ipaa oil & gas investment symposium april 20, 2004

TRANSCRIPT

IPAA

Oil & Gas Investment Symposium

April 20, 2004

2

Forward-looking Statements

This presentation contains projections and other forward-looking

statements within the meaning of Section 27A of the U.S. Securities

Act of 1933 and Section 21E of the U.S. Securities Exchange Act of

1934. These projections and statements reflect the Company’s

current views with respect to future events and financial performance.

No assurances can be given, however, that these events will occur or

that these projections will be achieved, and actual results could differ

materially from those projected as a result of certain factors. A

discussion of these factors is included in the Company’s periodic

reports filed with the U.S. Securities and Exchange Commission.

3

Good First Year…

• Combined the H&P and Key organizations– Grew our exploration staff by 45%

• Invested $160 MM in E&D (73% of Cash Flow)• Replaced production and grew our proved reserves• Strong earnings and cash flow– Net Income: $94.6 MM / $2.22 per share – Cash from operations: $217 MM

• No debt and over $40 MM of cash

4

Approach to the Business

• Consistent profitable growth

• Blended-risk exploration program

• Generate (versus buy) our own drilling inventory

• Some acquisitions, but not principle focus

• Multi-basin, lower-48 focus

• Local competitor and decentralized organization

5

Proved Reserves

By Region

422 Bcfe

Gulf Coast 11%

Western9%

Mid-Continent66%

Permian14%

PUD0.6%

PD99.4%

By Category

Oil 20%

Gas 80%

By Type

6

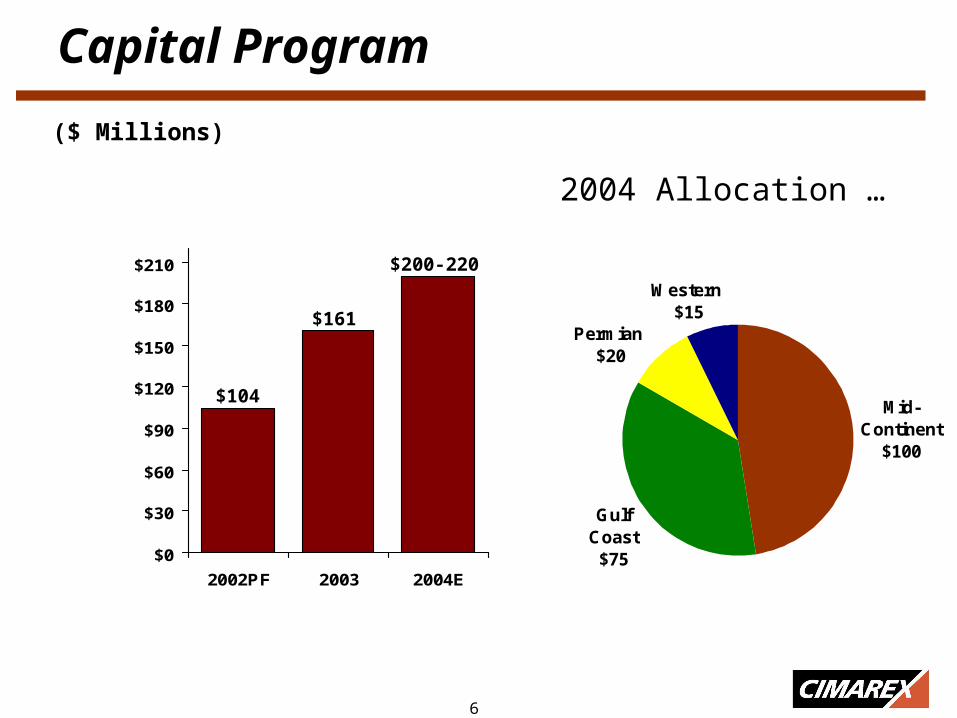

Capital Program

$0

$30

$60

$90

$120

$150

$180

$210

2002PF 2003 2004E

Mid-Continent

$100

Gulf Coast

$75

Permian $20

Western $15

2004 Allocation …

($ Millions)

$161

$104

$200-220

7

Strong Momentum Into 2004…

21.627.0

30.4

44.7

57.4

0

10

20

30

40

50

60

70

4Q02 1Q03 2Q03 3Q03 4Q03

Exploration and Development Expenditures

($ Millions)

8

Expanding Production

MMcfe Per Day

0

40

80

120

160

200

240

4Q02 1Q03 2Q03 3Q03 4Q03 1Q04 2Q04 3Q04 4Q04

180187

179 172181

185-195

190-205

200-215

205-220

Est. Est. Est. Est.

