investor update - s26.q4cdn.com

TRANSCRIPT

Investor Update

AUGUST 2021

SINGLE TENANT RETAIL PROPERTY REIT WITH

32 CONSECUTIVE ANNUAL DIVIDEND INCREASES

Safe Harbor

(All data as of June 30, 2021)

This presentation contains certain statements that are the Company’s and

Management’s hopes, intentions, beliefs, expectations, or projections of the future and

might be considered to be forward-looking statements under Federal Securities laws.

Prospective investors are cautioned that any such forward-looking statements are not

guarantees of future performance, and involve risks and uncertainties. The Company’s

actual future results may differ significantly from the matters discussed in these forward-

looking statements, and we may not release revisions to these forward-looking

statements to reflect changes after we’ve made the statements. Factors and risks that

could cause actual results to differ materially from expectations are disclosed from time

to time in greater detail in the company’s filings with the SEC including, but not limited

to, the Company’s report on Form 10-K and Form 10-Q, as well as company press

releases.

2

3

4

NNN’s Unique Long-Term Strategy

Consistent Predictable

Earnings Growth with Low Volatility

Strong Investment Grade Balance Sheet

Elite Level Long-Term Total Returns

5

Strong Investment Grade Balance Sheet

Long-Term Track Record of Success

Second Quarter Highlights

Low Risk Strategy Generates Consistent Growth

Summary – Attributes, Advantages & Risk Mitigation

6

High-quality portfolio produces consistent results

High occupancy through cycle

Strong lease renewal rates with very little capital expenditure (not buying-up rent)

Long-term, net leases adds stability to operating results

Quality comes from sustainable rents (market rent is barometer)

Balance sheet conservatism

In place long before 2008-09 and 2020 (no dilutive equity issuances needed)

Below-average leverage and strong liquidity to weather all environments

Unencumbered portfolio

No reliance on short-term debt to drive per share results

Fixed-rate debt focused to mitigate rising rate risks

Existing scale provides

High diversification (3,100+ properties)

Top exposure to every single-tenant retail acquisition prospect in sector

Low cost of capital relative to competitors

Indicators of competitive advantage

Equity multiple, credit spreads, dividend yield, etc.

Institutional ownership

Track record of annual dividend increases (32 years)

Summary – Attributes, Advantages & Risk Mitigation

7

Proven, tenured management team with domain expertise

Top five executives – average NNN tenure 20 years (range 16-28 years)

Next eight SVPs – average NNN tenure 19 years (range 12-29 years)

Sustainable model

Projections – no heroic assumptions (acquisitions volume, debt tenor, capital pricing, etc.)

Managed market expectations – not promising more than delivered in the past

Market cycle tested over many years

Focused investment strategy (single-tenant retail) – no strategy drift into multiple property types

Operating results are consistent and predictable

Balance sheet never under stress

Management manages for the long-term

Above average total returns over 15-, 20-, and 25-years with below average risk profile

Consistent and Simple Strategy

8

Focus on single-tenant net lease retail properties

Sustain high occupancy and maximize value of existing real estate assets

Maintain fully diversified portfolio

Grow through internal portfolio growth and well underwritten acquisitions

Utilize asset sales to manage risk, enhance value and partially finance new property

acquisitions

Preserve conservative balance sheet and financial flexibility through access to

multiple sources of capital and unsecured debt

Grow per share results mid-single digit percentage annually on a relatively leverage

neutral basis

Produce safe and growing dividends – 32 consecutive annual dividend increases

9

NNN’s Long-Term Retail Net Lease Strategy

Creates a Solid Foundation of Highly Predictable

Operating Income

NNN’s Disciplined Acquisition Approach

Generates Steady Earnings Growth Through

Higher Yields With Less Risk Than Development

and Other Acquisition Approaches

Strategy Generated 3.1% Average Annual

Core FFO Per Share Growth Since 2015

Retail Net Lease Strategy Generatesa Reliable Income Stream with Low Volatility

10

Well-selected retail tenants provide stronger performance through various economic cycles than office, industrial or other tenant types.

Main street locations provide strong market for replacement tenants and rent growth

Lower earnings volatility from higher occupancy (18-year low of 96.4%)

Retail properties more likely to renew lease at end of initial term

10-20-year initial lease terms; 10.6-year weighted average remaining lease term

Only 8.5% of leases expire through YE 2023

Tenants responsible for operating expenses, taxes and capital expenditures – no CAM leakage

No anchor or co-tenancy issues for tenants to leverage into reduced rent

High Quality, Well-Diversified Portfolio

$8.7 billion total assets (gross book basis)

3,173 properties (32.7 million SF) in 48 states

370+ national and regional retail tenants

Top 25 tenants (57% of rent) average 1,055 stores each

11

From 2003 – Q2 2021, NNN’s occupancy never fell below 96.4% while the REIT industry

average never rose above 93.7%.

