issue - ii • volume - vii • november - 2011 update

TRANSCRIPT

• ISSUE - II • VOLUME - VII • NOVEMBER - 2011

UPDATE

www.bizsolindia.com

UPDATE

THISMONTH

4U

November - 2011 W E B E L I E V E I N

IN THIS ISSUE

We believe in C-2

This Month 4 U C-2

Editorial 1

What's New 3

Sub-Contracor at per with Main Contractor in the service tax regime

..By Ashok B Nawal 21

Beyond the Onvious 23

Did you Miss this 29

Our Services 30

CSR C 3- 4

Payments Due Dates

Excise Duties-Oct 2011 05/11/11

Service Tax – Oct 2011 05/11/11

Excise Duties- Oct 2011 By E-Payment 06/11/11

Service Tax -Oct 2011–By E Payment 06/11/11

TDS/TCS- Oct 2011 07/11/11

Provident Fund-Oct 2011 15/11/2011

Central Sales Tax –Oct 2011Return-cum-Challan 21/11/2011

VAT – Oct 2011 21/11/2011

ESI Contribution 21/11/2011

Professional Tax 30/11/2011

Returns

ER-1 and ER-2 Monthly Return for Oct 2011 10/11/11

ER-4- 2010-11 30/11/11

ER-6- Oct 2011 10/11/11

E D I T O R I A LIt is an irony that once again the Greek Tragedy is

taking centre stage (pun intended). The only difference

now is that the phrase that was associated with a form of art

which in a way enthralled the audience is now refers to an

impending economic catastrophe. It also brings into sharp

focus the limits of capitalism in whichever form it is practiced

and the constraints of trade blocks, however well

intentioned they might be. Greece almost succeeded in

bringing the Euro Zone to its knees. By itself Greece may

be a tiny economy not capable of bringing down the

economic might of Europe but it holds out ominous

warnings to the entire Euro Zone which has countries like

Italy, Spain and Portuguese on the verge of bankruptcy. For

those outside it is a fascinating story unfolding. In a

tottering economy political stability becomes the first

casualty. Unpleasant decisions are called for, and the

layman has to have unshakable faith in the economist - tall

order indeed. With austerity measures and economic

sacrifices it is bound to test the limits of patience of the

population of any country. But Greece can take heart that if

Argentina and Russia could come out of such crises there is

still hope for Greece. Probably it will. But the real issue is

how many such passenger states the Euro Zone can afford

to carry. Austerity measures and fiscal sacrifices cannot

obviously be popular with the population of any country.

Consequently in these crisis times good economics is

disastrous politics – a modified cliché. Apparently the

whole thing looks like a case of economic mismanagement

and its consequences. It is definitely so; but what is more

important is that this crisis has shown the structural

deficiencies of the Euro Zone itself. The Euro Zone is all

about economic unification. But the Zone has no control or

influence over the social, cultural and political dynamics of

the member countries. How do you fix the economy of a

country without influencing the society first? As we go to

press there are rumours that a former Deputy President of

the European Central Bank is going to head the national

government. One is not sure whether the people of that

country know what is happening in India with a similar

experiment with an eminent economist at the helm in

government!

Staying abroad for a moment more let us look at what

happened at the recent G20 Summit. It was indeed a

Summit of disaster with the member countries working only

on a single point agenda of how to word the final joint

communiqué without the world knowing that it was indeed a

disaster. The one and only redeeming feature of the Summit

was the effort of the only non-government attendee of the

Summit who goes by the name Bill Gates. His pitch for a

financial transaction tax and his demand for the need to give

further thrust to education went largely unreported,

unnoticed and unheeded. After all, the heads of

governments are politicians first and their survival is more

important than their country's interest. It was touted at the

beginning of the Summit that it will fix the problem of Greece.

But the non European member countries knew better and

they refused to be drawn into this quagmire and they smartly

left it to the European Union to sort their own problems.

The instability in the world around us suddenly looks

quite scary. The Arab Spring, the Anna campaign, the

London Riots, the Chinese protests (they also protested!)

and now the 'Occupy-Wall-Street' movement. At no point in

time in living memory has there been such an upheaval

around the world at the same time. Rising food prices, huge

unemployment, lack of economic growth, rampant

corruption, governance deficit and a general sense of

disenchantment with the way the world operates have

brought the people of the world to the streets. It may be

manifesting in different ways; but in essence it appears to be

a movement of the people, for the people, by the people but

against the ruling dispensation. One has to wait and watch

what the future portends.

It would be fascinating to interview Ramalinga Raju of

Satyam fame after his recent release from the prison on bail.

After getting out of the prison he would have definitely

regretted his foolishness of admitting to committing frauds

and getting criminal actions initiated against him. He must

be feeling strange that when he is coming out of jail even if on

bail there are corporate executives making a beeline to the

prison and some others outside waiting in queue – all in the

name corporate governance or the lack of it. The venerable

names of Tatas, Ruias, Ambanis, Singhs, etc., etc., are all

there blemished and bruised beyond recognition. Raju must

be thinking that he happened to the unfortunate first fall guy

to go jail and earned an unfair adverse publicity.

November - 2011

1

November - 2011

2

When a government becomes a burden what does

the society do? They obviously fight back. When the civil

society falls apart what does the citizen do? This is not a

question for a quiz competition. In India governance has

virtually come to a standstill. The ruling party and

government are mired in corruption. The so called Civil

Society is falling apart. Economic reforms are a thing of the

past. Thanks to global factors inflation cannot be held in

check. When a common man is wondering how to find the

money for the next meal, the bureaucrats are struggling to

put together a formula to live within Rs.32/- a day! The

governments in the Euro Zone are imploding primarily

because of the decay which has set in their society. India is

no different. But then, whose country is it any way? It looks

like all of us trying to live up to the expectations of Winston

Churchill who once not-so-famously said 64 years ago that

we will become a corrupt nation run by politicians with

questionable integrity.

Next time if you happen to be in Pakistan, be careful

before you board an auto. It may be ferrying a mated

nuclear war-head along the busy and congested roads of

Pindi or Karachi. If a new article in “The Atlantic” is to be

believed, the Pakistani army is so scared of the Americans

after the latter's Obama operation that they constantly keep

shifting their nuclear arsenals either in mated or de-mated

conditions from one site to other without the knowledge of

the Americans. Conventional convoys which are visible to

the American satellites are, therefore, ruled out. We are

indeed living in dangerous times.

When a celebrity dies you mourn his death. You may

also feel bad that an eminent person passed away. But last

one month or so one got to see a few obituaries which went

beyond the normal passing away of a person. First it was

the Nawab of Patuadi. He continues to be a Nawab for an

entire generation even if the Government does not

recognise this title. Then there was Jagjit Singh. Before him

gazelles as a musical art form was not known to the aam

aadmi. It was he who popularised this music form to the

common man. If someone deserves to be called an inventor

of the future it was Steve Jobs. I knew none of them. They

did not have a chance of knowing me either. But in all these

cases I did indeed feel a sense of personal loss. This feeling

goes beyond the confines of a wreath. The feeling of this

sense of loss was indeed real and intense. They affected my

life in some way or other. When one feels bad when

somebody dies, it is never personal; but when one feels sad

at somebody's passing away it is indeed personal. Through

these columns I pay homage to these people who must have

affected a lot of people like me. Long live their souls in

heaven and long endure their work on earth.

Thank you.

Venkat R Venkitachalam

What's New…!!CUSTOMAnti Dumping Duty:

•Anti Dumping Duty on imports of Caustic Soda,

originating in, or exported from, Korea RP is

continued at reduced rate specified in the

notification and will be effective till 25th December,

2013 (CUS NTF NO. 94/2011 DATE 03/10/2011)

and (CUS NTF NO. 95/2011 DATE 03/10/2011)

•Anti Dumping Duty on Rubber Chemical PX-13

(6PPD), originating in, or exported from, Korea RP

(Heading 29,38) is continued at increased rate

specified in the notification and will be effective till

4th May, 2013 (CUS NTF NO. 92/2011 DATE

20/09/2011) and (CUS NTF NO. 93/2011 DATE

20/09/2011)

Tariff Notification

•All goods of the Chapter Heading 08041020 &

08041030 are included in the exemption

notification 21/2002 (Customs) and the rate of the

duty is brought down to 20% form 30%. (CUS NTF

NO. 97/2011 DATE 13/10/2011).

•Islamic Republic of Afghanistan has been included

as one of the beneficiary countries under SAFTA

(CUS NTF NO. 96/2011 DATE 12/10/2011)

Non-Tariff Notification

•CBEC revises tariff value of poppy seeds and brass

scrap (all grades) from 4241, 3061 to 3952 and

2207 respectively. (CUS NTF NO. 73/2011 (NT)

DATE 14/10/2011) and (CUS NTF NO. 71/2011

(NT) DATE 30/09/2011) CUS NTF NO. 76/2011 NT

Dt. 31/10/2011

•New duty drawback for certain items has been

notified after receiving representation also

correction in corresponding drawback Serial No.

against DEPB Serial No. has been amended.

