joc container trade europe conference 2016 – … container trade europe conference 2016 –...

TRANSCRIPT

1 Hamburg, 13 September 2016

JOC Container Trade Europe Conference 2016 – Keynote Address

2

Opening remarks

Industry challenges The industry needs to address supply chain inefficiencies Shippers underestimate the value of premium products that

can being delivered We must actively balance supply and demand

Sector update The industry is tough, but we are approaching a turning point The timing of this is somewhat uncertain, but it will be within

the next 12-24 months Hapag-Lloyd is well positioned to benefit from the upturn

Future hypothesis

It is no longer about “big ships” We must put the customer in the center of what we do We need to help our customers to improve their supply chains New services will be developed leveraging existing data

3

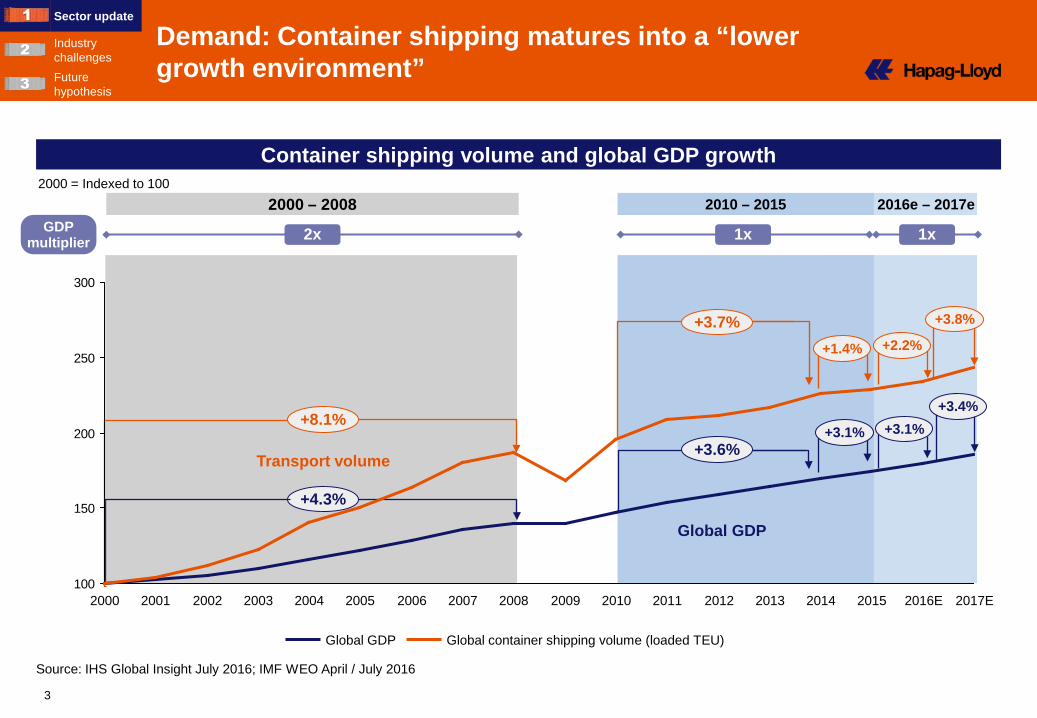

2000 = Indexed to 100

Global GDP Global container shipping volume (loaded TEU)

2016e – 2017e 2000 – 2008 2010 – 2015 GDP

multiplier 1x 1x 2x

Container shipping volume and global GDP growth

Transport volume

+8.1%

Global GDP

+4.3%

+3.6% +3.1%

+3.4%

+2.2%

+3.8%

Source: IHS Global Insight July 2016; IMF WEO April / July 2016

+3.7%

Demand: Container shipping matures into a “lower growth environment”

