investor presentation september, 2007

TRANSCRIPT

Online Magazines Trade shows Direct online sales

(NASDAQ-GS: GSOL)

Merle A. Hinrichs

Chairman and CEO

Investor PresentationSeptember, 2007

2

Safe Harbor

This presentation contains forward-looking statements within the meaning of Section 27-A of the Securities Act of 1933, as amended and Section 21-E of the Securities Exchange Act of 1934, as amended. The company's actual results could differ materially from those set forth in the forward-looking statements as a result of the risks associated with the company's business, changes in general economic conditions, and changes in the assumptions used in making such forward-looking statements.

3

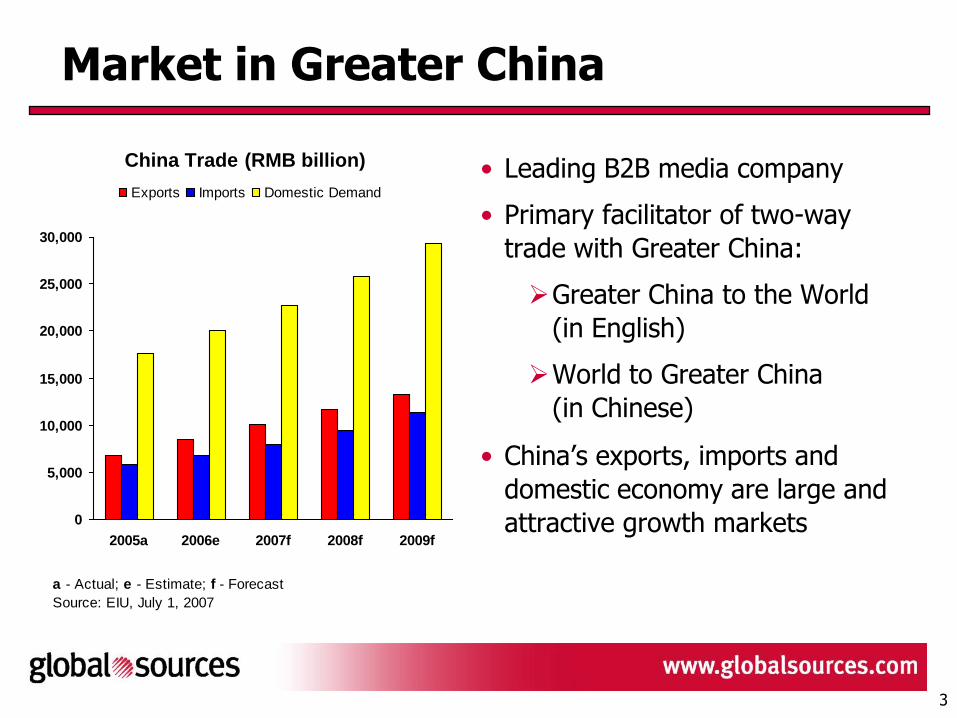

• Leading B2B media company

• Primary facilitator of two-way

trade with Greater China:

Greater China to the World

(in English)

World to Greater China

(in Chinese)

• China’s exports, imports and

domestic economy are large and

attractive growth markets

Market in Greater China

China Trade (RMB billion)