Details are given separately in this issue.

Notification No. - 75 / 2011 - CUSTOMS (N.T.) dt.

28.10.2011

•On-site Post Clearance Audit at the Premises of

Importers and Exporters Regulations, 2011 has

been issued by CBEC. Under this regulation the

department will be authorized to conduct Audit of

Imports & Exports document and records

maintained for 5 years. (CUS NTF NO. 72/2011

(NT) DATE 04/10/2011)

•Exchange Rate for the month of October, 2011

related to Import/export goods is notified vive CUS

NTF NO. 70/2011 (NT) DATE 28/09/2011.

•The Customs, Central Excise Duties and Service

Tax Drawback Rules, 1995 has been amended by

issuing Customs, Central Excise Duties and

Service Tax Drawback (Amendment) Rules, 2011

and many more goods have been included in the

list on which the duty drawback will be now

available. (CUS NTF NO. 69/2011 (NT) DATE

22/09/2011)

Circulars:

•Re-Export of goods imported under reward

schemes and DEPB – Re-credit of duty –(CUS CIR

NO. 45/2011 DATE 13/10/2011) is now allowed

subject to following condition.

(I) re-export of goods shall take place from the same port from where the goods were imported

(ii) the goods are re-exported within 6 months from the date of import

(iii) the Asstt. /Dy. Commissioner of Customs

November - 2011

3

been made at par i. e. above Rs 5 lakhs and upto Rs

50 lakhs. [Circular No. 957/18/2011-CX-3 dated

25.10.2011]

•DG (Systems) has prepared comprehensive

instructions outlining the procedure for electronic

filing of Central Excise duty and Service Tax returns

and electronic payment of taxes under ACES and

enclosed to this Circular. Further it is also requested

that the trade and industry may be provided all

assistance so as to help them in adopting the new

procedure.. [Circular No. 956/17/2011-CX dated

28.09.2011]

SERVICE TAXNotification

•CBEC is empowered to prescribe the documents

required for registration under service tax and to

extend the period for filling the service tax return by

way of Order. Also provided that for the purposes of

ST-3 Form, the words “received /paid” used herein

shall be construed as “received or receivable /paid or

payable', as the case may be, in terms of the Point of

Taxation Rules, 2011 [Notification No. 48/2011 – ST

dated19.10.2011]

•CBEC extended the date of submission of half yearly

return for the period April 2011 to September 2011 th thfrom 25 October 2011 to 26 December 2011.

[Order No.1 ST dated 20.10.2011]

Circulars

•Service tax is not leviable on the works contract

service provided by sub-contractor to the main

contractor for completion of the main infrastructure

projects of execution of works contract in respect of

roads, airports, railways, transport terminals, bridges

tunnels and dams. [Circular No. 147/16/2011 –

Service Tax dated 21.10.2011]

Please read detailed article on the subject in this

issue.

FOREIGN TRADE POLICYDGFT Notifications

•Export of non-Basmati rice under Food Aid

Programme is permitted freely by Public Sector

Undertakings or by government organizations also.

is satisfied about the identity of the goods

(iv) The goods are not put into use after import

(v) At the time of allowing the re-export, Customs shall issue a re-credit Certificate containing particulars of scrip used, date of import of re-exported goods and amount debited while importing such goods. There

shall be no need for issue of fresh scrip in such

cases by DGFT regional offices

(vi) Customs shall permit use of the said re-credit

amount to the extent of 98% only; (vii) The validity

of re-credit certificate shall be for six months from

the date of issuance of re-credit certificate; and

(viii) The remittances have to be properly

accounted for as per the prevalent guidelines for

the import and the export of the goods.

•After notifying new duty drawback rate (All Industry

Rate) number of representation were received

and merit representation has been considered and

new rates has been notified for such merit

representation. Similarly it has been clarified that

when export are made against fulfillment of export

obligations under Advance Authorization / DFIA

then All Industry Rate will not be applicable but

drawback can be claimed under Brand Rate

Fixation (Circular No. – 48/2011-Customs) Dt. st31 Oct-2011]

•Subsequent to supreme court decisions with

respect to issuance of Show cause notice by

DGCEI / DRI which has been set a side on the

grounds of authority and subsequent amendment

in the Act, instructions have been issued for

reissuing the show cause notice by the respective

Commissionerate wherever these are not hit by

time limitation. (CUS CIR NO. 44/2011 DATE

23/09/2011)

CENTRAL EXCISETariff

• No new Notification

Non Tariff

•No new Notification

Circulars

•The monetary limit for adjudicating cases by Joint

Commissioners / Additional Commissioners had

November - 2011

4

comprehensive.

(ii) Exporters would now be required certify both (a)

that the items have been obtained/sourced from an

APEDA registered integrated abattoir or from

APEDA registered meat processing plant and (b)

that the raw material have been sourced exclusively

from APEDA registered integrated abattoir/abattoir.

(iii) Designated Veterinary Authority of the State are

now authorized to issue the certificate on the basis of

the inspections carried out by Veterinarians duly

registered under the Indian Veterinary Council Act

1984 employed by the exporting unit in relevant

laboratories. [Notification No. 82(RE-2010)/2009-st2014 Dated 31 October, 2011]

•In relaxation of the prohibition 1053.625 MTs of

Casein and Casein products already manufactured

on or before 18.02.2011 would be permitted to be

exported. [Notification No. 83(RE-2010)/2009-st2014 Dated 31 October, 2011.]

•The Status Holders shall also be eligible for the

Status Holders Incentive Scrip on exports made

during 2012-2013. [Notification No. 84(RE-st2010)/2009-2014 Dated 31 October, 2011.]

DGFT Circulars• DFIA authorizations issued on or after 13.10.2011

will be transmitted by DGFT 'on-line' to Customs.

Policy Circular No. 41 (RE-2010)2009-14 dated th13 October, 2011

•Only 33 items are eligible to get FPS benefit under

heading “Technical Textiles” as per Sr.No.33, of

Table 4, Appendix 37D of HBPv1. The list of 33

items, so eligible, is in the Annexure to this Policy

Circular and this list is applicable for export made

with effect from 01.04.2011. Policy Circular No. 42 st(RE-2010)/2009-14, 21 October, 2011

•Implementation of bar coding on tertiary packing of

consignments of pharmaceuticals and drugs for

export with effect from 01.10.2011 provided vide

Public Notice No. 59 dated 30.06.2011 is

compulsory for pharmaceuticals and drugs

manufactured on or after 01.10.2011. Policy thCircular No. 43 (RE-2010)/2009-14 Dated the 25

October, 2011.

Export of non-Basmati rice under agreement

between India and Maldives will be permitted.

Notification No 76 (RE – 2010)/2009-2014 dated rd23 Sept. 2011.

•Prohibition on export of edible oils has been

extended upto 30.09.2012. But, this restrication will

not apply to relaxations/exemption granted through

any earlier notifications. Export of fish oil continues

to be free as per Notification No. 60 dated

20.11.2008. Notification No 77 (RE – 2010)/2009-th2014 dated 28 Sept. 2011.

•Export of cotton waste including yarn waste and

garneted stock [ITC(HS) Code 5202] will continue

to be free. Registration of contracts for cotton

waste is not required now. Notification No. 78 th(RE-2010)/2009-14 dated 10 October, 2011.

•Export of products to notified countries (in Table 3 of

Appendix 37C of HBPv1) will be entitled for

additional duty credit scrip @ 1% of FOB value of

exports (in free foreign exchange) made with effect

from 01.04.2011 and Focus Products notified under

Table 8 of Appendix 37D shall be granted additional

duty credit scrip @ 1% of FOB value of exports (in

free foreign exchange) for exports made with effect

from 01.10.2011 till 31.03.2012. detailed analysis

on FTP has been covered in separate section in this

update. Notification No. 79(RE-2010)/2009-2014 thdated 13 October, 2011.

•The import of “Radioimmunoassay kits” (Medical

equipments containing radioactive isotopes) will

not require an import authorization from DGFT.

However, prior permission of AERB will be

required. Notification No. 80 (RE-2010)/2009-th2014 17 October,2011.

•Conditions for issue of import licenses of Rough

Marble Blocks for the balance quantity for Financial

year 2011-12 has been issued. Notification No. st81(RE-2010)/2009-2014 Dated 21 October,

2011.

•(i) All the amendments/changes made in Chapter 2

between August 2009 and September 2011 have

been incorporated in this notification to make it

5

November - 2011

Sr. No. / Table

VKGUY Product

Code

ITC HS Code

Items

3 [Table 1A]

3 Chapter 07 Edible vegetables (Table 1A)

15 [Table 1B]

15 15153090 Castor oil and its fractions- other than edible grade (Table 1B)

18 [Table 2]

18"Chapter 03,

1604 and 1605"

Marine Products (Table 2)

6

November - 2011

•Vide Circular No.4/2004-Cus. dated 16.1.2004

the facility to allow the conversion of free shipping

bills to export promotion schemes were

withdrawn. In this background, instructions were

issued to the Regional Authorities not to grant

DEPB benefits against such shipping bills which

were converted by the Customs authorities.