Source: SNL Financial *REIT Industry Average as of Q1 2021

85%

90%

95%

100%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Q22021

NNN REIT Industry (Excludes Hotels & Health Care)

97.0%

98.3% 98.2% 98.3%

96.7%96.4%

96.9%

97.9% 98.2%

98.6%

99.1% 99.0% 99.1%

98.2%

99.0%

92.1%

93.0%

93.5% 93.5%

92.8%

92.0%

95.0%90.1%

90.8%90.7%

92.0%

92.7% 92.5%

93.3% 93.5%93.7% 93.6%

97.4% 97.4%98.0%

NNN Avg.

98.5 %

87.1%

98.3 %

*86.9%

NNN’s Strategy Results in Higher Occupancy and Less Volatility

NNN’s Acquisition Approach is Unique Because It’s More Difficult

12

Acquisition quality over quantity requires selectivity, discipline and patience:

Small transactions in areas of historical expertise (retail) rather than large portfolio transactions provides higher risk adjusted returns

Retail – NNN’s historical expertise generates higher and more consistent operating results vs. other net lease and non-net lease sectors

Approximately 25 relationships with managements of strong growing retail concepts

Underwriting focuses on alternative uses upon future rollover and current tenant strength

Multiple credit upgrades after NNN’s acquisition – 7-Eleven, Sunoco (Susser),

Bloomin’ Brands, Lowes (Orchard Supply), Advance Auto (Carquest), Darden

(Cheddar’s), Camping World

Lease terms and conditions negotiated based on unique aspects of location and tenant’s business and credit. Tenant “self selection”- unlikely to sign a long-term lease on questionable store

NNN’s Unique Acquisition ApproachGenerates Strong FFO Growth

13

Retail net lease market is very large yet has less buyer competition than other property types because properties are smaller

NNN’s more focused relationship based acquisition approach is more difficult and time consuming further resulting in less buyer competition

Less buyer competition results in higher initial cap rates and built-in rent growth (see page 15)

Careful targeting and underwriting of management and the future prospects of NNN’s retail tenants is supported by:

Consistently high portfolio occupancy; and

Multiple credit upgrades realized by relationship tenants

Consistently high portfolio occupancy results in less earnings volatility

All of the above generate greater per share accretion from lower acquisition volumes and allows NNN to continue to acquire accretively, despite cap rate compression and increased interest rates

14

2007 – 2021 Acquisitions Volumein $ Millions by Source

$340

$122

$17

$220 $194 $293 $333

$109

$249 $188

$106 $104

$22 $7

$357

$233

$36

$221

$552 $513 $337 $285 $617 $598 $567 $610 $648

$158 $202

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

$550

$600

$650

$700

$750

$800

$850

$900

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Relationship @ 7.6% Average Cap Rate ($5,934 million = 72%)

Market / Auction @ 7.5% Average Cap Rate ($2,304 million = 28%)

$238

$772

$707

$630 $618

$726$755

$716$752

$847

$697

$355

$180$209

15

NNN’s Acquisition Volumes vs. Other REIT Property Types

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

(Mill

ion

s)

9.5%

8.8%

8.4%

9.0%

9.4%

9.5%

8.4%

8.3%

7.8%7.5%

7.2%

6.9%

6.9%

6.8%

6.9%

6.5%6.4%

Historical Acquisition Volume at Weighted Average Initial Cash Cap Rates

NNN has consistently generated strong acquisition volumes at

significantly higher cap rates than other REIT property types

16

Strong Investment Grade Balance Sheet

Long-Term Track Record of Success

Second Quarter Highlights

Low Risk Strategy Generates Consistent Growth

Durable Capital Structure

17

Long-Term Balance Sheet Management

Objectives

Avoid financing risk (never need capital)

Maintain access to capital & flexibility to take advantage of market

opportunities and weather economic storms

Reduce cost of capital – competitive advantage

Longer duration capital reduces re-finance risks (vs. shorter duration capital)

Unencumbered properties maximizes flexibility (leasing, selling, expanding,

etc.) and lowers debt service burden

Maintain strong investment-grade debt ratings

Stagger debt maturities

Maintain bank line capacity to fund near-term debt maturities and acquisitions

Asset dispositions are a source of capital – sector leading expertise

In making capital allocation decisions, fully burden the cost of equity (expected

return) to limit dilution and maximize per share accretion

Strong Investment Grade Balance Sheet –Risk Management is a Core Competency

18

Investment-grade debt rating (BBB+ / Baa1) supported by industry leading leverage ratios