Sector update

Industry challenges Future hypothesis

+3.1%

+1.4%

100

150

200

250

300

2015 2016E 2013 2014 2008 2017E 2009 2010 2012 2011 2000 2001 2002 2003 2004 2005 2006 2007

4

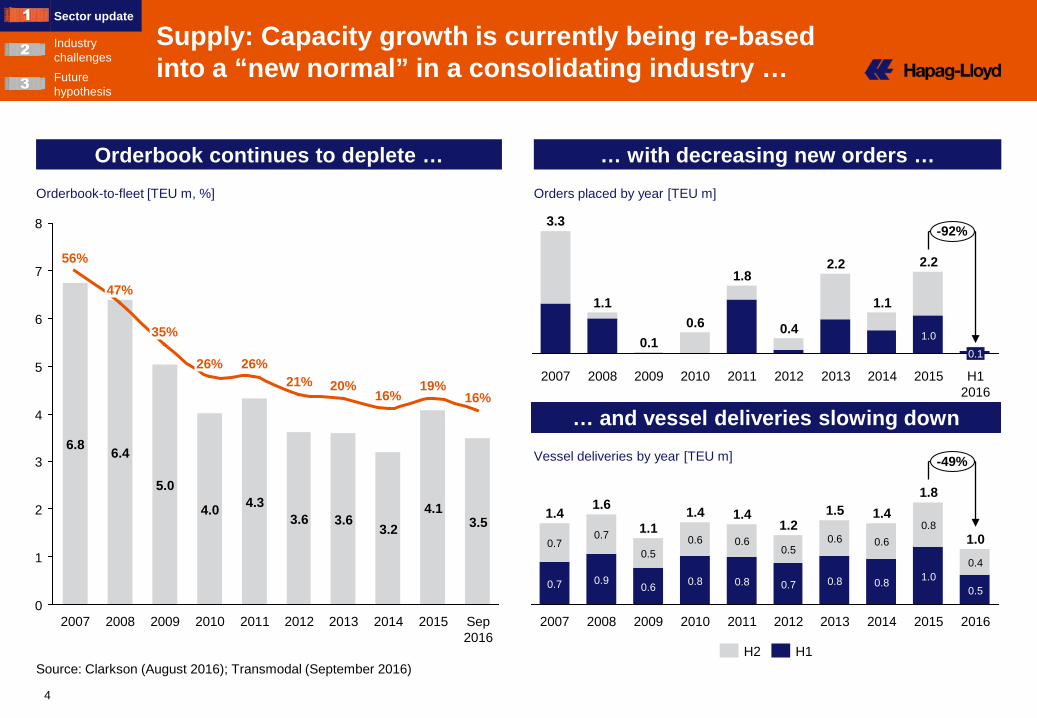

… and vessel deliveries slowing down

Source: Clarkson (August 2016); Transmodal (September 2016)

… with decreasing new orders … Orderbook continues to deplete … Orderbook-to-fleet [TEU m, %] Orders placed by year [TEU m]

Vessel deliveries by year [TEU m]

8

7

6

5

4

3

2

1

0 2012

21%

3.6

2011

26%

4.3

2010

26%

4.0

2009

35%

5.0

2008 Sep 2016

16%

3.5

2015

19%

4.1

2014

16%

3.2

2013

20%

3.6

47%

6.4

2007

56%

6.8

-92%

H1 2016

0.1

2015

2.2

1.0

2014

1.1

2013

2.2

2012

0.4

2011

1.8

2010

0.6

2009

0.1

2008

1.1

2007

3.3

0.7

0.7 0.7

0.9 0.6

1.0

0.5

0.4

1.8

1.0

0.8

2014

1.4

2013

1.5

2012

1.2

2011

1.4

2010

1.4

2009

1.1

2008

1.6

2007

0.7

0.6 0.5

0.8

0.6

0.8

2015

0.6 0.6

1.4

0.5

0.8

-49%

2016

0.8

H1 H2

Supply: Capacity growth is currently being re-based into a “new normal” in a consolidating industry …

Sector update

Industry challenges Future hypothesis

5

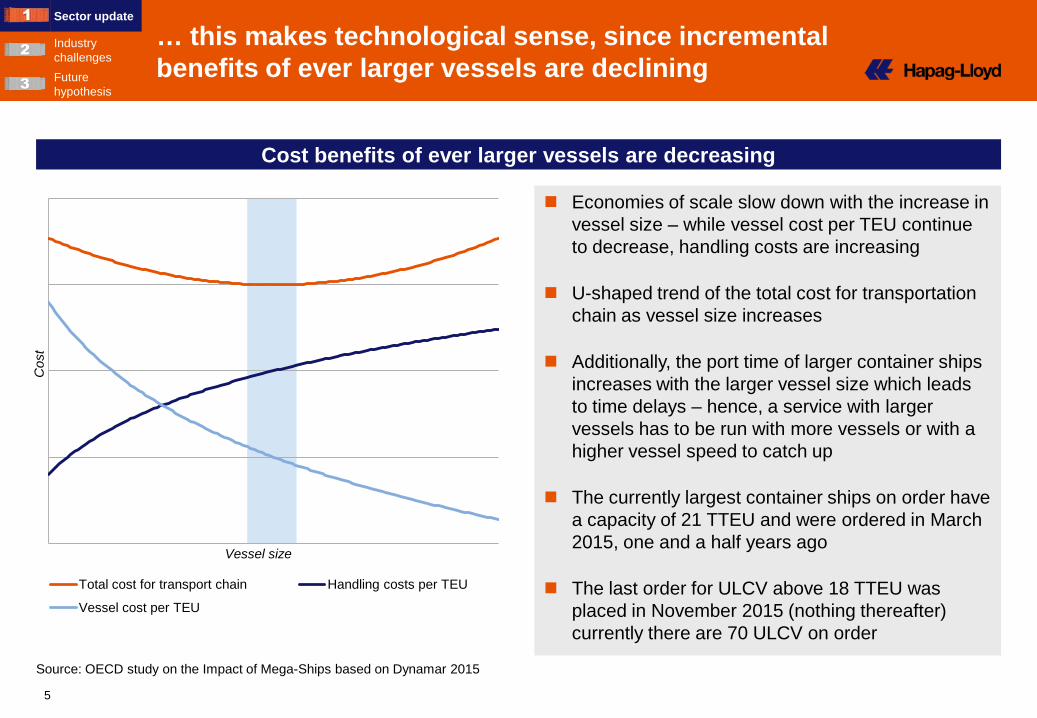

Cos

t

Vessel size

Total cost for transport chain Handling costs per TEU

Vessel cost per TEU

Cost benefits of ever larger vessels are decreasing

Economies of scale slow down with the increase in vessel size – while vessel cost per TEU continue to decrease, handling costs are increasing

U-shaped trend of the total cost for transportation chain as vessel size increases

Additionally, the port time of larger container ships increases with the larger vessel size which leads to time delays – hence, a service with larger vessels has to be run with more vessels or with a higher vessel speed to catch up