0

5,000

10,000

15,000

20,000

25,000

30,000

2005a 2006e 2007f 2008f 2009f

Exports Imports Domestic Demand

a - Actual; e - Estimate; f - Forecast

Source: EIU, July 1, 2007

4

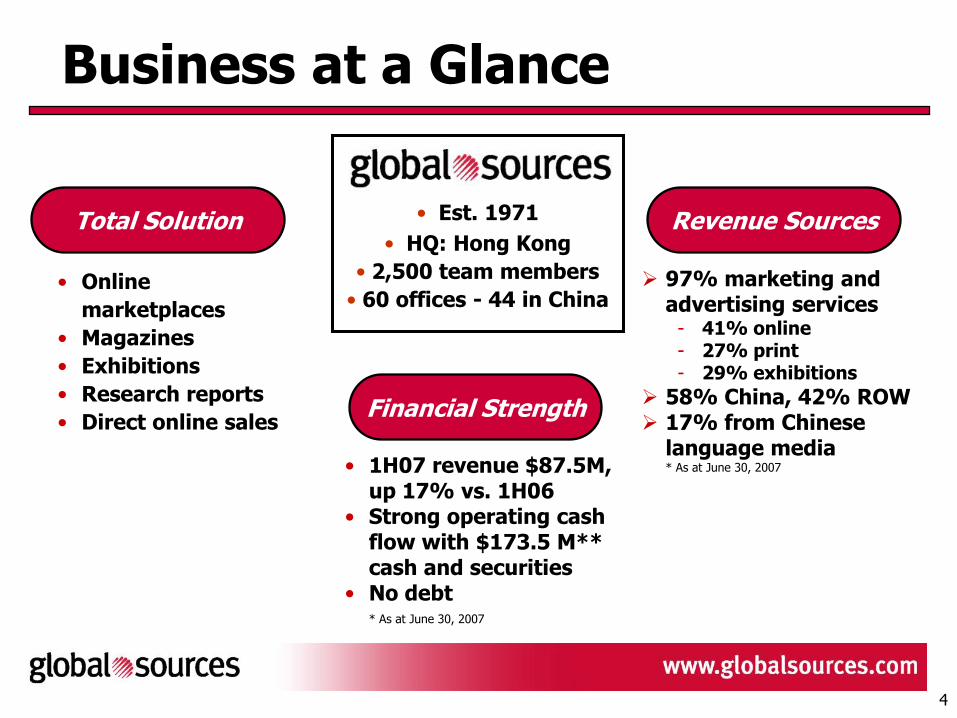

Business at a Glance

Revenue Sources

• Online

marketplaces

• Magazines

• Exhibitions

• Research reports

• Direct online sales

97% marketing and advertising services

41% online 27% print 29% exhibitions

58% China, 42% ROW 17% from Chinese

language media* As at June 30, 2007

• Est. 1971

• HQ: Hong Kong

• 2,500 team members

• 60 offices - 44 in China

• 1H07 revenue $87.5M, up 17% vs. 1H06

• Strong operating cash flow with $173.5 M** cash and securities

• No debt* As at June 30, 2007

Total Solution

Financial Strength

5

Community: 151,000 suppliers

Key Driver: Suppliers with quality products and the ability to export

Community: 635,000 active buyers in 230 countries (certified with E&Y)

Key Driver: Professional buyers that import and outsource in volume

Greater China to the World

RFI Generation: 18.7 million to suppliers through Global Sources Online alone for 12 months ending June 30, 2007

Product Shipments

RFI Generation: 18.7 million to suppliers through Global Sources Online alone for 12 months ending June 30, 2007

Product Shipments

14 VERTICAL MARKETS- Auto Parts & Accessories

- Baby & Children’s Products

- Computer Products

- Consumer Electronics

- Electronic Components

- Fashion Accessories

- Garments & Textiles

- Gifts & Premiums

- Hardware & DIY

- Home Products

- Machinery

- Security Products

- Telecom Products

- Underwear & Swimwear

6

Chief Executive

China is the

market leader

with a circulation

of 195,000 and

844,000

registered online

users.

World to Greater China

Community: Manufacturers of semiconductors and electronics equipment -- plus luxury consumer brands

Key Drivers: Companies want to penetrate the China market

7 VERTICAL MARKETS

- Electronic Engineering

- Electronic Design

- Electronics Manufacturing

- Fashion Accessories

- Baby & Children’s Products

- Lifestyle

- Management

Community: More than 1 million users/readers including BPA audited subscribers and registered online users

Key Drivers: Need and demand for imported products

International IC-China is China’s biggest semiconductor show. Held annually in three locations, in 2007 there were 29,000 attendees and 1050 booths including 12 of the world’s top 15 makers as exhibitors.

EE Times-China is

the market leader.

Combined with two

related titles, total

circulation 125,000

with some 400,000

registered online

users.

Product Shipments & Services

7

For export media, Global Sources has the most breadth, depth, verification and vertical specialization of sourcing content

Print OnlineTrade Shows

Direct Online Sales

Creative & Production

Services

Research Reports

Global Sources

Hong Kong TDC

Alibaba

Kenfair

B2bmanufacturers.com

Powerful Differentiation

Made-in-China.com

Ninetowns / Tootoo

Trade Easy

Canton Fair

8

Cont’…..Powerful Differentiation

RetailOnline Print Face-to-Face

GSOL My Catalog Magazines China Sourcing Reports

China Sourcing Fair

Vendor Summits

Private Sourcing Events

Carrefour

Casino

Coles Group

El Corte Ingles

Halfords

Lowe’s

Kingfisher

QVC

Sears

Staples

KarstadtQuelle

Woolworths

• Large-volume, professional buyers: Retail(Source: Agentrics members using our Private Sourcing Events)