Some of the exporters approached High Courts

claiming that DEPB should be given in cases

where the conversions have been allowed by

Customs. Therefore, between the two material

dates i.e. between 28.1.2003 and 15.1.2004, in

case if the Commissioner of Customs has already

allowed the conversion of free Shipping Bill to

DEPB Shipping Bill, the DEPB claims can be

admitted. Accordingly, RAs are instructed to

decide the admissibility of DEPB claims. Old

cases which were rejected can also be reviewed.

Policy Circular No. 44 (RE-2010)/2009-14

dated 01.11.2011

•For the payment of compounding fees for

shortfall of export obligation to the extent of 1% of

FOB of exports in INR will be calculated based on

shortfall in foreign currency and exchange rate

considered at the time of issuance of Advance

Authorisation.. Policy Circular No. 45/2009-

2014 (RE 2010 Dated: 8th November, 2011

•Advance Author izat ion (on and af ter

01.04.2009), Export Promotion Capital Goods

(on and after 01.04.2009), Duty Free Import

Authorization (on and after 13.10.2011) and

DEPB (which is on EDI mode for almost 6 years).

Only these authorizations are therefore available

for 'on-line' verification. Other authorizations i.e.

Annual Advance Authorization, Annual EPCG,

SHIS, restricted / SCOMET import / export

authorization, Chapter 3 Reward Scheme are yet

to be covered under message exchange with

customs. Therefore, these authorizations need

to be registered / operated by custom on

production of physical copy of authorization only

with no 'on-line' verification. Policy Circular No. th46 (RE 2010) 2009-14 Dated 8 November,

2011.

•the following procedure to grant DEPB on the

export of “Cotton yarn including Melange yarn”

made between the period from 01.04.2011 to

04.08.2011 and on the export of “Cotton” made

between the period from 01.10.2010 to

04.08.2011 on the basis of “Free Shipping Bills”: -

(I) The exporters will apply to RA by feeding the details

of the “Free Shipping Bill” manually on their on-line

application;

(ii) A hard copy of the “Free Shipping Bill”, duly attested

by the exporter will be submitted to the RA.;

(iii) On the basis of the export description given on the

shipping bill, the RA will decide whether that export

product is entitled for DEPB or not; and

(iv) If the RA is satisfied that description of the export

product in the shipping bill is the same as in the

relevant DEPB entry, based on the FOB value of

the shipping bill/Bank Realisation Certificate

(BRC), the DEPB will be issued. Policy Circular

No. 47 (RE-2010)/2009-14 Dated: 08.11.2011 v

Public Notices

•5,175 MTs of raw sugar is permitted to be exported to

USA under Tariff Rate Quota by M/s. Indian Sugar

Exim Corporation Ltd. Export must be completed by

31.10.2011. Public Notice No. 78 (RE-2010)/2009-nd2014 dated 22 September, 2011.

•Regional Authorities (RAs) would now allow clubbing

of Advance Authorisations. This is a decentralising

measure. The exporters will not be required to

approach DGFT Headquarters in cases covered

under the above categories. Public Notice No. 79 th(RE-2010)/ 2009-14 Dated 13 October, 2011

•Amendments in the Reward/Incentive Schemes of

Chapter 3 of FTP 2009-14:- Appendix 37A, Appendix

37C and Appendix 37D of Handbook of Procedure

Vol.1 has been made. PUBLIC NOTICE No. 80 th(RE2010)/2009-14 Dated 13 October, 2011. Details

are given below.

In Appendix 37A of Vishesh Krishi and Gram Udyog

Yojana (VKGUY), the following products are deleted

from Table 1A, Table 1B and Table 2 respectively with

immediate effect:

8

9

10

11

Sr. No.

FPS Product Code

ITC (HS) Code Description LINKED MARKETS FOR FOCUS PRODUCTS

108 108 87019090 Agriculture Tractors having capacity in excess of 1800 cc.

Turkey

109 109 8402 High Pressure Boilers and Parts of High Pressure Boilers

"Egypt, Kenya, Tanzania, South Africa, Brazil”

110 110 840290 Parts of High Pressure Boilers

111 111 84029090 Other - High Pressure Boilers and Parts of High Pressure Boilers

112 112 8406 Steam Turbines and Vapour Turbines

113 113 84069000 Parts of Steam & Vapour Turbines

114 114 843830 Machinery for Sugar Manufacture

115 115 84389010 Parts of Sugar Manufacturing Machinery

116 116 84389090 Other Sugar Plant & Machinery and Parts thereof

117 117 847420 Plant & Machinery for Mineral Crushing and Grinding

118 118 84749090 Parts of Plant & Machinery for Mineral Crushing and Grinding

119 119 3215 "Printing Ink, Wring / Drawing Ink and Other Ink W/N Concentrated or Solid"

"Algeria, Egypt, Kenya, Nigeria, Tanzania, South Africa, Ukraine, Brazil, Australia, New Zealand, Cambodia,

Vietnam, China and Japan"

120 120 Chapter 61 & 62

Apparels i.e. Readymade Garments USA-Only for Exports upto 31.03.2012

121 121 Chapter 61 & 62

Apparels i.e. Readymade Garments EU-Only for Exports upto 31.03.2012

TABLE 6: NEW MARKET LINKED FOCUS PRODUCTS

•The following products are added in Table 6 of Appendix 37D (New MLFPS), for exports made with effect from

01.04.2011. Mexico is deleted from Table 3 and Table 6 of MLFPS from the date of this Public Notice.

12

•Liquid Paraffin can also be imported as an alternate input for manufacture of certain export products in thPlastic Product Group. PUBLIC NOTICE NO. 81 /(RE-2010)/2009-2014 Dated 14 October, 2011.

•Procedure for sale or transfer of imported firearms is simplified and prior permission from

DGFT is dispensed with in respect of some categories. Public Notice No. 82 /2009-2014 (RE-th2010) Dated 17 October, 2011

•Special Bonus Benefit for exports made from 01.10.2011 till 31.03.2012 will be available for the

specified product as per list published in Appendix 37D. List is separately given. PUBLIC NOTICE NO.83 st(RE2010)/2009-14 DATED 31 October 2011.

November - 2011

13

The following products are added in Table 7 of Appendix 37D (Focus Product Scheme) for exports made with effect

from 01.04.2011:

Sr. No. FPS Product Code

ITC (HS) Code Description

170 170 39232100 Sacks & Bags of Polyethylene (Incl Cones)

171 171 72024900 Other Ferro- Chromium

TABLE 7 : FOCUS PRODUCT(S) /SECTOR(S) - B O N U S B E N E F I T S

Sr. No.

FPS Product Code

ITC (HS) Code

Description

1 1 720292 Ferro Vanadium

2 2 720310 Ferrous products obtained by direct reduction of Iron Ore

3 3 73110010 Liquefied Petroleum Gas (L.P.G.) Cylinder

4 4 73259920 Other Cast Articles of Alloy Steel Malleable

5 5 73259930 Other Cast Articles Stainless Steel Malleable

6 6 7410 "Copper Foil (W/N Printed or Backed With Paper, Paper board, Plastics or Similar Backing Materials) of a Thickness (Excl Backing) <=0.15 MM)"

7 7 8201 "Hand Tools like Spades, Shovels, Hoes, Forks, Axes & Similar hewing Tools Secateurs-Any Kind knives, Hedge Shears Etc Used in Agriculture/Forestry"

8 8 820210 Hand Saws

9 9 820310 "Files, Rasps & Similar Tools"

10 10 820320 "Pliers, Pincers, Tweezers & Similar Tools"

11 11 8204 Hand Operated Spanners & Wrenches (Including Torque Meter Wrenches But Not Tap Wrenches); Inter Changeable Spanner Sockets With Or Without Handle

12 12 8205 "Hand Tools (Including Glaziers Diamonds) NES Blow Lamps; Vices, Clamps, Other Than Accessories & Parts of Machine Tools; Anvils; Portable Forges Etc"

13 13 821220 Safety Razor Blades Including Razor Blade / Blanks in Strips

14 14 82121010 Twine Type Shaving System

15 15 821410 "Paper knives, Letter Openers, Erasing knives, pencil sharpeners & Blades Therefor"

16 16 84148011 Gas Compressors of a Kind used in Air Conditioning

17 17 84143000 Compressors used in Refrigerating Equipment

18 18 842620 Tower Cranes

19 19 8447 "Knitting Machines, Stich bonding machines and machines for making gimped yarn, tulle, lace, embroidery, trimmings, braid or net and machines for tufting"

20 20 85119000 Parts of Articles of Heading 8511

21 21 853521 Automatic Circuit Breakers For a Voltage of less than 72.5 KV

22 22 87060031 Chassis for 3-Wheeled Vehicles Heading 8703

TABLE 8 : SPECIAL BONUS BENEFIT @ 1% OF FOB VALUE OF EXPORTS (IN FREE FOREIGN EXCHANGE)

14

Sr. No.

