jac laubscher chief economist comments on the annual report of the south african reserve bank...

TRANSCRIPT

Jac LaubscherChief Economist

Comments on the Annual ReportComments on the Annual Report

of theof theSouth African Reserve BankSouth African Reserve Bank

Parliamentary Committeeon Finance

28 September 2001

Key points from SARB reports

International economic outlook

Implications for South Africa

Monetary policy implications

Some thoughts on inflation targeting

Agenda

Key points from SARB reports

Economic growth moderating

Exports performing well / Current account surplus

Inflation target likely to be attained

National finances are sound

Employment creation remained sluggish

Productivity growth because of job-shedding

Capital account remains vulnerable

Improvement in trade account cancelled out by deterioration in

services account

Steep depreciation in the rand

International economic outlook

Further weakening expected

40

45

50

55

60

96 97 98 99 00 01

1

2

3

4

5

6NAPM (lhs) GDP (rhs)

index%

ceg118

USA NAPM vs. GDP growth

International economic outlook

Further weakening expected

Heavily dependent on consumer confidence

80

90

100

110

120

130

140

150

96 97 98 99 00 01

%

1

3

5

7

9

11

13Consumer confidence (lhs) Retail sales (rhs)

US consumer confidence vs. retail salesUS consumer confidence vs. retail salesUys:

IGRAPH

usconf

!pc(usaret,12) -

monthly

Uys:

IGRAPH

usconf

!pc(usaret,12) -

monthly

International economic outlook

Further weakening expected

Heavily dependent on consumer confidence

Lower turning point postponed

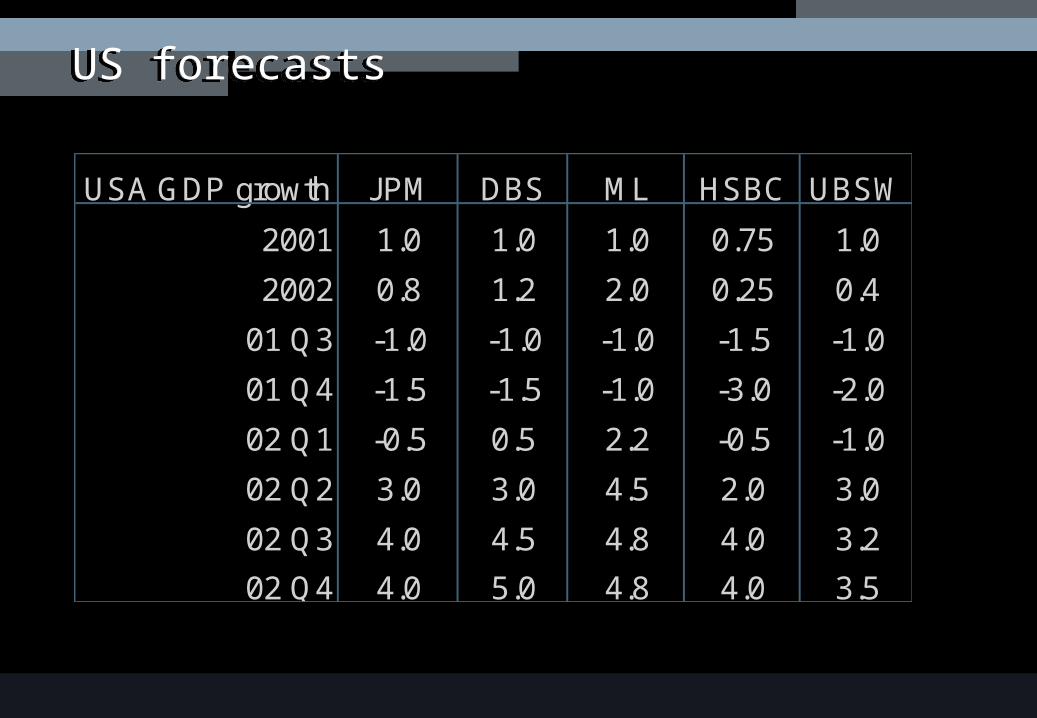

US forecastsUS forecasts

USA GDP growth JPM DBS ML HSBC UBSW

2001 1.0 1.0 1.0 0.75 1.0

2002 0.8 1.2 2.0 0.25 0.4

01 Q3 -1.0 -1.0 -1.0 -1.5 -1.0

01 Q4 -1.5 -1.5 -1.0 -3.0 -2.0

02 Q1 -0.5 0.5 2.2 -0.5 -1.0

02 Q2 3.0 3.0 4.5 2.0 3.0

02 Q3 4.0 4.5 4.8 4.0 3.2

02 Q4 4.0 5.0 4.8 4.0 3.5

International economic outlook

Further weakening expected

Heavily dependent on consumer confidence

Lower turning point postponed

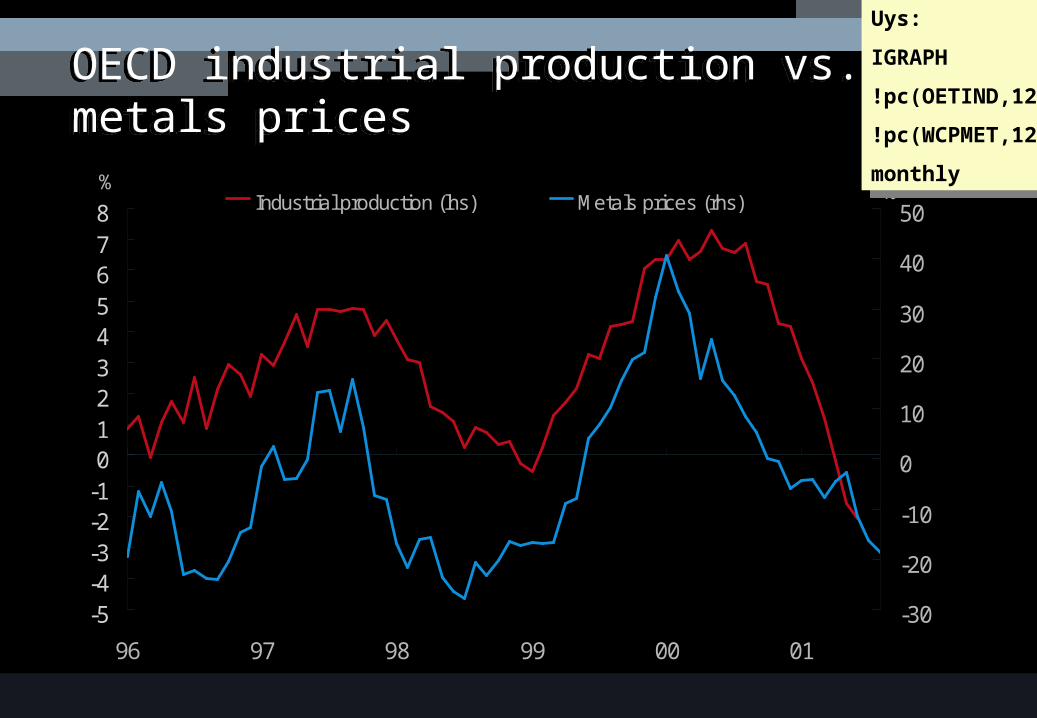

Commodity prices under pressure

-5-4-3-2-1012345678

96 97 98 99 00 01

%

-30

-20

-10

0

10

20

30

40

50%Industrial production (lhs) Metals prices (rhs)

OECD industrial production vs. metals pricesOECD industrial production vs. metals pricesUys:

IGRAPH

!pc(OETIND,12)

!pc(WCPMET,12)

monthly

Uys:

IGRAPH

!pc(OETIND,12)