9

Cont’…..Powerful Differentiation

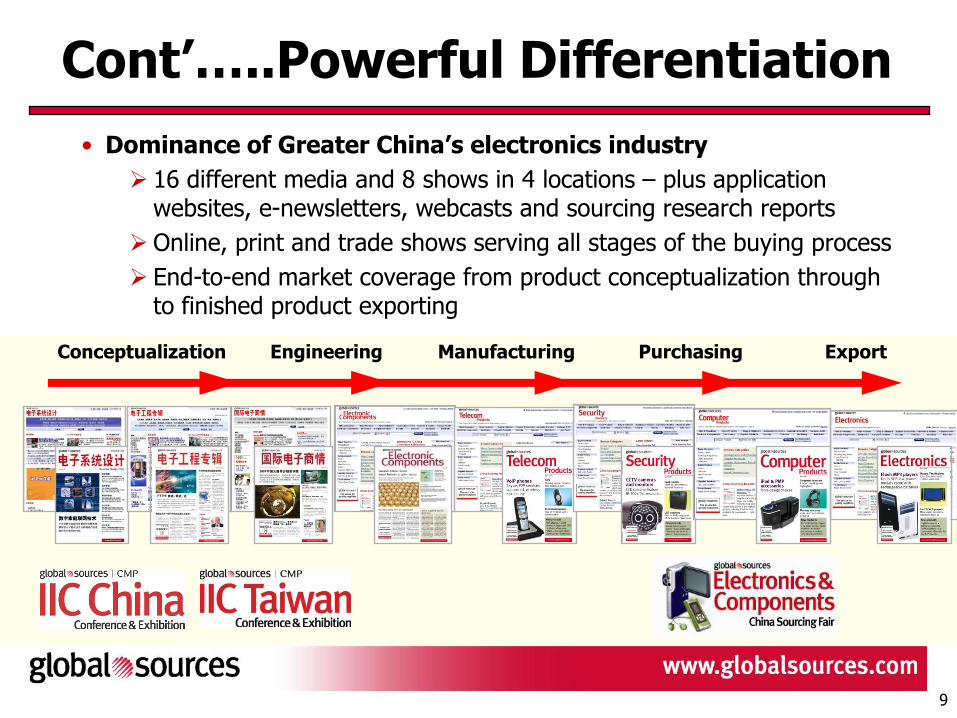

• Dominance of Greater China’s electronics industry

16 different media and 8 shows in 4 locations – plus application websites, e-newsletters, webcasts and sourcing research reports

Online, print and trade shows serving all stages of the buying process

End-to-end market coverage from product conceptualization through to finished product exporting

Conceptualization Engineering ManufacturingConceptualization Engineering Purchasing ExportManufacturing Purchasing Export

10

Strong Revenue and Earnings Growth

0

20

40

60

80

100

120

140

160

180

200

FY 2005 FY 2006 FY 2007

Guidance

Revenue (in US$ m)

112.2

156.5

182.0 – 183.5

Notes:

• 2006 Non-GAAP EPS excludes a $7.9 million gain from sale of 199 shares of the company’s subsidiary eMedia Asia Ltd.

• 2007 Non-GAAP EPS excludes an impairment charge of $1.8 million on the company’s HC International investment.

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

FY 2005 FY 2006 FY 2007

Guidance

GAAP Non-GAAP

EPS (in US$)

0.32

0.66

0.49

0.62 -0.65

0.66 -0.69

11

Improving Operating Margins

7%8%

10%

15%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Q206 Q207

Including non-cash stock based compensation expense

Excluding non-cash stock based compensation expense

• China Sourcing Fairs beginning to demonstrate leverage

• Increase in non-cash compensation expenses in Q207 due primarily to increased value of share awards resulting from the increase in share price at the end of Q207

12

Strong Cash Generation & High Visibility

• Cash and securities: $173.5 M;

72% of total assets

• No debt

• High visibility from advance

collections and recurring revenue

Deferred income leads

revenues

Online and print contracts

are for 6 or 12 months

Trade shows booth contracts

are for multiple events

• Strong organic cash generation

Profitable for 36 years

13 days sales outstanding

US

$ m

Cash & Deferred Income

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

160

170

180

2004 2005 2006 1H 2007

Cash and Securities Total deferred income and customer prepayments

13

Recognition

• Included in Russell 3000 Index

• Met requirements for NASDAQ Global Select, which has the highest listing requirements

• Awarded Best IR Website in Asia-Pacific, Small/Mid-Cap category; and Best in China for Disclosure Procedures by IR Global Rankings in 2007