FPS Product Code

ITC (HS) Code Description

23 23 870422 G.V.W. exceeding 20 tonnes : Lorries and Trucks

24 24 8711 Motor cycles (Including Mopeds) and Cycles Fitted with an Auxiliary Motor with or without Side-Cars

25 25 87149100 "Frames, Forks & Parts thereof"

26 26 28030010 Carbon Blacks

27 27 28047020 Phosphorus Red

28 28 28111100 Hydrogen Fluoride (Hydrofluoric Acid)

29 29 28276010 Potassium Iodide

30 30 28391900 Other Sodium Silicates

31 31 29071300 "Octylphenol, nonylphenol and their isomers; salts thereof"

32 32 29071990 Other Monophenols

33 33 29130090 "Other : Halogenated, sulphonated, nitrated or nitrosated derivatives of products of heading 2912"

34 34 29142310 Beta-Ionone

35 35 29147090 "Other: Halogenated, sulphonated, nitrated or nitrosated derivatives "

36 36 29171200 Adipic Acid Its Salts and Esters

37 37 29171990 Other: Acyllic Polycarbodylic acids and their derivatives

38 38 29181520 Sodium Citrate

39 39 29214990 Other : Aromatic polyamines and their derivatives; salts thereof

40 40 29225090 Other : Frusemide Aminodial Domperidone

41 41 29333914 Chlorpheniramine Maleate

42 42 29333990 Other Compounds containing an unfused pyridine ring

43 43 29350090 Other Sulphonamides

44 44 29362920 Nicotinic acid & nicotinamide (Niacinamide/niacine)

45 45 29411040 Cloxacilline & Its Salts

46 46 29414000 Chloramphenicol & Its Derivatives Salts Thereof

47 47 29415000 Erthromycine & Its Derivatives Salts Thereof

48 48 29419030 Ciprofloxacine & Its Salts

49 49 29419090 Other Antibiotics

15

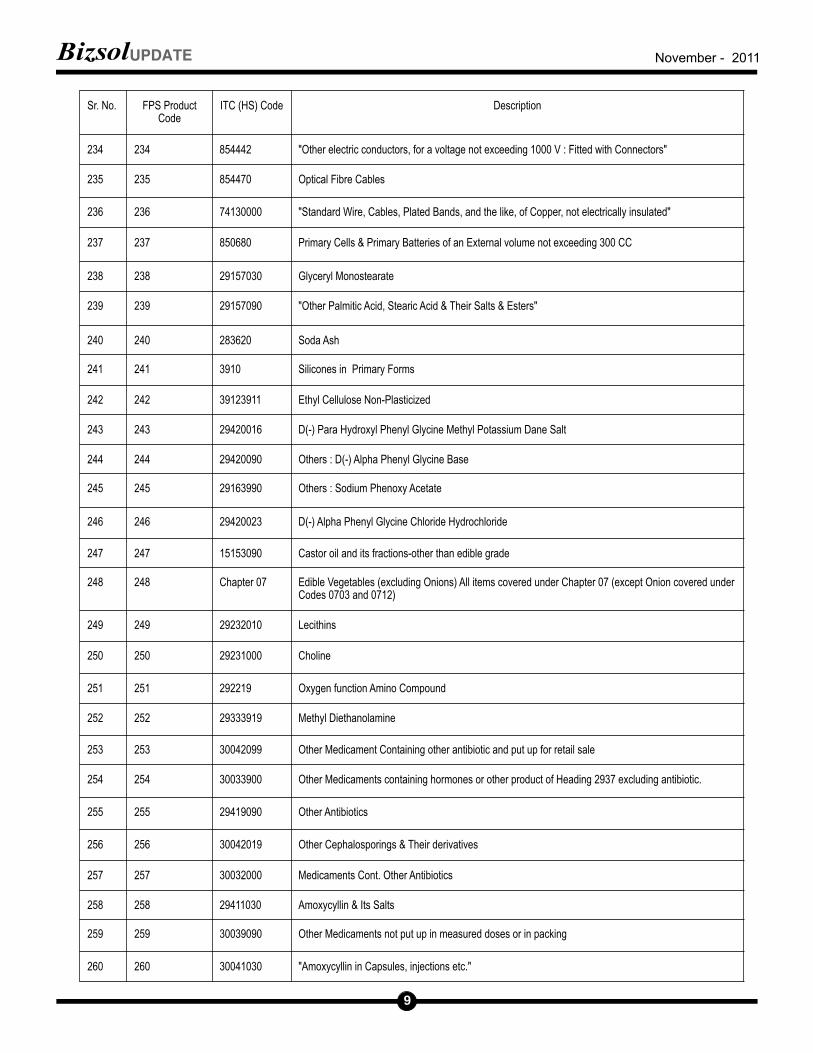

The following products are added in Table 4 of Appendix 37D (Focus Product Scheme) after Sl. No.338 for exports made with effect from 01.04.2011:

Income Tax Notifications

•Person who is entitled to receive any amount on

which TDS is deductible, should also make an

application for PAN. In lieu of this condition, Form

49AA have been introduced for application of PAN,

which will be applicable to LLP, Individuals not being

citizen of India, Companies, Firms, AOP (trusts),

AOP(non-trusts), BOI, Local authority, Artificial

Judicial Person, or any other entity formed or

registered outside India. (notification no. 56/2011

dated 17/10/2011).

•Due date for submission of quarterly Statement of

deduction of TDS to the DGIT have been extended th st th st thfrom 15 July to 31 July, 15 Oct to 31 Oct and 15

stJan to 31 Jan, if the deductor is an office of

Government. Further deductor should also state in

his statement the particulars of amount paid or

credited on which no tax was deducted because of

the deductee furnishing a declaration that tax on his

total income is nil. ( notification no. 57/2011 dated

24/10/2011).

Circulars

•When any amount is deposited in the bank directly

or through the court by the litigant pursuant to the

direction by the court, bank will deduct TDS as per

the existing procedure and the TDS certificate

should be issued by the bank in the name of

“depositor”. When the amount is deposited jointly

by more than one litigant, then TDS certificate

should be issued by the bank to each depositor

according to its respective share in the total

deposit. At the time of making deposit, the

depositor should submit a declaration in the format

prescribed for record purpose and better

administration of TDS. (circular no. 08/2011 dated

14/10/2011)

MVATNotifications / Circular

•Administrative relief in terms of waiver of penalty and

interest imposed on sale made by Handmade soap

manufacturers on turnover of sales of soap except

detergent not exceeding Rs. 20 lakhs can now be

availed by making an application to the assessing st stauthority itself for the period 1 April 2005 to 31 March

2010. (Circular No. 14T of 2011 dated 19/10/2011)

•Due date for submission of Refund application under

section 51 of MVAT Act, 2002 for the period 2009-10 in

Form 501 is now extended from 30.09.2011 to

31.12.2011. (Circular No. 15T of 2011 dated

02/11/2011)

COMPANY LAW:Notifications

•Draft of Companies(Demateria1ization of Certificates)

Rules, 2011 has been withdrawn. [Notification dated

28.10.2011]

•New Form 5 for Notice of consolidation, division, etc. or

increase in share capital or increase in number of

members is prescribed. [Notification dated

23.09.2011]

•In the Companies Regulation, 1956 in regulation 17 for

sub-regulation following regulation is substituted:

the Registrar shall not keep any document pending for approval and registration or for taking on record or for rejection or otherwise for more than Six days, from the date of it filling excluding the cases where approval from the Central Govt. for Regional Director or Company Law Board or Court or any other competent authority is required. [Notification dated 22.09.2011]

Circulars

•Time for furnishing details of PAN by DIN(Director's

Identity Number) Holder is extended upto

15.12.2011.[General Circular No. 66/2011 dated

04.10.2011]

•Online incorporation of companies within 24 hours on

thebasis of certification and declarations given by the

TABLE 4: NEW FOCUS PRODUCTS

Sr. No.

FPS Product

Code

ITC (HS) Code

Description

339 339 29420090 Others – Bulk Drugs / APIs

November - 2011

16

FEMA/RBI

Circular Number Date Of Issue

Department Subject Meant For

RBI/2011-2012/247 4.11.2011 Foreign Exchange Department

Foreign Direct Investment – Transfer of Shares

All Category – I Authorized Dealer banks

A.P.(DIR Series) Circular No. 43

RBI/2011-2012/246 4.11.2011 Urban Banks Department

Interest Rates on Rupee Export Credit - UCBs

The Chief Executive Officer Scheduled Primary (Urban) Co-operative Banks (holding AD Category I licence)

UBD.BPD (AD) Cir.No.3/13.05.000/2011-12

RBI/2011-2012/245 3.11.2011 Department of Banking Operations and Development

Guidelines on Commercial Real Estate (CRE)

All Scheduled Commercial Banks (excluding RRBs)

DBOD.BP.BC.No.