!pc(WCPMET,12)

monthly

International economic outlook

Further weakening expected

Heavily dependent on consumer confidence

Lower turning point postponed

Commodity prices under pressure

Negative for emerging market economies

Further easing in monetary policy expected

US Fed funds target rateUS Fed funds target rate

2

3

4

5

6

7

8

9

90 91 92 93 94 95 96 97 98 99 00 01

%

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5Nominal Real

%

Uys:

IGRAPH

fedfnd

monthly

Uys:

IGRAPH

fedfnd

monthly

International economic outlook

Further weakening expected

Heavily dependent on consumer confidence

Lower turning point postponed

Commodity prices under pressure

Negative for emerging market economies

Further easing in monetary policy expected

Fiscal policy to become expansionary

Greater awareness of risk

Constraining international capital flows

Implications for South Africa

Rand weakness

1 Jan. 2000 = 100

Exchange rates

eg74

IGRAPH data

!bs(usdzar,e,100)!bs((usdzar*eurusd),e,100)!bs((usdzar/usdjpy),e,100)!bs(gbpzar,e,100)

weekly based to 100=1/1/2000

USER49 = CURRENCY

IGRAPH data

!bs(usdzar,e,100)!bs((usdzar*eurusd),e,100)!bs((usdzar/usdjpy),e,100)!bs(gbpzar,e,100)

weekly based to 100=1/1/2000

USER49 = CURRENCY

Currency movements vs. US dollar

-57%

-28%

-17%

-14%

-13%

-11%

-10%

-9%

-8%

-7%

Turkey

Brazil

Chile

South Africa

Sweden

Australia

Pakistan

Sri Lanka

New Zealand

Israel

1 January to 26 September 2001

Dividend payments to foreigners

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

1995 1996 1997 1998 1999 2000 2001

9

10

11

12

13

14Dividends (lhs) % of exports (rhs)