99.7% of assets unencumbered - only $11.0 million of secured debt

Well-laddered debt maturities

$1.1 billion unsecured bank credit line (accordion to $2.0 billion)

No outstanding balance as of 6/30/21 ($249 million cash balance at 06/30/21)

Matures June 2025, plus two, six-month extensions at NNN’s option

Priced at LIBOR + 77.5 bps

Weighted average outstanding balance past seven years under $80 million

Raised $2.4 million of common equity and generated $40.4 million of property disposition proceeds in first half 2021

March 2021 issued $450 million of unsecured notes due 2051 at 3.50% effective rate

March 2021 repaid $350 million of unsecured notes due 2023 at 3.30% effective rate

19

Conservative Balance Sheet Management

(As of June 30, 2021 - total gross book assets)

Secured Debt - $11.0 million

Unsecured Debt - $3,049.7 million*wtd. avg. maturity 13.0 yrs; wtd. avg. effective interest rate 3.7%

Preferred Equity - $345.0 million

Common Equity - $5,330.6 million

Total Capitalization: $8.7 billion (gross book)

Interest coverage ratio: 4.7x

Fixed-Charge coverage ratio: 4.2x

Unsecured

Debt

34.9%

Preferred

Equity

4.0%Common

Equity

61.0%

Secured

Debt

0.1%

20

Credit Metrics Summary

2016 2017 2018 2019 2020

June

2021

Net debt / Total assets (gross book) 30.2% 35.3% 34.6% 35.3% 34.4% 35.0%

Net debt + preferred / Total assets (gross book) 43.9% 44.0% 42.6% 39.3% 38.4% 39.0%

Net Debt / EBITDA (last four quarters) 4.3 4.9 4.8 4.9 5.0 5.0

EBITDA / Interest expense (cash) 4.8 4.7 4.8 5.0 4.6 4.7

EBITDA / Fixed charges (cash) 3.4 3.5 3.7 4.0 4.0 4.2

Unencumbered assets / Total assets (gross book) 99.7% 99.7% 99.7% 99.7% 99.7% 99.7%

Bank line weighted average usage (millions) 70$ 98$ 122$ 24$ 19$ -$

Bank line usage (millions) (period end) -$ 121$ -$ 134$ -$ -$

Bank line availability (millions) (period end) 650$ 779$ 900$ 766$ 900$ 1,100$

Capital Raised (millions):

Common equity, net 274$ 253$ 341$ 525$ 124$ 2$

Preferred equity, net 334$ (288)$ -$ (288)$ -$ -$

Unsecured notes, gross 350$ 400$ 700$ -$ 700$ 450$

Secured debt, gross -$ -$ -$ -$ -$ -$

Property dispositions, net proceeds 103$ 97$ 148$ 126$ 54$ 40$

Retained AFFO (after all dividends) 91$ 102$ 116$ 129$ 75$ 86$

21

Well-Laddered Debt Maturities

NNN’s Low Leverage Balance Sheet Strategy is Enhanced by its Well-Laddered Debt Maturities

$-

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

2021 2022 2023 2024 2025 2026 2027 2028 2030 2048 2050 2051

Mill

ion

s

3.9%

4.0%

3.6%

5.2 %

4.8% 3.1%

2.5%

5.2%5.2%

3.5% 4.3%

3.5%

Weighted average debt maturity of 13.0 years

22

Credit Facility and Notes Covenants

The following is a summary of key financial covenants for the company's unsecured credit facility and notes,

as defined and calculated per the terms of the facility's credit agreement and the notes' governing

documents, respectively, which are included in the company's filings with the Commission. These

calculations, which are not based on U.S. GAAP measurements, are presented to investors to show that as

of June 30, 2021, the company believes it is in compliance with the covenants.