RBI/2011-2012/244 3.11.2011 Foreign Exchange Department

Foreign investment in India by SEBI registered FIIs in other securities

All Category – I Authorized Dealer banks

A.P. (DIR Series)Circular No. 42

RBI/2011-2012/243 2.11.2011 Department of Banking Operations and Development

Comprehensive Guidelines on Derivatives: Modifications

"The Chairman and Managing Directors/ Chief Executive Officers of All Scheduled Commercial Banks (excluding RRBs and LABs), All India Term-Lending & Refinancing Institutions & Primary Dealers"

DBOD.No.BP.BC. 44/21.04.157/2011-12

RBI/2011-2012/242 1.11.2011 Foreign Exchange Department

Memorandum of Instructions governing money changing activities

All Authorised Persons in Foreign Exchange

A.P. (DIR Series)Circular No. 41

RBI/2011-2012/241 1.11.2011 Foreign Exchange Department

Export of Goods and Software – Realisation and Repatriation of export proceeds – Liberalisation

All Category - I Authorised Dealer Banks

A.P.(DIR Series)Circular No. 40

RBI/2011-2012/240 1.11.2011 Foreign Exchange Department

"Deferred Payment Protocols dated April 30, 1981 and December 23, 1985 between Government of India and erstwhile USSR"

All Category - I Authorised Dealer Banks

A.P.(DIR Series)Circular No. 39

RBI Circulars

17

RBI/2011-2012/239 31.10.2011 Department of Banking Operations and Development

Banks' Exposure to Capital Market - Issue of Irrevocable Payment Commitments (IPCs)

All Scheduled Commercial Banks (excluding RRBs)

DBOD.Dir.BC. 43 /13.03.00/2011-12

RBI/2011-2012/238 31.10.2011 Urban Banks Department

Revision in Limits of Housing Loans and Repayment Period - Second Quarter Review of Monetary Policy 2011-12

"The Chief Executive Officer, All Primary (Urban) Co-operative Banks"

UBD.BPD.(PCB). Cir.No.7/09.22.010/2011-12

RBI/2011-2012/237 28.10.2011 Department of Non Banking Supervision

Implementation of Green Initiative of the Government

All Non Banking Financial Companies / Residuary Non Banking Companies

DNBS(PD).CC. No 248/03.10.01 /2011-12

RBI/2011-2012/236 28.10.2011 Department of Non Banking Supervision

"'Know Your Customer' (KYC) Guidelines – Anti Money Laundering Standards (AML) -'Prevention of Money Laundering Act, 2002 - Obligations of NBFCs in terms of Rules notified thereunder’-Reporting Format under Project FINnet"

All Non Banking Financial Companies / Residuary Non Banking Companies

DNBS(PD).CC. No247/03.10.42 /2011-12

RBI/2011-2012/235 28.10.2011 Department of Non Banking Supervision

List of Terrorist Individuals / Organisations- under UNSCR 1267 (1999) and 1822(2008) on Taliban /AL-Qaida Organisation

All Non Banking Financial Companies /Residuary Non Banking Companies

DNBS(PD).CC. No 246/03.10.42/2011-12

RBI/2011-2012/234 25.10.2011 Foreign Exchange Department

Memorandum of Instructions governing money changing activities- Location of Forex Counters in International Airports in India

All Authorised Persons in Foreign Exchange

A.P. (DIR Series)Circular No.38

RBI/2011-2012/233 25.10.2011 Department of Banking Operations and Development

Deregulation of Savings Bank Deposit Interest Rate - Guidelines

All Scheduled Commercial Banks (Excluding RRBs) )

DBOD.Dir.BC. 42/13.03.00/2011-12

Circular Number Date Of Issue

Department Subject Meant For

18

Circular Number Date Of Issue

Department Subject Meant For

RBI/2011-2012/224 18.10.2011 Rural Planning and Credit Department

Inclusion of Credit under KCC under direct financing for Agriculture

The Chairmen All Regional Rural Banks (RRBs)

RPCD.CO RRB. BC. NO. 24 03.05.33/2011-12

RBI/2011-2012/223 17.10.2011 Rural Planning and Credit Department

"Know Your Customer Norms – Letter issued by Unique Identification Authority of India (UIDAI) containing details of name, address and Aadhaar number"

The Chairmen / CEOs of All State and Central Co-operative Banks

RPCD.CO.RCB.AML.BC.No.23/07.40.00/2011-12

RBI/2011-2012/222 14.10.2011 Department of Banking Operations and Development

"Inclusion in the Second Schedule to the Reserve Bank of India Act, 1934 – Rabobank International (Coöperatieve Centrale Raiffeisen – Boerenleenbank B.A.)"

All Scheduled Commercial Banks

DBOD. No.Ret. BC. 40/12.06.131/2011-12

RBI/2011-2012/221 14.10.2011 Foreign Exchange Department

Processing and Settlement of Export related receipts facilitated by Online Payment Gateways - Enhancement of the value of transaction

All Category - I Authorised Dealer Banks

A.P. (DIR Series)Circular No.35

RBI/2011-2012/220 14.10.2011 Foreign Exchange Department

Exim Bank's Line of Credit of USD 27.50 million to the Government of the Republic of Senegal

All Category - I Authorised Dealer Banks

A.P. (DIR Series)Circular No.34

RBI/2011-2012/219 13.10.2011 Rural Planning and Credit Department

Inclusion of Credit under KCC under direct financing for Agriculture

The Chairman/Managing Director/ Chief Executive Officer [All Scheduled Commercial Banks (excluding Regional Rural Banks)]

RPCD.CO.Plan.BC. 22 /04.09.01/2011-12

RBI/2011-2012/218 13.10.2011 Rural Planning and Credit Department

"Know your Customer Norms – Letter issued by Unique Identification Authority of India (UIDAI) containing details of name, address and Aadhaar number"

The Chairmen All Regional Rural Banks (RRBs)

RPCD.CO RRB.AML.BC No. 21/03.05.33(E)/2011-12

RBI/2011-2012/217 13.10.2011 Department of Banking Operations and Development

Prudential Guidelines on Capital Adequacy and Market Discipline - New Capital Adequacy Framework (NCAF) - Revision of Rating Symbols and Definitions of Credit Rating Agencies

The Chairman / CMD / MD / CEO All Scheduled Commercial Banks (excluding LABs and RRBs)DBOD.No.BP.BC.39/21.0

6.007/2011-12

RBI/2011-2012/216 12.10.2011 Foreign Exchange Department

Memorandum of Instructions governing money changing activities

All Authorised Persons in Foreign Exchange

19

A.P. (DIR Series)Circular No.33

November - 2011

20

Circular Number Date Of Issue

Department Subject Meant For

RBI/2011-2012/215 11.10.2011 Department of Banking Operations and Development

Rupee Export Credit Interest Rates All Scheduled Commercial Banks (excluding RRBs)

DBOD.Dir.(Exp).BC.No.38 /04.02.001/2011-12

RBI/2011-2012/214 10.10.2011 Foreign Exchange Department

Liberalised Remittance Scheme for Resident Individuals-Revised Application cum Declaration form

All Authorised Persons in Foreign Exchange

A.P. (DIR Series) Circular No. 32

RBI/2011-2012/213 5.10.2011 Department of Payment and Settlement System

Domestic Money Transfer - Relaxations

The Chairman and Managing Director / Chief Executive Officer All Scheduled Commercial Banks including RRBs / Urban Co-operative Banks / State Co-operative Banks / District Central Co-operative Banks/Authorised Card Payment Networks

DPSS.PD.CO.No. 62/02.27.019/2011-2012

RBI/2011-2012/212 4.10.2011 Department of Banking Supervision

Calendar of Reviews for Board/Local Management Committee of foreign banks

The Chief Executives All foreign banks operating in India

DBS.ARS.BC. No. 03 / 08.91.020/ 2011-12

RBI/2011-2012/211 3.10.2011 Foreign Exchange Department

"Appointment of Agents / Franchisees by Authorised Dealer Category-I banks, Authorised Dealer Category-II and Full Fledged Money Changers– Revised guidelines"

All Authorised Persons in Foreign Exchange

A.P. (DIR Series)Circular No. 31

RBI/2011-2012/210 3.10.2011 Department of Payment and Settlement System

List of Terrorist Individuals / Organisations under UNSCR 1267(1999) and 1822(2008) on Taliban / Al-Qaida Organisation

"All Payment System Operators Authorised under the PSS Act, 2007"

DPSS. CO.AD. No. 604 /02.27.005 /2011-12

Service Tax unsettled issues getting settled

services provided by sub-contractor to the contractor is

always the major issue having cost impact.

It is unavoidable but the necessary requirement

for engaging sub-contractor associated with big projects.