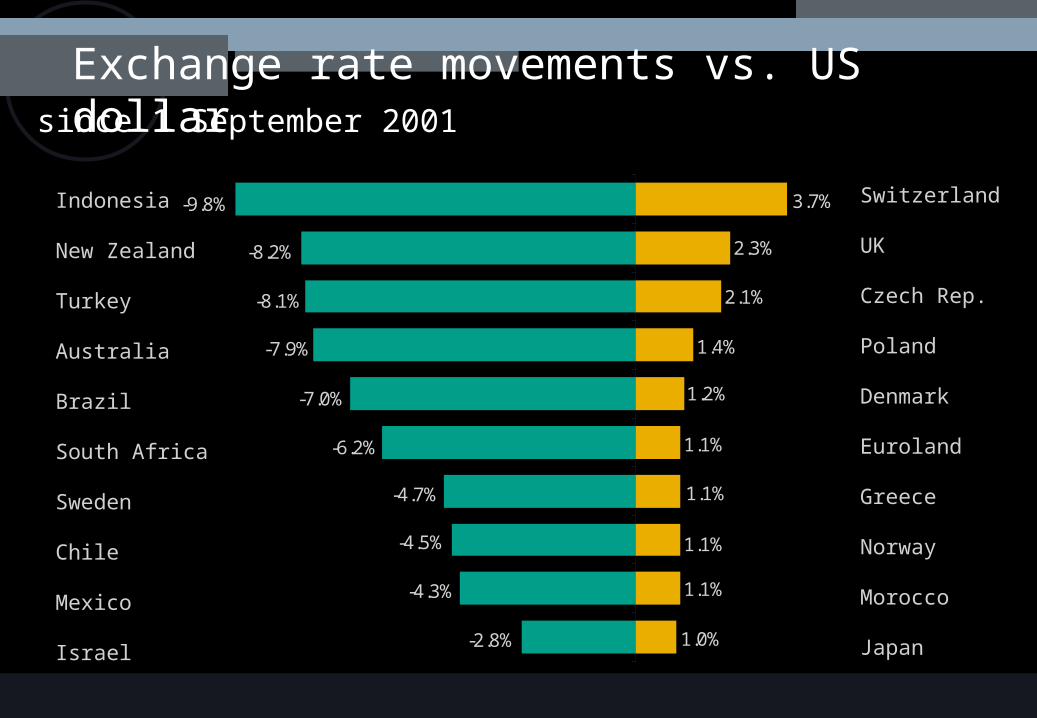

Exchange rate movements vs. US dollarsince 1 September 2001

-9.8%

-8.2%

-8.1%

-7.9%

-7.0%

-6.2%

-4.7%

-4.5%

-4.3%

-2.8%

2.3%

2.1%

1.4%

1.2%

1.1%

1.1%

1.1%

1.1%

1.0%

3.7%

-0.15 -0.1 -0.05 0 0.05

1

2

3

4

5

6

7

8

9

10

Indonesia

New Zealand

Turkey

Australia

Brazil

South Africa

Sweden

Chile

Mexico

Israel

Switzerland

UK

Czech Rep.