Unsecured Credit Facility Key Covenants Required June 30, 2021

Maximum leverage ratio < 0.60 0.34

Minimum fixed charge coverage ratio > 1.50 4.27

Maximum secured indebtedness ratio < 0.40 0.001

Unencumbered asset value ratio > 1.67 2.96

Unencumbered interest ratio > 1.75 4.93

Unsecured Notes Key Covenants Required June 30, 2021

Limitation on incurrence of total debt ≤ 60% 36.5%

Limitation on incurrence of secured debt ≤ 40% 0.1%

Debt service coverage ratio ≥ 1.50 4.43

Maintenance of total unencumbered assets ≥ 150% 274%

23

Strong Investment Grade Balance Sheet

Long-Term Track Record of Success

Second Quarter Highlights

Low Risk Strategy Generates Consistent Growth

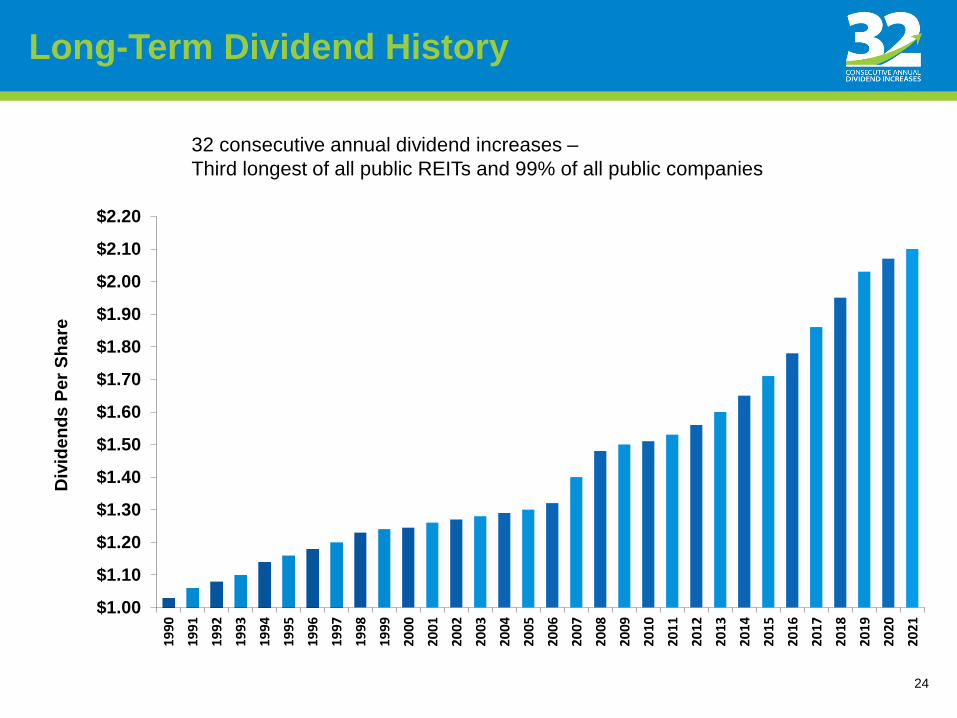

Long-Term Dividend History

24

$1.00

$1.10

$1.20

$1.30

$1.40

$1.50

$1.60

$1.70

$1.80

$1.90

$2.00

$2.10

$2.20

19

90

19

91

19

92

199

3

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

201

2

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

Div

ide

nd

s P

er

Sh

are

32 consecutive annual dividend increases –

Third longest of all public REITs and 99% of all public companies

25

Strong Investment Grade Balance Sheet

Long-Term Track Record of Success

Second Quarter Highlights

Low Risk Strategy Generates Consistent Growth

Second Quarter Highlights

26

Dividend yield at June 30, 2021 of 4.4%

Maintained high level of occupancy at 98.3%

Invested $102.9 million in property investments @ average 6.7% cap rate (initial cash

yield)

Sold 15 properties for $22.9 million

Maintained dividend payout ratio of approximately 68% of AFFO

Maintained significant balance sheet capacity and liquidity

Ended the quarter with $249.6 million of cash, no amounts drawn on $1.1 billion bank line

and no debt maturities until 2024

As of July 28, 2021, collected approximately 99% of rent originally due for the quarter

ended June 30, 2021

COVID-19 Update

NNN successfully continuing operations

IT systems investment paying off; most working in office; no layoffs/furloughs

Retail tenants challenged given prolonged continuation of business closures

and social-distancing practices

As of July 28, 2021, collected approximately 99% of rent for the quarter ended

June 30, 2021

Conservative balance sheet management and strong liquidity

Ended Q2 2021 with $249.6 million of cash, no amounts drawn on bank credit

facility and no debt due until 2024

Quality of Properties

Good retail real estate locations; historically high occupancy

27

Collections by Line of Trade

28

The following table details NNN’s rent collections received as of July 28, 2021, excluding the repayment of

amounts previously deferred according to the rent deferral lease amendments, by NNN’s top 20 lines of trade:

% of Total

% of Rent Collected

Quarter Ended Month Ended

Top 20 Lines Of Trade Annual Base

Rent(2)