There where number of controversies with respect to

applicability of service tax, to the sub-contractor,

entitlement of the exemption to the sub-contractor &

passing of incidence of service tax to get cascading effect

of service tax when services are provided by sub-

contractor through main contractor various projects e.g.

development of infrastructure project like road, airport,

dam, tunnel, EPC contract, services availed by SEZ

developer / Unit etc. etc…

Indore Commissioner ate have issued the Trade

Notice No. 5/98-Service Tax, dated 14-10-1998 when

services of the architect & interior decorators were brought

in the net of service tax.

Board clarified that, in cases where an

architect/interior decorator sub-contracts part/whole of his

work to another architect/interior decorator, it is clarified

that no service tax is required to be paid by the sub-

contractor provided that the principal architect/interior

decorator has paid the service tax on the services

rendered by him to the client and provided the sub-

contracting is in respect of the same service category. In

other words, work is sub-contracted by one architect to

another architect. In such cases, if the principal architect

pays the service tax on services rendered by him to his

client, the sub-contracting architect is not required to pay

the service tax. However, service tax would be required to

be paid in a case where sub-contracting is to a different

service category. For example where an architect sub-

contracts his work to a consulting engineer, then service

tax would be required to be paid by both the architect and

the consulting engineer on the services rendered by them.

Similarly, a market research agency would be required to

pay service tax on services rendered by it to an advertising

agency, even if the advertising agency is also liable to pay

service tax on the amount billed to its client for advertising

services (which, inter alia, includes the amount paid by the

advertising agency for such market research services to

the market research agency).

Board has clarified in the circular no. 96/07/2007

ST dt. 23.08.2007 to the issue by giving the eg. that A

taxable service provider outsources a part of the work by

engaging another service provider, generally known as

sub-contractor. Service tax is paid by the service provider

for the total work. In such cases, whether service tax is

liable to be paid by the service provider known as sub-

contractor who undertakes only part of the whole work &

then Board clarified that A sub-contractor is essentially a

taxable service provider. The fact that services provided by

such sub-contractors are used by the main service provider

for completion of his work does not in any way alter the fact

of provision of taxable service by the sub-contractor.

Services provided by sub-contractors are in the

nature of input services. Service tax is, therefore, leviable

on any taxable services provided, whether or not the

services are provided by a person in his capacity as a sub-

contractor and whether or not such services are used as

input services. The fact that a given taxable service is

intended for use as an input service by another service

provider does not alter the taxability of the service provided.

The plain reading of above clarification indicates

that sub-contractor is essentially a taxable service provider

& nature of service provided through the main contractor

does not alter the taxability of the services provided. In

other words if services provided by the main contractor is

exempted by way of notification then the services provided

by the sub-contractor for the same purpose through main

contractor is also exempted.

…….By Ashok B Nawal

November - 2011

21

Sub-contractor at par with Main Contractor inthe service tax regime

sub-contractor and therefore even the definition provides

“services provided to any person”.

The same ratio is applicable for service provided to

SEZ Developer / Units and even the wording of Rule 31 of

SEZ Rules, 2006 where it has been mentioned that

exemption from payment of service tax of taxable service

under sec 65 of Finance Act 1944 rendered to a Developer /

Unit including Unit under construction by any service

provider shall be available for authorized operation is a

special economic zone. Whereas Rule 10 of SEZ Rules,

2006 provides exemption / drawback and concession on the

goods and the services allowed to a Developer / Co-

developer as the case may be shall also be available to the

contractor including sub-contractor appointed by such

developer / co-developer and all the documents in such

cases shall bare the name of the Developer / Co-developer

along with Contractor and Sub-contractor and this should be

filed jointly in the name of Developer / Co-developer and the

contractor or sub-contractor as the case may be. The spirit

of the Act and Rules read with board circular is clearly

specifying that the service provided for the authorized

operation either by Main Contractor or through sub-

contractor will be exempted or granted refund being

exemption by way of refund.

In case service provided to SEZ Developer / Co-

developer / Unit by Main Contractor or Sub-Contractor is

falling under category 1 and category 2 as specified in

Export of Service Rules, 2005 and then there will be total

exemption and if it falls under category 3 as specified in

Export Of Service Rules, 2005 then exemption is granted by

way of refund. However if there is single Unit of a company

as SEZ the exemption can be claimed by giving FORM A,

otherwise proper documentation needs to be maintained for

claiming refund since the refund is granted only after

payment of service tax by Contractor or sub-contractor and

payment of their respective bills. To conclude, services

provided by sub-contractor for any services which exempt

are also exempted even though these are provided through

main contractor.

Now board has issued one additional circular no st147/16/2011 – ST dated 21 October 2011. Exemption of

service tax has been provided for commercial construction

services / infrastructure development, projects of roads,

airports, dams, tunnels etc and the services provided by

Main Contractor is exempted. The issue was raised

whether the classification of services when are the same of

the Main Contractor and sub-contractor, whether the

exemption provided will be applicable to the sub-

contractor. Board has clarified, though the classification of

the services provided by sub-contractor would be

independently done as per the rules of classification and

the taxability will arise accordingly. However, it is also

apparent that in case the services provided by the sub-

contractors to the main contractor are independently

classifiable under WCS, then they too will get the benefit of

exemption so long as they are in relation to the

infrastructure projects mentioned above. Thus, it may

happen that the main infrastructure projects of execution of

works contract in respect of roads, airports, railways,

transport terminals, bridges tunnels and dams, is sub-

divided into several sub-projects and each such sub-

project is assigned by the main contractor to the various

sub-contractors. In such cases, if the sub-contractors are

providing works contract service to the main contractor for

completion of the main contract, then service tax is

obviously not leviable on the works contract service

provided by such sub-contractor.

Board has been consistent in their views right

from 1998 till 2011 and therefore the spirit of the law maker

is very crystal clear that intension to provide exemption

cannot be defeated just because the services are provided

through the Main Contractor by Sub-Contractor. When the

object is very clear and therefore wherever exemption has

been provided to the taxable service provided irrespective

by Main Contractor or through Sub-contractor, object of

exemption cannot be defeated on the ground that the sub-

contractor is provided the services and there is no

relationship as client between ultimate service availer and

November - 2011

22

CENTRAL EXCISE

•Cenvat Credit – Service of transportation of

employees to the factory is admissible for credit as

input service under Rule 2(l) of the CENVAT Credit

Rules, 2004 – Pendency of the appeal by the revenue

in Supreme Court does not bar the High Court to

examine the issue. Appeal dismissed: PUNJAB

AND HARYANA HIGH COURT [2011-TIOL-650-HC-

P&H-ST]

• Cenvat Credit on outward transport from the place of

removal is admissible upto 31.3.2008 in view of the

Karnataka High Court order in case of ABB Ltd. -

Appeal rejected: CHENNAI CESTAT [2011-TIOL-

1380-CESTAT-MAD]

•16(1) and 16(2) in respect of the goods returned by

the customer. Prior permission under rule 16(3) is

not a pre-condition to avail the Cenvat Credit.

[2011(271) E.L.T. 574 (Tri. – Del.)

• Appellant an assessee under Central Excise Act,

1944 and contending that job work alone

undertaken. Revenue arguing that repair and

maintenance undertaken under the guise of job

work. Records not showing how repair and

maintenance charges were received instead of job

work charges. Contract is not available to explain

nature of activity carried out. In the absence of any

such documentary evidence, it cannot be said that

the appellant was undertaking repairs and

maintenance instead of job work. [2011(271) E.L.T.

591 (Tri. - Del.)]

•Interest for lapse of time between delivery of goods

and realization of money is admissible as

deduction to arrive at the assessable value on

An assesse may avail Cenvat Credit under rule

actual interest receivable for each invoice, and not as

average. As the deciding factor is lapse of time in

between the delivery of goods and realization of

money, it is not necessary to show interest separately

in invoice. [2011(271) E.L.T. 563 (Tri. - Del.)]

•An order served on assessee through Speed Post

and not received back is not in accordance with the

provisions of Section 35C of Central Excise Act, 1944

which require communication of order by registered

post with acknowledgment due. In such case there is

no evidence to prove that order was served on

assessee. [2011(271) E.L.T. 518 (P & H)]

•Assessee imported parts of printing machinery duty

free for doing job work on them for their foreign

supplier. Later, due to recession, foreign supplier

stopped job work and asked for return of balance of

imported goods. The assessee made the request for

re-export for balance of goods received by them

which was rejected by the Commissioner of

Customs. Held that re-export of such goods should

be allowed, as neither their import/export was

restricted nor any violation of condition of notification

under which they were imported.[2011(271) E.L.T.

554 (Tri. - Chennai)]

•Other charges collected from customers towards

post-manufacturing expenses such as octroi and

transportation are not to be added to the assessable

value if the assessee has not claimed any separate

deduction on account of such post-manufacturing

expenses. As the assessee has shown the other

charges collected by him on the invoices issued by

him, it cannot be said that there was any suppression

of the facts and hence extended period for issue of

show cause notice is not available to the Revenue.

[2011(271) E.L.T. 553 (Tri. - Ahmd.)]