The currently largest container ships on order have a capacity of 21 TTEU and were ordered in March 2015, one and a half years ago

The last order for ULCV above 18 TTEU was placed in November 2015 (nothing thereafter) currently there are 70 ULCV on order

Source: OECD study on the Impact of Mega-Ships based on Dynamar 2015

… this makes technological sense, since incremental benefits of ever larger vessels are declining

Sector update

Industry challenges Future hypothesis

6

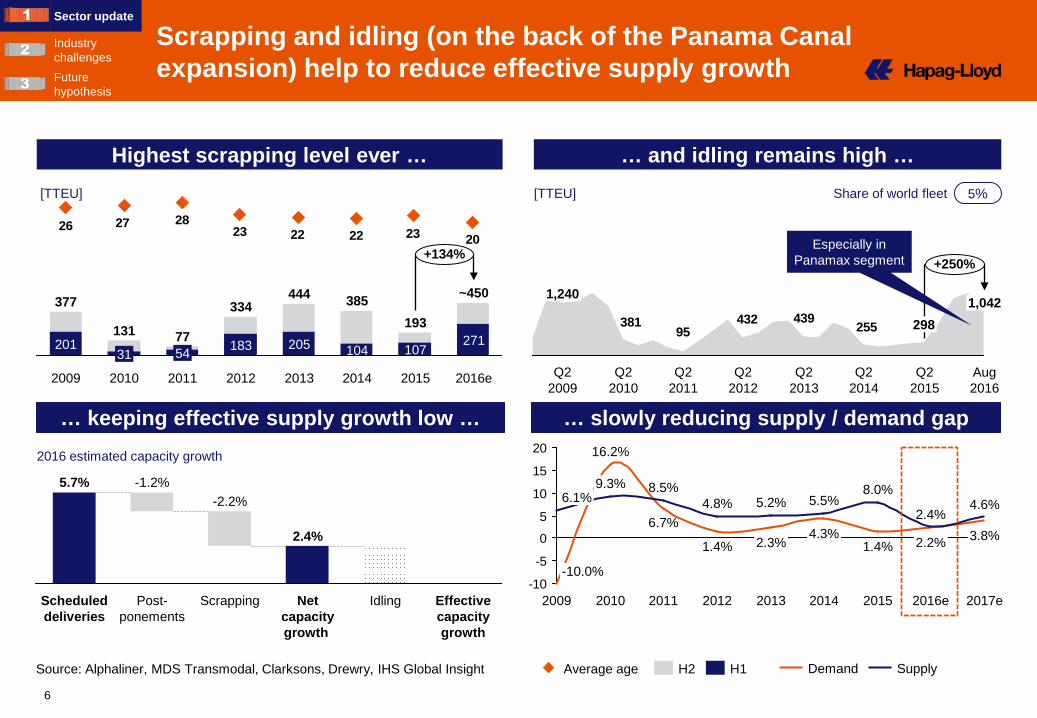

… slowly reducing supply / demand gap

Source: Alphaliner, MDS Transmodal, Clarksons, Drewry, IHS Global Insight

… and idling remains high … Highest scrapping level ever … [TTEU] [TTEU]

… keeping effective supply growth low … 2016 estimated capacity growth

2023222223282726

205 201

377

2011 2012

334

183 271

~450 444

2009

31

131

2010

54 77

2016e

+134%

2015

193

2013

104

385

2014

107

Average age H2 H1

25543943295

381

Q2 2012

Q2 2009

Q2 2011

1,240 1,042

Q2 2014

Q2 2015

298

Q2 2013

Aug 2016

Q2 2010

+250%

-10

-5

0

5

10

15

20

2009

6.7%

6.1% 4.6%

16.2%

-10.0%

2017e

2.2%

2015 2014

5.5% 5.2%

1.4% 4.3%

2013 2012

4.8% 8.5%

2.3% 1.4%

2011

9.3%

2010

8.0%

3.8%

2016e

2.4%

Demand Supply

Scheduled deliveries

5.7%

Post-ponements

-1.2%

Net capacity growth

2.4%

Scrapping

-2.2%

Idling Effective capacity growth

Especially in Panamax segment

5% Share of world fleet

Scrapping and idling (on the back of the Panama Canal expansion) help to reduce effective supply growth