14

New Product DevelopmentNew Product Development

Market Penetration

Market Penetration

Acquisitions/Alliances

Acquisitions/Alliances

Expand into China’s

Domestic B2B Market

Expansion intoChina’s Domestic

B2B Market

B2B Trade with and

within Greater China

Growth Strategy

15

1. Market Penetration

• Large prospect base of 151,000 suppliers

• Primary focus:

Cross sell to clients not using online, print and shows

China Sourcing Fairs: sell more booths; achieve higher revenue

per booth

Continued high revenue growth from China

New and Developing Initiatives

• 1H 2007 China revenue grew by 34% compared to 1H 2006, representing 58% of total revenue

• China Sourcing Fairs: 3,500 booths sold in 2005; 13,000 in 2006 --> over 200% YOY growth

• New Global Sources Online $50.0 $55.9

$83.7

$55.8 $56.3

$72.8

$ 0

$ 2 0

$ 4 0

$ 6 0

$ 8 0

$ 10 0

$ 12 0

$ 14 0

$ 16 0

$ 18 0

2 0 0 4 2 0 0 5 2 0 0 6

C hina R evenue Other R evenue

($ in millions)

Cont’d.....

16

New Global Sources Online

• One stop destination – Double the amount of product and supplier content

• Incentive program for new suppliers

• October 2007 launch

Vertical Search Engine with New and Distinctive Features

• Objective: Comprehensive results

• Three tiers of search results:

Verified Global Sources clients

Suppliers from other sites or marketplaces

Other suppliers from the Web

• Objective: Enhanced verification

Suppliers are who they claim to be

Consumer standards met

Manufacturing processes complied with

Suppliers post certifications and credit ratings

17

New and Developing Initiatives

2. New Product Development

• Primary focus:

More specialized online marketplaces, magazines and trade shows

New media formats (i.e. application websites, e-newsletters, direct

online sales)

• Continued trade show expansion: 22 shows in 2007 to 28 in 2008 New Hong Kong China Sourcing Fair: Gifts &

Home Products becomes Gifts & Premiums – and Home Products effective 2009 with capacity for 1000 additional booths

In 2008, 2 new China Sourcing Fairs in Dubai and new International IC show in Chengdu

• Sports and Leisure online marketplace and magazine effective Oct / Nov 2007

• Elegant Living online and magazine effective Sept

18

3. Expansion into China’s B2B Market

• Attractive growth market that complements our business serving export and import sectors

• Primary focus:

New online, print and trade shows – in existing or related industry sectors

Leverage brands, content, advertisers, sales, infrastructure, expertise and community

New and Developing Initiatives

• New Shanghai shows: China Sourcing Fair: Fashion Accessories and China Sourcing Fair: Baby & Children’s Products

Twice yearly June and December, starting

December 2007

• Extends China Sourcing Fair brands to the China

domestic market

• New China Global Sources Online

cont’d.....

19

New China Global Sources Online

• Objective: One stop sourcing, comprehensive, aggregated results – and verified suppliers

November launch

Buyers: China’s retailers, distributors and manufacturers purchasing in volume

Suppliers: Global Sources’ export customers, foreign suppliers, domestic China businesses

• Strategy: higher-end, vertically focused, multimedia solution

• Key Differentiators:

Comprehensive content, verified suppliers, higher quality products

Trade shows in various verticals

• Competitive advantages:

Large database of exporters who are domestic sellers and buyers

Cross-selling with export service and domestic shows

High brand recognition

• Free at launch to gain leadership traction

Initial development investment: US$600K

Supplier home page indicating a verified

supplier

20

Cont’d… New China Global Sources Online

• Large future market opportunity:

Many unserved and

underserved segments

Up to 25 million SME’s

Price point online-only up

to RMB 3,000 per year --

and RMB 15,000 with viable

trade show

China’s Domestic B2B Market

21

New and Developing Initiatives

4. Acquisitions/Alliances

• Primary focus:

Complementary businesses, technologies or products that will accelerate

achievement of strategic goals

Develop relationships such as those with CMP and Penton where we can

apply our China resources and expertise

• Blue Bamboo Ventures

Asset acquisition recorded as long term

investment

Primary value: R&D and related contribution

to various Chinese language initiatives

Websites complementary to Elegant Living,

Chief Executive China and our domestic

trade shows

22

Investment Highlights

• Huge and attractive market opportunity

• Clear growth opportunities for market penetration, product development and further expansion into China’s domestic B2B market