•Once the Apex Court either clarifies the provisions of

November - 2011

23

claimant was failure of discharge of the duties

according to law and un-necessary driving the

claimant to High Court for relief. Held that the copies

seized to be made available within 7 days and if

failing in providing, the cost of Rs. 50000/- to claimant

to be paid and recovered from the salary of the officer

concerned. [(2011 (272) E.L.T 42 (Bom.)]

•An Appeal, in which the rate of duty of excise or the

value of goods for the purposes of assessment is not

involved, can be heard under Sec 35Cof Central

Excise Act, 1944 by the HC [2011 (272) E.L.T 11

(ALL.)]

•Stricture against the Tribunal for distinguishing

Supreme Court judgment both on the fact and

interpretation of Rule 3. High Court did not find such

distinction. Tribunal not only differed on reasons

given on the same facts but also ventured to

distinguish reasons on question of Law. Tribunal

prima facie committed breach of judicial discipline in

distinguishing Supreme Court judgement applicable

to facts of case by giving own reasons. The

Department counsel called upon to explain how

CESTAT could have taken different view both on

facts and question of Law than taken by Hon'ble

Supreme Court. [2011 (272) E.L.T 11 (ALL.)]

•Transportation cost till buyers stores – Supply of

transformer to state Electricity Boards- Inclusion of

Fright Charges– Contract clearly indicates ex-works

price-Freight charges on Equalized basis mentioned

separately – Merely because Sales Tax paid on

amount inclusive of frights charges, it cannot be

concluded that sale taken place at destination. It is

stated by tribunal that freight charges cannot be

included in assessable value. [2011 (149) E.L.T 11

(Tal. Mum.)]

•Finished goods not entered into Daily Stock Register

was not liable for confiscation & penalty under Rule

25 of Central Excise Rules, 2002 in the absence of

intention to clear them without payment of duties.

However, penalty under Rule 27 will be impossible

for procedural lapse of Central Excise provision.

[2011 (272) ELT 315 (Tri. Delhi)]

law or declares any particular principle of Law, it

would apply right from day in respect of which law has

been declared and has been in existence. So, there is

no requirement of further clarification from the board

to clarify the effective date of the applicability of law.

[2011(271) E.L.T. 576 (Tri. - Mumbai)]

•Judgement which has held field for a long time,

should not be unsettled only because another view is

possible. Hardship or inconvenience can nor alter

meaning employed by legislature if such meaning is

clear on face of statute.[2011(271) E.L.T. 492 (S.C.)]

•The parts of machine can be classified as complete

machine if it can be established that parts are

removed as such so as to constitute a complete

machine , such parts have to be assessed to duty as

complete machine and not under the sub heading

relating to parts. [2011 (272) E.L.T. 104 (Tri. Mum)]

•Assessee discharged duty liability on sulphur

bentonite “under protest” in pursuance to order of

commissioner holding the Assessee product as

manufactured product. Consequent to final order of

tribunal holding such activity does not amount to

manufacture, Assessee claim the refund of amount

paid through PLA. [2011 (272) E.L.T 142 (Tri. Bang)]

•Findings of Clandestine Removal are required to be

arrived at on the basis of substantive and positive

evidence reflecting upon such clandestine activates

of the Assessee. The conformation of demand on the

basis of input/output calculation based on electricity

consumption in the factory cannot be upheld. [(2011

(272) E.L.T 94 (Tri. Ahmd)]

•In the case of delayed payment of duty no separate

show cause notice is required to be issued for

recovery of interest. [(2011 (272) E.L.T 136 (Tri.

Mum.)]

•The Managing Director of company is not liable for

penalty unless it is shown that he had , by his

commission or omissions, let goods become liable for

confiscation. [(2011 (272) E.L.T 51 (Ker.)]

•Refusal of revenue officer to provide the copies of

document seized during search & investigation to

24

November - 2011

•Quantification of duty due had to be ascertained on

each removal. Merely because evasion found for

some invoices clearance for other invoices not to be

treated similarly. [2011(272)E.L.T. 225(Tri. - Bang.)]

•In case of non-accountal of goods which are lying in

the factory and non-entry in the statutory record, they

cannot be confiscated without proof of mala fide

intention to clear them without payment of duty. But

penalty under Rule 27 of Central Excise Rules, 2002

can be imposed for procedural lapse of the Central

Excise provision. [2011(272)E.L.T. 315(Tri. - Del.)]

•Assessee paid excess duty of Rs 2,46,240/- in the

month of March 2003. Customer issued debit note in

June 2003 to the assessee for the excess amount of

duty and did not claim refund of excess duty. Books of

account of assessee disclosing that excess was not

paid by customer. Held that assessee was entitled to

refund of excess payment. Refund claim of assessee

could not be rejected on ground that debit note

pertained to month different than in which duty was

paid, or that it was mere adjustment of accounts, and

not proof of payment of duty.[2011(272)E.L.T.

191(Kar.)]

•Cenvat Credit of inputs used in workshop (which is

not the part of Factory) for repairs and maintenance

of capital goods, which is in turn used for manufacture

of final product is allowed. [2011(272)E.L.T. 318 (Tri.

- Bang.)]

CUSTOMS

•Penalty can be imposed on CHA on mis-declaration

and undervaluation of goods exported. [2011 (272)

E.L.T. 58(Tri. Kar)]

•Transaction Value if appears to be lower when

compared to contemporaneous records though the

country of origin is the same. But Bill of entry relied

upon the revenue are not matching with present BOE

either in time or in quantity or in model numbers. Also

Market of electronic items moves very fast on

account of introduction of new models in the field and

•Confiscation of goods classified under different tariff

heading for custom duties will not be allowed

because adoption of correct classification of goods is

in the hand of customs only. Further there is no

intention to evade duties by mis-declaring imported

goods. [2011 (272) ELT 282 Tri. – Del.)]

•Inputs received by the assessee are not those which

were mentioned in the invoice. As a prudent buyer

assessee taken the credit on the basis of invoice &

issue the inputs for manufacturing. The cenvat credit

will be allowed in accordance with circular No.

766/82/2003-CX, dated 15/12/2003. [2011 (272) ELT

280 Tri. - Mumbai)]

•Cenvat credit availed on inputs will not be denied only

because assessee has not maintained records of

inputs utilization in WIP & finished goods as on the

date of crossing SSI exemption limit. Matter

remanded to ascertain quantity of inputs by applying

formula for input & output as per Rule 3 (2) of CCR,

2004 (Eureka Conveyor Beltings Pvt. Ltd. [2011

(272) ELT 285 Tri. – Del.)]

•Section 35C (2A) of Central Excise Act, 1944 the

appeal is required to be heard within 180 days would

also be frivolous as the stay order is not co-terminus

with the period prescribed for disposal of appeal .

Period of Six months laid down therein is not even

mandatory. Department should have been careful in

filling of such frivolous appeals. [2011 (272) ELT 190

P&H)]

•Input Cenvat credit availed on LPG gas used for

canteen in the factory will be allowed & not denied

under Rule 2(k) of CCR, 2004. Canteen facility is

statutory requirement under Factories Act, 1948 &

necessary to run manufacturing activity. [2011 (272)

ELT 308 (Tri. – Mum.)]

•The Cenvat credit on inputs ordered by predecessor

of assessee & received by the assessee will be

allowed though invoice will not be in the name of

assessee. Further no permission from proper officer

will require as it is not a case of transfer of credit lying

in account of predecessor as given in Rule 9 of CCR,

2004. [2011 (272) ELT 288 (Tri. - Mumbai)]

November - 2011

25

carrying out local statutory requirements and other registrations under various laws and statutes such as registration under Service Tax, Custom, Central Excise Act, Export-Import Policy etc. These services do not involve any change or improvement in the management of an organisation and does not require any specialised knowledge of a Management Consultant but these services are only in the nature of compliance with the statutory requirements.: [2011-TIOL-1404-CESTAT-MAD]

•Services availed by the assessee in respect of

Effluent Treatment Plant are admissible input

services, as Effluent Treatment Plant required to be

used in relation to business and without this plant

assessee cannot set up factory. [2011 (24) S.T.R.

(Tri.-Ahmd.)]

•Department should know the meaning of each entry imposing service tax and it cannot be misguiding or taking benefit of the ignorance of an individual who is a small businessman. Department not to take advantage of ignorance of assessee. [2011(24)S.T.R. 84 (Tri.Del.)]

•Duty paid on direction of Revenue Officers and contested later in reply to Show Cause Notice , such payment has to be considered under protest and not on own volition of assessee. Time bar shall not applicable for claiming refund of such payments (Section 11B of Central Excise Act, 1944). [2011 (24) S.T.R. 110 (Tri.-Mumbai)]

•Refund claim not sanctioned by the Assistant Commissioner, in spite of order of Appellate Tribunal. Assistant Commissioner who was to sanction the refund had been transferred and no substitute had been posted. No submissions were made by the Commissioner or Assistant Commissioner seeking extension of time for implementing the Order of Tribunal or explaining the reasons for non-implementation. The attitude of the Commissioner seems to be one of disobedience and lack of judicial discipline. Therefore, the Commissioner concerned directed to appear in person and explain the reasons for not sanctioning the refund. [2011 (24)S.T.R.121 (Tri.-Ahmd.)]