Sector update

Industry challenges Future hypothesis

7

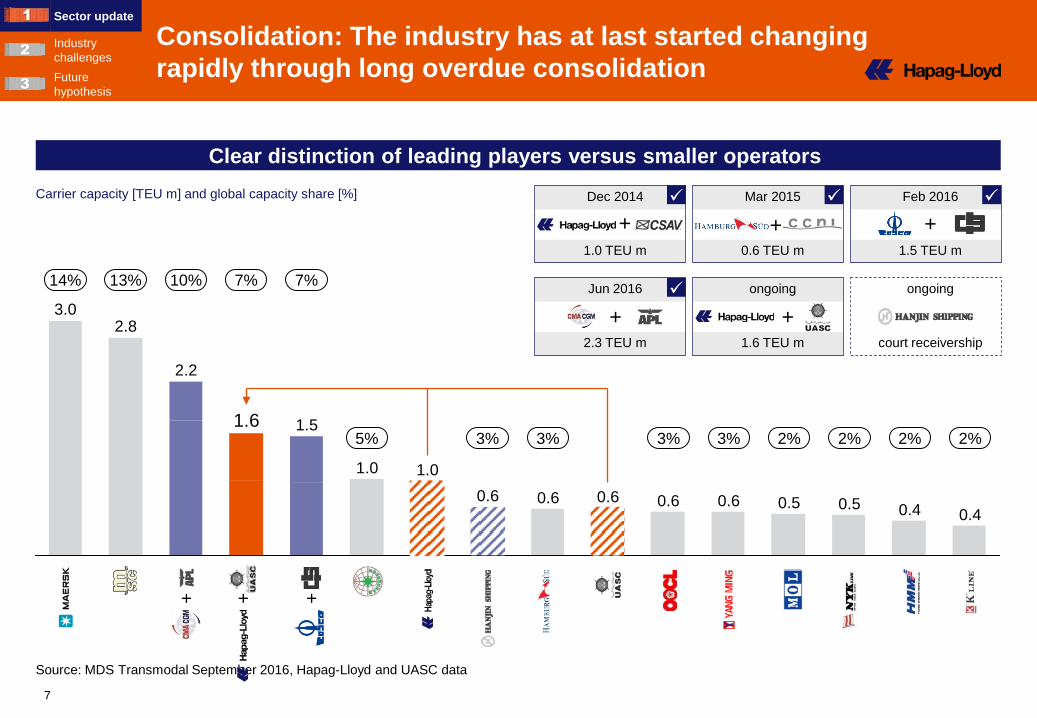

Clear distinction of leading players versus smaller operators

Consolidation: The industry has at last started changing rapidly through long overdue consolidation

Sector update

Industry challenges Future hypothesis

Source: MDS Transmodal September 2016, Hapag-Lloyd and UASC data

Carrier capacity [TEU m] and global capacity share [%]

1.0

0.6 0.6 0.5 0.5 0.6 0.6 0.6 0.4 0.4

2.2

1.6 1.5

1.0

2.8 3.0

+ + +

2.3 TEU m

Jun 2016

1.5 TEU m 0.6 TEU m

Feb 2016 Mar 2015

1.0 TEU m

Dec 2014 +

+

+

+

1.6 TEU m

ongoing +

court receivership

ongoing 14% 13% 10% 7% 7%

5% 3% 3% 3% 3% 2% 2% 2% 2%

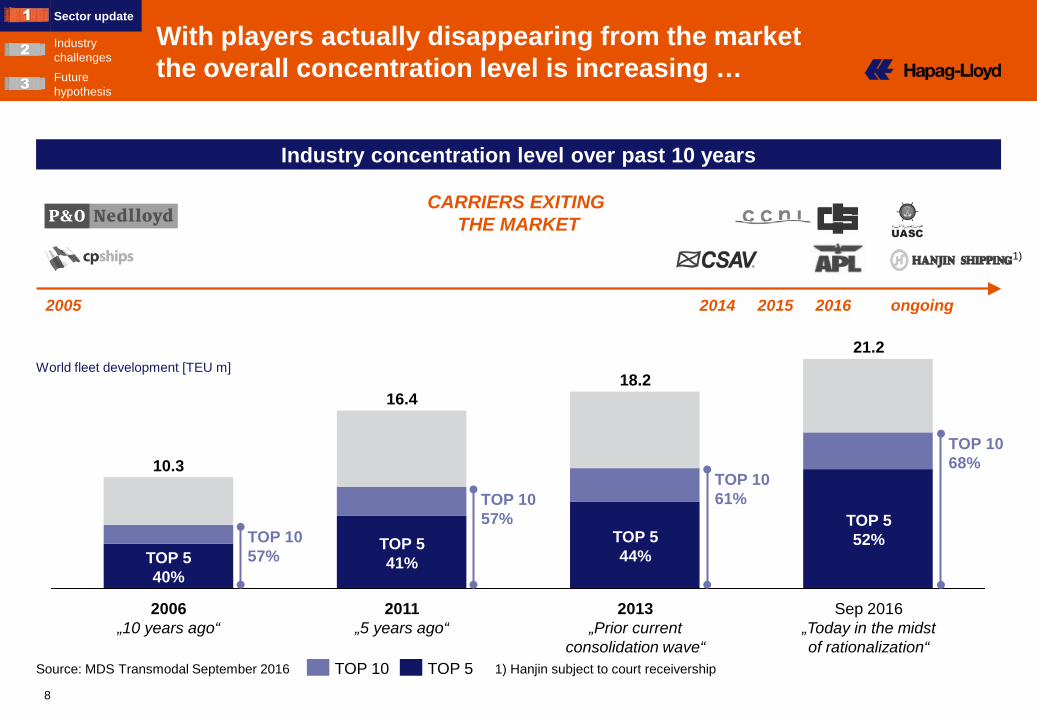

8

TOP 5 52%

21.2

Sep 2016 „Today in the midst of rationalization“

2006 „10 years ago“

TOP 5 41%

16.4

TOP 5 40%

10.3

2013 „Prior current

consolidation wave“

TOP 5 44%

2011 „5 years ago“

18.2

Industry concentration level over past 10 years

World fleet development [TEU m]

TOP 10 TOP 5

TOP 10 57%

TOP 10 57%

TOP 10 61%

TOP 10 68%

Source: MDS Transmodal September 2016

CARRIERS EXITING THE MARKET

2005 2014 2015 2016 ongoing

With players actually disappearing from the market the overall concentration level is increasing …