March 31, 2021(1)

June 30, 2021(2)

July 31, 2021(2)

1. Convenience stores 18.0 % 100.0 % 99.9 % 100.0 %

2. Automotive service 11.4 % 99.5 % 99.7 % 99.8 %

3. Restaurants – full service 9.9 % 91.3 % 93.9 % 93.9 %

4. Restaurants – limited service 9.2 % 99.9 % 99.7 % 99.7 %

5. Family entertainment centers 6.1 % 99.9 % 99.9 % 99.6 %

6. Health and fitness 5.2 % 94.3 % 99.3 % 100.0 %

7. Theaters 4.6 % 77.1 % 94.9 % 98.2 %

8. Recreational vehicle dealers, parts and

accessories

3.5 % 100.0 % 100.0 % 100.0 %

9. Equipment rental 3.2 % 100.0 % 100.0 % 100.0 %

10. Automotive parts 3.1 % 100.0 % 100.0 % 99.4 %

11. Home improvement 2.6 % 99.5 % 100.0 % 97.0 %

12. Wholesale clubs 2.5 % 100.0 % 100.0 % 100.0 %

13. Medical service providers 2.2 % 99.6 % 98.6 % 97.1 %

14. General merchandise 1.7 % 99.4 % 98.7 % 100.0 %

15. Furniture 1.6 % 99.2 % 99.5 % 100.0 %

16. Consumer electronics 1.6 % 100.0 % 100.0 % 100.0 %

17. Home furnishings 1.6 % 100.0 % 100.0 % 100.0 %

18. Travel plazas 1.5 % 100.0 % 100.0 % 100.0 %

19. Drug stores 1.4 % 100.0 % 100.0 % 100.0 %

20. Bank 1.3 % 100.0 % 100.0 % 100.0 %

Other 7.8 % 99.6 % 98.6 % 95.9 %

Total 100.0 % 97.7 % 98.9 % 98.8 %

As a percentage of annual base rent, which is the annualized base rent for all leases in place. (1) $684,283,000 as of March 31, 2021.

(2) $689,364,000 as of June 30, 2021.

% of Total

% of Rent Collected

Quarter Ended Month Ended

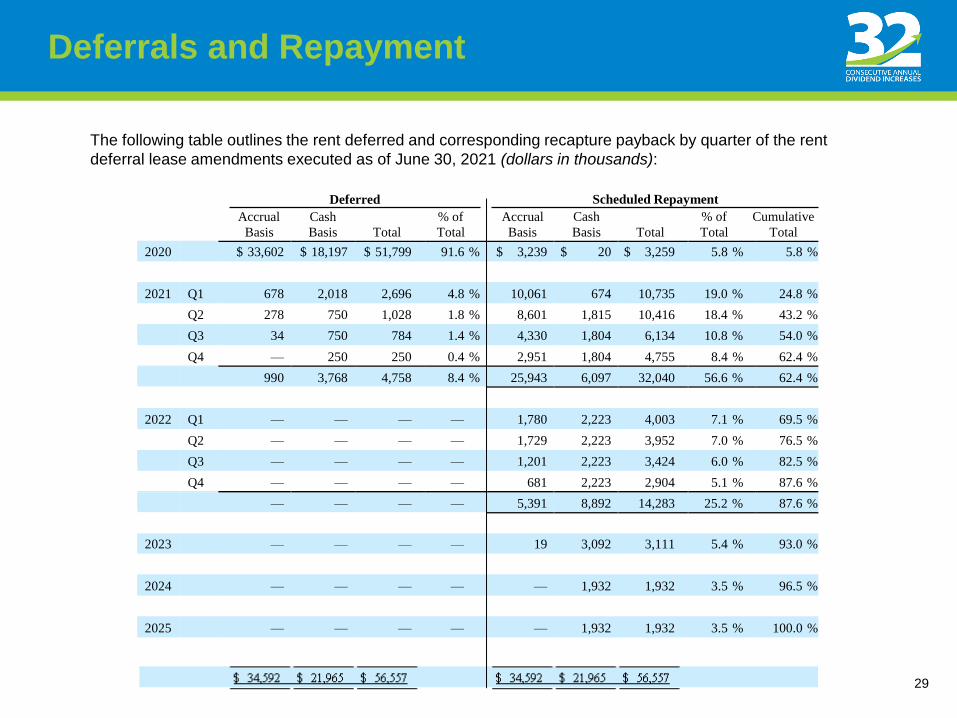

Deferrals and Repayment

29

The following table outlines the rent deferred and corresponding recapture payback by quarter of the rent

deferral lease amendments executed as of June 30, 2021 (dollars in thousands):