Poland

Denmark

Euroland

Greece

Norway

Morocco

Japan

Implications for South Africa

Rand weakness

Lower export volumes

Exports/GDP ratio

1

2

3

4

5

6

7

8

9

10

11

12

13

14

85 87 89 91 93 95 97 99 01

IGRAPH:EXPT/NGDPF

quarterly

IGRAPH:EXPT/NGDPF

quarterly

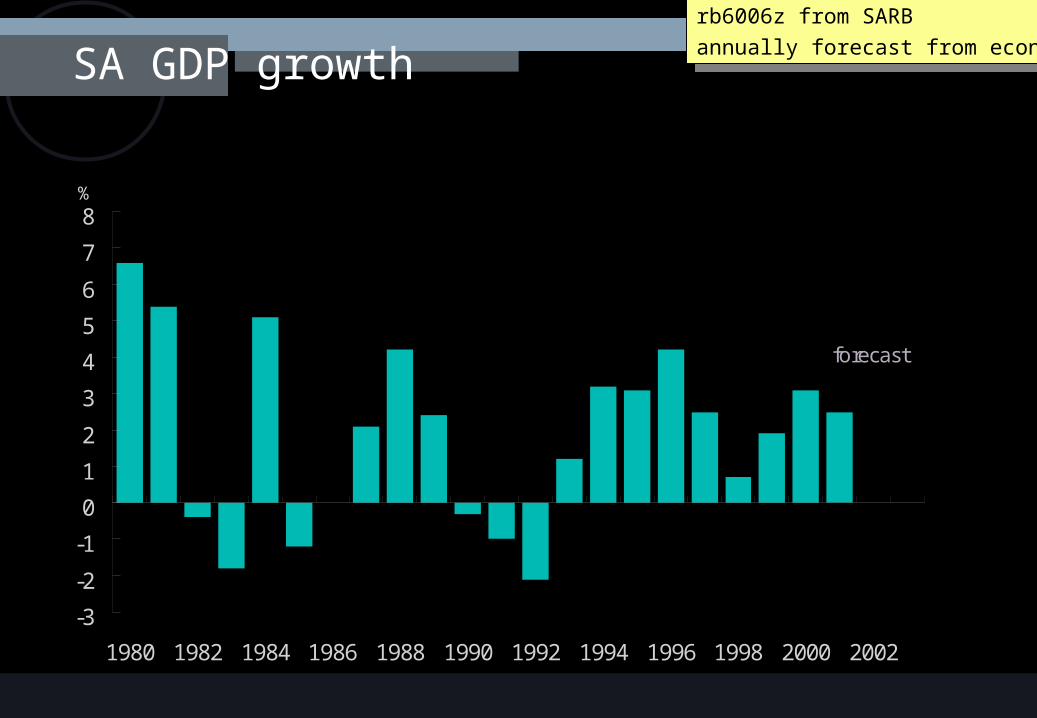

Implications for South Africa

Rand weakness

Lower export volumes

Weaker current account

Lower economic growth

SA GDP growth

-3

-2

-1

0

1

2

3

4

5

6

7

8

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002

%

forecast

IGRAPH:rb6006z from SARB

annually forecast from economic spreadsheet

IGRAPH:rb6006z from SARB

annually forecast from economic spreadsheet

Monetary policy implications

Beware of sentiment

Financial markets should not dominate thinking

Weekly change in All Share Index

-20

-15

-10

-5

0

5

10

15

95 96 97 98 99 00 01

%

Mean = 0.13Std.Dev. = 2.82

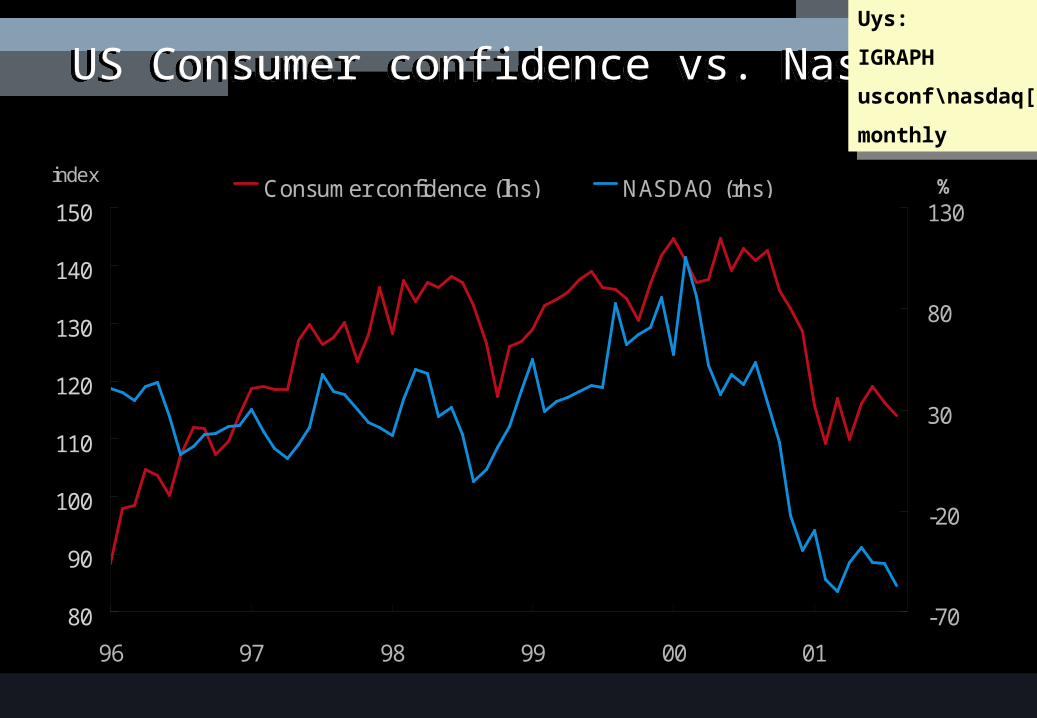

Monetary policy implications

Beware of sentiment

Financial markets should not dominate thinking

Monetary policy and asset prices

80

90

100

110

120

130

140

150

96 97 98 99 00 01

index

-70

-20

30

80

130%Consumer confidence (lhs) NASDAQ (rhs)

US Consumer confidence vs. NasdaqUS Consumer confidence vs. NasdaqUys:

IGRAPH

usconf\nasdaq[cl]

monthly

Uys:

IGRAPH

usconf\nasdaq[cl]

monthly

Monetary policy implications

Beware of sentiment

Financial markets should not dominate thinking

Monetary policy and asset prices

What to make of rand weakness

PPI Inflation : Imported vs. Domestic

-5

5

15

25

35

86 88 90 92 94 96 98 00

%

Imported Domestic

IGRAPH: (file jlgrowth – user49)

!pc(ppimps,12)\!pc(ppisas,12)

monthly

IGRAPH: (file jlgrowth – user49)