Sector update

Industry challenges Future hypothesis

1) Hanjin subject to court receivership

1)

9

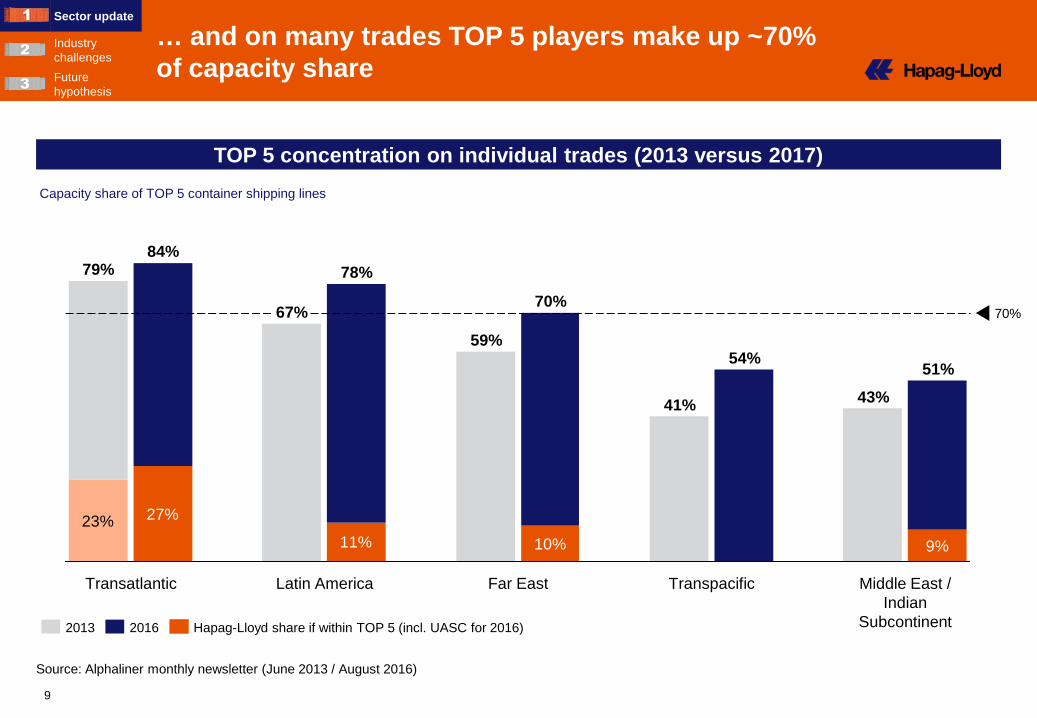

TOP 5 concentration on individual trades (2013 versus 2017) Capacity share of TOP 5 container shipping lines

9%10%11%

27%23%

54%

43% 41%

70%

51%

70%

59%

78%

67%

84% 79%

Transatlantic Transpacific Far East Latin America Middle East / Indian

Subcontinent 2016 Hapag-Lloyd share if within TOP 5 (incl. UASC for 2016) 2013

Source: Alphaliner monthly newsletter (June 2013 / August 2016)

… and on many trades TOP 5 players make up ~70% of capacity share

Sector update

Industry challenges Future hypothesis

10

New alliances set-up

Alliances have been re-shaped with start of operations in April 2017

Sector update

Industry challenges Future hypothesis

Today Tomorrow

2M

CKYHE

2M

Ocean Alliance

THE Alliance G6

Ocean 3

1) Hanjin subject to court receivership

1)

11

Apr Jan Oct Jul Apr Jan Oct Jul Apr Jan Oct Jul Apr Jan Jul Oct

+3.3%

YTD July 2016

88.8

YTD July 2015

85.9

Global volumes are developing okay …

Since Q3 average margins are negative …

… while H1 freight rates were a disaster

… and in H1 even market leaders are “red”

Q2 2016

-2.4%

-8.1%

Q1 2016

0.2%

-5.5%

Q4 2015

0.8%

-5.8%

Q3 2015

3.8%

-1.8%

Q2 2015

Q1 2015

Q4 2014

Q3 2014

Q2 2014

Q1 2014

Q4 2013

Q3 2013

Q2 2013

Q1 2013

Hapag-Lloyd EBIT margin Average carrier operating margins

Wor

ld c

onta

iner

vol

ume

(C

TS) [

TEU

m]

2014 2015 2016

CCFI composite index (SSE)

2013

Hapag-Lloyd

-1.0%

Wan-Hai

2.4%

Hyundai

-18.5% Yang-Ming

-14.9%

COSCO

-12.6%

Hanjin

-9.8%

Evergreen

-9.0%

MOL

-7.6%

K-Line

-7.1%

NYK

-3.3%

OOCL

-2.9%

CMA CGM

-1.4%

Maersk

-1.1%

1)

Q2

Carrier results are not sustainable – In H1 all global liner companies posted negative operating margins

Sector update

Industry challenges Future hypothesis

1) Average of APL (until Q1 16), CMA CGM, CSCL (until Q1 16), Evergreen, Hanjin, HMM, Hapag-Lloyd, K-Line, Maersk, MOL, NYK, Wan Hai, Yang Ming, Zim (until Q1 16)

Source: Company information, Alphaliner, CTS, Drewry, SSE Note: Company reporting. EBIT margin as stated, otherwise calculated