Deferred

Accrual Cash % of

Accrual

Scheduled Repayment

Cash % of Cumulative Basis Basis Total Total Basis Basis Total Total Total

2020 $ 33,602 $ 18,197 $ 51,799 91.6 % $ 3,239 $ 20 $ 3,259 5.8 % 5.8 %

2021 Q1 678 2,018 2,696 4.8 % 10,061 674 10,735 19.0 % 24.8 %

Q2 278 750 1,028 1.8 % 8,601 1,815 10,416 18.4 % 43.2 %

Q3 34 750 784 1.4 % 4,330 1,804 6,134 10.8 % 54.0 %

Q4 — 250 250 0.4 % 2,951 1,804 4,755 8.4 % 62.4 %

990 3,768 4,758 8.4 % 25,943 6,097 32,040 56.6 % 62.4 %

2022 Q1 — — — — 1,780 2,223 4,003 7.1 % 69.5 %

Q2 — — — — 1,729 2,223 3,952 7.0 % 76.5 %

Q3 — — — — 1,201 2,223 3,424 6.0 % 82.5 %

Q4 — — — — 681 2,223 2,904 5.1 % 87.6 %

— — — — 5,391 8,892 14,283 25.2 % 87.6 %

2023 — — — — 19 3,092 3,111 5.4 % 93.0 %

2024 — — — — — 1,932 1,932 3.5 % 96.5 %

2025 — — — — — 1,932 1,932 3.5 % 100.0 %

30

Appendix

NNN Attributes

31

Triple-net long-term leases

Small properties – typically $2 to $4 million investment size

High land value per asset

Net leases reduce volatility of returns – rent growth drops to bottom line

Large universe of investment opportunities

Fragmented non-institutional competition; NNN is a clear leader

Structured sale-leaseback acquisitions at great initial cap rates

Excellent capital recycling track record

Strong balance sheet with limited near-term maturities

Solid earnings profile with lower risk

32 consecutive years of increased annual dividends while reducing payout ratio

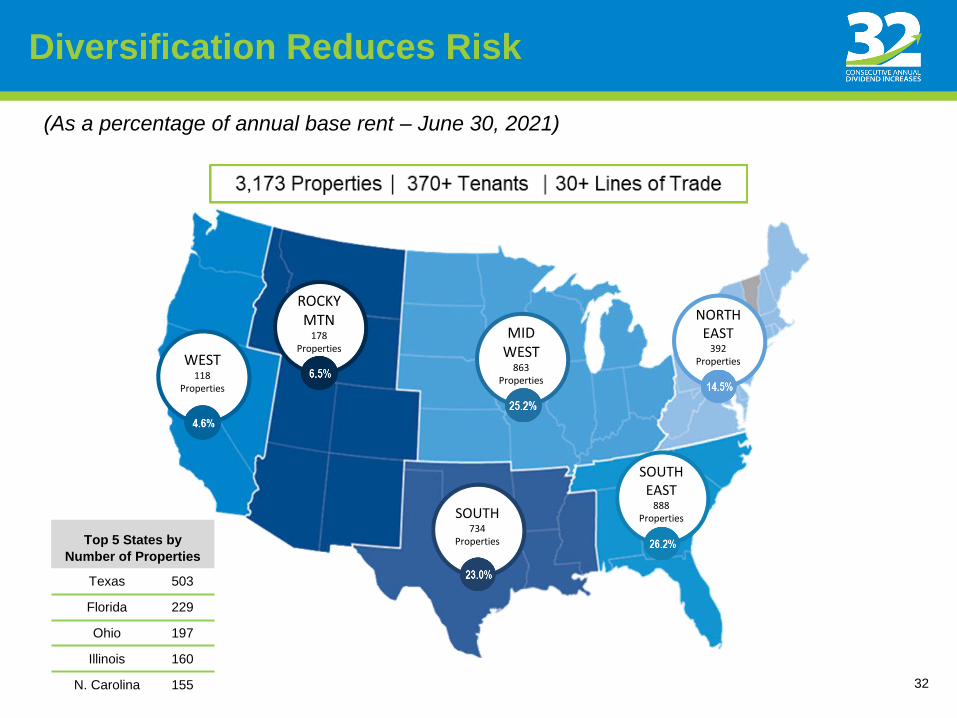

Diversification Reduces Risk

32

Top 5 States by

Number of Properties

Texas 503

Florida 229

Ohio 197

Illinois 160

N. Carolina 155

(As a percentage of annual base rent – June 30, 2021)