!pc(ppimps,12)\!pc(ppisas,12)

monthly

Monetary policy implications

Beware of sentiment

Financial markets should not dominate thinking

Monetary policy and asset prices

What to make of rand weakness

Outlook for the oil price / US dollar

Oil price vs. US dollar

5

10

15

20

25

30

35

40

85 87 89 91 93 95 97 99 01

price

-30

-20

-10

0

10

20

30

40

50

60

70

%

Oil price (lhs) US Dollar (rhs)

IGRAPH: BRSPOT\USDZAR[CL]

monthly

IGRAPH: BRSPOT\USDZAR[CL]

monthly

Monetary policy implications

Beware of sentiment

Financial markets should not dominate thinking

Monetary policy and asset prices

What to make of rand weakness

Outlook for the oil price / US dollar

Should the SARB follow global trends ?

Some thoughts on inflation targeting

Is inflation targeting still the appropriate monetary policy

regime ?

SARB Repo rate vs. Fed funds rate

8

12

16

20

24

Jan-98 Jul-98 Jan-99 Jul-99 Jan-00 Jul-00 Jan-01 Jul-01

%

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

%

SA Repo rate (lhs) Fed funds target rate (rhs)

IGRAPH: SAREP1\FEDFND

monthly

IGRAPH: SAREP1\FEDFND

monthly

Some thoughts on inflation targeting

Is inflation targeting still the appropriate monetary policy

regime ?

Escape clause should be communicated explicitly, or…

…the target redefined

Now is not the time for a tighter target range

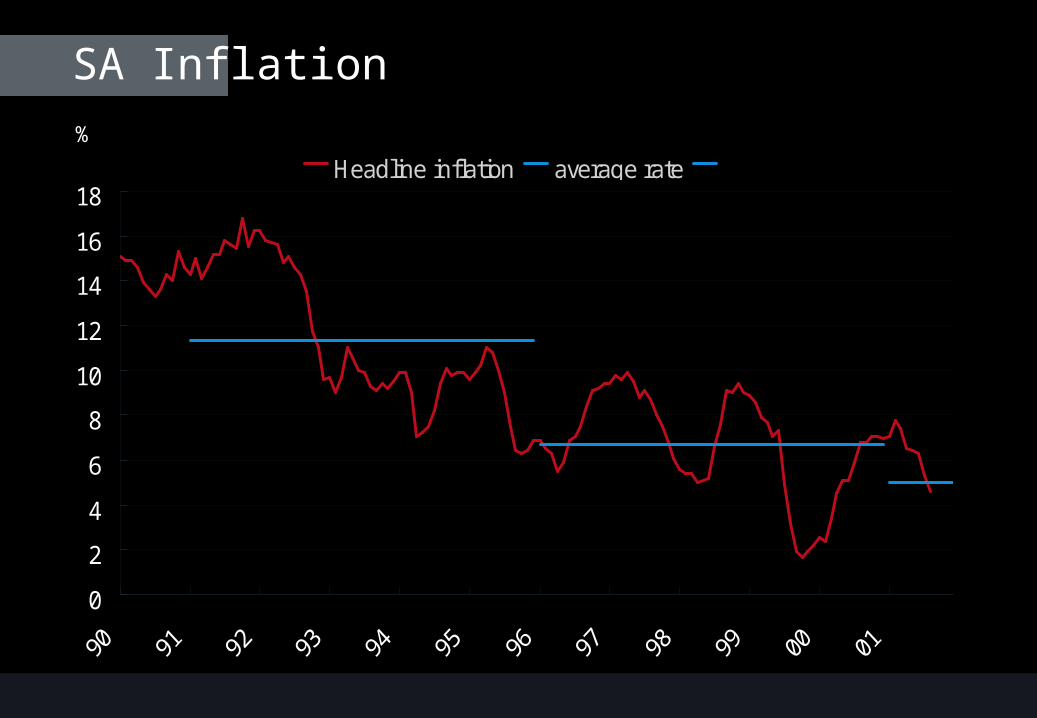

SA Inflation

0

2

4

6

8

10

12

14

16

18Headline inflation average rate

%