,000

25,000

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15

North America

4,676 4,661 5,131 5,362 5,248 5,4667,501 7,607

236 242 233 233 252 253232 228

0

5,000

10,000

15,000

20,000

25,000

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15

Europe

2,838 2,766 2,668 2,520 2,213 1,736 1,553 1,301

0

5,000

10,000

15,000

20,000

25,000

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15

South America

18,659 19,004 20,136 20,164 19,835 19,979 21,651 21,879

616 652631 583 580 610

559 513

0

5,000

10,000

15,000

20,000

25,000

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15

Total Group

• North American heavy-duty and medium-duty truck production is estimated to decrease by 17% compared to previous year’s level.

• European heavy-duty and medium-duty truck production is estimated to remain on the previous year’s level.

• Brazilian heavy-duty and medium-duty truck production is expected to continue to decrease.

• Chinese heavy-duty and medium-duty truck production is expected to grow by about 5% compared to previous year’s level

• The demand for the rolling stock is expected to continue to grow steadily.

• The market demand for Electronics segment’s products is expected to remain on the current level at the most.

Market Outlook – Full Year 2016

PKC Investor Presentation Q4 2015

• PKC Group estimates that with prevailing exchange rates 2016 revenue will be at or above previous year level and comparable EBITDA will be higher than previous year level. Revenue and comparable EBITDA improvement is to take place in the second half of the year.

• In 2015, PKC’s revenue was EUR 908.0 million and comparable EBITDA before non-recurring items was EUR 63.9 million.

PKC Group’s Outlook

PKC Investor Presentation Q4 2015

Key Figures

PKC Investor Presentation Q4 2015

EUR million 10-12/15 10-12/14 Change

%

1-12/15 1-12/14 Change

%

Revenue 231.8 209.2 +10.8 908.0 829.5 +9.5

EBITDA1)15.6 8.6 +80.9 63.9 48.6 +31.5

EBITDA%1)6.7 4.1 7.0 5.9

Non-recurring items -1.2 -11.7 -89.6 -9.0 -28.4 -68.4

Operating profit (loss) 5.7 -10.2 22.7 -7.0

EPS (EUR) 0.08 -0.63 0.29 -1.21

Cash flow from operations 53.6 34.4 +55.6 14.8 41.0 -63.9

Gross capital expenditure 5.9 4.0 +48.5 38.1 19.9 +91.5

Core working capital2) 92.7 70.2 +32.1 92.7 70.2 +32.1

ROCE, %3) 10.8 7.7

Gearing, % 31.4 -5.6

1) Excluding non-recurring items2) Inventories + trade receivables - trade payables3) ROCE, % = Adjusted operating profit (excl. NRIs) / ((Total equity + interest-bearing liabilities)(average))

• Revenue increased +12% including FX impact of +6%

– Light-vehicle build-outs still reduced revenue and truck revenue was lower from peak volumes in North America

– European revenue grew while revenue in Brazil decreased substantially due to poor market conditions

– KTP acquisition increased revenue by 9% while Chinese JV impact was 6%

• Adjusted EBITDA continued to improve– Lower losses in Brazil, favorable FX

translation impact and improvement in Europe

– Development program in Europe continuing

– The recent transactions in Poland and China included in Wiring Systems segment

Wiring Systems Segment, Q4 2015

PKC Investor Presentation Q4 2015

188.6191.3

195.4 196.7

205.7209.3

212.0

219.8

170

180

190

200

210

220

230

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15

Revenue

EUR million

11.7 13.5 15.510.7

15.3 16.5 16.9 17.7

-2.1 -1.0 -7.4 -9.7

0.0

-5.0

0.0

-0.7

6.27.1

7.9

5.5

7.4 7.9 7.9 8.1

-4

-2

0

2

4

6

8

10

-10

-5

0

5

10

15

20

25

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15

EBITDA excl. NRIs

NRIs

EBITDA excl. NRIs, % of revenue

EUR million %

Electronics Segment, Q4 2015

PKC Investor Presentation Q4 2015

15.4 14.7 14.8

12.5

20.8

14.7 13.912.0

0

5

10

15

20

25

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15

Revenue

EUR million

1.2 0.8 1.0 0.2

2.8

0.7 0.7

-0.5-0.2

8.0

5.26.5

1.4

13.6

4.7 4.7

-3.8-5

0

5

10

15

-1.0

0.0

1.0

2.0

3.0

4.0

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15

EBITDA excl. NRIs

NRIs

EBITDA excl. NRIs, % of revenue

EUR million %

• Revenue was down 4% in the quarter, but up 7% YTD

• Lower quarterly EBITDA impacted by lower revenue and unfavorable product mix of ODM products

Net Working Capital

PKC Investor Presentation Q4 2015

105.7 102.8 112.389.0

116.8 99.6 116.6 106.8

80.4 82.283.4

79.4

89.494.1

100.794.9

-87.0 -86.3 -95.9 -98.3 -102.7 -97.3 -92.8 -109.0

-17.6 -20.5-32.9 -44.0 -41.2 -36.7 -27.6

-37.6

0

2

4

6

8

10

12

14

16

18

-200

-150

-100

-50

0

50

100

150

200

250

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15

Trade payables Other liabilities and receivables***

NWC* % of Revenue** Core working capital* % of Revenue**

Inventories Trade receivables

* Average of previous four quarters ** Revenue of previous 12 months *** Related to employee benefits, taxes and financial

items. Since Q3/14 includes additional tax liability of EUR

8.3 million and non-recurring items booked, but not paid.