MID WEST

863Properties

WEST118

Properties

ROCKY MTN

178 Properties

NORTHEAST

392 Properties

SOUTH734

Properties

SOUTHEAST

888 Properties

33

Lease Expirations

(As a percentage of annual base rent – June 30, 2021)

0%

10%

20%

30%

40%

50%

60%

70%

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

The

rea

fte

r

Weighted average remaining lease term of 10.6 years

Only 8.5% of leases expire through 2023

Driving Per Share Growth -- Cost of Capital View Matters

Differing Views on the Cost of Equity in making Capital Allocation Decisions (all other variables the same)

NNN's View Other REITs' View

"Economic / Expected Return Cost of Equity" "Cash / Accounting Cost of Equity"

(inverse of FFO multiple driven)

Dividend yield 4.5%

Dividend per share growth 3.0 - 4.0%

FFO per share growth 3.0 - 5.0%

Weighting Cost Wtd Avg Weighting Cost Wtd Avg

Debt * 35% 2.20% 0.77% Debt * 35% 2.20% 0.77%

Preferred 5% 5.20% 0.26% Preferred 5% 5.20% 0.26%

Common 60% 8.00% 4.80% Common 60% 5.00% 3.00%

100.0% 5.83% 100.0% 4.03%

Reflects a focus on per share value creation Supports a focus on asset growth

Promotes selectivity Promotes lower return acquisitions

* Ten year, fixed rate debt only

34

Cost of Capital in Making Capital Allocation Decisions

23 Leases(95% of Prior)

19 Leases(107% of Prior)

22 Leases(87% of Prior)

31 Leases(101% of Prior)

16 Leases(79% of Prior)

39 Leases(95% of Prior)

39 Leases(87% of Prior)

32 Leases(101% of Prior)

40 Leases(100% of Pror)

139 Leases(101% of Prior)

46 Leases(103% of Prior))

58 Leases(97% of Prior)

81 Leases(104% of Prior)

76 Leases(100% of Prior)

66 Leases(87% of Prior)

$-

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$- $1,000,000 $2,000,000 $3,000,000 $4,000,000 $5,000,000 $6,000,000 $7,000,000 $8,000,000 $9,000,000

$10,000,000 $11,000,000 $12,000,000 $13,000,000 $14,000,000 $15,000,000 $16,000,000 $17,000,000 $18,000,000 $19,000,000 $20,000,000 $21,000,000 $22,000,000 $23,000,000 $24,000,000 $25,000,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

T.I

. /

Cap

ital E

xp

en

dit

ure

s

An

nu

al

Ren

t

Historical Lease Renewals (expirations within 18 months)

Prior Rent Renewal Rent T.I. / Capital Expenditures

35

Historical Lease Renewals

2007 through 2021:

84% of leases renewed – 727 leases out of 864 (199 tenants)

65% above prior rent, 24% below prior rent and 11% at prior rent

99% ($123.3 million) of prior rent ($126.7 million) – excluding 37 outliers, 101% of prior rent

$2.0 million of T.I./capital expenditures – not inclined to “buy” higher rent

36

Top 20 Lines of Trade

1. Convenience stores 18.0% 647 41 30 99.9%

2. Automotive service 11.4% 414 19 29 99.7%

3. Restaurants - full service 9.9% 426 77 38 93.9%

4. Restaurants - limited service 9.2% 568 56 34 99.7%

5. Family entertainment centers 6.1% 97 6 25 99.9%

6. Health and fitness 5.2% 33 2 17 99.3%

7. Theaters 4.6% 33 5 15 94.9%

8. RV dealers, parts and accessories 3.5% 38 1 20 100.0%

9. Equipment rental 3.2% 95 5 26 100.0%

10. Automotive parts 3.1% 155 6 33 100.0%

11. Home Improvement 2.6% 49 10 20 100.0%

12. Wholesale clubs 2.5% 11 1 6 100.0%

13. Medical service providers 2.2% 86 18 21 98.6%

14. General merchandise 1.7% 73 16 20 98.7%

15. Furniture 1.6% 44 14 20 99.5%

16. Consumer electronics 1.6% 17 2 14 100.0%

17. Home furnishings 1.6% 15 4 12 100.0%

18. Travel plazas 1.5% 25 4 6 100.0%

19. Drug stores 1.4% 32 4 16 100.0%

20. Bank 1.3% 57 5 9 100.0%

Other 8.2% 258 91 36 98.6%

Total 100.0% 3,173 98.9%

% Rent

Collections

Qtr. Ended

June 30, 2021(1)(2)