9

Key Principles

• Each region will be a top competitor

• Regional effort built upon local expertise

• Drilling program with mostly moderate risk prospects

• Close integration between geology, land, and engineering

• Monitor results and provide continuous feedback

10

West Gueydan Miogyp

Williston Basin

Yegua/Cook Mtn

North San Joaquin Basin

Anadarko Basin

A Diversified Approach

Permian / SENM

South Texas

Mountain Front

11

Mid-Continent/Permian Operations

• Capital ($MM): MC PB •2003A: 88 9•2004E: 100 20

• Gross wells: MC PB•2003A 148 7•2004E 175 25

Hugoton

Anadarko

Hardeman

Arkoma

Mt. Front

Permian

• Long-term player in western Oklahoma

• New and expanding program in the Permian Basin

12

Mid-Continent Progress

0

10

20

30

40

50

60

70

80

90

1996 1997 1998 1999 2000 2001 2002PF 2003 2004E

Gross Wells 45 56 41 51 51 56 98 148 175

Net Wells Drilled

Net Wells 6.6 11.7 13.2 16.0 24.4 24.3 52.0 70.5 85.0

Success Rate 89% 86% 76% 78% 80% 85% 93% 88% 90%

13

Anadarko Basin Targets

• Multiple targets at moderate depths

• Long-term deep potential

• Extensive acreage position

• This will continue to be a core drilling area

Granite Wash 10,000 ft.

Red Fork 12,500 ft.

Morrow 16,500 ft.

Springer 19,000 ft.

Hunton 20,000 ft.

Atoka 15,000 ft.

14

South Louisiana - West Gueydan Project

Riceville (1991)

115 Bcfe - 3 wells

South Lake Arthur (1980) 840 Bcfe - 23 wells

SE Gueydan (1970)

205 Bcfe - 11 wells

West Gueydan

Project Area

• Focus area is Camerina & Miogyp Trend

☼

0 1 2 3miles

CAMERINA & MIOGYP TREND

15

West Gueydan Prospects• Mauboules #1 discovery

– Miogyp formation at 17,500’ – First production: March 2004– Producing 24 MMcf/d and 370

BOPD– 64.5% WI / 46.4% NRI

• Mauboules #2 is currently drilling• Reserve Potential:

– 30-40 Bcfe gross (15-20 net)– #1 well – 15 Bcfe proved (7

net)• Other 2004 drilling

– Jelly prospect (64.5% WI)– Rangoon prospect: Spud April

11 (47.5%WI)

Mauboules #1

First sales: March 1

Jelly Prospect

15 - 20 Bcfe potential

Verm

ilion

Paris

h

Salt

Mauboules #2

Currently Drilling

Rangoon Prospect

Currently Drilling

16

Mauboules 1Upper Zone:

Miogyp A55.0’ Pay

Lower Zone: Miogyp B

21.5’ Pay

17

Mauboules Potential

Mauboules 1

Mauboules 2

A

B

Upside – 40 BCFE

12.5

12.0

3.0

Lowest known gas

Downdip potential

Pay on water

Proved

11.0

Proved

Potential

Potential

1.5

18

Cook Mountain Project – SE Texas

Liberty

Hardin

Jefferson

ChambersHarris

Trinity

Raywood

Moss Bluff

Hathaway

RaywoodSouth

Bauer Ranch

Cook Mountain Prospects

Yegua Prospects

Raywood Field

• 600 sq mi of 3D data

• 2003: 6 gross wells / 4 net wells ($18MM)

– Brookhollow tested5 MMcf/d & 300 BOPD

– Henderson #1 producing 10 MMcf/d and 700 BOPD

– Henderson #2 producing 6 MMcf/d and 325 BOPD

• Aggressive 2004 plans

– Ten or more locations ($20–25MM)

• Wells are:

– 12,000–15,000 feet deep

– $2-3 MM gross

19

Henderson 1:6000 MCFD, 300 BOD

20

Henderson Prospect – Liberty County

• Hathaway 3-D seismic survey

• 82% WI / 60% NRI• Henderson #1 – 13,800 foot Yegua

discovery in Nov. 2003– 4.3 Bcfe net proved

• Henderson #2 on production March 2004

• Potential Reserves (Bcfe)– 12-15 gross– 7-9 net

Henderson 2

2004 offset

Henderson 1

2003 discovery

21

Recap

• Right size to participate in meaningful exploration and acquisition projects

• Small enough to grow through drilling

• Strong cash flow, no debt and un-hedged

• Rising production profile from organic growth

• Solid 2003 drilling program

• Strong 2004 inventory and building momentum for 2005

22

CONTACT INFORMATION

Paul Korus

Cimarex Energy Co.

707 Seventeenth Street, Suite 3300

Denver, CO 80202-3404

Phone (303) 295-3995

Fax (303) 285-9299

www.cimarex.com