EUR million %

81.6 78.266.9

26.2

Core working capital = Inventories + trade receivables – trade payables

62.3 59.896.9

55.1

Cash Flow

PKC Investor Presentation Q4 2015

41.0

14.8

-20.3

-15.7

20.7

-0.9

0.0

-22.5

20.7

-23.4

-30

-20

-10

0

10

20

30

40

50

2014 2015

Cash from operations Net capex (organic)

Cash after net capex Acquisitions

Free cash flow

EUR million EUR million

-18.4

-31.8

7.4

1.60.9

-17.9

30.7

47.0

-40

-30

-20

-10

0

10

20

30

40

50

2014 2015

Q1 Q2 Q3 Q4

Free cash flow excl. acquisitions

EUR million

Balance Sheet and Return

PKC Investor Presentation Q4 2015

42.7

34.7

29.0

0

5

10

15

20

25

30

35

40

45

2013 2014 2015

Equity ratio, %

-1.1 -5.6

31.4

-10

0

10

20

30

40

50

60

70

80

90

100

2013 2014 2015

Gearing, %

-2.2-8.9

49.4

66.9

48.6

63.9

-20

-10

0

10

20

30

40

50

60

70

80

2013 2014 2015

Net debt EBITDA*

12.2

7.7

10.8

0

2

4

6

8

10

12

14

2013 2014 2015

ROCE, %

%

EUR million %

%

*EBITDA of previous 12 months excl. NRIs ROCE % = Adjusted operating profit (excl. NRIs) /

((Total equity + interest-bearing liabilities)(average))

PKC’s Strategy Captures Growth

Opportunities

PKC Investor Presentation Q4 2015

PKC Investor Presentation Q4 2015

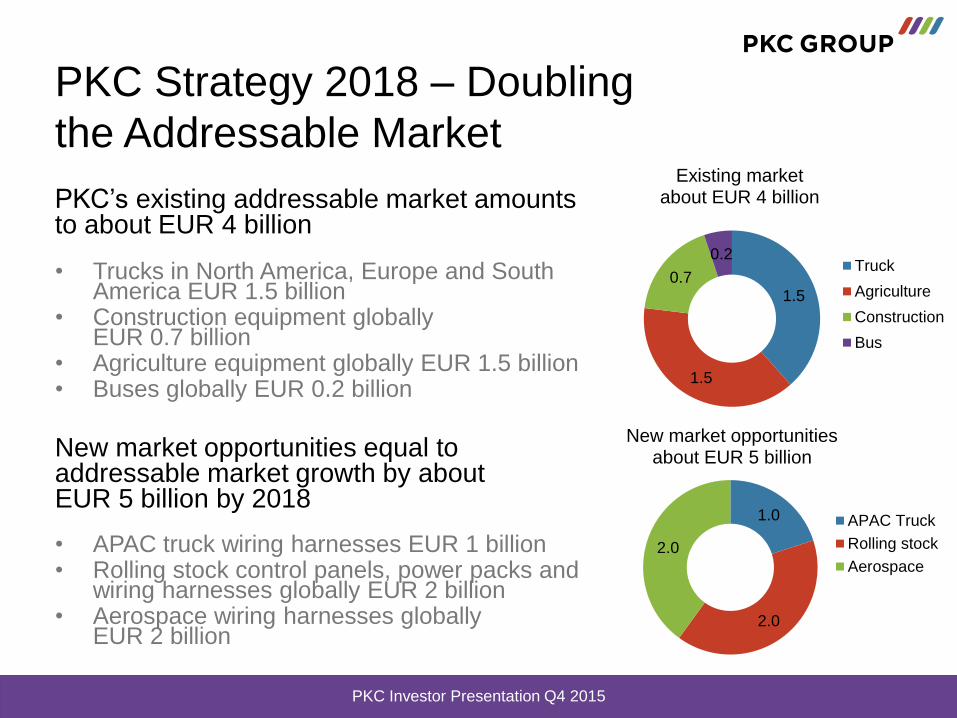

PKC’s existing addressable market amounts to about EUR 4 billion

• Trucks in North America, Europe and South America EUR 1.5 billion

• Construction equipment globally EUR 0.7 billion

• Agriculture equipment globally EUR 1.5 billion• Buses globally EUR 0.2 billion

New market opportunities equal to addressable market growth by about EUR 5 billion by 2018

• APAC truck wiring harnesses EUR 1 billion• Rolling stock control panels, power packs and

wiring harnesses globally EUR 2 billion• Aerospace wiring harnesses globally

EUR 2 billion

PKC Strategy 2018 – Doubling

the Addressable Market

1.5

1.5

0.7

0.2

Existing marketabout EUR 4 billion

Truck

Agriculture

Construction

Bus

1.0

2.0

2.0

New market opportunitiesabout EUR 5 billion

APAC Truck

Rolling stock

Aerospace

PKC Investor Presentation Q4 2015

• Doubling the addressable market

• Improved manufacturing footprint and expansion of engineering services enable to maintain strong market position in western truck markets and to capture further growth opportunities

• Expansion into rolling stock market well received by the customers, working on to globalize commercial relationships with the main industry OEM’s

• 1st Chinese PKC joint venture expanding into new customers. PKC knowhow recognized by the market and further organic and inorganic opportunities identified and in progress

Strategy Execution Proceeding

PKC Group Plc

Bulevardi 7

FI-00120 Helsinki, Finland

www.pkcgroup.comPKC Investor Presentation Q4 2015