# of

Tenants

# of

StatesLine of Trade

% Base

Rent

# of

Properties

(As of June 30, 2021)

(1) Based on the annual base rent of $689,364,000, which is the annualized base rent for all leases in place as of June 30, 2021 (2) Rent collections received as of July 28, 2021, excluding repayment of amounts previously deferred according to rent deferral lease amendments

37

Top 20 Tenants

Properties % Base Rent

1. 7-Eleven 139 5.0%

2. Mister Car Wash 120 4.7%

3. Camping World 47 4.3%

4. LA Fitness 30 3.8%

5. GPM Investments (Convenience Stores) 153 3.3%

6. Flynn Restaurant Group (Taco Bell/Arby's) 204 3.2%

7. AMC Theatre 20 3.0%

8. Couche-Tard (Pantry) 83 2.7%

9. BJ's Wholesale Club 11 2.5%

10. Sunoco 59 2.2%

11. Mavis Tire Express Services 123 2.1%

12. Main Event 18 1.8%

13. Frisch's Restaurants 73 1.8%

14. Fikes (Convenience Stores) 56 1.6%

15. Chuck E. Cheese's 53 1.6%

16. Best Buy 16 1.5%

17. Bob Evans 106 1.5%

18. Life Time Fitness 3 1.4%

19. Dave & Buster's 11 1.4%

20. Ahern Rentals 35 1.4%

Tenant

(As of June 30, 2021)

38

Acquiring properties directly from tenants produces more efficient pricing and higher initial returns

NNN assesses discrete risks vs.

More risks/unknowns in value-add, development, or

Typical lower yielding real estate investment

Each deal is structured based on its unique characteristics:

Real estate attributes, tenant corporate credit analysis, asset (store) level data

NNN Acquisitions Approach has Multiple Advantages

39

NNN Approach to Net Lease Acquisitions

Real Estate

AttributesCorporate

Credit

Competitive positioning

Management team track

record / vision

Credit analysis / leverage

profile

Pending maturities

Use of transaction

proceeds

Fixed charge and rent

coverage

Property location

Underlying land value

Area demographics

Market rent / similar

transaction comparables

Location of competitors

Alternative use

Replacement cost analysis

Local market conditions

Parking

Access

Co-tenants

Visibility

Traffic counts

Age of improvements

Historical sales and

profitability

Sales & Profit trends

Revenue drivers and margins

Rent as a % of Sales

Corp. G & A allocation

Rent coverage

Comparison with similar

stores

Remaining lease term

Newest prototype

Capital markets

environment

Current conditions in

tenants’ industry /

market(s)

Local and national

economy

NNN cost of capital

Cap rate trends

Legislative risk

Transaction

Proceeds &

Terms

Asset-Level

Performance

Market

Conditions

Due Diligence and Determination of Proceeds & Terms

The chart to the right summarizes our areas of focus, which: a) determine our interest in a transaction, and b) drive our specific negotiation of the terms, rates and proceeds for each deal

This sale-leaseback approach to acquisitions produces multiple advantages for NNN versus many of our REIT peers, and particularly our shopping center / mall REIT competitors

Our ability to assess these discrete risks in a single-tenant, sale-leaseback transaction has allowed us to execute transactions with very efficient pricing, higher initial returns and more stable cash flows versus the higher and greater unknowns associated with: a) value-add investing, b) new construction / development transactions, and / or, c) lower-yielding, core retail investment strategies

40

NNN’s proven disposition platform strengthens portfolio quality and long-term earning by reinvesting at higher return rates

Highly productive proprietary www.nnn1031.com website enables property sales at premium retail pricing, at volumes far above other triple-net sellers:

Standardizes downloadable due diligence information and contracts

Technologically sophisticated but user friendly

Low cost to maintain

Since 2005, sold 710 properties generating net proceeds over $1.9 billion

Disposition expertise provides ability to sell properties:

That do not meet hold criteria

To better control tenant and line of trade concentrations

Making NNN a more attractive buyer

Enhances acquisitions returns via higher effective cap rate on retained properties

NNN’s Disposition Platform

350+ service hours annually

Great People in a Supportive Culture

41

• 3000+ online courses available to associates on NNNU

• Virtual conferences

• Professional webinars

• Cross training / job shadowing

Educational Seminars

• Cyber Security

• Women Talk Money & Financial Planning

• Vitality Health and Wellness

• Emotional Wellbeing

• Healthcare Consumerism

Learning & Development Community Engagement

Top fundraising team

for RMH virtual event

Proud to be a member of the 2021 GEI, committed to driving accountability

through data transparency.

42