•The very nature of entry relating to Business Auxillary Service and the large number of disputes that arose regarding the scope of entry clearly shows that there was some confusion in the minds of prospective assessee about the scope of the entry. Sufficient reasons for failure on the part of the assessee to pay tax should exist, to get relief under Section 80 of Finance Act, 1994. Co-operation by the assessee after commencement of enquiry cannot be a sufficient reason to invoke Section 80 of Finance Act, 1994. [2011(24) S.T.R. 65 (Tri.-Del.)]

•Adjudication should take place first and till the

with new technology. Even a gap of 5 to 6 months

considered huge gap. So the enhancement of AV

cannot be justified. Also enhancement of MRP

declared by the appellant's bases upon the

enhanced AV, cannot be upheld. [2011 (272) E.L.T

144 (Tri. Ahmd.)]

•Circular No. 7/2010-Cus. Dated 23-03-2010

clarifying that paragraphs 2.25.1 & 2.25.4 of

Handbook of Procedures were not applicable to

Drawback scheme & it was not payable where

export proceeds had not been realized, found to be

inapplicable as it was not in vogue when transaction

had taken place. [2011 (272) ELT 193 All.]

•Inordinate delay & laches on part of department

disentitle them from taking action against successor

in the interest of Importer. [(2011 (272) ELT 172

Mad.)]

•The refund of Special Additional Duty will be

available even if an assessee sells imported goods

on payment of CST/VAT by raising commercial

invoice and the requirement of disclosure of “no

credit of the additional duty of customs levied under

sub-section (5) of section 3 of the Customs Tariff

Act, 1975 shall be admissible” is not necessary

under condition 2(b) of Notification No. 102/07-Cus

on the commercial invoice but is required while

issu ing invoices under Centra l Exc ise

L a w / C u s t o m s L a w / S e r v i c e T a x

law.[2011(272)E.L.T. 310(Tri. - Mumbai)]

•In view of the Board's Circular No. 643/34/2002-CX,

Erection and Commissioning Charges are not

includible in the assessable value of product even if

the product emerges at the customer's site.

[2011(272)E.L.T. 305(Tri. - Mumbai)]

SERVICE TAX

•Management Consultant Service – Filing of Documents with Statutory Authorities does not change or improvement in the management of an organisation -Not management Service : filing of requisite documents with the Registrar of Companies, and other statutory authorities,

November - 2011

26

•Once Appellant gives the Chartered Accountant's Certificate and shows the amount receivable in the balance sheet, it is necessary for the Revenue to reject these documents/ records. As utility of balance sheet is limited to the fact that balance sheet shows that these amounts as receivable and nothing more and in absence of duty element shown separately in the Central Excise invoice, the certificate issued by the Chartered Accountant certifying that assessee did not collect duty is sufficient.(Unjust enrichment) [2011(24) S.T.R. 108 (Tri.-Ahmed.)

•Tribunal in case of Gandhi & Gandhi Chartered Accountants [2010 (17)S.T.R. 25 (Tri.)] dropped the demand under BAS and held that billing activity is not taxable under BAS and was taxable under BSS, while in the case of Bellary Computers [2007 (8) S.T.R. 470 (Tri.-Bang.)] held that the billing activity was taxable under BAS. Tribunal has given conflicting decisions on same dispute in two different orders. In the present case appellant has made out a strong prima facie case against the demand and penalties therefore, pre-deposit waived and recovery stayed. [ 2011 (24)S.T.R. 92 (Tri.- Bang.)

EOU

•Customs cannot initiate recovery proceedings

against EOU due to failure to fulfill export obligation

without consensus of Development Commissioner. It

is more so where capital goods were not removed

clandestinely & it was case of their non-use. Also

seizure of warehoused goods was not permissible for

failure to fulfill export obligation when goods are not

removed from warehouse. ( 2011 (272) ELT 243 Tri-

Beng.)

SEZ•No custom duty will be levied on supplies from DTA to

SEZ. The reason is that both the units are located within territorial water of India. Custom duties are levied on goods imported into or exported beyond territorial waters of India (2011 (272) ELT 209 A.P.)

INCOME TAX

•Unrealized Export Proceeds for computation of

Benefit under Sec 10A: In absence of requisite

extension for realization of export proceeds from

Reserve Bank of India, the unrealized export

proceeds cannot be considered for the purpose of

computation of benefit under Sec 10A of the Income

Tax Act, 1961. [2011-TIOL-684-ITAT-MUM]

adjudication is made, no coercive steps shall be taken against the members of the petitioner- Association. In case members of the petitioner-association are aggrieved by any kind of adjudication, they can challenge the same before the appropriate forum in accordance with law. [2011 (24) S.T.R. 22 (Del.)]

•Telephone installed at residence of one of the partners and bills paid by the company. Telephone were used for business purpose and Department could not produce any evidence that telephone was not used for business purpose and also could not refute contention of the appellant that Income Tax Department has accepted such expenditure as business expenditure . Therefore it is held that where the input services used is integrally connected with the business of manufacturing the final products and the cost of that input service forms part of the final products then the credit of service tax paid on such input service would be allowable. [2011 (24) S.T.R. 30 (Tri-Mumbai)]

•Insurance Policy for workman's compensation taken for workers who are involved in the manufacturing process of final products to cover the risk therefore. Assessee is entitled for input service credit on service tax paid on such Insurance Policy as per Rule 2(l) of Cenvat Credit Rules, 2004. [ 2011 (24)S.T.R. 124 (Tri.-Del)]

•Stipulation of State Electricity Board to plant trees cannot be treated as mandate to undertake landscaping services. Therefore, it has been held that the landscaping services are not input services eligible of availing Cenvat Credit. [2011 (24) S.T.R. 71 (Tri. -Chennai)]

•Commissioner (Appeals) while concluding that payment of tax established set aside the adjudicating authorities findings, that relevant documentary evidence not submitted and directed authority to decide refund claim along with interest. Once requisite conditions fulfilled follows as a matter of law and is a mandate of statute. The fact that the petitioners submitted relevant documents once again at the personal hearing upon remand does not detract from the fact that all the necessary documents were already submitted by the petitioners in the first place before the adjudicating authority much prior to the Order of Remand. Therefore, Petitioner would be entitled to interest as permissible under Section 11BB after the expiry of a period of 3 months from the date of receipt of the application for refund. [2011 (24) S.T.R. 17 (Bom.)]

•If the assessee would have paid service tax during the disputed period and they would have been eligible for the refund in terms of Notification No. 41/2007 dated 06.10.2007. This is a case of revenue neutrality, involving no intention to evade tax. [2011 (24)S.T.R. 40 (Tri-Chennai)]

November - 2011

27

sale of those shares are liable to be assessed as

long term / short term capital gains and not as

business income. [2011-TIOL-663-HC-MUM-

IT]

•Whether maintenance charges towards the

promotion and upkeep of the Mall are liable

to be assessed as 'business income'' or as

income from house property : The

maintenance charges received were towards

the maintenance and promotion of the common

area and the amounts received towards

maintenance charges were business receipts

liable to be assessed under the head "income

from business.' [2011-TIOL-658-HC-MUM-IT]

•Depreciation on Accessories of Computers:

Computer accessories and peripherals such as,

printers, scanners and server, etc. form an

integral part of the computer system and

therefore entitled to depreciation at the higher

rate of 60%. [2011-TIOL-658-ITAT-DEL]

•Additional Depreciation: Assessee has

multiple units in India. Assessee has increased

the capacity in one of the unit and it claimed

additional depreciation on the capacity

enhancement of the said Unit. Additional

depreciation was not claimed on any other units

except for this unit in which there is an increase

in capacity. ITAT ruled that the capacity of the

unit needs to be considered for the purpose of

eligibility of additional depreciation and not of

the business as a whole. [2011-TIOL-656-ITAT-

MUM]

RTI Expenses, administ rat ive d i ff icu l t ies,

deployment of staff, undue hardship and

clogging of administrative set up are no ground

to deny information under RTI which has

statutory recognition and arise out of

fundamental right guaranteed with article 19 (1)

of the Constitution. [2011 (272) E.L.T 18 (Ker.)]

•

•Netting of Export Proceeds: For the purpose

of claiming deduction under Sec 10A, the export

proceeds are required to be realized. However

in case of netting the Export proceeds are

adjusted against the Import payment. ITAT ruled

that netting is allowed for the purpose of

computation of exemption under Sec 10A and

accordingly such exports will be counted for the

purpose of exemption. [2011-TIOL-684-ITAT-

MUM]

•Whether payment of commission and bonus

to Directors will amount to diversion of

Profits: Payments of Commission and Bonus

are reward to given the employee as an

incentive for the good work being done by him /

her. Thus, these expenses were incurred for the

purpose of business expediency and for