• Strong revenue and earnings growth, and diversified revenue streams

• Strong cash flow generation with $173.5 million in cash and securities, and no debt

• 36 year track record of profitability and success

• Well positioned with end-to-end offerings, leading brands, and an extensive infrastructure

GSOL is a proxy for

investing in B2B China trade

Thank you

Online Magazines Trade shows Direct online sales

24

Guidance*

• Q3 2007

Revenue expected to be between $33.5 million and $34.0 million

• 14% to 16% growth compared to Q3 2006

EPS (diluted) expected to be between $0.11 and $0.12

• 10% to 20% growth compared to Q3 2006

• Full Year 2007

Revenue expected to be between $182.0 million and $183.5 million

• 16% to 17% growth compared to full year 2006

GAAP EPS (diluted) expected to be between $0.62 and $0.65

Non-GAAP EPS (diluted) expected to be between $0.66 and $0.69

• 35% to 41% growth compared to full year 2006

• Provided August 09, 2007• EPS calculations based on increase in number of shares from the 1 for 10 bonus share distribution, announced March 2007

25

Financials – GAAP to Non-GAAP Reconciliation

Q2 Q2 y-y 1H 1H y-y

(in US$ millions except number of shares and % data) 2007 2006 growth % Jun-07 Jun-06 growth %

Revenues

Online 18.5 15.7 18 35.8 30.8 16

Print 12.0 12.3 (2) 23.8 23.4 2

Exhibitions 20.9 16.4 27 25.7 20.1 28

Miscellaneous 1.1 0.4 175 2.2 0.6 267

Total revenue 52.5 44.8 17 87.5 74.9 17

Operating expenses (47.4) (41.6) (14) (75.7) (67.6) (12)

Operating income 5.1 3.2 59 11.8 7.3 62

Interest and dividend income 1.7 1.3 31 3.1 2.3 35

Gain on sale of available-for-sale securities 0.0 0.2 (100) 0.0 0.3 (100)

Loss on investment, net (1.8) 0.0 (100) (1.8) 0.0 (100)

Foreign exchange losses, net (0.2) (0.2) 0 (0.5) (0.2) (150)

Income before income taxes 4.8 4.5 7 12.6 9.7 30

Income tax expense (0.3) (0.2) (50) (0.6) (0.4) (50)

Minority Interest (0.3) (0.3) 0 (1.3) (1.1) (18)

Cumulative effect of change in accounting

principle 0.0 0.0 0 0.0 0.2 (100)

Net income 4.2 4.0 5 10.7 8.4 27

Net income per diluted share 0.10 0.10 0.25 0.20

GAAP to Non-GAAP Reconciliation

GAAP net income 4.2 4.0 5 10.7 8.4 27

Add-back :

Loss of investment, net 1.8 0.0 (100) 1.8 0.0 (100)

Non-GAAP net income 6.0 4.0 50 12.5 8.4 49

Non-GAAP net income per diluted share 0.14 0.10 0.29 0.20

Total shares used in diluted net income per share

calculations (GAAP and Non-GAAP Net Income) 42,828,613 42,340,666 42,631,899 42,300,614

26

Operating Margin Reconciliation

Note 1 – Increase in non-cash compensation expenses in Q2 2007 was due mainly to increase in value of share awards resulting from the

increase in share price at the end of Q2 2007.

$ % $ % $ % $ %

Total Revenue ( net ) 52,545 100 44,826 100 87,492 100 74,857 100

Total Operating Expenses 47,397 90 41,600 93 75,698 87 67,537 90

Income from Operation / Operating Margin 5,148 10 3,226 7 11,794 13 7,320 10

Non-cash Compensation Expenses ( Note 1 ) 2,769 5 538 1 3,293 4 1,355 2

Income from Operation / Operating Margin excluding

non-cash compensation expenses 7,917 15 3,764 8 15,087 17 8,675 12

2ND QTR 2007 2ND QTR 2006 YTD 2007 YTD 2006

INCOME FROM OPERATION / OPERATING MARGIN

ACTUAL ACTUAL ACTUAL ACTUAL

In U.S. Dollars Thousands

27

Global Sources 2008 Show Schedule

Hong Kong – April & OctoberDubai - June

Hong Kong – April & OctoberShanghai – June & DecemberDubai - June

Hong Kong – April & October

Shanghai – June & December

ShenzhenBeijing - MarchShanghaiChengdu

ShenzhenBeijing - MarchShanghaiChengdu

GuangzhouBeijing - NovemberShanghai

Taipei - August

Taipei - August

Hong Kong – April & OctoberDubai - June