12

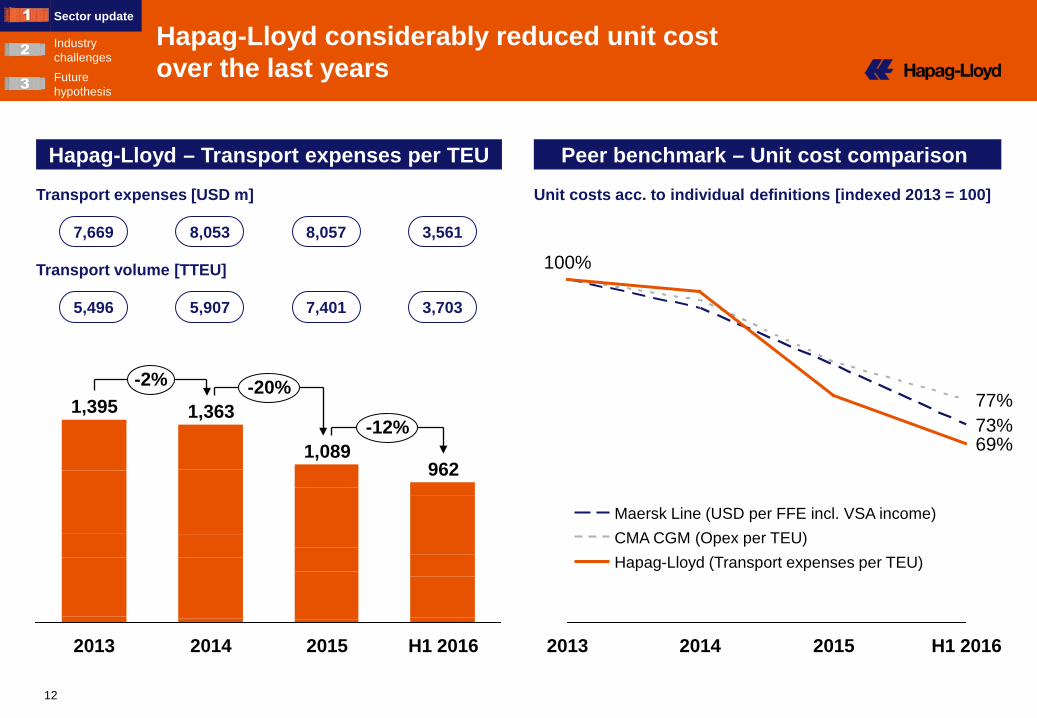

Hapag-Lloyd – Transport expenses per TEU Peer benchmark – Unit cost comparison

-12%

2015 H1 2016

962

-20% -2% 1,363

2013

1,395

1,089

2014

100%

H1 2016 2015 2014 2013

69% 73% 77%

Transport volume [TTEU]

5,496 5,907 7,401 3,703

Transport expenses [USD m]

7,669 8,053 8,057 3,561

Unit costs acc. to individual definitions [indexed 2013 = 100]

Hapag-Lloyd (Transport expenses per TEU) CMA CGM (Opex per TEU) Maersk Line (USD per FFE incl. VSA income)

Sector update

Industry challenges Future hypothesis

Hapag-Lloyd considerably reduced unit cost over the last years

13

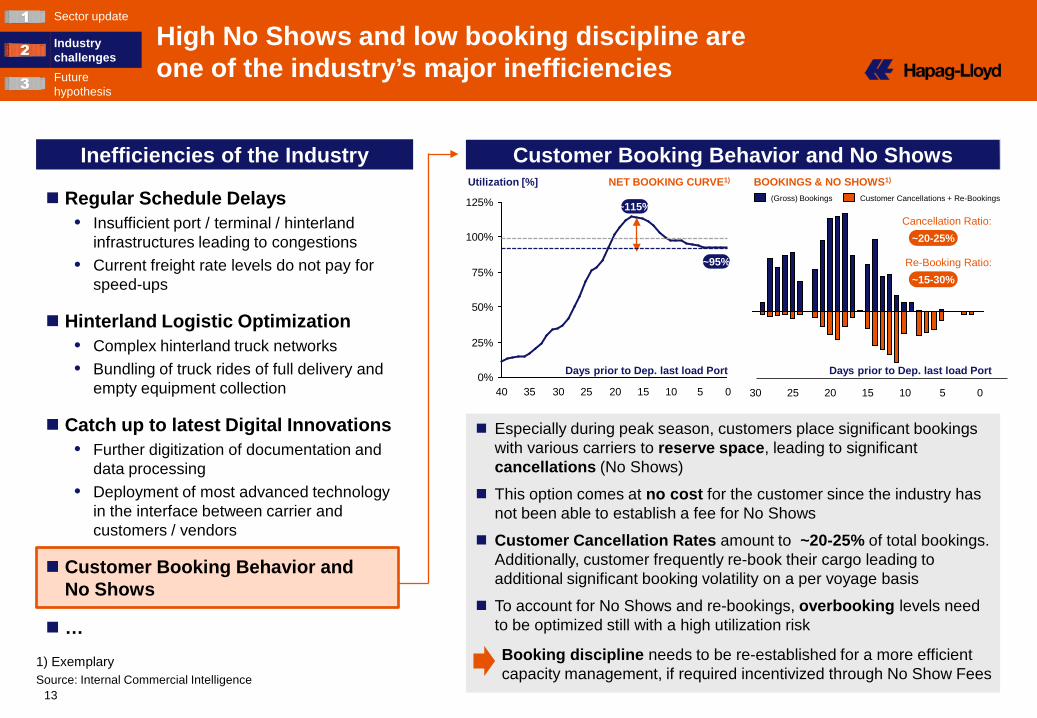

Inefficiencies of the Industry Customer Booking Behavior and No Shows

Especially during peak season, customers place significant bookings with various carriers to reserve space, leading to significant cancellations (No Shows)

This option comes at no cost for the customer since the industry has not been able to establish a fee for No Shows

Customer Cancellation Rates amount to ~20-25% of total bookings. Additionally, customer frequently re-book their cargo leading to additional significant booking volatility on a per voyage basis

To account for No Shows and re-bookings, overbooking levels need to be optimized still with a high utilization risk

Source: Internal Commercial Intelligence

Regular Schedule Delays • Insufficient port / terminal / hinterland

infrastructures leading to congestions • Current freight rate levels do not pay for

speed-ups

Hinterland Logistic Optimization • Complex hinterland truck networks • Bundling of truck rides of full delivery and

empty equipment collection

Catch up to latest Digital Innovations • Further digitization of documentation and

data processing • Deployment of most advanced technology

in the interface between carrier and customers / vendors

Customer Booking Behavior and No Shows

…

0%

25%

50%

75%

100%

125%

5 40 35 30 25 0 20 15 10

Days prior to Dep. last load Port

Utilization [%]

~95%

~115%

NET BOOKING CURVE1) BOOKINGS & NO SHOWS1)

Days prior to Dep. last load Port

1) Exemplary Booking discipline needs to be re-established for a more efficient capacity management, if required incentivized through No Show Fees

5 20 15 10 25 0 30

(Gross) Bookings Customer Cancellations + Re-Bookings

Cancellation Ratio: ~20-25%

Re-Booking Ratio: ~15-30%

High No Shows and low booking discipline are one of the industry’s major inefficiencies

Sector update

Industry challenges Future hypothesis

14

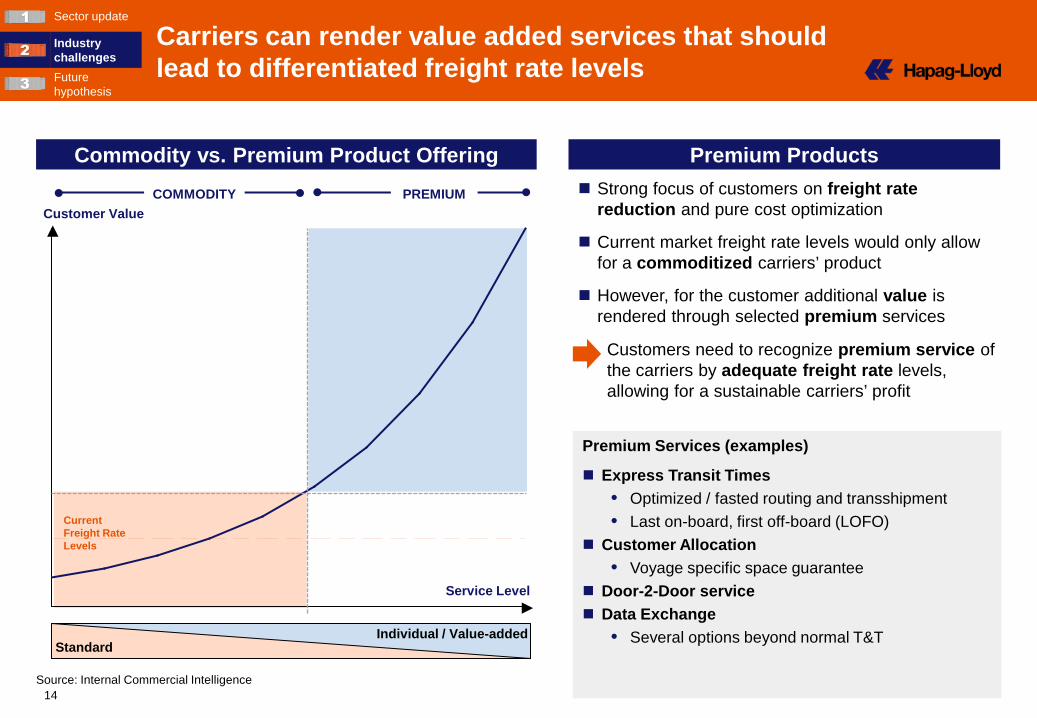

Commodity vs. Premium Product Offering Premium Products

Premium Services (examples)

Express Transit Times • Optimized / fasted routing and transshipment • Last on-board, first off-board (LOFO)

Customer Allocation • Voyage specific space guarantee

Door-2-Door service Data Exchange

• Several options beyond normal T&T

Customer Value

Service Level

Current Freight Rate Levels

Standard Individual / Value-added

COMMODITY PREMIUM Strong focus of customers on freight rate reduction and pure cost optimization

Current market freight rate levels would only allow for a commoditized carriers’ product

However, for the customer additional value is rendered through selected premium services

Source: Internal Commercial Intelligence

Customers need to recognize premium service of the carriers by adequate freight rate levels, allowing for a sustainable carriers’ profit

Carriers can render value added services that should lead to differentiated freight rate levels

Sector update

Industry challenges Future hypothesis

15

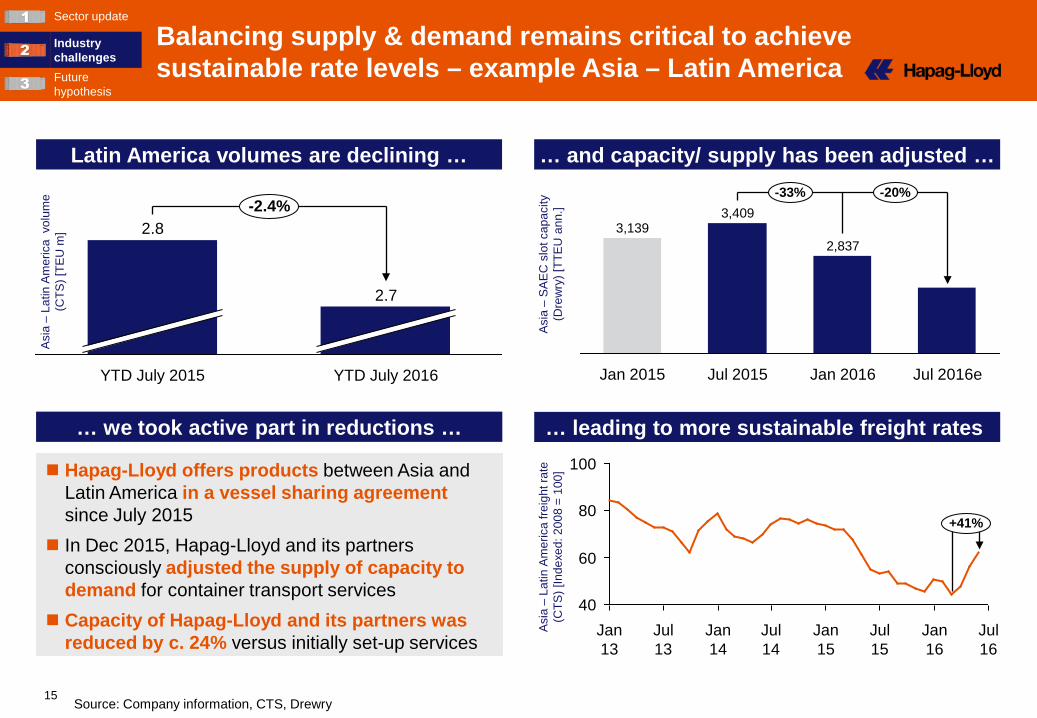

-2.4%

YTD July 2016

2.7

YTD July 2015

2.8

Latin America volumes are declining …

… we took active part in reductions …

… and capacity/ supply has been adjusted …

… leading to more sustainable freight rates

Source: Company information, CTS, Drewry

Asi

a –

Latin

Am

eric

a v

olum

e (C

TS) [

TEU

m]

-33% -20%

Jul 2016e Jan 2016

2,837

Jul 2015

3,409

Jan 2015

3,139

40

60

80

100

Jul 16

Jan 16

Jul 15

Jan 15

Jul 14

Jan 14

Jul 13

Jan 13

+41%

Hapag-Lloyd offers products between Asia and Latin America in a vessel sharing agreement since July 2015

In Dec 2015, Hapag-Lloyd and its partners consciously adjusted the supply of capacity to demand for container transport services

Capacity of Hapag-Lloyd and its partners was reduced by c. 24% versus initially set-up services

Asi

a –

SA

EC

slo

t cap

acity

(D

rew

ry) [

TTE

U a

nn.]

Asi

a –

Latin

Am

eric

a fre

ight

rate

(C

TS) [

Inde

xed:

200

8 =

100]

Balancing supply & demand remains critical to achieve sustainable rate levels – example Asia – Latin America

Sector update

Industry challenges Future hypothesis

16

1

2

3

4

It is no longer about “big ships”

We must put the customer in the center of what we do

We need to help shippers improve their supply chains

New services will be developed leveraging existing data

Benefits of ever larger container vessels are decreasing

Handling costs are exceeding slot cost advantages

Refocus on customer value and not only cut short term costs

New and additional services

We cannot save more cost by squeezing our suppliers

We need to cooperate between shippers & carriers

Available big data to be utilized further to optimize networks

IT infrastructure can be used for more effective decisions

A few hypothesis on the future

Sector Update

Industry Challenges Future hypothesis

Container shipping will continue to change

17

Disclaimer

Forward-looking Statements

This presentation contains forward-looking statements that involve a number of risks and uncertainties. Such statements are based on a number of assumptions, estimates, projections or plans that are inherently subject to significant risks, as well as uncertainties and contingencies that are subject to change. Actual results can differ materially from those anticipated in the Company´s forward-looking statements as a result of a variety of factors, many of which are beyond the control of the Company, including those set forth from time to time in the Company´s press releases and reports and those set forth from time to time in the Company´s analyst calls and discussions. We do not assume any obligation to update the forward-looking statements contained in this presentation.

This presentation does not constitute an offer to sell or a solicitation or offer to buy any securities of the Company, and no part of this presentation shall form the basis of or may be relied upon in connection with any offer or commitment whatsoever. This presentation is being presented solely for your information and is subject to change without notice.